Turkey Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

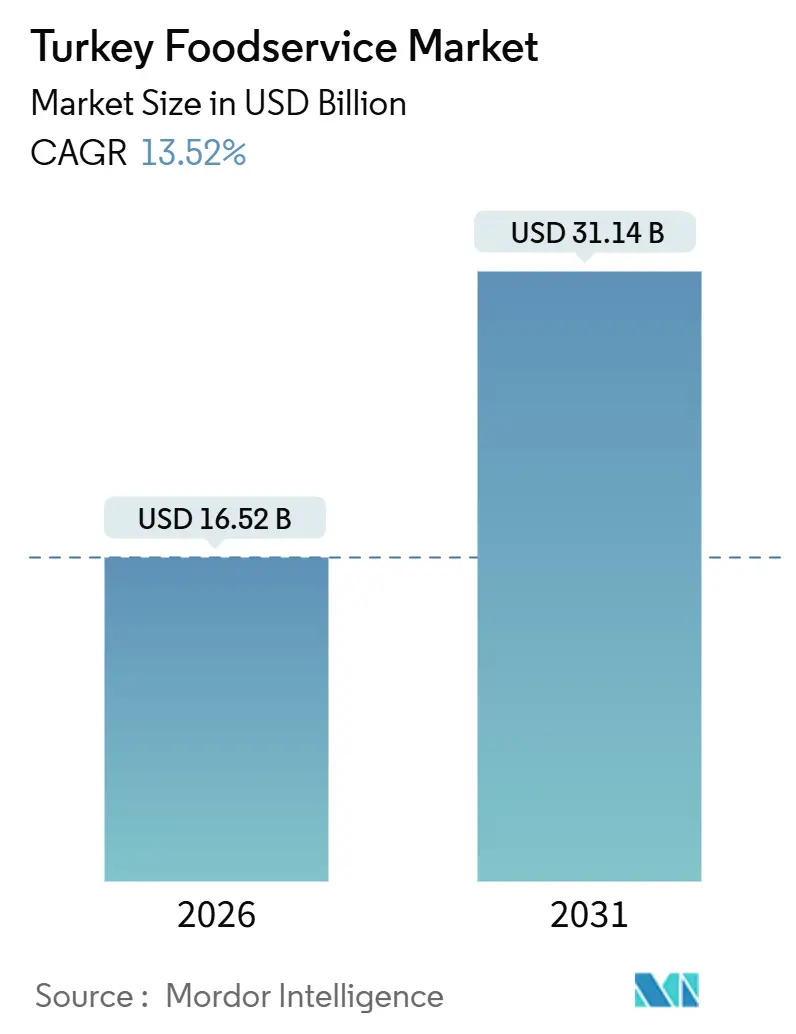

| Market Size (2026) | USD 16.52 Billion |

| Market Size (2031) | USD 31.14 Billion |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

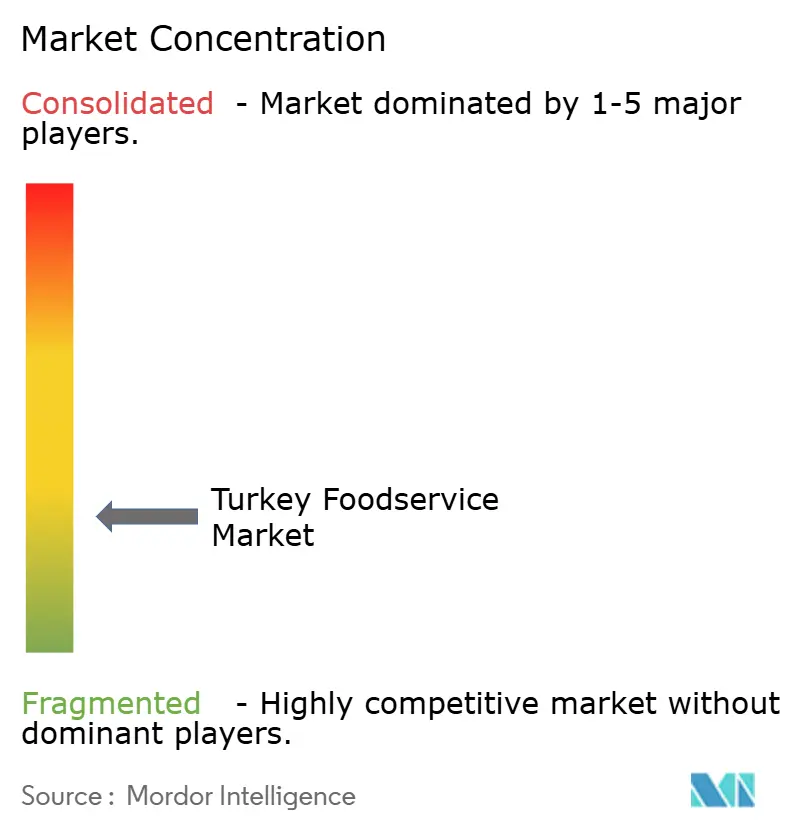

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Turkey Foodservice Market Analysis by Mordor Intelligence

Turkey's foodservice market, valued at USD 16.52 billion in 2026, is expected to grow significantly, reaching USD 31.14 billion by 2031, with a strong CAGR of 13.52% during the forecast period. This growth is driven by rapid urbanization, the rise of digital ordering through aggregators, and a recovery in tourism, which is boosting demand from both residents and visitors. Quick Service Restaurants (QSRs) continue to attract the most customers, while cloud kitchens, designed for delivery, are expanding faster than traditional brick-and-mortar restaurants. Chained operators are closing the gap with independent players by using standardized supply chains and tailoring menus based on data, although they face challenges like labor shortages and inefficiencies in cold-chain logistics, which increase costs. The competitive landscape is also evolving with major consolidations among delivery platforms. For example, Uber's USD 700 million acquisition of Trendyol GO and its ongoing USD 1 billion bid for Getir Food highlight the growing importance of controlling logistics in the market.

Key Report Takeaways

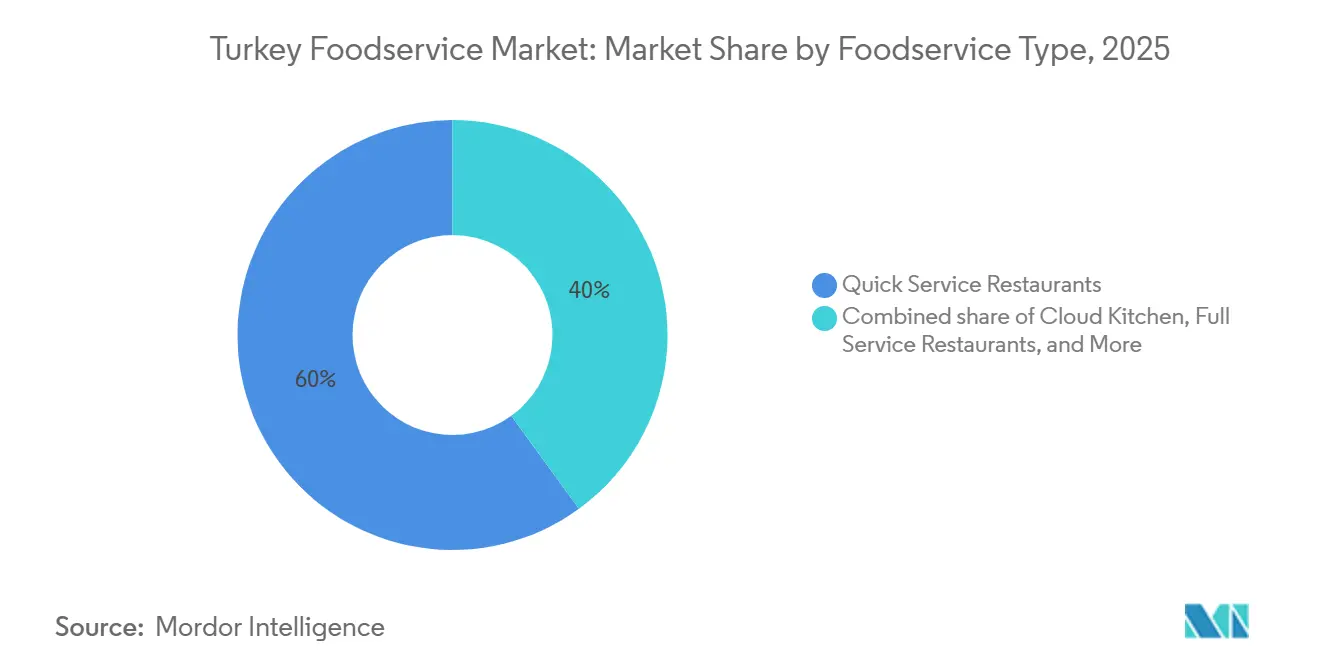

- By foodservice type, Quick Service Restaurants led with a 60.01% share of the Turkish foodservice market in 2025, while the cloud-kitchen segment is advancing at a 14.01% CAGR through 2031.

- By outlet, independent operators held 72.65% of the Turkey foodservice market in 2025; chained outlets recorded the fastest growth at 13.87% CAGR to 2031.

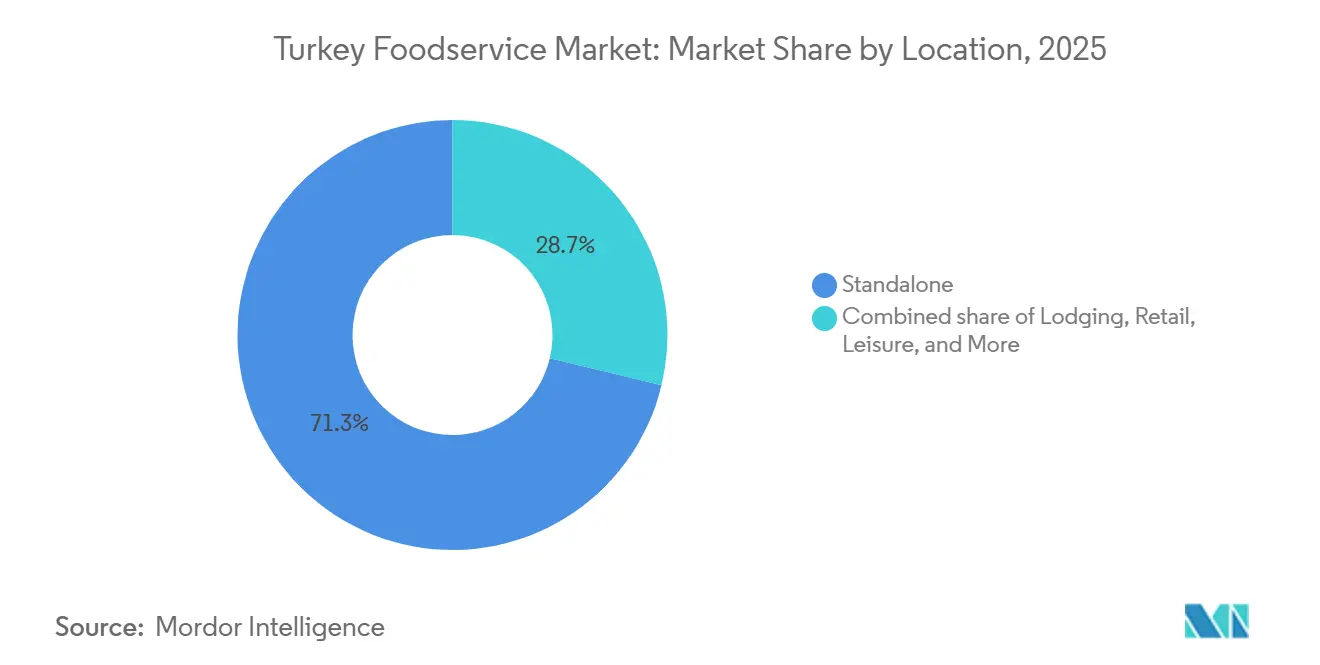

- By location, standalone venues captured 71.25% of the Turkey foodservice market size in 2025, and lodging-based outlets are expanding at a 14.75% CAGR through 2031.

- By service type, dine-in accounted for 55.71% of the Turkey foodservice market size in 2025, whereas delivery is projected to expand at a 15.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Foodservice Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of cloud and virtual kitchens in major cities | +2.8% | Istanbul, Ankara, Izmir, Bursa | Medium term (2-4 years) |

| Menu innovation and localization aligning offerings with Turkish tastes | +2.1% | National, with early gains in Istanbul, Antalya, Izmir | Short term (≤ 2 years) |

| Young urban consumers increasingly dining out at cafés, QSRs, and casual restaurants | +2.5% | Istanbul, Ankara, Izmir, Antalya | Medium term (2-4 years) |

| Tourist hubs like Istanbul, Antalya, Izmir, and Bodrum seeing strong food and beverage demand due to inbound tourism | +3.2% | Istanbul, Antalya, Izmir, Bodrum | Long term (≥ 4 years) |

| Third-party delivery platforms driving restaurant deliveries and cloud-kitchen growth | +2.4% | National, concentrated in top-10 cities | Short term (≤ 2 years) |

| Major cities' dense HoReCa infrastructure supporting robust supplier and logistics ecosystem | +1.8% | Istanbul, Ankara, Izmir | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cloud and Virtual Kitchens in Major Cities

Health-conscious Turkish consumers are increasingly choosing locally sourced, minimally processed foods over ultra-processed options with additives and artificial flavors. This shift is led by urban millennials and Gen Z, who prefer transparency, clean labels, and traditional Turkish cuisine over imported fast food. McDonald's Turkey has responded by sourcing 95% of its ingredients locally and introducing items like the Köfte Burger and Turkish Breakfast Plate, highlighting the need for global QSR brands to adapt or lose market share to local competitors. However, reformulating recipes, sourcing organic proteins, and improving supply-chain transparency are raising costs for operators without guaranteeing higher prices. Cloud kitchens and delivery-only brands also face challenges, as they must balance low costs with growing consumer demand for better ingredient quality.

Menu Innovation and Localization Aligning Offerings with Turkish Tastes

McDonald's Turkey sources 95% of its ingredients locally and has expanded its Turkey-only menu. Items like the Köfte Burger boosted market share by 30%, while the Turkish Breakfast Plate increased breakfast sales from 3% to 9% of total revenue. Burger King rebranded as "Borgir" in Turkey, achieving 76% growth in Q2 2025. TAB Gıda, with 1,830 restaurants, includes Usta Dönerci and Usta Pideci, focusing on traditional Turkish street food. Surveys show 56% of consumers find McDonald's products suitable for Turkish cuisine, and 90% prefer local ingredients. Glocalization drives both new and repeat purchases, reduces import reliance, shortens supply chains, and meets the demand for fresh, minimally processed foods, giving operators a competitive edge.

Menu Innovation and Localization Aligning Offerings with Turkish Tastes

McDonald's Turkey asserts that 95% of its ingredients are sourced locally. The fast-food giant has expanded its Turkey-exclusive menu, introducing items like the Köfte Burger, which has bolstered the brand's market share by 30%. Another addition, the Turkish Breakfast Plate, has notably increased breakfast sales from 3% to 9% of total revenue. Meanwhile, Burger King has made waves in Turkey by rebranding itself as "Borgir", a move that has paid off with a remarkable 76% growth in Q2 2025. TAB Gıda, with its expansive portfolio of 1,830 restaurants, is championing traditional Turkish street food through its Usta Dönerci and Usta Pideci formats. Consumer sentiment leans heavily in favor of these adaptations: 56% of surveyed individuals feel McDonald's offerings resonate with Turkish cuisine, and a striking 90% express a preference for locally sourced ingredients. This trend underscores the potency of glocalization in driving both initial trials and repeat purchases. Furthermore, localizing the menu not only buffers against import fluctuations and streamlines supply chains but also aligns with the growing consumer demand for fresh, minimally processed foods. This strategy offers a sustainable edge to operators who commit to local sourcing and culinary tweaks.

Young Urban Consumers Increasingly Dining Out at Cafés, QSRs, and Casual Restaurants

Turkey is the fifth-largest market for branded coffee shops in Europe, driven by the growing popularity of café culture among younger generations who use these spaces for socializing and work. Espressolab operates about 160 stores in Turkey as part of its global network of 400 locations. Starbucks Turkey runs 685 outlets, including 13 premium Reserve stores designed for urban professionals seeking high-end experiences. This trend is supported by urbanization rates exceeding 80%, higher disposable incomes in cities, and the growth of co-working spaces and university campuses, which attract significant foot traffic to quick-service and casual dining venues[1]Source: World Bank, "Urban population (% of total population) - Turkiye", data.worldbank.org. To appeal to this audience, operators focus on digital loyalty programs, mobile ordering, and visually appealing interiors. These efforts cater to consumers who see dining out as both a convenience and a lifestyle choice, driving the market's strong 13.52% CAGR through 2031.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perishable supply chain gaps and cold-chain limitations | -1.6% | National, acute in rural and secondary cities | Medium term (2-4 years) |

| Food safety, traceability, and sustainability compliance overhead | -1.2% | National | Short term (≤ 2 years) |

| Consumer pushback on ultra-processed items | -0.9% | Urban centers, spreading nationally | Medium term (2-4 years) |

| Labor shortages and high staff turnover | -1.4% | Istanbul, Ankara, Izmir, Antalya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Perishable Supply Chain Gaps and Cold-Chain Limitations

Cold-chain infrastructure in Turkey is largely limited to major cities, leaving rural and secondary areas with poor temperature control. This leads to higher spoilage rates and restricts menu options for businesses relying on fresh produce, dairy, and proteins. While Istanbul, Ankara, and Izmir have strong refrigerated logistics networks, operators in inland and eastern regions face higher costs and delays, reducing profitability and limiting perishable-heavy menus. In 2024, Migros expanded to 73 distribution centers by adding 16 new ones, but last-mile cold-chain gaps persist outside top-tier cities. The Turkish Food Codex mandates traceability and temperature monitoring for perishables, adding compliance costs that smaller operators struggle to bear. Cold-chain failures can result in recalls and reputational damage, forcing some businesses to close. Despite ongoing investments in refrigerated trucks, insulated packaging, and real-time monitoring, infrastructure development lags behind demand, creating bottlenecks that reduce the market's 13.52% CAGR through 2031 by about 1.6 percentage points.

Food Safety, Traceability, and Sustainability Compliance Overhead

The Turkish Food Codex requires food businesses to adopt HACCP systems and register with the Ministry of Agriculture and Forestry. Traceability regulations further mandate detailed documentation of ingredient sourcing, processing, and distribution, increasing administrative and technology costs for all operators. In 2023, TAB Gıda conducted 2,641 supplier audits and 352 internal audits, highlighting the high resource demands of compliance. Its plan to transition to 100% RSPO Mass Balance palm oil by March 2024 reflects the growing complexity of meeting sustainability standards required by international franchisors. Smaller operators, lacking quality-assurance teams, must handle regulatory filings, audits, and certifications themselves, diverting focus from customer service and innovation. Progress toward aligning with EU food-safety standards is ongoing but incomplete, creating uncertainty for exporters and cross-border franchisors. While compliance builds public trust, it disproportionately impacts smaller players, driving consolidation and reducing annual growth by about 1.2 percentage points as weaker operators exit or merge.

Segment Analysis

By Foodservice Type: QSR Dominance Meets Cloud-Kitchen Disruption

Quick service restaurants held 60.01% of the Turkey foodservice market in 2025, anchored by TAB Gıda's 1,830-unit portfolio spanning Burger King, Popeyes, Sbarro, Arby's, Usta Dönerci, Usta Pideci, and Subway as of December 2024, and DP Eurasia's 655 Domino's stores that channel majority of delivery sales through online platforms. Turkish consumers, especially young urbanites, prefer QSRs for their speed, affordability, and consistent quality. Operators use standardized menus, centralized commissaries, and economies of scale to ensure fast service under 10 minutes and competitive pricing. Drive-thru options and delivery partnerships further expand their reach. However, growth in top-tier cities is slowing due to market saturation, limited prime real estate, and the need for continuous menu innovation and promotions.

Cloud kitchens are growing at 14.01% annually through 2031, the fastest among all foodservice types. Migros, with 35 to 40 cloud kitchens, doubled its gross merchandise value from TL 7.9 billion to TL 15.1 billion and tripled order volumes from 1.4 million to 4.8 million year-on-year, achieving breakeven before marketing costs in 2024. Cloud kitchens avoid lease commitments, reduce labor needs, and allow multi-brand production in one location. They enable quick adjustments to offerings using delivery-platform analytics. Compliance with the Turkish Food Codex and HACCP certification ensures food safety during rapid expansion. Full-service restaurants and cafés-and-bars grow slower due to higher costs, longer service times, and reliance on dine-in traffic, which is vulnerable to economic and tourism fluctuations. However, they remain popular for offering unique dining experiences and social interactions that QSRs and delivery services cannot match.

Note: Segment shares of all individual segments available upon report purchase

By Outlet: Independents' Scale Versus Chains' Efficiency

In 2025, independent outlets accounted for 72.65% of Turkey's foodservice market, reflecting a fragmented landscape dominated by family-owned restaurants, neighborhood cafés, and single-unit operators. These businesses benefit from low costs, flexible menus, and strong community ties but struggle to compete with chains' digital tools, supply-chain advantages, and brand recognition. Without mobile apps, loyalty programs, or data analytics, independents rely on delivery aggregators, which charge 15% to 30% commissions and control customer relationships. Despite their large market share, independents are vulnerable to economic shocks, regulatory costs, and labor shortages, lacking the financial reserves and management expertise that chains use to scale and endure downturns.

Chained outlets are growing at 13.87% annually through 2031, led by TAB Gıda's 1,830 restaurants, Starbucks Turkey's 685 stores (including 9 drive-thru and 13 Reserve formats), and Simit Sarayı's 300+ branches serving nearly one million customers daily. Chains ensure consistency with standardized operations, centralized procurement, and franchisee training. Their strong brands and marketing attract customers and justify higher prices, unlike independents. Digital ordering, kiosks, and delivery-platform integration boost chains' efficiency, allowing growth without proportional increases in costs. As chains expand into secondary cities and tourist areas, they will reduce independents' share. However, independents' agility and local authenticity will help them retain a presence in neighborhood markets and niche cuisines that chains find less profitable.

By Location: Standalone Ubiquity Versus Lodging's Tourism Tailwind

In 2025, standalone locations led Turkey's foodservice market with a 71.25% share. These include street-front restaurants, shopping-district cafés, and neighborhood eateries that rely on walk-in traffic, delivery, and repeat local customers. Their visibility, accessibility, and freedom from landlord restrictions allow operators to adjust hours, menus, and pricing based on demand. Unlike retail, travel, and lodging outlets, standalone formats avoid revenue-sharing and operational constraints, preserving margins and autonomy. This dominance reflects Turkey's urban density and pedestrian-friendly areas, where dining out is often within walking distance. However, rising rents in prime areas and competition from delivery-only cloud kitchens, which cut costs by eliminating front-of-house operations, pose challenges.

Lodging-based outlets are growing the fastest among location types, with a 14.75% annual growth rate through 2031. In 2024, Turkey attracted 60.4 million tourists, and achieved a 70.5% hotel occupancy rate, driving demand for hotel foodservice. Antalya, with 17 million visitors in 2024, is a key hub, while operators like Nusr-Et have expanded in Istanbul, Bodrum, and Marmaris to cater to affluent tourists seeking premium dining[2]Republic of Türkiye Ministry of Culture and Tourism. "Tourism Statistics", ktb.gov.tr. Lodging outlets benefit from higher check averages, steady traffic, and opportunities to sell alcohol and premium items. However, they are vulnerable to seasonal tourism and economic downturns. Retail, leisure, and travel outlets grow more slowly due to landlord restrictions, revenue-sharing agreements, and dependence on anchor tenants or transportation hubs that limit their flexibility.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Dine-In's Base Meets Delivery's Velocity

In 2025, dine-in services accounted for 55.71% of Turkey's foodservice market, driven by a cultural preference for social dining and full-service restaurants offering ambiance, table service, and diverse menus. Cafés like Starbucks, with 685 outlets, and Espressolab, with 160 locations, attract urban professionals and students using these spaces as work and social hubs. Full-service restaurants cater to families, business diners, and tourists seeking relaxed meals. However, dine-in growth faces challenges such as high labor costs, expensive real estate, and economic downturns, which push consumers toward more affordable and convenient options like QSRs and delivery services.

Delivery channels are growing at 15.57% annually through 2031, the fastest among service types. Uber's USD 700 million acquisition of 85% of Trendyol GO in May 2025 and its negotiations to buy Getir Food for USD 1 billion are accelerating digital adoption and consolidating aggregator control. DP Eurasia reports most Domino's delivery sales come from online channels, while aggregators hold 61.8% of Turkey's delivery sales, highlighting the risks for restaurants without proprietary apps. Takeaway services grow slower, appealing to cost-conscious consumers who prefer picking up orders to avoid delivery fees. However, aggregator-subsidized delivery costs are shifting consumer habits toward on-demand convenience, reducing takeaway's market share.

Geography Analysis

Turkey's foodservice market is driven by key cities like Istanbul, Ankara, Izmir, Antalya, and Bodrum. Antalya attracts 17 million visitors annually, boosting demand for both tourist-focused and local outlets. Istanbul, with its corporate hubs, universities, and cultural sites, supports Starbucks Turkey's 685 stores, TAB Gıda's Burger King and Popeyes units, and Migros' 35-40 cloud kitchens, serving 16 million residents and visitors. Seasonal tourism in Antalya and Bodrum contributes to a 70.5% national hotel occupancy rate in 2024, with tourists spending around USD 900 per visit. This ensures steady revenue for restaurants offering Turkish cuisine and premium dining. Izmir's industrial and port activities sustain year-round demand, while Ankara's government and diplomatic presence supports corporate catering and business dining.

Secondary cities like Bursa, Adana, and Gaziantep are seeing rapid chain expansions as operators move beyond saturated top-tier markets. Migros, with 3,621 stores across all 81 provinces, added 356 new outlets in 2024. Its Migros Yemek delivery platform expanded nationwide by 2023, showing how digital platforms can unlock demand in smaller cities where traditional stores face challenges like lower population density and purchasing power. Rural and eastern regions remain underserved due to cold-chain gaps, longer logistics, and lower incomes. However, these areas offer opportunities for value-focused QSR formats and local chains willing to adapt menus and accept lower margins for first-mover advantages.

Turkey aims to attract 90 million visitors by 2028, up from 60.4 million in 2024, benefiting coastal and cultural destinations. This strengthens Istanbul, Antalya, Izmir, and Bodrum while creating demand in nearby provinces like Muğla, Aydın, and Çanakkale, known for resorts and archaeological sites. Operators in these secondary markets must manage seasonal fluctuations but can capitalize on high tourist spending during peak periods. Many adopt hybrid models, serving locals year-round and scaling up during peak seasons. Government investments in airports, highways, and convention centers support this growth, enabling chains to expand into emerging markets and independents to improve operations with centralized supply chains and digital platforms.

Competitive Landscape

The Turkey foodservice market is fragmented, with a large number of independent restaurants, cafés, street food vendors, and small family-owned eateries operating alongside national and international chains. Key players in the market include DP Eurasia NV, Simit Sarayi Yatirim Ve Ticaret Anonim Sirketi, TAB Gida, Anadolu Group (McDonald’s), and Alshaya Group (Shaya Kahve). Traditional food outlets, including kebab houses, lokantas, bakeries, and tea cafés, form the backbone of the market and are deeply embedded in local dining culture. This high presence of small operators limits market concentration and ensures that no single company or group of brands holds a dominant position across the country.

Organized foodservice chains are expanding, particularly in quick-service restaurants, fast-casual formats, and coffee chains, driven by urbanization and changing consumer lifestyles. However, their overall share remains constrained by strong consumer loyalty to local establishments, regional cuisine preferences, and price sensitivity. Many independent operators compete effectively through personalized service, localized menus, and flexible pricing, which continues to sustain a highly competitive and diverse market structure.

Competition in the Turkey foodservice market is shaped more by location, menu variety, and service quality than by scale advantages. Digital food delivery platforms have further intensified fragmentation by enabling small restaurants to reach a wider customer base without significant investment in physical expansion. As a result, while selective consolidation is occurring in chain-led segments, the dominance of independent outlets and traditional dining formats maintains the fragmented nature of the Turkey foodservice market.

Turkey Foodservice Industry Leaders

-

DP Eurasia NV

-

Simit Sarayi Yatirim Ve Ticaret Anonim Sirketi

-

TAB Gida

-

Anadolu Group (McDonald’s)

-

Alshaya Group (Shaya Kahve)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kentucky Fried Chicken (KFC), one of the leading fast-food chains, has signed a new franchise agreement in Türkiye with local operator HD Holding, which plans to relaunch and expand the restaurant network with the first outlets.

- June 2025: ROKA launched in Turkey with a dual launch at Mandarin Oriental, Bodrum. According to the brand, the Japanese robatayaki concept expands Azumi Group’s footprint with new fine dining and beachside experiences.

- December 2024: Carla, as part of the expansion, opened in Istanbul's Kuruçeşme district. Carla, with its sustainable gastronomic approach, rich cocktail bar, and impressive DJ performances. According to the brand, it hosts brunch events on Sundays and parties on Friday and Saturday evenings.

Turkey Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| Outlet | Chained Outlets | ||

| Independent Outlets | |||

| Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms