Postpartum Depression Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

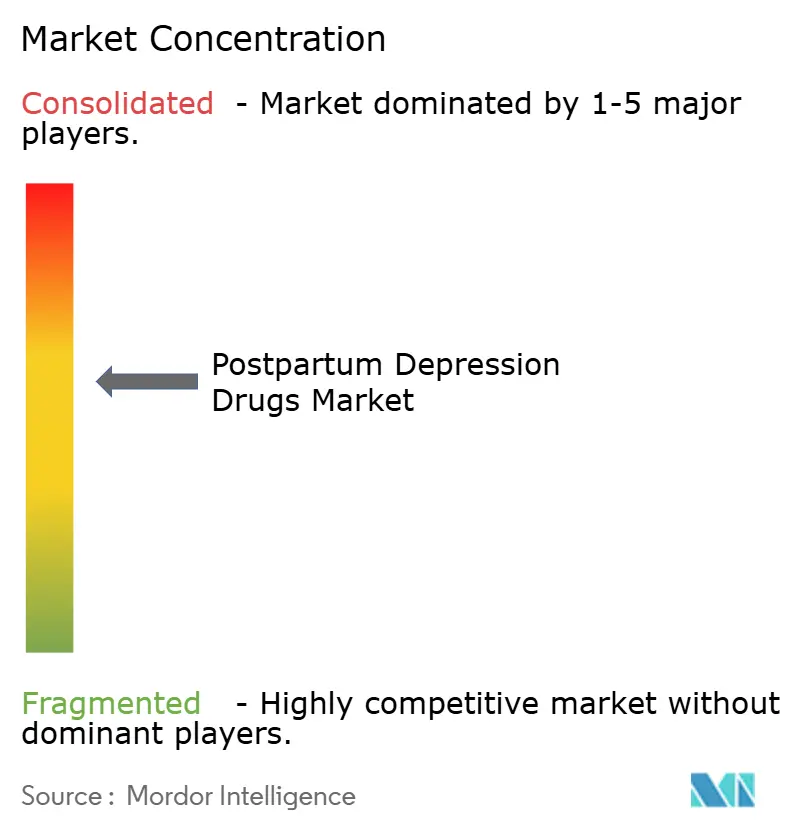

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postpartum Depression Drugs Market Analysis by Mordor Intelligence

The postpartum depression drugs market size is expected to grow from USD 1.05 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 1.79 billion by 2031 at 9.27% CAGR over 2026-2031. Growth rests on rapid neurosteroid approvals, expanding screening mandates, and stronger reimbursement protections that shorten time-to-therapy and reduce out-of-pocket costs. The postpartum depression drugs market benefits from regulatory momentum: zuranolone secured FDA clearance in 2023, offering symptom relief within 3 days, while the 2025 withdrawal of brexanolone redirected demand toward outpatient-friendly oral regimens [1]Source: Federal Register, “Sage Therapeutics, Inc.; Withdrawal of Approval of a New Drug Application for ZULRESSO,” federalregister.gov . Rising digital screening tools, parity laws, and Asia-Pacific healthcare investments further widen patient pools. Nonetheless, high list prices, REMS legacy concerns, and supply-chain pressure on neurosteroid active ingredients temper the otherwise robust trajectory of the postpartum depression drugs market.

Key Report Takeaways

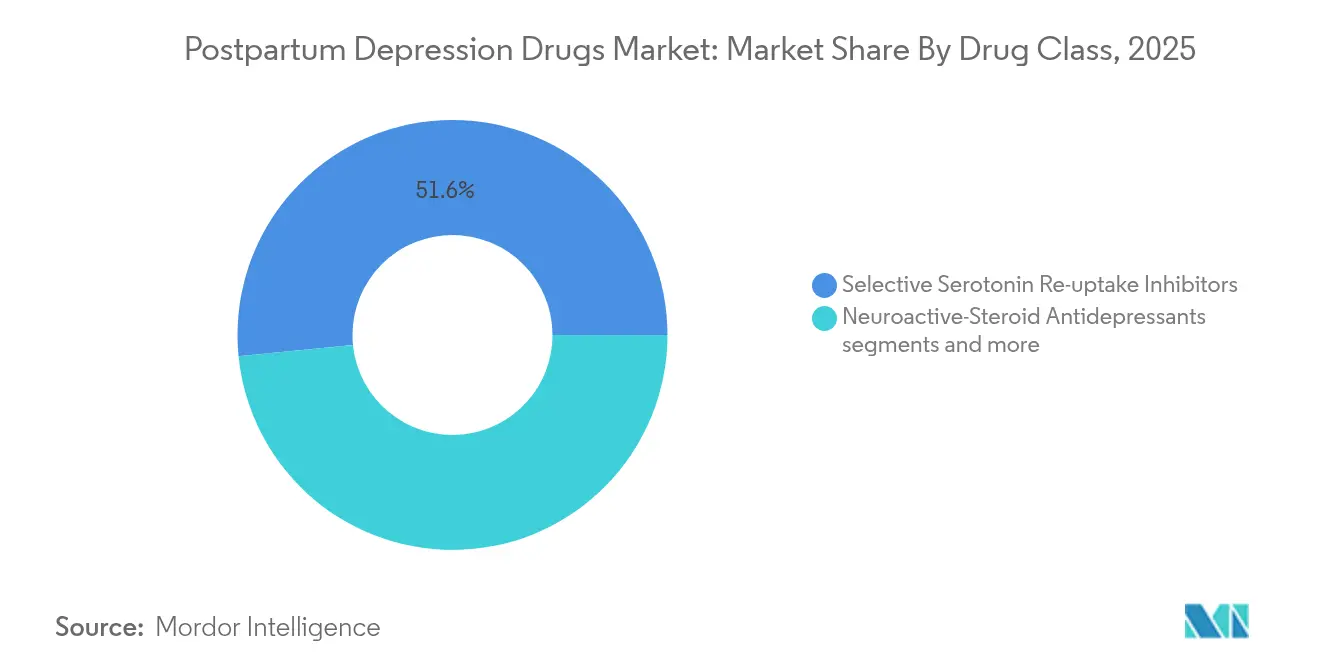

- By drug class: Selective serotonin reuptake inhibitors held 51.58% of postpartum depression drugs market share in 2025, while neuroactive-steroid antidepressants are projected to grow at 9.88% CAGR to 2031.

- By route of administration: Oral formulations commanded 71.62% of the postpartum depression drugs market size in 2025 and are advancing at 10.35% CAGR through 2031.

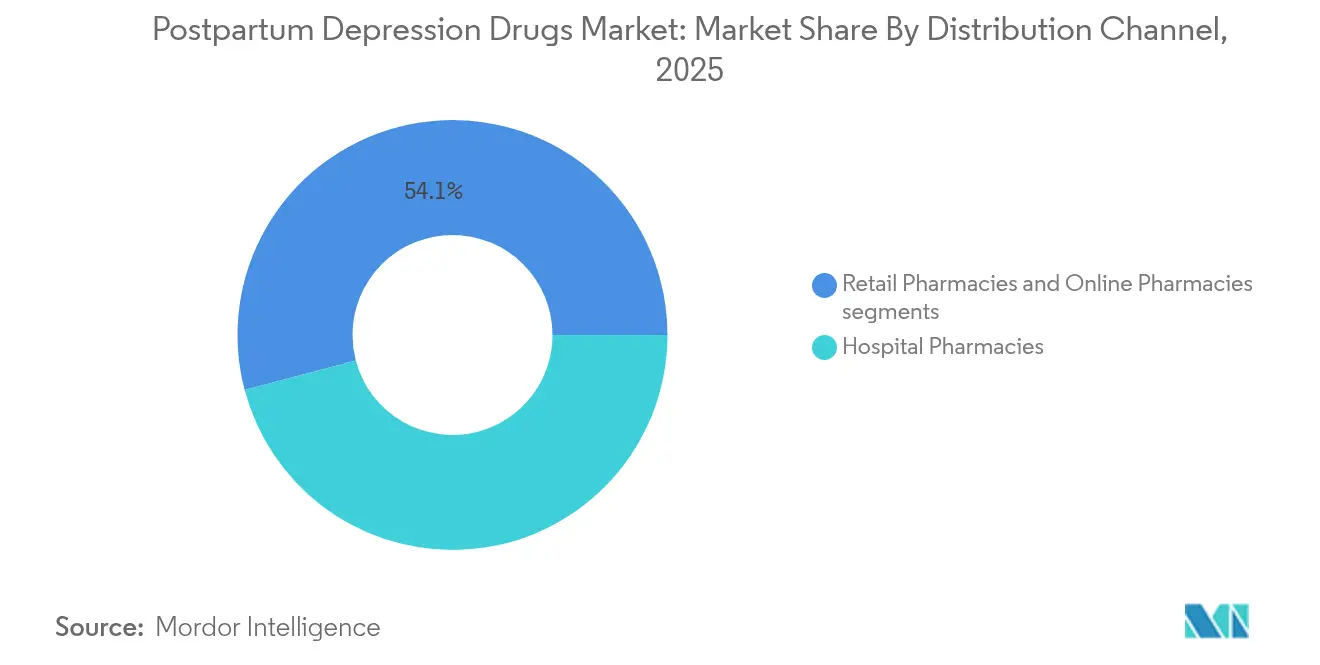

- By distribution channel: Hospital pharmacies led with 45.88% share of the postpartum depression drugs market size in 2025, whereas online pharmacies record the fastest CAGR at 10.72% through 2031.

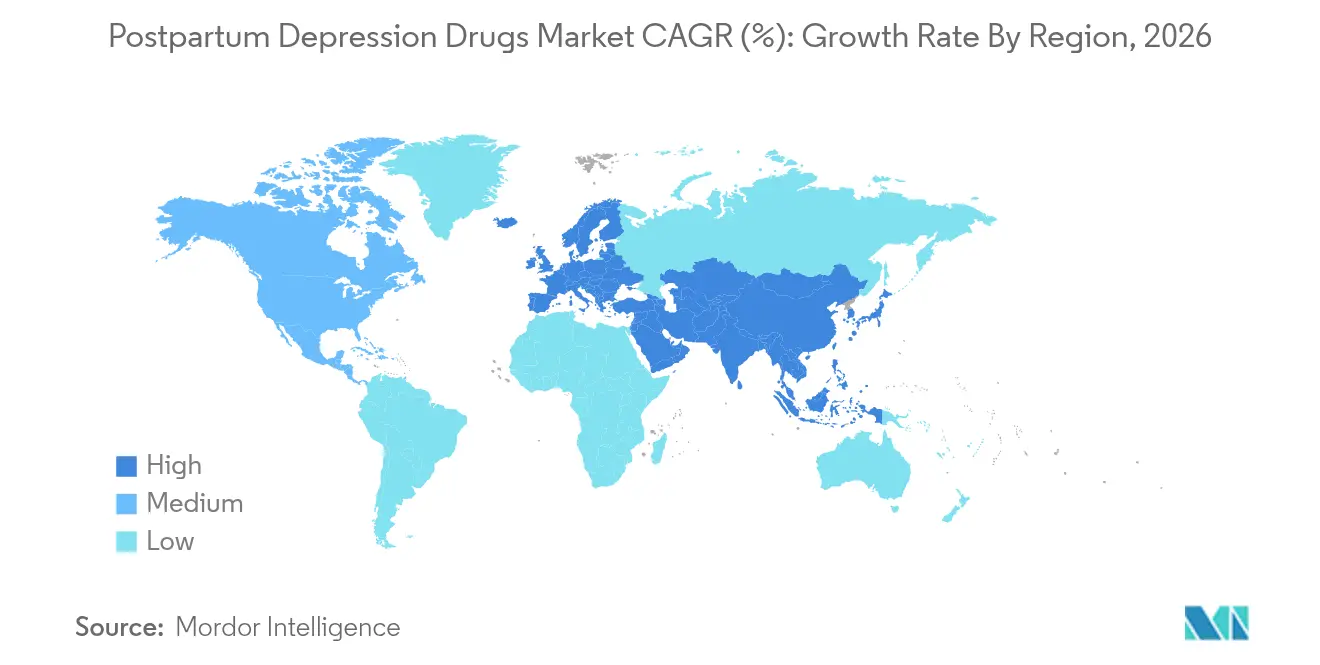

- By geography: North America accounted for 40.73% of the postpartum depression drugs market in 2025; Asia-Pacific is expanding at 11.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Postpartum Depression Drugs Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid FDA approvals of neuroactive-steroid antidepressants | +2.1% | North America, with regulatory spillover to EU and APAC | Short term (≤ 2 years) |

| Rising prevalence & screening of postpartum depression | +1.8% | Global, with concentrated impact in developed markets | Medium term (2-4 years) |

| Favorable reimbursement & maternal-mental-health parity laws | +1.5% | North America & EU, expanding to select APAC markets | Medium term (2-4 years) |

| Growing APAC healthcare spend on maternal mental health | +1.2% | APAC core, with spillover to emerging markets | Long term (≥ 4 years) |

| Digital therapeutic companions boosting adherence | +0.9% | Global, with early adoption in tech-forward markets | Short term (≤ 2 years) |

| Shift toward outpatient-friendly oral regimens | +0.8% | Global, with faster uptake in developed healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid FDA approvals of neuroactive-steroid antidepressants

Zuranolone gained breakthrough designation and priority review, compressing development by 18 to 24 months and signalling agency commitment to rapid-acting maternal therapies. Regulators accepted surrogate endpoints on Hamilton Depression Rating Scale improvements within 14 days, underpinning a more predictable pathway for follow-on compounds. Parallel guidance from the European Medicines Agency and Health Canada mirrors this stance, enlarging the addressable postpartum depression drugs market. Investor confidence has responded with heightened neurosteroid R&D budgets, and clinical pipelines now feature once-daily oral and sublingual candidates aiming for outpatient initiation.

Rising prevalence & screening of postpartum depression

Mandatory HEDIS reporting in 2025 requires US health plans to document screening rates, doubling detection versus a decade earlier. Adoption of the Edinburgh Postnatal Depression Scale in routine obstetric visits uncovers an estimated 50% formerly missed caseload, directly expanding therapy demand inside the postpartum depression drugs market. Smartphone-based assessments and AI blood tests extend reach into rural settings and normalize mental-health check-ups during pediatric appointments. Persistently higher diagnosis triggers payer recognition of unmet need, lending further support to formulary inclusions.

Favorable reimbursement & maternal-mental-health parity laws

More than 90% of US commercial and Medicaid lives now hold coverage policies that list zuranolone on preferred tiers, cutting average patient costs from USD 15,900 to routine copays. CMS maternal-mortality initiatives align federal resources behind parity enforcement, encouraging other high-income regions to match coverage breadth. State Medicaid programs fund neurosteroids and digital therapeutics in tandem, reinforcing integrated care pathways. These shifts underpin expanded utilization across the postpartum depression drugs market despite premium drug pricing.

Growing APAC healthcare spend on maternal mental health

China rolled out pediatric-integrated screening across 300 hospitals, formalizing maternal assessments within infant check-ups. Japan mandates mental-health visits at weeks 2 and 4, while India budgets for tele-counselling centers that funnel high-risk mothers into pharmaceutical care streams frontiersin.org. Private equity inflows into APAC maternal-health ventures soared 180% since 2023, accelerating digital platform expansion. These investments widen the postpartum depression drugs market footprint and lift regional demand curves above the global mean.

Restraints Impact Analysis of Postpartum Depression Drugs Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & limited coverage of novel therapies | -1.9% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| REMS & safety-monitoring burden for brexanolone | -1.1% | North America & EU, regulatory spillover globally | Short term (≤ 2 years) |

| Limited long-term efficacy data for zuranolone | -0.8% | Global, with heightened scrutiny in EU and Canada | Medium term (2-4 years) |

| Neurosteroid API supply-chain bottlenecks | -0.6% | Global, with concentrated impact in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost & limited coverage of novel therapies

Although most US payers now list zuranolone, coverage criteria vary and pre-authorization delays blunt its rapid-acting promise. Middle-income families often straddle eligibility thresholds for assistance programs, shouldering burdensome copays. Outside high-income countries, reimbursement pathways for neurosteroids remain scarce, constraining global expansion of the postpartum depression drugs market. Health technology assessors also flag limited long-term efficacy data beyond 45 days, complicating cost-effectiveness decisions compared with generic SSRIs.

REMS & safety-monitoring burden for brexanolone

Mandatory continuous monitoring and specialized infusion facilities inflated provider costs above reimbursement, leading to limited adoption and eventual withdrawal in 2025. The experience sharpened industry focus on oral neurosteroids but left lingering caution among regulators and insurers. Providers remain wary of therapies requiring complex safety programs, moderating risk-taking among sponsors entering the postpartum depression drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Postpartum Depression Drugs Market Segment Analysis

By Drug Class:

Neurosteroids Challenge SSRI DominanceSelective serotonin reuptake inhibitors retained 51.58% of postpartum depression drugs market share in 2025, underscoring their entrenched first-line status. The postpartum depression drugs market size for neuroactive-steroid antidepressants is forecast to expand at 9.88% CAGR to 2031, reflecting clinicians’ preference for rapid-acting therapies. Neurosteroids modulate GABA-A receptors, addressing hormonal disruptions that follow childbirth more directly than monoamine-based agents, a distinction that resonates with payers and guideline committees. Trial data show symptom relief within 3 days and sustained benefit through 45 days, matching the critical period for maternal–infant bonding.

Traditional classes such as tricyclics continue to shrink amid breastfeeding safety concerns, while serotonin–norepinephrine reuptake inhibitors occupy a small but stable niche when comorbid anxiety prevails. Competitive pipelines now center on once-daily or single-dose neurosteroid candidates and psychedelic analogues, suggesting the postpartum depression drugs market will tilt further toward mechanistic interventions over symptom management.

By Route of Administration:

Oral Formulations Drive AccessibilityOral products captured 71.62% of the postpartum depression drugs market size in 2025 and are growing at 10.35% CAGR as outpatient-friendly regimens become the default standard. The intravenous segment contracted after brexanolone’s withdrawal, underscoring provider reluctance toward REMS-laden infusions. Oral bioavailability breakthroughs enable therapy initiation in primary care and community obstetric settings, improving rural access and adherence. Future delivery-technology innovation, such as sublingual films and transdermal patches, remains in early development but could widen options for mothers with gastrointestinal intolerance.

Lower facility costs and reduced staffing needs make oral neurosteroids attractive to payers seeking value. Providers appreciate scheduling flexibility that aligns with postpartum visits and telehealth follow-ups. Consequently, formulary committees increasingly treat oral neurosteroids as a distinct benefit category within the postpartum depression drugs market, easing prior-authorization requirements.

By Distribution Channel:

Digital Transformation AcceleratesHospital pharmacies held 45.88% of postpartum depression drugs market share in 2025, reflecting the specialized oversight required during initial launches. Yet online pharmacies are advancing at 10.72% CAGR, propelled by patient demand for privacy, doorstep fulfillment, and digital-therapeutic bundling. Retail chains retain relevance through in-store counselling and vaccination services that dovetail with postpartum check-ups.

Digital platforms leverage integrated adherence modules, automated refill reminders, and telepsychiatry links, improving persistence. For payers, e-pharmacy routing supports closed-loop analytics on medication gaps. The competitive playbook therefore merges pharmaceutical and digital-health competencies—an emerging hallmark of leadership in the postpartum depression drugs market.

Geography Analysis

North America Postpartum Depression Drugs Market

North America dominated with 40.73% of the postpartum depression drugs market in 2025, underpinned by FDA leadership in neurosteroid approvals, expansive insurance parity laws, and high diagnostic rates exceeding 75% in major metropolitan areas. Canada mirrors US regulatory trends, while Mexico’s social-security reforms widen maternal mental-health coverage. Ongoing cost-containment debates, especially in rural regions, may temper absolute volume growth, but value gains from rapid-acting therapies remain strong.

APAC Postpartum Depression Drugs Market

Asia-Pacific is the fastest-growing region, advancing at 11.21% CAGR to 2031. China’s hospital-based screening mandates and Japan’s government-funded postpartum care programs form a template for neighboring markets . Digital health adoption, including AI risk-prediction apps, enables scalable outreach across populous nations such as India and Indonesia. The postpartum depression drugs market size for APAC is expected to accelerate as regulators streamline neurosteroid approvals and private insurers extend maternal riders.

Europe Postpartum Depression Drugs Market

Europe shows steady, policy-driven expansion. Centralized EMA approvals facilitate entry, but national price negotiations cause staggered launches. Germany and the United Kingdom lead uptake owing to robust maternal-mental-health strategies, whereas Southern Europe moves at a measured pace. Long-term efficacy data requests from health technology assessment bodies shape reimbursement timelines yet, once listed, neurosteroids achieve sustained dispensing volumes. Eastern Europe’s modernization programs add incremental demand, broadening the regional postpartum depression drugs market.

Competitive Landscape

Competition centers on a handful of neuropsychiatry specialists rather than diversified antidepressant giants. Supernus Pharmaceuticals’ USD 795 million acquisition of Sage Therapeutics in June 2025 gave the buyer control of zuranolone, the sole approved oral neurosteroid, cementing leadership in the postpartum depression drugs market. Biogen maintains a profit-sharing role, ensuring global commercialization heft while minimizing balance-sheet exposure.

Emerging rivals target differentiated mechanisms. Marinus Pharmaceuticals continues ganaxolone trials with an eye on seizure comorbidity segments, while psychedelic-based RE104 advanced into Phase II under Cleveland Clinic sponsorship. Digital-first entrants bundle cognitive-behavioral modules with prescription fulfilment, creating integrated patient journeys that blur traditional competitive lines.

Supply-chain resilience for neurosteroid active ingredients has become a strategic pillar. Firms now dual-source key intermediates after USP flagged decade-high shortages across US drug classes [2]Source: United States Pharmacopeia, “U.S. Drug Shortages Reach Decade-High,” usp.org . Partnering with contract manufacturers in India and Ireland mitigates regional risk. Companies that demonstrate secure supply and digital-engagement capability are expected to capture outsized share as the postpartum depression drugs market matures.

Postpartum Depression Drugs Industry Leaders

Pfizer Inc.

Bausch Health Companies Inc.

Lilly

Sage Therapeutics, Inc.

Cipla Inc.

- *Disclaimer: Major Players sorted in no particular order

Postpartum Depression Drugs Market Companies Covered in this Report

- Sage Therapeutics

- Biogen

- Pfizer

- Eli Lilly and Company

- GlaxoSmithKline

- Johnson & Johnson

- H. Lundbeck

- Teva Pharmaceutical Industries

- Abbvie

- Novartis

- AstraZeneca

- Sanofi

- Otsuka Pharma

- Mitsubishi Tanabe

- Cipla

- Dr Reddy’s

- Sun Pharmaceuticals Industries

- Lupin

- Amneal Pharma

- Takeda Pharmaceuticals

Recent Industry Developments in Postpartum Depression Drugs Market

- January 2025: Biogen submitted an unsolicited acquisition proposal to Sage Therapeutics for USD 7.22 per share, valuing the company at USD 1.5 billion. Sage’s board initiated strategic review

- February 2025: Sage Therapeutics outlined a 2025 strategy focused on zuranolone commercialization, digital marketing, and disciplined expense management

Postpartum Depression Drugs Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the postpartum depression (PPD) drugs market as the global prescription sales value of pharmacologic agents, mainly selective serotonin reuptake inhibitors, serotonin-norepinephrine reuptake inhibitors, and the emerging neuroactive-steroid class that treat depressive episodes beginning during pregnancy or within one year after delivery.

We exclude over-the-counter supplements, psychotherapy fees, home-based doula services, and broader maternal mental health programs.

Segments Covered in This Report

- By Drug Class

- Neuroactive-Steroid Antidepressants

- Selective Serotonin Re-uptake Inhibitors

- Serotonin-Norepinephrine Re-uptake Inhibitors

- Tricyclic & Other Classes

- By Route of Administration

- Intravenous

- Oral

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asis-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed obstetric psychiatrists, hospital pharmacy directors, and payer formulary managers across North America, Europe, and Asia. These dialogues verified treated patient pools, typical therapy length, and real-world price dispersion that desk sources could not resolve.

Desk Research

We began with tier-one public sources such as WHO maternal mental health dashboards, OECD prescription data, and US CDC Medicaid claims extracts. Regulatory portals from the FDA and EMA clarified approval dates and indicated populations, while trade groups like the Global Maternal Health Alliance reported screening uptake. Company 10-K filings supplied average selling prices, and paid platforms including Dow Jones Factiva and D&B Hoovers enriched revenue splits. Peer-reviewed journals, for example, JAMA Psychiatry, supported prevalence ranges. The sources mentioned illustrate only part of the secondary evidence pool that our team consulted.

Market-Sizing & Forecasting

We apply a top-down treated population model that starts with live birth counts, adjusts for region-specific PPD prevalence, screening rates, and treatment penetration, and multiplies by therapy duration and weighted average price. Supplier roll-ups and channel checks offer selective bottom-up validation. Key variables include neuroactive-steroid adoption, reimbursed price per course, guideline-driven screening coverage, unemployment trends, and substitution away from parenteral drugs. A multivariate regression of birth trend, payer policy index, and macroeconomic drivers produces the 2025-2030 outlook. Gaps in country volumes are bridged with proxy indicators such as SSRI import value and urban birth share.

Data Validation & Update Cycle

Every draft model passes two independent analyst reviews, variance checks against historical sales, and anomaly triggers above a five percent threshold. We refresh the dataset yearly and issue interim revisions when label expansions or safety withdrawals materially shift demand.

How Mordor Intelligence's Postpartum Depression Drugs Market Size Compares to Other Published Estimates

Published estimates often diverge because firms use different inclusion rules, prevalence inputs, and currency bases. Our team, by anchoring scope strictly to prescription drugs and by refreshing assumptions soon after the Zurzuvae launch, reduces those disconnects.

Key gap drivers include whether psychotherapy revenue is bundled, whether one-time hospital infusion costs are counted, and the exchange rate year chosen for average price conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.05 billion (2025) | Mordor Intelligence | |

| USD 915.6 million (2024) | Global Consultancy A | Excludes neuroactive-steroid launches and keeps historical prices static |

| USD 1.0 billion (2024) | Industry Research B | Bundles hormonal therapy revenue with drug sales |

| USD 79.9 million (2024) | Sector Insights C | Counts North America only and omits generic SSRI revenue |

The comparison shows that Mordor's disciplined scope selection and annual refresh deliver a balanced, transparent baseline traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the postpartum depression drugs market?

The market is valued at USD 1.15 billion in 2026 and is projected to reach USD 1.79 billion by 2031, growing at a 9.27% CAGR.

Which drug class is expanding fastest?

Neuroactive-steroid antidepressants are the fastest-growing class, advancing at 9.88% CAGR through 2031 while challenging the dominance of SSRIs.

Why did brexanolone leave the market?

Mandatory REMS monitoring, a 60-hour infusion, and high administration costs limited adoption, leading to FDA withdrawal in 2025.

Which region has the biggest share in Global Postpartum Depression Drugs Market?

In 2025, the North America accounts for the largest market share in Global Postpartum Depression Drugs Market.

How are parity laws influencing access?

More than 90% of US commercial and Medicaid plans now cover neurosteroid therapies, sharply reducing patient out-of-pocket costs and accelerating uptake.

Page last updated on: