Ultrasound Probe Disinfection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

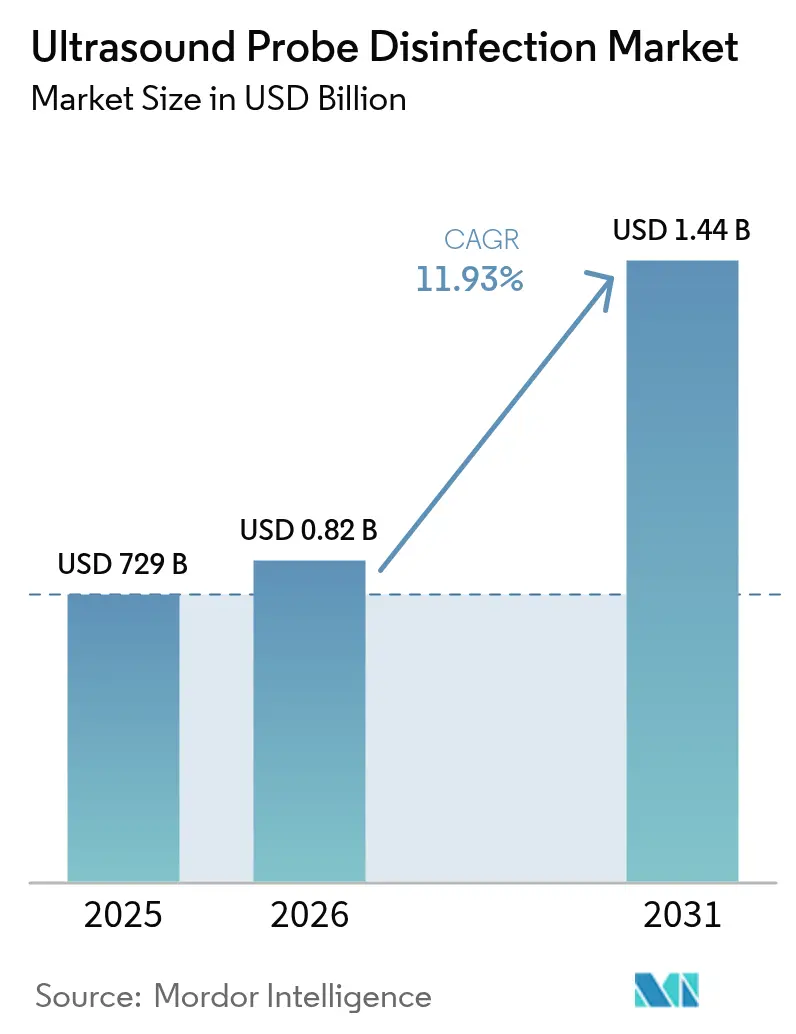

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 11.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasound Probe Disinfection Market Analysis by Mordor Intelligence

Ultrasound probe disinfection market size in 2026 is estimated at USD 820 million, growing from 2025 value of USD 729 million with 2031 projections showing USD 1.44 billion, growing at 11.93% CAGR over 2026-2031. Accelerated adoption stems from the relentless rise in ultrasound procedures, stringent global mandates for high-level probe reprocessing, and quick, automated systems that document each cycle for auditors. Hospitals are prioritizing chemical-free cabinets that complete cycles in under two minutes, while ambulatory centers choose compact devices that pair with handheld scanners for point-of-care use. Vendors are embedding RFID logs to simplify audits, and competitive pressure is intensifying as core patents expire and mid-tier suppliers launch lower-priced units. Health systems view these upgrades as risk-mitigation investments that can curb costly HAI-related penalties.

Key Report Takeaways

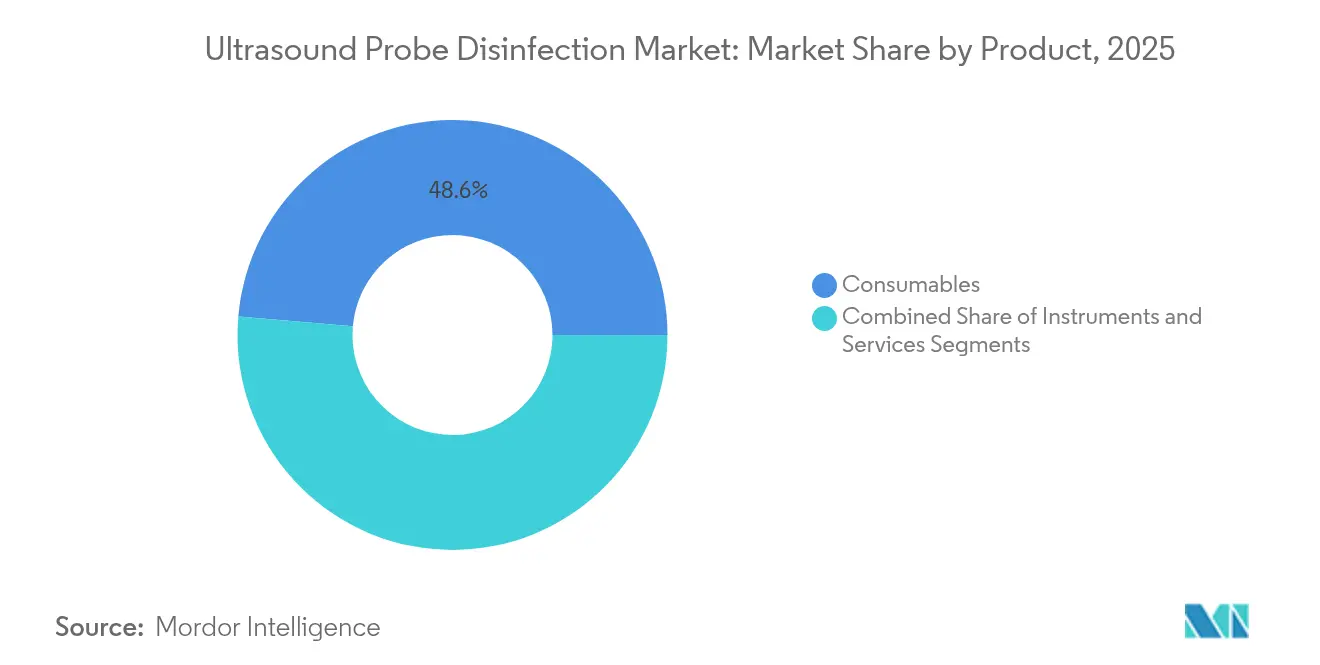

- By product category, consumables led with 48.62% revenue share in 2025, while services are projected to expand at a 13.76% CAGR through 2031.

- By process, high-level disinfection captured 60.05% of the ultrasound probe disinfection market share in 2025, and it remains the fastest-growing process at a 12.98% CAGR.

- By technology, hydrogen-peroxide mist accounted for 43.70% share of the ultrasound probe disinfection market size in 2025; UV-C systems are advancing at a 14.55% CAGR.

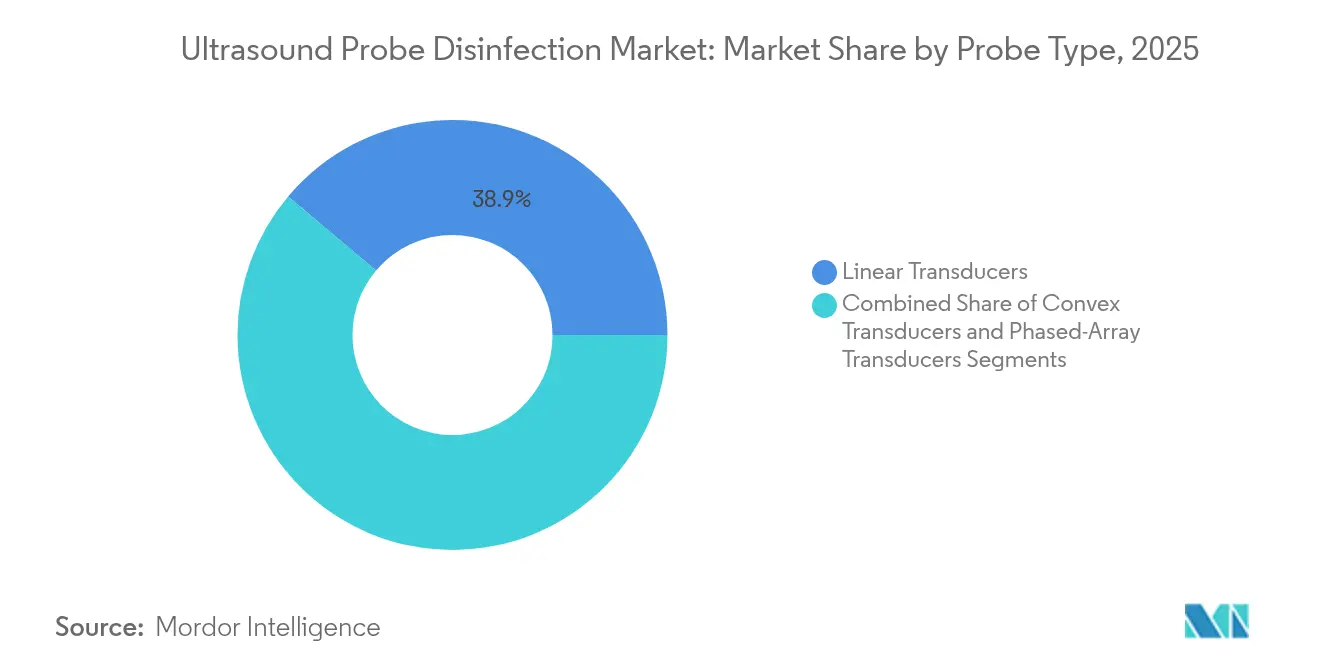

- By probe type, linear transducers held 38.85% share of the ultrasound probe disinfection market size in 2025, whereas phased-array probes record the quickest 12.74% CAGR.

- By end user, hospitals and diagnostic laboratories captured 66.60% of the ultrasound probe disinfection market share in 2025, while ambulatory care centers are poised to grow at a 13.25% CAGR to 2031.

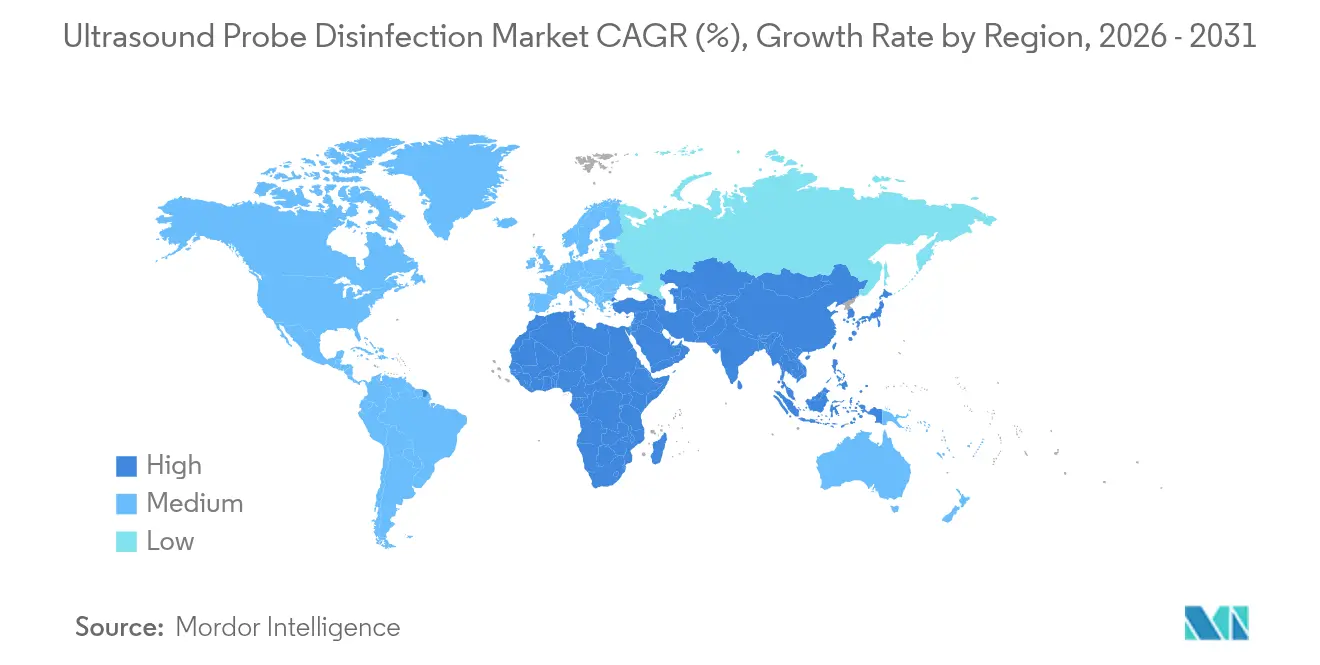

- By geography, North America contributed 36.45% share of the ultrasound probe disinfection market size in 2025, whereas Asia Pacific is forecast to expand at 14.22% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasound Probe Disinfection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ultrasound imaging procedure volumes | +2.8% | Global; strongest in North America and APAC | Medium term (2-4 years) |

| Escalating incidence & penalties for HAIs | +2.1% | North America, EU; extending to APAC | Short term (≤ 2 years) |

| Regulatory mandates for high-level disinfection | +1.9% | Global, led by FDA, Health Canada, CE regions | Long term (≥ 4 years) |

| Rapid adoption of automated HLD systems & UV-C cabinets | +2.3% | North America, EU; emerging MEA | Medium term (2-4 years) |

| Expiry of core HLD device patents | +1.5% | Developed markets first | Short term (≤ 2 years) |

| Integration of RFID/IoT traceability | +1.7% | North America, EU; gradual APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Ultrasound Imaging Procedure Volumes

Global ultrasound utilization continues to soar as physicians broaden applications across emergency, critical-care, and musculoskeletal disciplines. Point-of-care adoption allows clinicians to scan at the bedside, compressing diagnostic timelines and lifting procedural counts. In low- and middle-income countries, 80% of providers surveyed rated ultrasound access as essential to improving care quality.[1]Amy Sarah Ginsburg, “A Survey of Barriers and Facilitators to Ultrasound Use in Low- and Middle-Income Countries,” Scientific Reports, nature.comPortable, battery-powered scanners expand outreach clinics but introduce mobile disinfection challenges, thereby magnifying demand for quick-cycling, countertop units. Health ministries are bundling probe reprocessors into national imaging upgrades to guarantee infection control parity with advanced economies. As procedure volumes climb, every incremental scan increases the risk of cross-contamination, reinforcing the ultrasound probe disinfection market’s growth trajectory.

Escalating Incidence & Penalties For Hospital-Acquired Infections (HAIs)

Governments and private insurers impose financial penalties on facilities that exceed HAI benchmarks, and contaminated probes remain a documented vector. A multicenter study showed over 90% of transvaginal probes harbored pathogens after low-level wipes, evidencing shortfalls in legacy cleaning workflows. The CDC’s 2025 health alert on gel-borne Paraburkholderia fungorum infections renewed scrutiny of sonography suites.[2]Centers for Disease Control and Prevention, “Alert: Use Only Sterile Ultrasound Gel for Percutaneous Procedures,” cdc.gov Hospitals now calculate potential fines plus reputational damage when budgeting for automated cabinets. Cost analyses reveal damaged transesophageal probes can add USD 1,800–USD 9,000 in repair charges, often precipitated by improper manual cleaning. Consequently, facilities fast-track investments that standardize disinfection cycles and log proof of compliance.

Regulatory Mandates For High-Level Disinfection Of Semi-Critical Probes

The FDA classifies endocavitary probes as semi-critical devices that demand high-level disinfection, and recent guidance explicitly calls for validated protocols.[3]U.S. Food and Drug Administration, “Marketing Clearance of Diagnostic Ultrasound Systems and Transducers—Guidance for Industry and Food and Drug Administration Staff,” fda.gov Professional societies such as AIUM and ACEP codify similar requirements, extending them to sterile gel use during invasive scans.[4]American Institute of Ultrasound in Medicine, “Guidelines for Cleaning and Preparing External- and Internal-Use Ultrasound Transducers and Equipment Between Patients as Well as Safe Handling and Use of Ultrasound Coupling Gel,” aium.orgEuropean CE authorities mirror these stipulations, forming a harmonized compliance baseline that multinational hospital chains must observe. Accrediting bodies now audit probe logs during site visits, and non-conformance can stall reimbursement. As regulators converge, the ultrasound probe disinfection market gains a predictable, policy-driven demand floor that persists beyond cyclical capital budgets.

Rapid Adoption Of Automated HLD Systems & UV-C Cabinets

Automation removes operator variability, shortens cycle time, and feeds electronic health records with time-stamped logs. Comparative trials found UV-C devices could finish a cycle in 7.9 minutes versus 49 minutes for chemical baths, while halving residual contamination sites. Germitec’s Chronos won FDA de novo clearance in 2024 as the first chemical-free UV-C cabinet for probes, completing cycles in 90 seconds and eliminating bacteria, fungi, and spores. Healthcare executives struggling with staffing shortages value these unattended systems that keep ultrasound rooms turning over safely during peak hours. RFID tagging of each probe feeds centralized dashboards that flag missed cycles, cutting administrative burden and enhancing audit readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of automated reprocessors | -1.8% | Global; acute in emerging markets | Medium term (2-4 years) |

| Low awareness & training gaps | -1.3% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Hydrogen-peroxide supply-chain constraints | -0.9% | Emerging APAC, MEA, Latin America | Short term (≤ 2 years) |

| Threat of single-use sterile probe covers | -1.1% | Global; higher in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost Of Automated Reprocessors

Automated cabinets can exceed USD 25,000 each, a hurdle for rural hospitals and budget-constrained clinics. Nanosonics noted that tight capital budgets slowed new placements early in fiscal 2024, although second-half orders rebounded 14% as purchasing cycles normalized. Total cost of ownership extends to consumable cartridges and annual service contracts, stretching limited budgets. Facilities in markets where infection-prevention investments lack direct reimbursement must reconcile the up-front outlay with longer-term savings from fewer HAIs and lower labor costs. Until financing programs or pay-for-prevention incentives mature, adoption may lag in cash-strapped settings, tempering the ultrasound probe disinfection market’s upside.

Low Awareness & Training Gaps In Low- And Mid-Income Facilities

Clinicians in low-resource regions often receive ultrasound proficiency training but little instruction on probe reprocessing. Surveys cite education deficits and equipment competition as key barriers to safe ultrasound roll-out. Programs in Haiti and Kenya demonstrate that targeted training raises diagnostic accuracy yet rarely covers disinfection protocols. Without standardized curricula and competency checks, inconsistent cleaning persists, dampening demand for advanced cabinets. Donor-funded imaging projects increasingly bundle reprocessors, but power and maintenance constraints still challenge consistent use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Services Drive Comprehensive Solutions

Consumables controlled 48.62% of 2025 revenue as facilities restock disinfectant cartridges, probe covers, and filters daily. Services, however, are projected to pace the ultrasound probe disinfection market at a 13.76% CAGR through 2031 as hospitals outsource maintenance, calibration, and compliance audits. The shift mirrors broader healthcare moves toward outcome-based contracting, where vendors guarantee uptime and accreditation readiness rather than selling stand-alone kits.

Some health systems bundle training, software updates, and remote diagnostics into multiyear service plans that spread cost and free internal staff. Nanosonics added 2,340 units in fiscal 2024, reaching 34,790 global installations, which feed a recurring revenue stream of consumables and digital monitoring fees. Providers value rapid support that avoids exam cancellations, reinforcing service uptake across the ultrasound probe disinfection industry.

By Process: High-Level Disinfection Dominates Standards

High-level disinfection accounted for 60.05% share of the ultrasound probe disinfection market size in 2025 and will outpace other processes at a 12.98% CAGR as regulators tighten rules on semi-critical devices. Spaulding classification places endocavitary probes squarely in the high-level category, and compliance audits increasingly flag any deviation.

Intermediate and low-level wipes remain permissible for surface scans on intact skin, but many hospitals standardize on high-level cycles to simplify staff training and limit error. Automated logs that record temperature, concentration, and exposure times help clinicians demonstrate adherence to FDA and CE guidance. Over the forecast horizon, multi-tiered protocols may give way to single high-level standards that protect all patients equally, driving steady gains for the segment.

By Technology: UV-C Light Emerges As Chemical-Free Alternative

Hydrogen-peroxide mist retained 43.70% share in 2025, reflecting a decade of clinical familiarity and broad regulatory clearance. UV-C systems are projected to grow 14.55% annually, propelled by chemical-free cycles that remove staff exposure risks and ventilation requirements. Germitec’s Chronos cabinet completes a high-level cycle in 90 seconds without consumables, appealing to high-volume emergency rooms.

Ozone and chlorine-dioxide foams occupy niche roles where facility design limits liquid use, and updated ANSI/AAMI standards now recognize chlorine-dioxide as a valid high-level option. Procurement teams evaluate each platform’s through-put, cost per cycle, and environmental footprint, shaping a competitive field that will diversify the ultrasound probe disinfection market.

By Probe Type: Phased-Array Applications Expand Specialty Care

Linear probes captured 38.85% of the ultrasound probe disinfection market share in 2025 thanks to broad usage in vascular, musculoskeletal, and abdominal imaging. Phased-array probes will grow fastest at 12.74% as cardiology, critical-care, and anesthesiology expand bedside echocardiography routines.

Convex probes remain vital in obstetrics and general surgery, but rising adoption of portable cardiac ultrasound boosts demand for fast-cycle cabinets sized for phased-array heads. Each probe geometry presents unique crevices that complicate manual cleaning, reinforcing hospitals’ preference for validated automated units. Specialty growth broadens the ultrasound probe disinfection industry’s customer base beyond radiology departments.

By End User: Ambulatory Care Centers Drive Decentralized Growth

Hospitals and diagnostic labs held 66.60% of 2025 demand, benefiting from bundled imaging budgets and dedicated infection-control teams. Ambulatory care centers will expand 13.25% yearly as outpatient surgery, urgent-care, and imaging chains decentralize scanning services. Portable handheld scanners paired with compact UV-C cabinets allow centers to meet the same accreditation standards as tertiary hospitals.

Research and academic institutes pilot experimental probes and disinfection protocols, accelerating commercial adoption once efficacy is proved. Their willingness to beta-test IoT dashboards and AI-driven cycle-quality analytics shapes next-gen feature roadmaps. Decentralization thus multiplies sites needing compliant reprocessing, sustaining the ultrasound probe disinfection market well beyond core hospital campuses.

Geography Analysis

North America led the ultrasound probe disinfection market with 36.45% of global revenue in 2025, underpinned by FDA mandates, insurer penalties for HAIs, and capital budgets that prioritize automated HLD cabinets. Hospitals routinely integrate RFID-enabled reprocessors with electronic health records, streamlining Joint Commission audits and reinforcing best-practice diffusion across the region. The mature reimbursement climate offsets high device costs, allowing health systems to adopt premium chemical-free units rapidly.

Europe remains a substantial contributor, leveraging CE harmonization to expedite technology circulation across member states. Environmental regulations encourage migration to UV-C systems that avoid chemical disposal, and procurement frameworks increasingly weigh life-cycle sustainability metrics. Cross-border hospital groups standardize preferred vendor lists, giving compliant suppliers pan-regional scale. Meanwhile, national infection-prevention action plans push smaller clinics to match the standards of flagship university hospitals, enriching the total addressable market.

Asia Pacific is forecast to post a 14.22% CAGR as China, India, and Southeast Asian nations pour funds into imaging capacity and infection-control modernization. Government insurance schemes finance rural ultrasound deployment, frequently stipulating high-level disinfection capabilities to curb cross-infection risks. Domestic manufacturers in China and South Korea introduce cost-effective peroxide cabinets, raising competitive stakes. Emerging regions in MEA and Latin America continue to upgrade basic disinfection infrastructure, but financing gaps and supply-chain volatility temper near-term momentum.

Competitive Landscape

The ultrasound probe disinfection market is moderately fragmented. Nanosonics anchors the field with its trophon platform and logged USD 170 million revenue in fiscal 2024, supported by 34,790 installed units that protect an estimated 27 million patients each year. Competitors such as Germitec and CS Medical emphasize chemical-free UV-C and fully enclosed peroxide baths, respectively, seeking differentiation through cycle speed, footprint, and user-interface design.

Patent cliffs are lowering entry barriers, enabling mid-tier suppliers to deliver peroxide mist or ozone cabinets at disruptive price points. To defend share, incumbents bundle cloud dashboards, preventive maintenance, and staff training into subscription plans that embed switching costs. Strategic partnerships also unfold: ultrasound OEMs integrate reprocessors into equipment leases, and distributors sign exclusive regional agreements to secure service revenue.

M&A activity signals consolidation. Medline’s planned purchase of Ecolab’s global surgical solutions unit will add reprocessing accessories to its vast distribution network, potentially reshaping competitive dynamics. Vendors investing in IoT telemetry and AI-driven cycle validation are poised to command premium segments, while budget buyers weigh open-architecture cabinets that accept third-party consumables. Overall, competition pivots on regulatory compliance, documented efficacy, and lifetime cost rather than headline unit price.

Ultrasound Probe Disinfection Industry Leaders

CIVCO Medical Solutions

Tristel plc

Ecolab

Germitec

CS Medical LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: CS Medical renewed its Strategic Partner Collaborator status with APIC for 2025, strengthening education outreach to more than 15,000 infection-prevention professionals.

- February 2025: An updated ANSI/AAMI standard formally acknowledged chlorine-dioxide foam as a high-level disinfection modality for ultrasound probes, echoing 2024 WFUMB guidance.

- February 2025: Peer-reviewed research confirmed sporicidal efficacy of cabinet-based high-level disinfection devices in clinical settings.

Global Ultrasound Probe Disinfection Market Report Scope

As per the scope of this report, ultrasound probe disinfection is high-level disinfectants substances used for sterilizing or cleaning instruments and devices used in hospitals for medical application. The disinfectants are used to prevent the ultrasound probes from bacterial contamination. The Ultrasound Probe Disinfection market is segmented by Product(Instrument, Consumables and Services), By Process ( Intermediate/ low- level disinfection and High-level disinfection), Probe Type ( Linear Transducers, Convex Transducers, Phased Array Transducers, Endocavitary Transducers and Transesophageal Echocardiography Transducers), End User (Hospitals and Diagnostic Laboratories, Ambulatory care centers, Academic and Research Institutes and Others) and Geography ( North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Instruments |

| Consumables |

| Services |

| Intermediate / Low-level Disinfection |

| High-level Disinfection |

| Hydrogen-Peroxide Mist |

| UV-C Light |

| Ozone-based |

| Chlorine-Dioxide & Other Chemicals |

| Linear Transducers |

| Convex Transducers |

| Phased-Array Transducers |

| Hospitals & Diagnostic Laboratories |

| Ambulatory Care Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Instruments | |

| Consumables | ||

| Services | ||

| By Process | Intermediate / Low-level Disinfection | |

| High-level Disinfection | ||

| By Technology | Hydrogen-Peroxide Mist | |

| UV-C Light | ||

| Ozone-based | ||

| Chlorine-Dioxide & Other Chemicals | ||

| By Probe Type | Linear Transducers | |

| Convex Transducers | ||

| Phased-Array Transducers | ||

| By End User | Hospitals & Diagnostic Laboratories | |

| Ambulatory Care Centers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the ultrasound probe disinfection market?

The ultrasound probe disinfection market size stands at USD 820 million in 2026 and is projected to reach USD 1.44 billion by 2031.

Which process segment leads the market?

High-level disinfection captures 60.05% of 2025 revenue and remains the fastest-growing process at a 12.98% CAGR.

Why are UV-C cabinets gaining popularity?

UV-C systems deliver chemical-free, 90-second cycles that reduce staff exposure and simplify ventilation requirements, driving a forecast 14.55% CAGR.

Which region is growing quickest?

Asia Pacific posts the highest regional CAGR at 14.22% thanks to infrastructure expansion and stricter infection-control mandates.

How does RFID traceability benefit hospitals?

RFID-enabled cabinets auto-record each cycle, achieving 99.70% counting accuracy and streamlining accreditation audits.

What factor most restrains adoption in emerging markets?

High up-front capital costs for automated reprocessors limit uptake in budget-constrained facilities despite long-term infection-prevention savings.

Page last updated on: