United Kingdom Car Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

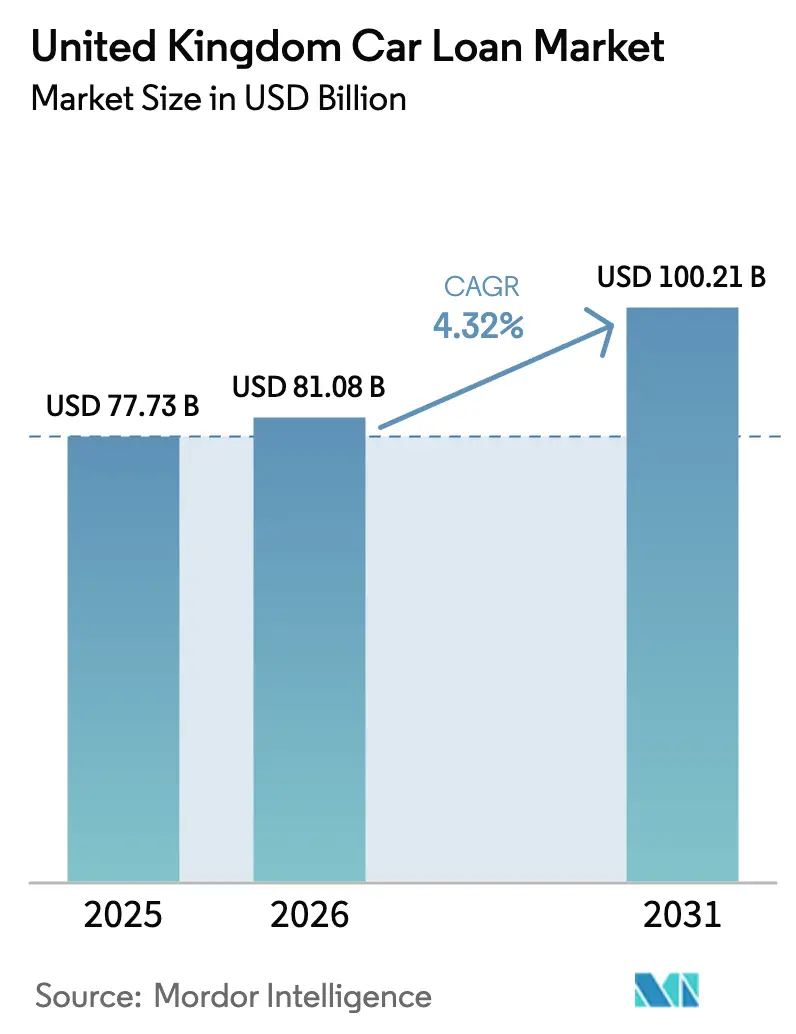

| Base Year Market Size (2025) | USD 77.73 Billion |

| Market Size (2026) | USD 81.08 Billion |

| Market Size (2031) | USD 100.21 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

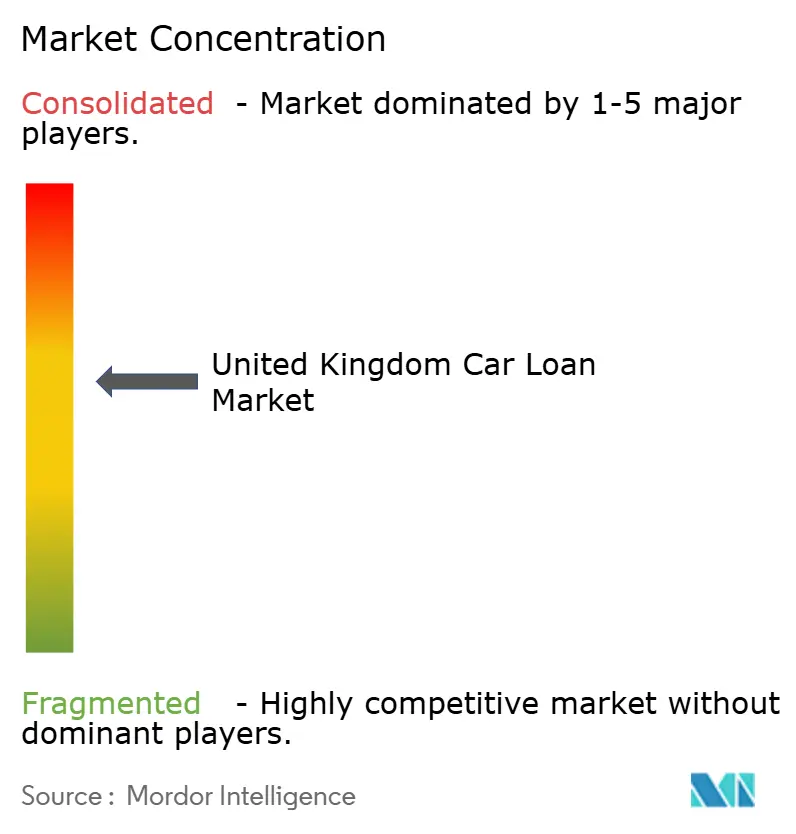

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Car Loan Market Analysis by Mordor Intelligence

The United Kingdom car loan market size is expected to grow from USD 77.73 billion in 2025 to USD 81.08 billion in 2026 and is forecast to reach USD 100.21 billion by 2031 at 4.32% CAGR over 2026-2031. Demand remains resilient as court clarity on dealer commissions calms regulatory risk and the Financial Conduct Authority (FCA) advances a sector-wide redress framework[1]Supreme Court of the United Kingdom, “Judgment: Johnson v FirstRand Bank,” supremecourt.uk. Digitization accelerates underwriting speeds, while agency-model rollouts let original-equipment-manufacturer (OEM) captives recapture finance margins. Electric-vehicle (EV) financing expands in response to the Zero Emission Vehicle (ZEV) mandate, yet volatile used-EV values compel tighter loan-to-value ratios. Fintech entrants armed with alternative credit engines widen access for near-prime applicants, intensifying competition against incumbent banks and dealer-led point-of-sale (POS) channels.

Key Report Takeaways

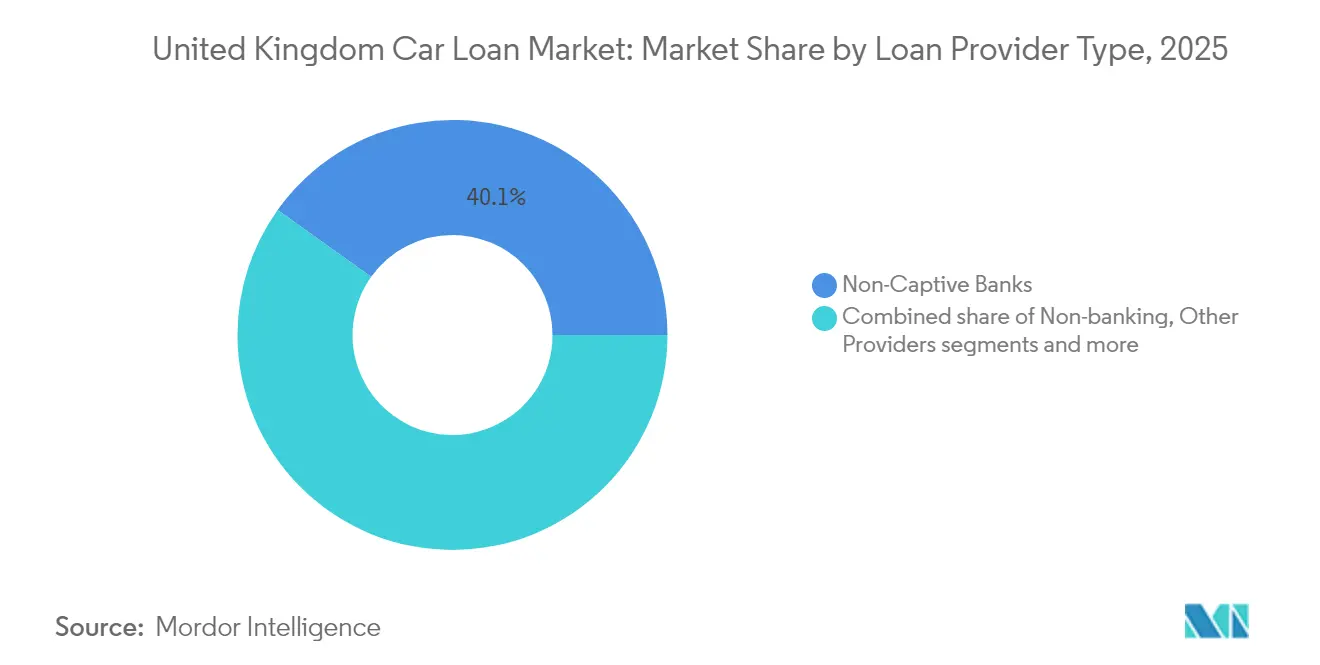

- By loan provider type, non-captive banks led with 40.12% United Kingdom car loan market share in 2025, while non-banking financial services are projected to grow at a 4.83% CAGR through 2031.

- By vehicle type, used cars accounted for 57.05% of the United Kingdom car loan market size in 2025 and are advancing at a 5.46% CAGR to 2031.

- By distribution channel, dealership POS held 70.65% revenue share of the United Kingdom car loan market in 2025, whereas OEM captives are forecast to expand at a 4.21% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United kingdom contributes to a system defined not by any single country or region but by the interaction of many. The global car loan market data by Mordor Intelligence represents that combined structure.

United Kingdom Car Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitised point-of-sale (POS) platforms accelerate dealer-originated approval times | +0.8% | Global, with early gains in London, Manchester, Birmingham | Medium term (2-4 years) |

| Growing adoption of "green-EV" finance products tied to UK ZEV mandate incentives | +1.2% | National, with concentration in urban centers and Scotland | Long term (≥ 4 years) |

| OEM deposit-subsidy campaigns amid agency-model roll-outs | +0.6% | National, with premium segments in South East leading adoption | Short term (≤ 2 years) |

| Fleet electrification boosting salary-sacrifice & contract-hire demand | +0.9% | National, with corporate hubs in London, Edinburgh, Manchester driving uptake | Medium term (2-4 years) |

| FCA-driven commission disclosure rules increasing migration to fixed-rate loans | +0.7% | National regulatory compliance requirement | Short term (≤ 2 years) |

| Alternative credit-risk engines (open-banking & bureau-API) widen near-prime access | +0.5% | National, with higher impact in regions with limited traditional banking access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitised Point-of-Sale Platforms Accelerate Dealer-Originated Approval Times

Automated decisioning now delivers 80% of approvals inside 60 seconds, shrinking proposal-to-payout intervals for more than 4,000 dealer forecourts[2]Blue Motor Finance, “Dealer Technology Report 2024,” bluemotorfinance.co.uk. Technology investments by Evolution Funding, Close Brothers, and MotoNovo raise average dealer conversion rates to 40% from prior 28% levels. API links with classifieds portals give lenders real-time vehicle-demand insights, sharpening risk-based pricing. The FCA’s Consumer Duty framework incentivizes further digitization because automated systems evidence fair treatment. Independent dealers gain access to sophisticated underwriting once reserved for franchised groups, narrowing competitive gaps. Electronic signatures and remote onboarding remove geographic barriers, letting rural retailers match urban finance performance.

Growing Adoption of Green-EV Finance Products Tied to the ZEV Mandate

The ZEV mandate compels 22% EV sales in 2024, rising to 80% by 2030, spurring lenders to launch battery-specific products[3]VDA, “UK Zero Emission Vehicle Mandate Briefing,” vda.de. Close Brothers pledged GBP 1 billion for battery-electric-vehicle lending over five years. Residual-value swings used EVs retain only 46% of cost versus 85% two years earlier, forcing lenders to recalibrate risk capital. BNP Paribas’s partnership with Jaguar Land Rover bundles charging, energy, and lifecycle services, illustrating integrated mobility finance. Government tariff waivers and full-expensing allowances add policy certainty, lengthening loan tenors acceptable to risk committees. Fleet salary-sacrifice schemes multiply because tax advantages offset depreciation anxiety for corporate buyers.

OEM Deposit-Subsidy Campaigns Amid Agency-Model Rollouts

Stellantis, BMW, and Mercedes-Benz use deposit subsidies to smooth the transition toward direct-to-consumer agency models, shifting finance margins from dealers to captives. Integrated digital journeys take customers from OEM websites to localized delivery while preserving pricing control. Premium marques spend aggressively because lifetime value justifies higher acquisition costs. The August 2025 Supreme Court ruling clarifies that dealers are not fiduciaries, reducing litigation fears and accelerating OEM strategy execution. Captives synchronize subsidy offers with EV launches to manage complex buyer education. FCA oversight ensures that incentive structures remain transparent, maintaining consumer trust during structural change.

Fleet Electrification Boosting Salary-Sacrifice and Contract-Hire Demand

More than 780,000 battery-electric cars operated on the United Kingdom roads by mid-2023, and corporate electrification targets lift demand for fixed-cost leasing. Paragon Bank rapidly scales operating-lease products that shelter clients from depreciation risk. Clean-air and ultra-low-emission zones raise compliance costs for diesel fleets, accelerating replacement cycles. Salary-sacrifice schemes save employees' income tax and national insurance, aligning environmental and financial objectives. Contract-hire bundles servicing and charging infrastructure, simplifying EV management for firms lacking in-house expertise. Lenders embed telematics to monitor utilization, supporting residual-value forecasting and proactive maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potential £9-18 bn redress over legacy discretionary-commission cases | -1.8% | National regulatory requirement affecting all major lenders | Short term (≤ 2 years) |

| Rising used-EV residual-value volatility inflates lender RV risk capital | -0.9% | National, with higher impact in urban EV adoption centers | Medium term (2-4 years) |

| Stricter affordability rules under Consumer Duty curb sub-prime approval rates | -0.6% | National FCA regulatory compliance, with higher impact in lower-income regions | Short term (≤ 2 years) |

| Bank funding-cost spikes widen pricing gap vs. captives & fintech lenders | -0.8% | National, with traditional banks in London and major cities most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Potential GBP 9-18 Billion Redress Over Legacy Discretionary-Commission Cases

FCA review findings expose lenders to as much as GBP 18 billion in compensation liabilities, prompting Lloyds to provision GBP 1.25 billion already. Close Brothers forecasts GBP 10–15 million yearly compliance costs, constraining lending appetite[4]Close Brothers Group, “Annual Report 2025,” closebrothers.com. This coming October 2025 consultation could mandate repayments on contracts dating to 2007, freezing expansion plans until capital buffers strengthen. Smaller brokers have existed, reducing product choice and denting competition. Securitization and asset sales shore up capital but elevate funding costs, widening price gaps against fintech rivals. Dividends remain suspended at several banks, signaling defensive priorities.

Rising Used-EV Residual-Value Volatility Inflates Lender Risk Capital

Average used-EV retention sank to 46% of original cost, versus 85% in 2022, slashing operating-lease profitability. Lloyds recorded higher depreciation charges on operating-lease books, revealing balance-sheet sensitivity. OEM price cuts, especially by Tesla, create further downside pressure on nearly new stock. Limited battery-health data compels conservative loan-to-value ratios, raising consumer deposit requirements. Supply shortages of three-to five-year-old cars obscure true market-clearing prices, complicating models. Higher risk-weight assets inflate capital intensity, making personal-loan substitutes increasingly attractive to price-sensitive borrowers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Provider Type: Fintech Momentum Challenges Bank Dominance

Non-captive banks controlled 40.12% of the United Kingdom car loan market in 2025, leveraging long-standing dealer ties and diversified funding. Yet non-banking financial services post the fastest 4.83% CAGR as platforms like Carmoola secure GBP 300 million securitizations to scale originations. Challenger lenders deploy open-banking data and behavioral analytics to price near-prime risk, compressing approval times to minutes. Traditional institutions counter with API upgrades and co-origination agreements, but legacy systems slow feature deployment. The FCA’s uniform disclosure rules narrow differentiation that once favored high-street banks, nudging customers toward digital specialists.

The United Kingdom car loan industry nonetheless remains relationship-driven; POS dealers still originate most bank submissions. Regulatory capital resilience gives banks room to absorb redress costs, sustaining underwriting capacity during turbulence. Captive arms of OEMs integrate finance into online configurators, improving customer stickiness even as overall share lags volume lenders. Peer-to-peer platforms serve thin-file borrowers but face scaling limits from retail-investor funding. Consolidation may see capital-strong banks acquiring high-growth fintechs to blend cost efficiency with brand trust.

By Vehicle Type: Used-Car Financing Leads in Value and Pace

Used-vehicle contracts represented 57.05% of the United Kingdom car loan market size in 2025, reflecting consumer value preferences during macro uncertainty. Supply gaps dating to pandemic shutdowns lifted prices, protecting lender collateral and spurring 5.46% segment CAGR forecasts. Dealers expand sourcing radii and rely on digital auctions to replenish aging lots. Lenders loosen age and mileage ceilings but tighten residual buffers on electric stock. Certification programs and warranty add-ons reassure borrowers about mechanical risk.

New-car finance growth moderates as agency models alter dealer incentives and OEM captives push direct online journeys. EV penetration in nearly new stock surpasses 20% of sub-one-year parc, offering lenders early trial runs of emerging depreciation curves. Manufacturer-backed used platforms like SPOTiCAR blur new versus used shopping paths, further lifting finance attach rates. Regulators standardize battery-health reporting, improving underwriting clarity over time. Fragmented independent dealers embrace fintech partnerships to stay competitive against vertically integrated OEM channels.

By Distribution Channel: POS Stronghold Meets Omnichannel Innovation

Dealership POS origination accounted for 70.65% of 2025 lending volume, confirming the enduring importance of in-person guidance for high-ticket commitments. On-site finance desks bundle credit, insurance, and add-on products in a single interaction, sustaining convenience advantages. Supreme Court guidance on commissions removes reputational ambiguity, giving dealers confidence to promote finance openly. Nonetheless, online marketplaces such as Zuto recorded double-digit revenue gains as comparison shopping migrates to mobile. Consumers increasingly pre-qualify credit online, then finalize at the showroom, blending channels.

OEM captives achieve 4.21% growth by integrating finance into build-and-price tools and by offering home delivery. Broker consolidation, exemplified by Evolution Funding’s Creditas acquisition, expands technology reach across thousands of independent retailers. Fintech lenders issue loan codes redeemable at any dealership, cementing omnichannel flexibility. The United Kingdom car loan market thus shifts toward hybrid models wherein digital origination funnels into physical fulfillment, preserving dealer relevance while satisfying customer demand for speed. FCA Consumer Duty oversight ensures pricing parity regardless of channel, promoting confidence in both digital and brick-and-mortar experiences.

Geography Analysis

Regional economics shape lending appetite: London and the South East post the largest balances, due to GDP per head of GBP 69,077, more than double the North East figure. Higher incomes translate into larger average loan amounts and higher EV penetration, reinforcing the growth skew toward metropolitan areas. Scotland shows outsized EV uptake supported by developed incentives, driving brisk demand for salary-sacrifice leases.

Northern Ireland contends with cross-border supply complications that occasionally delay vehicle deliveries, causing lenders to extend offer validity periods. Wales and the Midlands experience heightened commercial-vehicle finance as logistics firms modernize fleets to meet clean-air-zone stipulations. Urban clean-air expansion in Birmingham, London, and Edinburgh propels localized EV loan growth that runs ahead of national averages, though rural regions still favor diesel due to charging constraints.

Regional challenger banks partner with the British Business Bank to funnel asset-finance guarantees into SMEs, sustaining approval rates in economically weaker zones. Retail loan-to-value caps vary modestly by postcode as lenders weigh unemployment and property-value metrics. Digital-only lenders close historic geographic gaps, enabling remote onboarding regardless of customer location. EV infrastructure grants concentrate in city clusters, further widening regional demand dispersion. Despite disparities, FCA rules maintain unified consumer-protection standards nationwide, compelling lenders to vary pricing strictly on risk, not postcode bias.

The car loan market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe and Asia. This is complemented by country-specific insights for France, Russia, China, South Korea, India, Japan, and India, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Market concentration remains moderate as no single entity controls more than one-fifth of originations. Lloyds’s Black Horse unit, Volkswagen Financial Services, and Santander Consumer United Kingdom headline traditional leaders, though each battles reputational scars from commission scrutiny. Close Brothers holds a GBP 2.016 billion book and invests in automated decisioning to offset rising compliance overheads.

Digital disruptors intensify pressure; Blue Motor Finance processes 80% of applications within 60 seconds, setting new speed benchmarks. Carmoola’s GBP 300 million securitization underscores investor belief in app-based lending models. Consolidation accelerates: Evolution Funding bought Creditas to broaden dealer coverage, while venture capital acquired majority stakes in LE Capital, combining capital depth with agile tech.

Strategic focus shifts toward EV lifecycle products that pair finance with charging and energy packages. Captives realign to agency sales, reclaiming margin from dealers but assuming greater consumer-experience responsibility. Traditional banks explore white-label fintech stacks to rejuvenate dated systems. Compliance competence becomes a competitive differentiator under FCA Consumer Duty, rewarding lenders that can demonstrate consistent, good customer outcomes through data transparency. The United Kingdom car loan market, therefore, evolves along twin axes of scale and technology, with winners blending both.

United Kingdom Car Loan Industry Leaders

Lloyds Banking Group (Black Horse)

Volkswagen Financial Services UK

Santander Consumer (UK)

Close Brothers Motor Finance

Toyota Financial Services UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Carmoola secured up to GBP 300 million asset-backed-securities funding arranged with NatWest and Chenavari Investment Managers, lowering the cost of funds and expanding lending headroom.

- April 2025: TransUnion completed the acquisition of Monevo, enhancing credit-prequalification services for more than 150 lenders worldwide.

- April 2025: Constellation Automotive Group bought Aston Barclay and The Car Buying Group to stabilize remarketing capacity during volatile used-vehicle conditions.

- March 2024: Evolution Funding acquired Creditas Financial Solutions, extending technology benefits to independent dealers and enlarging lender-panel access.

United Kingdom Car Loan Market Report Scope

A car loan, also known as an auto loan or vehicle loan, is a type of financing provided by a financial institution or lender to help individuals purchase a car.

The UK car loan market is segmented by product type and provider type. By product type, the market is sub-segmented into used cars and new cars, and by provider type, the market is sub-segmented into banks, non-banking financial services, original equipment manufacturers, and other provider types. The report offers the value (USD) for the above segments.

| Non-Captive Banks |

| Non-banking Financial Services |

| Original Equipment Manufacturers (Captives) |

| Other Providers |

| New Car |

| Used Car |

| Dealership Point-of-Sale |

| Online Direct Lending |

| Brokers & Marketplaces |

| By Loan Provider Type (Value) | Non-Captive Banks |

| Non-banking Financial Services | |

| Original Equipment Manufacturers (Captives) | |

| Other Providers | |

| By Vehicle Type (Value) | New Car |

| Used Car | |

| By Distribution Channel (Value) | Dealership Point-of-Sale |

| Online Direct Lending | |

| Brokers & Marketplaces |

Key Questions Answered in the Report

Which provider segment is growing fastest in United Kingdom vehicle finance?

Non-banking financial services, driven by fintech lenders, are forecast to grow at a 4.83% CAGR through 2031.

Why are used-car loans more popular than new-car loans?

Used vehicles offer better value amid economic uncertainty, leading to a 57.05% share of 2025 loan balances and the highest 5.46% growth rate.

How will the ZEV mandate impact car-loan demand?

The requirement for 80% EV sales by 2030 drives demand for specialized green-EV finance products and fleet salary-sacrifice schemes.

What regulatory risk most threatens lenders?

Potential GBP 9-18 billion redress for past discretionary commissions could restrain capital and accelerate market consolidation.

Are digital originations replacing dealer POS finance?

Online channels are growing quickly, but dealership POS still captures 70.65% of originations, suggesting a hybrid future combining both experiences.

How large is the United Kingdom car loan market in 2026?

It stands at USD 81.08 billion and is projected to hit USD 100.21 billion by 2031 at a 4.32% CAGR.

Page last updated on: