Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

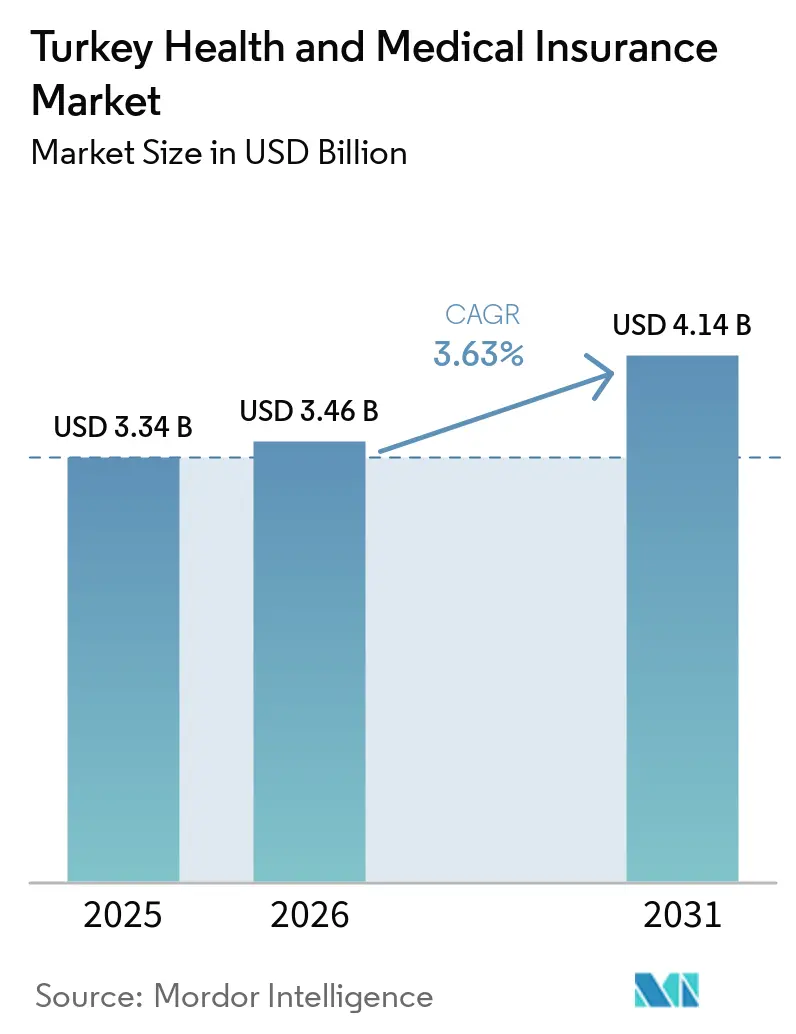

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 3.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Health and Medical Insurance Market Analysis by Mordor Intelligence

The Turkey Health And Medical Insurance Market size is expected to grow from USD 3.34 billion in 2025 to USD 3.46 billion in 2026 and is forecast to reach USD 4.14 billion by 2031 at 3.63% CAGR over 2026-2031.

Nominal premium growth has been strong in recent periods, yet the inflationary environment has kept real expansion restrained, which shapes how carriers price benefits and how households evaluate value for money. The state-led Social Security Institution framework remains the backbone of coverage, and private players focus on differentiated value, such as faster access to private providers and complementary products that reduce out-of-pocket expenses. Complementary Health Insurance, known locally as TSS, has become the main bridge between compulsory social coverage and private hospital access as carriers refine products and networks for affordability and speed. Regulatory reforms led by SEDDK that took effect in 2026, including lifetime renewal guarantees under defined conditions, push the Turkey health and medical insurance market from transactional annual contracts toward longer-term relationships that require careful actuarial calibration. On the operating side, the integration of e Nabız personal health records and SGK’s MEDULA backbone into claim flows supports faster adjudication, fraud controls, and more standardized documentation for both TSS and private medical insurance.

Key Report Takeaways

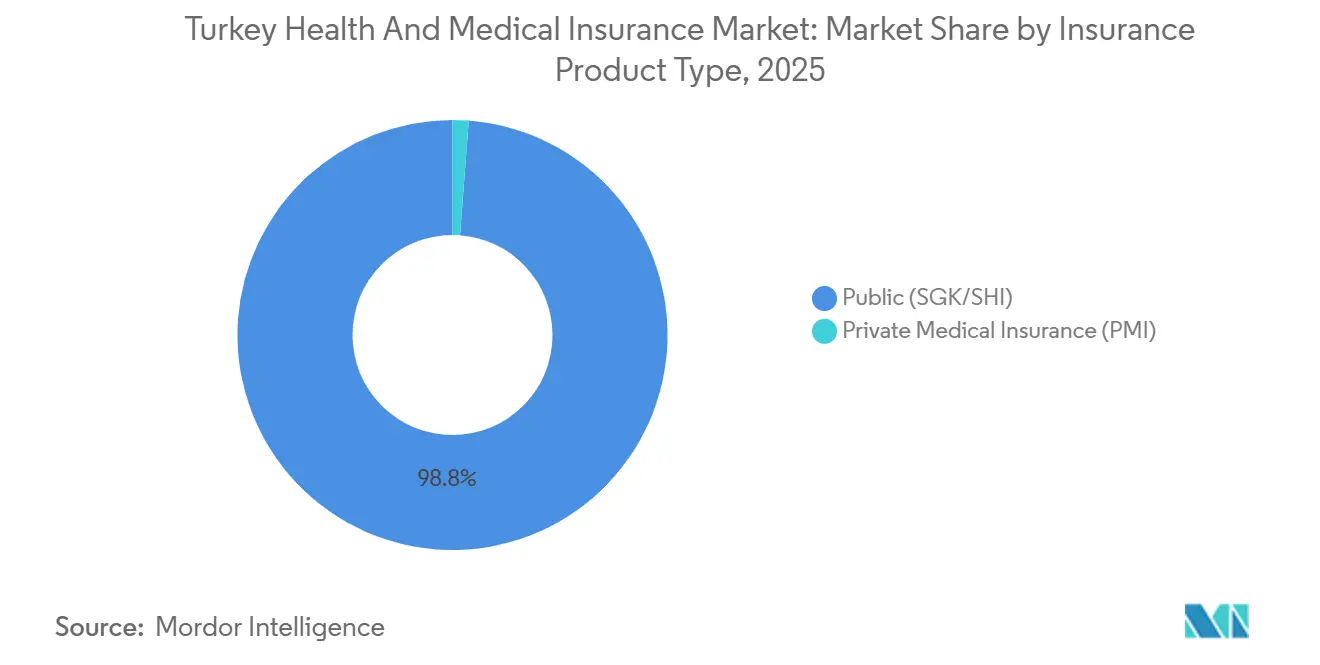

- By insurance product type, public and social security schemes led by SGK held 98.80% of the Turkey health and medical insurance market share in 2025, while Individual Private is the fastest-growing product at a 4.44% CAGR through 2031.

- By term of coverage, long-term policies held the largest share at 86.05% of the Turkey health and medical insurance market share in 2025, while short-term policies are projected to expand at a 3.69% through 2031.

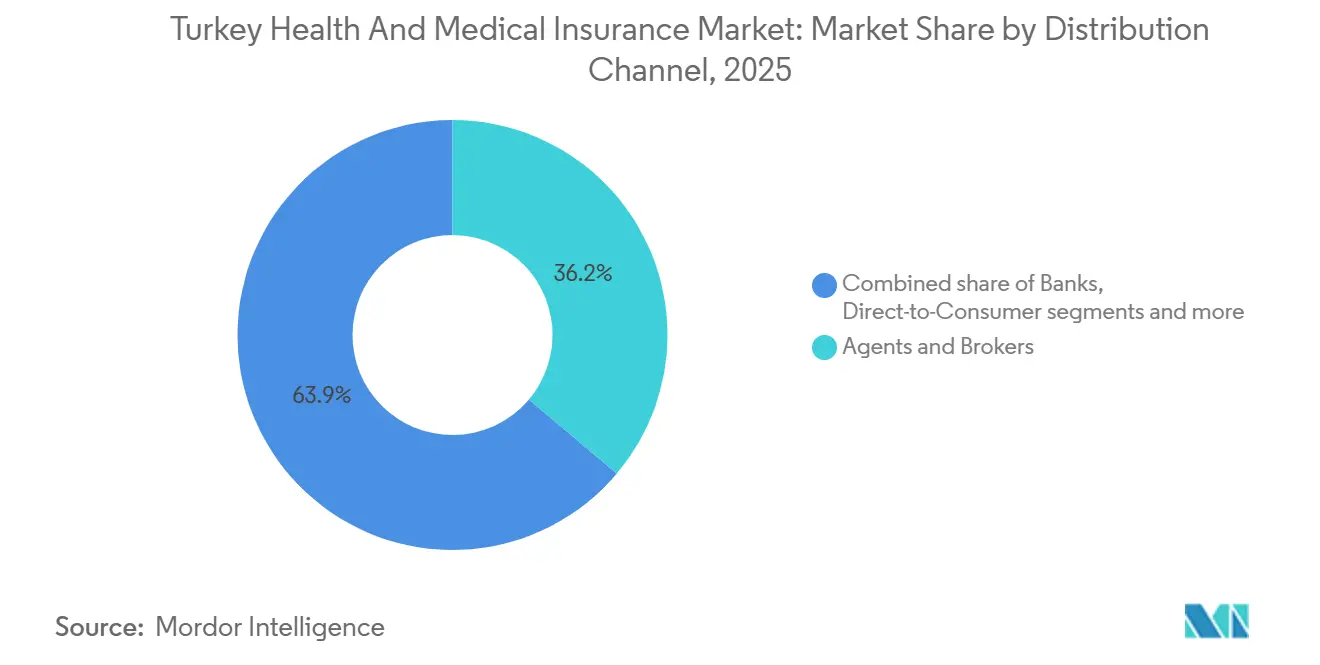

- By distribution channel, brokers and agents held 36.15% of the Turkey health and medical insurance market share in 2025, while direct-to-consumer is the fastest-growing channel with a projected 4.03% through 2031.

- By end-user segment, individuals accounted for 51.45% of the Turkey health and medical insurance market share in 2025, and SMEs are expected to post a 3.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TSS adoption surge bridging SGK co-pay gaps | +1.8% | National, higher in Marmara, Aegean, and Ankara | Medium term (2-4 years) |

| Employer-sponsored group PMI momentum | +0.6% | Major urban centers with spillovers to secondary cities | Long term (≥ 4 years) |

| Residence-permit requirement sustaining foreigner demand | +0.5% | National, concentrated in Istanbul, Ankara, Antalya, university hubs | Short term (≤ 2 years) |

| Agency and broker distribution depth | +0.4% | National, critical regions with limited digital access | Long term (≥ 4 years) |

| e‑Nabız and MEDULA integration | +0.7% | National, broad user base with the highest cost savings in urban centers | Medium term (2-4 years) |

| Emergence of participation (takaful) health cover | +0.2% | National, with a stronger appeal in conservative regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

TSS Adoption Surge Bridging SGK Co Pay Gaps

TSS sits at the center of private coverage growth because it targets the difference fees SGK beneficiaries face when using contracted private hospitals and shortens access times for common services. In the Turkey health and medical insurance market, TSS functions as a practical bridge between broad public entitlements and the service speed and choice households expect in private settings. As carriers refine benefit tiers and preferred networks, e Nabız documentation and MEDULA checks reduce administrative friction and help channel claims to contracted facilities that follow standardized processes. SEDDK’s 2026 renewal guarantee framework further strengthens buyer confidence by clarifying long-term rights once tenure and eligibility conditions are met, which supports persistence in the Turkey health and medical insurance market [1]Insurance and Private Pension Regulation and Supervision Authority, “Strategic Plan 2024–2028,” SEDDK, seddk.gov.tr.

e Nabız and MEDULA Integration Enabling Faster Adjudication and Anti-Fraud

Digital infrastructure is now embedded in claims flows through the personal health record platform e Nabız and SGK’s MEDULA system, which together support verification, reduce duplication, and compress adjudication times. For the Turkey health and medical insurance market, this integration means hospitals transmit standardized data, insurers validate eligibility and service history more quickly, and patients receive decisions with less paperwork and fewer post-visit frictions. The infrastructure has demonstrated measurable efficiency gains by curbing redundant diagnostics and enabling near real-time approvals, and it forms the backbone for both TSS and private medical insurance claims. Features such as two-step authentication and user-managed consent settings inside e Nabız also raise data-governance standards, which is important because health data sits under strict legal protections. These gains reinforce insurer efforts to expand digital self-service and steer volumes to in-network providers that share standardized data with fewer exceptions, which improves the operating profile of the Turkey health and medical insurance market.

Residence Permit Requirement Sustaining Foreigner Health Policy Demand

Residence permit processes require proof of adequate health insurance, which sustains demand for compliant private policies among foreign residents, students, and certain dependents [2]Directorate General of Migration Management, “Residence Permit Types,” Presidency of Migration Management, en.goc.gov.tr. In the Turkey health and medical insurance market, this requirement supports issuance peaks around application and renewal cycles and concentrates activity in provinces with large foreign resident populations and universities. Policy certificates and verification codes must align with official formats and authenticity checks, which encourages carriers to standardize documentation and digital channels. As oversight tightens, insurers refine provider networks and service scripts that meet administrative criteria while guiding policyholders to contracted care pathways. These features reinforce how the Turkey health and medical insurance market links regulatory compliance with service design across foreign resident segments.

Agency and Broker Distribution Depth Sustaining Reach

Intermediaries remain critical in connecting households and employers to suitable products, especially in provinces where digital adoption or provider density is lower. In the Turkey health and medical insurance market, agents and brokers explain benefit tiers, network differences, co-payment rules connected to SGK contracts, and renewal conditions, which reduces mismatches and improves retention. The channel’s strength is most visible at renewal, where intermediaries reconcile claims experience with plan adjustments and guide policyholders through documentation in systems like e Nabız or hospital portals. SEDDK’s broader supervisory agenda has emphasized strengthening market conduct and capability standards, which support larger intermediaries and digital-hybrid models. As carriers expand direct-to-consumer options, agent-led advisory is likely to remain important where personalized guidance cuts through complexity in the Turkey health and medical insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medical inflation outpacing SUT updates pressures affordability | -1.2% | National, acute in metropolitan private hospital clusters | Short term (≤ 2 years) |

| KVKK explicit-consent friction hampers underwriting and renewals | -0.4% | National, more pronounced where digital infrastructure is weaker | Medium term (2-4 years) |

| Low bancassurance penetration limits distribution | -0.3% | Urban banking corridors; limited effect in rural areas | Long term (≥ 4 years) |

| Network co-payment ceilings under SGK contracts constrain product design | -0.6% | National, across SGK-tied networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Medical Inflation Outpacing SUT Updates Pressures Affordability

Private providers and insurers face pressure when input costs for health services rise faster than scheduled updates in the Health Implementation Communiqué, known as SUT. In the Turkey health and medical insurance market, this mismatch narrows room for maneuver on co-payments and plan design because TSS must align with SGK-linked ceilings and network rules. Hospitals tend to seek tariff renegotiations while carriers respond with tighter preferred networks and digital navigation that steer volumes to contracted facilities. Pharmacy claims have also moved onto standardized electronic rails, which improve reconciliation processes and support oversight in reimbursement flows tied to SGK and contracted pharmacies. These dynamics force careful balancing between access, user affordability, and combined ratios across product tiers in the Turkey health and medical insurance market.

Network Co-Payment Ceilings Under SGK Contracts Constrain Product Design

Co-payment ceilings attached to SGK-contracted networks limit how far carriers can differentiate product tiers on cost-sharing, even when risk segmentation might support more varied structures. For the Turkey health and medical insurance market, this standardization curbs the ability to deploy high-deductible options or targeted coinsurance differences across hospital groups, which many international markets use to manage moral hazard. It also complicates the task of aligning hospital price corridors with benefit tiers since policy structures must remain consistent with SGK-linked access and payment rules. In practice, carriers respond by tightening preferred networks or by embedding soft incentives such as digital care navigation instead of hard co-pay differentials, which can reduce clarity for some consumers. These constraints make it harder to translate actuarial insights into product features that balance affordability with sustainability in the Turkey health and medical insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Product Type: TSS Explosive Growth Reshapes Mix

Public (SGK/SHI) held 98.80% of the Turkey health insurance market share in 2025. Private medical insurance in Turkey includes individual and group plans, while Complementary Health Insurance provides targeted benefits that align with SGK contracted private networks. Within the private segment, individual policies are projected to grow at 4.44% through 2031. The Turkey health and medical insurance market continues to see households choose TSS to reduce difference fees and shorten scheduling, while upper-income users select comprehensive private cover for broader outpatient and maternity benefits. Policy documentation and pre-authorization through e Nabız and MEDULA sustain smoother claims and support consistent facility routing, which helps both users and carriers manage expectations. The 2026 renewal guarantee framework adds persistence to the product mix by clarifying eligibility and rights for long tenured members across private health lines in the Turkey health and medical insurance market.

Public and social security schemes remain the country’s backbone for health access, and private plans operate as complements rather than substitutes, which defines competitive approaches and service design. In dense provider markets, TSS supports faster specialist access and wider private facility choice, while in provinces with fewer private beds, carriers use navigation tools to direct care to regional hubs. These practices align the Turkey health and medical insurance market with standardized digital documentation and help maintain predictable out-of-pocket structures tied to SGK contracted networks. Over the forecast period, balanced growth between TSS and comprehensive private plans will hinge on claims governance and network economics under stable regulatory rules.

By Term of Coverage: Long Term Dominance Faces Short Term Nibbling

Long-term policies of 12 months or more dominate with an 86.05% share in 2025, which reflects budgeting cycles and the structure of renewal guarantees that policyholders can earn under defined conditions. In the Turkey health and medical insurance market, short-term coverage grows from a smaller base because it serves transitional needs for foreign residents and students ahead of broader eligibility or longer stays. Standardized disclosures help users convert short-term to long-term without unnecessary re-underwriting, where eligibility allows, which supports continuity of care and predictable cost sharing. The digital backbone supports continuity by keeping consistent documentation and eligibility checks, which helps both members and carriers when terms change in the Turkey health and medical insurance market.

Short-term (Less Than 12 months) is the fastest-growing benefit set at a projected 3.69% CAGR from 2026 to 2031. Short-term products retain a role in niche segments where timing or residency status drives coverage choices, but long-term policies remain the dominant form as renewal protections make multi-year commitments more attractive. Carriers focus on portability and documentation to prevent gaps when users shift terms, and they streamline process flows to align with e Nabız records. Over the forecast period, long-term dominance and short-term flexibility together can stabilize utilization while keeping the Turkey health and medical insurance market accessible for residents and qualifying foreign applicants. These patterns align with SEDDK’s goals for consumer protection and sustained participation under clearer renewal standards.

By Distribution Channel: Agents Defend Share Against Digital Surge

Brokers and agents hold 36.15% of distribution in 2025 as advisory remains critical for explaining SGK-linked co-pay rules, provider networks, and renewal eligibility under standardized terms. Direct-to-consumer channels expand as mobile and web journeys simplify buying and claims tasks, which fits well with standardized documentation and e Nabız integration in the Turkey health and medical insurance market. Banks with strong retail footprints can complement these routes when post-sale support is integrated to protect relationships should claims issues arise. SEDDK’s supervisory agenda supports professionalization and market conduct, which encourages both larger intermediaries and digital hybrid models to scale responsibly. These trends suggest a blended distribution mix that balances advisory depth with the convenience of self-service across the Turkey health and medical insurance market.

Bancassurance remains smaller than the agent-broker channel in 2025, while the Turkey health and medical insurance market size for direct-to-consumer is still the fastest growing at a 4.03% CAGR through 2031. Banks hold broad account relationships with 62% of adults reporting an account, which gives the channel headroom if product scripts and post-sale support are simplified for branch teams. SEDDK’s push for standardized terms and stronger market conduct is raising capability thresholds across distributors, which favors hybrid models that combine digital flows with compliant advice. Carriers are aligning channel roles to this framework by using self-service for quotes and issuance, while reserving agents for plan selection and renewals that depend on claims history and network preferences.

By End User Segment: Individuals Lead, SME Potential Untapped

Individuals accounted for 51.45% of the Turkey health and medical insurance market share in 2025, and the Turkey health and medical insurance market size for SMEs is projected to grow at a 3.79% CAGR through 2031. Large corporates maintain high group coverage as part of retention strategies and often set service benchmarks that shape wider expectations in the Turkey health and medical insurance market. SMEs show steady interest as micro group options lower barriers, and digital onboarding simplifies administration for firms that lack dedicated benefits teams. Clearer renewal rules and provider navigation help individuals and SMEs compare TSS against comprehensive private options based on needs and budgets across the Turkey health and medical insurance market.

Residence permit rules generate periodic demand from foreign students and residents, which adds to the individual pool during application windows and renewals. Individuals who value speed of access and broad provider choice often select robust TSS within strong networks, while households that prioritize comprehensive outpatient and maternity benefits consider individual private cover where budgets allow. Employer purchasing for large corporates stabilizes utilization and shapes facility contracts that influence local access conditions in the Turkey health and medical insurance market. Over the forecast period, the end-user mix should broaden with standardized rules, transparent disclosures, and stronger digital navigation that reduce friction at purchase and claim.

Geography Analysis

Marmara accounts for the largest share of private health policies, given Istanbul’s scale and the concentration of SGK-contracted private hospitals that anchor preferred networks and TSS claims. Central Anatolia follows as Ankara’s government presence and large hospital complexes raise the need for supplementary access, including to flagship facilities like Ankara City Hospital with 4,050 beds. [3]Ankara City Hospital, “About Us,” Republic of Turkey Ministry of Health, ankarasehirhastanesi.saglik.gov.tr. The Aegean region shows steady demand supported by private hospital density and expatriate communities that value wide provider networks and language support within the Turkey health and medical insurance market. Southeastern Anatolia and Black Sea provinces show lower private bed density and rely more on referral pathways to metropolitan centers for advanced diagnostics and specialty care. These patterns place a premium on clear contracting, digital navigation, and consistent authorization flows to maintain predictable experiences across regions.

In Marmara and the Aegean, broad provider networks and standardized documentation help TSS deliver faster outpatient access and reduce scheduling delays under SGK alone. Central Anatolia’s administrative and industrial base supports employer-sponsored group coverage and advanced care access at large multi-hospital campuses that can be reached within defined network maps. Regions with fewer private beds use referral routes and stronger pre-authorization to maintain care quality while directing users to contracted hubs under consistent documentation rules. The Turkey health and medical insurance market should see regional disparities narrow as digital servicing reduces paperwork and as rules standardize portability and renewal protections in higher churn areas. Over time, claims governance, provider contracting, and localized distribution will shape region-specific experiences tied to facility density and user preferences.

Banks and large employers have outsize roles in Marmara and Central Anatolia because account ownership, payroll density, and provider concentration enable scale benefits that lower acquisition and servicing costs. In provinces with lower connectivity, agent-led advisory remains the practical bridge to explain SGK-linked co-pay rules and renewal guarantees introduced by SEDDK. This balance supports a resilient regional approach inside the Turkey health and medical insurance market, where service design, channel mix, and provider maps are tailored to local realities. As digital rails extend and documentation standardizes further, the share gap between higher and lower density regions should gradually compress under stable oversight.

Competitive Landscape

The private segment features national insurers and bancassurance-linked carriers that compete on network quality, digital servicing, and benefit clarity rather than on displacing SGK coverage. In the Turkey health and medical insurance market, differentiation often starts with TSS plan design and provider contracting, since these benefits address the largest source of household friction in accessing private care. Leading carriers also invest in digital authorization and self-service claim flows to compress processing times and improve communications, anchored in the national e Nabız infrastructure. Product pages and service portals emphasize simple explanations of co-pay rules and network navigation, reflecting the regulatory push for standardized disclosures. Over the forecast window, service efficiency and network strategy are likely to be the main drivers of share shifts inside the Turkey health and medical insurance market.

Strategic moves by incumbents point to deeper digitalization, stronger navigation tools, and broader network partnerships. Banks with strong retail footprints explore simplified sales flows for health products, with emphasis on post-sale servicing so that branch relationships are protected when claims arise. Large state and private hospitals continue to invest in capacity and specialized services, which draw both SGK and private volumes and raise the importance of clear contracting and price corridors. Regulatory guidance shapes how far carriers can flex deductibles, co-pay, and waiting periods, which points competitive energy toward user experience, digital touchpoints, and preventive-care engagement. These features will influence how the Turkey health and medical insurance market allocates capital between acquisition, claims governance, and technology.

Two visible directions are rising. First is the deepening of TSS, where carriers expand networks and refine outpatient benefits, and second is broader digital integration that reduces the cost to serve and tightens fraud controls. Insurers that align quickly to lifetime renewal guarantees and embed transparent renewal journeys are positioned to improve retention and lifetime value. Partnerships with large hospital groups and the development of clear navigation pathways are likely to determine satisfaction and complaints incidence, which feed back into brand strength and growth. Over time, the Turkey health and medical insurance market is expected to converge on simpler products, stronger digital experiences, and tighter network economics that balance access and sustainability.

Turkey Health and Medical Insurance Industry Leaders

Acıbadem Sigorta

Anadolu Anonim Türk Sigorta Şirketi

Allianz Sigorta A.Ş.

Türkiye Sigorta A.Ş.

AXA Sigorta A.Ş.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Allianz Turkey introduced a standalone health insurance plan for children, enabling individuals aged 15 days to 18 years to obtain independent coverage, reflecting the company’s commitment to comprehensive family healthcare solutions.

- March 2025: Türkiye implemented health insurance reforms, effective April 1, 2025, for foreign residents, enhancing coverage standards, increasing costs, and phasing out low-cost policies, while expanding access to select public hospitals, primarily for emergency treatments.

- March 2025: Alternatif Bank and Zurich Insurance Group Türkiye established a long-term strategic partnership, enabling Alternatif Bank’s retail, commercial, and corporate customers to access Zurich Türkiye’s comprehensive insurance offerings across life, private pension, health, and elementary sectors.

- January 2025: Unico Insurance had introduced a new range of health insurance products, including UniHealth Supplementary Health Insurance, which had alleviated financial burdens from additional fees at SGK-affiliated private healthcare facilities.

Turkey Health and Medical Insurance Market Report Scope

Health insurance is defined by its flexibility, offering broad coverage for diverse health conditions. Conversely, medical insurance provides limited, pre-defined coverage, focusing on specific health emergencies, including particular injuries, accidents, and illnesses. The distinction lies in the scope and comprehensiveness of coverage provided.

The Turkey health and medical insurance market is segmented by insurance product type (private medical insurance with individual and group policy coverage, public/social security schemes), term of coverage (short-term less than 12 months, long-term 12 months or more), distribution channel (brokers/agents, banks bancassurance, direct-to-consumer, employer-sponsored, other channels), and end-user segment (individuals, SMEs, large corporates). The market forecasts are provided in terms of value (USD).

By Insurance Product Type

| Private Medical Insurance (PMI) | Individual Policy Coverage |

| Group Policy Coverage | |

| Public / Social Security Schemes |

By Term of Coverage

| Short-term (Less Than 12 months) |

| Long-term (Greater Than Equal to 12 months) |

By Distribution Channel

| Brokers / Agents |

| Banks (Bancassurance) |

| Direct-to-Consumer (Online / Phone) |

| Employer-Sponsored (Companies) |

| Other Channels (Affinity, Associations) |

By End-user Segment

| Individuals |

| SMEs |

| Large Corporates |

| By Insurance Product Type | Private Medical Insurance (PMI) | Individual Policy Coverage |

| Group Policy Coverage | ||

| Public / Social Security Schemes | ||

| By Term of Coverage | Short-term (Less Than 12 months) | |

| Long-term (Greater Than Equal to 12 months) | ||

| By Distribution Channel | Brokers / Agents | |

| Banks (Bancassurance) | ||

| Direct-to-Consumer (Online / Phone) | ||

| Employer-Sponsored (Companies) | ||

| Other Channels (Affinity, Associations) | ||

| By End-user Segment | Individuals | |

| SMEs | ||

| Large Corporates |

Key Questions Answered in the Report

What is the size and growth outlook of the Turkey health and medical insurance market to 2031?

The Turkey health and medical insurance market size is USD 3.46 billion in 2026 and is projected to reach USD 4.14 billion by 2031 at a 3.63% CAGR.

How are regulations shaping the Turkey health and medical insurance market in 2026?

SEDDK introduced lifetime renewal guarantees and standardized policy terms, which shift pricing and underwriting to a multi-year view and improve portability and disclosures for consumers.

What role does digital infrastructure play in claims and servicing?

The e‑Nabız and MEDULA systems enable standardized documentation, faster adjudication, and stronger fraud controls across the claim lifecycle, improving experience and reducing handling costs.

Which regions are most important for private coverage in Turkey?

Marmara, Central Anatolia, and the Aegean lead due to provider density, large hospital complexes, and expatriate or medical travel dynamics, while agents remain key in regions with lower connectivity.

How are distribution channels evolving for the Turkey health and medical insurance market?

Agents and brokers remain central for advisory and complex renewals, while direct-to-consumer channels expand with digital literacy, and banks consider simplified flows for select customer groups.

Page last updated on: