Middle East Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Chocolate Market Analysis by Mordor Intelligence

The Middle East Chocolate Market size was valued at USD 2.84 billion in 2025 and estimated to grow from USD 3.00 billion in 2026 to reach USD 3.94 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031). This growth highlights a combination of evolving consumer preferences and structural shifts in demand that go beyond the traditional drivers such as rising disposable incomes. Ferrero Gulf, the regional arm of Ferrero International, has announced an ambitious strategy to double its presence in the Middle East within the next five years. This follows its successful expansion, having already doubled its footprint since 2020. Such moves emphasize the strategic importance of the Middle East for global chocolate manufacturers, who view the region not only as a growing market for increasing sales volumes but also as a key area for driving profitability and margin growth.

Key Report Takeaways

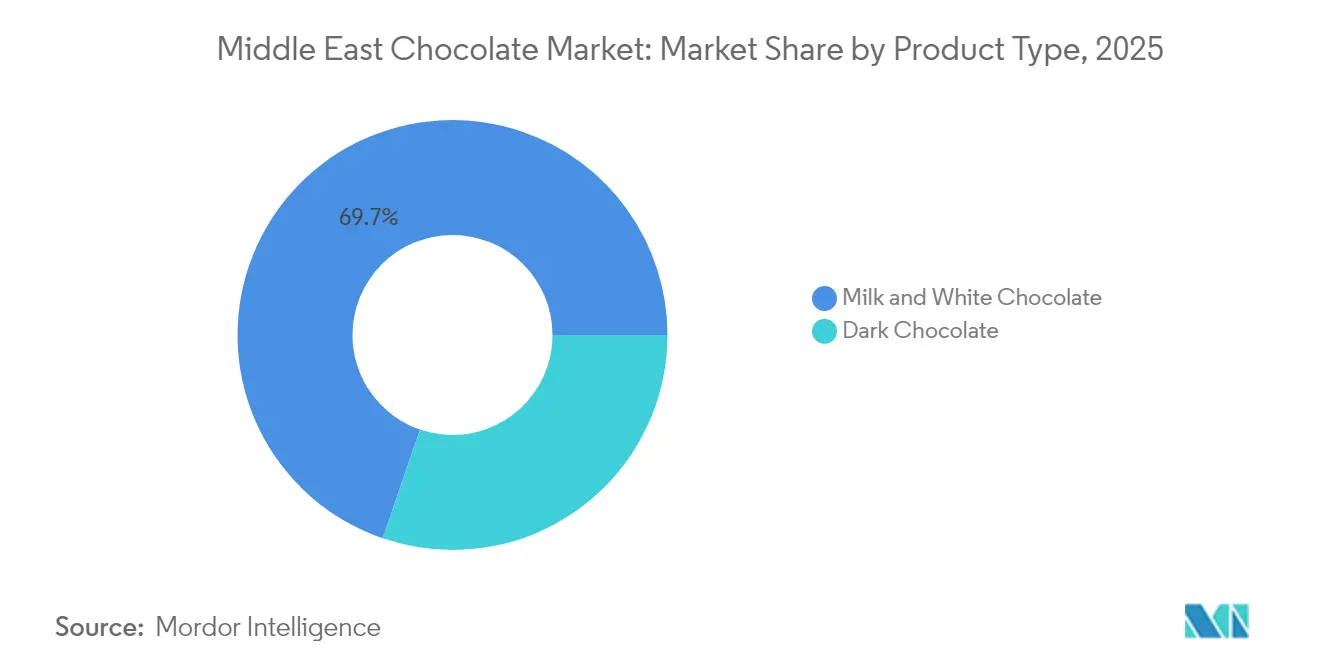

- By product type, milk and white chocolate accounted for 69.74% of the Middle East chocolate market share in 2025, while dark chocolate is projected to grow at a CAGR of 6.65% through 2031.

- By form, tablets and bars represented 39.10% of the Middle East chocolate market size in 2025. Pralines and truffles are expected to grow at the fastest rate, with a CAGR of 6.74% over 2026-2031.

- By price tier, mass products constituted 67.10% of sales in 2025. Premium offerings are anticipated to grow at a CAGR of 6.88% through 2031.

- By ingredient, dairy-based variants accounted for 52.60% of the market in 2025, while single-origin chocolate is projected to grow at a CAGR of 6.70% through 2031.

- By distribution channel, supermarkets and hypermarkets contributed 47.55% of sales in 2025. Online retail is expected to expand at a CAGR of 6.95% through 2031.

- By geography, Saudi Arabia held 43.80% of the market value in 2025. The United Arab Emirates is forecast to be the fastest-growing country, with a CAGR of 6.60% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and artisanal chocolates | +1.2% | United Arab Emirates, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Expansion of gifting culture during festivals and celebrations | +1.5% | Saudi Arabia, United Arab Emirates, Bahrain, Oman, Kuwait | Long term (≥ 4 years) |

| Increased consumer interest in novel flavors | +0.8% | United Arab Emirates, Saudi Arabia | Short term (≤ 2 years) |

| Westernization of snacking and confectionery habits | +0.9% | United Arab Emirates, Qatar, Saudi Arabia | Medium term (2-4 years) |

| Health-oriented product launches | +0.7% | GCC-wide, with concentration in United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Increase in promotional activities and chocolate-themed events | +0.5% | United Arab Emirates (Dubai), Saudi Arabia (Riyadh) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium and Artisanal Chocolates

Affluent consumers in the United Arab Emirates and Saudi Arabia are increasingly opting for single-origin and bean-to-bar chocolate products, reflecting a growing trend of premiumization within the Gulf Cooperation Council food retail market. Bateel, backed by LVMH, plans to significantly increase its revenues and expand its store network from around 200 locations to over 500 by 2029. The company's product pricing ranges from AED 22 for a Dubai Chocolate Bar to AED 1,185 for premium gift sets (equivalent to USD 19 to USD 386). Mirzam Chocolate Makers, an artisan producer based in Dubai, received five Academy of Chocolate Awards in 2025 for its single-origin dark chocolate and vegan collections. The company has also formed corporate gifting partnerships with organizations such as Etihad Airways, Burj Al Arab, and the Museum of the Future. Furthermore, the viral "Dubai chocolate" trend, featuring pistachio-knafeh bars priced at EUR 8 to EUR 10 per 100 grams, demonstrates how novelty products can command prices three to four times higher than standard chocolate bars. However, this trend has also led to the emergence of counterfeit products, 96% of which failed German food-safety inspections.

Expansion of Gifting Culture During Festivals and Celebrations

Ramadan and Eid gifting traditions drive significant demand surges, surpassing Western holiday patterns. Nearly half of Middle Eastern consumers purchase chocolate as gifts during Eid festivals. Ferrero Rocher leads boxed chocolate sales during Ramadan, while Nutella achieves the highest household penetration globally in Saudi Arabia, reflecting its alignment with family-oriented consumption occasions. Patchi, operating several branches in Saudi Arabia, has developed its business model around premium gift packaging and seasonal collections designed for Islamic holidays. According to the National Confectioners Association's State of Treating report, a large majority of consumers globally value confectionery sharing and gifting traditions, with this figure likely higher in the Middle East due to cultural practices. This predictable demand enables manufacturers to pre-position inventory and streamline production schedules, alleviating working-capital pressures. Bateel's partnership with InterContinental Al-Ahsa and the opening of its Seoul boutique highlight how gifting-focused brands are expanding geographically to target diaspora and tourist markets.

Increased Consumer Interest in Novel Flavors

The Dubai chocolate trend, brought into the spotlight by pistachio-knafeh bars that gained traction on social media, has inspired similar products worldwide. For example, Lindt introduced limited-edition variants at a premium price, with restricted availability per store. Additionally, United States brands such as Béquet, Pinkbox, and Amoretti launched pistachio-cream products. This rising interest in regional ingredients—such as dates, pistachios, saffron, and rose water—is shaping product development strategies. A study by Agriculture Canada on product launches in the Gulf Cooperation Council region identified a growing focus on chocolate-flavored plant-based or high-protein products, reflecting a combination of flavor innovation and health-conscious positioning. Brands like Mirzam offer Ramadan and Eid collections featuring local spices and single-origin cocoa sourced from India and Tanzania. Similarly, Al Nassma's camel-milk chocolate provides a distinctive flavor profile, appealing to tourists seeking authentic Middle Eastern experiences.

Westernization of Snacking and Confectionery Habits

Urbanization and the growing presence of expatriate communities in the United Arab Emirates and Qatar are driving changes in snacking habits, promoting consumption outside traditional meal times. This shift has increased demand for portion-controlled formats, such as countlines and molded blocks, which align with the convenience and lifestyle needs of modern consumers. Ferrero's Kinder Bueno has gained popularity among Arab millennials, highlighting its appeal to this demographic, while Kinder Joy remains a leader in the children's chocolate segment, showcasing the brand's ability to cater to diverse age groups. Additionally, the expansion of convenience stores and the growth of quick-commerce platforms are reshaping chocolate purchasing patterns, offering consumers instant access to products without relying on traditional supermarket visits. The quick-commerce market in the Middle East and North Africa is expected to grow significantly, capturing a notable share of the region's expanding e-commerce sector. However, the influence of Westernization has also brought increased health scrutiny. According to WHO EMRO data, 11 out of 22 Eastern Mediterranean countries impose excise taxes on sugar-sweetened beverages, with Saudi Arabia applying a 42.03% total tax share and the United Arab Emirates and Oman at 36.51%. This trend suggests that sugar-heavy confectionery products may face similar fiscal challenges in the future [1]ource: World Health Organization, “Situation analysis of sugar sweetened beverages taxation in Eastern Mediterranean Region,” who.int.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and complexity of maintaining product quality | -0.9% | GCC-wide, particularly United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Limited availability of premium raw materials | -1.1% | Regional (all Middle East markets dependent on imports) | Long term (≥ 4 years) |

| Challenges in localization of international flavors to regional tastes | -0.4% | Saudi Arabia, Kuwait, Oman | Medium term (2-4 years) |

| Counterfeit and low-quality chocolates affecting brand trust | -0.6% | United Arab Emirates, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost and Complexity of Maintaining Product Quality

Cocoa futures experienced a significant surge during the 2023/24 crop year, with Intercontinental Exchange (ICE) New York spot prices exceeding $8,400 per metric tonne in early May 2024—nearly three times higher than the previous year. This sharp increase was attributed to several challenges, including the widespread impact of the Swollen Shoot Virus affecting cocoa crops in West Africa, delays in farmgate payments to farmers, and the enforcement of European Union deforestation regulations aimed at promoting sustainable sourcing. Additionally, the prices of cocoa butter and cocoa liquor rose at a faster pace compared to cocoa beans, with processing ratios determined by major processors nearly doubling. Barry Callebaut, a leading cocoa and chocolate manufacturer, sources the majority of its cocoa from West Africa and reported significant growth in its Asia, Middle East, and Africa (AMEA) volume. The company's investment in expanding its factory in Egypt in 2024, along with the opening of its Casablanca facility in Morocco in October 2023, underscores its strategic focus on regionalizing processing operations and mitigating supply chain risks. Similarly, Nestlé's factory in Jeddah, Saudi Arabia, scheduled to begin production in 2025, reflects a proactive approach to reducing dependency on imports and addressing potential supply disruptions. However, smaller players in the industry face significant challenges, as they often lack the financial resources to secure forward contracts for cocoa or invest in local processing capacity. According to estimates by Jefferies, cocoa accounts for a notable portion of the cost of goods sold for Mondelēz International and The Hershey Company, indicating that mid-tier brands may experience margin pressures unless they adopt measures such as reformulating products with compound chocolate (replacing cocoa butter with vegetable fat) or implementing shrinkflation strategies.

Limited Availability of Premium Raw Materials

Pistachio supply constraints, influenced by Turkey's significant role in global production and regional droughts, have led to rising prices. This has posed challenges for the production of Dubai chocolate, which relies heavily on chopped pistachios and pistachio paste. A report by GROLAB in May 2025 highlighted that the strong demand for Dubai chocolate, combined with simultaneous shortages of essential raw materials like cocoa and pistachios, has created a quality-control crisis. Testing conducted by authorities in North Rhine-Westphalia found widespread defects in imported Dubai chocolate samples, with issues such as contamination by mycotoxins, the presence of Salmonella, undeclared allergens, and the substitution of palm oil for cocoa butter. Additionally, data from the European Commission emphasizes that the European Union is a key exporter of chocolate and sugar confectionery to Gulf Cooperation Council countries, reflecting the dependence of Middle Eastern manufacturers on imported cocoa derivatives and specialty ingredients [2]Source: European Commission, “Middle East – Gulf countries,” commission.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains Health Halo

Milk and white chocolate collectively held a significant 69.74% of the market share in 2025. This dominance is primarily driven by their popularity in family consumption and gifting traditions, where the preference for sweetness and familiarity plays a crucial role. These product types are widely favored for their universal appeal and are often chosen for celebratory occasions, making them a staple in many households. Their established presence in the market reflects a strong connection with consumer preferences for indulgent and comforting flavors.

On the other hand, dark chocolate is experiencing notable growth, with a compound annual growth rate (CAGR) of 6.65% projected for the period 2026-2031, making it the fastest-growing product type. This growth is fueled by increasing demand from affluent consumers in countries such as the United Arab Emirates, Saudi Arabia, and Qatar. These consumers are drawn to dark chocolate for its perceived health benefits, including higher cocoa content, which is associated with antioxidants, essential minerals, and a lower sugar profile. Meanwhile, white chocolate continues to cater to a niche audience, appealing to younger demographics and those seeking novelty. However, its lack of cocoa solids limits its ability to capitalize on health-related claims, which restricts its broader market potential.

By Form: Pralines and Truffles Capture Gifting Premiums

Tablets and bars accounted for 39.10% of form-based sales in 2025, primarily due to their convenience, ease of portion control, and suitability for impulse purchases in retail environments such as supermarkets and convenience stores. These forms are particularly favored by consumers seeking quick and accessible options. On the other hand, pralines and truffles are experiencing significant growth, with a compound annual growth rate (CAGR) of 6.74% projected for the period 2026-2031. This rapid expansion is largely driven by their popularity as premium gifting options during festive occasions like Ramadan and Eid. During these celebrations, the emphasis on premium packaging and artisanal presentation enables brands to command higher price points, appealing to both corporate and personal gifting markets.

Bateel, a prominent luxury brand, offers gift sets priced between AED 75 and AED 1,185 (USD 20 to USD 323), positioning pralines and date chocolates as high-end offerings. These products cater to discerning customers who value quality and exclusivity. Similarly, Patchi, which operates approximately 62 branches in Saudi Arabia, has built its reputation around premium pralines and seasonal collections. The brand's dedication to quality and innovation earned it recognition as one of Forbes' top luxury brands in the Middle East in 2005. Meanwhile, molded blocks and other forms serve niche purposes, such as baking, industrial applications, or novelty shapes. However, these forms typically lack the profit margins associated with pralines, making them less lucrative for manufacturers focusing on premium offerings.

By Price Form: Premium Segment Outpaces Mass Market

In 2025, mass-market chocolate accounted for 67.10% of the market share, underscoring the price sensitivity of middle-income consumers and the widespread availability of global chocolate brands in supermarkets and hypermarkets. This segment's dominance reflects the affordability and accessibility that appeal to a broad consumer base. On the other hand, premium chocolate is anticipated to grow at a compound annual growth rate (CAGR) of 6.88% between 2026 and 2031, representing the fastest growth among price tiers. This trend is fueled by increasing urbanization and higher disposable incomes in key markets such as Saudi Arabia and the United Arab Emirates, which are encouraging consumers to upgrade to higher-quality and more luxurious chocolate options.

The growing popularity of unique chocolate offerings in Dubai, such as pistachio-knafeh bars, demonstrates consumers' willingness to pay three to four times the price of standard chocolate for products that provide novelty and appeal, particularly on social media. Premium chocolate brands are capitalizing on the Middle East's strong gifting culture, where factors like sophisticated presentation and brand prestige are as important as taste. For instance, Ferrero has positioned Ferrero Rocher as a favored boxed chocolate during Ramadan, aligning with cultural preferences. Similarly, Patchi emphasizes luxury packaging and seasonal collections to meet the demand for premium gifting options in the region.

By Ingredient Type: Single-Origin Chocolate Emerges as Niche Growth Driver

Dairy-based chocolate accounted for 52.60% of the market share in 2025, primarily due to the popularity of milk chocolate in family consumption and gifting occasions. This category continues to dominate as it appeals to a broad consumer base with its familiar taste and versatility. On the other hand, single-origin chocolate, which is made using cocoa beans sourced from a single region, is projected to grow at a compound annual growth rate (CAGR) of 6.70% from 2026 to 2031. This represents the fastest growth among ingredient types, driven by affluent consumers who value the unique characteristics of origin-specific cocoa, including provenance, traceability, and distinctive flavor profiles. For example, Mirzam Chocolate Makers has introduced single-origin collections sourced from regions like India and Tanzania, earning five Academy of Chocolate Awards in 2025 for their commitment to quality and innovation.

Producing single-origin chocolate requires establishing direct relationships with cocoa cooperatives and managing extended lead times, which creates significant entry barriers. These challenges favor established players such as Barry Callebaut and Lindt over smaller regional startups. Barry Callebaut, a leading global chocolate manufacturer, sources 75% of its cocoa from West Africa and operates production facilities in Egypt and Morocco, leveraging its scale and infrastructure. However, the Middle East faces a scarcity of locally grown cocoa, preventing brands in the region from vertically integrating their supply chains. This leaves them exposed to fluctuations in global commodity prices. For instance, cocoa futures surged by 131% during 2023/24 due to the outbreak of the Swollen Shoot Virus in West Africa, delays in farmgate payments to farmers, and the enforcement of European Union (EU) deforestation regulations. These factors have significantly compressed profit margins for single-origin chocolate producers, highlighting the challenges of operating in this niche market.

By Distribution Channel: Online Retail Surges on Quick-Commerce Backbone

Supermarkets and hypermarkets accounted for 47.55% of distribution in 2025, benefiting from high customer foot traffic, strategically positioned impulse-purchase displays, and promotional campaigns tied to seasonal events. In contrast, online retail is projected to grow at a compound annual growth rate (CAGR) of 6.95% from 2026 to 2031, emerging as the fastest-growing distribution channel. This growth is fueled by quick-commerce platforms offering delivery within 15 to 30 minutes. For instance, DNOC Distribution partnered with noon in April 2025 to launch noon Minutes hubs, while YallaMarket secured USD 2.3 million in pre-seed funding to facilitate 15-minute deliveries in Dubai through the use of dark stores. However, the temperature sensitivity of chocolate necessitates cold-chain logistics, which increases costs that quick-commerce platforms must either absorb or transfer to consumers. Additionally, rising interest rates have further escalated cold-storage expenses, prompting operators to enhance delivery density and optimize route efficiency. Supported by nearly 100% internet and mobile phone penetration among the United Arab Emirates population, the Dubai Chamber of Commerce and Industry projects eCommerce to generate USD 8 billion in sales by 2025 .

Brands that offer subscription boxes, corporate gifting portals, or limited-edition products can secure higher profit margins compared to those relying solely on third-party marketplaces. Mirzam's corporate gifting partnerships with organizations such as Etihad Airways, Burj Al Arab, and the Museum of the Future highlight how business-to-business (B2B) channels can effectively complement business-to-consumer (B2C) e-commerce strategies.

Geography Analysis

Saudi Arabia emerged as the leading geographic segment in 2025, holding a significant 43.80% share of the market. This leadership is driven by factors such as high per-capita chocolate consumption, a population exceeding 36 million, and the Vision 2030 initiatives, which aim to boost local food manufacturing. A notable example of this trend is Nestlé's investment of USD 72 million in a factory located in Jeddah, which is expected to produce 15,000 tonnes annually starting in 2025. This move underscores how multinational corporations are localizing production to reduce dependency on imports and minimize exposure to tariff fluctuations. Additionally, AlBabtain Food announced plans for a chocolate factory investment in August 2024, further emphasizing the growth of local production. Patchi, a prominent chocolate brand, operates approximately 62 branches across Saudi Arabia, marking the highest concentration of outlets in any single market. Furthermore, Ferrero's Nutella has achieved the highest household penetration globally in Saudi Arabia, reflecting its strong alignment with family-oriented consumption habits.

The United Arab Emirates stands out as the fastest-growing geographic segment, with a projected compound annual growth rate of 6.60% between 2026 and 2031. This growth is fueled by a combination of factors, including increasing tourism inflows, a large expatriate population, and the popularity of the "Dubai chocolate" phenomenon, which has gained global recognition and inspired imitation worldwide. However, this trend has also brought to light certain quality concerns. German food inspectors reported that 96% of imported chocolate samples were defective, with issues such as undeclared allergens, the presence of mycotoxins, Salmonella contamination, and the substitution of palm oil for cocoa butter, raising questions about product safety and quality standards.

Other markets in the region, including Kuwait, Oman, Qatar, Bahrain, and the Rest of the Middle East, collectively represent smaller but strategically important segments. Qatar, known for its high-income levels and frequent hosting of international events, has seen a growing demand for premium chocolate products. Meanwhile, Oman imposes a total tax share of 36.51% on chocolate products, which influences pricing and consumption patterns. These markets, while smaller in size, play a critical role in the overall dynamics of the Middle Eastern chocolate market.

Competitive Landscape

The Middle East chocolate market shows moderate consolidation, with global players such as Mars, Mondelēz, Nestlé, and Ferrero holding significant market shares while leaving room for regional specialists and artisanal producers. Ferrero's plan to expand its presence in the Gulf Cooperation Council (GCC) countries within five years, following its recent growth, highlights the aggressive expansion strategies of multinational companies targeting the region as a high-margin market. Investments like Nestlé's factory in Jeddah and Barry Callebaut's expansion in Egypt reflect a shift toward localized manufacturing to address risks from cocoa price volatility and import tariffs.

Joint ventures remain a key strategy for market entry and expansion. For example, Ferrero has partnered with Al Seer Group in the United Arab Emirates (UAE), Al Bustan Al Khaleeji in Kuwait, and Ismail Abudawood in Saudi Arabia to establish direct distribution channels, bypassing third-party importers and capturing higher margins. Opportunities for growth are concentrated in health-oriented products, such as plant-based chocolate, which is gaining traction in the Middle East and North Africa (MENA) region and is expected to grow significantly in the coming years. Additionally, single-origin chocolate appeals to affluent consumers seeking products with provenance and traceability.

Smaller players are also finding success by focusing on quality and brand differentiation. For instance, Mirzam Chocolate Makers, a Dubai-based artisan producer, has received multiple Academy of Chocolate Awards and established corporate gifting partnerships with companies like Etihad Airways, Burj Al Arab, and the Museum of the Future. This demonstrates how niche players can create defensible positions through premium offerings and storytelling.

Middle East Chocolate Industry Leaders

Mars, Incorporated

Mondelēz International Inc.

Nestlé S.A.

Ferrero International S.A.

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fix Dessert Chocolatery introduced a new chocolate flavor in Dubai, expanding its product range to cater to evolving consumer tastes. This launch strengthens Fix’s brand presence and reflects innovation in the dynamic Middle East chocolate market.

- October 2024: Barry Callebaut invested USD 30 million to establish a chocolate factory in Egypt, targeting local demand and positioning Egypt as a regional export hub for chocolate products across Middle Eastern and African markets, thereby supporting industry growth.

- August 2024: Abdulaziz and Mansour Ibrahim AlBabtain Co. approved investment in a Saudi chocolate production factory, supporting strategic expansion and responding to increasing regional demand in the Middle East chocolate market, while enabling future growth in foreign markets.

Middle East Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates are covered as segments by Country.| Dark Chocolate |

| Milk and White Chocolate |

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

| Mass |

| Premium |

| Dairy-based |

| Plant-based |

| Single Origin |

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| Bahrain |

| Kuwait |

| Oman |

| Qatar |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Form | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single Origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels | |

| By Geography | Bahrain |

| Kuwait | |

| Oman | |

| Qatar | |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms