Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

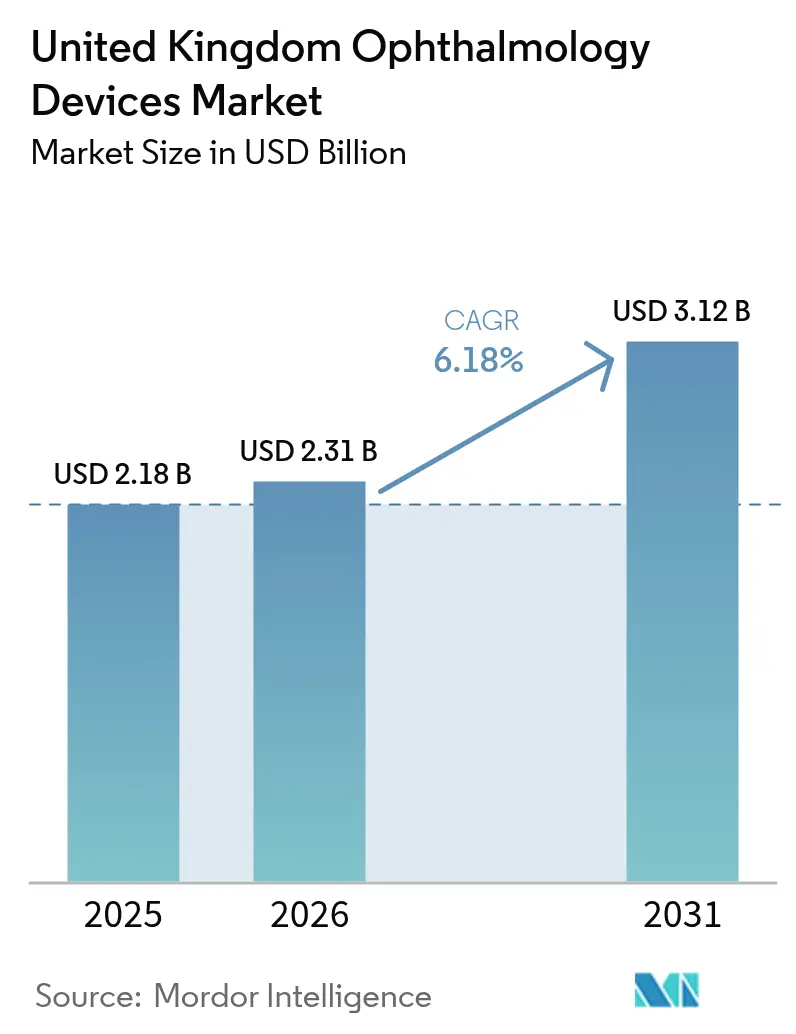

| Base Year Market Size (2025) | USD 2.18 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

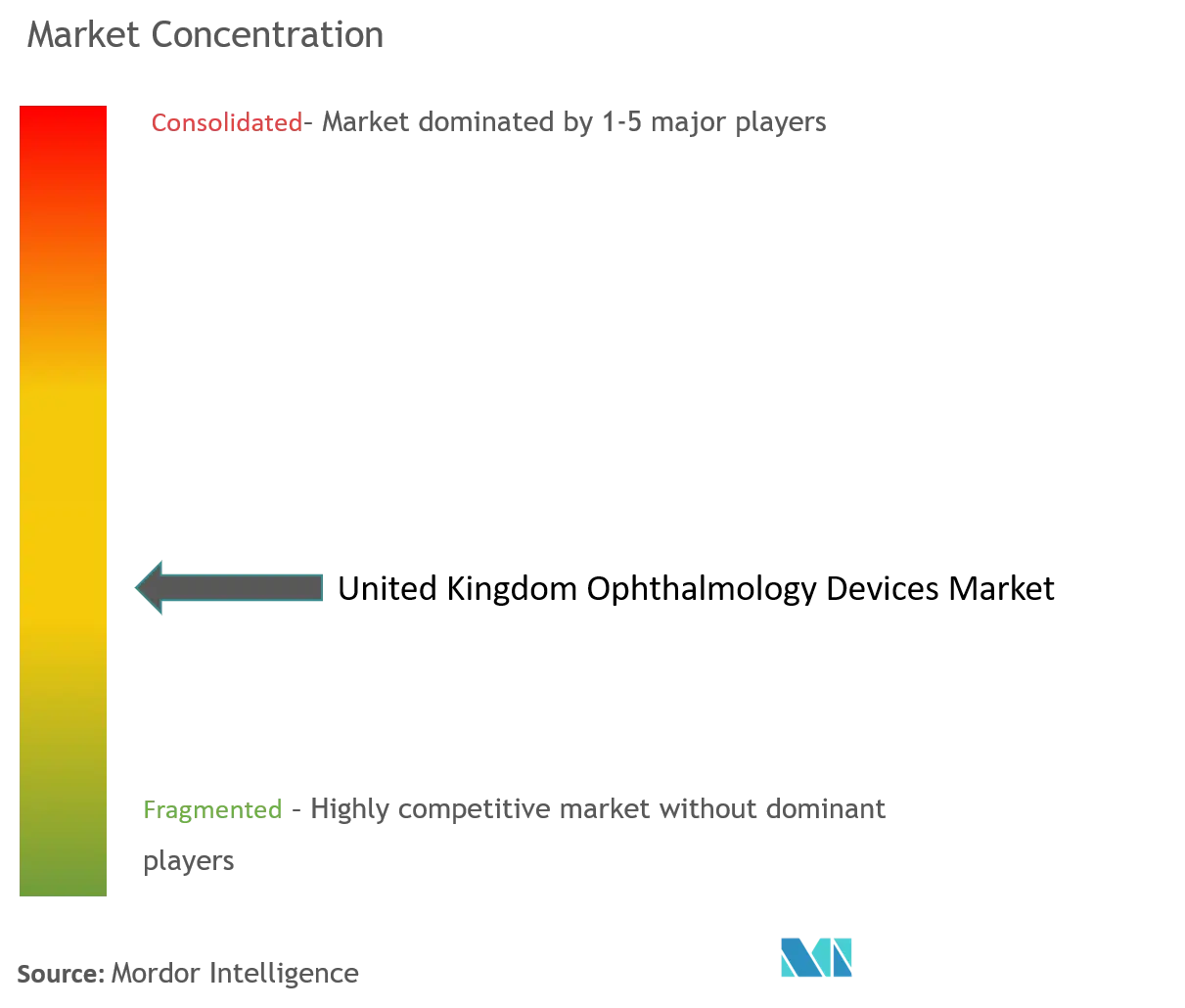

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Ophthalmology Devices Market Analysis by Mordor Intelligence

United Kingdom Ophthalmic Devices market size in 2026 is estimated at USD 2.31 billion, growing from 2025 value of USD 2.18 billion with 2031 projections showing USD 3.12 billion, growing at 6.18% CAGR over 2026-2031. Robust demand for sight-saving surgery, an ageing population that expands the cataract pool, and National Health Service (NHS) framework contracts that reward outcome documentation collectively underpin sustained growth in the United Kingdom Ophthalmic Devices market. Vision-care consumables secure stable volumes through retail channels, yet heightened spending on imaging and analytics indicates a gradual pivot toward data-rich diagnostics. Private equity-funded ambulatory surgery centres (ASCs) continue to roll out modular theatres, nudging suppliers to refine value-based pricing compatible with NHS tariffs and commercial self-pay packages. NHS backlogs created during the pandemic are not expected to clear before mid-2026, locking high baseline volumes for cataract, glaucoma, and retina devices.

Key Report Takeaways

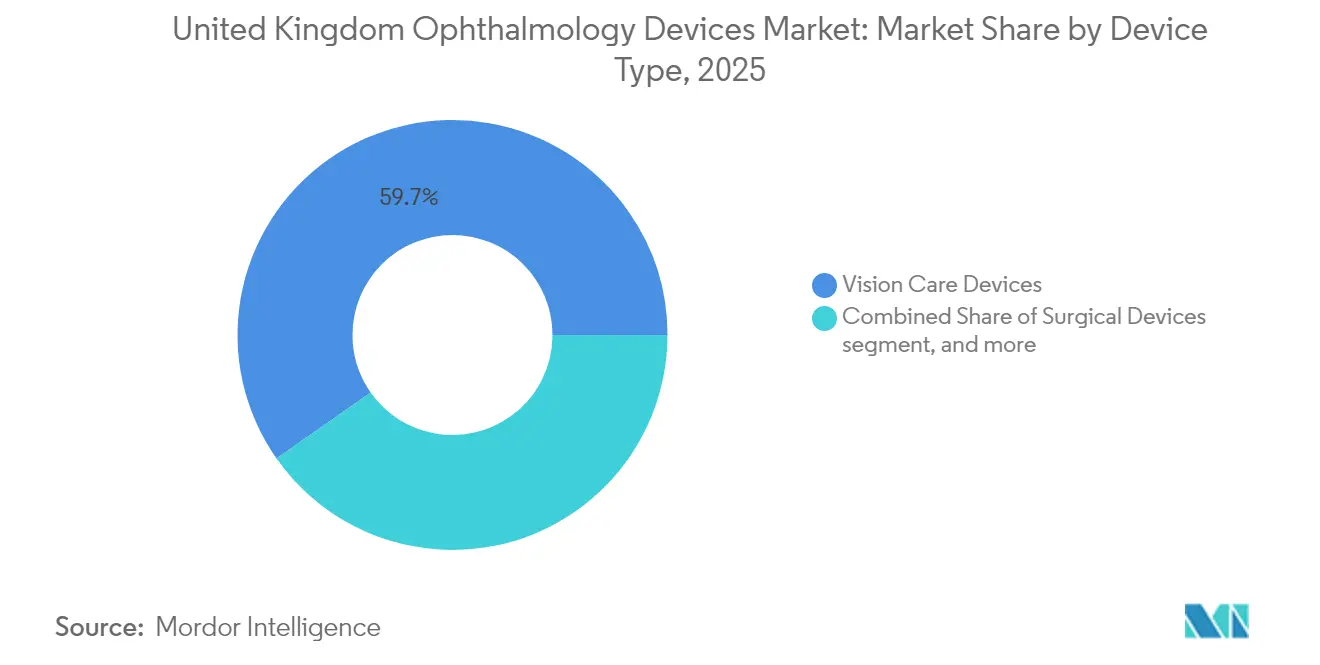

- By device type, vision care devices led with 59.74% of United Kingdom ophthalmic devices market share in 2025, while diagnostic & monitoring devices are forecast to rise at an 8.46%CAGR through 2031.

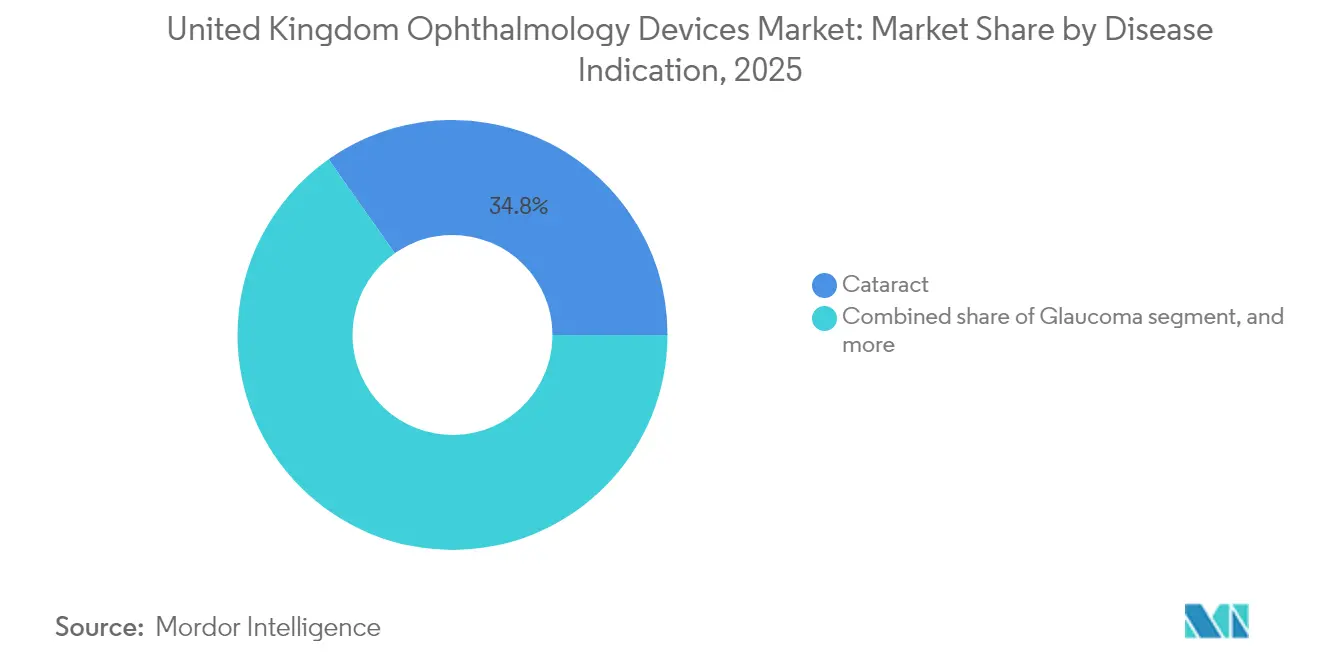

- By disease indication, cataract equipment captured 34.78% of the United Kingdom ophthalmic devices market size in 2025, yet diabetic-retinopathy systems are set to expand at a 7.62%CAGR to 2031.

- By end user, hospitals held 40.05% share in 2025 and ASCs are moving ahead at a 7.45%CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Ophthalmology Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing UK population driving cataract and glaucoma burden | +1.2% | United Kingdom | Long term (≥ 4 years) |

| Myopia “epidemic” among under-25s post-pandemic screen-time surge | +1.1% | United Kingdom | Long term (≥ 4 years) |

| NHS elective-surgery backlog accelerating private ophthalmic investments | +1.0% | England | Short term (≤ 2 years) |

| Roll-out of high-street OCT services by large optical chains | +0.9% | United Kingdom | Short term (≤ 2 years) |

| UK MHRA’s Innovation Pathway fast-tracking novel implants | +0.8% | United Kingdom | Medium term (2-4 years) |

| Surge in adoption of minimally invasive glaucoma surgery (MIGS) devices | +0.7% | United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing UK Population Driving Cataract and Glaucoma Burden

United Kingdom census updates published in March 2025 show that residents aged ≥65 now account for 19.6 million people, or 28% of the total population, up from 26% in 2024[1]Office for National Statistics, “UK Population Estimates 2025,” ons.gov.uk. Royal College of Ophthalmologists (RCOphth) modelling projects that cataract operations will rise by 50% between 2025 and 2035 if service capacity keeps pace. Hospital Episode Statistics confirm the trend: cataract extractions exceeded 475,000 in financial-year 2024/25, marking a 6.2% jump on the previous year and the steepest annual increase since electronic records began in 2010. Glaucoma workload is following suit; English NHS trusts recorded 8% more trabeculectomies in 2024 than in 2023, while outpatient visits for chronic open-angle glaucoma surpassed 1.6 million for the first time. Device makers selling phaco systems, glaucoma stents and intraocular lenses are therefore locking in multiyear supply agreements as commissioners try to ring-fence inventory against a clearly visible demographic bulge.

Myopia “Epidemic” Among Under-25s Post-Pandemic Screen-Time Surge

A peer-reviewed study released by University College London in February 2025 found that 34% of British 18- to 24-year-olds are now myopic, compared with 28% in 2020, attributing the acceleration to sustained screen exposure during pandemic lockdowns[2]University College London, “Post-Lockdown Myopia Trends,” ucl.ac.uk. Boots Opticians reported a 22% year-on-year rise in orders for myopia-control contact lenses during calendar-year 2024, while Specsavers introduced axial-length measurement in 650 stores by December 2024 to meet demand for earlier intervention. The data resonate with the College of Optometrists’ 2024 survey in which 61% of practitioners cited “more teenage myopia fittings than at any time in their careers”. Device suppliers are responding with oxygen-permeable daily disposables and spectacle-lens designs that slow axial elongation, targeting a market segment with decades of lifetime value. The cascading effect is that manufacturers traditionally focused on geriatric indications are now re-tooling marketing to parents and universities, broadening the revenue base beyond post-retirement consumers.

NHS Elective-Surgery Backlog Accelerating Private Ophthalmic Investments

Elective-care waiting-list data published in April 2025 show 7.13 million outstanding referrals across England, with ophthalmology contributing 646,000 cases—second only to orthopaedics[3]NHS England, “Elective Recovery Data April 2025,” england.nhs.uk. In response, NHS England awarded GBP 225 million in outsourcing contracts to independent-sector providers for 2025/26, 32% higher than the previous framework year. Private-equity activity has kept pace: Morgan Stanley Private Credit injected USD 102 million into Unifeye Vision Partners in May 2025 to finance U.K. site acquisitions, while BGF closed a GBP 20 million follow-on round for OCL Vision in March 2025 aimed at doubling theatre throughput. These infusions underpin record orders for modular microscopes and phaco machines configured for day-surgery turnovers of ≤15 minutes. The commercial momentum shortens payback periods for capital equipment, incentivising vendors to pitch subscription-style leases that bundle maintenance and consumables into predictable monthly fees.

Roll-out of High-Street OCT Services by Large Optical Chains

Specsavers, Vision Express and Boots collectively added more than 450 spectral-domain OCT scanners to their retail estates during 2024, taking the national total in community optometry to >2,100 units. Specsavers confirmed in January 2025 that OCT screening is now a standard, no-cost inclusion in all “Enhanced Eye Tests” across its 1,000 U.K. outlets, reducing referral time to secondary care by an average 12 days in pilot data from Devon and Cornwall. Boots Opticians reported that 38% of its OCT-detected abnormalities in 2024 were sight-threatening conditions requiring urgent hospital review, evidence used to negotiate new referral pathways with six Integrated Care Boards in 2025. For device manufacturers, optical-chain demand delivers volume stability outside the traditional hospital tender cycle and creates secondary revenue streams in cloud analytics and remote-reading licences. NHS England has signalled intent to formalise data-sharing protocols with accredited chains by Q4 2025, which could transform community OCT scans into reimbursable “diagnostic first touchpoints”.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of ophthalmologists limiting surgical throughput | −0.9% | United Kingdom | Short term (≤ 2 years) |

| Post-Brexit regulatory divergence increasing compliance costs | −0.8% | United Kingdom | Medium term (2-4 years) |

| Reimbursement caps on premium IOLs | −0.7% | United Kingdom | Medium term (2-4 years) |

| High device re-processing standards raising cost of ownership | −0.6% | United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Ophthalmologists Limiting Surgical Throughput

General Medical Council workforce statistics released in May 2025 reveal that the ophthalmology consultant vacancy rate sits at 9.4%, up from 8.7% in 2024 and comfortably above the 7% target threshold. RCOphth’s 2025 census concludes that 234 additional consultants are needed immediately to meet present demand, a figure projected to double by 2030 unless training numbers rise sharply. Workforce strain translates into theatre under-utilisation: GIRFT audit data show that 17% of cataract lists booked in 2024 were cancelled or cut short due to surgeon unavailability. Device utilisation rates therefore lag installed base growth, dampening replacement cycles and tugging down capital-equipment ROI for providers.

Post-Brexit Regulatory Divergence Increasing Compliance Costs

Effective 16 June 2025, the Medicines and Healthcare products Regulatory Agency (MHRA) introduced the UK Conformity Assessed (UKCA) plus Post-Market Surveillance Regulations, compelling manufacturers to maintain lifetime performance dashboards for every ophthalmic device sold domestically. The Association of British HealthTech Industries surveyed 61 eye-care suppliers in March 2025 and found average compliance costs have risen 14% since 2023, with small firms reporting increases of up to 28%. Parallel adherence to Europe’s Medical Device Regulation (MDR) remains mandatory for exporters, creating dual-testing burdens that delay launches by three-to-six months. Multinationals have absorbed the overhead via dedicated U.K. regulatory teams; however, two niche implant makers publicly announced withdrawal from the British market in late-2024 citing cost-benefit concerns. Higher barriers to entry limit competitive variety for NHS buyers and could nudge prices upward as smaller innovators exit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Dominance Meets Diagnostic Upswing

Vision Care Devices hold roughly 59.74% of United Kingdom Ophthalmic Devices market share in 2025 and continue to anchor recurring revenue with stable contact-lens sales. Diagnostic & Monitoring Devices, however, are set to outpace with an 8.46%CAGR, aided by NHS contracts that bundle analytics services at premium prices. Interoperable OCT platforms capable of sub-second scans shorten examination cycles, letting clinics process more patients without extra chair investment. The Computer-Assisted Retinal Analysis (CARA) system’s reported sensitivity above 80% for referable diabetic retinopathy exemplifies how clinical validation accelerates uptake. Suppliers retrofit legacy fundus cameras only when AI compatibility demands hardware parity, indicating a sustained refurbishment pipeline that dampens short-term unit sales but lifts aftermarket accessory revenue.

Suppliers integrating anterior-segment modules address both refractive and corneal surgery without increasing footprint, appealing to space-constrained urban theatres. Contact-lens innovation around oxygen-permeable materials sustains retail momentum but margin pressure from price competition keeps absolute revenue growth moderate. Diagnostic device vendors offset lump-sum capital expenditure concerns by offering leasing plans matched to NHS payment cycles. Such arrangements embed service contracts that expand high-margin software revenue, supporting longer product-development timelines. Data-driven monitoring functions also satisfy the MHRA’s heightened evidence requirements, creating a compliance moat around connected platforms.

By Disease Indication: Cataract Stability, Diabetic-Retinopathy Momentum

Cataract instruments command 34.78% of the 2025 United Kingdom Ophthalmic Devices market size, a position backed by Royal College of Ophthalmologists modelling that forecasts 50% more cataract surgeries by 2035. Predictable demand secures economies of scale for implant and phaco suppliers, while NHS outsourcing to private clinics maintains procedural volume even during public-hospital capacity squeezes. Diabetic-retinopathy systems record the fastest growth at 7.62%CAGR, powered by rising diabetes incidence and the nationwide OCT rollout. Trusts negotiate multi-year contracts aligning hardware depreciation with screening-cycle commitments, ensuring steady cash flows for imaging vendors.

Glaucoma management benefits from migration to minimally invasive devices such as the PRESERFLO MicroShunt, which surgeons adopt when guidelines advise earlier intervention. Age-related macular degeneration (AMD) workflows rely on higher-resolution imaging that supports timely anti-VEGF therapy decisions, driving upgrades in combined wide-field and OCT-angiography systems. Cross-indication platforms reduce procurement complexity, letting buyers serve AMD and diabetic patients with the same unit. Vendors positioned with such flexible systems shorten sales cycles and defend pricing, especially when capital budgets tighten.

By End-User: Hospitals Anchor Volume, ASCs Accelerate

Hospitals hold 40.05% share of United Kingdom Ophthalmic Devices market size in 2025 on the back of broad service scope and complex case management. Yet ASCs advance at 7.45%CAGR as day-surgery becomes default for routine ophthalmology. The Getting It Right First Time (GIRFT) “Day Case First” dataset shows 84% of procedures already completed same-day in England. Private providers exploit this efficiency to win NHS cataract outsourcing agreements, often bundling refractive-lens upgrades for self-pay patients. Their procurement dossiers emphasise portability and short turnover cycles, pushing manufacturers to design lighter microscopes and rapid-cycle sterilisation cassettes.

Specialist clinics leverage premium interiors and next-generation microscopes with digital overlays as marketing differentiators, repositioning equipment performance as part of patient experience. Public hospitals hedge capacity shortfalls by partnering with independent-sector treatment centres in hub-and-spoke models that share imaging devices. Vendors offering uniform after-sales support across both settings reinforce recurring-revenue bases through maintenance contracts that travel with the equipment, regardless of ownership.

Geography Analysis

England remains the primary volume driver thanks to its larger population and NHS England’s direct purchasing power. Framework contracts covering diabetic-retinopathy screening concentrate imaging demand, creating periodic spikes that ripple through the diagnostics supply chain. Scotland prioritises teleophthalmology to reach remote communities, expanding demand for portable imaging systems with satellite connectivity. Wales adopts outcome-based commissioning pilots that reward documented visual-acuity gains, pushing suppliers to integrate analytics dashboards. Northern Ireland’s smaller hospital network accelerates refurbishment cycles to maintain alignment with England’s equipment standards, ensuring cross-border clinician credentialing.

London’s teaching hospitals drive early adoption of AI-enhanced diagnostics, offering reference-site status in exchange for bundled training packages. Manchester and Birmingham trust clusters replicate these deployments, seeking to reduce outpatient backlogs from pandemic disruptions. Regional ASCs across the Midlands and the South-West attract private-equity backing, forming multi-site networks that standardise ophthal-microscope fleets from a single OEM. Suppliers meeting both devolved-nation governance and central-government cybersecurity standards find it easier to secure multi-region agreements. As digital governance frameworks equalise, procurement cycles are expected to align more closely across the devolved administrations, smoothing demand peaks and reducing logistical friction.

Competitive Landscape

The United Kingdom ophthalmic devices market shows moderate concentration. Alcon and Johnson & Johnson Vision Care leverage entrenched distributor networks to maintain dominant positions, while domestic player Rayner doubles intraocular-lens capacity to meet NHS sustainability procurement criteria. Carl Zeiss Meditec’s software ecosystem links OCT, field analysers, and surgical microscopes into a single data layer, letting surgeons view patient metrics across peri-operative touchpoints. STAAR Surgical hedges cataract dependence through an implantable collamer-lens portfolio aligned with rising refractive-surgery demand among younger demographics. Regeneron’s purchase of Oxular broadens its retinal drug-delivery platform, illustrating how pharmaceutical majors seek device synergies.

Private-equity influence shapes procurement decisions as sponsors standardise equipment across clinic networks to unlock volume discounts. Morgan Stanley Private Credit’s financing of Unifeye Vision Partners and Carlyle’s EUR 250 million commitment to Sanoptis typify consolidation strategies that aggregate purchasing power. Clinics under such ownership negotiate master agreements guaranteeing minimum purchase volumes, which compress unit margins but secure vendor share-of-wallet. Smaller specialist players retain influence in niche areas such as specialty contact lenses, proving that innovation can offset scale disadvantages when regulatory barriers are low.

Technological differentiation now pivots on integration rather than isolated performance metrics. Vendors that couple hardware with analytics and secure cloud gateways meet both clinical and regulatory imperatives under the MHRA’s lifetime-monitoring rule. Those lacking connected platforms often pursue partnerships or acquisitions to plug gaps, a trend expected to continue as compliance costs rise. Hospitals increasingly request evidence of cybersecurity certification in tender documents, effectively elevating the entry threshold for smaller device firms.

United Kingdom Ophthalmology Devices Industry Leaders

Alcon Inc.

Johnson & Johnson Vision Care

Carl Zeiss Meditec AG

Bausch + Lomb Corp.

CooperVision Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Morgan Stanley Private Credit arranged growth funding for Unifeye Vision Partners to support its partnership with Brooks Eye Associates, bolstering technological upgrades and liquidity for acquisitions.

- March 2025: BGF finalised a multi-million-pound investment in OCL Vision to scale theatre capacity and enhance digital marketing as private demand for eye surgery rises.

- March 2025: Carlyle committed EUR 250 million to Sanoptis, earmarked for bolt-on clinic acquisitions and broader surgical-technology access.

- January 2025: Regeneron completed the acquisition of Oxular and its Oxulumis delivery device, strengthening sustained retinal-therapy capabilities.

- June 2024: EssilorLuxottica acquired an 80% stake in Heidelberg Engineering, expanding its OCT portfolio and signalling a strategic pivot toward clinical diagnostics.

United Kingdom Ophthalmology Devices Market Report Scope

Ophthalmology devices are medical devices used in ophthalmology and optometry. These devices range from non-invasive devices and equipment frequently used for diagnostics to invasive ones such as contact lenses (and the care products that go with them) and implantable devices like intraocular lenses and glaucoma stents.

The United Kingdom Ophthalmology Devices Market is segmented by Devices (Surgical Devices (Glaucoma Drainage Devices, Glaucoma Stents and Implants, Intraocular Lenses, Lasers, and Other Surgical Devices), Diagnostic and Monitoring Devices (Autorefractors and Keratometers, Corneal Topography Systems, Ophthalmic Ultrasound Imaging Systems, Ophthalmoscopes, Optical Coherence Tomography Scanners, and Other Diagnostic and Monitoring Devices), and Vision Correction Devices(Spectacles and Contact Lenses)). The report offers value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current size of the United Kingdom Ophthalmic Devices market?

The United Kingdom Ophthalmic Devices market size stands at USD 2.31 billion in 2026.

How fast is the United Kingdom Ophthalmic Devices market expected to grow?

It is forecast to advance at a 6.18%CAGR, reaching USD 3.12 billion by 2031.

Which device segment is growing fastest within the market?

Diagnostic & Monitoring Devices show the highest momentum, with an 8.46%CAGR expected through 2031.

Why are ambulatory surgery centres important for market growth?

ASCs deliver most routine eye procedures as day cases and are expanding at a 7.45%CAGR, driving demand for portable, high-throughput equipment.

How will MHRA regulations affect device suppliers?

Stricter lifetime-performance monitoring raises compliance costs, favouring manufacturers that embed secure data-capture capabilities into their platforms.

Page last updated on: