Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

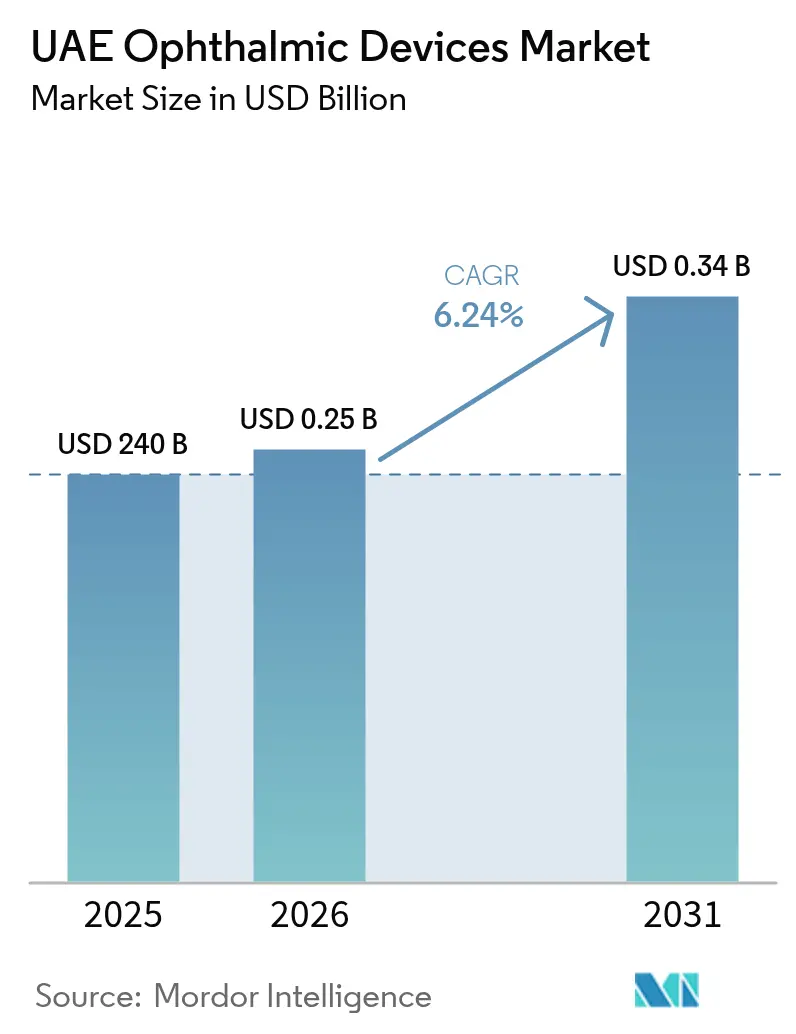

| Base Year Market Size (2025) | USD 240 Billion |

| Market Size (2026) | USD 0.25 Billion |

| Market Size (2031) | USD 0.34 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Ophthalmic Devices Market Analysis by Mordor Intelligence

UAE ophthalmic devices market size in 2026 is estimated at USD 254.98 million, growing from 2025 value of USD 240 million with 2031 projections showing USD 344.9 million, growing at 6.24% CAGR over 2026-2031. Sustained demand arises from the country’s high diabetes prevalence, mandatory vision-screening regulations, and the government’s commitment to AI-enabled eye-care programs. Vision-care products—spectacles, contact lenses, and related accessories—retain the largest revenue pool, while diagnostic systems such as fundus cameras and OCT scanners post the fastest unit growth. Hospitals continue to underwrite capital-intensive purchases, but ambulatory surgery centers (ASCs) are attracting fresh device installations as cataract and refractive procedures shift to day-care settings. International manufacturers deepen their regional presence through partnerships with Emirati hospital groups, using Dubai and Abu Dhabi as launchpads for premium innovations.

Key Report Takeaways

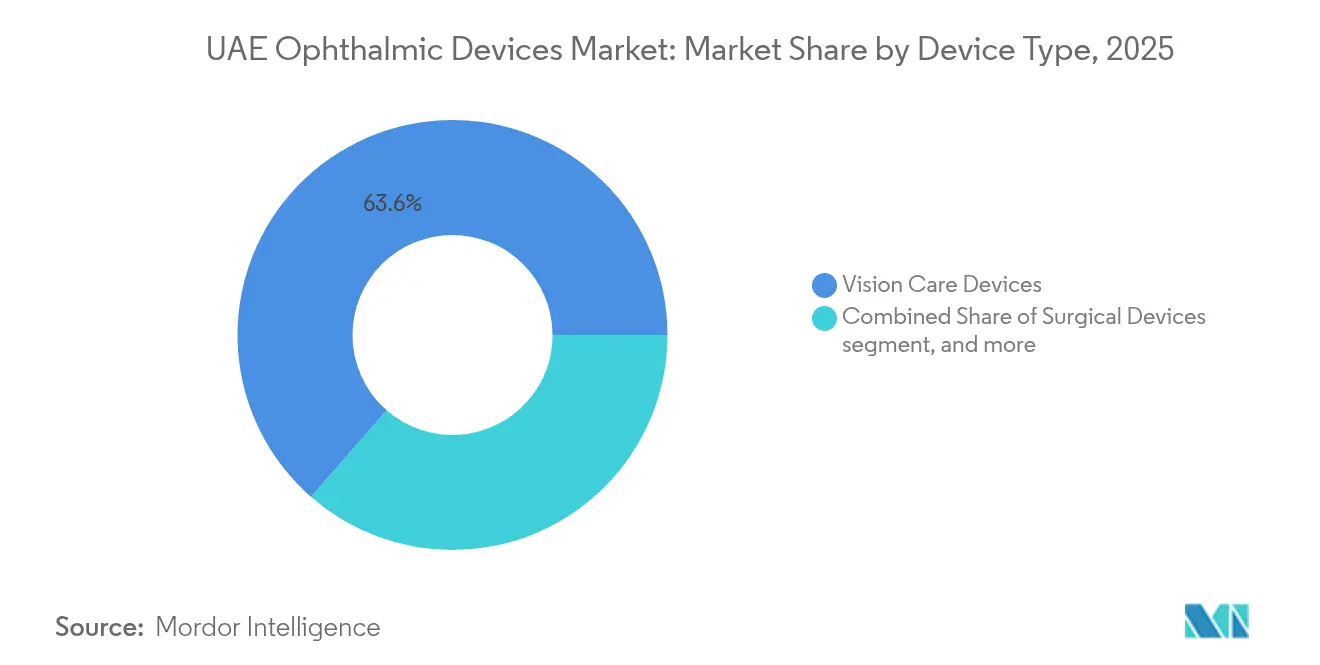

- By device type, vision-care products held 63.58% of the UAE ophthalmic devices market share in 2025; diagnostic and monitoring systems are expanding at an 8.42% CAGR to 2031.

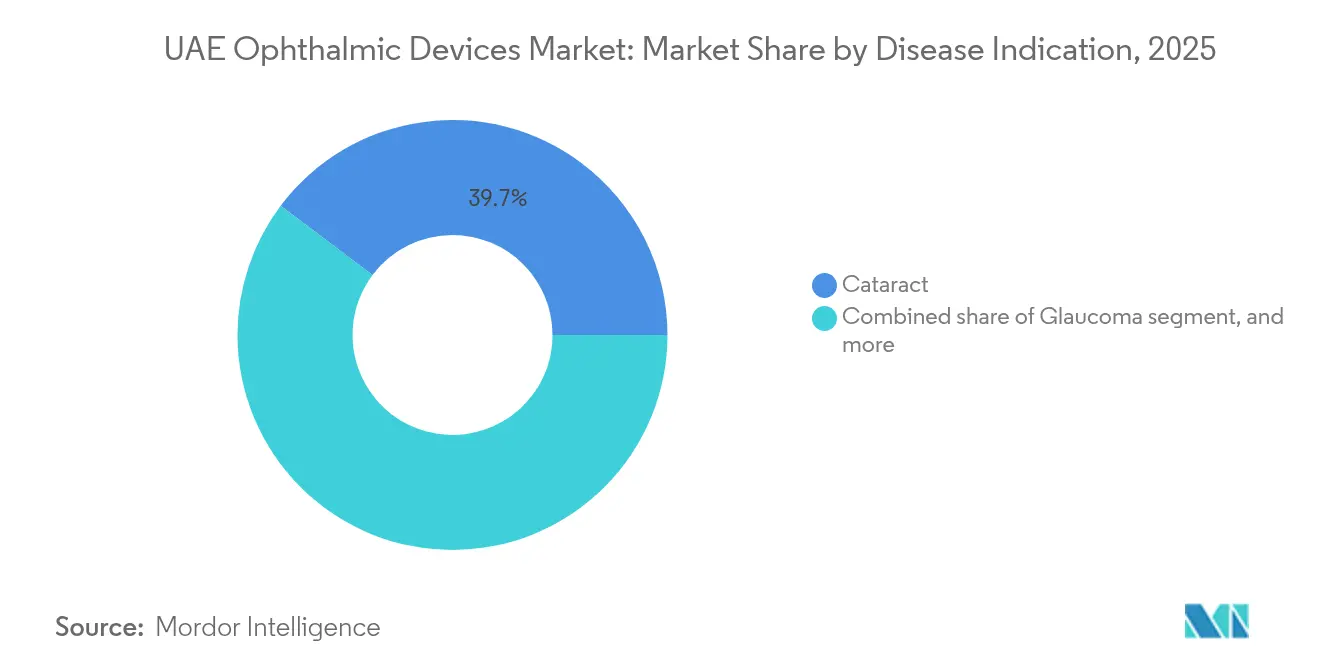

- By disease indication, cataract accounted for a 39.74% slice of the UAE ophthalmic devices market size in 2025, whereas diabetic retinopathy cases are climbing at a 7.63% CAGR through 2031.

- By end-user, hospitals dominated with 41.86% revenue in 2025, while ASCs represent the fastest-growing setting at a 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes-linked retinopathy in Emirati population | +1.5% | Abu Dhabi & Dubai concentration | Long term (≥ 4 years) |

| Mandatory periodic vision screening for driving-license renewals | +1.2% | Nationwide | Medium term (2-4 years) |

| Medical-tourism initiatives boosting premium eye-care demand | +0.9% | Dubai & Abu Dhabi | Medium term (2-4 years) |

| Surge in femto-laser cataract procedures at day-surgery centers | +0.7% | Urban hubs (Dubai & Abu Dhabi) | Short term (≤ 2 years) |

| Government-funded AI & tele-ophthalmology pilots | +0.6% | Pilots in Abu Dhabi; national rollout | Medium term (2-4 years) |

| Expansion of vision insurance (Thiqa, Dubai mandatory plans) | +0.5% | Nationwide, stronger in Dubai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes-Linked Retinopathy in Emirati Population

A 19% diabetes rate among UAE adults pushes demand for early retinal screening as payers and providers race to curb vision loss[1]American Academy of Ophthalmology, “Global Burden of Eye Diseases,” aao.org. National AI screening programs accelerate fundus analysis from half an hour to three minutes, spurring orders for OCT and ultra-wide field cameras that integrate seamlessly with cloud-based algorithms.

Mandatory Periodic Vision Screening for Driving License Renewals

All emirates require eyesight checks at each license renewal, creating a continuous flow of patients to optical centers. Dubai Health Authority’s 2025 standards specify autorefractors, keratometers, and slit-lamp biomicroscopes as mandatory equipment, reinforcing baseline demand for entry-level diagnostics[2]Dubai Health Authority, “Investment Guide 2024,” dha.gov.ae.

Medical-Tourism Initiatives Boosting Premium Eye-Care Demand

Dubai registered double-digit growth in inbound patients for refractive and cataract surgery in 2024, with Cleveland Clinic Abu Dhabi noting a 35% jump in international volumes[3]Cleveland Clinic Abu Dhabi, “Medical Tourism Statistics 2024, clevelandclinicabudhabi.ae. Hospitals are lining up femtosecond lasers and trifocal IOLs to meet expectations of overseas clientele seeking same-day discharge.

Surge in Femto-Laser Cataract Procedures at Day-Surgery Centers

Outpatient cataract programs reduce phaco energy by 35% and incision variability by 28%, allowing ASCs to cut chair time and improve throughput. Device makers highlight smaller footprints and faster setup to suit multi-theatre ambulatory hubs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced OCT & femto lasers | –0.8% | Strongest in smaller emirates | Short term (≤ 2 years) |

| Shortage of fellowship-trained ophthalmic surgeons outside tier-1 cities | –0.6% | Northern emirates | Medium term (2-4 years) |

| Import tariff & registration delays for new devices | –0.4% | Nationwide | Short term (≤ 2 years) |

| Safety concerns over low-cost IOL failures | –0.3% | Nationwide, higher in price-sensitive clinics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced OCT & Femto Lasers

Initial price tags ranging from USD 300,000 to USD 500,000 strain clinic budgets, especially outside Dubai and Abu Dhabi where average surgical volumes are lower. Financing programs from manufacturers soften cash-flow pressures but do not erase maintenance overheads that remain close to 10% of equipment value annually.

Shortage of Fellowship-Trained Ophthalmic Surgeons Outside Tier-1 Cities

Cataract and retinal devices often sit idle in northern emirates because only a handful of subspecialists reside there. Local universities run accelerated residency tracks, yet the pipeline will take several years to close existing gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Holds Leadership While Diagnostics Accelerate

Vision care products retained 63.58% of the UAE ophthalmic devices market in 2025 on the back of mandatory insurance cover and a consumer preference for high-fashion frames. Optical retail majors leverage robust footfall from license-renewal examinations to cross-sell premium lenses. Diagnostic platforms, registering an 8.42% CAGR to 2031, scale rapidly as AI algorithms demand high-resolution imaging inputs. Vendor roadmaps focus on portable OCT units operable in primary-care settings, enlarging reach beyond tertiary hospitals.

Momentum for surgical systems centers on femtosecond laser consoles and micro-invasive glaucoma shunts. Hospital groups trial disposable phaco tips to shorten re-processing cycles, enhancing ASC economics. These upgrades maintain revenue diversity and cushion suppliers against cyclical swings in vision-care accessories.

By Disease Indication: Cataract Remains Dominant as Diabetic Retinopathy Surges

Cataract captured a 39.74% UAE ophthalmic devices market share in 2025, propelled by sunlight exposure and a greying expatriate workforce. Clinics differentiate through premium trifocal lenses that extend clear focus across all distances, lifting procedure revenue per case. Diabetic retinopathy, growing at 7.63% CAGR, overtakes glaucoma as the second-largest value pool by 2031. Laser photocoagulation devices equipped with pattern-scan modules secure higher adoption as payers authorise early-intervention protocols to limit downstream costs.

Marker-based AMD monitoring and micro-shunt implants for glaucoma round out the therapeutic mix. Suppliers integrate voice-activated microscopes to streamline theatre workflow, an appealing feature given the surgeon shortfall in peripheral emirates.

By End-User: Hospitals Retain Scale Advantage as ASCs Gain Momentum

Hospitals supplied 41.86% of total device revenue in 2025, reflecting their capacity to absorb USD 1 million+ multi-room surgical build-outs. Integrated ophthalmology departments within quaternary centres handle complex cases such as combined corneal-retinal repairs that command higher average selling prices. ASCs, registering a 7.45% CAGR, benefit from insurance reimbursement parity for same-day cataract surgery, steering a volume shift away from inpatient settings. Purpose-built day-surgery facilities now feature three-room layouts that accommodate parallel surgery lists, further boosting equipment utilisation.

Specialty eye clinics thrive in preventive care and chronic disease follow-ups, particularly in diabetic retinopathy management where monthly OCT scans are routine. Their procurement skew favours compact imaging units that fit within 1,000 sq ft footprints typical of retail-adjacent premises.

Geography Analysis

Dubai anchors the UAE ophthalmic devices market thanks to a concentration of private hospitals, a vibrant optical retail scene, and the emirate’s branding as a medical-tourism hub. The Dubai Health Authority’s investment promotion programme offers streamlined licensing and 100% foreign ownership, enticing multinational manufacturers to situate regional headquarters in Dubai Healthcare City. Continuous inflows of affluent visitors seeking Lasik and lens-replacement procedures underpin premium-device turnover.

Abu Dhabi positions itself as an innovation centre, leveraging public-private partnerships through its Department of Health. Cleveland Clinic Abu Dhabi’s adoption of the PreserFlo MicroShunt for glaucoma management signals first-mover status in high-value subsegments. The Thiqa insurance scheme’s broad coverage of ophthalmic interventions supports steady patient flows. Government AI pilots run out of Abu Dhabi’s tech parks bolster demand for interoperable imaging modalities.

Northern emirates—Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain—present underpenetrated retail and surgical opportunities. MAGRABi Retail Group’s takeover of Kefan Optics injects modern dispensing formats into these catchments. Public hospitals procure autorefractors and slit lamps in bulk as part of primary-care upgrades, yet adoption of femtosecond lasers lags due to limited surgeon availability. Tele-consult platforms that connect metropolitan specialists to peripheral clinics aim to bridge this gap, subtly stimulating demand for high-definition fundus cameras compatible with cloud networks.

Competitive Landscape

Global suppliers—Alcon, Johnson & Johnson Vision, Carl Zeiss Meditec, and Bausch + Lomb—anchor the UAE ophthalmic devices market through direct offices and preferred-supplier contracts with flagship hospitals. Johnson & Johnson’s rollout of its TECNIS Odyssey IOL range targets cataract cases seeking spectacle independence. Alcon drives adoption of its image-guided femtosecond system that calibrates capsulotomy diameter in real time.

Regional consolidation intensifies in vision care. MAGRABi Retail Group’s acquisition of Kefan Optics adds more than 100 outlets, creating a pan-Gulf dispensing network that guarantees volume commitments to lens manufacturers. EssilorLuxottica’s majority stake in Ghanada Optical Co. secures an Abu Dhabi prescription laboratory, tightening control over edging and surfacing, and enabling two-day delivery to coastal emirates.

Technology partnerships, increasingly featuring AI layers, distinguish premium suppliers. Heidelberg Engineering teams with RetinSight to embed deep-learning algorithms into OCT workstations, elevating clinicians’ capacity to assess geographic atrophy progression. Bayer’s RAFEK initiative with the Emirates Society of Ophthalmology illustrates cross-sector collaboration where pharmaceutical know-how dovetails with device-based disease monitoring.

UAE Ophthalmic Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

EssilorLuxottica SA

Johnson & Johnson Vision Care

Bausch + Lomb Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MAGRABi Retail Group acquired Kefan Optics, enlarging its store footprint across the Gulf.

- March 2025: Cleveland Clinic Abu Dhabi celebrated its 10th anniversary, crossing 1 million treated patients and 26,000 surgeries in 2024, many in ophthalmology.

- March 2025: Burjeel Holdings posted AED 5.0 billion revenue, up 10.5%, citing expanded eye-care services as a growth pillar.

- February 2025: Moorfields Eye Hospital Abu Dhabi restored sight to a patient blind for 30 years, highlighting advanced corneal and retinal techniques.

- January 2025: Dubai Health Authority issued new standards for optical centers covering equipment and staffing minimums.

UAE Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology is a branch of medical science that deals with structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment for diagnosis, surgical, and vision correction purposes. The UAE ophthalmic devices market is segmented by devices (surgical devices (glaucoma drainage devices, glaucoma stents and implants, intraocular lenses, lasers, and other surgical devices), diagnostic and monitoring devices (autorefractors and keratometers, corneal topography systems, ophthalmic ultrasound imaging systems, ophthalmoscopes, optical coherence tomography scanners, other diagnostic and monitoring devices), and vision correction devices (spectacles and contact lenses).

The report offers the value (USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current value of the UAE ophthalmic devices market?

The market is valued at USD 254.98 million in 2026 and is projected to hit USD 344.9 million by 2031.

Which device category leads revenue generation?

Vision-care products hold 63.58% of revenue owing to mandatory insurance coverage and high consumer uptake.

Why are diagnostic systems growing the fastest?

AI-enabled screening initiatives and mandatory license-renewal examinations push demand for fundus cameras and portable OCT units, driving an 8.42% CAGR.

How does medical tourism influence the market?

A rising influx of international patients, especially to Dubai and Abu Dhabi, accelerates adoption of premium technologies like femtosecond lasers and trifocal IOLs.

What are the main challenges limiting market growth?

High upfront equipment costs, a shortage of fellowship-trained surgeons in smaller emirates, and import-registration delays temper wider device penetration.

Which end-user segment is expanding the quickest?

Ambulatory surgery centers record a 7.45% CAGR as cataract and refractive surgeries migrate to day-care settings that offer faster discharge and lower costs.

Page last updated on: