Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

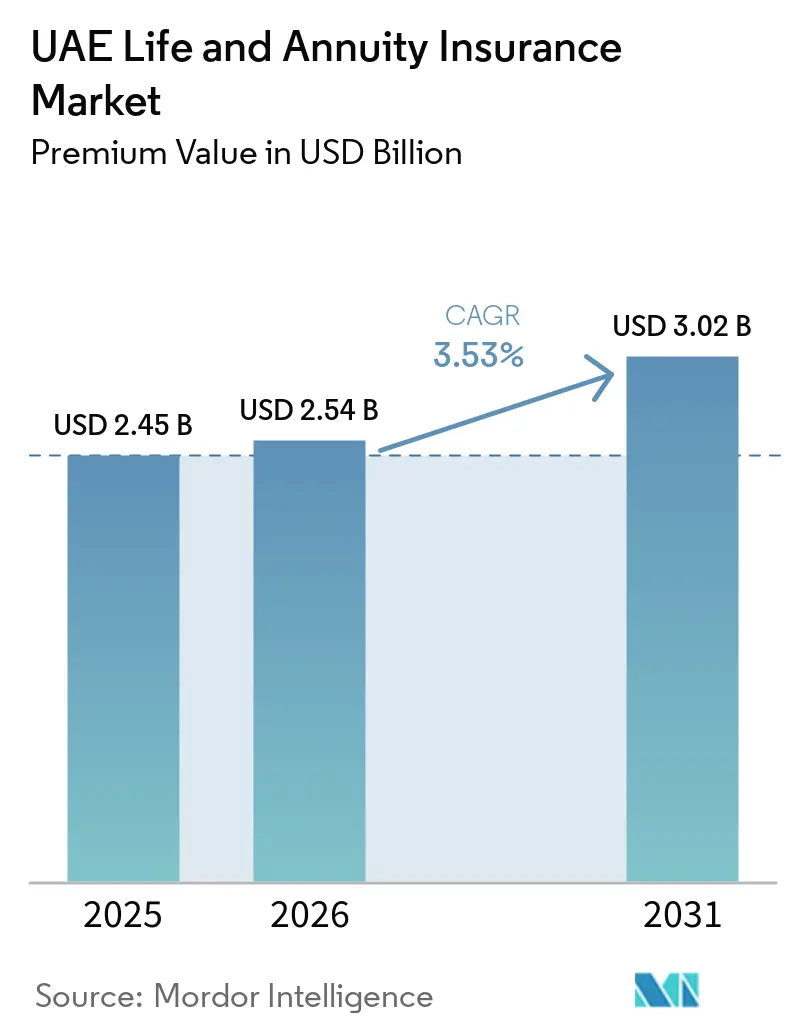

| Base Year Market Size (2025) | USD 2.45 Billion |

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

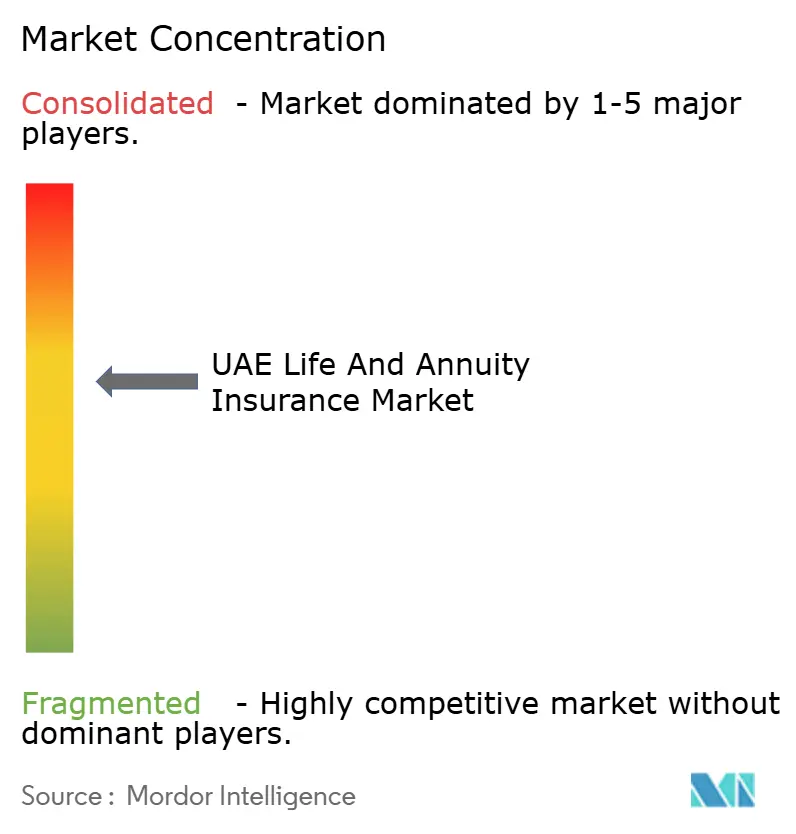

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Life and Annuity Insurance Market Analysis by Mordor Intelligence

The UAE Life And Annuity Insurance Market size in terms of premium value is projected to expand from USD 2.45 billion in 2025 and USD 2.54 billion in 2026 to USD 3.02 billion by 2031, registering a CAGR of 3.53% between 2026 to 2031.

Growth stems from the 2025 corporate pension mandate, an expanding expatriate population that increasingly wants to retire locally, and a zero-tax environment that magnifies after-tax returns. Digital distribution, product innovation in Sharia-compliant solutions, and Dubai’s role as the financial hub further reinforce scale economies and capital inflows. Meanwhile, policy lapses tied to workforce mobility, low retail financial literacy, and equity-market volatility temper momentum but do not derail the long-run uptick in systematic savings demand.

Key Report Takeaways

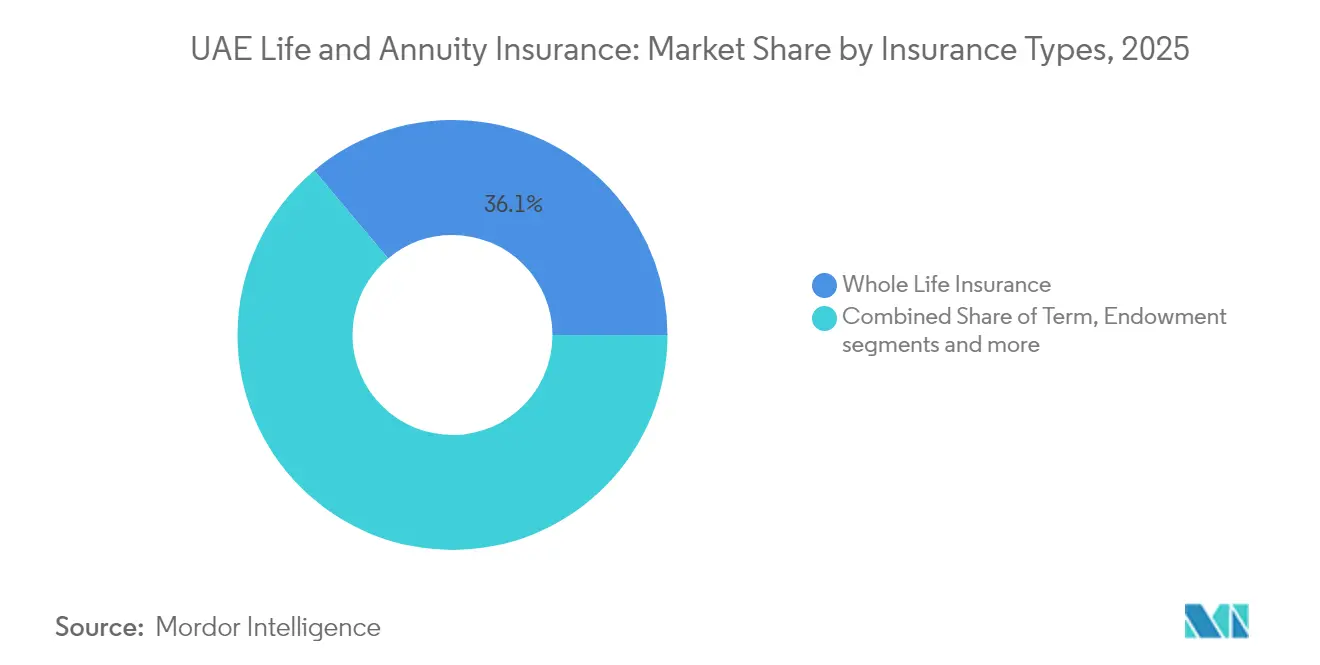

- By insurance type, whole life led with 36.12% of UAE life and annuity insurance market share in 2025; unit-linked policies are set to expand at a 10.12% CAGR to 2031.

- By distribution channel, bancassurance held 43.02% revenue share in 2025, while direct digital is projected to grow the fastest at 15.05% CAGR through 2031.

- By premium payment, regular premium products accounted for 69.35% of the UAE life and annuity insurance market size in 2025; single premium plans will advance at a 9.42% CAGR over the forecast window.

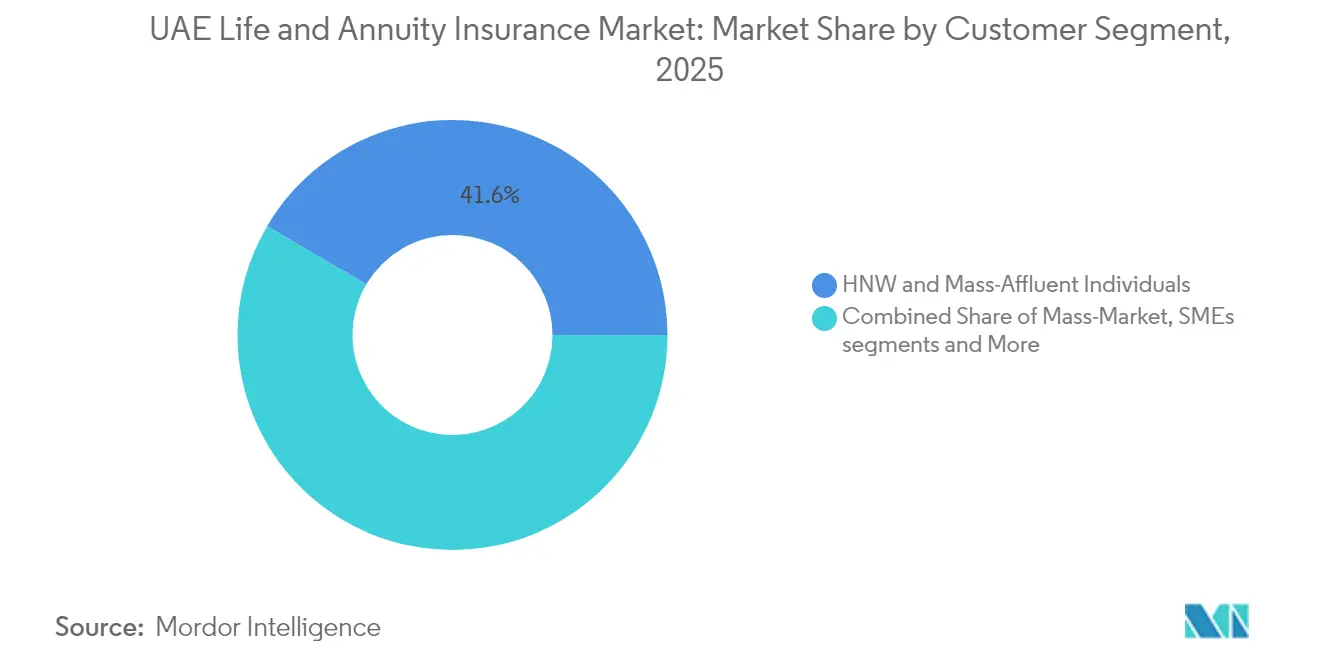

- By customer segment, HNW & mass-affluent policyholders represented 41.55% of premiums in 2025, whereas the mass-market segment is poised for a 9.14% CAGR.

- By emirate, Dubai captured 39.92% of market revenue in 2025 and is set to post an 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Life and Annuity Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory corporate pension reform (2025) | +1.2% | UAE-wide (Dubai, Abu Dhabi strongest) | Medium term (2–4 years) |

| Rising expatriate workforce & remittance-linked savings | +0.8% | Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Rapid digital-first distribution (mobile, robo-advice) | +0.6% | Urban centers nationwide | Short term (≤ 2 years) |

| Favorable zero-tax regime | +0.4% | Nationwide | Long term (≥ 4 years) |

| Growing demand for Sharia-compliant retirement solutions | +0.3% | Northern Emirates highlighted | Medium term (2–4 years) |

| Insurtech–telco micro-pension partnerships | +0.2% | Mobile-first demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory corporate pension reform (2025)

Federal Decree-Law No. 57 of 2023 makes monthly pension contributions compulsory for private-sector staff, splitting 26% of salary between employers and employees and creating a recurrent pool estimated at USD 3.3 billion each year. The rule lifts retirement savings from a one-off end-of-service gratuity to disciplined, investment-grade funding that insurers can channel into annuity and unit-linked products. Employers may opt for regulated investment funds instead of lump-sum accruals, giving life companies a pipeline of stable assets under management. Voluntary top-ups of up to 25% of salary further widen the premium base, especially for mid-income Emiratis and expatriates. International agencies view the framework as a regional template for modern social protection[1]General Pension & Social Security Authority, “Corporate Pension Framework Overview,” gpssa.gov.ae.

Rising expatriate workforce & remittance-linked savings

Roughly 65% of foreign residents now plan to settle permanently, a marked shift from the transient mindset of earlier years. Among them, 48% already save regularly for retirement, even though only 32% qualify for a state pension in their home country. Cultural priorities such as children’s overseas education push demand for protection-cum-investment products that blend tuition funding with life cover. Remittance-linked plans that credit overseas dependents meet this need while locking in long-term premium flows. The projected USD 980 billion generational wealth transfer by 2028 adds another layer of opportunity for estate-planning life contracts.

Rapid digital-first distribution

Smartphone penetration above 95% enables instant onboarding, with insurers issuing fully underwritten term policies in under 10 minutes via UAE PASS log-ins. Aggregator sites and super-apps post a 15.62% CAGR in new business, outpacing all other channels. Open-Finance rules effective April 2024 force banks and insurers to share product APIs, paving the way for embedded cover inside fintech wallets[2]Central Bank of the UAE, “Annual Insurance Statistics 2024,” cbuae.gov.ae . Partnerships such as Policybazaar.ae with SALAMA and Sukoon’s collector-app illustrate how niche segments—from non-GCC car owners to high-net-worth art collectors—are captured at low acquisition cost. Data trails from these platforms allow dynamic pricing and personalised riders that improve persistency.

Favourable zero-tax regime

Absence of income, capital gains, and inheritance taxes means investment gains inside unit-linked wrappers compound untaxed, enhancing long-run returns relative to competing offshore centres. The same tax neutrality lets single-premium whole-of-life plans serve as estate-liquidity tools for expatriates holding global assets. Dubai’s financial hub status adds complementary advantages: DIFC courts enforce common-law structures, and banks such as Emirates NBD report record USD 7.4 billion profits that bolster bancassurance capacity[3]Emirates NBD, “2024 Full-Year Results,” emiratesnbd.com. Together, these factors position the UAE as the Gulf’s pre-eminent wealth-accumulation domicile, drawing both regional and international premium flows. Government rhetoric continues to affirm the no-tax stance, reinforcing consumer confidence.

Restraints Impact Analysis*

| Restraint | ( ~ ) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low retail financial literacy | -0.7% | Northern Emirates most acute | Medium term (2–4 years) |

| High policy lapse ratio among transient expatriates | -0.5% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Equity-market volatility dampening unit-linked returns | -0.4% | Nationwide | Short term (≤ 2 years) |

| Cultural bias against annuitisation | -0.3% | Varies by expatriate group | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low retail financial literacy

An estimated 38% of adults are financially illiterate and 25% save nothing each month, stalling uptake of products with variable returns. Only 12% of expatriates seek professional advice; instead, 35% rely on friends or family, leading to under-insurance and mis-sold policies. Complex fee structures in unit-linked plans exacerbate mistrust when market dips erode account values. While schools now include budgeting modules, the impact on new sales will take years. Insurers must invest in plain-language apps, animated explainers and advisor training to bridge the comprehension gap.

High policy lapse ratio among transient expatriates

Roughly 81% of expats still expect to retire abroad, prompting early surrenders when job contracts end. Lapses force insurers to amortise acquisition costs over shorter horizons, pressuring margins. Cash-value withdrawals also undermine long-term investment performance for remaining policyholders. Product portability and reduced surrender charges can ease attrition but require capital buffers. Enhanced employer portability through the 2025 pension law should gradually curb churn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Unit-Linked Momentum within a Guaranteed-Benefit Core

Whole Life retained a 36.12% slice of the UAE life and annuity insurance market revenue in 2025, favored for estate planning and straightforward guarantees. Unit-linked contracts, though smaller, are earmarked for 10.12% CAGR growth as affluent investors seek transparent fee structures and equity-style upside. The UAE life and annuity insurance market size for Unit-Linked solutions is forecast to widen markedly alongside capital-market sophistication and zero-tax investment compounding.

Investors increasingly blend protection with accumulation, prompting insurers to add global multi-asset funds and goal-based dashboards. Term Life fills pure-risk needs for cost-sensitive households, while Endowment plans answer education-funding gaps common among Indian and Filipino families. Competitive differentiation centers on digital valuation tools, multi-currency switches, and ESG fund links that resonate with younger professionals.

By Distribution Channel: Digital Gains, Bancassurance Persists

Bancassurance controlled 43.02% of premiums in 2025 through embedded cross-selling and payroll integration. Yet mobile apps and web aggregators will drive a 15.05% CAGR, lifting the direct slice of the UAE life and annuity insurance market share by 2031. Open-finance rules compel banks and insurers to share data, accelerating omnichannel experiences that combine biometric sign-in, instant underwriting, and robo-advice.

Large banks deepen wallet share with wealth portals offering insurance, funds, and structured notes in one view, while fintechs target niche segments with subscription-style micro-covers. Brokers pivot to high-touch advisory for complex expatriate portfolios, and tied agents upgrade to hybrid video-consult models.

By Premium Payment: Wealth Concentration Spurs Single-Premium Uptake

Regular Premium contracts still represent 69.35% of the UAE life and annuity insurance market size in 2025, mirroring salaried income streams and employer schemes. Single-Premium business, however, should notch 9.42% CAGR as bonuses, business exits, and property gains funnel lump sums into tax-efficient wrappers. Pension reform permits voluntary top-ups to 25% of salary, enriching periodic contribution flows without cannibalising one-off placements.

Affluent buyers favor single-pay whole-of-life cover for estate liquidity, taking advantage of the absence of inheritance tax. Mass retail relies on monthly deductions aligned to end-of-service gratuity funding, underscoring the duality of payment preferences.

By Customer Segment: Democratisation at the Base

HNW & Mass-Affluent clients commanded 41.55% of 2025 premium income, yet mass-market retail will expand 9.14% CAGR thanks to policy denominations as low as USD 27 per month on mobile apps. Gamified wellness riders and cashback incentives cater to digitally native users and mitigate persistency risk.

Group schemes for SMEs scale as mandatory pensions institutionalise employer funding, whereas micro-pension platforms ride telecom APIs to enrol lower-income expatriates in under two minutes. The UAE life and annuity insurance market thus widens from the top and bottom simultaneously.

Geography Analysis

Dubai’s concentration gives the UAE life and annuity insurance market a cosmopolitan pulse. Financial-services GDP, rising visitor numbers, and record USD 7.4 billion pre-tax profit at Emirates NBD in 2024 support investment-led policies and cross-selling through digital wealth platforms. DIFC passports enable carriers to tap cross-GCC demand from a single hub.

Abu Dhabi offers counter-cyclical ballast; government payrolls and sovereign wealth investments steady premium flows even when private-sector churn peaks. Voluntary end-of-service benefit funds approved by regulators unlock investment-linked policies for local and expatriate staff alike, diversifying away from lump-sum gratuities.

The Northern Emirates contribute an emerging volume. RAK Bank’s all-digital Takaful suite and Sharjah’s SME corridors enlarge the retail base. Tourism projects in Fujairah and Ajman import service workers who demand affordable protection, while federal pension rules guarantee consistent product frameworks nationwide.

Competitive Landscape

The UAE life and annuity insurance market features moderate fragmentation; roughly one-third of premium income is distributed among the five largest carriers, leaving room for mid-tier consolidation. Digital excellence is the litmus test: Sukoon won multiple innovation awards after rebranding, leveraging API-driven onboarding and portfolio analytics. Abu Dhabi National Insurance Company’s cross-border acquisition of a 51% stake in a Saudi carrier signals outward growth as domestic scale thresholds loom.

Islamic insurers outperform on profitability as Takaful resonates with cultural norms and attracts GCC cashflows. Dar Al Takaful’s merger with Watania formed a larger Sharia-focused entity able to negotiate reinsurance rates and invest in AI underwriting. Banks such as Emirates NBD exploit captive distribution and balance-sheet funding to embed life wrappers within discretionary portfolio management, while fintech aggregators intensify price transparency and churn pressure. Regulation accelerates change; the Central Bank’s open-finance framework obliges insurers to expose product and customer data via secure APIs, favouring players with robust cyber resilience and analytics teams. Telco collaborations for micro-pensions, wellness-linked cashback models, and cross-border portability features will separate innovators from laggards.

UAE Life and Annuity Insurance Industry Leaders

Orient Insurance

Abu Dhabi National Insurance Company

SALAMA

Emirates Insurance Company

Al Ain Ahlia Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sukoon Insurance finalized the purchase of Chubb’s UAE life portfolio, adding unit-linked and protection lines and integrating global digital standards.

- December 2024: Nexus Underwriting agreed to acquire Arma Underwriting, bolstering specialty reinsurance capabilities for life writers.

- November 2024: Emirates NBD launched “Next Generation” with INSEAD to prepare heirs for a USD 980 billion wealth transition, elevating estate-planning insurance needs.

- October 2024: Regulators deferred the life-insurance conduct regime to 16 Oct 2024, giving carriers extra compliance runway on disclosure, refund windows, and commission caps.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the study treats the UAE life & annuity insurance market as the total gross written premium (GWP) earned by licensed carriers on individual and group life policies plus immediate or deferred annuity contracts that guarantee income or death benefits. Savings-only products without mortality or longevity risk and pure-investment unit trusts are outside scope.

Scope exclusion: Group pension funds managed by asset managers rather than insurers are excluded.

Segmentation Overview

- By Insurance Type

- Term Life Insurance

- Whole Life Insurance

- Endowment Insurance

- Unit-Linked / Investment-Linked

- Annuity Insurance

- Other Types

- By Distribution Channel

- Bancassurance

- Insurance Brokers

- Agency Force

- Direct (Digital & Branch)

- Others

- By Premium Payment Type

- Regular Premium

- Single Premium

- By Customer Segment

- HNW & Mass-Affluent Individuals

- Mass-Market Retail

- SMEs & Group Life Schemes

- By Region

- Abu Dhabi

- Dubai

- Sharjah

- Ras Al Khaimah

Detailed Research Methodology and Data Validation

Primary Research

Interviews with actuaries, bancassurance heads, independent brokers, insurtech founders, and regulator advisers across Dubai, Abu Dhabi, and Sharjah helped us stress-test lapse rates, average ticket sizes, rider attach probabilities, and annuity appetite among expatriates and Emirati nationals. Their forward views on interest-rate paths and corporate pension reform filled data gaps and grounded our model assumptions.

Desk Research

Our analysts began with statutory filings and public dashboards from the UAE Central Bank-Insurance Sector, the Insurance Authority archive, Federal Competitiveness & Statistics Centre population tables, and Ministry of Economy national accounts. We then drew trend signals from Emirates Insurance Association yearbooks, OECD and IMF economic outlooks, as well as peer-reviewed studies on takaful uptake. Commercial insights were cross-checked through company 10-Ks, investor decks, and reputable media captured on Dow Jones Factiva; carrier financial splits were verified in D&B Hoovers.

These sources supplied historic premium pools, distribution-channel mixes, regulatory shifts, and macro inputs that anchor our base year. Many additional public and proprietary references supported validation and are available on request.

Market-Sizing & Forecasting

The size model starts with a top-down reconstruction of 2024 life-sector GWP reported by the regulator, subtracts non-life lines, and re-maps the remainder into our study segments. Select bottom-up checks, sampled policy volumes times average premium, plus carrier channel splits, are layered in to temper outliers. Key variables include premium density per capita, insurance penetration as a share of GDP, expatriate workforce growth, bancassurance share, prevailing five-year UAE bond yield, and sharia-compliant product mix. For forecasting, we employ a multivariate regression that links real GDP, population aging, and yield curve shifts with premium growth, supplemented by scenario analysis for pension-mandate adoption speed. Where company-level splits were incomplete, ratios from matched peers and primary interviews bridged the gaps.

Data Validation & Update Cycle

Outputs pass three rounds of variance checks: historical back-casting, peer comparison, and senior-analyst audit, before sign-off. Mordor's dashboards refresh annually, with interim edits whenever material events such as regulatory circulars, M&A, or tax changes occur; a final pre-publication sweep ensures clients always receive the newest baseline.

Why Mordor's UAE Life And Annuity Insurance Baseline Stands Firm

Published numbers often diverge because research houses pick different scopes, base years, exchange rates, and forecasting levers. We acknowledge these gaps upfront so decision-makers can see how each estimate was built.

Key gaps arise when other studies fold corporate pension assets into life premiums, deploy aggressive GDP multipliers, ignore lapse behavior, or convert currencies at spot rather than average annual rates, whereas Mordor aligns strictly with regulator-defined GWP and applies five-year moving-average FX.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.45 B (2025) | Mordor Intelligence | - |

| USD 14 B (2023) | Regional Consultancy A | Includes workplace savings plans and uses nominal GDP multiplier |

| USD 8 B (2023) | Trade Journal B | Counts earned premium, not written, and blends credit-life covers |

In sum, Mordor's disciplined scope selection, variable transparency, and annual refresh cadence deliver a balanced, reproducible baseline that executives can rely on for strategic planning.

Key Questions Answered in the Report

What is the 2026 size of the UAE life and annuity insurance market and its growth outlook?

The UAE life and annuity insurance market stands at USD 2.54 billion in 2026 and is projected to reach USD 3.02 billion by 2031, delivering a 3.53% CAGR.

How does the 2025 pension reform affect insurers?

Mandatory employer-employee contributions inject roughly USD 3.3 billion annually into long-term savings vehicles, directing stable cash flows to unit-linked and annuity products.

Why are digital channels expanding so quickly?

Smartphone penetration, open-finance APIs, and instant underwriting reduce onboarding time, enabling direct digital sales to grow at a 15.05% CAGR—far faster than traditional channels.

What advantages do Sharia-compliant products offer?

Takaful solutions align with Islamic principles, tap the GCC’s dominant share of global Sharia premiums, and benefit from tax-free investment growth in the UAE.

Page last updated on: