GCC Flat Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

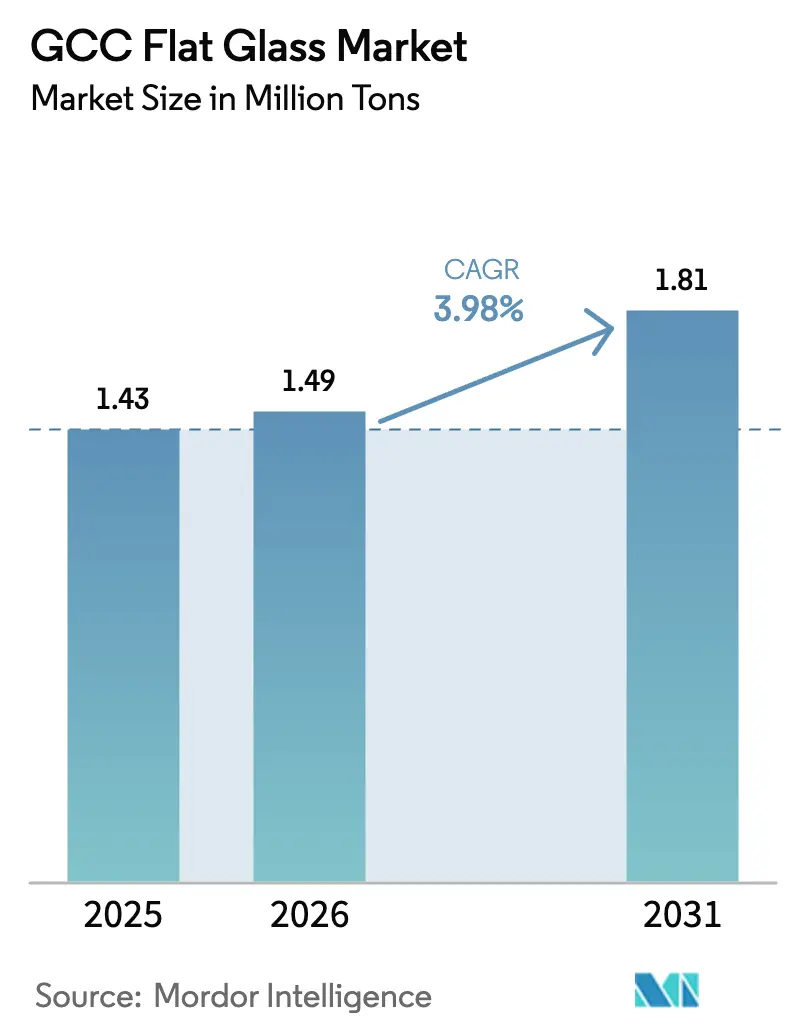

| Base Year Market Size (2025) | 1.43 Million tons |

| Market Volume (2026) | 1.49 Million tons |

| Market Volume (2031) | 1.81 Million tons |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

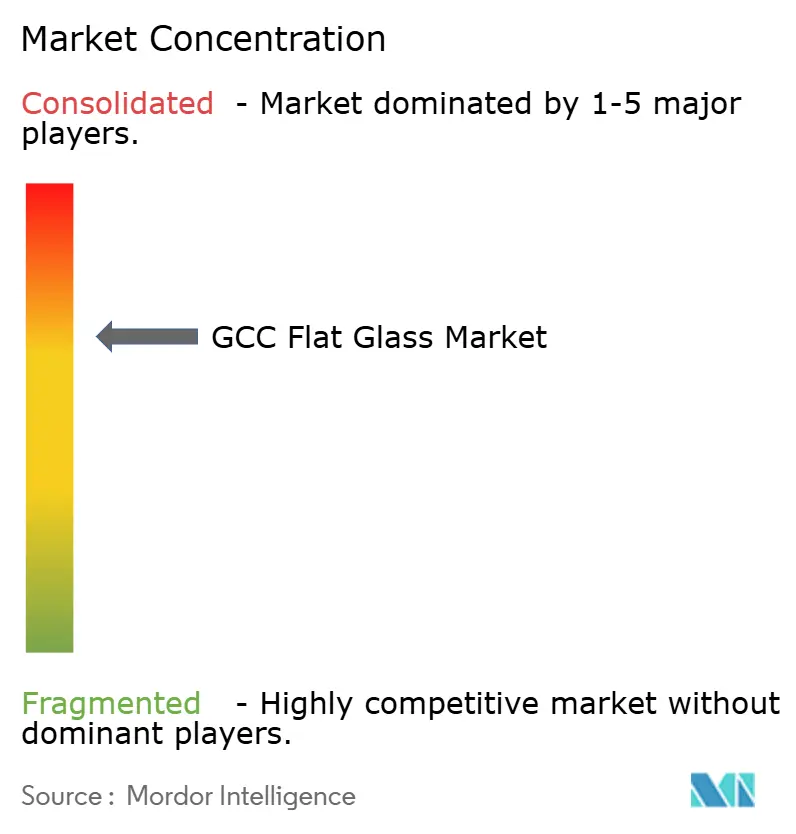

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Flat Glass Market Analysis by Mordor Intelligence

The GCC Flat Glass Market size was valued at 1.43 million tons in 2025 and estimated to grow from 1.49 million tons in 2026 to reach 1.81 million tons by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). Expansion stems from the synchronized infrastructure agenda of Gulf economies, the steady rollout of renewable energy megaprojects, and policy pressure to localize material supply. Energy-efficient glazing regulations in Saudi Arabia, the United Arab Emirates, and Qatar have accelerated the switch from basic to value-added products, while the solar industry’s rapid scale-up is introducing specialized demand for low-iron, anti-reflective glass. Manufacturing investments totaling more than USD 1 billion since 2024 underscore confidence in regional self-sufficiency, although natural gas price swings and trade defense measures complicate cost planning for producers. Competitive positioning depends on integrated production footprints, advanced coating capabilities, and the ability to serve engineering, procurement, and construction contractors that prefer single-source façade packages.

Key Report Takeaways

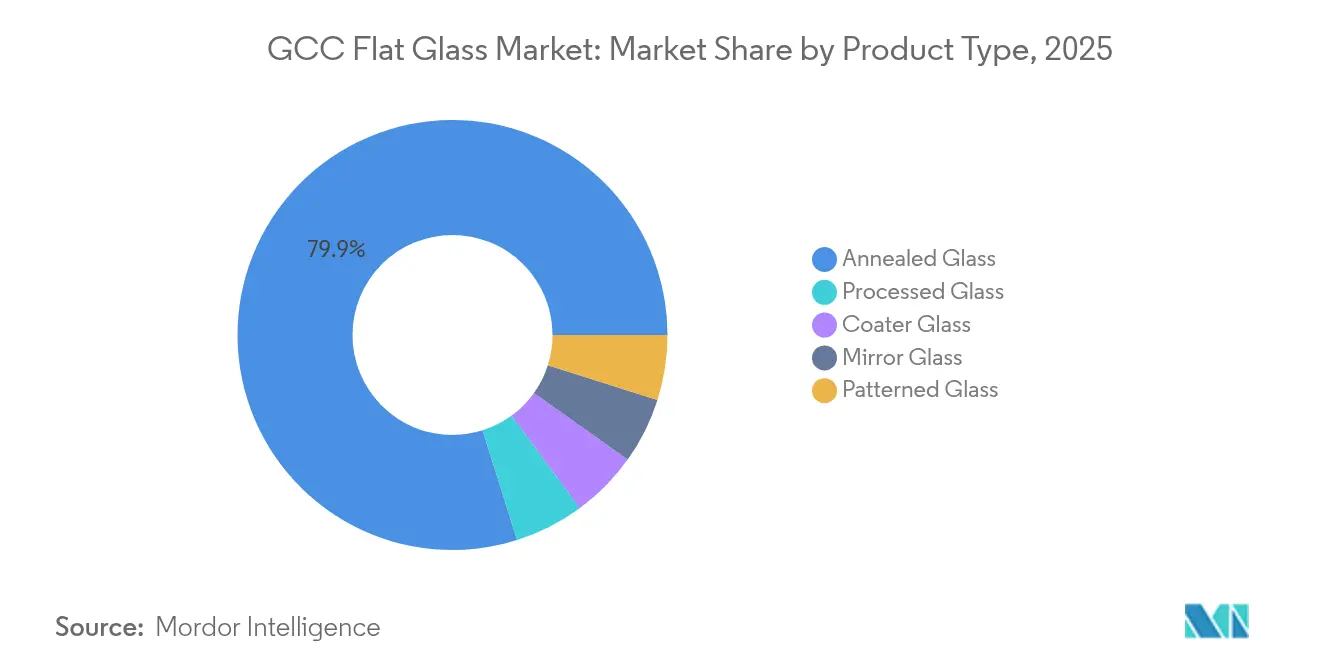

- By product type, annealed glass led with an 79.86% share of the GCC flat glass market in 2025, while processed glass is projected to post the fastest growth of 4.72% CAGR through 2031.

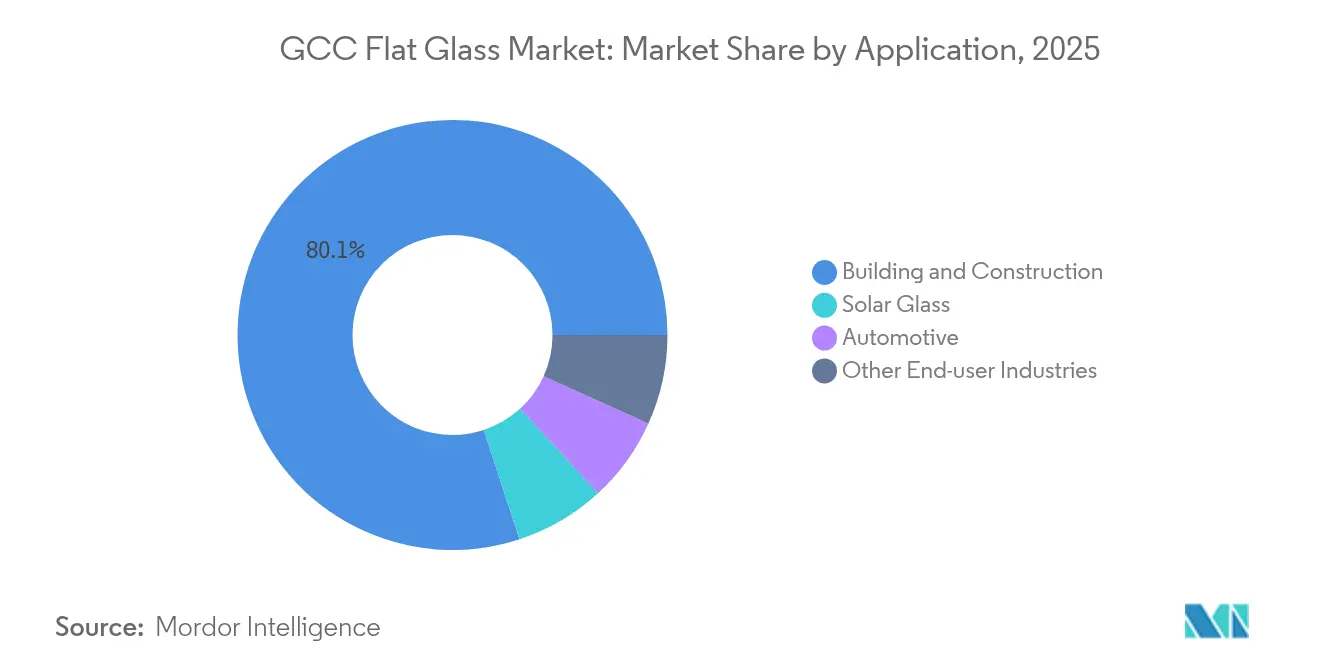

- By application, building and construction accounted for 80.05% share of the GCC flat glass market size in 2025, and solar glass is expected to expand at a 6.65% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 60.10% of the GCC flat glass market share in 2025 and is projected to grow at a 4.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Flat Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in GCC Green-Building Mandates | +1.2% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Mega-Projects (NEOM, Lusail, Expo-City) Unlocking Demand | +1.8% | Saudi Arabia, UAE, Qatar | Long term (≥4 years) |

| Rise of Integrated Façade Contracting | +0.7% | GCC-wide, led by UAE, Saudi Arabia | Short term (≤2 years) |

| Localization Push for Float-Line Capacity | +0.9% | Saudi Arabia, spillover to Kuwait, Bahrain | Medium term (2-4 years) |

| Growth of Solar-Glass for CSP Plants | +1.1% | Saudi Arabia, UAE | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Boom In GCC Green-Building Mandates

Tighter building codes, introduced in 2024, require energy-saving glazing for large new projects. Saudi Arabia’s Green Building Code requires structures exceeding 1,000 m² to utilize glass configurations that meet stringent thermal-performance targets, which has prompted developers to adopt low-emissivity coatings[1]Saudi Green Building Council, “Saudi Green Building Code Overview,” sgbgbc.org. Dubai’s Al Sa’fat framework enhances rating points for façades, ensuring solar heat-gain coefficients remain below 0.25 —a requirement that drives demand for coated or laminated units. Qatar and Kuwait have enacted parallel code updates capping allowable U-values, further widening the specification gap between annealed and processed products. Collectively, these rules support the 4.80% growth path for processed glass by channeling mainstream demand into higher-margin categories. Manufacturers capable of securing GSO 2663:2024 and GSO 2891:2024 certifications now enjoy preferred status in major tenders, giving established regional producers a competitive edge.

Mega-Projects (NEOM, Lusail, Expo-City) Unlocking Demand

Flagship schemes are multiplying overall square meters of glazing consumed. NEOM alone is estimated to need 50 million m² of specialized glass for its linear city, industrial districts, and tourism assets. Saudi Arabia’s Red Sea Amaala and Diriyah Gate clusters add thousands of hotel keys, each specified with high-performance façades. Qatar’s post-World-Cup project slate in Lusail keeps specialty glass orders flowing, while Dubai’s Expo City is committed to net-zero operations that depend on smart glazing. Developers favor local or regional suppliers to minimize logistics risk and comply with local-content rules, prompting manufacturers to expand their capacity near demand centers. Specifications often exceed commodity thresholds, favoring suppliers who can tailor optical, acoustic, and safety properties to meet project briefs.

Rise Of Integrated Façade Contracting (EPC-Glass Synergies)

Contractors are shifting away from fragmented sourcing in favor of single-vendor façade packages that encompass design, manufacturing, and installation. Dubai Investments’ glass cluster secured AED 2 billion in 2024 contracts by offering float, coating, and assembly services from a single platform. The integrated approach shortens project cycles and reduces coordination risk, creating entry barriers for standalone processors. Regional firms with local code knowledge and logistics agility can compete effectively against import-dependent suppliers. Consolidation among mid-sized processors is accelerating as they seek to achieve scale and technical breadth to meet EPC expectations.

Localization Push For Float-Line Capacity (Saudi Vision 2030)

Vision 2030 aims for 70% local content in construction inputs by 2030. Obeikan’s SAR 520 million second float line raised domestic capacity by 180,000 tons in 2024, supported by loans from the Saudi Industrial Development Fund, which covered up to 75% of the project cost. Import-duty adjustments further tilt price structures in favor of domestic output. New processing partnerships, such as Obeikan’s 2025 alliance with Isoclima, extend the localization narrative into automotive glass and advanced laminates. Rising self-sufficiency is expected to shift intra-GCC trade flows, positioning Saudi Arabia as a net exporter by the decade’s close.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural-Gas Price Volatility Affecting Furnace Economics | -0.8% | GCC-wide, especially UAE, Qatar | Short term (≤2 years) |

| Increasing Antidumping Probes On Imported Flat Glass | -0.5% | GCC-wide | Medium term (2-4 years) |

| Slow Certification Cycles For New Glazing Technologies | -0.3% | GCC-wide, led by Saudi Arabia, UAE | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Natural-Gas Price Volatility Affecting Furnace Economics

Glass furnaces run nonstop at nearly 1,600 °C and consume 80-87% of plant energy. When gas costs surge past 40% of total production expense, small producers face margin compression and may idle capacity[2]EFI Foundation, “Energy Intensity in Glass Manufacturing,” efi.org. UAE and Qatar, which link gas tariffs to global LNG benchmarks, feel volatility more acutely than Saudi Arabia’s administered system. Larger groups like Emirates Float Glass hedge exposure with long-term contracts and heat-recovery upgrades. Smaller players lacking scale or capital for efficiency retrofits risk market exit, a trend that accelerates capacity consolidation.

Increasing Antidumping Probes On Imported Flat Glass

The GCC initiated an antidumping investigation in October 2024, covering imports from China and Iran under HS 7005.21 and 7005.29. Preliminary margins range from 15% to 40%, signaling likely duties that will increase import costs. Domestic producers stand to gain share, yet builders may face higher glazing bills just as mega-projects peak. Potential duty imposition influences foreign investors to relocate manufacturing to the region, balancing supply loss from curtailed imports with new localized output.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Annealed Glass Dominance Faces Processing Revolution

Annealed glass remains the workhorse of the GCC flat glass market, accounting for 79.86% of the volume in 2025, thanks to its cost-efficient supply for mass residential and commercial builds. The rising popularity of curtain-wall façades with low-emissivity coatings is steering architects toward processed options. This shift is evident in procurement for NEOM’s mixed-use towers, where coated units replace commodity clear glass to meet thermal comfort targets.

Processed glass, led by tempered and laminated categories, is on track for a 4.72% annual growth rate through 2031, signaling a structural upgrade cycle. Coated products benefit from low-solar-gain specifications, while mirror and decorated variants are used in hotel and luxury retail fit-outs in Dubai, Riyadh, and Doha. Investments by Saint-Gobain and Guardian in magnetron-sputter coating lines enable the local production of triple-silver low-e glass, which was previously imported. Domestic processors, such as Obeikan, are forming technical alliances with European firms to capture premium applications, thereby shrinking lead times and reducing currency exposure for contractors. As these capabilities scale, the GCC flat glass market will rely less on imported processed units, an inflection that supports the region’s localization agenda.

By Application: Solar Glass Accelerates Beyond Construction Dominance

Building and construction kept an 80.05% share of the GCC flat glass market size in 2025. Mid-market residential towers, hospitals, and educational campuses, which form part of national housing and social infrastructure programs, anchor baseline demand. Curtain-wall systems, atriums, and skylights across mixed-use complexes reinforce high-volume draw.

Solar glass, though starting from a smaller base, outpaces all other applications at a 6.65% CAGR to 2031. Renewable-energy targets adopted by the UAE and Saudi Arabia require low-iron, anti-reflective sheets for utility-scale CSP and photovoltaic farms. Almaden’s planned 500,000-ton plant in Abu Dhabi alone will add enough capacity to glaze 5 GW of panels yearly, a scale that reconfigures supply dynamics. Automotive glass is expected to maintain mid-single-digit growth, buoyed by Saudi Arabia's ambitions to localize vehicle assembly. Building-integrated photovoltaic façades illustrate convergence between construction and solar applications, combining energy generation with envelope performance. As policy incentives broaden, specialized solar glass could erode construction’s share by the end of the decade, diversifying revenues for producers able to meet optical and durability benchmarks.

Geography Analysis

Saudi Arabia holds the lion’s share of 60.10% of the GCC flat glass market and is forecast to compound at 4.64% per year through 2031. The pipeline of giga-projects—NEOM, Red Sea, and Diriyah Gate—creates scale unmatched in the region. Local production is expanding: Obeikan’s second float line lifted nameplate capacity to 360,000 tons, and Gulf Guard is commissioning a USD 215 million expansion. Vision 2030 incentives favor domestic over imported glass, and duty tweaks reinforce price competitiveness. The kingdom’s renewables push adds solar-glass pull, aligning construction and energy sectors in driving demand.

The United Arab Emirates serves as a technology hub within the GCC flat glass market. Ras Al Khaimah’s industrial zone hosts Guardian Glass, Saverglass, and a growing cohort of solar-glass specialists. Glass Technology’s AED 350 million plant, inaugurated in April 2025, produces 5.5 million module sets annually, underpinning Abu Dhabi’s solar roadmap. Dubai’s luxury high-rise backlog sustains the appetite for smart and decorative glazing, allowing for premium pricing that funds further coating innovations. UAE manufacturers export across the Gulf and East Africa, leveraging free-zone logistics and trade pacts.

Qatar, Oman, Kuwait, and Bahrain represent smaller but stable slices. Qatar continues to retrofit stadium infrastructure into mixed-use assets, keeping specialty orders alive. Oman’s Duqm projects and Kuwait’s oil-sector office schemes maintain baseline consumption. These markets increasingly secure supply from Saudi and UAE plants, shaving lead times and reducing currency fluctuation risks tied to Asian imports. Over the forecast horizon, intra-GCC trade is expected to dominate more than 70% of shipments, confirming the bloc’s manufacturing self-reliance.

Competitive Landscape

The GCC Flat Glass market is moderately concentrated. Global majors Saint-Gobain, Guardian Industries, and AGC maintain a formidable presence via patented coating technology, global procurement leverage, and long-standing ties with multinational contractors operating in the Gulf. Their regional subsidiaries enjoy early-spec status on mega-projects that require documented performance histories. Nevertheless, regional champions such as Emirates Glass, Obeikan Glass, and Dubai Investments have closed the capability gap by adding magnetron sputter lines, automated cutting facilities, and integrated façade-assembly units.

GCC Flat Glass Industry Leaders

Saint-Gobain

Guardian Industries

Emirates Glass LLC

Obeikan Glass Company

Şişecam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Obeikan Glass and the Chinese technology company Liaoning Zhongyuan signed an agreement to launch a second float glass (a type of flat glass) line in Yanbu, Saudi Arabia. The move aims to strengthen Obeikan Glass’s industrial presence. The float glass line will have a capacity of 650 tpd.

- January 2024: Aria Holding, a prominent Qatari conglomerate, signed a deal with the Government of Maharashtra, India, to set up a float glass (a type of flat glass) manufacturing facility in India, with an investment of USD 240 million. This venture is poised to bolster the revenue streams of the Qatari conglomerate and provide a boost to the local market.

GCC Flat Glass Market Report Scope

Flat glass, also called sheet or plate glass, is frequently used to create solar panels, windows, mirrors, and doors. Sand, silica, limestone, and soda ash are melted to create a liquid, which is then cooled to create a product of the required thickness.

The GCC flat glass market report is segmented by product type, end-user industry, and geography. By product type, the market is segmented into annealed glass (including tinted glass), coater glass, reflective glass, processed glass, and mirrors. By end-user industry, the market is segmented into building and construction, automotive, solar glass, and other end-user industries (electronics, aerospace, etc.). By geography, the market is segmented into Saudi Arabia, United Arab Emirates, Qatar, Kuwait, and the Rest of GCC. The report also covers the market size and forecasts for the flat glass market in 4 countries in the region. For each segment, the market sizing and forecasts are provided in terms of value (USD).

| Annealed Glass |

| Coater Glass |

| Processed Glass |

| Mirror Glass |

| Patterned Glass |

| Building and Construction |

| Automotive |

| Solar Glass |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Product Type | Annealed Glass |

| Coater Glass | |

| Processed Glass | |

| Mirror Glass | |

| Patterned Glass | |

| By Application | Building and Construction |

| Automotive | |

| Solar Glass | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain |

Key Questions Answered in the Report

How large will GCC flat glass demand be by 2031?

Volumes are forecast to reach 1.81 million tons by 2031, rising from 1.49 million tons in 2026.

Which country drives most consumption?

Saudi Arabia accounts for 60.10% of regional demand and combines the highest volume with a 4.64% CAGR outlook.

What segment is growing quickest?

Solar glass leads with a projected 6.65% CAGR to 2031 due to large-scale CSP and photovoltaic projects.

Why are processors adding capacity in the UAE?

Free-zone logistics, proximity to solar-park projects, and supportive industrial policy attract investments like Almaden’s 500,000-ton plant.

How do energy prices affect manufacturers?

Natural-gas volatility can raise furnace running costs to more than 40% of total production expenses, eroding margins for smaller plants.

Page last updated on: