Tungsten Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

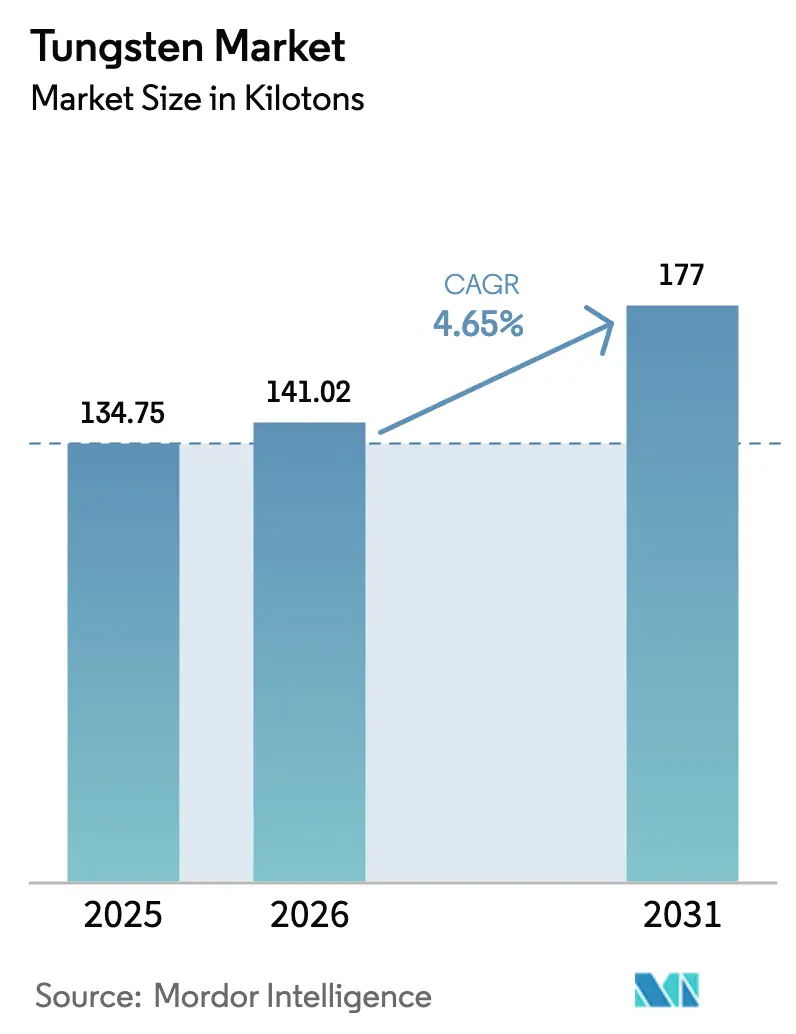

| Market Volume (2026) | 141.02 kilotons |

| Market Volume (2031) | 177 kilotons |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

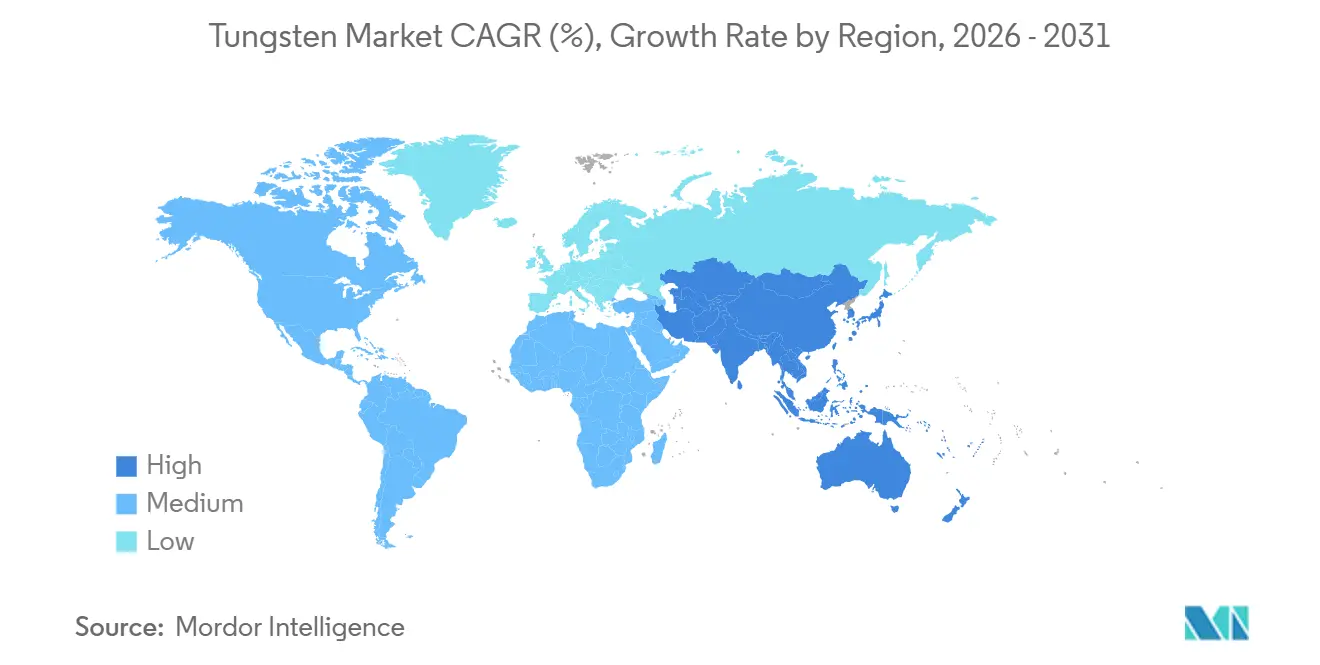

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tungsten Market Analysis by Mordor Intelligence

The Tungsten Market size was valued at 134.75 kilotons in 2025 and is estimated to grow from 141.02 kilotons in 2026 to reach 177 kilotons by 2031, at a CAGR of 4.65% during the forecast period (2026-2031). Structural shifts in precision manufacturing, defense procurement, and next-generation energy storage are sustaining demand even when commodity prices soften. Wire continues to dominate in electrical-discharge machining and high-temperature furnaces, while tubes post the fastest growth as aerospace OEMs specify tungsten-alloy nozzles for hypersonic propulsion. Tungsten carbide retains a majority share thanks to cutting-tool applications, yet chemicals such as ammonium paratungstate and tungsten hexafluoride are expanding swiftly on the back of semiconductor and battery usage. Vertically integrated Chinese suppliers are broadening their reach, but recyclers in Vietnam, Rwanda, and India are easing supply-chain risk for Western buyers. Rising regulatory pressure on dust exposure and export-quota uncertainty are moderating the pace but have not derailed the long-term trajectory of the tungsten market.

Key Report Takeaways

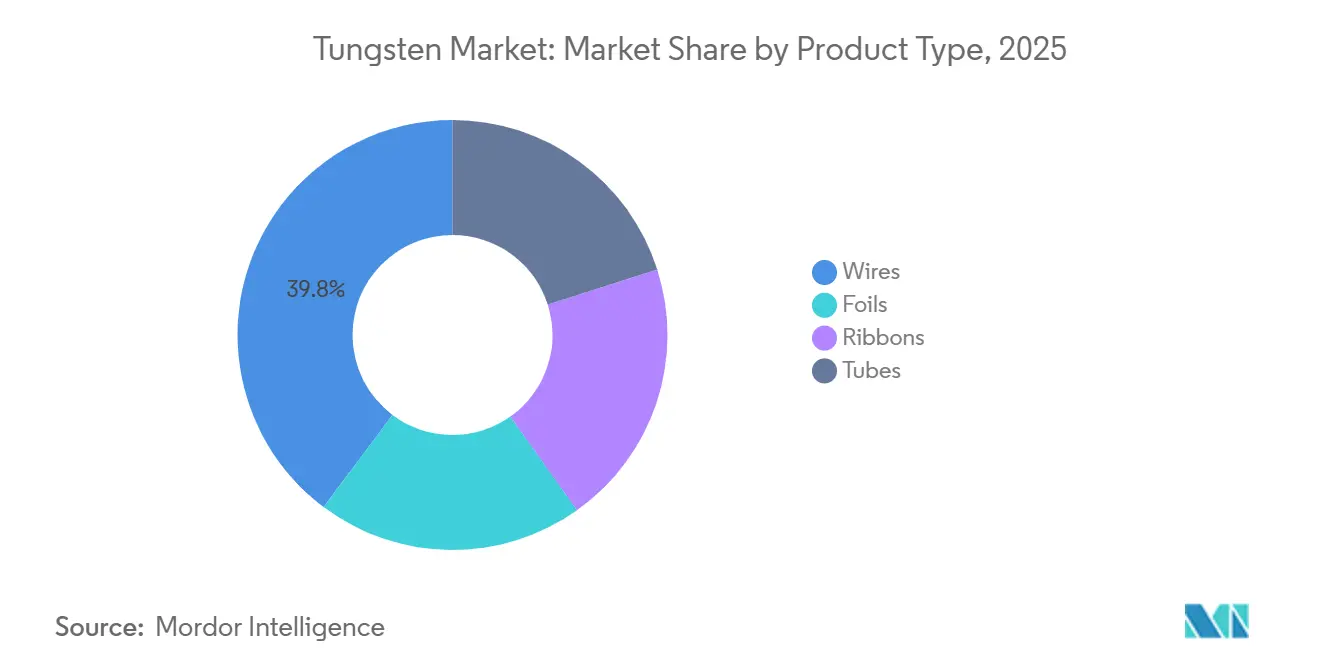

- By product type, wires held 39.75% of the Tungsten market share in 2025, whereas tubes are advancing at a 5.10% CAGR through 2031.

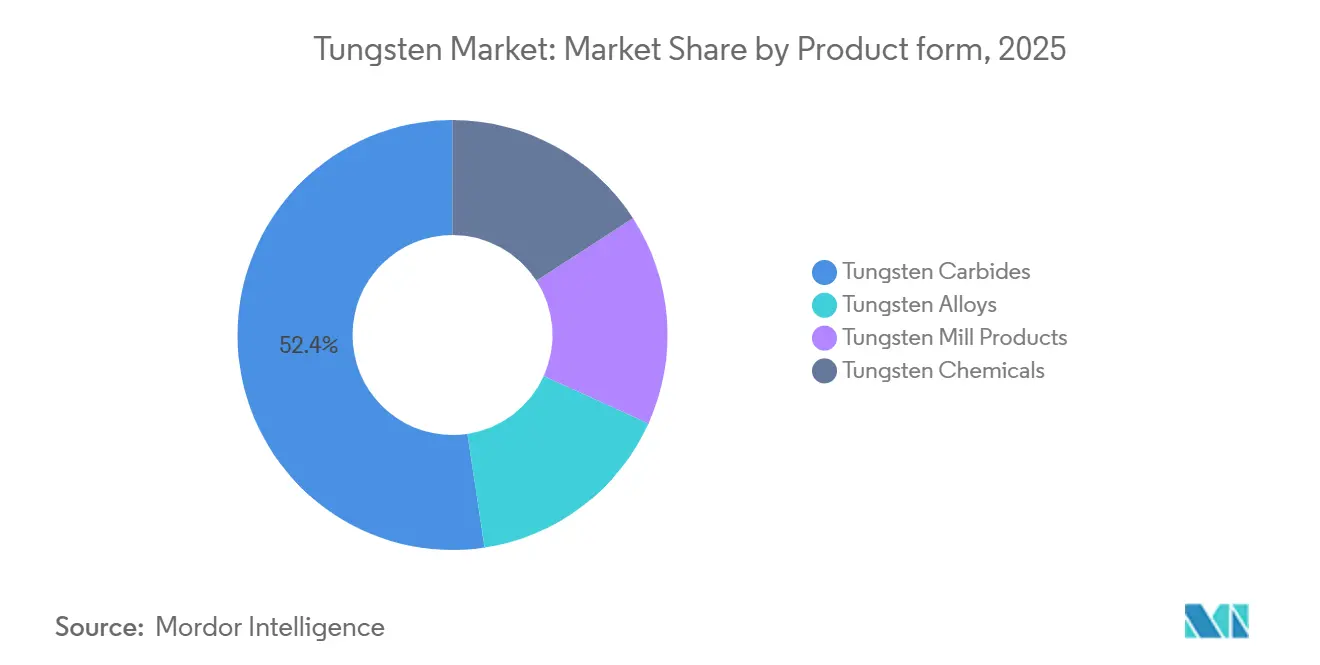

- By product form, tungsten carbide accounted for 52.38% share of the Tungsten market size in 2025; tungsten chemicals are projected to expand at 5.48% CAGR between 2026 and 2031.

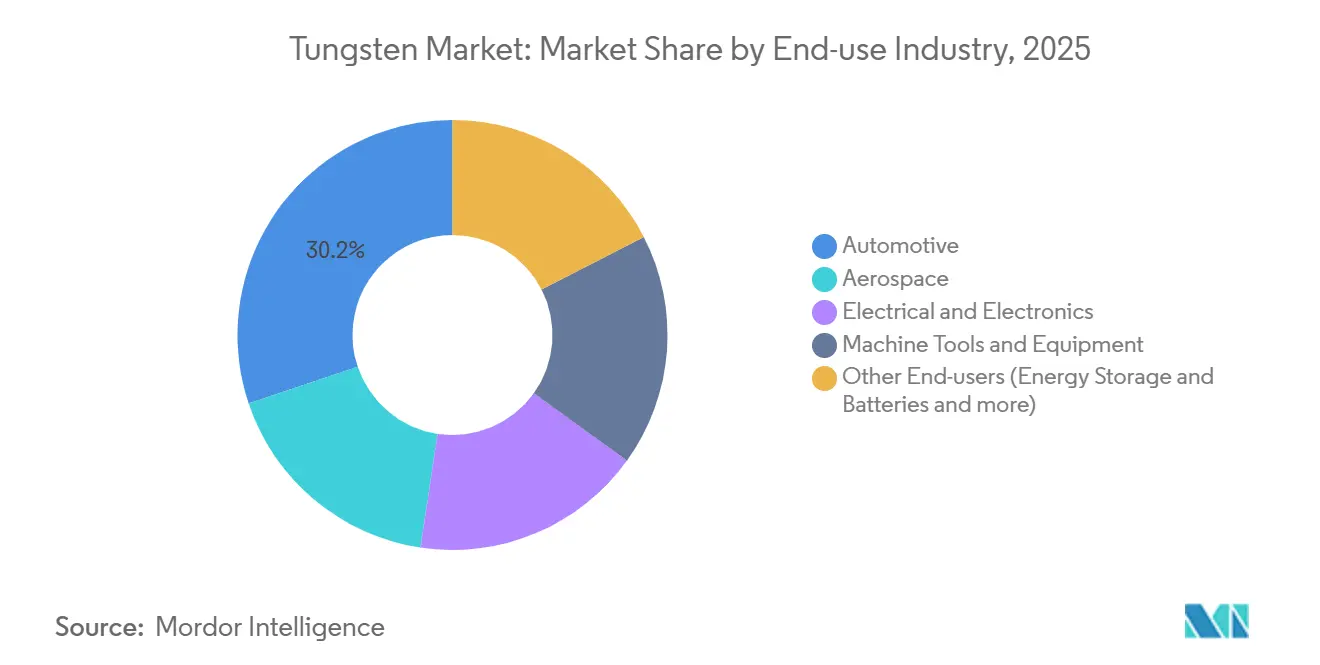

- By end-use, automotive commanded 30.16% of demand in 2025, while the other end-user industries, which include batteries and medical imaging, are growing at a 5.29% CAGR through 2031.

- By geography, Asia-Pacific captured 58.28% of the 2025 volume and is forecast to grow at a 5.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tungsten Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cemented-carbide cutting tools in automotive and aerospace | +1.2% | Global (Germany, Japan, United States, China) | Medium term (2-4 years) |

| Electronics miniaturization with high-density interconnects | +0.9% | Taiwan, South Korea, Japan, United States | Long term (≥ 4 years) |

| Defense adoption of kinetic-energy penetrators | +0.6% | North America, Europe, India | Medium term (2-4 years) |

| Li-ion and solid-state batteries using tungsten disulfide | +0.8% | China, South Korea, Japan, United States | Long term (≥ 4 years) |

| Additive manufacturing of radiation-shielding parts | +0.5% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand Surge From Cemented-Carbide Cutting Tools in Automotive and Aerospace

Cemented-carbide inserts remain indispensable for machining hardened steels, titanium, and aluminum composites in powertrain and airframe components. The shift to electric vehicles raises tolerance demands on battery housings, prompting OEMs to specify ultra-fine-grain carbide grades with cobalt binders below 6 wt% to minimize magnetic interference near cells. Aerospace primes are adopting diamond-like-carbon-coated carbide end mills that cut carbon-fiber panels 25% faster while extending life beyond 10,000 parts per edge[1]Sandvik AB, “2024 Annual Report,” home.sandvik. ISO 513:2024 reclassified grade nomenclature, triggering a tooling refresh cycle that keeps replacement demand buoyant. Tier-1 suppliers in Germany and Japan are consolidating purchases with integrated producers that co-engineer geometry and coatings, a dynamic that supports premium pricing.

Electronics Miniaturization Boosting High-Density Interconnects

Semiconductor manufacturers are shifting from aluminum to tungsten for via-fill and contact metallization at sub-3-nanometer nodes. Intel’s 18A process, entering high-volume production in late 2025, consumes roughly 15 g of tungsten hexafluoride per 300 mm wafer. TSMC expanded tungsten-CVD capacity by 40% in 2024 to backstop its 2 nm ramp. Samsung filed a dozen patents on atomic-layer-deposited WS₂ barriers, pointing to broader adoption of two-dimensional tungsten compounds. Advanced packaging needs—chiplets and 3D stacking—are multiplying tungsten usage per device, making electronics a resilient growth pillar for the tungsten market.

Defense Adoption of Kinetic-Energy Penetrators

Western militaries are replacing depleted-uranium rounds with tungsten-heavy alloys that offer densities of 17-18.5 g cm⁻³ minus radiological concerns. The US Army’s USD 47 million contract with Allegheny Technologies in 2024 secures billet supply through 2027[2]U.S. Department of Defense, “Contract Awards August 2024,” defense.gov. India’s DRDO validated homegrown penetrators performing within 5% of uranium analogs at 1,700 m s⁻¹ impact speeds. NATO ammunition-replenishment programs are pulling forward demand and tightening spot availability, lengthening commercial lead times from 8 weeks to 14 weeks.

Li-Ion and Solid-State Batteries Using Tungsten-Disulfide Anodes

Nature Energy reported that adding 5 wt% WS₂ nanosheets tripled lithium-ion cycle life to 1,500 cycles at 1C. QuantumScape is evaluating tungsten-oxide coatings to curb interface resistance in solid-state prototypes slated for pilot trials in 2026. CATL’s 2025 patent spree on high-purity WS₂ synthesis underscores commercial intent for its Qilin cells. These battery applications underpin the fastest-growing product-form segment—tungsten chemicals—inside the broader tungsten market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China-centric supply volatility and export quotas | -0.8% | Global (acute in North America, Europe) | Short term (≤ 2 years) |

| Health risks from tungsten-carbide dust exposure | -0.4% | Europe, North America | Medium term (2-4 years) |

| Substitution by advanced ceramics and cermets | -0.6% | Global (cutting-tool niche) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China-Centric Supply Volatility and Export Quotas

Beijing’s 2024 export-licensing rule for tungsten powder, carbide, and alloys amplified uncertainty for Western buyers. Spot prices for ammonium paratungstate rose 22% in two months before easing as European consumers drew down stocks and Vietnamese smelters boosted secondary output. The US Geological Survey highlighted tungsten as high risk since domestic mining ended in 2015, and the National Defense Stockpile holds only 15% of the authorized level. Alternative supply from Rwanda and South Korea will cover less than 8% of European demand by 2028, leaving exposure elevated.

Health Risks of Tungsten-Carbide Dust Exposure

The European Chemicals Agency added tungsten carbide with cobalt to its REACH Authorization List in 2024, requiring permits by 2027. OSHA proposed a tenfold stricter US exposure limit in 2025, pushing small shops to spend USD 50,000–200,000 on ventilation and surveillance upgrades. Some firms are switching to nickel- or iron-binder carbides, but the 10-15% lower rupture strength restricts use in interrupted cutting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wire Dominance Anchored in EDM and Furnace Applications

Wire captured 39.75% of the Tungsten market share in 2025, a lead it retains through 2031 because EDM shops and furnace builders rely on its unique high-temperature strength. Commodity filament wire is tapering with LED adoption, but precision-drawn grades for EDM and guidewires are rising 6% annually. Plansee’s 2025 lanthanum-oxide-doped wire raises recrystallization temperature to 1,800 °C, cutting scrap 12% for tool-and-die makers. Tubes are the fastest-growing product, clocking a 5.10% CAGR as hypersonic vehicle programs and MRI makers need thin-wall tungsten-rhenium thermocouples. Only four firms command rotary-swaging capabilities for sub-0.5 mm walls, creating a technological moat.

A smaller share belongs to foils and ribbons. Foils down to 0.025 mm shield X-ray sources and space electronics, while ribbons serve as evaporation boats in thin-film deposition. Demand is niche yet stable because few substitutes match tungsten’s 3,422 °C melting point. Collectively, these trends embed durable upsides for specialty manufacturers even as legacy lighting uses recede, helping the tungsten market maintain a balanced growth profile.

By Product Form: Carbide Supremacy Challenged by Chemical-Precursor Growth

Tungsten carbide commanded 52.38% of the tungsten market size in 2025, but growth is slower than the overall market. Innovation keeps margins healthy. Kennametal’s Beyond Blast inserts with sub-0.4 µm grains fetch a 25% premium. Tungsten chemicals are the breakout segment, rising 5.48% CAGR as semiconductor fabs add low-resistivity tungsten gates and battery firms scale WS₂ additives. Applied Materials saw a 35% jump in tungsten-CVD equipment orders in 2024, validating the uptrend.

Alloys and mill products serve defense, aerospace, and fusion-energy pilots. Tungsten-copper composites carrying 10–20% copper reach 180 W m⁻¹ K⁻¹ thermal conductivity, enabling 8–12% lighter EV busbars. Mill-product demand swings with furnace and fusion investments but shows a steady upward drift as India and Southeast Asia build heat-treat capacity. Together, these dynamics confirm that diversification beyond carbide is central to the sustainable expansion of the tungsten market.

By End-Use Industry: Automotive Still Leads While Batteries and Healthcare Accelerate

Automotive applications commanded 30.16% of the Tungsten market share in 2025 as cemented-carbide tooling remained indispensable for machining powertrain and body-in-white components. The transition to electric vehicles is not eroding volume, because precision machining of high-strength aluminum housings and stainless-steel exoskeletons raises insert consumption; Tesla disclosed that each Cybertruck battery pack uses 40% more carbide inserts than a Model 3 pack owing to tougher alloys. Internal-combustion machining is sliding in Europe and North America but stays buoyant in India and Southeast Asia, where ICE vehicles still dominate new-car output. Aerospace demand, though smaller, is rising in tandem with the 1,050 narrow-body jets Boeing and Airbus delivered in 2024, each requiring roughly 18 kg of tungsten for cutting tools, turbine-blade inserts, and landing-gear bushings.

The other category, encompassing batteries, medical imaging, and oncology, expanded the fastest at a 5.29% CAGR and is steadily enlarging its share of the overall tungsten market size. Lithium-ion and solid-state battery makers now blend tungsten-disulfide nanosheets and tungsten-oxide coatings into electrodes and separators; CATL’s Qilin cell adopted WS₂ interlayers that lifted energy density 13% to 255 Wh kg⁻¹ in 2024. Hospitals are upgrading to tungsten-rhenium X-ray targets that last 30% longer than pure-tungsten parts, trimming downtime and maintenance costs for radiology suites. Oncology centers are also adopting 3D-printed tungsten collimators for intensity-modulated radiotherapy, shrinking lead times from 12 weeks to 3 weeks and reinforcing long-term demand for additive-grade powders.

Geography Analysis

Asia-Pacific controlled 58.28% of 2025 volume and is on a 5.02% CAGR path to 2031. China integrates 75% of carbide and 90% of ammonium-paratungstate refining, pricing exports 25–35% below Western levels even after tariffs. India labeled tungsten a critical mineral in 2024 and fast-tracked Degana, targeting 1,800 t yr⁻¹ by 2028. Japan’s JPY 1.8 trillion machine-tool orders in 2024 keep ultra-fine-grain carbide demand buoyant. South Korean memory fabs push tungsten-CVD consumption as SK Hynix and Samsung expand 3D-NAND layers.

North America's lack of domestic mine output keeps exposure high, but a USD 200 million Defense Production Act allocation in 2024 aims to seed refining and recycling capacity. Canada’s Almonty will feed North American toolmakers when Sangdong starts in 2027. Mexico’s USD 5.2 billion auto FDI boom in 2024 raises carbide-tool needs for nearshored machining lines.

In Europe, German producers face Chinese carbide imports priced 30% lower even after a 6.5% anti-dumping duty. The 2024 Critical Raw Material Act mandates 15% recycled tungsten by 2030, prompting Umicore’s EUR 45 million Hoboken upgrade to process 3,000 t yr⁻¹ of scrap. Russian concentrate stays mostly domestic due to sanctions, while Rwanda’s newly commissioned concentrator feeds European smelters. Outside the big three regions, Latin America, Africa, and the Middle East jointly supplied around 8% of global volume, with Bolivia and Rwanda as notable contributors.

Competitive Landscape

The Tungsten market is moderately concentrated. Chinese leaders integrate mine to carbide-tool lines, letting them offer bundled contracts; Xiamen Tungsten internally consumes 68% of its carbide output, reducing exposure to spot swings. Western rivals pull ahead on engineering service and digital machining twins—Kennametal’s NOVO platform predicts insert life within 5%, cutting downtime and justifying 20-25% premiums. Process automation widens the gap between top players, who control density uniformity to ±0.2%, and smaller firms that still run batch-mode sintering. This divergence is likely to spur acquisitions as integrated majors hunt recycling capacity and niche alloy know-how.

Tungsten Industry Leaders

Xiamen Tungsten Co., Ltd.

China Minmetals Non-Ferrous Metals Co.

China Molybdenum Co., Ltd.

H.C. Starck Tungsten GmbH

Global Tungsten & Powders Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: It was reported that the United States (US) is backing Cove Kaz Capital Group LLC's private bid for Kazakhstan's Upper Kairakty and North Katpar tungsten deposits, facing off against state-backed Chinese contenders. This move underscores a strategic pivot: the US aims to reduce reliance on China's dominance in the mine-to-powder supply chains. Additionally, the US has set a 2027 procurement deadline.

- October 2025: The first shipment of tungsten concentrate (WO₃) from Trinity Metals’ Nyakabingo mine in Rwanda arrived at Global Tungsten and Powders’ (GTP) plant in Towanda, United States (US). GTP is the largest tungsten processor in the US and is part of Austria’s Plansee Group, a global manufacturer of tungsten-made components used in aerospace, defense, and industrial applications.

Global Tungsten Market Report Scope

Tungsten, often known as wolfram, is a chemical element that has the symbol W and the atomic number 74. Tungsten is a rare metal that occurs nearly entirely in nature in compounds with other metals.

The tungsten market is segmented by form, products, end-user industry, and geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). By form, the market is segmented into foils, ribbons, wires, and tubes. By products, the market is segmented into carbides, tungsten alloys, tungsten mill products, and tungsten chemicals. By end-user industry, the market is segmented into automotive, aerospace, machine tools and equipment, electrical and electronics, and other end-user industries. The report also covers the market size and forecasts for the concrete bonding agent market in 11 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD).

| Foils |

| Ribbons |

| Wires |

| Tubes |

| Tungsten Carbides |

| Tungsten Alloys |

| Tungsten Mill Products |

| Tungsten Chemicals |

| Automotive |

| Aerospace |

| Electrical and Electronics |

| Machine Tools and Equipment |

| Other End-users (Energy Storage and Batteries, Medical Imaging and Oncology) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Rest of the World | South America |

| Middle East and Africa |

| By Product Type | Foils | |

| Ribbons | ||

| Wires | ||

| Tubes | ||

| By Product Form | Tungsten Carbides | |

| Tungsten Alloys | ||

| Tungsten Mill Products | ||

| Tungsten Chemicals | ||

| By End-use Industry | Automotive | |

| Aerospace | ||

| Electrical and Electronics | ||

| Machine Tools and Equipment | ||

| Other End-users (Energy Storage and Batteries, Medical Imaging and Oncology) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Rest of the World | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the tungsten market?

The tungsten market size reached 141.02 kilotons in 2026 and is forecast at 177 kilotons by 2031.

What is the expected growth rate for tungsten demand?

Global demand is projected to expand at a 4.65% CAGR between 2026 and 2031.

Which product type leads consumption?

Wire products lead with 39.75% share in 2025, primarily due to EDM and furnace uses.

Why are tungsten chemicals growing faster than carbide?

Semiconductor interconnects and battery additives require high-purity chemicals, driving a 5.48% CAGR for the segment.

Which region dominates supply and demand?

Asia-Pacific holds 58.28% of global volume in 2025, with China integrating most mining and carbide capacity.

Page last updated on: