UAE Health Insurance Third Party Administrators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

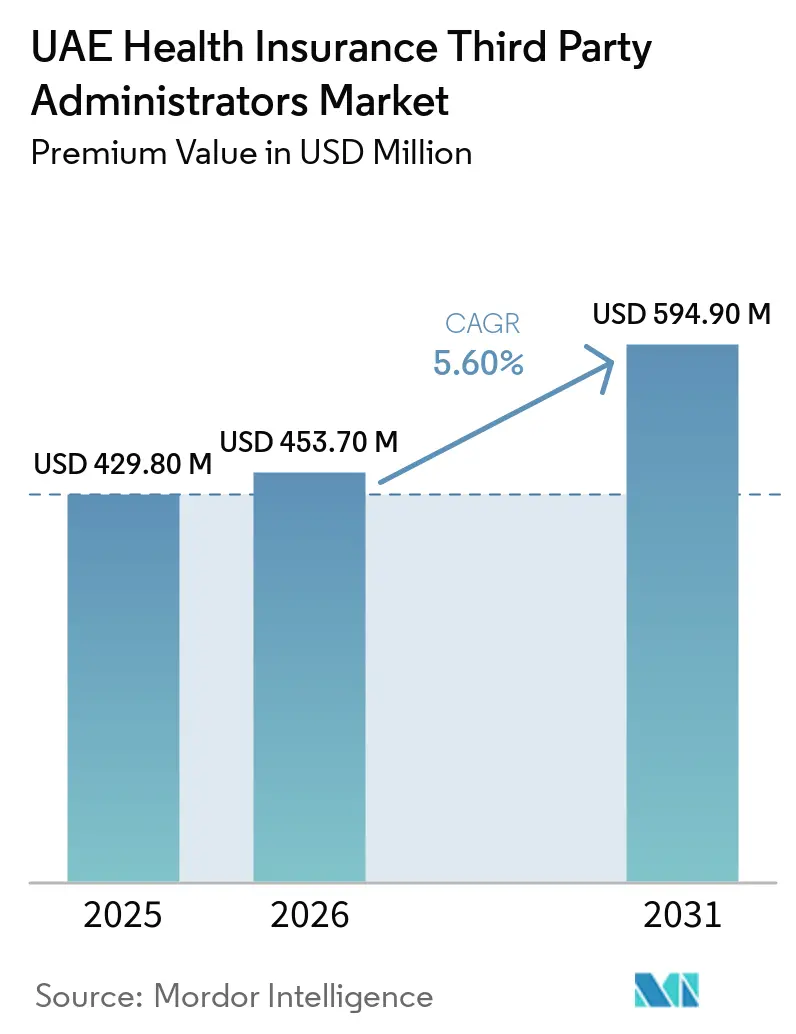

| Base Year Market Size (2025) | USD 429.80 Million |

| Market Size (2026) | USD 453.70 Million |

| Market Size (2031) | USD 594.90 Million |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

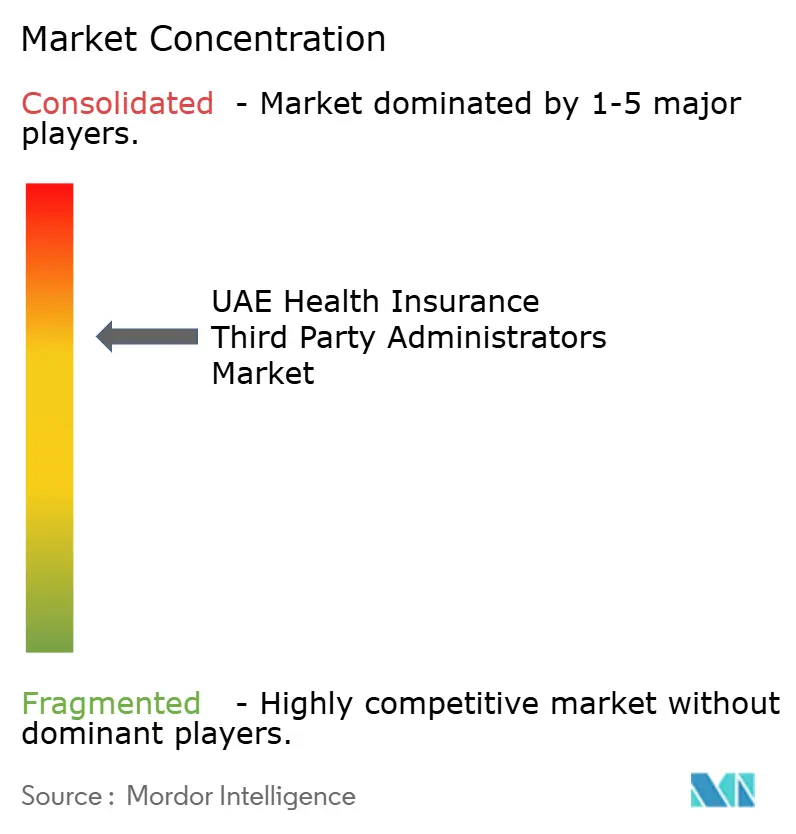

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Health Insurance Third Party Administrators Market Analysis by Mordor Intelligence

The UAE Health Insurance Third Party Administrators Market size in terms of premium value is projected to be USD 429.80 million in 2025, USD 453.70 million in 2026, and reach USD 594.90 million by 2031, growing at a CAGR of 5.60% from 2026 to 2031.

Enrollment growth tied to visa-linked coverage requirements in the Northern Emirates is adding newly insured lives and creating steady throughput for benefits administration across smaller employer segments. The reclassification of third-party administrators as licensed financial institutions has lifted compliance thresholds on capital, solvency, cybersecurity, and fraud reporting, which favors scaled operators with audited, certifiable platforms. Digital mandates in Dubai, coupled with interoperability efforts through Riayati and emirate health information exchanges, are compressing settlement timelines and rewarding automation-first workflows. Employers are shifting spend toward outcomes-based wellness and disease management to address the high prevalence of non-communicable conditions, which is pulling administrators into longitudinal care and analytics programs. As these forces converge, the UAE health insurance third-party administrators market is moving from transactional claims handling to integrated, value-adding administration that links fees to measurable health outcomes.

Key Report Takeaways

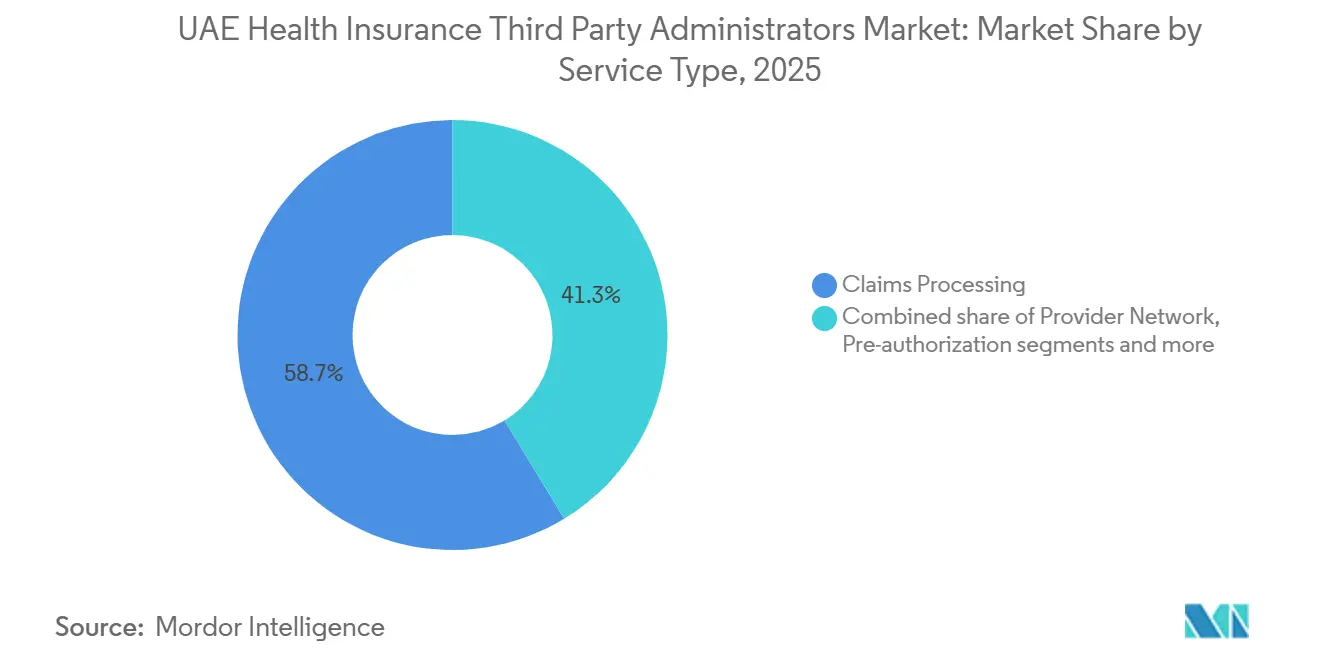

- By service type, Claims Processing held 58.7% of the UAE health insurance third-party administrators market in 2025; Wellness & Disease Management is forecast to advance at an 11.6% CAGR through 2031 in the UAE health insurance third-party administrators market.

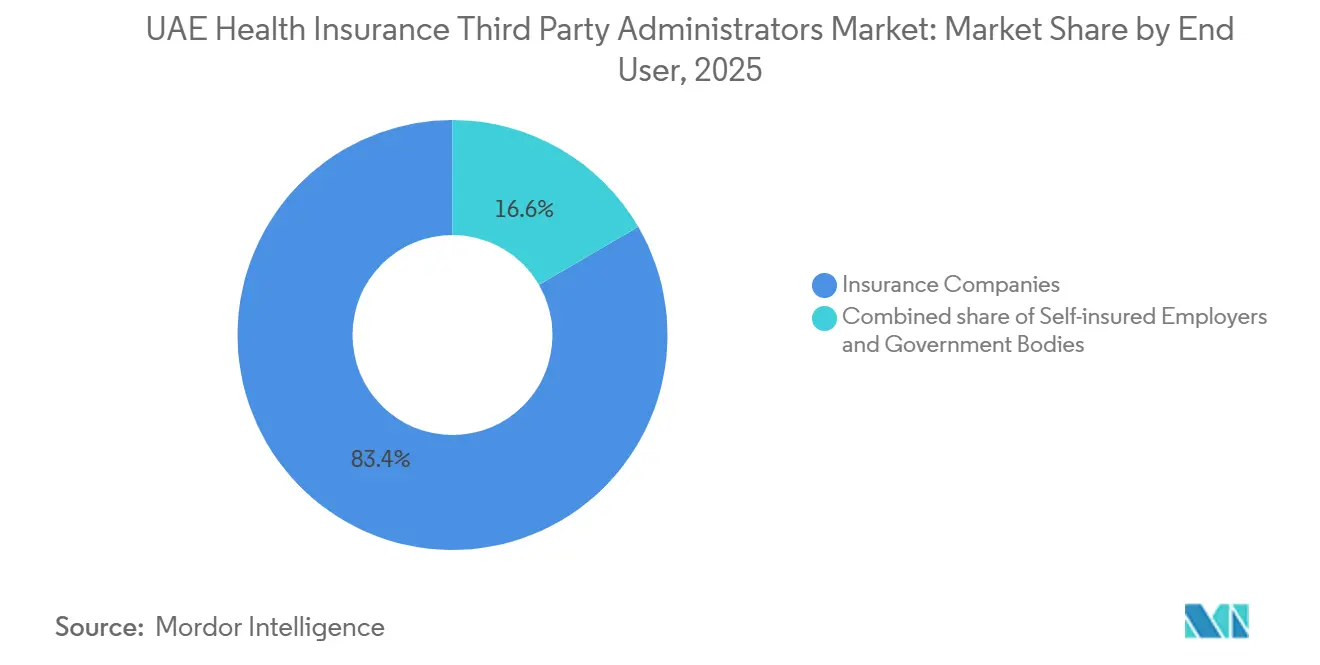

- By end user, Insurance Companies accounted for 83.3% of the UAE health insurance third-party administrators market in 2025; Self-insured Employers are expected to grow at a 9.74% CAGR to 2031 in the UAE health insurance third-party administrators market.

- By geography, Dubai led the UAE health insurance third-party administrators market with 49.7% revenue share in 2025; the Rest Emirates segment is projected to expand at a 13.9% CAGR to 2031 in the UAE health insurance third-party administrators market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Health Insurance Third Party Administrators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insurer-TPA portfolio consolidation | +0.8% | UAE-wide, concentrated in Dubai and Abu Dhabi with spillover to Northern Emirates | Medium term (2-4 years) |

| Employers shift to outcomes-based wellness | +1.2% | Global with early gains in Dubai, Abu Dhabi, and large private-sector hubs | Long term (≥ 4 years) |

| Growth in self-insured employers | +1.4% | Dubai, Abu Dhabi, Sharjah (free zones), national entities | Medium term (2-4 years) |

| Expansion of visa-linked mandatory coverage | +1.6% | Northern Emirates with federal coordination | Short term (≤ 2 years) |

| Benefit design complexity | +0.9% | Dubai and Abu Dhabi | Short term (≤ 2 years) |

| AI-enabled adjudication in payer RFPs | +1.1% | UAE-wide, led by tech-forward insurers and government payers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Insurer-TPA Portfolio Consolidation Post Major Mergers Increases Demand for Scaled Multi-Emirate Administration Partners

The legal reclassification of third-party administrators as licensed financial institutions has raised the bar on capital adequacy, solvency reporting, cybersecurity audits, and fraud monitoring across the sector. Insurers are responding by rationalizing vendor panels to reduce counterparty risk and by concentrating volumes with administrators that can provide uniform service quality across all emirates on a single technology stack. Connectivity to Dubai’s NABIDH, Abu Dhabi’s Malaffi, and the federal Riayati platform is now a baseline requirement for real-time decisions and post-acute care coordination in the UAE health insurance third-party administrators market[1]Dubai Health Authority, “Circulars,” Dubai Health Authority, services.dha.gov.ae. Scaled operators with audited information security and dedicated compliance functions are better positioned to meet these obligations at sustainable unit costs. Regional platforms that standardize claims engines and workflow rules across markets are increasingly favored in payer procurements focused on resilience and interoperability. This consolidation dynamic underpins a steady shift toward fewer, larger partners in the UAE health insurance third-party administrators market over the medium term.

Employers Shift to Outcomes-Based Wellness for NCDs Increases Demand for TPA Disease and Case Management

Population screening has identified meaningful burdens of pre-diabetes and hypertension, which are prompting employers to invest in early detection, adherence, and risk reduction programs at scale. Corporate leaders report that well-being investments are tied to productivity gains and reduced absence, which is strengthening demand for administrator-run disease management services and measurable outcomes reporting. Administrators are building nurse-led outreach, biometric screening, and digital engagement capabilities that close care gaps for diabetes and cardiovascular risk while integrating pharmacy and lab data for adherence tracking. The rollout of e-prescription requirements in Abu Dhabi further enables real-time medication reconciliation and supports interventions for non-adherence or duplication. Insurer-aligned platforms are expanding analytics and member-facing tools to link nudges and follow-ups to clinical outcomes in the UAE health insurance third-party administrators market. As fee models evolve, contracts increasingly recognize performance on disease control metrics alongside service-level delivery.

Growth in Self-Insured Employers and Quasi-Government Entities Outsourcing Administration to TPAs

Large enterprises and quasi-government sponsors are adopting self-insurance to gain direct visibility into claims data, configure benefits, and manage cost trends with targeted programs[2]Department of Health Abu Dhabi, “Shafafiya,” Department of Health Abu Dhabi, doh.gov.ae. These sponsors are selecting administrators for technology dashboards, real-time analytics, and the ability to run bespoke chronic disease interventions aligned with workforce profiles. Direct provider-administrator collaborations are expanding access to multi-specialty facilities and supporting preventive campaigns in workplace and community settings. In the UAE health insurance third-party administrators market, self-insured sponsors value granular reporting and rapid course corrections on formularies and referral paths that reduce avoidable utilization. Regulatory clarity on outsourcing administration to licensed entities underpins the model and reinforces the need for certified systems and auditability. Over time, this mix shift is raising demand for administrators who blend compliant operations with advanced clinical management.

Expansion and Enforcement of Visa-Linked Mandatory Coverage Expands Enrolled Base

The federal mandate now links proof of basic health insurance to residency permit issuance and renewal in Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah, which closes historical coverage gaps and accelerates enrollment. The mandated basic plan defines minimum inpatient, outpatient, and pharmacy benefits with specified copays and annual limits designed to balance access and affordability. Employers are adopting tiered offerings that combine compliance with optional upgrades, which increases eligibility and benefit-adjudication complexity for administrators. Administrators with robust enrollment, eligibility, and real-time claims engines are absorbing onboarding surges from newly insured populations in the UAE health insurance third-party administrators market. The enrollment wave also expands the use of primary care and diagnostics as previously uninsured members access care earlier in the disease course. These dynamics are expected to support stable volume growth over the near term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance overhead from PDPL and sectoral rules | -0.6% | UAE-wide with DHA, DoH, and MOHAP jurisdictions | Short term (≤ 2 years) |

| Tariff and base-rate focus on affordability | -0.9% | Northern Emirates, Abu Dhabi, and Dubai basic plans | Medium term (2-4 years) |

| Emirate-specific code-set timing | -0.4% | Dubai eClaimLink and Abu Dhabi Shafafiya | Short term (≤ 2 years) |

| Emergency settlement timelines and penalties | -0.5% | Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Compliance Overhead from PDPL and Sectoral Health-Data Rules; Limits to Offshoring Analytics

The UAE’s personal data protection framework and sectoral health data rules limit cross-border transfers of health information, which constrains offshoring options for analytics and adjudication. Distinct interoperability and exchange specifications for NABIDH, Malaffi, and Riayati add integration complexity that administrators must address in parallel. Administrators must maintain role-based access, security certifications, and detailed audit trails to meet supervision by financial and health regulators. The combined impact elevates fixed costs and places a premium on scaled, compliant infrastructure in the UAE health insurance third party administrators market. As rules evolve, administrators will need sustained investments in interoperability and governance to remain in good standing. These requirements make compliance a structural consideration in operating models and vendor selection.

Tariff and Base-Rate Focus on Affordability Compresses Admin Fees and Margins

The mandated basic plan in the Northern Emirates sets a low premium level and comprehensive minimum benefits, which constrains the administrative fee pool for insurers and their administrators. Abu Dhabi’s basic plan updates define copays and annual coverage limits that protect affordability and member access while anchoring plan pricing. Dubai’s electronic claims and settlement timelines increase discipline on working capital and reduce tolerance for manual cycles, intensifying the need for automation and first-pass accuracy. Administrators are investing in AI-enabled adjudication and coding QA to improve straight-through rates and cut rework in the UAE health insurance third party administrators market. Pharmacy digitization and standardization efforts in Abu Dhabi support better control of medication costs through safer substitutions and monitoring. The net effect is margin pressure for non-automated models and an advantage for platforms with robust digital capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Case Management Eclipses Transactional Processing

Claims Processing retained the largest share at 58.7% in 2025, reflecting the core role of high-volume adjudication even as fee pressure rises with stricter service levels and growing automation. The UAE health insurance third-party administrators' market share concentration in Claims Processing underscores the need for accurate, near real-time benefit decisions that align with Dubai and Abu Dhabi digital mandates. Utilization review and pre-authorization are expanding as plans introduce more nuanced network tiers and copay structures that require precise rule application at the point of service[3]Daman, “Health & Medical Insurance Plans,” Daman, damanhealth.ae. Administrators are deploying AI for coding QA and fraud detection to reduce denials and resubmissions in the UAE health insurance third-party administrators market. Wellness & Disease Management is the fastest-growing service at 11.6% CAGR to 2031, supported by employer demand to improve diabetes and hypertension outcomes tied to measurable KPIs. Companies are adding nurse-led outreach, workplace screenings, and digital nudges to drive adherence and risk reduction.

Corporate leaders cite productivity gains from wellbeing programs, which support sustained investment in disease management services delivered by administrators. Claims Processing remains essential but is absorbing continued unit-cost pressure as payers demand higher straight-through rates and faster authorization decisions. Leading platforms now emphasize auditable automation, integrated fraud analytics, and interoperability with emirate exchanges in the UAE health insurance third-party administrators industry. Administrators with diversified service portfolios and clinical capabilities are better positioned to offset pricing pressure in transactional processing. Over the forecast period, differentiation will center on measurable clinical value rather than only claims throughput in the UAE health insurance third-party administrators market.

By End User: Self-Insured Employers Disrupt Traditional Insurer Dominance

Insurance Companies accounted for 83.4% in 2025, reflecting deep relationships with administrators across expatriate and national coverage schemes and the breadth of insured populations under carrier programs. The UAE health insurance third-party administrators market share held by carriers is stable, yet enterprise sponsors are increasingly choosing self-insurance to gain transparency and control over benefit design and claims data. Self-insured Employers are the fastest-growing end user at a 9.7% CAGR to 2031, as vendors offer real-time dashboards and targeted disease programs aligned with workforce needs. Direct collaborations between healthcare providers and administrators have expanded access options, screenings, and patient education that support preventive care. Insurer-aligned administrators are also investing in automation to retain fully insured clients under tighter turnaround and coding standards in the UAE health insurance third-party administrators market. Regulatory expectations around solvency, cybersecurity, and fraud monitoring further elevate selection criteria toward well-capitalized, certified operators.

Sponsors seek administrators who provide near real-time cost analytics, predictive risk segmentation, and flexible plan levers that can be tuned mid-year. Government programs continue to shape volumes and service requirements, with Abu Dhabi’s basic plan updates reinforcing affordability while clarifying cost-sharing rules that administrators must apply accurately. In both fully insured and self-insured models, clinical management maturity is rising as a selection factor in RFPs across the UAE health insurance third-party administrators industry. Over the forecast period, performance-linked fees tied to disease control metrics are likely to gain a share of administrator compensation. This end-user mix shift reinforces the need for robust analytics and compliance in the UAE health insurance third-party administrators market.

Geography Analysis

Dubai and Abu Dhabi anchor the UAE health insurance third party administrators market, with Dubai’s 49.7% share in 2025 supported by digitized pre-authorization and claims, and Abu Dhabi’s model shaped by DRG-linked reimbursement that demands coding rigor. The Rest Emirates moved to mandatory coverage for private sector employees and domestic workers through a policy that ties insurance to visa issuance and renewal, which is expanding insured enrollment and utilization. These policy and infrastructure settings position administrators to handle greater transaction volumes while maintaining compliance with service timelines and data standards. In this environment, providers and administrators are aligning more tightly on accurate benefit displays and referral management to reduce member friction. The geographic mix now requires unified quality standards combined with local rules proficiency in the UAE health insurance third-party administrators market[4]Ministry of Health and Prevention, “Riayati,” MOHAP, mohap.gov.ae.

Abu Dhabi’s reimbursement modernization has increased the importance of licensed grouping and code-finding engines within administrator workflows, especially for day care procedures. Plan design updates have codified diagnostic and inpatient copays that must be applied with precision at intake and during claims adjudication. E-prescription requirements launched in 2026 are adding medication reconciliation checks that can prevent duplication and support adherence outreach. These steps reinforce a model that values accurate clinical documentation and coding integrity in the UAE health insurance third-party administrators market. For administrators, readiness depends on coders, clinical reviewers, and interoperable systems that can support near real-time decisions. As adoption matures, the operational gap with fee-for-service settings will narrow through standardized claim edits and transparent audit trails.

In Dubai, end-to-end electronic claims management is mandatory and tied to explicit authorization windows and settlement deadlines, which is compressing tolerance for manual cycles. Administrators must run accurate rules engines for eligibility, coding, and benefit application at intake to avoid penalties and research-heavy resubmissions. The Rest Emirates are moving toward more structured adjudication as coverage expands and systems adoption deepens. Federal exchange initiatives are gradually improving data continuity across emirates, which should reduce duplication and data reconciliation issues over time. Administrators with multi-emirate presence and standard operating protocols are best equipped to manage these transitions in the UAE health insurance third-party administrators market. This combination of policy enforcement and digital infrastructure will continue to shape geographic performance profiles through 2031.

Competitive Landscape

Competition is intensifying around automation, compliance maturity, and measurable clinical impact as payer tenders raise the weight of technology capabilities. Administrators backed by large insurers and regional platforms are deploying AI-enabled adjudication, coding QA, and fraud analytics that support faster turnaround and lower denial rates in the UAE health insurance third-party administrators market. Provider-administrator partnerships are broadening access while enabling preventive screening and patient education that support early intervention. Under the financial-sector regulatory umbrella, prudential and cybersecurity expectations are reinforcing the need for certified systems, transparent audit trails, and real-time fraud reporting. These forces are narrowing the field to well-capitalized operators that can meet technology and compliance thresholds sustainably. Over time, the UAE health insurance third-party administrators market will reward platforms that combine robust adjudication with outcome-focused disease management.

Insurer-led modernization is visible in digital transformation initiatives focused on eligibility, pre-authorization automation, and claims routing using cloud and machine learning capabilities. Administrators who demonstrate transparent AI audit trails, bias mitigation, and cybersecurity controls are scoring higher in tenders as payers elevate these criteria. Pharmacy digitization in Abu Dhabi and codified cost-sharing rules are driving common expectations for accuracy in benefit calculation and medication safety checks in the UAE health insurance third-party administrators market. Regional players are also relaunching and expanding their UAE operations with proprietary claims engines and member apps that enhance engagement. These moves indicate continued investment in platforms designed for volume growth without linear headcount increases. Over the forecast period, buyer selection will converge on administrators that can prove both operational excellence and patient outcome improvements.

Vertical integration is also under consideration as carriers weigh build-versus-buy strategies for core claim and authorization workflows. However, replicating the specialized compliance and multi-standard integration required across emirates raises cost and complexity, which supports the role of dedicated administrators in the UAE health insurance third-party administrators market. Partnerships between administrators and providers are likely to expand as sponsors seek value-based arrangements and measurable ROI from wellness and disease programs. As federal and emirate regulators continue to define digital and security baselines, administrators with audited controls and proven automation will hold a defensible position. The competitive center of gravity will remain with those that pair scalable technology with strong clinical governance.

UAE Health Insurance Third Party Administrators Industry Leaders

NEXtCARE Claims Management LLC

MedNet UAE

Neuron LLC

NAS Administration Services / NAS Neuron Health Services

Almadallah Healthcare Management FZ-LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Abu Dhabi Department of Health issued Circular USO/38/2026 on March 5, 2026, mandating implementation of the e-Prescription Platform for all healthcare facilities in the Emirate of Abu Dhabi, establishing digital infrastructure for prescriptions to enable real-time medication reconciliation and reduce polypharmacy risks.

- November 2025: Dubai Health Authority issued Directive PD-05-2025, effective November 16, 2025, mandating end-to-end electronic claims management through eClaimLink for all Dubai-regulated entities, imposing strict timelines for prior authorizations, claims settlement within 45 days, and levying daily delay fees for late settlements.

- November 2025: Department of Health Abu Dhabi issued Circular No. 2025/186 on September 26, 2025, announcing implementation of the Day Care DRGs System for reimbursement in the Emirate of Abu Dhabi effective November 1, 2025, following a shadow billing phase and requiring licensed DRG tools and technical upgrades.

- September 2025: Federal Decree-Law No. 6 of 2025 Regarding the Central Bank, Regulation of Financial Institutions and Activities, and Insurance Business became effective September 16, 2025, consolidating banking and insurance regulation under the Central Bank of the UAE and reclassifying third party administrators as licensed financial institutions subject to prudential and cybersecurity standards.

UAE Health Insurance Third Party Administrators Market Report Scope

Third-party administrators are the entities responsible for the processing of health insurance claims. TPAs facilitate insurance claim settlement by administrating tasks such as dealing with documents and settling hospital bills.

The UAE health insurance third-party administrator market is segmented by geography, including Dubai, Abu Dhabi, and Other Citiess.

The report offers market size and forecasts for the health insurance TPA in the UAE market in terms of revenue (USD) for all the above segments.

| Claims Processing |

| Provider Network Management |

| Pre-authorization & Utilization Review |

| Wellness & Disease Management |

| Insurance Companies |

| Self-insured Employers |

| Government Bodies |

| Dubai |

| Abu Dhabi |

| Rest (Sharjah, Ajman, UAQ, RAK, Fujairah) |

| By Service Type | Claims Processing |

| Provider Network Management | |

| Pre-authorization & Utilization Review | |

| Wellness & Disease Management | |

| By End User | Insurance Companies |

| Self-insured Employers | |

| Government Bodies | |

| By Emirate | Dubai |

| Abu Dhabi | |

| Rest (Sharjah, Ajman, UAQ, RAK, Fujairah) |

Key Questions Answered in the Report

What is the projected size and growth of the UAE health insurance third party administrators market to 2031?

The UAE health insurance third party administrators market size is set to rise from USD 453.7 billion in 2026 to USD 594.9 billion by 2031 at a 5.6% CAGR over 2026-2031.

Which service line is growing fastest in the UAE health insurance third party administrators market?

Wellness & Disease Management is the fastest-growing service at 11.6% CAGR to 2031, reflecting employer demand for measurable outcomes in diabetes and hypertension programs.

How are regulations shaping UAE health insurance third party administrators in 2026?

TPAs are licensed financial institutions under Federal Decree-Law No. 6 of 2025 and must meet solvency and cybersecurity standards, while Dubai mandates electronic claims with firm authorization and settlement timelines.

Which end user is expanding fastest in the UAE health insurance third party administrators market?

Self-insured Employers are the fastest-growing end user at a 9.7% CAGR as sponsors seek transparent, data-rich administration and customized chronic care programs.

What geographic trend most affects administrators in the UAE?

The Rest Emirates are the fastest-growing geography at a 13.9% CAGR through 2031 due to the federal linkage of insurance to visa issuance and renewal.

Which technologies are prioritized in administrator tenders?

Payer RFPs favor AI-enabled adjudication, coding QA, fraud analytics, and interoperable systems with audit-ready controls across DHA and DoH requirements.

Page last updated on: