Germanium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

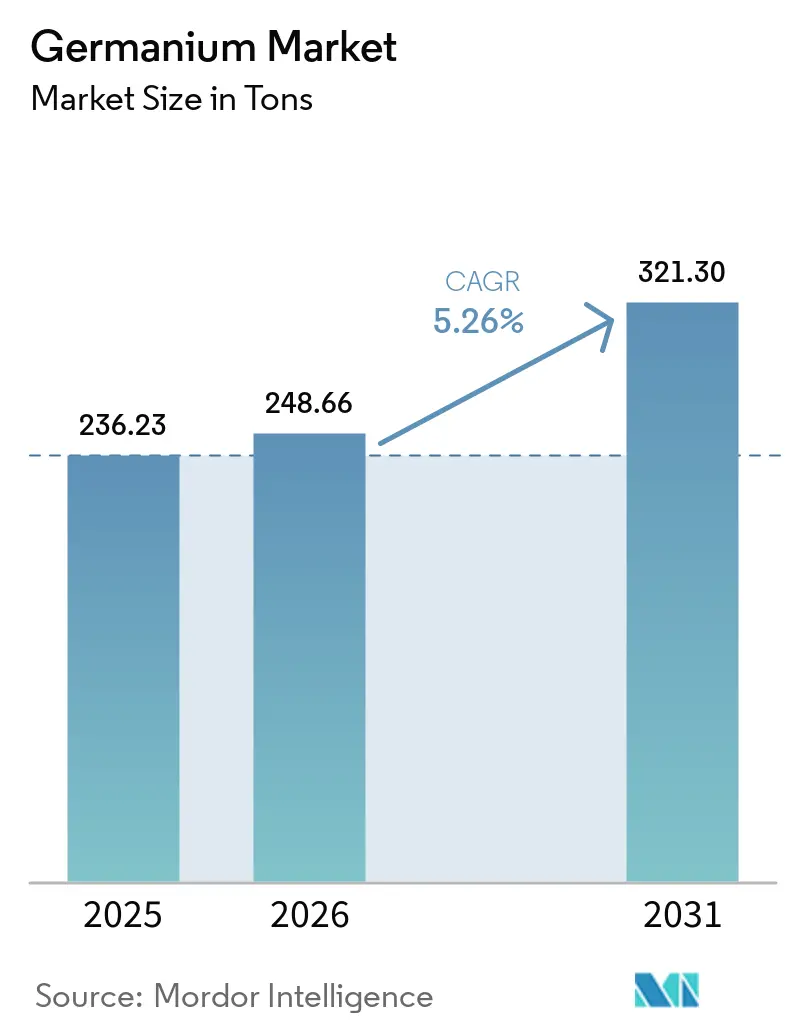

| Market Volume (2026) | 248.66 tons |

| Market Volume (2031) | 321.30 tons |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germanium Market Analysis by Mordor Intelligence

The Germanium Market size was valued at 236.23 tons in 2025 and is estimated to grow from 248.66 tons in 2026 to reach 321.30 tons by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). Demand for high-purity feedstock is rising because fiber-optic telecom, quantum-computing hardware, and autonomous-vehicle thermal sensors all rely on germanium’s unique optical and electronic properties. Asia-Pacific dominates the Germanium market with a 58.92% share, owing to China’s zinc-smelter recovery network and Japan’s precision-optics ecosystem. Fiber-optic systems account for 34.88% of volume and represent the fastest-growing application, pushed by hyperscale data-center interconnects and 5G back-haul that consume Germanium tetrachloride (GeCl₄) for low-loss preforms. Competitive intensity stays moderate: three Chinese refiners supply roughly half of global tonnage, while Western firms leverage recycling and 6N-7N purification to secure premium segments.

Key Report Takeaways

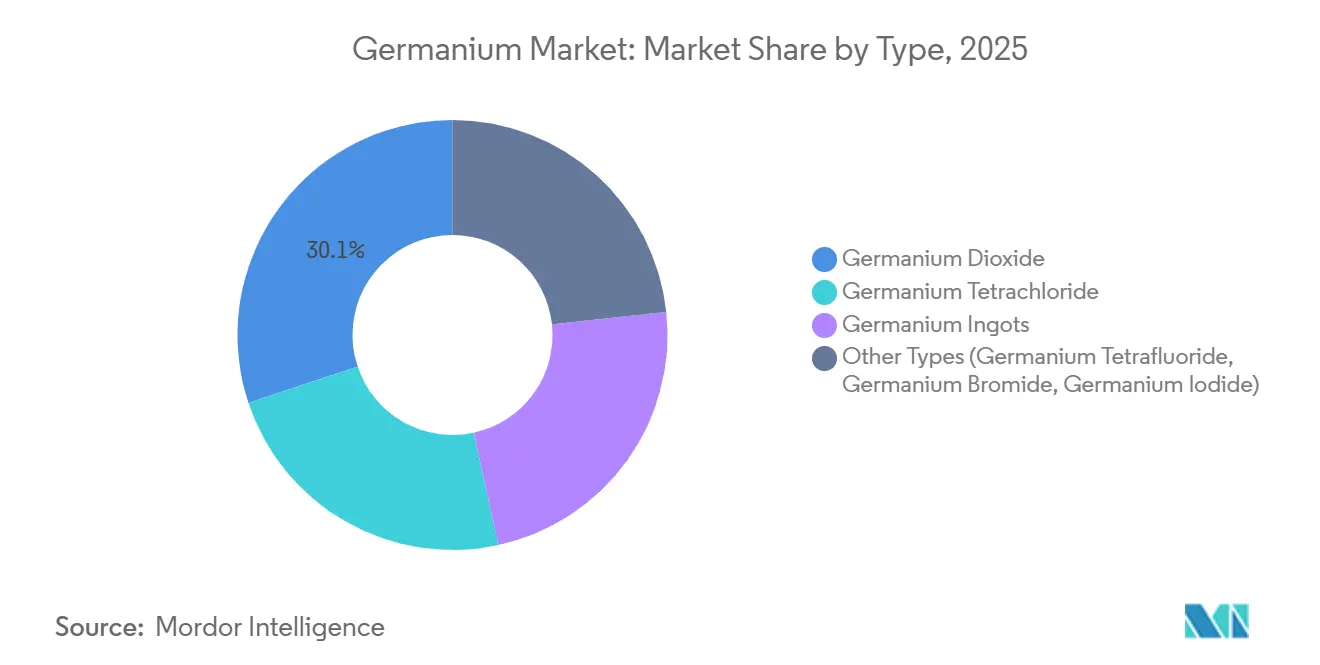

- By type, germanium dioxide accounted for 30.12% of the Germanium market size in 2025, while germanium tetrachloride is poised for the quickest rise at a 5.58% CAGR during the forecast period (2026-2031).

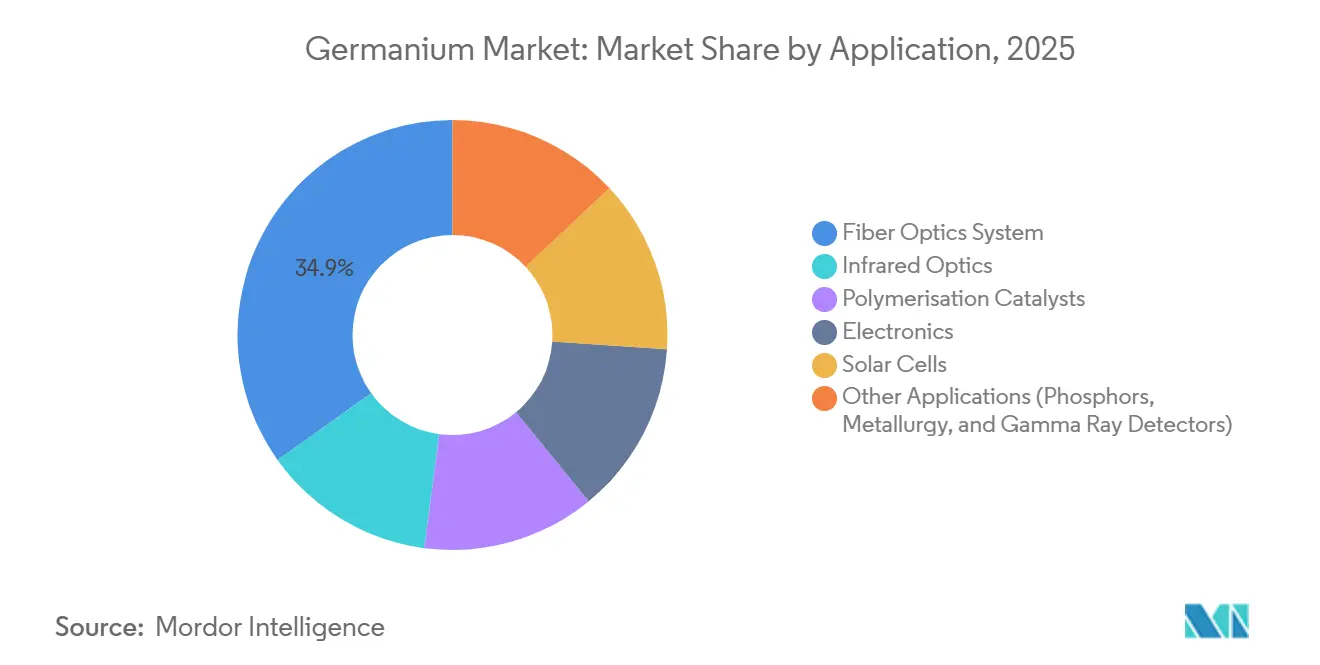

- By application, fiber-optic systems led with 34.88% of the Germanium market share in 2025 and are forecast to advance at a 5.72% CAGR during the forecast period (2026-2031).

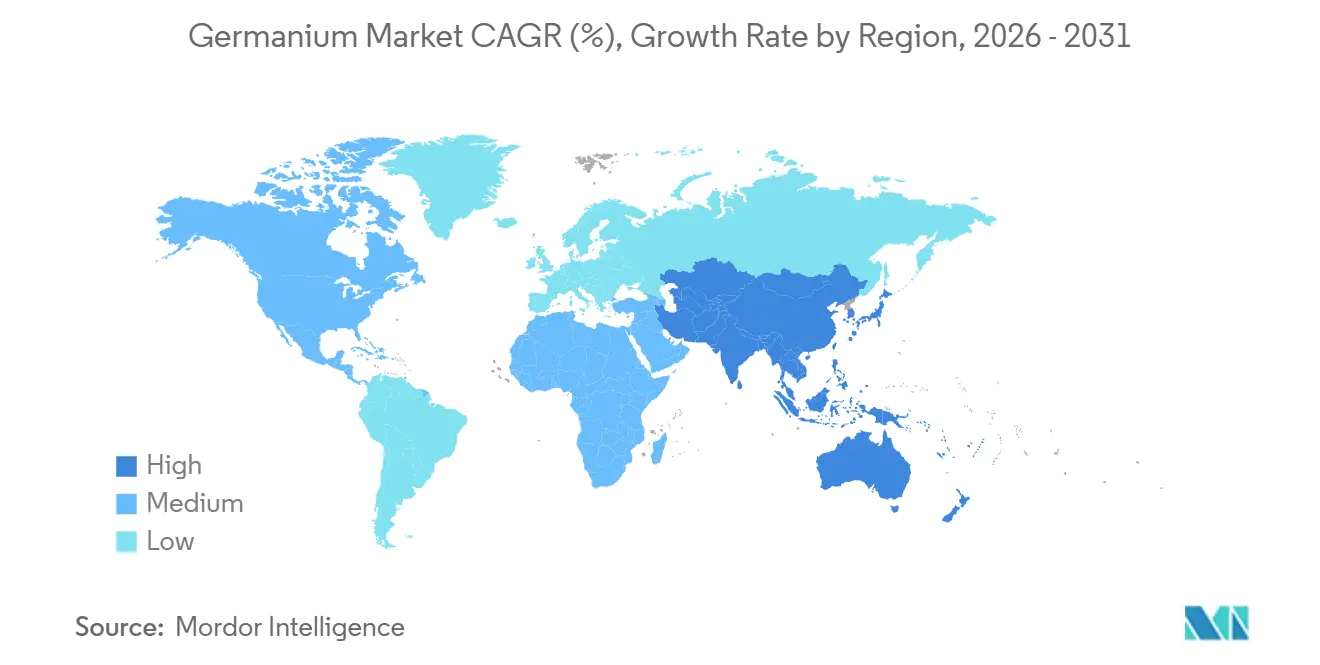

- By geography, Asia-Pacific captured 58.92% of the Germanium market share in 2025, and the region should continue growing at a 5.59% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Germanium Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Fiber-Optic Telecommunications | +1.8% | Global with focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Surging Need for Infrared Optics in Autonomous Vehicles and Industrial Imaging | +1.2% | North America, Europe, fast-growing APAC | Medium term (2-4 years) |

| Adoption of Ge Substrates in High-Efficiency Multi-Junction Solar Cells | +0.9% | Global, early gains in space and CPV | Long term (≥4 years) |

| Ultra-High-Purity Ge for Quantum-Computing Qubits and Cryogenic Detectors | +0.7% | North America, Europe, select APAC | Long term (≥4 years) |

| Defense Funding to On-Shore Semiconductor-Grade Ge Wafer Capacity | +0.6% | United States, European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Fiber-Optic Telecommunications

Global internet traffic is doubling every 24 months, and carriers are deploying bend-insensitive single-mode fiber with germanium-doped cores that cut attenuation below 0.15 dB/km at 1550 nm[1]Institute of Electrical and Electronics Engineers, “Low-Loss Fiber Preforms via GeCl₄ MCVD,” ieee.org. Major performance suppliers report six-month order backlogs, signaling a tightening supply of Germanium tetrachloride (GeCl₄). China’s rural broadband push and India’s BharatNet Phase III together add 15 million fiber-km by 2027, equivalent to about 18 tons of annual Germanium tetrachloride (GeCl₄) demand. Hollow-core fiber alternatives remain laboratory curiosities because production costs exceed conventional Modified Chemical Vapor Deposition (MCVD) by more than three times. Only Belgium and Japan operate hydrolysis plants that recycle preform off-gas, so the Germanium market still relies on primary smelter output. These factors reinforce a multi-year upswing in the Germanium market size devoted to telecom infrastructure.

Surging Need for Infrared Optics in Autonomous Vehicles and Industrial Imaging

Thermal cameras operating in the 8-12 µm band require germanium lenses to exploit atmospheric transmission peaks[2]SPIE, “Germanium Lenses for Automotive Thermal Cameras,” spie.org. Automotive Tier-1 suppliers have lifted per-vehicle germanium loadings from 12 g in 2024 to an expected 22 g by 2028. Industrial predictive-maintenance systems consumed 11 tons of germanium optics in 2025, and growth is strongest in semiconductor fabs and petrochemical complexes. Chalcogenide glass poses limited substitution risk because brittleness and moisture sensitivity restrict large-scale deployment. Defense programs provide a steady 4-5 ton floor in annual demand, insulating the Germanium market from economic cycles.

Adoption of Ge Substrates in High-Efficiency Multi-Junction Solar Cells

Space agencies specify germanium wafers as lattice-matched substrates for III-V quadruple-junction cells that exceed 32% conversion efficiency under AM1.5G (Air Mass 1.5 Global) illumination. The European Space Agency and NASA programs account for roughly 3.5 tons of 6-inch wafers per year, priced at USD 800-1,200 per kg. Terrestrial concentrator photovoltaics remain niche, limited to less than 50 MW of annual capacity. Ge-on-Si tandem concepts could halve substrate costs and open new demand if pilot lines launching in 2027 meet cost targets. Until then, the segment’s contribution to the Germanium market size is small but strategically vital because space missions prize radiation hardness over price.

Ultra-High-Purity Ge for Quantum-Computing Qubits and Cryogenic Detectors

Isotopically enriched Ge wafers have demonstrated 99.9% single-qubit fidelities, crossing error-correction thresholds for scalable quantum processors. Global enrichment capacity is under 200 kg per year, and lead times stretch to 24 months. Intel and Diraq are funding 300 mm pilot lines, pushing spot prices toward USD 50,000 per kg. High-purity germanium detectors for gamma-ray spectroscopy consume natural-abundance material refined to 10N, supplied by fewer than five vendors worldwide. Quantum-hardware funding in the US and Europe tops USD 1.2 billion through 2028, which could triple ultra-pure demand and intensify supply bottlenecks in the Germanium market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility from zinc-mine by-product nature | -0.80% | Global, with acute effects in regions dependent on imported feedstock | Short term (≤2 years) |

| High purification and crystal-growth costs vs. silicon | -0.50% | Global, particularly affecting emerging producers and cost-sensitive applications | Medium term (2-4 years) |

| Recycling bottlenecks for telecom-grade GeCl₄ | -0.40% | Global, with concentration in Asia-Pacific and Europe where fiber-optic production is highest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility from Zinc-Mine By-Product Nature

Since germanium is captured from zinc-smelter flue dust, refined output mirrors zinc-mine economics rather than germanium demand. Spot prices swung from USD 1,650 per kg in January 2025 to USD 2,180 in September 2025 after unplanned smelter outages overlapped with fiber-optic restocking. Long-term contracts mitigate risk for Asian buyers but transfer margin pressure to refiners. A transparent futures market does not exist, so bilateral deals dominate and widen information asymmetry. Mining primary germanium remains uneconomic because ore grades rarely exceed 100 ppm (parts per million).

High Purification and Crystal-Growth Costs vs. Silicon

Zone-refining to 6N purity requires 15-20 passes consuming 180 kWh per kg, more than four times silicon’s energy demand. Chlorination and hydrolysis add USD 200-300 per kg in reagents and energy, bringing total production expense to USD 600-800 before crystal pulling. Czochralski growth of 6-inch ingots needs furnaces costing over USD 5 million each. Silicon’s mature supply chain drives solar-grade costs below USD 15 per kg, so germanium’s premium confines usage to niches where its high refractive index or lattice constant outweighs price sensitivity. These structural cost hurdles cap volume growth in the broader Germanium market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tetrachloride Gains as Fiber Preforms Outpace Optics Blanks

Germanium dioxide held 30.12% share of the Germanium market in 2025, anchored by polymerization catalysts and infrared-optics blanks. Growth lags the overall Germanium market size because PET (Polyethylene Terephthalate) producers trial cheaper antimony systems. Germanium tetrachloride is the fastest-rising type at 5.58% CAGR during the forecast period (2026-2031); MCVD (Modified Chemical Vapor Deposition) and PCVD (Plasma Chemical Vapor Deposition) fiber-preform lines rely on GeCl₄ doping that supports 400 G and 800 G transceiver rollouts. Commodity-grade ingots trade near USD 1,200 per kg, while 7N isotopically enriched wafers fetch USD 50,000 per kg, reflecting divergent purity needs. Niche compounds such as germanium tetrafluoride and iodide represent under 3% of tonnage and show limited commercial momentum.

Recycling initiatives could supply an extra 6-8 tons annually by 2030, especially from GeCl₄ off-gas and end-of-life infrared lenses. ISO 9001 suffices for mainstream quality control, but quantum and defense buyers require traceability to NIST SRM 1537 (National Institute of Standards and Technology Standard Reference Material 1537). Historical CAGR from 2020-2025 was 4.1% because COVID-19 slowed telecom and auto production; the rebound to 5.26% through 2031 demonstrates pent-up infrastructure demand. Consequently, the Germanium market share commanded by tetrachloride will keep expanding as optical-fiber deployment accelerates worldwide.

By Application: Fiber Optics Dominates Share and Growth, While Quantum Niches Command Premiums

Fiber-optic infrastructure claimed 34.88% of the Germanium market in 2025 and is projected to outpace all other uses at 5.72% CAGR during the forecast period (2026-2031). Germanium tetrachloride (GeCl₄) doping lowers refractive-index contrast, enabling compact cable routing in congested city conduits. Infrared optics remains the second-largest slice of the Germanium market; germanium’s high refractive index allows thin lenses for automotive night-vision and industrial thermography. Polymerization-catalyst usage is stable at 8-10 tons but faces headwinds from antimony-free alternatives under the European Union Registration, Evaluation, Authorisation and Restriction of Chemicals (EU REACH) regulation. Electronics applications, mainly SiGe HBTs (Silicon-Germanium Heterojunction Bipolar Transistors), consumed 9 tons in 2025, powered by 5G base-station demand.

Space-grade solar cells contribute 3.5 tons annually, and new Ge-on-Si tandems could enlarge that base post-2027. HPGe (High-Purity Germanium) detectors continue to grow modestly as nuclear-security budgets rise. Other minor outlets, LED (light-emitting diode) phosphors, and aluminum-alloy additives total 6-7 tons. Compliance with IEC 60825 (International Electrotechnical Commission 60825) for fiber safety and MIL-STD-810 (Military Standard 810) for defense optics adds certification overhead but seldom constrains supply. The Germanium market, therefore, remains anchored in telecom and thermal-imaging applications while ultra-high-purity quantum niches capture disproportionate revenue per ton.

Geography Analysis

Asia-Pacific led the Germanium market with 58.92% share in 2025 and is set to grow at 5.59% CAGR through 2031. China’s Yunnan province houses integrated zinc-smelter–refinery complexes that enjoy ore grades of 0.8-1.2% germanium in flue dust, giving cost advantages over imported feedstock. Japan builds on decades of zone-refining expertise to supply 6N-7N ingots for precision optics, while South Korea’s foundries demand 4-5 tons yearly for SiGe epitaxy. India’s fiber-optics construction recorded 22% year-on-year consumption growth in 2025 as rural broadband expanded.

In North America, Teck Resources’ Trail smelter recovers 8-10 tons per year and plans a 4-ton expansion by 2027, while 5N Plus upgrades imported feedstock to 7N wafers in Montreal. Quantum-computing clusters in California and Massachusetts anchor demand for enriched Ge. Canada’s Critical Minerals Strategy targets a doubling of refining capacity by 2030, but financing hurdles persist.

In Europe, the European Union (EU)'s 2030 mandate to process 40% of critical minerals locally drives feasibility studies in Belgium and Germany, yet high electricity tariffs slow project approvals. The rest of the World accounted for a substantially less market share, with small recovery operations in the Democratic Republic of Congo and sanctions-isolated Russia pivoting to domestic customers. Overall, regional diversification efforts will alter trade flows but leave Asia-Pacific firmly atop the Germanium market share leaderboard through 2031.

Competitive Landscape

The Germanium market is moderately consolidated. Chinese firms wield cost leadership through vertically integrated zinc smelting, whereas Western suppliers differentiate on recycling, isotopic enrichment, and stringent ESG (Environmental, Social, and Governance) compliance. Tech upgrades focus on automating zone-refining furnaces and installing real-time spectroscopy that lifted Umicore’s 6N yield from 82% to 91% between 2023 and 2025. Regulatory influence is still light, limited to export controls on isotopic material and environmental permits for chlorination lines, but critical-mineral designations in the United States and the European Union are starting to shape capital allocation.

Germanium Industry Leaders

Teck Resources Limited

Umicore

Yunnan Chihong Zinc & Germanium Co., Ltd.

5N Plus

CNGE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Blue Moon Metals Inc. announced that Teck American Incorporated, a subsidiary of Teck Resources Limited, had transferred 100% ownership of the past-producing Apex germanium (Ge), gallium (Ga), and copper (Cu) mine located in Utah to Blue Moon. This positioned Teck as a key stakeholder in supporting an integrated pipeline of U.S. critical mineral projects aimed at securing the North American supply.

- August 2025: Korea Zinc and Lockheed Martin have signed an MOU to strengthen germanium supply and procurement, aiming to establish a resilient supply chain. Korea Zinc will produce high-purity germanium using raw materials sourced outside China and supply it to Lockheed Martin.

Global Germanium Market Report Scope

Germanium is a chemical element with the symbol Ge and atomic number 32. It is a lustrous, hard, grayish-white metalloid in the carbon group. Germanium has properties similar to those of silicon and is used in various high-tech applications.

Germanium market is segmented on the basis of type, application, and geography. By type, the market is segmented into germanium tetrachloride, germanium dioxide, germanium ingot, and others (germanium wafers, germanium compounds). By application, the market is segmented into IR optics, fiber optics, electronics, and others (LED technology, solar cells). The report also covers the market size and forecasts for the germanium market in 11 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Germanium Dioxide |

| Germanium Tetrachloride |

| Germanium Ingots |

| Other Types (Germanium Tetrafluoride, Germanium Bromide, Germanium Iodide) |

| Fiber Optics System |

| Infrared Optics |

| Polymerisation Catalysts |

| Electronics |

| Solar Cells |

| Other Applications (Phosphors, Metallurgy, and Gamma Ray Detectors) |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Belgium | |

| Russia | |

| Rest of Europe | |

| Rest of the World | South America |

| Middle-East and Africa |

| By Type | Germanium Dioxide | |

| Germanium Tetrachloride | ||

| Germanium Ingots | ||

| Other Types (Germanium Tetrafluoride, Germanium Bromide, Germanium Iodide) | ||

| By Application | Fiber Optics System | |

| Infrared Optics | ||

| Polymerisation Catalysts | ||

| Electronics | ||

| Solar Cells | ||

| Other Applications (Phosphors, Metallurgy, and Gamma Ray Detectors) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Belgium | ||

| Russia | ||

| Rest of Europe | ||

| Rest of the World | South America | |

| Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of germanium demand by 2031?

The Germanium market is forecast to reach 321.30 tons by 2031, expanding at a 5.26% CAGR from 2026-2031.

Which application segment will add the most incremental volume?

Fiber-optic systems will contribute the largest incremental tonnage, growing at 5.72% CAGR on the back of 5G and hyperscale data-center deployments.

Why is germanium supply so sensitive to zinc prices?

Nearly all refined germanium is recovered as a by-product of zinc smelting, so any fluctuation in zinc-mine output directly alters germanium feedstock availability and spot pricing.

How are policy initiatives shaping regional supply?

United States CHIPS and European Union Critical Raw Materials legislation are funding domestic refining and wafer production, aiming to diversify supply away from China by the end of the decade.

What purity grades are required for quantum-computing wafers?

Quantum processors use 7N-grade, isotopically enriched ⁷⁴Ge wafers priced near USD 50,000 per kg because they deliver qubit fidelities above 99.9%.

Page last updated on: