Turf Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

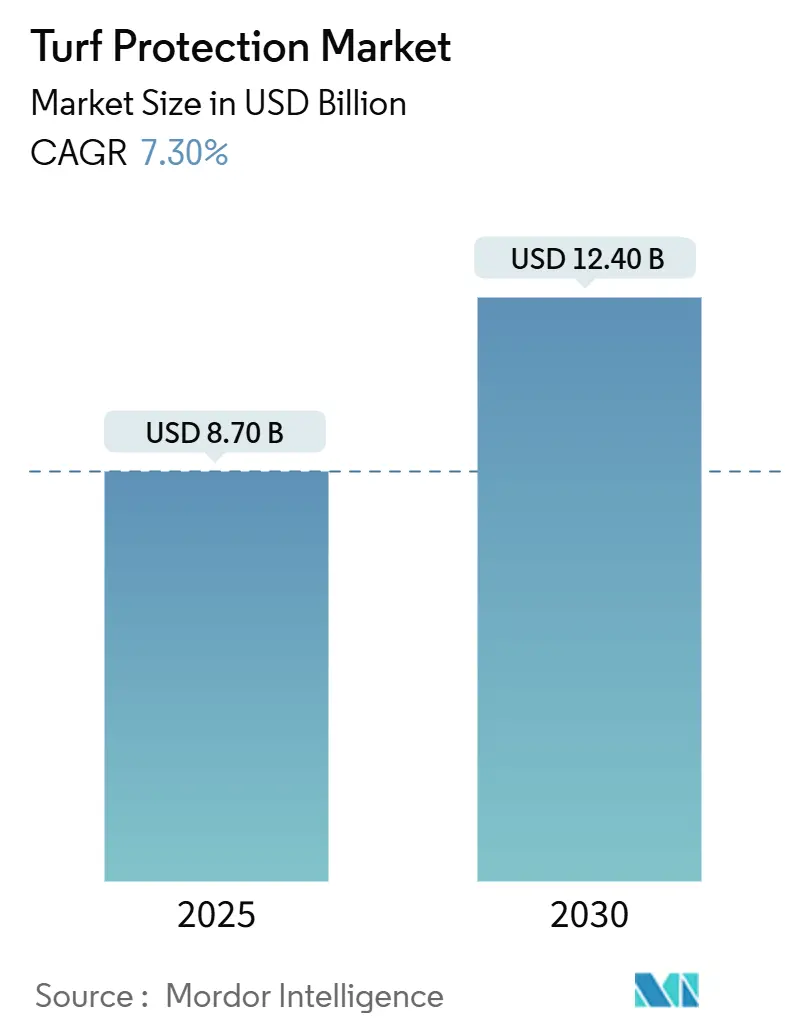

| Market Size (2025) | USD 8.70 Billion |

| Market Size (2030) | USD 12.40 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

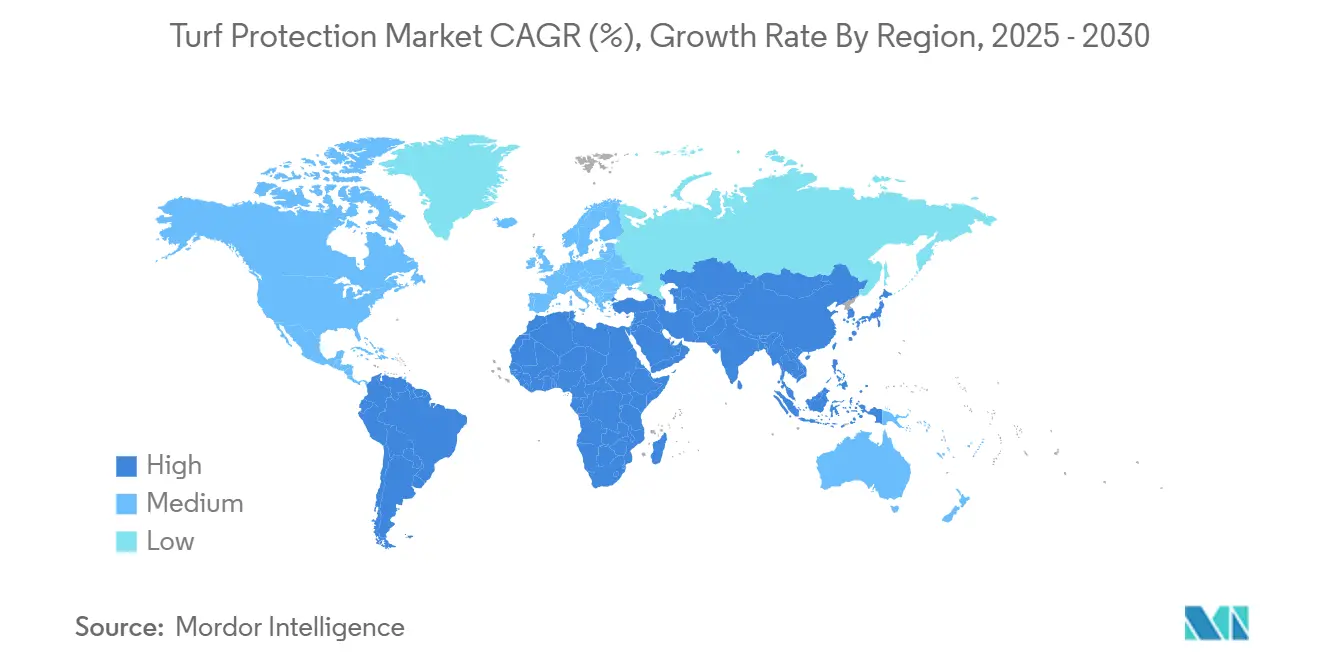

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

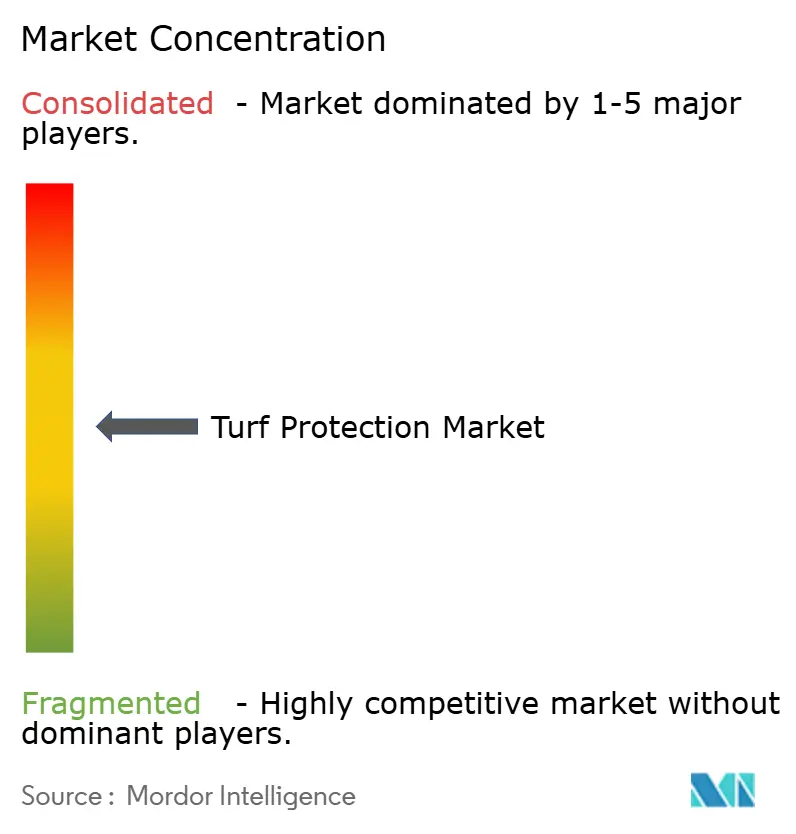

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Turf Protection Market Analysis by Mordor Intelligence

The turf protection market size stands at USD 8.7 billion in 2025 and is forecast to reach USD 12.4 billion by 2030, translating into a 7.3% CAGR over the period. This expansion reflects accelerating investment in golf courses, professional sports venues, and high-end residential landscapes that demand resilient, visually appealing playing and leisure surfaces. Rising climate volatility, tighter player-safety standards, and the shift toward integrated pest-management programs are lifting demand for advanced fungicides, biostimulants, and precision application technologies. Biological products are registering double-digit growth as regulators scrutinize synthetic chemistries and owners look to reduce environmental footprints. On the competitive front, the top five suppliers account for the majority share in global revenue, with Syngenta accounting for the highest share, followed by Bayer CropScience yet fragmentation still enables regional specialists to penetrate niches such as biostimulants and precision-sensor packages. North America sustains leadership due to mature sports infrastructure and high household spending on lawn care, while Asia-Pacific logs the fastest gains as urbanization and mega-facility construction spur incremental demand.

Key Report Takeaways

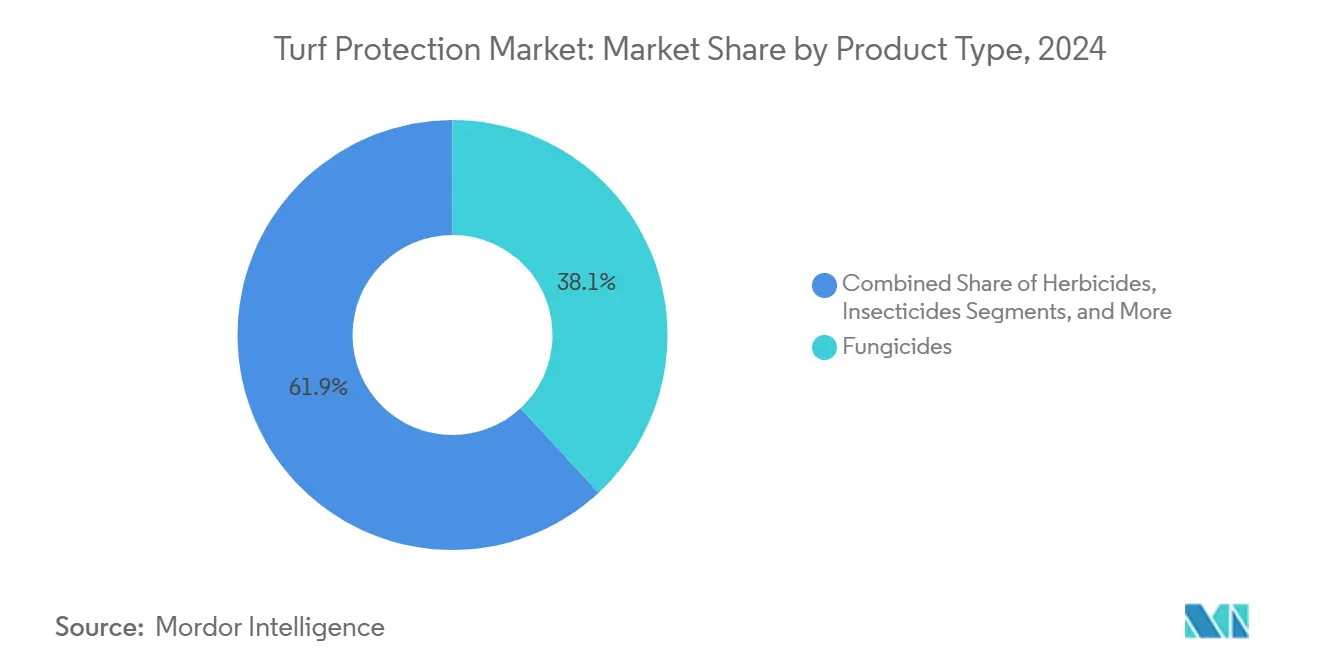

- By product type, fungicides led with a 38.1% turf protection market share in 2024, while biostimulants are projected to rise at an 11.5% CAGR through 2030.

- By application, landscaping accounted for 42.5% of the turf protection market size in 2024; sports fields are forecast to expand at a 9.8% CAGR by 2030.

- By end-user, residential customers held 46.0% of the turf protection market share in 2024, whereas sports facility owners are set to record a 9.3% CAGR between 2025 and 2030.

- By mode of action, chemical formulations captured 72.0% of revenue in 2024, but biological solutions are advancing at a 12.2% CAGR.

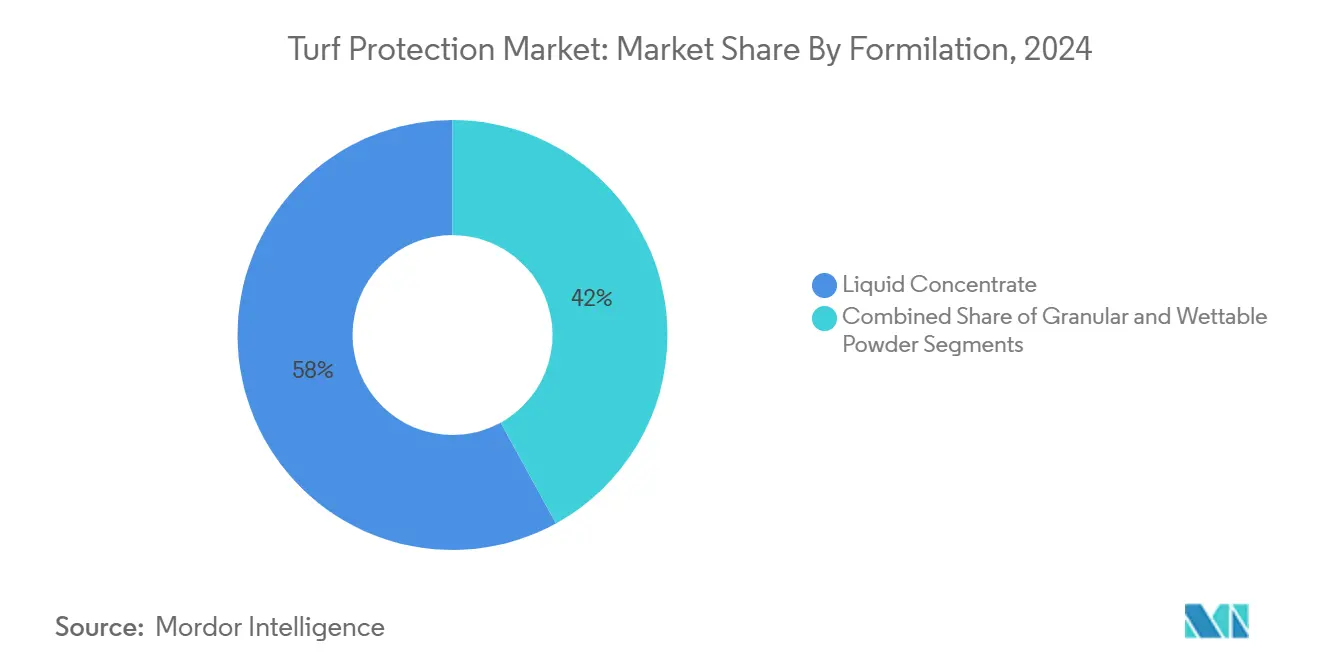

- By formulation, liquid concentrates represented 58.0% of sales in 2024 and will post a 10.9% CAGR over the forecast horizon.

- By region, North America held 35.0% of the turf protection market in 2024, while Asia-Pacific will accelerate at an 8.7% CAGR through 2030.

- By company, the five largest players collectively controlled 51.1% of the turf protection market share in 2024; Syngenta led with 15.2% followed by Bayer CropScience at 12.8%.

Global Turf Protection Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction of golf courses and professional sports venues | +1.8% | Global, highest in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Increasing incidence of turfgrass diseases | +1.5% | North America and Europe | Short term (≤ 2 years) |

| Growing residential demand for aesthetic lawns | +1.2% | North America and Europe | Medium term (2-4 years) |

| Shift toward biological fungicides and biostimulants | +1.0% | Europe and North America | Long term (≥ 4 years) |

| Adoption of sensor-based precision turf management | +0.8% | North America, Europe, and developed Asia-Pacific | Long term (≥ 4 years) |

| Climate-change-induced heat-stress mitigation solutions | +0.9% | Warmer global regions | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Construction of Golf Courses and Professional Sports Venues

Capital allocations for new facilities surged after the pandemic, particularly across India, China, and Gulf states, creating steady pull-through demand for hybrid turf systems that balance durability with natural playability. Professional leagues have formalized surface-quality metrics, prompting venue owners to specify fungicides, plant growth regulators, and stress-mitigation products that pass stricter safety tests. Once built, each venue requires season-long disease control, anchoring recurring revenue for suppliers. Developers also lean on integrated packages that bundle seed, nutrition, and digital monitoring, opening cross-selling opportunities in the turf protection market.

Increasing Incidence of Turfgrass Disease

Milder winters and prolonged humidity are intensifying outbreaks of dollar spot and brown patch, prompting superintendents to adopt dynamic rotation programs that respond to real-time pathogen pressure instead of calendar schedules. Research shows tall fescue plots receiving high nitrogen suffer 40% higher brown patch severity than moderately fertilized turf, underscoring the need for balanced nutrition strategies. Advanced diagnostic kits and AI models now detect dollar spot with 97% accuracy, enabling earlier interventions and optimized fungicide loads. The trend is pushing the turf protection industry toward predictive analytics and site-specific treatments that preserve beneficial soil organisms.

Growing Residential Demand for Aesthetic Lawns

Homeowners increasingly view lawn quality as an asset that supports property valuation and outdoor lifestyles. Products such as Primo Maxx cut mowing frequency by up to 50% while thickening turf canopies, positioning growth regulators as a retail staple. Drought regulations in western states favor low-maintenance, water-efficient blends supplemented with biostimulants. Retailers are widening their premium shelves, letting do-it-yourself consumers access formerly trade-only technologies, which further broadens the turf protection market.

Shift Toward Biological Fungicides and Biostimulants

Environmental policy and public pressure against synthetic residues are propelling biological inputs. Corteva’s Bexfond forms microbial bio-barriers that suppress soil pathogens and stimulate root vigor, exemplifying next-generation offerings. The European Union’s microplastic restrictions in artificial turf are also nudging facility owners toward natural surfaces fortified with bio-solutions. Enhanced shelf stability, easy-to-mix formulations, and evidence of improved drought tolerance have expanded adoption among high-end courses and sports complexes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of artificial turf solutions | −1.2% | Global, water-scarce regions | Medium term (2-4 years) |

| High R&D cost for novel chemistries | −0.8% | Global | Long term (≥ 4 years) |

| Regulatory pressure on conventional fungicides | −1.0% | Europe and North America | Short term (≤ 2 years) |

| Micro- and nanoplastic pollution concerns from turf inputs | −0.6% | Europe, North America, Australia | Medium term (2-4 years) |

Source: Mordor Intelligence

Rapid Penetration of Artificial Turf Solutions

Synthetic fields eliminate routine mowing and pesticide spending, enticing school boards and municipalities wrestling with labor and water constraints. Installations in the United States now run between 1,200 and 1,500 per year[1]Source: Environmental Health News, “EU Microplastic Restrictions,” ehn.org. Nonetheless, PFAS contamination findings and microplastic-shed estimates of 16,000 tons annually in Europe have triggered policy reviews that could stall conversions and breathe life into natural alternatives. Turf protection vendors are responding with hybrid technology and communication campaigns highlighting the health and sustainability benefits of natural systems.

Regulatory Pressure on Conventional Fungicides

The U.S. Environmental Protection Agency’s interim decision on chlorothalonil imposes tighter application windows and label amendments, pressuring distributors to reformulate portfolios[2]Source: GCSAA, “EPA Issues Chlorothalonil Decision,” gcsaa.org. Europe’s Sustainable Use Regulation similarly curbs certain strobilurins. These moves accelerate the migration to integrated programs but could temporarily dampen sales of legacy products.

Segment Analysis

By Product Type: Biologicals Drive Innovation

Fungicides generated the largest slice of turf protection market revenue with a 38.1% share in 2024, reflecting the continual threat of dollar spot, brown patch, and Pythium. Sophisticated rotation plans mixing SDHI, QoI, and DMI chemistry remain indispensable for courses aiming to maintain tournament-grade surfaces. However, biostimulants, posting an 11.5% CAGR, highlight the market’s pivot toward sustainable inputs backed by proven stress tolerance and root health gains. Herbicides corner roughly 31.4% of demand as managers tackle annual bluegrass and broadleaf weeds, while plant growth regulators find traction by trimming mower fuel and labor costs.

The turf protection market size for plant growth regulators is poised to expand alongside heightened labor constraints and sustainability targets. Iron-based alternatives and microbial cocktails now supplement conventional fungicides, demonstrating equivalent dollar spot suppression with lower environmental risk. Biologicals and synthetics are spawning co-formulations that enhance uptake and persistence, broadening choice for superintendents.

Note: Segment share of all individual segments available upon report purchase

By Application: Sports Fields Accelerate Growth

Landscaping maintained 42.5% of overall demand in 2024, supported by steady residential and commercial spending on curb appeal. Product mixes focus on broad-spectrum weed control, slow-release nutrition, and colorants that deliver a uniform appearance. In contrast, sports fields are heading the growth table at 9.8% CAGR as franchises and universities prioritize athlete safety and surface consistency. The NFL’s push for standardized field testing is already shaping purchasing specifications toward high-performance fungicide programs and hybrid overseeding blends.

The turf protection market size dedicated to golf courses remains sizable at 28.6%, but growth plateaus relative to sports arenas as many mature courses transition from capital expansion to renovation mode. Sod farms, while niche, exert influence through their role in supplying disease-free rolls that demand intensive pest shielding.

By End-User: Facility Owners Lead Precision Adoption

Homeowners purchased 46.0% of turf protection products in 2024, reflecting easy access to pro-grade formulations through big-box and e-commerce outlets. Clear labeling, hose-end sprayers, and subscription lawn-care kits simplify adoption, feeding segment momentum. Sports facility owners, expanding at 9.3% CAGR, reflect the surge in semi-professional leagues and community recreation complexes that demand stadium-quality surfaces.

Commercial landscape contractors command 41.2% of purchases and increasingly bundle agronomic consulting, irrigation installs, and digital monitoring into service contracts. Private-equity investment is fueling consolidation among contractors, enabling bulk procurement and vendor partnerships that shape turf protection market dynamics.

By Formulation: Liquid Concentrates Dominate

Liquid concentrates captured 58.0% of sales in 2024 and posted the fastest growth at 10.9% CAGR because they dissolve quickly, support tank mixes, and suit precision booms. Encapsulation advances such as Corteva’s Enversa 3CS extend residual life and crop safety, making liquids even more attractive. Granulars still play a vital role in pre-emergent herbicide programs and combination fertilizer products, favored for slow release and ease of application through broadcast spreaders.

Ultra-low-volume liquids are emerging, requiring less carrier and supporting drone-based treatments. Such innovation aligns with sustainability goals and labor savings, reinforcing the leading position of liquid concentrates in the turf protection market.

By Mode of Action: Integrated Solutions Gain Traction

Chemical still accounted for 72.0% of revenue in 2024 on the strength of broad-spectrum activity and predictable results. Yet, biological inputs are growing at 12.2% CAGR as university trials demonstrate performance against Rhizoctonia and Fusarium comparable to synthetics. Integrated programs blending Bacillus strains with reduced-rate fungicides deliver resistance management benefits and environmental relief.

The turf protection market share for pure biologicals is expected to rise as pending reviews of older actives push buyers toward lower-risk options. Ultraviolet treatments and heat-shock applications appear on the horizon as non-chemical complements, underscoring the market’s continuous diversification.

Geography Analysis

North America retained 35.0% of global revenue in 2024, anchored by more than 15,000 golf courses and one of the world’s largest portfolios of professional stadiums. The United States represents roughly 90% of regional demand and benefits from the early adoption of IoT soil probes and AI spray scheduling tools. Canada’s shorter growing window concentrates disease outbreaks into intense summer peaks, encouraging premium fungicide programs. Mexico’s resort corridors channel investment into salt-tolerant turf cultivars and fertility programs that thrive in coastal soils.

Asia-Pacific is projected to clock an 8.7% CAGR, the fastest worldwide. China’s research institutes are expanding germplasm collections for stress-resistant turf, but course operators still import many premium cultivars. India’s urban golf and cricket infrastructure underpins robust demand for fungicide and growth-regulator packages capable of withstanding monsoon swings. Japan’s mature golf scene is pivoting toward precision irrigation and biological inputs to meet government sustainability targets. Australian course managers face stringent water quotas, increasing reliance on wetting agents and drought-resilient blends to safeguard playing quality.

Europe remains a technology- and regulation-driven arena. The European Commission’s push for sustainable pesticide use and microplastic bans incentivizes biological programs and biodegradable carriers[3]Source: European Commission, “Proposal for Restricting Microplastics,” ec.europa.eu. Germany and the United Kingdom spearhead the uptake of connected-sensor networks that fine-tune fungicide timing. France’s grounds crews are early adopters of biostimulant seed treatments to comply with national pesticide-reduction objectives, showcasing how policy influences procurement choices.

Competitive Landscape

The turf protection market is moderately fragmented; the top five suppliers hold a combined 51.1%. Syngenta leads with a 15.2% share, leveraging the Heritage fungicide franchise and GreenCast digital advisory platform. Bayer CropScience follows at 12.8%, differentiating through combined chemical and biological pipelines. BASF ranks third at 10.4% and sets itself apart via AI-powered decision support tools and substantial R&D funding.

Consolidation is gaining pace. Envu’s 2024 purchase of FMC’s turf division expanded its footprint in professional segment fungicides and insecticides. Bigger players are also pouring resources into biologicals; Corteva’s launch of Bacillus-based Bexfond and Syngenta’s acquisition of Valagro exemplify the pivot. Smaller innovators compete on specialization, offering niche growth regulators or stress-tolerance enhancers that large players may later acquire.

Technology is an increasingly decisive battleground. BASF’s Xarvio suite couples weather analytics with disease models to boost spray precision, while Syngenta pilots machine-vision scouting robots. Partnerships with sensor manufacturers and software developers are common as vendors strive to integrate product portfolios with real-time agronomic advice, deepening customer lock-in, and expanding recurring revenue streams.

Turf Protection Industry Leaders

-

Syngenta AG

-

Bayer Cropscience AG

-

BASF SE

-

UPL Limited

-

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Syngenta announced the launch of TREFINTI Turf nematicide. Developed exclusively for nematode management, TREFINTI introduces a new active ingredient with strong activity and low use rates as an unscheduled product.

- January 2025: The EPA finalized interim registration review for chlorothalonil, tightening use limits and mandating revised labels.

- July 2024: Envu completed the acquisition of FMC’s turf assets, reinforcing its professional turf presence.

- May 2024: BASF launched its all-new dual-active fungicide known as Aramax Intrinsic brand fungicide. This is designed to deliver control of 26 cool- and warm-season turf diseases, like snow mold, large patch, brown patch, and dollar spot on golf course fairways.

Global Turf Protection Market Report Scope

Turf protection chemicals shield turfgrass from pests and diseases, simultaneously boosting its health and appearance. These products include fungicides, insecticides, herbicides, and nematicides. The Turf Protection Market is segmented into Application (Landscaping, Golf, Sports, and Other Applications) and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

| By Product Type | Fungicides | ||

| Herbicides | |||

| Insecticides | |||

| Plant Growth Regulators | |||

| Biostimulants and Bio-fertilizers | |||

| By Application | Landscaping | ||

| Golf Courses | |||

| Sports Fields | |||

| Sod Farms | |||

| By End-user | Residential Customers | ||

| Commercial Landscape Contractors | |||

| Sports Facility Owners | |||

| Municipalities and Schools | |||

| By Mode of Action | Chemical | ||

| Biological | |||

| Integrated Solutions | |||

| By Formulation | Granular | ||

| Liquid Concentrate | |||

| Wettable Powder | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of the North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East | Saudi Arabia | ||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| Fungicides |

| Herbicides |

| Insecticides |

| Plant Growth Regulators |

| Biostimulants and Bio-fertilizers |

| Landscaping |

| Golf Courses |

| Sports Fields |

| Sod Farms |

| Residential Customers |

| Commercial Landscape Contractors |

| Sports Facility Owners |

| Municipalities and Schools |

| Chemical |

| Biological |

| Integrated Solutions |

| Granular |

| Liquid Concentrate |

| Wettable Powder |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of the North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current value of the turf protection market?

It is valued at USD 8.7 billion in 2025 and is projected to hit USD 12.4 billion by 2030.

Which region leads turf protection spending?

North America holds 35.0% of global revenue owing to its dense golf and professional sports infrastructure.

Why are biological turf products growing faster than chemicals?

Regulatory pressure on conventional fungicides and demand for sustainable solutions are propelling biologicals at a 12.2% CAGR.

What application segment is expanding the quickest?

Sports fields post the highest growth at 9.8% CAGR as leagues enforce stricter player -safety and surface-quality standards.

How concentrated is the competitive landscape?

The top five companies command just over half of global sales, indicating moderate concentration and room for niche innovators.

Which formulation type is most popular?

Liquid concentrates lead with a 58.0% share, favored for ease of mixing and compatibility with precision-spray equipment.

Page last updated on: June 24, 2025