Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

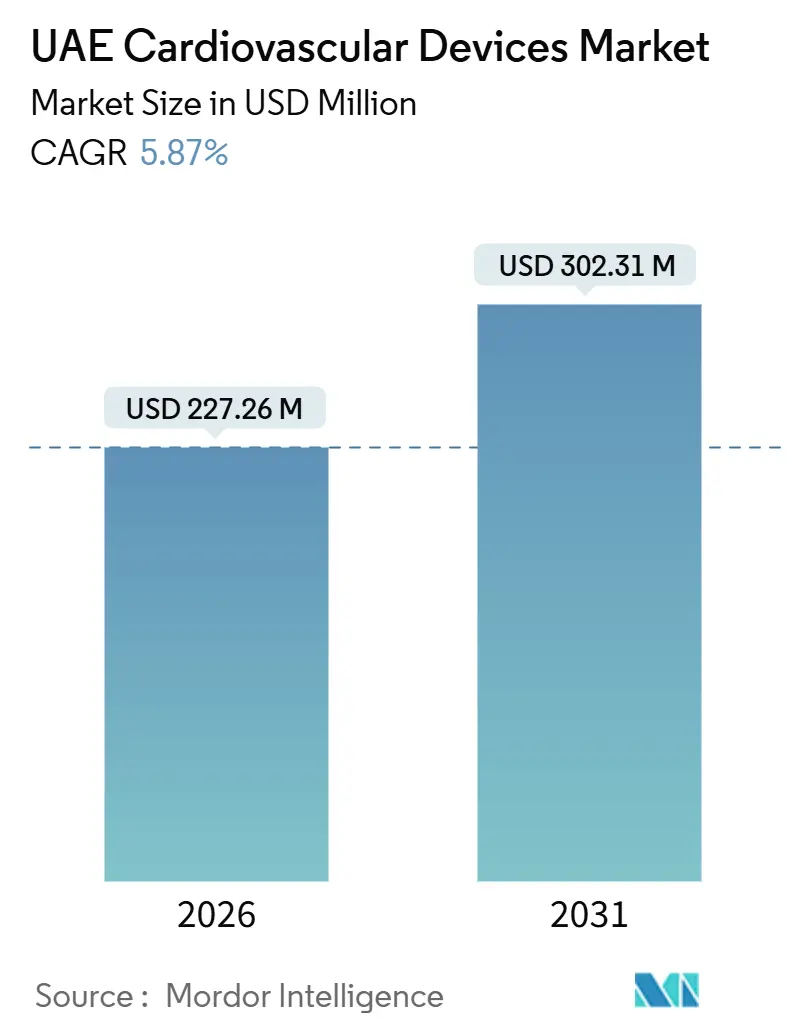

| Market Size (2026) | USD 227.26 Million |

| Market Size (2031) | USD 302.31 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

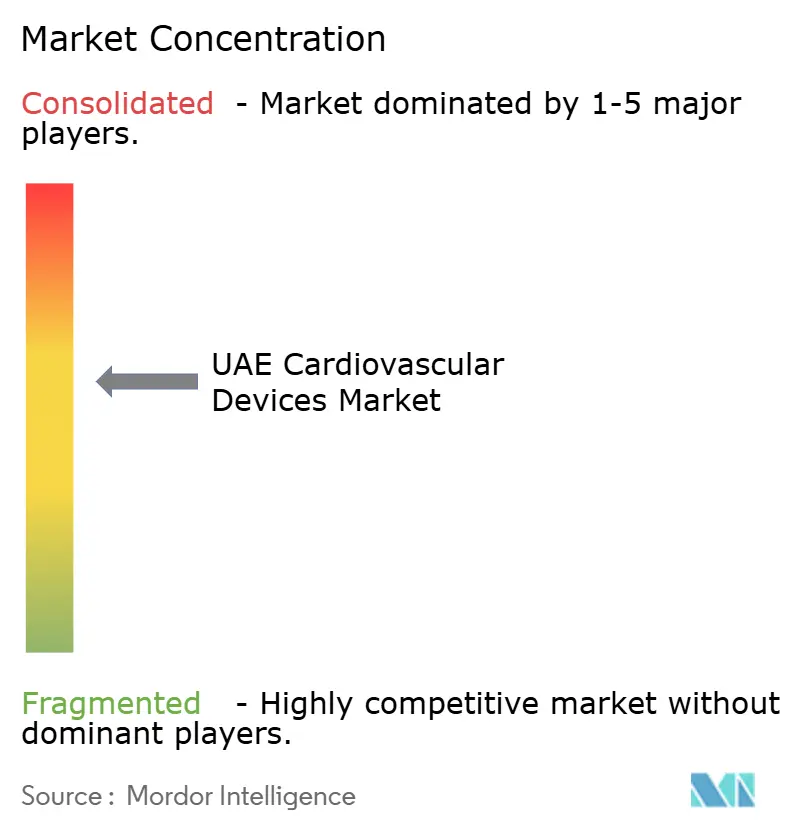

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Cardiovascular Devices Market Analysis by Mordor Intelligence

The UAE Cardiovascular Devices Market size is estimated at USD 227.26 million in 2026, and is expected to reach USD 302.31 million by 2031, at a CAGR of 5.87% during the forecast period (2026-2031).

Demand expands because cardiovascular disease causes 34% of all deaths in the federation. In comparison, federal reforms now allow 100% foreign ownership and encourage multinational manufacturers to base Gulf operations in Dubai and Abu Dhabi free zones. Transcatheter procedures shorten hospital stays, remote monitoring pilots shift follow-up care to patients’ homes, and medical tourism channels 691,478 visitors into premium cardiac programs, all of which reinforce equipment turnover in catheterization labs and electrophysiology suites. Manufacturers respond by coupling implants with cloud subscriptions that align with payers’ readmission-reduction incentives and by localizing assembly to trim logistics costs and qualify for “Made in the UAE” procurement preferences. Together, these elements sustain healthy pricing power and encourage the rapid rollout of novel technologies, such as pulsed-field ablation systems and leadless dual-chamber pacemakers, underpinning the long-term growth of the UAE cardiovascular devices market.

Key Report Takeaways

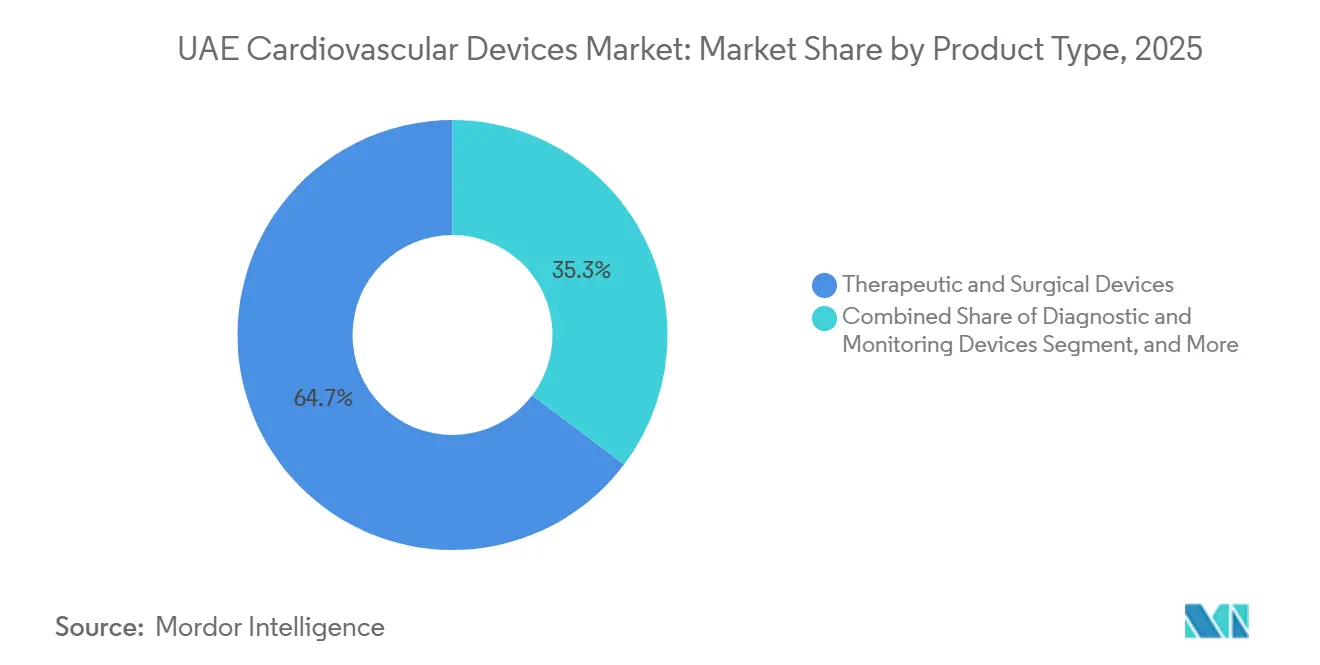

- By product type, therapeutic & surgical devices led the UAE cardiovascular devices market with a 64.71% share in 2025, whereas diagnostic and monitoring devices recorded the fastest growth, at a 6.62% CAGR through 2031.

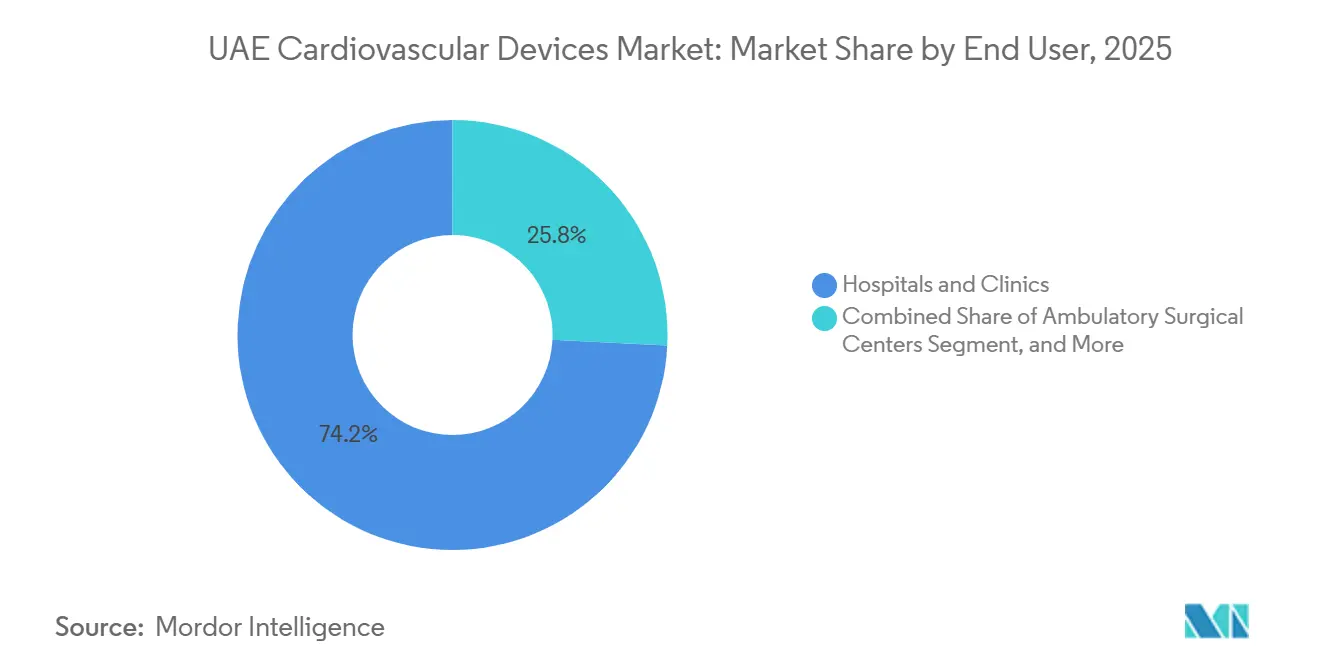

- By end user, hospitals and clinics accounted for 74.23% of revenue in 2025; ambulatory surgical centers are projected to advance at an 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CVD Prevalence and Comorbidities | +1.5% | National, strongest in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| Surge in Minimally Invasive Procedures | +1.3% | National, concentrated in tertiary hospitals | Medium term (2-4 years) |

| Government Investment and Medical Tourism | +1.0% | Dubai and Abu Dhabi, spill-over to Sharjah | Medium term (2-4 years) |

| Import-Friendly Ecosystem for Global Majors | +0.8% | National | Short term (≤ 2 years) |

| Remote AI-Based Cardiac Monitoring Pilots | +0.7% | National, pilot phase in MOHAP facilities | Long term (≥ 4 years) |

| Foreign-Ownership Reform and Assembly Hubs | +0.6% | Dubai and Abu Dhabi free zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising CVD Prevalence and Comorbidities

Cardiovascular disease claims 34% of all deaths and 70% of non-communicable disease mortality, magnified by obesity, hypertension, diabetes, and physical inactivity among residents.[1]World Health Organization, “UAE Health Profile,” who.int Mandatory annual cardiovascular screening for citizens over 40 will result in approximately half a million additional electrocardiograms, Holter monitors, and echocardiograms being incorporated into health-system workflows by 2028. The policy encourages hospitals to expand their diagnostic fleets while vendors bundle remote-monitoring services with implantable loop recorders, shifting revenue toward recurring software streams. Employers also fund workplace screening campaigns that rely on portable ultrasound and handheld electrocardiogram devices. These moves embed early-detection technology into primary care, broadening the user base and creating durable tailwinds for the UAE cardiovascular devices market.

Surge in Minimally Invasive Procedures and Device Innovation

Cleveland Clinic Abu Dhabi surpassed 500 transcatheter aortic valve implantations, underscoring a national shift from open surgery to percutaneous intervention. Boston Scientific’s FARAPULSE pulsed-field ablation reduces atrial-fibrillation procedure time by 40% and frees cath-lab schedules for additional cases.[2]Boston Scientific, “FARAPULSE Pulsed Field Ablation System,” bostonscientific.com Edwards Lifesciences’ SAPIEN 3 Ultra RESILIA valve extends durability to about 15 years, encouraging use in younger cohorts. These advances reshape care pathways, reduce the length of stay, and increase throughput, thereby reinforcing equipment demand. Local manufacturing targets in the Dubai Industrial Strategy 2030 further quicken adoption by shortening supply chains and assuring hospitals of consistent inventory. Altogether, minimally invasive innovation accelerates procedure volumes and drives premium mix for the UAE cardiovascular devices market.

Government Investment and Medical Tourism Positioning

Public-private partnerships have added three catheterization labs and two hybrid operating rooms since 2024, as authorities seek to offset an anticipated deficit in cardiology beds.[3]Dubai Health Authority, “Essential Benefit Plan,” dha.gov.ae Medical tourism visas on arrival now cover 87 countries, attracting international patients who generate a higher average revenue per case, particularly for structural heart and ventricular assist device procedures. Cleveland Clinic Abu Dhabi registers a 22% annual increase in referrals from Central Asia and East Africa, cementing the city as the Gulf’s hub for structural heart care. Hospitals leverage this influx to justify capital expenditure on advanced imaging and hybrid suites. Manufacturers use high-profile centers to showcase new technology before broader Middle East release, further energizing the UAE cardiovascular devices market.

Import-Friendly Ecosystem for Global Majors

MOHAP clears devices that hold FDA or CE approvals within about 45 days, a timeline that favors multinational firms with complete regulatory dossiers. Abbott, Medtronic, Boston Scientific, and Edwards Lifesciences operate wholly owned subsidiaries in Dubai Healthcare City and Jebel Ali Free Zone, bypassing traditional distributor markups and securing sole-source contracts with government hospitals. The consolidated pathway lowers market-entry costs and accelerates product cycles, sustaining technological leadership. Centralized regulation under the new Emirates Drug Establishment harmonizes UAE rules with Gulf Cooperation Council standards, which streamlines regional expansion. This predictable environment supports steady inflows of innovative products and anchors growth in the UAE cardiovascular devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Approvals and High Procedure Costs | -0.5% | National | Short term (≤ 2 years) |

| Shortage of TAVR and EP Specialists | -0.4% | National, acute in Northern Emirates | Medium term (2-4 years) |

| Insurance Caps Limiting Expatriate Access | -0.3% | Dubai and Abu Dhabi | Medium term (2-4 years) |

| Distributor Oligopoly and Opaque Tenders | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Approvals and High Procedure Costs

Device registration requires clinical-trial evidence, post-market plans, and Arabic labeling, demands that stretch smaller innovators without dedicated regulatory teams. The Essential Benefit Plan caps coverage at AED 150,000, leaving expatriates to self-fund implants, such as left ventricular assist devices, which cost USD 80,000 to USD 120,000. The Department of Health tariffs reimburse hospitals AED 45,000 for single-chamber pacemakers and AED 65,000 for dual-chamber systems. This spread is insufficient to offset the 20% price premium of MRI-conditional or leadless devices. Co-pays under the Basic Health Insurance Scheme reach 20%, pushing out-of-pocket costs above AED 13,000 for a TAVR case. These factors constrain demand for complex devices and temper the growth trajectory of the UAE cardiovascular devices market.

Shortage of TAVR and EP Specialists and Cath-Lab Capacity

The Unified Professional Qualification Requirements 2025 require interventional cardiologists to log 250 supervised percutaneous coronary interventions and 50 structural-heart procedures before practicing independently, reducing the eligible provider pool by approximately 30%. Fellowship programs at the Cleveland Clinic Abu Dhabi and the Mohammed Bin Rashid University graduate only around 10 interventional cardiologists each year, well below the estimated needs. Cath-lab utilization exceeds 90% in high-volume centers, leaving little buffer for emergent or elective structural-heart work. The resulting backlog slows adoption of devices like pulsed-field ablation systems and leadless dual-chamber pacemakers because electrophysiologists cannot maintain procedural competence. This supply-side bottleneck restrains the UAE cardiovascular devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Devices Lead, Diagnostics Accelerate

Therapeutic & Surgical Devices captured 64.71% of revenue in 2025, driven by an installed base of pacemakers, implantable cardioverter-defibrillators, and cardiac resynchronization systems that require periodic replacement, serving as a dependable engine for the UAE's cardiovascular devices market share. Diagnostic & Monitoring Devices, on the other hand, will expand at a 6.62% CAGR through 2031, thanks to remote monitoring pilots that have enrolled more than 15,000 patients, as well as mandatory annual screening for residents over 40. Within therapeutic devices, cardiac rhythm management dominates, as Cleveland Clinic Abu Dhabi implanted the country’s first leadless dual-chamber pacemaker in 2024, signaling a transition away from transvenous leads that can fracture or become infected. Catheters of all types are experiencing a surge in procedural growth; Al Qassimi Hospital alone logged 1,312 catheterizations in the first half of 2024. Drug-eluting balloon catheters are gaining a share in below-the-knee disease that once required stents.

Cardiac assist devices remain niche because transplant-related implants fall outside basic insurance, limiting volumes to a small group of well-insured Emiratis and medical tourists. Grafts serve open-heart cases that plateau as transcatheter options migrate into intermediate-risk cohorts. Diagnostic momentum, by contrast, stems from three forces. First, GE HealthCare’s USD 5,000 Vscan Air SL probe democratizes point-of-care ultrasound in family medicine clinics. Second, Mediclinic Middle East reduced heart-failure readmissions by 18% after integrating implantable cardioverter-defibrillator telemetry with Huma’s digital platform, demonstrating the value of continuous monitoring. Third, preoperative clearance protocols require electrocardiograms and echocardiograms, thereby integrating diagnostic workflows into routine surgical preparation. Taken together, diagnostics are accelerating faster than therapy volumes, thereby increasing the UAE cardiovascular devices market size for this category.

By End User: Hospitals Dominate, ASCs Surge

Hospitals & clinics owned 74.23% of spending in 2025 because high-acuity procedures, such as transcatheter aortic valve replacement and left ventricular assist device implantation, require intensive care backup and round-the-clock cath lab access. Ambulatory surgical centers are expected to grow at an 8.19% CAGR through 2031, driven by day-case surgery targets that reimburse outpatient pacemaker implants at 85% of the inpatient tariff, as well as by devices that do not require complex fluoroscopy. Diagnostic Centers scale in line with preventive screening but cede ground as hospitals bring imaging in-house to capture downstream interventions. Home Healthcare settings remain small yet important; Cleveland Clinic Abu Dhabi’s nightly remote interrogation service detects battery depletion six months earlier than office checks, delaying replacements and saving cost.

Hospitals retain primacy because only 45 catheterization labs serve the entire federation, a capacity limit that sustains high device prices and concentrates procurement among a handful of buyers. Ambulatory surgical centers thrive as leadless pacemakers and subcutaneous defibrillators reduce procedure time to under 30 minutes, enabling same-day discharge and lowering facility overhead. Boston Scientific’s WATCHMAN FLX Pro lets electrophysiologists close the left atrial appendage under conscious sedation, well-suited to an outpatient suite. Diagnostic Centers face price competition from Chinese ultrasound vendors that offer CE-marked systems at steep discounts, prompting some operators to focus on cardiac CT and nuclear studies where reimbursement remains stronger. Remote monitoring will become viable at scale once HL7 FHIR interoperability rules take effect, unlocking insurer reimbursement and lifting uptake across the UAE cardiovascular devices market.

Geography Analysis

Abu Dhabi and Dubai account for a significant share of sales in the UAE cardiovascular devices market, owing to their concentration of tertiary healthcare centers, employer-funded insurance, and robust medical tourism infrastructure. Cleveland Clinic Abu Dhabi has performed over 500 transcatheter valve implants. It conducts a high volume of heart transplants, attracting referrals from Oman, Kuwait, and East Africa that sustain premium device demand. Dubai Healthcare City welcomes 691,478 medical tourists who spend AED 1.03 billion on care, with a significant portion of this expenditure focused on cardiac surgery and catheterization, thereby boosting the utilization of imaging systems and disposables. Visa-on-arrival rules for 87 countries shorten booking cycles and fortify international case flow.

Al Qassimi Hospital performed 106 open-heart operations and 1,312 catheterizations in the first half of 2024, solidifying Sharjah as a secondary hub. Nonetheless, specialist shortages slow the diffusion of novel devices; the Professional Qualification Requirements reduce the pool of eligible interventional cardiologists, and fellowship programs graduate only about 10 per year. Consequently, advanced devices like pulsed-field ablation systems reach these emirates two to three years after debuting in Abu Dhabi and Dubai.

Federal Decree-Law No. 26 of 2020 draws manufacturers to free-zone facilities near Jebel Ali Port, where packaging and sterilization shorten supply lead times by 10 days. The Dubai Industrial Strategy 2030 allocates AED 25 billion to advanced manufacturing, and cardiac devices qualify for preferential procurement when labeled “Made in the UAE”. Local production not only meets domestic demand but also positions the UAE as a re-export gateway to Saudi Arabia, Oman, and Bahrain, thereby extending the influence of the UAE's cardiovascular devices market across the wider Gulf Cooperation Council.

Competitive Landscape

Abbott, Medtronic, Boston Scientific, and Edwards Lifesciences collectively hold a significant share of the UAE cardiovascular devices market through direct subsidiaries that secure exclusive tenders with government networks. Their strategy hinges on long-term supply agreements with volume centers such as the Cleveland Clinic Abu Dhabi, which relies on consistent deliveries for its high case load. They also embed proprietary data platforms; GE HealthCare’s Vscan Air SL links handheld ultrasound to cloud analytics, making cardiologists reluctant to switch brands after integration.

Local distributors, including Al Naghi Medical, Atlas Medical, and Advanced Healthcare, continue to influence purchasing in private hospitals through bundled service contracts, but face erosion as foreign ownership reform permits manufacturers to bypass intermediaries. Price pressure arises from Chinese firms offering CE-marked electrocardiogram systems at 40% discounts, which appeals to budget-constrained institutions in the Northern Emirates. Yet government tenders favor brands with local clinical evidence and service footprints, slowing disruptive entry.

White-space opportunities cluster in remote monitoring, leadless pacemakers, and pulsed-field ablation. Mediclinic Middle East’s Huma pilot shows measurable savings but remains limited to one network, leaving 170 hospitals without a comparable platform. Dual-chamber leadless pacemakers eliminate the risk of lead fracture, yet their adoption lags because qualification rules restrict the number of trained implanters. Pulsed-field ablation trims procedure time by 40% yet requires manufacturer-certified training, which is bottlenecked by limited fellowship capacity. Companies that solve training or reimbursement gaps stand to capture share in the UAE cardiovascular devices market.

UAE Cardiovascular Devices Industry Leaders

Abbott Laboratories

Advanced Healthcare LLC

GE Healthcare

Al Naghi Medical Co.

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Dubai Health Authority approved Boston Scientific’s PulseSelect pulsed-field ablation system, enabling atrial-fibrillation treatment with microsecond energy bursts that spare collateral tissue.

- January 2025: Emirates Health Services initiated an artificial-heart program to implant total artificial hearts as bridge-to-transplant therapy, addressing organ-donor shortages.

- December 2024: Al Qassimi Hospital implanted the UAE’s first Fantom Encore bioabsorbable coronary stent that dissolves in three years, mitigating late thrombosis risk.

- August 2024: Abbott launched the FreeStyle Libre 3 glucose monitor in the UAE, integrating real-time data into cardiovascular care pathways for diabetic patients undergoing interventions.

UAE Cardiovascular Devices Market Report Scope

As per the report's scope, cardiovascular devices are utilized to treat cardiovascular ailments that incorporate various issues. The UAE cardiovascular devices market is segmented by device type (diagnostic and monitoring devices (electrocardiogram (ECG), remote cardiac monitoring, and other diagnostic and monitoring devices) and therapeutic and surgical devices (cardiac assist devices, cardiac rhythm management devices, catheters, grafts, heart valves, stents, and other therapeutic and surgical devices). The report offers the value (USD million) for all the above segments.

By Product Type

| Diagnostic & Monitoring Devices | Electrocardiogram |

| Remote Cardiac Monitoring | |

| Other Diagnostic & Monitoring Devices | |

| Therapeutic & Surgical Devices | Cardiac Assist Devices |

| Cardiac Rhythm Management Devices | |

| Catheters | |

| Grafts | |

| Other Therapeutic & Surgical Devices |

By End User

| Hospitals & Clinics |

| Diagnostic Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| By Product Type | Diagnostic & Monitoring Devices | Electrocardiogram |

| Remote Cardiac Monitoring | ||

| Other Diagnostic & Monitoring Devices | ||

| Therapeutic & Surgical Devices | Cardiac Assist Devices | |

| Cardiac Rhythm Management Devices | ||

| Catheters | ||

| Grafts | ||

| Other Therapeutic & Surgical Devices | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Centers | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare Settings | ||

Key Questions Answered in the Report

What is the projected value of the UAE cardiovascular devices market in 2031?

The market is forecast to reach USD 302.31 million by 2031.

Which device category is growing fastest in the UAE?

Diagnostic & monitoring devices are advancing at a 6.62% CAGR, outperforming therapeutic segments.

Which end-user segment is expanding quickest?

Ambulatory surgical centers are experiencing an 8.19% CAGR as day-case cardiac procedures increase.

How are regulatory reforms affecting manufacturers?

Federal Decree-Law No. 26 of 2020 allows 100% foreign ownership, enabling global firms to open UAE subsidiaries and local assembly hubs.

What limits access to high-cost cardiac implants for expatriates?

Basic insurance caps annual benefits at AED 150,000 and excludes devices like ventricular-assist systems, leading to significant out-of-pocket expenses.

Page last updated on: