Global Treatment-Resistant Depression Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

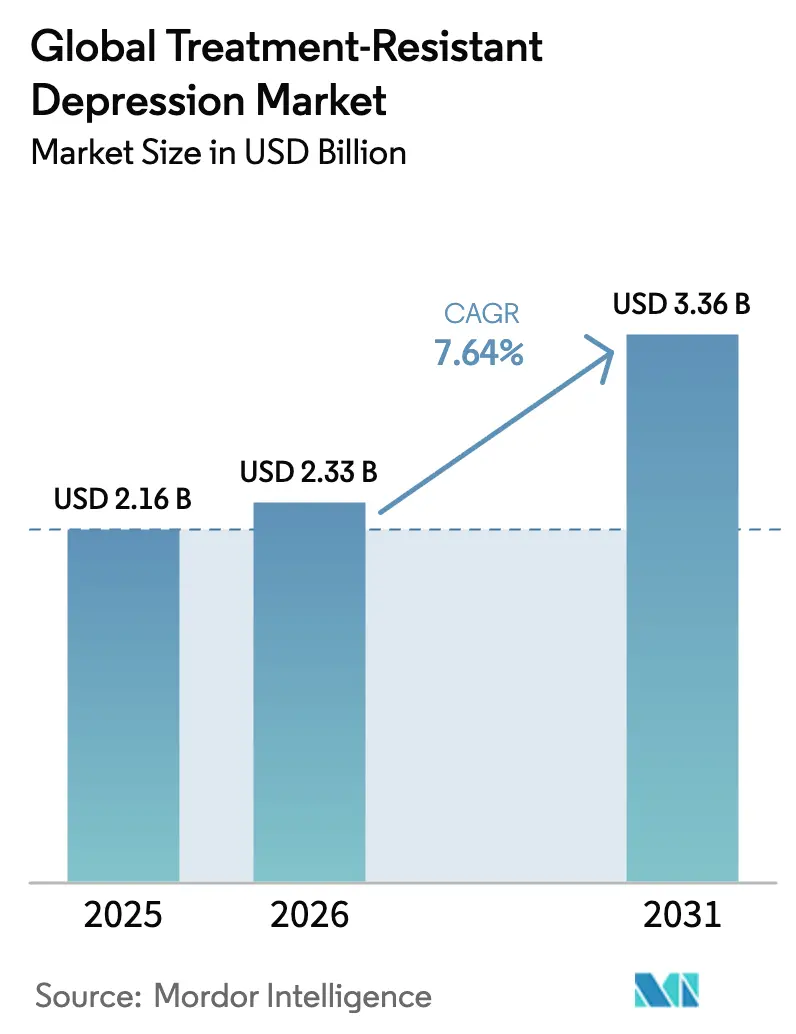

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 7.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Treatment-Resistant Depression Market Analysis by Mordor Intelligence

The treatment-resistant depression market size is expected to grow from USD 2.16 billion in 2025 to USD 2.33 billion in 2026 and is forecast to reach USD 3.36 billion by 2031 at 7.64% CAGR over 2026-2031. This expansion shows that clinicians, payers, and patients now prioritize rapid-acting and mechanistically novel therapies that move beyond serotonin and norepinephrine modulation. Growth is propelled by the broad commercial rollout of esketamine, maturing real-world evidence showing functional gains, and the first positive Phase 3 read-out for a psilocybin-based agent. Regulatory bodies in the United States, Canada, Australia, and the European Union are enabling these developments by granting Breakthrough, Fast-Track, and Special Access designations that shorten time to market and open reimbursement conversations earlier. Clinical pipelines are diversifying into NMDA receptor antagonists, psychedelics, neuroactive steroids, and precision psychiatry platforms, each aiming to serve the 70% of patients who fail two adequate antidepressant regimens. Digital health infrastructure, including remote monitoring and AI-enabled patient stratification, reduces treatment friction points and positions the treatment-resistant depression market for broader adoption in outpatient settings.

Key Report Takeaways

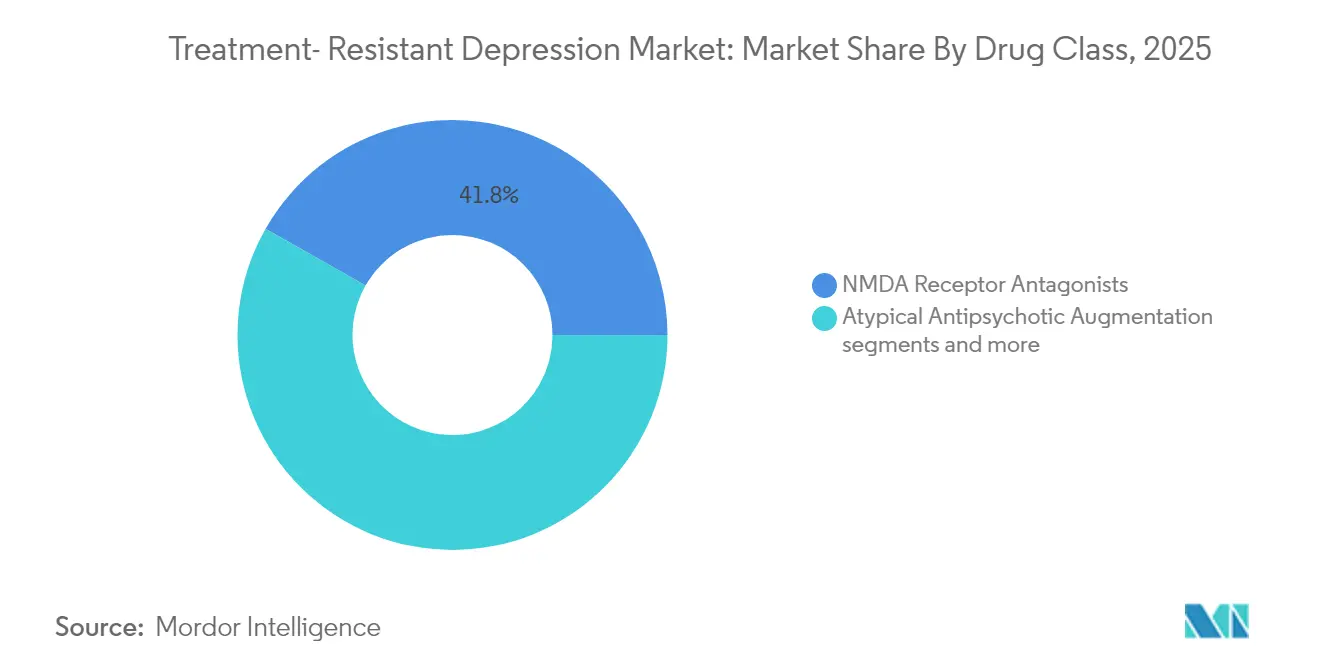

- By drug class, NMDA receptor antagonists led with 41.78% revenue share in 2025, while psychedelics and novel compounds are forecast to expand at an 7.80% CAGR to 2031.

- By end user, hospitals captured 44.02% of the treatment-resistant depression market share in 2025, whereas homecare and telepsychiatry are set to advance at an 8.34% CAGR through 2031.

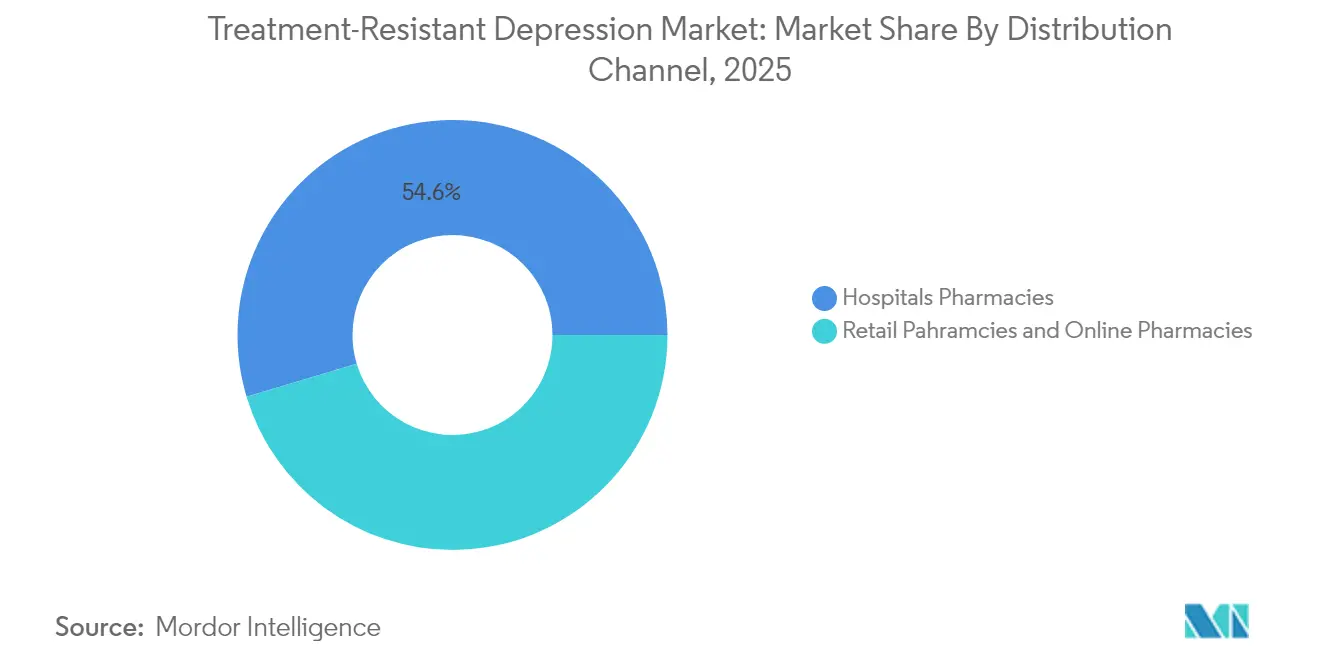

- By distribution channel, hospital pharmacies controlled 54.63% of sales in 2025, and online pharmacies are projected to grow the fastest at 8.68% CAGR to 2031.

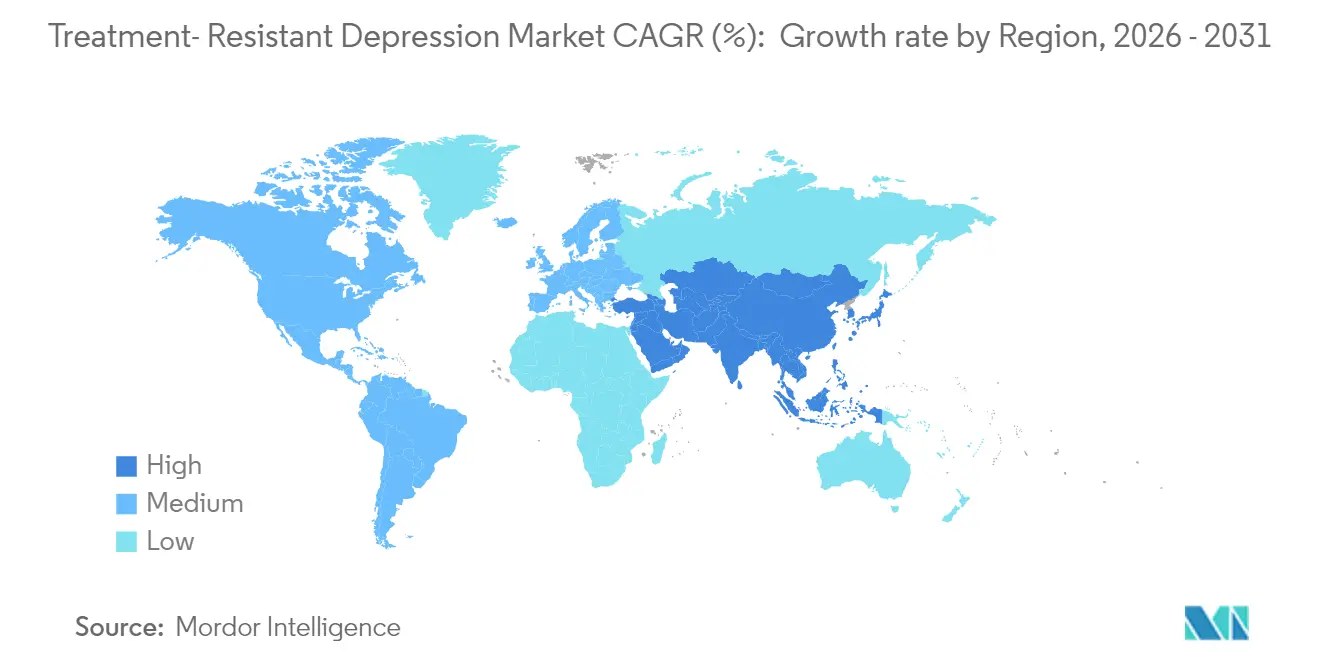

- By geography, North America commanded 47.91% revenue share in 2025, while Asia Pacific is expected to grow at an 8.51% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Treatment-Resistant Depression Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of partial/non-response to SSRI/SNRI therapy | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid commercial uptake of esketamine (Spravato) in key markets | +1.5% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Rising payer willingness to reimburse novel-mechanism add-ons | +1.2% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Psychedelic-assisted therapy clinics scaling in North America & Europe | +0.9% | North America & Europe core, early APAC adoption | Long term (≥ 4 years) |

| FDA Breakthrough & Fast-Track designations accelerating pipelines | +0.7% | Global, with regulatory spillover effects | Short term (≤ 2 years) |

| AI-enabled precision-psychiatry tools boosting treatment matching | +0.6% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Monoamine-based antidepressants leave 70% of patients without full remission, and this unresolved burden fuels continuous demand for alternatives that work on glutamatergic, GABAergic, and neuroplasticity pathways. Stanford researchers segmented major depressive disorder into six biological subtypes, demonstrating that treatment-resistant depression is a heterogeneous collection of conditions rather than a single disease[1]Source: Nicholas Bagley, “Coverage Restrictions under Medicare Part D,” Health Affairs, healthaffairs.org . Biomarker-driven trials now enroll smaller but more responsive cohorts, improving study power and reducing development risk. Pharmaceutical pipelines increasingly test agents in matched subpopulations where response probabilities are higher. Health-economic models forecast that every 1-percentage-point improvement in functional remission cuts long-term medical spending by USD 220 million across the United States alone, reinforcing the commercial logic behind personalized strategies. Together, these dynamics ensure sustained momentum for therapies that promise faster action, neuroplastic repair, and durable symptom relief.

Rapid Commercial Uptake of Esketamine in Key Markets

Esketamine’s real-world 25.6% functional remission rate versus 11.5% for older add-on options translates into tangible workplace productivity gains and drives positive word-of-mouth among psychiatrists. The United States widened the label to include monotherapy in January 2025, effectively doubling the treatable population because clinicians can now start esketamine earlier. Europe follows a cautious but still positive course, with several national agencies issuing conditional reimbursement linked to outcomes monitoring. Registries in Canada, Germany, and Japan track functional changes six months post-induction and feed live dashboards that inform payer renewals. Hospital buying committees increasingly bundle REMS-compliant rooms with esketamine supply contracts, locking in steady demand.

Rising Payer Willingness to Reimburse Novel-Mechanism Add-Ons

Payers face mounting costs from repeat hospitalizations, emergency visits, and lost productivity associated with chronic depressive episodes. Actuarial reviews indicate that rapid-acting agents recoup their upfront drug costs within three years through reduced downstream utilization. United States commercial plans now pilot outcomes-based contracts that rebate 25% of drug costs if functional remission targets are missed at the six-month mark. European sickness funds mirror this logic by waiving co-pays once patients achieve predefined quality-of-life thresholds. These financial experiments broaden access and spur manufacturers to collect robust real-world evidence. Meanwhile, expanding data sets help refine cost-effectiveness models that once underestimated the value of fast relief and improved daily functioning. As more countries adopt health-technology-assessment frameworks that consider productivity gains, reimbursement barriers for cutting-edge interventions are expected to fall further.

Psychedelic-Assisted Therapy Clinics Scaling in North America & Europe

North America already hosts over 200 specialized clinics capable of administering psilocybin, MDMA, or ketamine in a controlled setting, and a further 150 centers are in construction or planning. Europe is following suit, spurred by a 2024 European Medicines Agency workshop that laid out design principles for integrated therapy centers. Standardized training modules now certify nurses and psychotherapists, ensuring session consistency and safety. Multi-center registries collect dissociation profiles, integration session attendance, and relapse timing, producing the data needed for wider payer adoption. Revenue per clinic is forecast to expand 18% annually through 2028 because the bundled model combines the drug, the experiential session, and follow-up psychotherapy. Investors view these clinics as critical infrastructure that lowers the implementation hurdle for each new psychedelic asset that wins approval.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & REMS burden for intranasal esketamine administration | -1.1% | Global, most pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Stringent insurance step-edit requirements delaying uptake | -0.8% | North America & Europe, varying by payer type | Short term (≤ 2 years) |

| Social-stigma & regulatory uncertainty around psychedelic agents | -0.6% | Global, with regional variation in acceptance | Long term (≥ 4 years) |

| Limited specialist capacity for intensive dosing & monitoring | -0.5% | Global, acute in underserved regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and REMS Burden for Intranasal Esketamine Administration

Risk Evaluation and Mitigation Strategy protocols stipulate two-hour on-site monitoring after each dose, driving fixed clinic costs independent of patient numbers. Real-world audits show median induction phases extending to 64 days instead of the recommended 28 days, inflating staffing and facility expenses. Smaller hospitals struggle to justify dedicated rooms and trained personnel, pushing patients toward larger centers and lengthening travel times. The United Kingdom’s cost watchdog declined broad National Health Service funding in 2024, citing unfavorable incremental cost-effectiveness ratios, which illustrates how financial and operational hurdles can stall adoption even when clinical benefit is clear. Manufacturers respond by developing once-weekly or extended-release formulations that could cut monitoring windows in half, but these remain several years from approval.

Stringent Insurance Step-Edit Requirements Delaying Uptake

Many commercial payers still mandate failure on at least two selective serotonin reuptake inhibitors and one augmentation strategy before covering novel mechanisms[2]Source: Stanford Medicine, “AI Identifies Depression Biotypes,” med.stanford.edu . Physicians surveyed in 2025 reported spending a median of 6 hours per month on prior authorization paperwork for esketamine alone. Administrative bottlenecks prolong untreated episodes, leading to emergency interventions that counterintuitively raise costs. Several United States states now contemplate legislation that limits step therapy to one failed trial in severe depression, but enactment timelines vary. Until reforms materialize, long lead times will temper the growth trajectory of novel agents, particularly in smaller practices without dedicated reimbursement staff.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: NMDA Antagonists Sustain Leadership While Psychedelics Accelerate

In 2025, NMDA receptor antagonists generated 41.78% of treatment-resistant depression market revenue. Esketamine accounts for the bulk of this share, buoyed by consistent real-world remission data and the January 2025 monotherapy approval that broadened its reach. Psychedelics and novel compounds represent the fastest-growing drug class with an 7.80% CAGR forecast to 2031, a trajectory underpinned by the COMP360 Phase 3 success that demonstrated a 3.6-point mean MADRS advantage over placebo. The treatment-resistant depression market size attributable to psychedelics is expected to surpass USD 645.7 million by 2031, assuming regulatory approvals across at least three major regions.

Competitive dynamics are shifting as large pharmaceutical firms buy or license early-stage psychedelic assets, recognizing their potential to complement existing portfolios. At the same time, extended-release ketamine candidates could lower monitoring burdens and draw volume back toward the established NMDA category. Atypical antipsychotic augmentation regimens remain relevant for clinicians familiar with the protocols, but their growth moderates because of metabolic side-effects and payer scrutiny. Triple reuptake inhibitors and neuroactive steroids occupy a promising but still emergent niche, with early-phase data suggesting synergistic action when combined with glutamatergic modulators.

By End User: Hospitals Dominate While Telepsychiatry Gains Momentum

Hospitals controlled 44.02% of 2025 revenues because their psychiatric units, emergency departments, and outpatient infusion centers possess the staffing and observation capabilities necessary for high-intensity therapies. These institutions benefit from bundled remuneration that covers both drug acquisition and facility fees, thereby smoothing cost recovery. Homecare and telepsychiatry, though currently smaller, will expand fastest at an 8.34% CAGR through 2031. High patient acceptability, measured at 71% in recent surveys, underpins this shift, as do insurance incentives that reimburse virtual consultations at parity with in-person visits. The treatment-resistant depression market size generated by telepsychiatry platforms is projected to reach USD 762.4 million by 2031, contingent on the approval of formulations that can be administered safely in a home environment.

Specialty clinics bridge the gap by offering advanced interventions without the overhead of large hospitals. These facilities harness standardized protocols, group therapy models, and digital symptom tracking to boost throughput and margins. Academic centers continue to set clinical benchmarks by running pivotal trials that validate emerging modalities, thus attracting grant funding and industry partnerships. Commercial success in this segment increasingly depends on integrating pharmacologic care with digital follow-up that maintains patient engagement between in-person sessions.

By Distribution Channel: Hospital Pharmacies Retain Primacy Amid Online Growth

Hospital pharmacies dispensed 54.63% of treatment-resistant depression prescriptions in 2025, reflecting strict storage controls for controlled substances and the requirement to align drug availability with REMS-compliant observation areas. Online pharmacies, growing at 8.68% CAGR, benefit from digital prescribing, automated refills, and direct-to-patient education that reduce friction and improve adherence. Notably, the treatment-resistant depression market share captured by online channels is forecast to climb from 9.18% in 2025 to nearly 14.92% by 2031, provided cybersecurity safeguards and identity verification protocols keep pace.

Retail chains lag because many novel agents demand on-site monitoring or physician administration, limiting their immediate relevance. Nevertheless, extended-release or oral psychedelic formulations now in Phase 2 could become viable for retail dispensing once safety profiles are established. Pharmaceutical companies experiment with hybrid models that place inventory in central hospital hubs but fulfill maintenance doses via mail-order pharmacy, thereby balancing safety oversight with patient convenience.

Geography Analysis

North America generated 47.91% of 2025 revenue and remains the reference market for regulatory and reimbursement precedents. The January 2025 United States decision to permit esketamine monotherapy immediately expanded the treatment-resistant depression market size across the region. Canada’s Special Access Program issued 176 psilocybin exemptions with a 78% approval rate, producing post-session data that informs subsequent label expansions. Payer adoption is streamlined by established diagnostic coding and outcome registries that track functional remission, work attendance, and hospital readmission in near real time. The ecosystem’s maturity ensures that new entrants can scale quickly once they secure approval.

Europe contributes a significant revenue block thanks to strong academic networks and multinational consortia that facilitate Phase 3 trials. The European Medicines Agency signaled openness to innovative mental-health interventions during its 2024 workshop, yet reimbursement debates continue at the member-state level. Germany and the Netherlands show the highest clinic density and earliest psychedelic pilot programs, whereas some Southern European markets still focus resources on conventional pharmacotherapy. Despite this variability, continental alignment on clinical-trial requirements accelerates dossier preparation for psychedelics, NMDA modulators, and neuroactive steroids alike.

Asia Pacific is the fastest-growing geography with an 8.51% CAGR projected through 2031. Japan leads clinical adoption of non-invasive brain stimulation and provides a model for outcome-based reimbursement. Australia broke new ground by approving psilocybin therapy in 2023, catalyzing regional investment in purpose-built clinics and therapist training pipelines. China’s mental-health reforms elevate the importance of early diagnosis and escalate demand for rapid-acting solutions, although domestic approval pathways still prioritize local data. South Korea and Singapore leverage robust biotech ecosystems to host multi-center trials that produce Asia-specific safety and efficacy evidence. Overall, the region’s demographic scale, rising disposable income, and evolving regulatory clarity make it an indispensable growth vector for global players.

Competitive Landscape

Consolidation intensified in 2025 as large incumbents raced to assemble multi-mechanism portfolios. Johnson & Johnson’s USD 14.6 billion purchase of Intra-Cellular Therapeutics added CAPLYTA to an already strong esketamine franchise, giving the firm coverage across NMDA modulation, dopamine-serotonin antagonism, and glutamatergic stabilization. This transaction signals that big pharma now values psychiatric assets on par with oncology and immunology when projecting future revenue streams.

Specialists such as COMPASS Pathways validate their strategic focus by delivering the first positive Phase 3 psilocybin data set, which lowered investor skepticism regarding regulatory risk. The company coordinated therapist training, data management, and supply-chain logistics as part of its go-to-market blueprint, thereby setting a benchmark that smaller developers must match. Mid-cap players like Axsome and Relmada refine traditional molecules through formulation science, aiming to capture share with intellectual-property extensions and differentiated safety profiles.

Partnerships proliferate at earlier stages where neurobiology intersects with digital therapeutics and artificial intelligence. AbbVie’s USD 2 billion alliance with Gilgamesh grants access to neuroplastogens that promise ketamine-like efficacy without dissociation. Technology firms supply machine-learning models that mine electronic health records, genomic panels, and imaging data to optimize trial enrollment and post-market treatment matching. These collaborations accelerate cycle times while spreading risk across multiple stakeholders, highlighting a broader competitive trend: the convergence of pharmacology, data science, and care-delivery innovation.

Global Treatment-Resistant Depression Industry Leaders

AstraZeneca

Pfizer

GlaxoS

Eli Lilly and Company

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Supernus Pharmaceuticals agreed to acquire Sage Therapeutics for up to USD 795 million, adding ZURZUVAE to its mood-disorder portfolio.

- January 2025: FDA approved Spravato (esketamine) monotherapy for treatment-resistant depression, unlocking a larger eligible cohort for Johnson & Johnson.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the treatment-resistant depression (TRD) market as all pharmacologic, device-based, and psychedelic interventions commercialized for adults who have failed to achieve adequate response after at least two distinct antidepressant regimens of appropriate dose and duration. Revenue is tracked at ex-manufacturer value across hospitals, specialty mental-health clinics, retail, and online pharmacies in 28 countries covering over 90% of global TRD spending.

Scope exclusion: pediatric TRD trials and non-medical self-care products are not counted.

Segmentation Overview

- By Drug Class (Value)

- NMDA Receptor Antagonists

- Atypical Antipsychotic Augmentation

- Monoamine Modulators (SSRI/SNRI, MAOI, TCA)

- Psychedelics & Novel Compounds

- Others

- By End User (Value)

- Hospitals

- Specialty Clinics

- Homecare & Telepsychiatry

- Research & Academic Centers

- By Distribution Channel (Value)

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and surveys were conducted with psychiatrists, payers, hospital pharmacy managers, and neuro-stimulation operators across North America, Europe, and Asia-Pacific. Their inputs helped us validate real-world esketamine uptake, typical transcranial magnetic stimulation (TMS) course volumes, and average selling prices, closing key gaps left by desk research.

Desk Research

Mordor analysts began by mapping treated-patient volumes using public data sets such as the WHO Global Health Observatory, CDC's National Health Interview Survey, Eurostat's EHIS, and Japan's MHLW Patient Survey. They then aligned drug and device sales with customs and IMS shipment records. Clinical-evidence trends were gathered from PubMed-indexed journals and international guidelines issued by bodies like NICE, APA, and CANMAT. Financial baselines were refined with company 10-Ks, investor decks, and press releases, and further vetted through paid platforms, D&B Hoovers for company splits and Dow Jones Factiva for deal flow. This list is illustrative; many additional sources informed the work.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort model establishes the demand pool. Incidence, remission rate, treatment-seeking share, and second-line failure ratio are the principal variables. Results are cross-checked through selective bottom-up roll-ups of NMDA antagonist shipments, sampled clinic TMS course counts, and psychedelic-assisted session data. Multivariate regression with GDP per capita, psychiatrist density, and reimbursement breadth projects 2026-2030 growth; scenario analysis adjusts for pipeline launch timing. Where primary volume data were sparse, region-specific average doses and adherence curves filled gaps.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent sales audits before a multi-analyst review. Reports refresh annually, with interim updates triggered by major approvals or reimbursement shifts; a final validation pass occurs just prior to client release.

Why Mordor's Treatment-Resistant Depression Baseline Commands Reliability

Published TRD figures vary because firms differ on patient-flow assumptions, therapy mix, and refresh cadence.

Key gap drivers include: some publishers limit geography to seven high-income nations, others fold pipeline revenue into current sales, while a few count only pharmacy invoices and overlook specialty-clinic procedures such as TMS. Mordor's wider country coverage, dual-channel capture, and yearly refresh narrow these divergences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.16 B (2025) | Mordor Intelligence | - |

| USD 3.49 B (2024) | Global Consultancy A | Counts pipeline drug sales and covers only seven mature markets |

| USD 1.99 B (2025) | Trade Journal B | Tracks list-price pharmacy sales, omits device-based TMS revenue |

| USD 1.27 B (2024) | Industry Database C | Relies on inpatient prescription volumes, excluding outpatient and telepsychiatry channels |

In sum, the disciplined blend of broad scope, primary validation, and transparent variable selection makes Mordor's baseline a dependable starting point for strategic decisions.

Key Questions Answered in the Report

What proportion of patients with major depressive disorder meet criteria for treatment resistance?

About 70% of patients do not achieve full symptom remission after two adequate antidepressant trials, a level that defines treatment-resistant depression in most clinical guidelines.

How fast can NMDA antagonists relieve symptoms compared with traditional SSRI therapy?

Esketamine often produces measurable improvement within 24 hours, whereas selective serotonin reuptake inhibitors typically require four to six weeks for comparable relief.

Are psychedelic therapies safe when delivered in a medical setting?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Treatment-Resistant Depression Market?

Phase 3 data for COMP360 psilocybin showed no serious safety events and a statistically significant 3.6-point MADRS improvement over placebo when administered under professional supervision

Why do some payers require multiple failed treatments before covering new options?

Step-edit policies aim to control costs but often delay access to effective interventions, leading to prolonged illness and higher downstream spending, as documented in Medicare Part D .

Page last updated on: