UK Islamic Finance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.81 Billion |

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 9.42 Billion |

| Growth Rate (2026 - 2031) | 3.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Islamic Finance Market Analysis by Mordor Intelligence

The UK Islamic finance market size is expected to grow from USD 7.81 billion in 2025 to USD 8.06 billion in 2026 and is forecast to reach USD 9.42 billion by 2031 at 3.19% CAGR over 2026-2031. The growth profile shows a gradual shift from niche positioning toward mainstream acceptance as Shariah-compliant products gain traction among faith-based and ethical investors alike. Government tax reforms that removed double-levy issues in Islamic mortgages, together with the Bank of England’s Alternative Liquidity Facility, have lowered structural frictions and drawn new institutional capital. Steady demographic expansion of the UK Muslim population underpins deposit inflows, while the rise of digital-only platforms widens access beyond London’s traditional financial corridors. Momentum in green sukuk issuance further broadens the investor base as ESG mandates converge with Shariah requirements.

Key Report Takeaways

- By financial sector, Islamic banking held 64.82% of the UK Islamic finance market share in 2025, whereas sukuk is projected to register the fastest 4.66% CAGR through 2031.

- By customer type, the consumer segment accounted for 54.10% share of the UK Islamic finance market size in 2025 and is growing at a 3.86% CAGR to 2031.

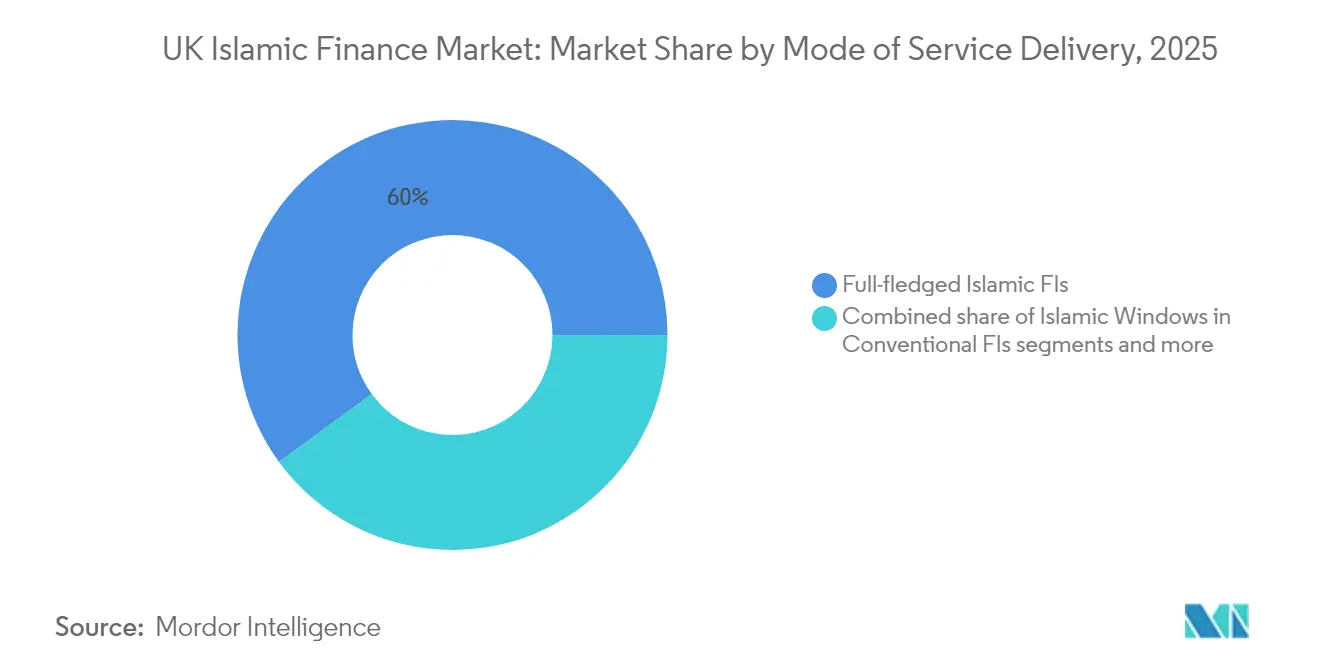

- By mode of service delivery, full-fledged Islamic financial institutions commanded 60.05% revenue share in 2025, while digital-only and fintech platforms are forecast to expand at 4.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Islamic Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government tax & regulatory parity measures | +0.8% | UK National | Medium term (2-4 years) |

| Rising domestic Muslim population & demand | +0.6% | UK National, concentrated in London, Birmingham, Manchester | Long term (≥ 4 years) |

| UK's role as Western Islamic-finance hub | +0.5% | Global, with the UK as the primary beneficiary | Long term (≥ 4 years) |

| Islamic fintech democratizing distribution | +0.7% | UK National, with international expansion potential | Short term (≤ 2 years) |

| ESG/green-sukuk pull in ethical investors | +0.4% | Global, with the UK as the key issuance center | Medium term (2-4 years) |

| CGT/ATED reforms unlocking home finance | +0.3% | UK National, particularly high-value property markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Tax & Regulatory Parity Measures

Tax neutrality provisions have eliminated the double taxation that previously placed Islamic mortgages at a pricing disadvantage compared with conventional equivalents[1]Norton Rose Fulbright, “Islamic Finance: Tax Developments Update 2025,” nortonrosefulbright.com. . The Bank of England’s Alternative Liquidity Facility supplies a Shariah-compliant instrument that satisfies high-quality liquid-asset (HQLA) rules, giving Islamic banks balance-sheet flexibility otherwise unavailable through interest-bearing gilts. These reforms collectively signal credible long-term policy support and attribute foreign issuers' value when selecting sukuk listing venues. The UK thereby cements its standing as the only Western jurisdiction offering a fully articulated regulatory framework for Shariah-compliant banking. Market participants consequently anticipate a steady pipeline of new product launches targeting retail and wholesale segments.

Islamic Fintech Democratizing Distribution

Fintech platforms remove geographic barriers by offering Shariah-compliant products via mobile channels, reaching consumers outside the main urban Muslim clusters. Wahed Invest’s halal workplace pension demonstrates how low-cost digital architecture can solve underserved pain points while meeting Shariah governance standards. Reduced operating overheads allow competitive pricing that appeals to non-Muslim ethical savers, widening the total addressable base for the UK Islamic finance market. Regulatory sandboxes administered by the Financial Conduct Authority (FCA) shorten product-development cycles and ensure early compliance feedback. The result is an ecosystem where agile entrants can scale quickly, pressuring incumbent banks to retool their digital propositions.

UK’s Role as Western Islamic-Finance Hub

London hosts more sukuk listings than any other non-Muslim majority jurisdiction, leveraging deep legal expertise and a tried-and-tested clearing infrastructure[2]LSEG, “London Stock Exchange Sukuk Listings 2025,” lseg.com.. English law’s adaptability enables complex Shariah structures to coexist with conventional contractual remedies, reducing cross-border enforcement risk for global issuers. Professional-services clusters, legal, accounting, and ratings, specialize in Islamic transactions, lowering execution costs through network effects. The city’s time-zone overlap with MENA and Asia provides execution advantages that alternative European centers struggle to replicate. Combined, these factors anchor the UK Islamic finance market as the preferred Western gateway for international capital seeking compliant structures.

ESG/Green-Sukuk Pulls in Ethical Investors

Sukuk principles already exclude alcohol, gambling, and conventional financial services, naturally aligning with ESG screens that bar exposure to harmful sectors[3]Fitch Ratings, “EMEA Islamic Banks Outlook 2025,” fitchratings.com.. The UK government’s sustainable-finance taxonomy further validates asset-backed structures favored in Islamic instruments, reinforcing investor confidence in environmental and social outcomes. Green sukuk deals executed in London enjoy oversubscription from both Islamic and conventional mandates, demonstrating crossover appeal. As institutional investors ramp up net-zero commitments, demand for compliant fixed-income alternatives escalates, providing new growth corridors for the UK Islamic finance market. Issuers benefit through access to a diversified funding base that carries reputational advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-scale balance sheets limit profitability | -0.4% | UK National, affecting smaller Islamic banks | Medium term (2-4 years) |

| Scarcity of Shariah-compliant HQLA tools | -0.3% | UK National, with global implications | Long term (≥ 4 years) |

| Fragmented Shariah standards & scholar pool | -0.2% | Global, affecting UK operations | Long term (≥ 4 years) |

| Legal-enforcement friction in DSOA mortgages | -0.1% | UK National, particularly in dispute resolution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sub-scale Balance Sheets Limit Profitability

Most dedicated Islamic banks in the UK operate with total assets below USD 5 billion, a level that constrains economies of scale relative to universal lenders. Thin capital bases raise the unit cost of regulatory compliance, especially under Basel III and Senior Managers regimes. HSBC’s exit from the UK Amanah proposition illustrates the difficulty of attaining sustainable returns when customer density remains low. Smaller institutions respond by focusing on specialist niches such as real-estate bridging finance, yet such concentration elevates portfolio risk. Without consolidation or fresh equity injections, profitability headwinds will restrict the growth runway for the UK Islamic finance market.

Scarcity of Shariah-Compliant HQLA Tools

Despite the Alternative Liquidity Facility, the aggregate supply of eligible sukuk and commodity-murabaha instruments falls short of demand, especially during stress events. Limited inventory raises bid-offer spreads and forces banks to maintain higher cash buffers, eroding margin potential. The mismatch grows acute as balance-sheet size increases, discouraging aggressive expansion. Development of UK sovereign sukuk would alleviate strain, but issuance cadence remains unpredictable. Until depth improves, treasury constraints temper growth prospects for Islamic banks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Financial Sector: Banking Dominance Faces Sukuk Disruption

Islamic banking represented 64.82% of 2025 revenue, anchoring the UK Islamic finance market through deposit mobilization and retail financing. However, sukuk’s 4.66% CAGR illustrates an investor pivot toward fixed-income assets structured under Shariah rules, leveraging the London Stock Exchange’s efficient listing processes. The UK Islamic finance market size for sukuk is projected to widen as issuers such as Al Rajhi Bank and Khazanah Nasional tap London for benchmark deals. Liquidity benefits also spill back to banks that hold sukuk as secondary reserves, reinforcing a virtuous capital-market loop.

Although banking retains critical mass, fee income from capital markets advisory and custody of sukuk lifts non-interest revenue proportions, Takaful remains embryonic but gains traction from real-estate and motor policies, a shift encouraged by regulators clarifying solvency-margin calculations for Shariah-compliant insurers. Specialized players such as Cobalt Underwriting illustrate how niche focus can complement full-service banking, deepening ecosystem maturity. As sukuk depth expands, pricing transparency enhances market efficiency and raises competitive pressure on banks to streamline cost bases.

By Customer Type: Consumer Segment Drives Market Evolution

Retail clients supplied 54.10% of 2025 assets, reflecting demographic growth and successful product innovation in pensions and ethical savings. The UK Islamic finance market share commanded by consumers is expected to edge higher as price parity in mortgages and digital onboarding reduces friction. Fintech interfaces allow micro-investment products that appeal to Gen-Z Muslims, a cohort previously underserved due to minimum-balance thresholds.

Institutional customers still dominate large syndicated sukuk and real-estate project financings, providing scale that underwrites market credibility. Yet the faster 3.86% CAGR in retail assets indicates a redistribution of growth drivers. Corporate treasurers also experiment with Islamic payables-financing tools, but these remain pilot programs. Overall, consumer deepening underpins a steady broadening of the UK Islamic finance market size while diversifying risk away from chunky wholesale exposures.

By Mode of Service Delivery: Digital Transformation Accelerates

Traditional Islamic banks held 60.05% of transactions routed through branch or call-center channels in 2025, but the digital-only cohort is on track for a 4.78% CAGR, outpacing sector averages. Lower operating expenditure enables fintech players to waive account fees and offer competitive rates funded by leaner cost-income ratios. The UK Islamic finance market size attributable to online channels will therefore expand faster than the legacy footprint.

Conventional banks operating Islamic windows face strategic decisions after HSBC’s retreat, weighing compliance complexity against incremental revenue. Meanwhile, peer-to-peer platforms bring asset-specific structures such as commodity-murabaha micro-loans to geographically dispersed borrowers, broadening inclusion. FCA sandbox participation fosters experimentation without compromising consumer protection. As APIs integrate open-banking data, user experience gains further traction, reinforcing the upward trajectory of digital distribution inside the UK Islamic finance market.

Geography Analysis

London anchors most of the Islamic finance activity by virtue of its financial-services density and the London Stock Exchange’s sukuk capabilities, driving transaction volume that cements the UK Islamic finance market as Europe’s core Shariah hub. Muslim population concentrations in Greater London, Birmingham, and Manchester generate natural retail demand, while corporate headquarters in the City seek compliant treasury options.

Regional spillover is increasingly visible. Digital platforms extend reach to Scotland and Northern Ireland, geographies historically underpenetrated due to sparse branch networks. Fintech uptake among millennials accelerates retail asset growth outside metropolitan hubs, diversifying the geographic contribution to the UK Islamic finance market size. Government policy, including devolved enterprise funding, supports regional Islamic SMEs, linking faith-compliant finance to broader leveling-up agendas.

Internationally, London’s time zone straddles between Asia and the United States, positions it for lead-manager mandates on global sukuk programs. While Dubai and Kuala Lumpur offer alternative venues, issuers still favor English law for high-value cross-border projects. Consequently, spill-in flows mitigate Brexit-related trade frictions, keeping foreign-currency sukuk issuance buoyant in the UK Islamic finance market.

Regulatory Landscape

Islamic finance in the United Kingdom operates under a secular, activity-based framework. Shariah-compliant providers are regulated on the same basis as conventional institutions under the long-standing policy stance of “no obstacles, but no special favours.” Conduct supervision sits with the Financial Conduct Authority (FCA), while prudential oversight is led by the Prudential Regulation Authority (PRA), so Islamic banks, windows, and investment firms must meet the same authorization, capital, consumer-protection, and financial-crime standards as their peers.

A key UK-specific enabler is the Bank of England's Alternative Liquidity Facility (ALF), which supports Shariah-compliant liquidity management. It enables eligible Islamic banks to meet prudential liquidity requirements without relying on interest-bearing instruments. On the legislative and tax side, the UK has used the “alternative finance” framework to reduce structural frictions, including recognition and treatment of Alternative Finance Investment Bonds (AFIBs) such as sukuk, supported by changes made under the Finance Act 2018. More recently, Finance Bill amendments (2024-2025) targeted tax issues around using alternative finance to raise capital on existing assets, reinforcing parity for Shariah-compliant structures used in banking and capital markets.

Value Chain Analysis

The UK Islamic finance value chain begins with product structuring and governance (Shariah boards, Shariah review and audit, and legal documentation under English law). It then moves into origination by full-fledged Islamic banks, Islamic windows of conventional banks, and fintech platforms that distribute savings, home finance, business finance, and investment products. Funding and risk intermediation draw on deposit mobilization, wholesale funding, and capital-markets issuance, with the London Stock Exchange functioning as a key venue for sukuk listings and associated services such as listing, custody, clearing, and investor access.

Professional services (law firms, accountants, and advisors) and specialist assurance providers for Shariah compliance act as core enablers. The chain also depends on valuation, servicing, and asset-management infrastructure, particularly for property-backed UK portfolios. Liquidity and balance-sheet management remains a bottleneck node, with Shariah-compliant HQLA scarcity increasing reliance on tools such as the Bank of England's ALF and elevating the role of secondary-market sukuk. Distribution is increasingly multi-channel, with digital onboarding and partnerships linking customer acquisition to regulated balance sheets, while tax-parity changes under the UK alternative finance framework reduce execution friction across mortgages, funds, and sukuk structures.

Competitive Landscape

Market rivalry is moderate. Al Rayan Bank leads retail deposits, leveraging scale in home finance and savings. Gatehouse Bank carves a profitable niche in real-estate bridging and build-to-rent developments, exploiting risk appetite differences that deter universal bankers. BLME Holdings maintains focus on wealth management, serving high-net-worth clients through tailored leasing structures.

Fintech entrants inject competitive verve. Wahed Invest targets millennial savers with fractional-share ETFs, while Nomo Bank, powered by BLME, provides cross-border digital banking for GCC clients. These challengers deploy cloud-native cores, achieving sub-40% cost-income ratios that traditional banks struggle to match. Incumbents respond by digitizing legacy workflows and partnering with reg-tech firms to automate Shariah screening.

Consolidation talk resurfaces periodically, propelled by sub-scale balance-sheet economics. Yet divergent shareholder missions and varied Shariah-governance practices complicate mergers. Strategic collaborations, such as Islamic fintechs white-labeling back-office services from established banks, offer an interim solution. FCA oversight preserves competitive parity, discouraging rent-seeking behavior while allowing product differentiation inside the UK Islamic finance market.

UK Islamic Finance Industry Leaders

Gatehouse Bank

Al Rayan Bank

QIB UK

BLME

HSBC Amanah UK

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

For the UK Islamic finance market, a clear opportunity sits in expanding the supply and usability of Shariah-compliant liquid assets and sterling-based instruments for UK-regulated balance sheets. The Bank of England's Alternative Liquidity Facility addresses part of the constraint, but it does not remove it. Policy signaling on sovereign issuance also remains relevant to this opportunity set: in 2026, Chief Secretary to HM Treasury Lucy Rigby publicly stated that discussions on a potential third UK sovereign sukuk had reached an advanced stage, tying directly to needs around benchmarks, liquidity tools, and international positioning.

On the asset-management and alternative-investment side, the opportunity set is broadened through new regulated vehicles and specialist funding structures that add product variety beyond core retail banking. In 2026, Channel Capital Advisors LLP announced a first close for the Corniche Sharia fund as an FCA-regulated alternative investment fund. In parallel, Offa completed a GBP-denominated working-capital raise using a sukuk and warrant structure listed on The International Stock Exchange (Guernsey). Together, these moves support a wider pipeline for Shariah-compliant funds and private-market exposures, and they complement ongoing tax-parity work in alternative finance, including 2024-2025 Finance Bill changes, that reduces structural frictions in raising capital using Shariah-compliant structures.

Recent Industry Developments

- July 2026: Offa completed a GBP 6.5 million working capital raise using a sukuk and warrant structure listed on The International Stock Exchange (Guernsey). The transaction broadened funding routes for UK-focused Shariah-compliant specialist lenders and demonstrated the use of capital-markets style structures to support non-bank balance sheets.

- May 2026: Gatehouse Bank increased finance-to-income ratios across its Home Purchase Plan products, allowing residential property finance up to six times gross income for customers in England and Wales. The change expanded addressable demand in Shariah-compliant home finance and intensified competitive pressure on product design and affordability metrics across Islamic retail offerings.

- May 2025: Masraf Al Rayan (Al Rayan Bank) announced the issuance of a USD 500 million, 5-year senior unsecured Reg S sukuk. The deal reinforced sukuk market depth and provides a reference point for UK-linked Islamic finance activity connected to international balance sheets and London capital-markets intermediation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this study, the UK Islamic finance market is defined as the value of Sharia-compliant financial products and services provided in the United Kingdom across banking, capital markets, and related Islamic financial activities, counted where the underlying contract structure is Sharia-aligned and revenue-bearing.

Scope exclusions: Purely conventional financial products, informal community lending, and non-UK booked Islamic assets that are only marketed in the UK are excluded.

Segmentation Overview

- By Financial Sector

- Islamic Banking

- Islamic Insurance (Takaful)

- Islamic Bonds (Sukuk)

- Islamic Funds

- Other Islamic Financial Institutions (OIFLs)

- By Customer Type

- Business

- Consumer

- By Mode of Service Delivery

- Full-fledged Islamic FIs

- Islamic Windows in Conventional FIs

- Digital-only / FinTech Platforms

- Alternative Platforms (Crowdfunding, P2P)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the UK market boundary using public, non-paywalled sources such as Bank of England statistical releases, UK government publications from HM Treasury and the Office for National Statistics, and FCA policy and market updates. We also used reference materials from trade bodies and exchanges, such as London Stock Exchange content on sukuk listings, and industry association briefs that describe product structures in plain terms.

To turn these inputs into a workable model, we reviewed annual reports, regulatory disclosures, investor presentations, and reputable press coverage to capture shifts in product launches and balance sheet trends. Paid subscriptions were used only where they add structure, mainly for company financials and intelligence, news and financials, and selective patent database checks to spot product innovation themes. The sources listed here are illustrative, and many other public documents were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with market participants across Islamic banking, sukuk and fund structuring, takaful-related activity, and distribution partners, so assumptions could be tested against how products are actually booked and priced in the UK. We also spoke with advisors and industry observers to triangulate demand drivers, the pace of new issuance, and how Islamic windows are counted versus fully Islamic institutions, which helped us close gaps left by public reporting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 57% |

Market-Sizing & Forecasting

Sizing used a top-down and bottom-up approach, where UK-level demand pools and regulated financial activity were reconstructed first, then cross-checked using selective roll-ups to keep the totals realistic. The top-down build anchored on UK Islamic finance signals that can be tracked over time, such as Islamic banking asset growth and product penetration, sukuk listing and issuance activity tied to London, and the pace of Sharia-compliant investment product launches.

Those macro signals were then corroborated with bottom-up approximations using sampled pricing and volume logic, including typical fee and margin ranges, product mix splits across banking, sukuk, funds, and takaful-linked activity, and observed balance sheet and AUM movements from public disclosures. When company reporting was incomplete, gaps were handled through peer benchmarking within the same product type and by applying conservative ranges that were validated in primary discussions.

Forecasting relied on scenario analysis supported by trend consistency in the key drivers, mainly expected demand from retail and institutional customers, the pipeline for sukuk and Sharia-compliant funding, and interest rate and inflation conditions that influence financing volumes and spreads. Assumptions were reviewed with practitioners so the forward view stays tied to what is feasible in product rollout and underwriting capacity.

Data Validation & Update Cycle

Outputs were validated by triangulating the model against independent signals, then checking for year-to-year jumps that do not match known regulatory or market events. If a variance looked large, analysts re-checked the input series, revisited conversion and timing assumptions, and re-contacted selected respondents to confirm whether the change came from scope, booking location, or a genuine activity shift.

Before sign-off, the work goes through a multi-step internal review where logic, math, and market consistency are tested by another analyst. The report is refreshed annually, and interim updates are made when material events occur that can shift issuance, product availability, or demand. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's UK Islamic Finance Market Size Compared Against Other Published Estimates

Published numbers for UK Islamic finance often do not match because the market can be measured as annual activity and revenues, or as total assets and balances, and the two do not move in the same way each year. Differences also come from whether a source counts only fully Islamic institutions or includes Islamic windows and digitally delivered products.

Evidence such as reported UK Islamic finance asset figures, sukuk listing and issuance signals linked to London, and year-on-year movements visible in financial disclosures are the checks that keep Mordor Intelligence's estimate aligned to the value-based market boundary used in this report, rather than a broader assets-outstanding tally.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.81 B (2025) | |

| Industry Report A | USD 7.50 B (2024) | Uses a different base year and is presented as a broad sector estimate, with limited clarity on whether Islamic windows, funds, and fee-based services are consistently included in the measured value. |

| Global Finance Index B | USD 42.60 B (2023) | Tracks Islamic finance assets in the UK, which is a stock measure that can include balances and holdings not equivalent to annual market value, so it naturally sits higher than a value-based sizing approach. |

The table shows that the spread is mainly explained by what is being measured (value generated in a year versus assets outstanding), plus base year timing. By keeping the scope tied to clearly defined Sharia-compliant activity booked in the UK and then validating assumptions through public signals and primary checks, the final number stays transparent and repeatable.

Key Questions Answered in the Report

How large is the UK Islamic finance market in 2026?

The UK Islamic finance market size is USD 8.06 billion in 2026, projected to reach USD 9.42 billion by 2031.

Which segment is expanding fastest within the sector?

Sukuk issuance is growing at a 4.66% CAGR to 2031, outperforming banking, takaful, and funds.

What drives consumer uptake of Islamic mortgages?

Removal of double-tax costs, digital onboarding, and competitive pricing have boosted retail demand.

How important are fintech platforms to future growth?

Digital-only providers are forecast to grow at a 4.78% CAGR, making them pivotal to distribution expansion.

Why is London favored for international sukuk listings?

London combines a flexible legal framework, deep professional services expertise, and favorable time-zone coverage, all underpinned by supportive regulation.

What is the outlook for Islamic banks’ profitability?

Profitability hinges on scaling balance sheets, expanding HQLA supply, and digitizing operations to cut cost-income ratios.

Page last updated on: