Ultrasonic Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

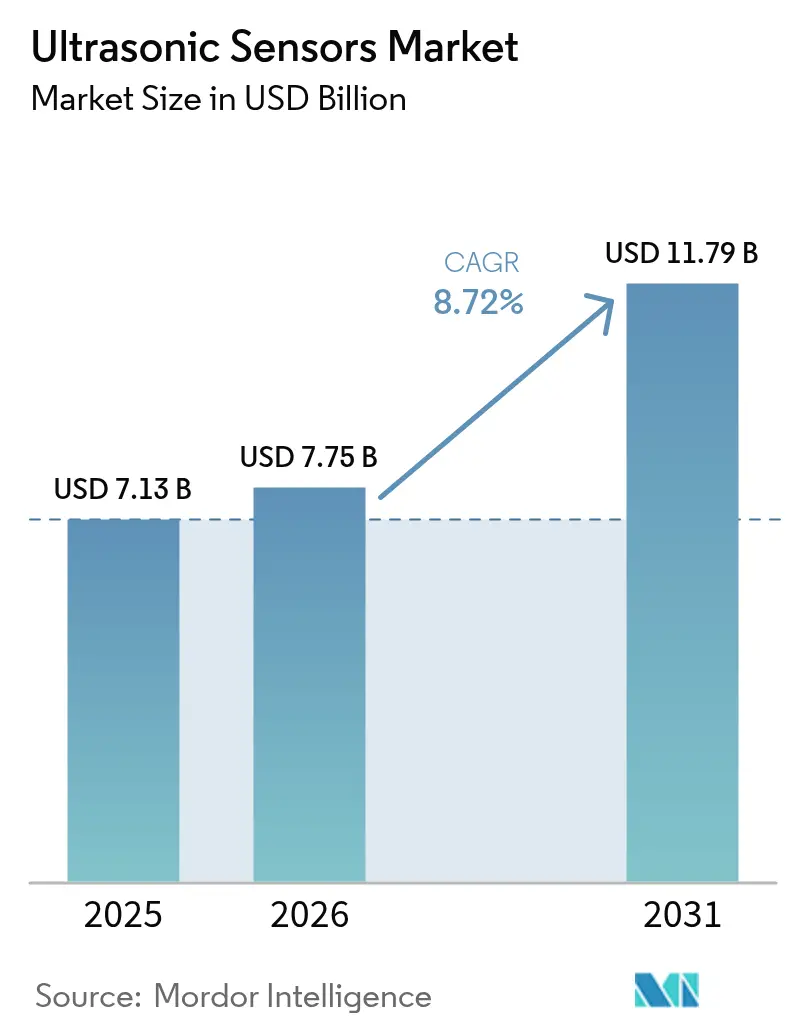

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 11.79 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Sensors Market Analysis by Mordor Intelligence

The ultrasonic sensors market size was valued at USD 7.13 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 11.79 billion by 2031, at a CAGR of 8.72% during the forecast period (2026-2031). Rising investments in Industry 4.0 automation, mandatory automotive safety mandates, and growing acceptance of non-contact measurement technologies continue to pull demand upward. Precision sensing now underpins predictive maintenance initiatives that cut downtime and stabilize production yields. Automotive manufacturers integrate multi-sensor arrays to satisfy UNECE R159 and EU GSR2 rules, while water utilities deploy ultrasonic level probes to optimize treatment plant performance. High-frequency micromachined ultrasound transducers (MUTs) widen use cases in portable medical imaging and wearable devices, and regional diversification toward South American mining and infrastructure projects broadens the revenue base. Competitive intensity rises as suppliers embed artificial intelligence in signal-processing firmware to counter cross-talk and strengthen object classification accuracy.

Key Report Takeaways

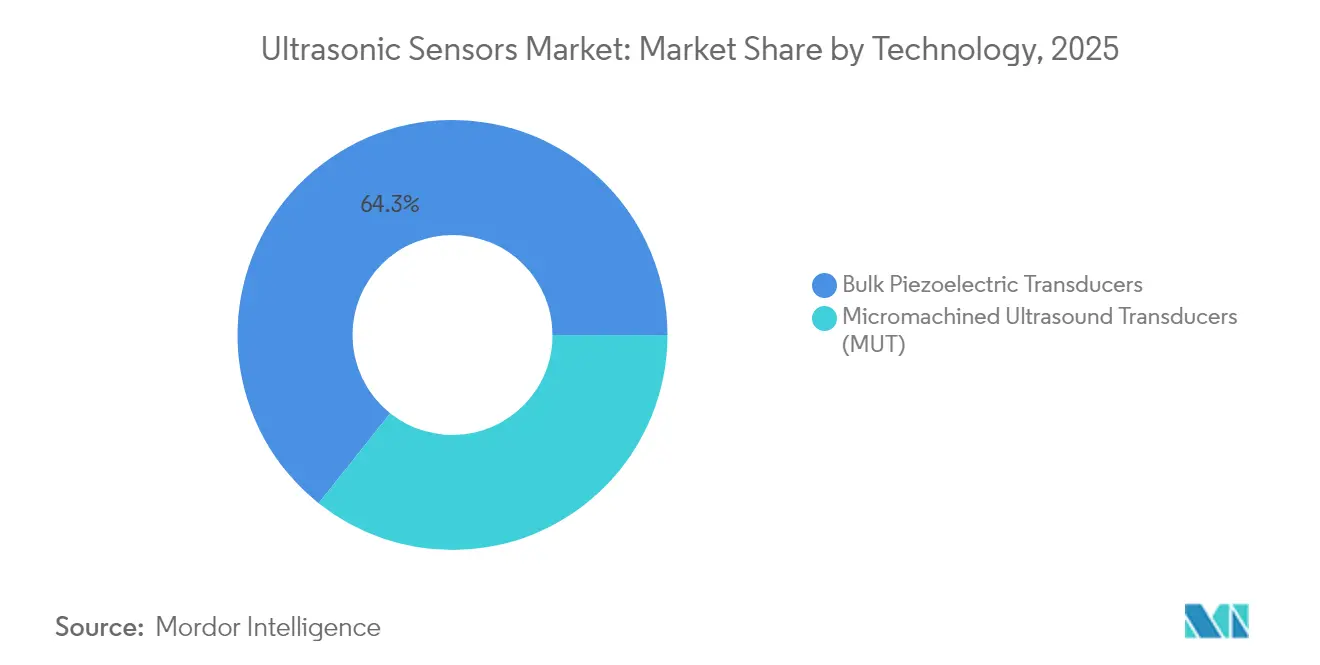

- By technology, bulk piezoelectric transducers led with 64.30% of the ultrasonic sensors market share in 2025; micromachined ultrasound transducers are poised to expand at a 12.64% CAGR through 2031.

- By product type, proximity and distance sensors accounted for 39.40% of the ultrasonic sensors market's revenue in 2025, while level and depth sensors are projected to post a 11.58% CAGR through 2031.

- By range, short-range units held 54.30% of the ultrasonic sensor market size in 2025; the long-range sub-segment is projected to grow at a 10.63% CAGR to 2031.

- By mounting, in-line and threaded formats captured 69.10% share of the ultrasonic sensors market in 2025, whereas block sensors are advancing at a 10.02% CAGR.

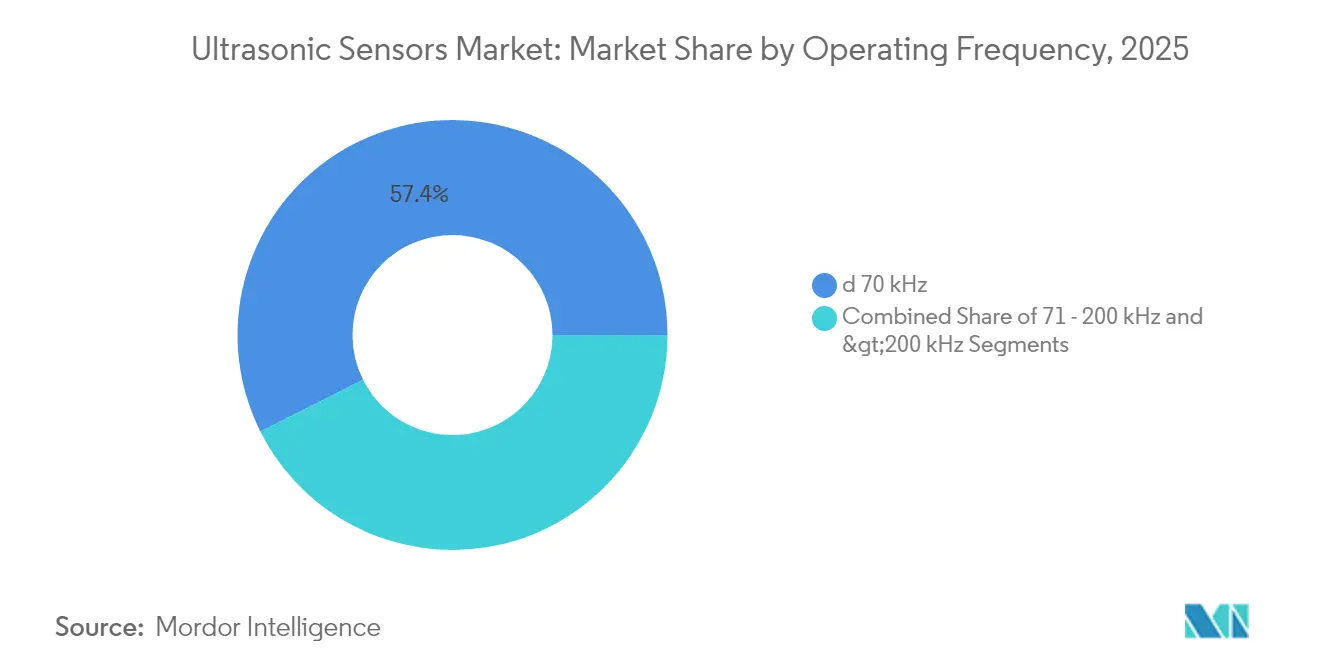

- By operating frequency, low-frequency models represented 57.40% share of the ultrasonic sensors market, while high-frequency devices are rising at 12.12% CAGR.

- By end-user, industrial manufacturing accounted for a 27.60% share of the ultrasonic sensors market in 2025, and the automotive sector is projected to grow at a 11.08% CAGR to 2031.

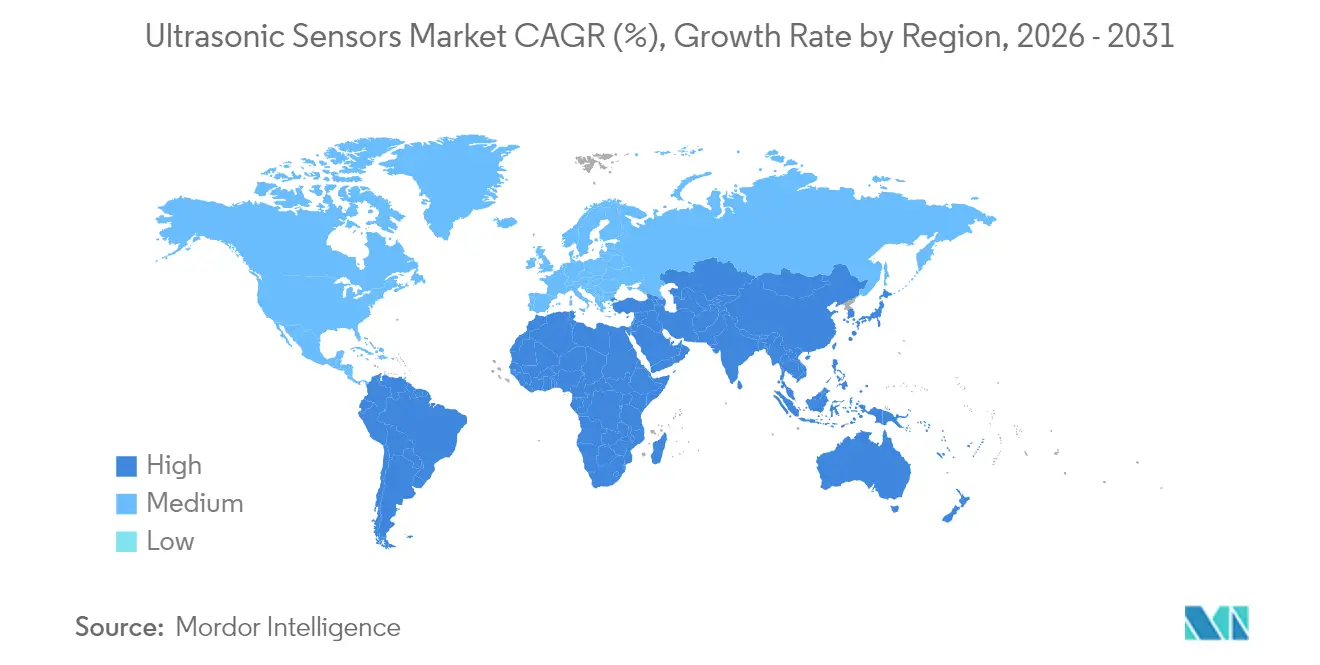

- By geography, the Asia Pacific commanded a 37.60% share of the ultrasonic sensors market in 2025; South America is projected to track a 9.76% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasonic Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising installation of high-precision ultrasonic sensors in Industry 4.0 production cells | + 2.1% | Germany, Japan, South Korea, expanding globally | Medium term (2-4 years) |

| Mandatory front-rear obstacle-detection mandates in Chinese and EU passenger-car safety regulations | + 1.8% | China, European Union, spill-over to ASEAN | Short term (≤ 2 years) |

| Rapid adoption of non-contact level monitoring in smart water and wastewater utilities across GCC countries | + 1.3% | GCC, wider MENA | Medium term (2-4 years) |

| Use of high-frequency (> 200 kHz) MUT arrays in medical point-of-care imaging devices | + 1.6% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Deployment of corrosion-resistant PVDF probes in offshore wind O&M robots | + 0.9% | North Sea, Baltic Sea, US East Coast, Asian offshore | Long term (≥ 4 years) |

| AI-driven sensor-fusion algorithms that cut false positives in industrial and mobile robotics | + 1.0% | United States, Germany, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Installation of High-Precision Ultrasonic Sensors in Industry 4.0 Production Cells

Industry 4.0 cells now demand sub-millimeter accuracy, pushing suppliers to adopt capacitive MUTs that achieve > 400 kHz and 40% broader bandwidth than legacy ceramics. IO-Link enabled devices feed machine-learning models that cut unplanned downtime by 30% through condition-based alerts. Global manufacturers localize capacity, exemplified by Omron’s USD 9.2 million expansion in South Carolina, to shorten lead times for customized probes

Mandatory Front-Rear Obstacle-Detection Mandates in Chinese and EU Passenger-Car Safety Regulations

EU GSR2 and synchronized Chinese rules compel every new light vehicle to incorporate autonomous emergency braking and lane-keeping functions that rely on close-range ultrasonic sensing. Shipments leapt from 3 million units in 2009 to 200 million in 2023. Bosch couples ultrasonic, radar, and camera signals with AI fusion algorithms that distinguish pedestrians from static objects, meeting vulnerable road user requirements

Rapid Adoption of Non-Contact Level Monitoring in Smart Water and Wastewater Utilities Across GCC Countries

GCC utilities leverage ultrasonic level probes to mitigate water scarcity and cut maintenance. World Bank research highlights the water-energy nexus, urging desalination efficiency gains that ultrasonic devices deliver through non-intrusive, corrosion-resistant measurement documents1. Pepperl+Fuchs’ LoRaWAN-enabled WILSEN.sonic modules extend coverage across vast plants, allowing real-time overflow alerts. [2]Pepperl+Fuchs, “Wireless Ultrasonic Sensors,” pepperl-fuchs.com

Deployment of Corrosion-Resistant PVDF Probes in Offshore Wind O&M Robots

Offshore wind operators adopt polyvinylidene fluoride (PVDF) ultrasonic heads inside maintenance robots to detect blade erosion and sub-sea weld defects in saline environments. Early trials in the North Sea confirm lifetime extension of sensors despite constant spray exposure, supporting long-term O&M savings for European installations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Signal attenuation in multi-sensor ADAS clusters beyond 10 m ranges | –1.4% | Global premium vehicle programs | Short term (≤ 2 years) |

| Performance drift of piezoelectric stacks under −40°C Nordic operating conditions | –0.8% | Nordic countries, Northern Canada, Siberia | Medium term (2-4 years) |

| High fabrication cost of high-frequency MUT wafers for medical imaging | –0.7% | United States, Europe, Japan | Long term (≥ 4 years) |

| Supply-chain constraints for specialty piezoelectric materials (e.g., bismuth titanate and KNN) | –0.6% | Global, with acute exposure in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Signal Attenuation in Multi-Sensor ADAS Clusters Beyond 10 m Ranges

High vehicle sensor density breeds ultrasonic cross-talk that lowers detection accuracy past 11 meters. Automotive designs now integrate 12-16 devices per car, widening interference risks. Research confirms that atmospheric variations magnify these effects, making radar or LiDAR pairing essential Sonair’s acoustic ranging and detection platform reduces sensor count by widening field-of-view to 180

Performance Drift of Piezoelectric Stacks Under −40°C Nordic Operating Conditions

Temperature swings alter dielectric constants and piezoelectric coefficients, degrading readings below −20°C. Nordic field tests call for heated housing or alternative materials. Bismuth titanate ceramics withstand high temperatures but raise cost, limiting use beyond specialty fleets.[3] MDPI, “Bismuth Titanate as an Ultrasonic Transducer for High Temperatures,” mdpi.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: MUT Arrays Drive Premium Applications

Bulk piezoelectric transducers retained a 64.30% ultrasonic sensors market share in 2025, anchored by economical mass production for automotive parking systems. The segment’s scale advantage keeps unit costs low. In contrast, MUT arrays are growing at 12.64% CAGR as medical imaging and precision robotics demand miniaturized high-frequency performance. The ultrasonic sensors market size tied to MUT technology is expected to swell sharply as PMUTs excel in air-coupled detection while CMUTs dominate liquid-coupled imaging.

The technology transition reflects physical limits in ceramic plates when shrinking form factors. Potassium sodium niobate PMUTs recorded 105.5 dB/V at 10 cm, outclassing aluminum nitride competitors . Integration with CMOS electronics simplifies on-chip beamforming that lowers total bill of materials for smart devices.

By Product Type: Level Sensors Gain Industrial Traction

Proximity and distance models captured 39.40% of 2025 revenue, favored for automotive bumpers and robot safety curtains. Level and depth sensors, however, are registering a 11.58% CAGR thanks to smart infrastructure projects. Continuous fluid-level insight curbs maintenance in water, chemical, and food facilities.

Wireless telemetry extends coverage to remote tanks, enabling predictive scheduling that trims service truck rolls. Transparent-liquid detection and through-wall sensing give ultrasonic probes an advantage over optical or float approaches, cementing market leadership across harsh industrial settings

By Range: Long-Range Applications Accelerate Growth

Short-range units (< 2 m) held 54.30% of ultrasonic sensors market size in 2025, serving core ADAS and factory safety fences. Long-range devices (> 10 m) are advancing at 10.63% CAGR as infrastructure managers seek wide-area monitoring. Microwave-inspired coding schemes now filter echoes so outdoor probes distinguish valid targets despite rain or mist.

TDK’s ICU-30201 achieves reliable 9.5 m reach at millimeter precision, making it attractive for warehouse automation and smart building occupancy analytics. Advanced field-programmable gate arrays further enhance gain control, expanding deployment in agriculture and traffic management.

By Mounting Type: Block Sensors Enable Flexible Installation

Traditional in-line and threaded formats held 69.10% share given their direct compatibility with pipes and machine housings. Retrofit-friendly block sensors are rising 10.02% annually as brownfield plants avoid disruptive pipe cutting. Clamp-on flow meters now underpin mature oilfield surveillance, providing real-time output without process interruption.

Wireless blocks mount externally on tanks, leveraging lithium batteries and mesh radios to support temporary field trials that validate process improvements before full capital commitment.

By Operating Frequency: High-Frequency Applications Drive Innovation

Low-frequency units (≤ 70 kHz) retained 57.40% share for applications requiring deep penetration or dusty-air tolerance. High-frequency devices (> 200 kHz) show a 12.12% CAGR supported by medical imaging demand. Frequency agility allows probes to sweep bands, combining near-field and far-field coverage in one package.

Portable scanners use > 5 MHz internally reflected waves for soft tissue diagnostics while industrial wafers deploy 300 kHz bursts for sub-millimeter inspection of semiconductor wafers.

By End-User Vertical: Automotive Mobility Accelerates Adoption

Industrial manufacturing led with 27.60% share in 2025, grounded in decades of automation spend. Automotive is growing 11.08% annually via mandatory safety features and autonomous capability roadmaps. Consumer electronics taps ultrasonic time-of-flight for gesture control, while agriculture leverages sensors for grain fill monitoring and livestock presence.

Medical adoption climbs as point-of-care devices shrink cost and power requirements, enhancing chronic disease management and remote examinations.

Geography Analysis

Asia secured 37.60% of 2025 revenue on the back of China’s vehicle electronics boom and Japan’s precision manufacturing heritage. Government mandates make ultrasonic proximity detection standard in new passenger cars, while semiconductor clusters enable native MUT fabrication. South Korea supplies sensor ASICs, and India’s affordable vehicle market increases penetration of cost-optimized designs. Policy-driven smart-city spending further embeds the ultrasonic sensors market in regional infrastructure rollouts.

North America concentrates on premium niches. The United States advances high-frequency probes for ambulatory diagnostics, while the aerospace sector exploits ruggedized units for structural health monitoring. Canada’s winter environment shapes demand for temperature-compensated stacks. FDA guidance streamlines approvals, bringing new platforms to bedside and home settings faster than in earlier regulatory cycles.

Europe blends regulatory leadership and industrial prowess. EU GSR2 triggers synchronized automotive demand, and Germany’s robotics clusters pioneer IO-Link enabled probes for real-time process feedback. Nordic utilities request heated sensor packages that withstand −40 °C, spurring material engineering breakthroughs. Meanwhile, South America posts the fastest 9.76% CAGR as mining firms automate remote sites and governments modernize water networks, enhancing need for resilient non-contact measurement.

Competitive Landscape

The ultrasonic sensors market shows moderate fragmentation as no single player dominates every niche. Keyence, Pepperl+Fuchs, and Sick AG leverage proven reliability and broad distribution, enabling rapid global delivery. Bosch, Denso, and Texas Instruments embed AI engines in sensor controllers, elevating object recognition and lowering false-positive rates. Start-ups such as Sonair introduce 3D acoustic ranging that trims sensor counts and system costs.

Strategic moves spotlight software differentiation. Bosch is investing EUR 2.5 billion in AI through 2027, positioning edge-processed data as a service for OEMs.[1] Robert Bosch GmbH, “AI that gets things moving,” bosch-presse.de BinMaster’s buyout of Senix broadens industrial level sensing lines, while Omron’s US plant targets rapid customization for North American clients. White-space opportunities remain in harsh offshore and Arctic domains, where PVDF heads and thermal compensation claim premium pricing.

Ultrasonic Sensors Industry Leaders

Keyence Corporation

Pepperl+Fuchs AG

Honeywell International Inc.

Baumer Ltd

Rockwell Automation Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sonair secures funding to develop a new 3D ultrasonic sensor for autonomous mobile robots, set to reduce costs by 50-80% compared to conventional LiDAR systems.

- May 2025: TDK InvenSense released the ICU-30201 time-of-flight sensor via Mouser Electronics

- January 2025: Bosch Sensortec outlined plans to ship 10 billion intelligent sensors by 2030

- October 2024: BinMaster acquired Senix Corporation to enhance ToughSonic level offerings.

Global Ultrasonic Sensors Market Report Scope

The basic working principle of ultrasonic sensors is based on echolocation, involving the transmission of ultrasonic waves to the target object, which reflects it to the source after receiving the initial wave. Ultrasonic sensors detect the object's exact position by calculating the distance from the source's "echo" generated by the object.

The study tracks the revenue accrued from sales of ultrasonic sensor-based solutions offered by market vendors across the globe.

Ultrasonic sensors market is segmented by technology (bulk piezoelectric transducer, micromachined ultrasound transducers (MUT)), by end-user vertical (automotive, consumer, industrial, medical, other end-user verticals), by geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Rest of Europe], Asia Pacific [China, Japan, India, Rest of Asia Pacific], Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Bulk Piezoelectric Transducers | |

| Micromachined Ultrasound Transducers (MUT) | PMUT (Piezo-MUT) |

| CMUT (Capacitive-MUT) |

| Proximity and Distance Sensors |

| Level/Depth Measurement Sensors |

| Flow-measurement Sensors |

| Ultrasonic Imaging Modules |

| Short-range ( < 2 m) |

| Medium-range (2 - 10 m) |

| Long-range ( > 10 m) |

| In-line / Threaded |

| Block / Side-Looking |

| Splice / Clamp-on |

| <70 kHz |

| 71 - 200 kHz |

| > 200 kHz |

| Industrial Manufacturing |

| Automotive and Mobility |

| Consumer Electronics and Appliances |

| Medical and Healthcare |

| Agriculture and Smart Farming |

| Others (Oil and Gas, Marine, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | Bulk Piezoelectric Transducers | |

| Micromachined Ultrasound Transducers (MUT) | PMUT (Piezo-MUT) | |

| CMUT (Capacitive-MUT) | ||

| By Product Type | Proximity and Distance Sensors | |

| Level/Depth Measurement Sensors | ||

| Flow-measurement Sensors | ||

| Ultrasonic Imaging Modules | ||

| By Range | Short-range ( < 2 m) | |

| Medium-range (2 - 10 m) | ||

| Long-range ( > 10 m) | ||

| By Mounting Type | In-line / Threaded | |

| Block / Side-Looking | ||

| Splice / Clamp-on | ||

| By Operating Frequency | <70 kHz | |

| 71 - 200 kHz | ||

| > 200 kHz | ||

| By End-user Vertical | Industrial Manufacturing | |

| Automotive and Mobility | ||

| Consumer Electronics and Appliances | ||

| Medical and Healthcare | ||

| Agriculture and Smart Farming | ||

| Others (Oil and Gas, Marine, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the ultrasonic sensors market?

The ultrasonic sensors market stands at USD 7.75 billion in 2026 and is projected to reach USD 11.79 billion by 2031.

Which technology segment is growing fastest?

Micromachined ultrasound transducers are expanding at a 12.64% CAGR through 2031, driven by medical imaging and precision industrial uses.

How do automotive regulations influence demand?

EU GSR2 and parallel Chinese mandates require obstacle-detection systems, boosting vehicle sensor shipments and accelerating integration of ultrasonic arrays.

Which region offers the highest growth outlook?

South America exhibits the fastest regional CAGR at 9.76% between 2026 and 2031, thanks to infrastructure and mining automation investments.

Page last updated on: