United Kingdom Cyber Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

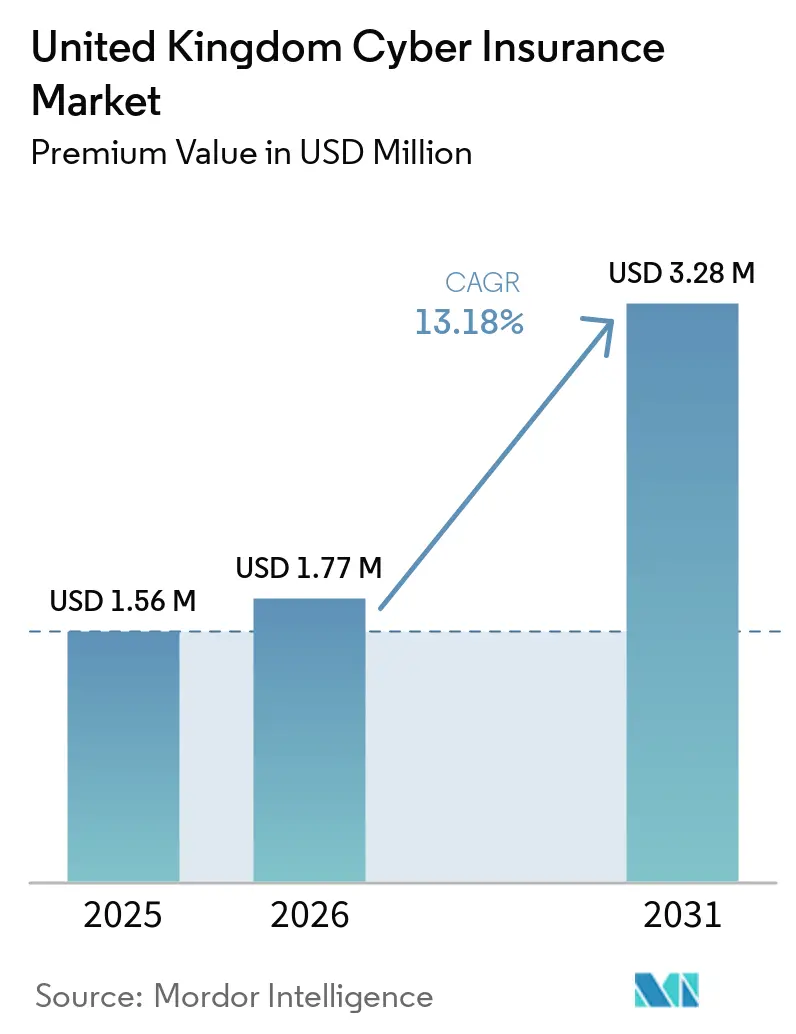

| Base Year Market Size (2025) | USD 1.56 Million |

| Market Size (2026) | USD 1.77 Million |

| Market Size (2031) | USD 3.28 Million |

| Growth Rate (2026 - 2031) | 13.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Cyber Insurance Market Analysis by Mordor Intelligence

The United Kingdom Cyber Insurance Market size in terms of premium value is projected to be USD 1.56 million in 2025, USD 1.77 million in 2026, and reach USD 3.28 million by 2031, growing at a CAGR of 13.18% from 2026 to 2031.

Heightened ransomware activity, intensifying regulatory enforcement, and expanding third-party and cloud dependencies are shaping the next growth leg of the UK cyber insurance market. Premium rates fell across 2025 despite rising incidents, which raised questions about sustainability if loss trends from recent underwriting years remain elevated. Large-scale attacks on critical buyer segments and supply chains have driven more boards to extend limits and tighten incident response oversight. Government-backed schemes and NHS procurement standards continue to harden baseline security expectations, especially for SMEs and mid-market suppliers embedded in essential services. Consolidation among specialty carriers could compress pricing competition in select segments, while alternative risk transfer and broker-facilitated capacity keep overall coverage options broad in the UK cyber insurance market.

Key Report Takeaways

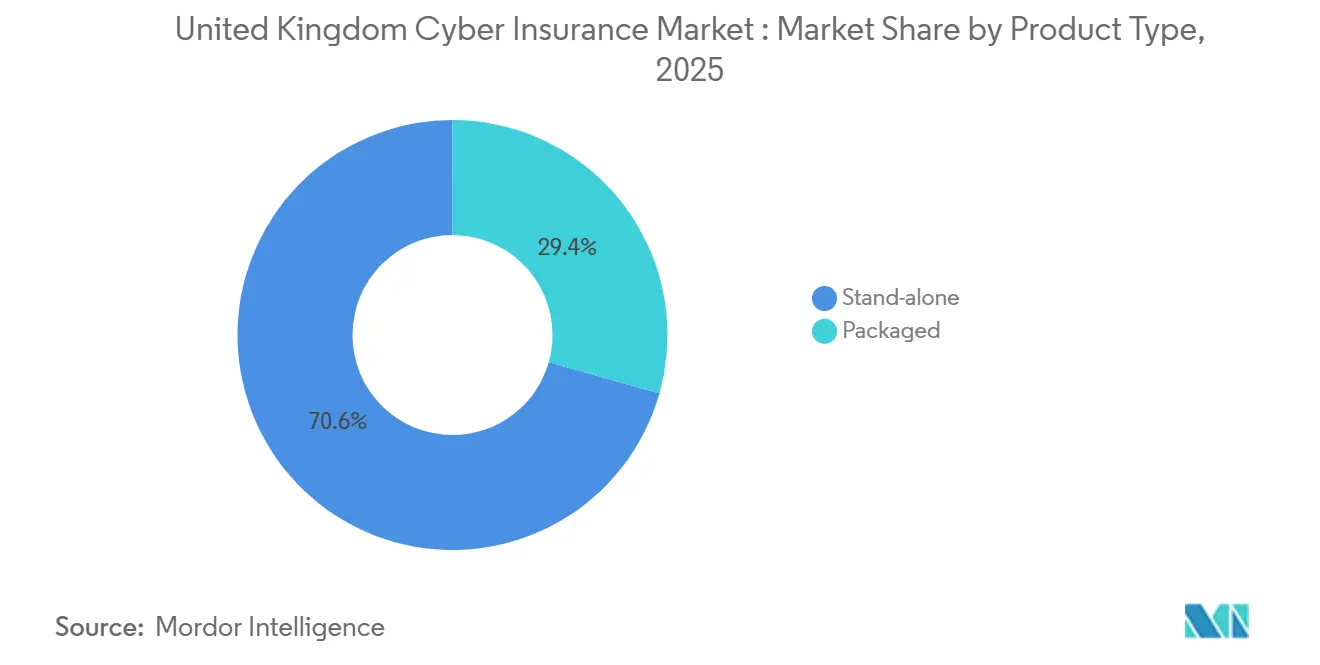

- By product type, stand‑alone policies accounted for 70.62% of the market revenue of the UK cyber insurance market in 2025, while the same segment is projected to grow at a 12.92% CAGR through 2031.

- By enterprise size, large enterprises held 43.56% of the total revenue of the UK cyber insurance market in 2025, while small and micro enterprises are expected to expand at a 13.34% CAGR through 2031.

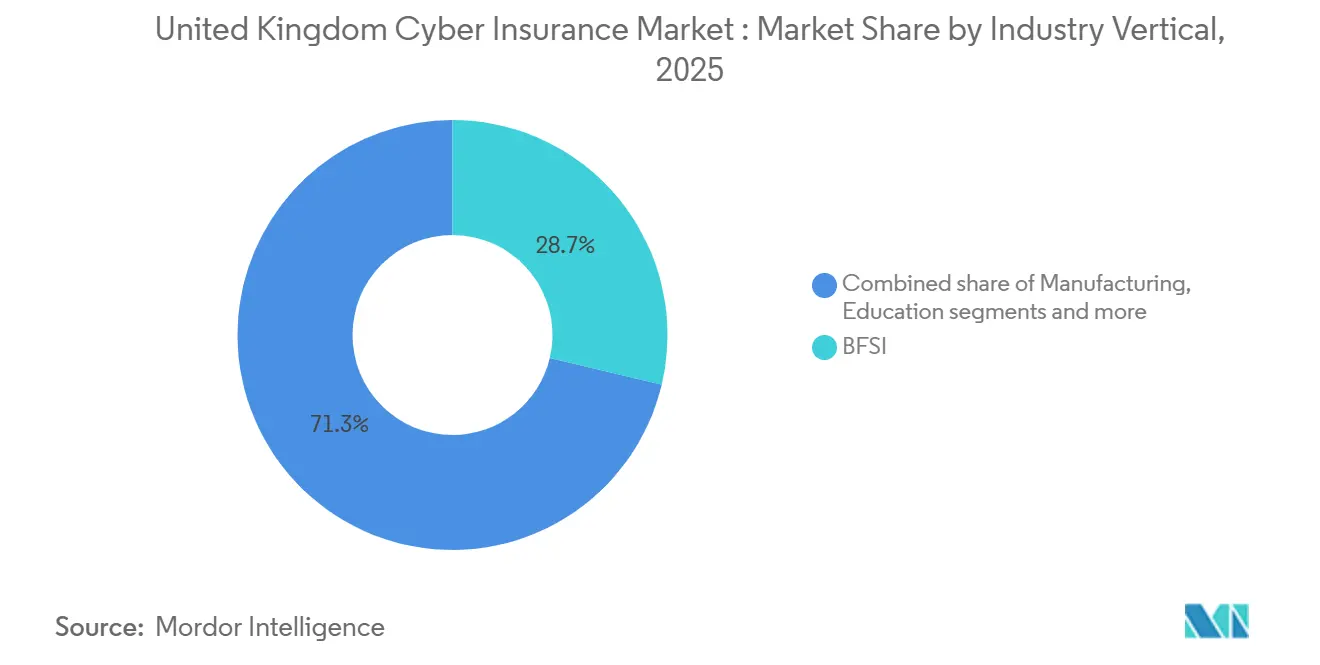

- By industry vertical, BFSI represented 28.71% of the segment value of the UK cyber insurance market in 2025, while healthcare and life sciences are forecast to record a 12.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Cyber Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating ransomware frequency & severity | +2.3% | National, concentrated in manufacturing hubs and retail corridors | Short term (≤ 2 years) |

| Mandatory GDPR & ICO breach-notification fines | +1.9% | National, heightened in data-intensive sectors (BFSI, healthcare) | Medium term (2-4 years) |

| Post-COVID remote-work attack-surface expansion | +1.4% | National, acute in London, Manchester, Edinburgh hybrid workforces | Short term (≤ 2 years) |

| SME-focused digital broker platforms (embedded cyber) | +1.7% | National, early gains in Midlands, North West SME clusters | Medium term (2-4 years) |

| UK government Cyber Essentials scheme uptake | +1.1% | National, enforcement concentration via NHS, CNI procurement | Long term (≥ 4 years) |

| NHS & CNI zero-trust procurement mandates | +1.6% | National, NHS trusts, energy, transport, water critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Ransomware Frequency & Severity: Median Payouts Stabilize While Volume Surges

Ransomware victimization affecting UK businesses doubled from under 0.5% of organizations in 2024 to 1.0% in 2025, or an estimated 19,000 affected organizations, which elevated the urgency of risk transfer throughout the UK cyber insurance market [1]UK Government, “Cyber Security Breaches Survey 2025,” GOV.UK, gov.uk . Although global ransom demand values declined in 2024, UK median payouts remained significant at USD 82,000 in the most recent reporting, and helped keep ransomware as the dominant share of insurer payouts relative to notifications. UK businesses encountered an extreme attack tempo during 2025, exceeding 2,000 daily cyberattacks for much of the year, which further tested preparedness and insurance limits across the UK cyber insurance market [2]Beaming, “2025 Cyber Threat Report | 2026 Security Priorities,” Beaming, beaming.co.uk . Major retail incidents such as the Marks & Spencer outage in April 2025 demonstrated the revenue and operational impact during sustained disruptions, with multiday losses surpassing GBP 1 million per day, or USD 1.27 million using the 2025 average rate, over several weeks. Government policy development in 2025 signaled potential restrictions on public-sector ransom payments and a possible pre-payment notification regime for private entities, changes that would alter incident response decision sets and insurer advisory practices.

Mandatory GDPR & ICO Breach-Notification Fines: Average Penalties Surge Tenfold in Single Year

In 2025, the ICO ramped up its enforcement activities, doling out penalties that were markedly heftier than those of the prior year. This shift underscores a pronounced pivot towards stringent actions against significant data-protection breaches. A defining moment in this trend was the landmark case against Capita. Here, the ICO levied an unprecedented fine after uncovering delays in addressing a cyberattack from 2023. Further solidifying its tough stance, the ICO penalized Advanced Computer Software Group. Their security oversights, linked to a ransomware attack that hampered healthcare services, were scrutinized. The ICO pointed out deficiencies in multi-factor authentication (MFA) and software patching. In a separate notable case, 23andMe faced penalties after a credential-stuffing breach unveiled sensitive genetic information. The ICO's investigation spotlighted the company's lackluster authentication and monitoring measures. These heightened enforcement actions came amidst a backdrop of increasing regulatory intricacies, influenced by frameworks like NIS2, DORA, and the evolving landscape of UK data-protection regulations. Such complexities have amplified the demand for cyber-insurance, particularly policies that cater to regulatory probes, breach alerts, and remediation for affected data subjects.

Post-COVID Remote-Work Attack-Surface Expansion: Phishing Searches Hit Twenty-Year Peak

Distributed work practices have enlarged the identity and device attack surface, with nearly one-third of UK organizations reporting at least one incident linked to remote or hybrid arrangements into early 2026. Phishing drove a large majority of cyber breaches across the UK private and charity sectors in 2025, which intensified the need for layered identity controls and email security among insureds in the UK cyber insurance market. Public search interest for phishing reached a two-decade high by late 2025, which aligned with field evidence on social engineering that targeted cloud identities across productivity suites and collaboration tools. Losses to deepfake-driven investment scams in the first half of 2025 approached GBP 100 million, or USD 127 million, which expanded the perimeter of fraud risks considered in insurance placements. Training and MFA gaps persisted in smaller companies during 2025, and those control deficits frequently correlated with higher incident rates and adverse underwriting terms.

NHS & CNI Zero-Trust Procurement Mandates: Supply-Chain Charter Engagement Expands from November 2025

NHS England’s Cyber Security Supply Chain Charter advanced from principles to active supplier engagement by January 2026, which tightened the baseline for patching, monitoring, MFA, and incident reporting in healthcare supply chains within the UK cyber insurance market. The Charter calls for 24/7 monitoring, immutable backups, tested recovery, and board-level exercises that align with zero-trust practices and reduce long-tail incident costs. NHS procurement frameworks require Cyber Essentials or ISO 27001 certification, and cloud and software suppliers must also align with NCSC Cloud Security Principles. Recent NHS-affecting incidents highlighted the direct operational cost of cyber disruptions and reinforced momentum for stronger control baselines. The Cyber Security and Resilience Bill in 2026 aims to expand the regulated scope to managed service providers, large data centers, and critical suppliers, which will increase minimum standards and incident reporting discipline for a significant portion of the UK digital economy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium inflation & coverage sub-limits | -1.8% | National, pricing pressure from Lloyd's syndicates and London market | Short term (≤ 2 years) |

| Limited actuarial loss history for UK market | -0.9% | National, data deficits hinder SME underwriting and tertiary-sector pricing | Long term (≥ 4 years) |

| War-exclusion & systemic-risk uncertainty | -1.3% | National, Lloyd's LMA5381 mandate amplifies London market impact | Long term (≥ 4 years) |

| Reinsurance capacity tightening (post MOVEit supply-chain attacks) | -1.2% | National, capacity flows from Bermuda and continental European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Inflation & Coverage Sub-Limits: Rates Approach "Lower End of Sustainability"

Premiums declined 11% across 2025 even as incident counts rose, which broker analyses described as nearing the lower end of sustainable pricing in the UK cyber insurance market[3]Lockton, “Cyber Insurance Market Update: Rates Decline Despite Rising Claims,” Lockton, lockton.com . Q4 2025 registered a further 12% fall in primary-layer rates, supported by abundant capacity and new entrants, although such conditions may normalize if loss emergence persists. Buyers expanded limits through 2025 in response to high-profile outages, yet coverage structures often retained sub-limits on ransomware, contingent business interruption, and regulatory penalties. Lloyd’s mandated clearer exclusions for state-backed attacks beginning in 2023, which introduced attribution uncertainties that may restrict recoveries for large-scale national events. UK insurers paid GBP 197 million in claims in 2024, equal to USD 248.2 million, with ransomware and malware representing a rising share of losses, which intensified underwriting focus on control maturity and incident response readiness.

War-Exclusion & Systemic-Risk Uncertainty: Lloyd's LMA5381 Mandate Amplifies Attribution Disputes

Lloyd’s directive to include clear state-backed attack exclusions across standalone cyber lines was designed to reduce ambiguity, but it introduced grey areas where sponsorship is contested or concealed. Systemic exposures tied to common technologies and service providers continue to challenge aggregation management within the UK cyber insurance market. Alternative risk transfer structures have begun to supplement traditional capacity, but outstanding tail scenarios still exceed current private capital appetite. Calls for a UK backstop have focused on pooling and state support for extreme events that could trigger widespread economic loss. Market guidance has encouraged shared practices on exposure monitoring, talent investment, and dynamic risk assessment to better cope with potential systemic events.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stand-Alone Policies Dominate Despite Packaged Convenience for Sub-GBP 1m Risks

Stand-alone policies accounted for a 70.62% share of the UK cyber insurance market size in 2025, establishing a clear leadership position among product formats. Buyers favored dedicated cyber contracts to avoid restrictive sub-limits and to secure specialized breach response partners with known fee schedules. UK primary limits under stand-alone covers with excess placements building combined towers over GBP 100 million, or USD 127 million, where warranted by exposure. SME-focused packaged policies remained attractive for micro businesses that prioritize simplicity and consolidated renewals. Yet many packaged endorsements include higher deductibles and narrower grants for business interruption and regulatory response, which has prompted more mid-market buyers to migrate toward stand-alone placements in the UK cyber insurance market.

The UK cyber insurance market share tilt toward stand-alone also reflects underwriting innovation, including real-time risk monitoring and proactive response capabilities that reduce loss frequency and severity. UK guidance has highlighted buyer knowledge gaps, with a material share of organizations unsure whether they hold cyber cover at all, especially when coverage is embedded in packages. New SME extensions that pay when a named customer’s incident triggers order cancellations address a coverage gap exposed by manufacturing and retail outages in 2025. As products evolve, brokers continue to emphasize explicit control maintenance and attestation to reduce post-incident disputes for UK buyers.

By Enterprise Size: Large Enterprises Hold 43.56% Share; Micro/Small Cohort Accelerates at 13.34% CAGR

Large enterprises held 43.56% of UK cyber insurance market share in 2025, reflecting greater regulatory exposure and demand for higher limits, broader terms, and specialized advisory resources. Mid-market firms used stand-alone policies to address sustained business interruption and regulatory investigation risks that exceed common packaged sub-limits. Small and micro enterprises accelerated their adoption due to security scheme updates, embedded distribution, and supply-chain mandates that make certification and cover a de facto prerequisite for certain contracts in the UK cyber insurance market. Premium differences between the UK and the US for comparable SME covers continued to reflect model uncertainty and portfolio experience variance in 2024 and 2025. Training and MFA adoption lagged within many small businesses, which sustained elevated incident rates relative to control-mature large firms.

The UK cyber insurance market size for small and micro enterprises is projected to expand at a 13.34% CAGR to 2031, driven by April 2026 scheme changes that embed MFA and a 14-day patch requirement. Claims patterns in 2025 showed SME severity near GBP 40,000, or USD 50,800, and long lifecycle durations, which reinforced the importance of fit-for-purpose limits and incident response services. Large enterprises continued to increase limits and refine coverage for third-party and regulatory exposures as supply-chain and cloud-driven risks advanced. Policy terms increasingly tied to control attestations encouraged all company sizes to improve authentication, endpoint management, and recovery preparedness in the UK cyber insurance market. Brokers and carriers highlighted budget constraints in micro businesses, which trade groups proposed to address via premium tax reforms and awareness campaigns.

By Industry Vertical: BFSI Commands 28.71% Share; Healthcare Accelerates at 12.83% CAGR Amid CNI Mandates

BFSI accounted for 28.71% of segment value in 2025, reflecting stringent regulatory obligations for data protection, operational resilience, and incident response planning, along with higher control maturity in identity and transaction verification. Healthcare and life sciences exhibited the fastest growth profile with a 12.83% projected CAGR to 2031, underpinned by NHS procurement requirements and the operational lessons from sector-specific incidents. Retail and e-commerce events demonstrated the revenue impact of outages in 2025, with one leading retailer reporting losses that surpassed GBP 1 million per day, or USD 1.27 million, during a multi-week disruption. Manufacturing faced the largest single-event severity, as the August 2025 attack on a top automaker drove a loss estimate of GBP 1.9 billion, or USD 2.4 billion, with cascading effects on SME suppliers. Technology and telecom firms maintained higher control maturity, which helped constrain severity despite persistent phishing exposure.

The UK cyber insurance market continued to design vertical-specific solutions, including blended covers for BFSI that combine cyber and crime, and new SME endorsements for supplier-driven business interruption in manufacturing and retail. Median UK claim severity for non-ransomware events, such as business email compromise and funds transfer fraud, trailed ransomware by a considerable margin, which encouraged more frequent adoption of social engineering and payment fraud extensions by BFSI and mid-market buyers. Education and charities faced persistent exposure with lower insurance penetration, which elevated the value of security certification and awareness training in future placements. Healthcare suppliers advanced cyber programs in line with NHS charter expectations, which included 24/7 monitoring and immutable backups that reduce long-tail loss development in the UK cyber insurance market. Cross-sector pressure from data protection enforcement sustained demand for regulatory response coverage and legal support within incident response retainer structures.

Geography Analysis

London and the South East concentrate a large share of UK premium and capacity due to BFSI headquarters, technology corridors, and proximity to Lloyd’s syndicates that anchor the UK cyber insurance market. Prominent 2025 retail and manufacturing incidents triggered additional board-level scrutiny in metropolitan centers and accelerated limit purchases. Specialty carriers headquartered in London scaled services that blend prevention, response, and capacity to meet complex buyer expectations. Data center corridors and cloud ecosystem hubs around London and key English cities deepened dependencies that increased third-party risks across regional portfolios in the UK cyber insurance market. NHS frameworks reinforced certification baselines for suppliers nationwide, which cascaded into local procurement practices.

Manufacturing clusters in the Midlands and the North West drove rapid growth through supply-chain security and contracting requirements that favored stand-alone policies with robust business interruption terms. The August 2025 auto sector outage concentrated losses around Midlands production sites and highlighted downstream exposure for SMEs that historically relied on packaged policies in the UK cyber insurance market. Wales and Northern Ireland exhibited measured growth due to sector mix and digital infrastructure constraints, with fintech growth in Cardiff and aerospace and financial services shaping Belfast’s exposure profile. Scotland’s procurement policies and cyber programs moved in close alignment with UK-wide requirements and supported steady growth among Edinburgh-based financial and technology firms. Persistent phishing exposure and hybrid workforce challenges created sustained demand for advisory and training support.

Lloyd’s remained the capacity hub for the UK cyber insurance market, while mergers and capital markets activity shifted competitive dynamics. Specialty carriers added catastrophe bond and ILS capacity that diversified risk-bearing across investors and geographies. Broker facilities scaled cross-border placement options and enhanced access for regional buyers, which supported broader adoption outside London. The UK’s legislative roadmap signaled wider regulatory scope for managed service providers and data centers, which is expected to lift baseline security and reporting discipline for critical suppliers. Embedded distribution models advanced reach into regional SME communities, especially in the Midlands and the North West.

Competitive Landscape

The UK cyber insurance market featured both consolidation and new-entrant growth, with specialty carriers expanding capacity while recent M&A concentrated expertise and portfolios within larger platforms. Technology-enabled underwriting and proactive incident response differentiated leading MGAs and carriers as primary rates softened through 2025. Specialty programs blended prevention, monitoring, and event response with insurance capital to reduce frequency and shorten disruption windows in the UK cyber insurance market. Catastrophe bond programs scaled protection for systemic events and signalled market leadership in alternative capital deployment. Broker research and advisory capabilities guided limit-setting, control prioritization, and risk transfer structuring for complex buyers.

Carrier and MGA strategies emphasized SME growth via embedded distribution and modular product extensions, while large-cap buyers prioritized excess towers and specialized clauses for third-party and cloud exposure. Syndicate partnerships with technology providers expanded proactive monitoring and portfolio-wide risk intelligence within the UK cyber insurance market. Brokers invested in European placement facilities and product innovation, including stop-loss and event-based structures to address accumulation and surge scenarios. Alternative risk transfer advanced as key carriers issued sub-layered cat bonds and prepared dedicated ILS strategies, which broadened investor participation in cyber risk. Trade groups promoted measures to reduce protection gaps for SMEs, including premium tax reforms and a potential systemic-event backstop.

Across 2025, premium competition and broader terms benefited buyers, while claims emergence from prior underwriting years placed pressure on long-run economics in the UK cyber insurance market. Control-based incentives, such as credits linked to certification frameworks, encouraged investment in MFA, patching, and detection, which supported improved loss performance. Legal and regulatory trends sustained demand for incident response and regulatory investigation coverage and shaped new wording around state-sponsored and systemic risk. Market guidance prioritized exposure aggregation management through shared practices and better data, which will inform capacity deployment in 2026 and beyond. New products around AI risk and third-party cloud resilience reflected changing threat vectors and buyer priorities.

United Kingdom Cyber Insurance Industry Leaders

AIG

Beazley

Hiscox

Allianz

AXA XL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SCOR partnered with Baobab to expand cyber underwriting capacity in Europe via the SCOR Syndicate at Lloyd’s, supporting Baobab’s CyberSafe product and leveraging Baobab’s Deep Scan vulnerability alerting technology.

- January 2026: CFC introduced a global SME focused extension covering business interruption when a key customer suffers a cyber event, inspired by cascading supplier disruption following the Jaguar Land Rover 2025 ransomware event.

- January 2026: NHS England advanced its Cyber Security Supply Chain Charter implementation, contacting suppliers to evidence controls such as MFA, monitoring, patching and compliance with the Data Security and Protection Toolkit.

- October 2025: CFC created a US-based cyber development team led by John Keebler, Morgan Justice, and Annie Lyons to accelerate US cyber growth and support brokers with faster underwriting decisions.

United Kingdom Cyber Insurance Market Report Scope

Cyber liability insurance is an insurance policy that provides businesses with a combination of coverage options to help protect the company from data breaches and other cyber security issues. It's not a question of if the organization will suffer a breach but when. Travelers and cyber insurance policyholders can also access tools and resources to manage and mitigate cyber risk. Cyber insurance generally covers your business's liability for a data breach involving sensitive customer information, such as Social Security numbers, credit card numbers, account numbers, driver's license numbers, and health records.

The UK cyber (liability) insurance market is segmented by product type (packages, standalone) and application type (banking & financial services, IT & telecom, healthcare, retail, and other application types).

The report offers market size and forecasts for the UK cyber (liability) insurance market in value (USD) for all the above segments.

| Packaged |

| Standalone |

| Large Enterprises |

| Medium Enterprises |

| Small and Micro Enterprises |

| BFSI |

| IT & Telecom |

| Retail & E-commerce |

| Healthcare & Life Sciences |

| Manufacturing |

| Government & Public Sector |

| Education |

| By Product Type | Packaged |

| Standalone | |

| By Enterprise Size | Large Enterprises |

| Medium Enterprises | |

| Small and Micro Enterprises | |

| By Industry Vertical | BFSI |

| IT & Telecom | |

| Retail & E-commerce | |

| Healthcare & Life Sciences | |

| Manufacturing | |

| Government & Public Sector | |

| Education |

Key Questions Answered in the Report

What is the current size and growth outlook for the UK cyber insurance market?

The UK cyber insurance market size was USD 1.56 million in 2025 and is expected to reach USD 3.28 million by 2031, at a 13.18% CAGR over 2026-2031.

Which product type leads and how fast is it growing?

Stand-alone policies led with 70.62% share in 2025, and are projected to grow at a 12.92% CAGR through 2031.

Which customer segment is expanding the fastest?

Small and micro enterprises are projected to grow at a 13.34% CAGR to 2031, supported by Cyber Essentials updates and embedded distribution.

Which verticals are most important for demand?

BFSI held 28.71% of segment value in 2025, while healthcare and life sciences is the fastest-growing vertical at a projected 12.83% CAGR to 2031.

How are premiums and capacity trending in the UK?

Premiums fell through 2025 as capacity remained abundant and new entrants arrived, although brokers flagged sustainability risks if loss trends stay elevated.

What regulations are shaping buying behaviour?

ICO enforcement, NHS supply-chain requirements, and the UK Cyber Security and Resilience Bill are elevating baseline controls and incident reporting expectations across buyers.

Page last updated on: