United Kingdom MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

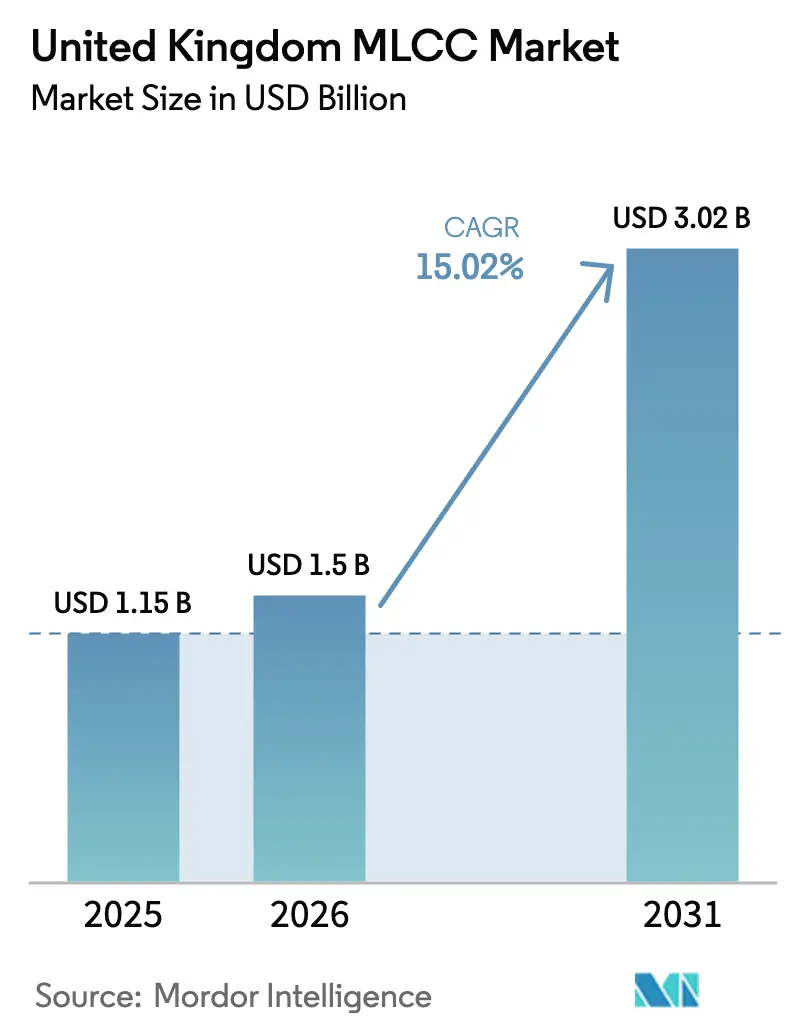

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 15.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom MLCC Market Analysis by Mordor Intelligence

The United Kingdom MLCC market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.50 billion in 2026 to reach USD 3.02 billion by 2031, at a CAGR of 15.02% during the forecast period (2026-2031). Solid policy support for zero-emission vehicles, favorable capital-allowance rules inside Freeport zones, and defense-electronics localisation under AUKUS together energize local demand. Tight global capacity, however, continues to lift average selling prices, nudging buyers toward dual-sourcing and buffer-stock strategies. Local distributors are responding by expanding bonded inventory close to automotive and medical hubs to limit allocation risk. At the same time, the pivot to 800-volt vehicle platforms, miniaturised medical implants, and high-frequency 5G radios is tilting the product mix toward high-voltage, ultra-stable, and ultra-small capacitors.

Key Report Takeaways

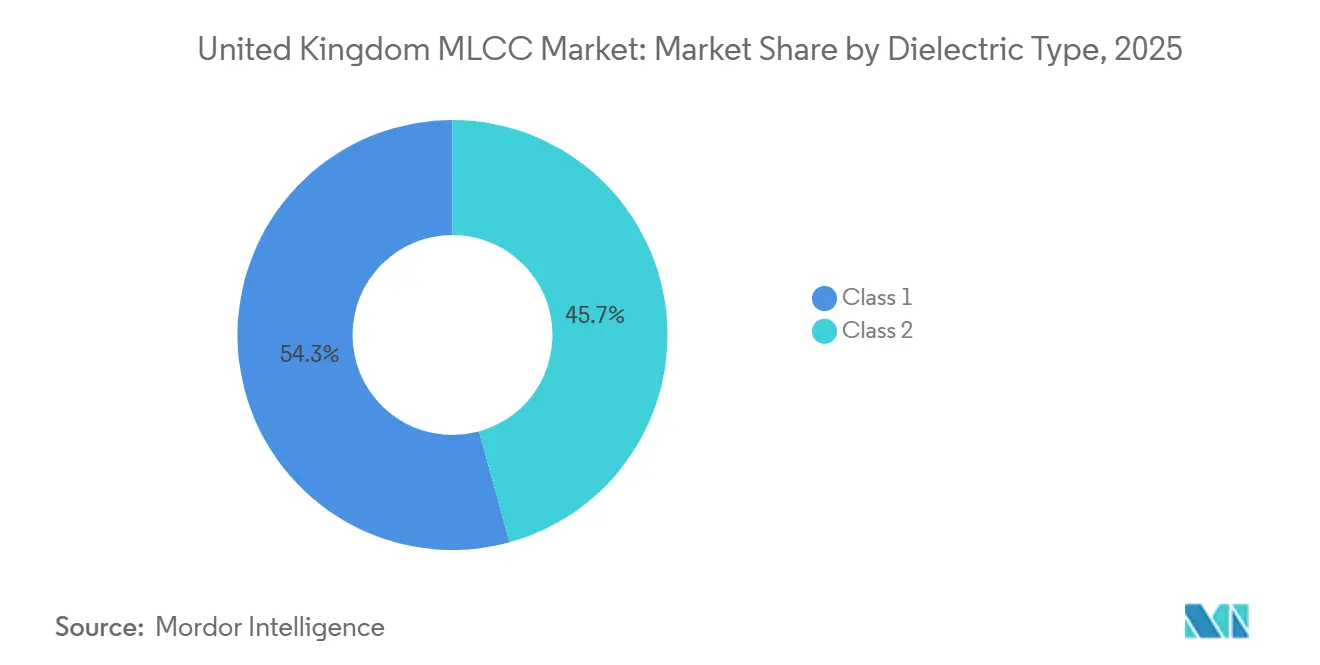

- By dielectric type, Class 2 grades commanded 45.72% of United Kingdom MLCC market share in 2025, while Class 1 grades are on track to post a 15.42% CAGR through 2031.

- By case size, the 402 format led with 37.29% revenue share in 2025; the 201 format is forecast to expand at a 15.83% CAGR to 2031.

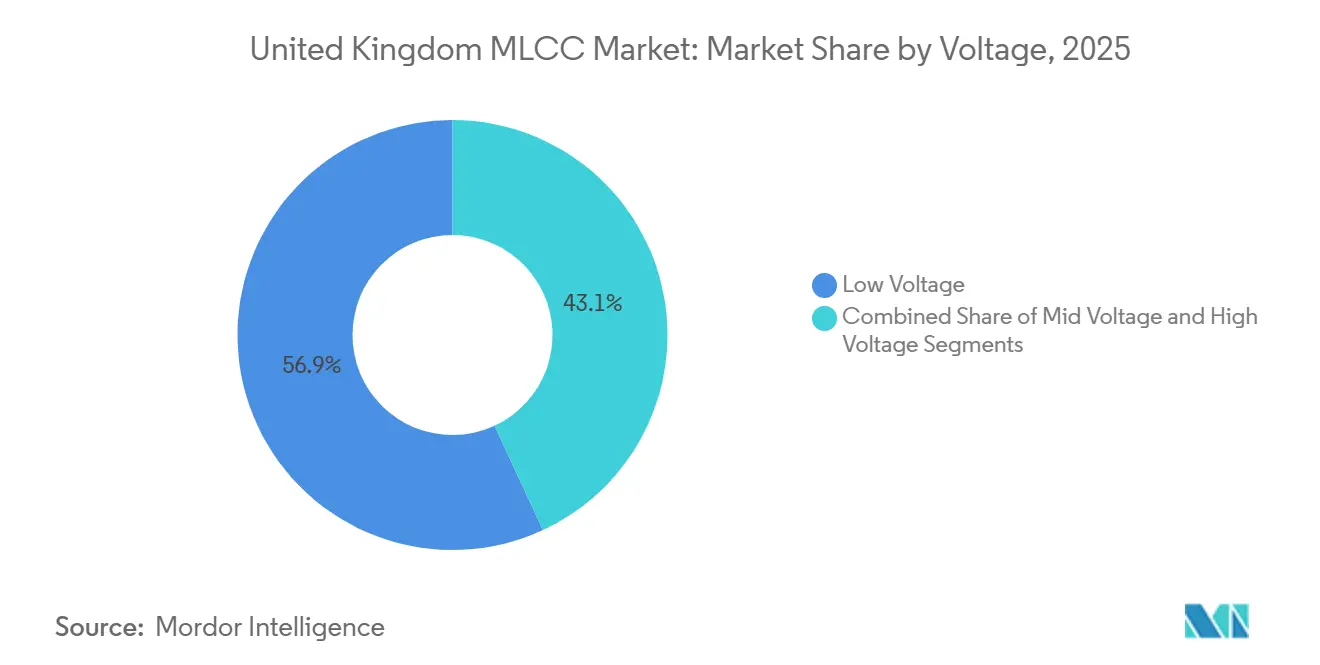

- By voltage rating, low-voltage parts accounted for 56.91% of 2025 revenue and high-voltage parts are advancing at a 15.64% CAGR through 2031.

- By mounting type, surface-mount technology held 63.81% of 2025 revenue while metal-cap radial leads are projected to grow at a 15.52% CAGR to 2031.

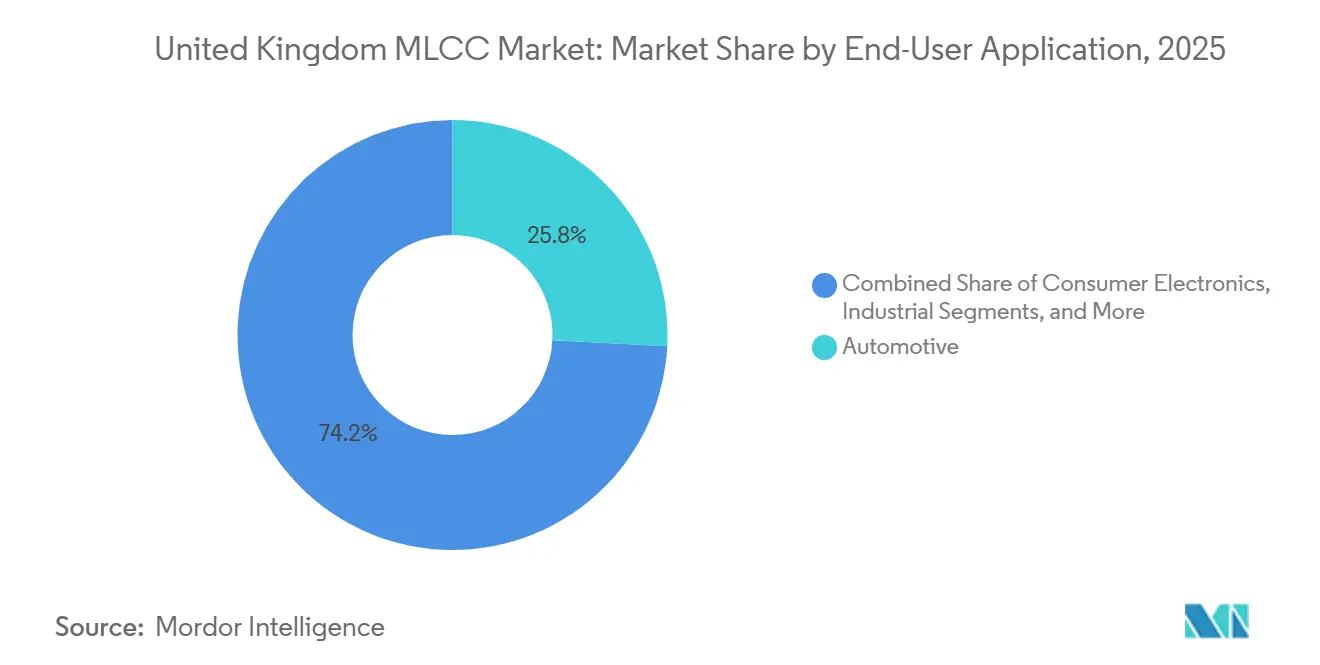

- By end-user, automotive applications captured 25.84% share in 2025 and medical devices represent the fastest-growing segment at a 16.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV manufacturing ahead of 2030 UK ICE-ban | +4.2% | West Midlands, North East, South East | Medium term (2-4 years) |

| Accelerated 5G infrastructure roll-out boosting small-cell demand | +2.8% | Greater London, Manchester, Birmingham | Short term (≤ 2 years) |

| Rising demand for compact medical wearables and implantables | +2.5% | Cambridge, Oxford, wider South East | Medium term (2-4 years) |

| Government tax incentives for on-shore passive-component production | +1.9% | Thames, Teesside, Humber, Liverpool, Plymouth Freeports | Long term (≥ 4 years) |

| Battery-management-system design shifts to higher capacitance | +1.6% | West Midlands, North East automotive clusters | Medium term (2-4 years) |

| Defence-electronics localisation under AUKUS and UK MoD initiatives | +1.4% | South West, Scotland, North East defense clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in EV Manufacturing Ahead of the 2030 UK ICE Ban

United Kingdom vehicle makers are scaling up electric-vehicle output to meet the 2030 ban on internal-combustion engines, lifting per-car capacitor content roughly threefold. Gigafactory investments by Tata in Somerset and AESC in Sunderland anchor local battery and power-electronics ecosystems, pulling qualification work into the United Kingdom MLCC market. The GBP 2.5 billion DRIVE35 program earmarks USD 2.6 billion for capital expenditure on power-electronics supply chains, signaling continued policy pull. Each electric vehicle contains about 10,000 capacitors, and design migration to 800-volt architectures further raises voltage-rating requirements. Local distributors now maintain bonded stock near West Midlands OEM sites to avoid Asian allocation shocks. These moves jointly amplify the growth outlook of the United Kingdom MLCC market.

Accelerated 5G Roll-Out Boosting Small-Cell Demand

Telecom operators are densifying 5G networks with thousands of small-cell base stations, each loaded with dozens of 0201 and 0402 capacitors for high-frequency bypass functions. Ofcom’s Connected Nations data confirms rapid urban coverage expansion in London, Manchester, and Birmingham.[1]Ofcom, “Connected Nations and infrastructure reports,” OFCOM.ORG.UK, ofcom.org.uk Murata’s capacitor revenue rose 9% year on year in the first half of fiscal 2025, driven partly by telecommunications orders. As power density climbs, designers prefer X7R and X5R dielectrics with stable capacitance under bias, and they favor suppliers with advanced material know-how. This telecom build-out therefore feeds an incremental tailwind into the United Kingdom MLCC market.

Rising Demand for Compact Medical Wearables and Implantables

National Health Service programs that fast-track innovative wearables intensify demand for ultra-small, high-reliability Class 1 capacitors. Regulatory changes effective June 2025 require lifecycle evidence and post-market surveillance for artificial-intelligence-enabled devices. Implantable cardiac monitors and continuous glucose sensors require zero-aging C0G parts with biocompatible terminations, prompting OEMs to source ISO 13485-certified products from Knowles’ Norwich plant. Domestic production shortens qualification cycles and satisfies traceability mandates. Consequently, medical electronics has become the fastest-growing opportunity in the United Kingdom MLCC market.

Government Tax Incentives for On-Shore Passive-Component Production

Freeport zones grant 100% first-year capital allowances on plant and machinery until September 2026, trimming the after-tax cost of new assembly lines. The Thames Freeport alone plans USD 5.9 billion of public-private spending across advanced manufacturing projects. Coupled with a GBP 27.8 billion National Wealth Fund, these incentives entice suppliers to localise screening, tape-and-reel, and failure-analysis capacity. OEMs gain shorter logistics pipelines, while the United Kingdom MLCC market benefits from higher domestic value capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent supply–demand imbalance inflating lead-times | -2.8% | Global, felt in UK procurement | Short term (≤ 2 years) |

| Nickel and copper price volatility | -1.7% | Global commodity markets | Short term (≤ 2 years) |

| Regulatory hurdles for new fabs | -1.2% | UK planning regimes | Long term (≥ 4 years) |

| Substitution by embedded capacitors in HDI PCBs | -0.9% | Global adoption hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

Artificial-intelligence server demand has pushed Murata’s global utilisation towards 95%, draining buffer inventory.[2]Murata Manufacturing, “Q2 Earnings Release Conference for FY2025,” MURATA.COM, corporate.murata.com Allocation risk forces UK buyers to accept longer contract horizons or pay premiums on the spot market. Automotive and defense programs that need traceable lots face the greatest exposure. Some tier-1s now dual-source with polymer hybrids or film capacitors, but re-qualification costs remain high, tempering substitution.

Nickel and Copper Price Volatility Squeezing Margins

Nickel inner-electrodes and copper terminations expose MLCC makers to commodity swings, with spot prices moving faster than customer price-adjustment clauses. Distributors must hedge inventory but still risk margin erosion when metal prices climb between quarterly resets. Cost pressure is accelerating interest in embedded-capacitor technologies for high-density PCBs, though adoption outside data-center boards remains limited.[3]TDK, “Thin-film Capacitors Designed for Integration in Circuit Boards,” TDK.COM, product.tdk.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Demand Lifts Long-Term Stability Requirements

Class 2 compositions held 45.72% of the United Kingdom MLCC market share in 2025, anchored by high-capacitance X7R and X5R grades. Their dominance comes from volumetric efficiency that suits decoupling and energy-storage tasks across consumer and industrial boards. However, Class 1 C0G and NP0 parts are projected to expand at a 15.42% CAGR through 2031 as automotive inverters, radar modules, and implantables prioritize near-zero aging and tight tolerance. The United Kingdom MLCC market for precision timing and sensing circuits is therefore tilting toward Class 1 technology.

Suppliers are widening high-voltage Class 1 offerings, such as TDK’s 10 nF, 1,250 V C0G in 3225 format. Automotive engineers value stable capacitance under bias for battery-management accuracy, while medical device makers need temperature-invariant behavior over decades. These attributes let Class 1 parts capture design wins even where their cost per microfarad is higher, reinforcing their forecast outperformance in the United Kingdom MLCC market.

By Case Size: Miniaturisation Accelerates Around the 201 Format

The 402 size accounted for 37.29% of the United Kingdom MLCC market share in 2025, reflecting its balance of pick-and-place yield and capacitance headroom. Yet board-area scarcity in 5G radios and glucose patches is driving a 15.83% CAGR for the 201 format. Designers can now achieve the same capacitance in fewer footprints due to breakthroughs such as TDK’s 1608 case capacitors with tenfold capacitance gains at 100 V.

As more logic shifts to chiplet packages, the passive placement area shrinks further, raising demand for smaller formats. The United Kingdom MLCC market size allocated to 201 and even 01005 footprints will likely rise fastest in medical wearables and telecom small cells. In contrast, power-electronics boards in vehicles still rely on 1210 or larger parts for ripple-current handling. This dual-track demand keeps a broad case-size portfolio essential for suppliers.

By Voltage: High-Voltage Parts Surging With 800-Volt EV Platforms

Low-voltage grades (less than or equal to 100 V) delivered 56.91% of 2025 revenue, but high-voltage grades (greater than 500 V) are forecast to log a 15.64% CAGR to 2031. The jump to 800-volt batteries trims cable weight and charging times yet pushes designers to specify capacitors rated above 1 kV for derating safety. The United Kingdom MLCC market share held by high-voltage parts will rise as new vehicle platforms adopt higher system voltages.

Suppliers flank the shift with products such as Knowles’ 6 kV, 0603 C0G range for electric drivetrains. Industrial inverters and renewable-energy converters also need greater than1 kV ratings, broadening the customer base. While thicker dielectrics lower the cost per component, they reduce series resistance and heat rise, improving the total cost of ownership for end users.

By MLCC Mounting Type: Metal-Cap Radial Leads Win in Harsh Zones

Surface-mount formats generated 63.81% of 2025 sales, underpinned by automated assembly in consumer devices. Nonetheless, metal-cap radial-lead MLCCs are set to grow at 15.52% CAGR because under-hood modules face high vibration and thermal cycling. Eaton’s hybrid-polymer alternates promote crack-resistant solutions, but many designers instead shift from 0805 SMT to metal-cap through-hole MLCCs for robustness.

Stacked metal-cap arrays further boost capacitance while absorbing board flex. As Freeport incentives lower domestic assembly costs, contract manufacturers can add radial-lead insertion lines, expanding local share of the United Kingdom MLCC market size dedicated to harsh-environment hardware.

By End-User Application: Medical Devices Emerge as the Fastest-Growing Niche

Automotive electronics accounted for 25.84% of revenue in 2025, but medical devices are projected to register a 16.11% CAGR through 2031. Post-market surveillance rules for artificial-intelligence-enabled diagnostic wearables sharpen reliability demands, steering buyers toward C0G parts with proven long-term drift performance.

Implantables such as neurostimulators and defibrillators require ISO 13485 traceability and biocompatible terminations, which are supplied by only a handful of vendors. As Norwich-based Knowles increases output, the United Kingdom MLCC market share captured by medical device OEMs will rise, helping diversify demand away from cyclical consumer electronics.

Geography Analysis

The West Midlands anchors power-electronics activity with the UK Battery Industrialisation Centre and multiple drive-train research labs. Local demand centers on high-voltage, AEC-Q200-qualified capacitors for traction inverters and on-board chargers. Proximity to these facilities encourages stocking distributors to keep Class 1 and Class 2 lines on hand for rapid design iterations, reinforcing the regional pull on the United Kingdom MLCC market.

The North East houses AESC’s Sunderland gigafactory and Nissan’s vehicle plant, generating sizable demand for mid-voltage capacitors used in battery-management systems. The Ministry of Defence’s acquisition of a gallium-arsenide foundry in Newton Aycliffe adds defense-electronics requirements, notably MIL-PRF-123 parts with lot-traceability tags. Freeport customs easements in Teesside further enhance the area’s attractiveness for final assembly and failure-analysis labs catering to the United Kingdom MLCC market.

Greater London and the South East lead telecom infrastructure rollout and medical-device research. Ofcom data show continued densification of 5G small cells, each requiring miniature high-frequency capacitors. The Thames Freeport’s 1,700-acre footprint offers bonded-warehouse benefits and 100% capital allowances, drawing electronics assemblers and shortening time to market for OEMs located in the Oxford-Cambridge Arc.

Competitive Landscape

Innovation and Customization Drive Future Success

Global heavyweights-Murata, TDK, Samsung Electro-Mechanics, Yageo, and TAIYO YUDEN-control most high-layer-count production and therefore dictate allocation terms for UK buyers. Murata’s 90-95% utilization and stated intention to rebuild inventory signal sustained tightness, giving suppliers pricing leverage. Samsung Electro-Mechanics booked USD 8.5 billion revenue in 2025, buoyed by AI-server MLCC demand, and approved a Philippine greenfield plant to secure future output.

TDK is deepening vertical integration through a planned ceramic-powder joint venture with Nippon Chemical Industrial, which should accelerate the introduction of new dielectrics. TAIYO YUDEN lifted capacity 10-15% in fiscal 2024 and opened the Tamamura building to pilot advanced stacking processes, underlining the industry-wide capacity race.

Domestic capability remains limited but is growing. Knowles’ Norwich factory offers AEC-Q200 lines plus FlexiCap terminations, giving UK customers a home-shore alternative for medical, aerospace, and harsh-environment parts. Allocation pressure has also opened space for polymer-hybrid or film-capacitor challengers in select power stages, though qualification inertia limits rapid displacement. The competitive mix therefore balances global oligopoly power with emerging domestic niche suppliers, shaping the evolution of the United Kingdom MLCC market.

United Kingdom MLCC Industry Leaders

Kyocera AVX Components Corporation

MARUWA Co., Ltd.

Murata Manufacturing Co., Ltd.

Nippon Chemi-Con Corporation

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electro-Mechanics announced 2025 Q4 business performance, underscoring double-digit multilayer ceramic capacitor revenue growth driven by AI-server and automotive segments.

- November 2025: TDK and Nippon Chemical Industrial signed a basic agreement to explore a joint venture aimed at accelerating ceramic-material development for next-generation MLCCs.

- September 2025: TDK introduced low-resistance soft-termination C0G MLCCs with 22 nF at 1,000 V in 3225 size, targeting high-voltage automotive modules.

- July 2025: The UK government launched the GBP 2.5 billion DRIVE35 program to spur zero-emission-vehicle supply chains, including power-electronics components.

United Kingdom MLCC Market Report Scope

The United Kingdom MLCC (Multilayer Ceramic Capacitor) Market refers to the market for multilayer ceramic capacitors within the United Kingdom. MLCCs are passive electronic components widely used in various applications due to their ability to store and regulate electrical energy.

The United Kingdom MLCC Market Report is Segmented by Dielectric Type (Class 1, Class 2), Case Size (201, 402, 603, 1005, 1210, Other Case Sizes), Voltage (Low Voltage, Mid Voltage, High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, Surface Mount), End-User Application (Aerospace and Defense, Automotive, Consumer Electronics, Industrial, Medical Devices, Power and Utilities, Telecommunication, Other End-User Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Class 1 |

| Class 2 |

| 0201 |

| 0402 |

| 0603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (Less Than or Equal to 100 V) |

| Mid Voltage (100-500 V) |

| High Voltage (Greater Than500 V) |

| Metal Cap |

| Radial Lead |

| Surface Mount |

| Aerospace and Defense |

| Automotive |

| Consumer Electronics |

| Industrial |

| Medical Devices |

| Power and Utilities |

| Telecommunication |

| Other End-User Applications |

| By Dielectric type | Class 1 |

| Class 2 | |

| By Case Size | 0201 |

| 0402 | |

| 0603 | |

| 1005 | |

| 1210 | |

| Other Case Sizes | |

| By Voltage | Low Voltage (Less Than or Equal to 100 V) |

| Mid Voltage (100-500 V) | |

| High Voltage (Greater Than500 V) | |

| By MLCC Mounting Type | Metal Cap |

| Radial Lead | |

| Surface Mount | |

| By End-User Application | Aerospace and Defense |

| Automotive | |

| Consumer Electronics | |

| Industrial | |

| Medical Devices | |

| Power and Utilities | |

| Telecommunication | |

| Other End-User Applications |

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform