Transformerless UPS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

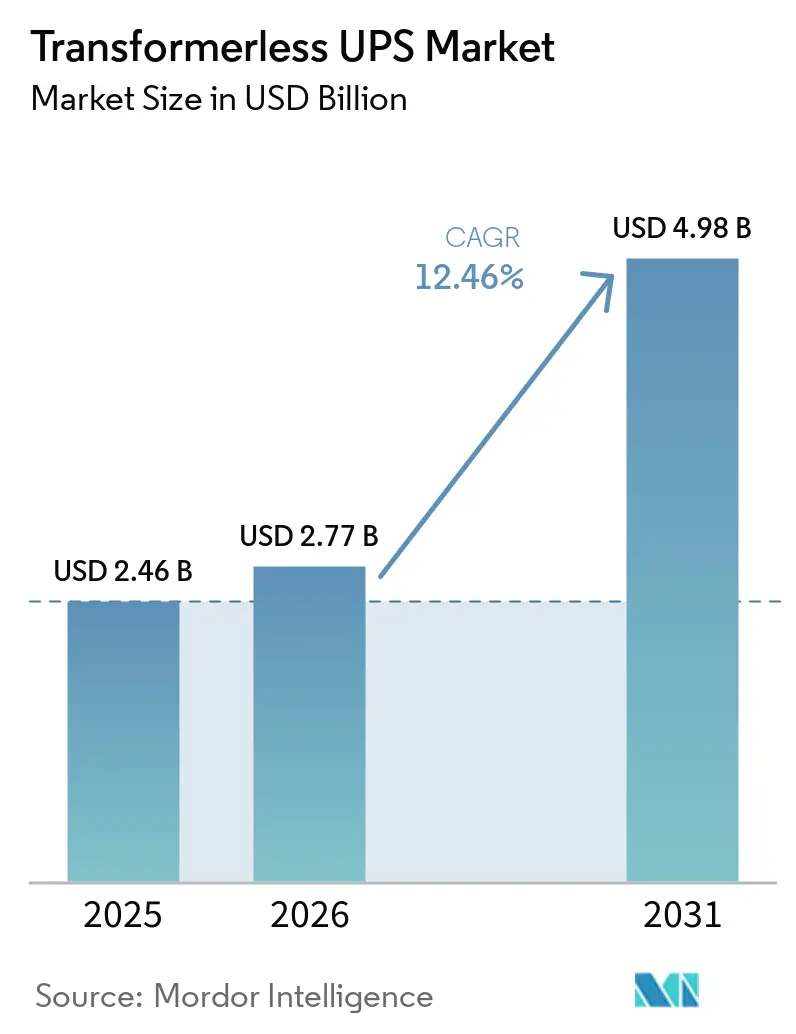

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 4.98 Billion |

| Growth Rate (2026 - 2031) | 12.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transformerless UPS Market Analysis by Mordor Intelligence

The transformerless UPS market size was valued at USD 2.46 billion in 2025 and is estimated to grow from USD 2.77 billion in 2026 to reach USD 4.98 billion by 2031, at a CAGR of 12.46% during the forecast period 2026-2031. The transformerless UPS market is entering a stronger growth phase as AI workloads, hyperscale data center expansion, and broader edge deployment are increasing the need for fast-response, high-efficiency power protection across more critical facilities. Higher double-conversion efficiency, lower weight, and a smaller installation footprint are making transformerless systems a preferred option in projects where energy loss, cooling burden, and room utilization are all being examined more closely during procurement. The transformerless UPS market is also gaining from modular buying patterns, because operators now prefer staged capacity additions and maintenance models that reduce downtime while preserving flexibility as load forecasts continue to change. Competition remains moderate, with European suppliers defending premium positions through certified performance and integration strength, while Chinese OEMs continue to scale through manufacturing depth, broader product coverage, and supply chain proximity in Asia. Growth still faces clear pressure from high system and battery capex, compatibility issues in legacy high-inrush environments, cybersecurity exposure in network-connected power controls, and wider semiconductor qualification timelines that can slow delivery and commissioning in time-sensitive projects.

Key Report Takeaways

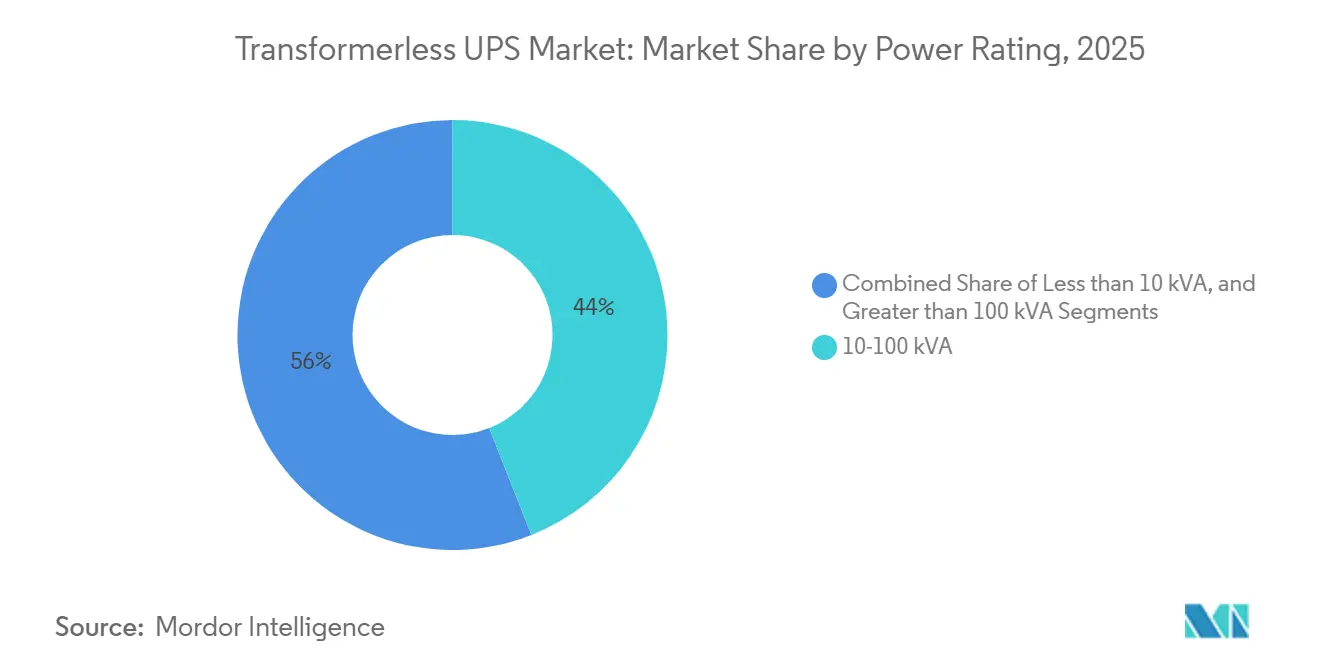

- By power rating, 10-100 kVA accounted for 44.02% share of the transformerless UPS market in 2025, while more than 100 kVA is forecast to grow at 12.68% CAGR through 2031.

- By phase, three-phase systems led with 66.23% share of the transformerless UPS market in 2025, while single-phase systems are projected to advance at 12.91% CAGR through 2031.

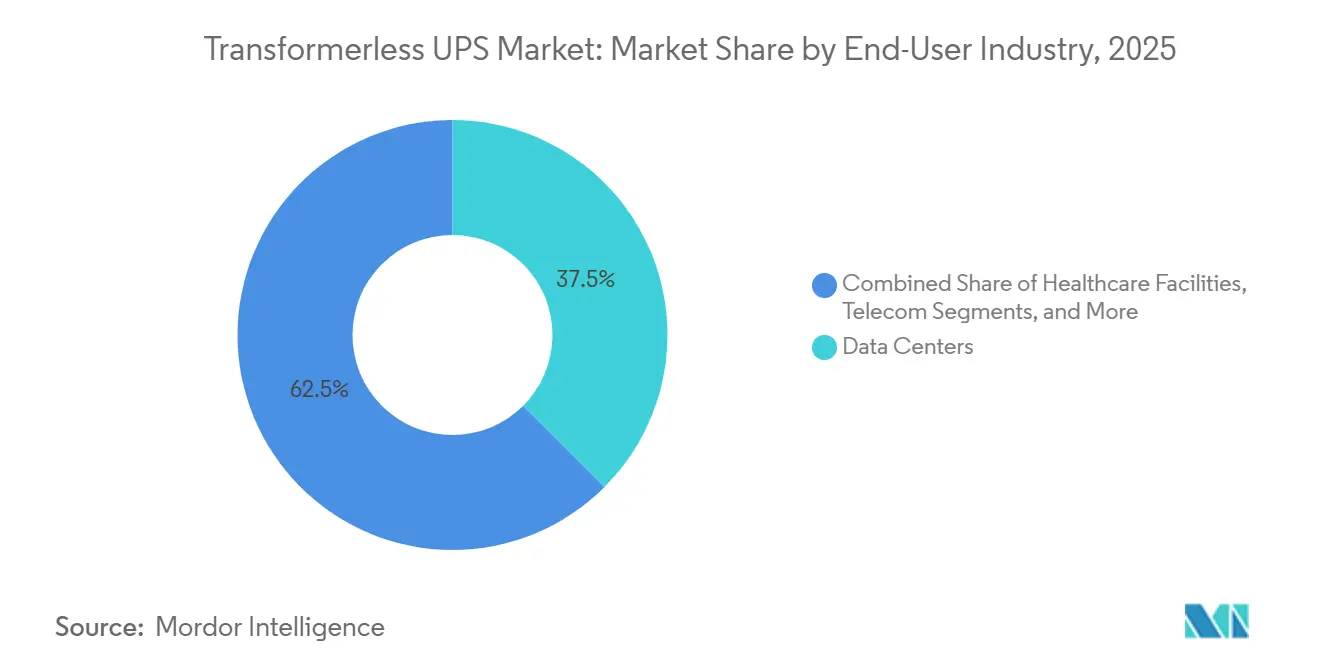

- By end-user industry, data centers held 37.51% share of the transformerless UPS market in 2025, while telecom is projected to expand at 13.08% CAGR through 2031.

- By form factor, tower systems captured 40.17% share of the transformerless UPS market in 2025, while modular systems are expected to grow at 12.82% CAGR through 2031.

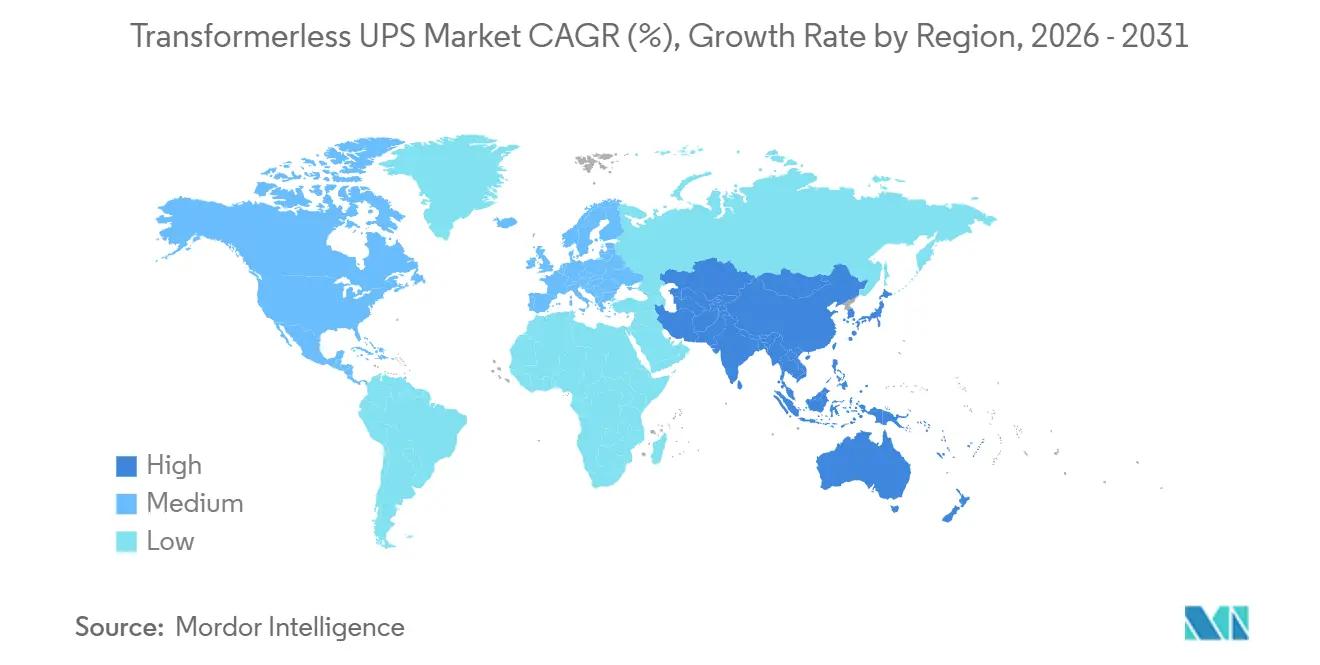

- By geography, Asia-Pacific held 43.54% share of the transformerless UPS market in 2025, while Asia-Pacific is forecast to expand at 12.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Transformerless UPS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale Data Center Capacity Expansion | +3.2% | Global, concentrated in North America and Asia-Pacific core, with spill-over to Europe and the Middle East | Short term (≤ 2 years) |

| Rising Energy Efficiency and Total Cost of Ownership Focus | +2.5% | Global, highest regulatory intensity in Europe and North America | Medium term (2-4 years) |

| Growing Preference for High Power Density and Reduced Footprint | +2.0% | Global, highest intensity in Asia-Pacific and North America hyperscale corridors | Short term (≤ 2 years) |

| Modular UPS Adoption for Staged Capacity Expansion | +1.6% | North America, Europe, and Asia-Pacific data center build zones | Medium term (2-4 years) |

| Silicon Carbide Power Stage Efficiency Gains | +1.1% | Global, with R&D origins in Europe and North America and manufacturing scale in Asia-Pacific | Long term (≥ 4 years) |

| Grid-Interactive UPS Use for Tariff Optimization | +0.7% | North America, Asia-Pacific core, with spill-over to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Data Center Capacity Expansion

The transformerless UPS market is closely tied to the current data center build cycle, because new AI campuses are being planned around higher rack density, faster power swings, and much lower tolerance for voltage instability than earlier enterprise facilities. Amazon announced in April 2026 that it will invest USD 25 billion in Mississippi data centers, which shows that very large-scale infrastructure commitments are still flowing into new digital capacity.[1]Amazon Staff, “Amazon to Invest $25 Billion in Mississippi Data Centers,” About Amazon, aboutamazon.com This matters for UPS vendors because dense AI rooms require protection systems that can respond quickly, remain efficient under heavy load, and fit into power rooms already under pressure from cooling and switchgear requirements. Vertiv’s December 2024 launch of a compact, high-power-density UPS platform for large data centers, with ratings from 250 kW to 1,250 kW, demonstrated that supplier roadmaps are already shifting toward larger protected loads in fewer cabinets. Piller also supplied more than 200 UPS units for Nebius Group’s expansion in Finland, where the site is being expanded to 75 MW with a target PUE as low as 1.1, which reflects the deployment scale now shaping procurement decisions. As more projects move toward hyperscale, colocation, and AI-focused campuses, the transformerless UPS market is increasingly aligning with fast-response, high-frequency power architectures that can support dense, highly dynamic compute environments.

Rising Energy Efficiency And Total Cost Of Ownership Focus

The transformerless UPS market is also expanding because energy loss is now a financial issue alongside resilience, rather than a secondary technical consideration left for facility teams to solve after installation. Vertiv reported up to 97.5% double-conversion efficiency for its PowerUPS 9000 platform, which reflects the performance threshold now expected in large, critical environments where power costs and thermal loads are both under review. Centiel stated that PremiumTower S2 achieves up to 97.1% efficiency in VFI mode and avoids scheduled component replacements over a design life exceeding 15 years, supporting the move toward lifecycle-based procurement rather than first-cost decisions alone. The U.S. Department of Energy’s wide-bandgap power electronics framework also highlighted how advanced power electronics can improve efficiency, power density, and system performance across industrial and grid-connected applications, which supports the technology case for newer transformerless designs. In practical terms, this means buyers in the transformerless UPS market are now weighing power loss, cooling demand, maintenance cycles, and operating profile with greater discipline than in earlier procurement cycles. In Europe, the EU Ecodesign Directive has reinforced that direction by setting a practical procurement floor for many installations above 10 kVA.

Growing Preference For High Power Density And Reduced Footprint

The transformerless UPS market is benefiting from a stronger preference for high power density and reduced footprint, especially in facilities where every square meter of technical space has a direct revenue or utilization value. Vertiv said its compact, high-power-density UPS launched in December 2024 delivered a 32% smaller physical footprint than the prior generation while supporting 250-1,250 kW per unit, underscoring how strongly suppliers are pushing cabinet-level density. Centiel stated that its scalable architecture can support applications ranging from 10 kW to 3.75 MW within a common cabinet family, helping operators standardize deployment logic from edge environments to large campuses without changing platform direction. These characteristics matter because transformerless designs remove the heavy magnetic block that once added weight, footprint, and installation constraints in many sites, especially where access routes and floor loading are already tight. They also fit better with prefabricated and containerized deployment models, where shipping size, installation speed, and reduced on-site assembly work all influence the investment case. As density rises in AI rooms, colocation halls, industrial plants, and telecom shelters, the transformerless UPS market continues to favor systems that can protect more load without demanding the same increase in floor area.

Modular UPS Adoption For Staged Capacity Expansion

The transformerless UPS market is gaining from modular architecture because buyers now place much more value on staged expansion and maintenance flexibility than they did when demand growth was easier to forecast. Centiel’s modular platform illustrates this shift, with a scale path from smaller edge applications to multi-megawatt deployments inside a common design approach that supports continuity across different site types. Vertiv’s Liebert APM2 brochure positions the modular UPS for flexible scaling from 30 kW to 600 kW, strong operating efficiency, and easier service planning in critical environments where downtime windows are limited, and capacity needs can change over time. This model reduces stranded capacity, shortens repair windows, and lets operators add power blocks closer to actual demand rather than committing the full power room budget years ahead of need. It also fits distributed 5G, edge inference, and smaller colocation deployments, where each site has limited installed load but the overall network expands gradually across a large number of locations. For that reason, modular systems are moving from an attractive option to a mainstream buying model across the transformerless UPS market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront System and Battery Capex | -2.0% | Global, most acute in South America, Africa, and Southeast Asia | Short term (≤ 2 years) |

| Load Compatibility Limits in High-Inrush and Legacy Environments | -1.3% | Global, concentrated in legacy industrial, healthcare, and manufacturing deployments | Medium term (2-4 years) |

| Cybersecurity Exposure of Network-Connected Power Controls | -0.8% | Global, highest regulatory intensity in North America and Europe | Long term (≥ 4 years) |

| Wide-Bandgap Semiconductor Supply Concentration | -0.5% | Global, most acute in regions outside Asia-Pacific’s domestic SiC supply cluster | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront System And Battery Capex

Upfront costs remain a real brake on the transformerless UPS market, especially when lithium-ion battery cabinets are added to projects that are still being judged mainly on acquisition price rather than long-term operating economics. Smaller enterprises, distributed telecom operators, and budget-constrained institutions often face approval processes that reward the lowest initial capital request, even when a more efficient system would perform better across the asset life. The issue becomes sharper in healthcare, where NFPA 99 and NFPA 110 set strict requirements for essential electrical systems and emergency power performance, raising the total project budget beyond UPS hardware alone and making capital approval more difficult for smaller hospital networks.[2]National Fire Protection Association, “NFPA 99, Health Care Facilities Code,” National Fire Protection Association, nfpa.org That means the case for lithium-ion, lower replacement frequency, faster recharge, reduced cooling demand, and less maintenance labor, can still lose against short-budget planning and fragmented procurement authority. The barrier is most visible in South America, Africa, and parts of Southeast Asia, where battery supply depth, financing options, and long-horizon facility planning are often less developed than in mature markets. Even when operators accept the lifecycle argument, the transformerless UPS market can still lose near-term orders if the initial package exceeds the capital threshold a site can approve.

Load Compatibility Limits In High-Inrush And Legacy Environments

Load compatibility still limits the transformerless UPS market in brownfield industrial and healthcare projects, where the existing electrical profile was designed around older isolation-based equipment, and site teams are cautious about introducing a different behavior pattern. Legacy facilities often include motor-driven loads, transfer schemes, harmonic mitigation equipment, and generator interfaces that were sized for earlier rectifier profiles and inrush absorption characteristics different from those seen in modern transformerless systems. That creates a need for additional engineering checks, site modeling, commissioning work, and, in some cases, the redesign of adjacent electrical equipment before a replacement can proceed with confidence. The issue does not signal a broad rejection of transformerless systems, but it does slow adoption in environments with strict uptime requirements and where operators cannot absorb commissioning surprises in live production or care environments. It is especially relevant in industrial retrofits, because automation upgrades in automotive, pharmaceutical, and food processing sites are often layered onto existing power rooms rather than designed into new shells from the start. These compatibility questions do not stop long-term demand, but they do stretch project timelines and make the transformerless UPS market harder to penetrate in the most legacy-heavy environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Mid-Range kVA Anchors Volume, High-Power Tier Accelerates

The 10-100 kVA segment accounted for 44.02% of the transformerless UPS market in 2025, making it the volume center of demand across commercial buildings, edge nodes, mid-size enterprise data centers, telecom base stations, and a wide base of repeat replacement activity. This range fits projects that need meaningful resilience without the space commitment, engineering complexity, and capital burden associated with much larger installations, which is why it remains relevant across both mature and emerging deployment settings. It also aligns well with the practical operating profile of many enterprise and telecom sites, where systems spend long periods below peak load, thereby benefiting from strong partial-load efficiency and manageable installation requirements. The less than 10 kVA range still serves distributed branch offices and small facilities, but its smaller scale and lower efficiency limit its influence as procurement priorities shift toward lifecycle cost, density, and performance across the broader transformerless UPS market.

The more than 100 kVA segment is projected to grow at a 12.68% CAGR through 2031, supported by AI data center buildouts, large colocation halls, and industrial critical loads moving into megawatt-scale protection requirements. Vertiv’s PowerUPS 9000 supports 250-1,250 kW per unit and scales to 5 MW, which shows how suppliers are targeting larger protected load blocks with higher cabinet density and a stronger fit for large digital campuses.[3]Vertiv, “Vertiv Introduces Industrial-Grade UPS Designed for Commercial and Industrial Environments,” Vertiv, vertiv.com Peer-reviewed research on a 500 kW SiC-based three-phase UPS also showed that an optimized filter and heat-dissipation design can support large-capacity operation with credible commercial relevance, helping validate the technical path for larger transformerless platforms. That combination of commercial product readiness and technical validation suggests that the upper power tier will continue to gain weight as the transformerless UPS market shifts toward high-density compute, large industrial automation, and larger critical facilities.

By Phase: Three-Phase Systems Anchor Critical Infrastructure Revenue

Three-phase systems held 66.23% of the revenue share in 2025, keeping them at the center of deployment in large data centers, industrial plants, and major commercial facilities, where balanced power distribution and higher-density load support are standard design assumptions. That lead reflects the installed architecture of critical infrastructure, because large facilities already depend on electrical layouts that favor three-phase topology for efficiency, stability, and straightforward integration with upstream and downstream equipment. The segment also benefits from a regulatory and reporting environment that increasingly rewards more efficient power infrastructure in Europe and other mature markets, making older, low-efficiency equipment harder to justify in new projects and replacement cycles. In practice, this keeps three-phase platforms as the default choice whenever projects move beyond smaller room-level, branch-level, or single-cabinet backup requirements in the transformerless UPS market.

Single-phase systems are projected to grow at a 12.91% CAGR through 2031, making them the fastest-growing phase segment and signaling wider use in distributed digital infrastructure rather than a retreat from critical applications. Growth comes from 5G small cells, edge computing nodes, branch facilities, and compact enterprise sites where three-phase supply is either unavailable or oversized relative to the installation's actual demand profile. Modern single-phase designs have narrowed earlier performance gaps through better output power factor, cleaner power delivery, and higher efficiency, thereby improving their credibility in smaller yet still sensitive applications. As deployment expands across many compact or remote sites instead of a few very large ones, single-phase products are broadening the transformerless UPS market rather than displacing the installed base of three-phase systems.

By End-User Industry: Data Centers Anchor Demand While Telecom Scales Fastest

Data centers held a 37.51% share in 2025, making them the largest end-user group in the transformerless UPS market and confirming that digital infrastructure remains the main demand anchor for premium efficiency and fast-response power protection. This position reflects the dependence of modern data halls on power systems that can respond to rapid load shifts, support dense rack environments, and limit energy loss at scale across facilities where uptime and operating efficiency are both under constant scrutiny. Piller supplied more than 200 UPS units for Nebius Group’s expansion in Finland, where site capacity is being increased to 75 MW with a target PUE as low as 1.1, illustrating the deployment scale and performance expectations that now define this end-user segment. Industrial manufacturing, commercial buildings, and healthcare also remain meaningful pockets of demand because each links power continuity to operating output, equipment protection, business continuity, or regulated service delivery in different ways.

Telecom is projected to expand at a 13.08% CAGR through 2031, making it the fastest-growing end-user segment and tying a rising share of new demand to 5G densification and distributed network infrastructure. Small cells and edge telecom sites draw materially more power than earlier network generations, and they need compact backup systems that can fit inside constrained shelters, roadside enclosures, and cabinet-based deployments without sacrificing reliability. Vertiv launched the PowerUPS 6000 Industrial in March 2026 for commercial and industrial environments, demonstrating how suppliers are expanding their addressable market with products designed for harsher conditions, broader battery compatibility, and tighter environmental tolerances. Healthcare demand remains structurally steady as NFPA 99 and NFPA 110 continue to anchor essential power requirements for operating rooms, intensive care units, and other critical hospital areas that cannot tolerate interruption.

By Form Factor: Tower Leads, Modular Changes Capital Planning

Tower systems captured a 40.17% share in 2025, maintaining their position as the largest form factor in installed revenue and reflecting the continued weight of brownfield replacement programs in data centers and commercial buildings. That lead came from replacement-in-kind buying patterns, because many operators still prefer a familiar cabinet layout when upgrading existing power rooms with limited space for redesign or long shutdown windows for major reconfiguration. Centiel’s PremiumTower S2 launch in October 2025 showed that the tower format is still evolving, with 10-80 kW coverage, support for lead-acid, lithium-ion, NiCd, and flywheel options, and up to 97.1% efficiency in VFI mode. Rack-mounted systems continue to serve distributed enterprise and edge environments where direct integration into standard IT rack rows is more important than large-cabinet scale or megawatt-class density.

Modular systems are forecast to grow at a 12.82% CAGR through 2031, making them the fastest-growing form factor in the transformerless UPS industry and reflecting a clear shift in how operators want to fund and maintain critical power. That pace is tied to staged deployment logic because modular systems let operators add capacity over time rather than buying fixed headroom years before the load actually arrives at the site. Vertiv’s modular Liebert APM2 platform, available in sizes from 30 kW to 600 kW, illustrates how suppliers are aligning modular design with scalable deployment, high operating efficiency, and easier service access in mission-critical environments. As hyperscale, colocation, and edge users all seek staged expansion, modular architecture is changing how the transformerless UPS industry allocates capital, plans service, and reduces downtime exposure across the life of the installation.

Geography Analysis

Asia-Pacific held a 43.54% share in 2025, and the regional transformerless UPS market is forecast to grow at a 12.55% CAGR through 2031, keeping the region as both the largest and the fastest-growing geography in the current outlook. This position reflects the combined effect of China’s digital infrastructure programs, Japan’s semiconductor-fab revival, and India’s Digital Public Infrastructure agenda, all of which support new demand for efficient, compact power protection across data center, telecom, and industrial settings. The region also benefits from closer access to SiC and related power-electronics supply chains, which improves manufacturing economics and can reduce lead-time pressure as procurement cycles tighten. That supply chain advantage matters because buyers in large data center and telecom programs are placing more value on delivery reliability, flexible configuration, and cost discipline as project size continues to increase. For these reasons, the transformerless UPS market in Asia-Pacific is likely to remain the main growth engine through the forecast period.

North America forms the second major demand center in the transformerless UPS market, supported by hyperscale expansion, grid investment, and continued capital spending on large data center campuses. Amazon said in April 2026 that it would invest USD 25 billion in Mississippi data centers, signaling that significant new critical power infrastructure is still being planned in the region. Eaton reported that U.S. investor-owned utilities plan around USD 400 billion in grid upgrades over 5 years in response to rising data center power demand, underscoring the broader system impacts now surrounding digital infrastructure growth.[4]Eaton, “2025 Data Center Progress Report, Digital Transformation and Energy Management in the Wake of AI,” Eaton, eaton.com Europe remains commercially important because efficiency regulations and replacement cycles continue to favor modern, high-efficiency systems, especially in data center and industrial settings, where operating losses and reporting obligations are taken more seriously. That keeps Europe central to premium demand, even if it does not match Asia-Pacific's scale.

South America, the Middle East, and Africa remain smaller in absolute terms, but they are strategically important because 5G rollout, colocation buildout, and grid instability are creating demand patterns that differ from mature regions and often favor compact, efficient backup architectures. Brazil and Argentina remain the main South American demand centers, while the United Arab Emirates and Saudi Arabia are generating larger three-phase requirements through state-backed digital infrastructure programs and AI-linked facility development. In Africa, telecom applications remain central because operators need longer backup capability within constrained cabinets, and UPTECH markets transformerless UPS products that combine compact size, efficiency, and telecom-grade reliability. These frontier regions will not define current revenue leadership, but they do widen the addressable base of the transformerless UPS market and strengthen the case for broader product portfolios across the forecast period.

Competitive Landscape

The transformerless UPS market shows moderate concentration, with a recognizable group of European specialists and a fast-scaling set of Chinese OEMs shaping competition across the major application categories. Vertiv, Centiel, Socomec, Riello, and Piller compete heavily on efficiency, certified performance, resilience credentials, and the ability to integrate into large critical power projects where uptime, compliance, and service depth all influence supplier choice. Kehua Data, KSTAR, INVT Power, and East Group compete more on manufacturing scale, product breadth, and proximity to Asian component ecosystems, which gives them an advantage in cost control and regional responsiveness. This creates a two-speed structure in which premium suppliers defend margins through performance and service, while lower-cost challengers continue to pressure pricing and lead-time expectations. As a result, the transformerless UPS market is neither fragmented in an unstructured way nor concentrated enough for any single supplier bloc to dictate project standards without strong competition.

Centiel took a notable strategic step in April 2026 when it listed on the SIX Swiss Exchange at an implied market capitalization of CHF 261 million (USD 277 million), providing it with fresh capital for international expansion and deeper partnerships in critical power solutions. Vertiv expanded its addressable base in March 2026 with the PowerUPS 6000 Industrial, a product aimed at commercial and industrial environments that need higher environmental tolerance, broader battery compatibility, and reliable operation in more demanding site conditions. Piller strengthened its relevance in large AI facilities through the Nebius deployment in Finland, where more than 200 UPS units were supplied for a site expanding to 75 MW.[5]Piller Group GmbH, “Piller Supports Finland’s AI Infrastructure Expansion With Critical Power Protection,” Piller, piller.com These moves show that access to capital, application-specific design, and proof of execution in large facilities are becoming as important as raw electrical performance in competitive positioning. Chinese suppliers also continue to gain long-term leverage from localized component ecosystems, even though export certification and premium-brand trust remain higher barriers in some Western procurement environments.

Technology direction has become a decisive theme in the transformerless UPS market because SiC adoption, predictive maintenance, and grid-aware software can change both product economics and customer retention over time. Vertiv’s December 2024 launch also highlighted Next Predict's predictive maintenance capability using AI and machine learning, pointing to service-led revenue opportunities that extend beyond hardware sales and deepen supplier relationships after installation. Nature Energy research showed that software orchestration reduced power use by 25% in a 256-GPU AI cluster during grid stress events without affecting compute quality of service, supporting longer-term interest in grid-interactive UPS strategies and smarter control layers around critical power assets. If that model matures further, the transformerless UPS market will capture more value from software, controls, energy participation, and analytics, rather than solely from hardware efficiency and cabinet design.

Transformerless UPS Industry Leaders

Socomec Group S.A.

ABB Ltd.

Riello Elettronica S.p.A.

Vertiv Group Corporation

Fuji Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bergen Engines, part of Langley Holdings Power Solutions Division, parent of Piller Group GmbH, secured over 500 MW in orders from Liberty Energy for AI data center power services, a scale indicative of the structural shift in critical power procurement as AI campuses move from tens of megawatts to multi-hundred-megawatt planning horizons.

- April 2026: Centiel SA is listed on the SIX Swiss Exchange under the ticker CNTL following a reverse merger with HT5 AG, with shares opening at CHF 3.20 per share (USD 3.39) and an implied market capitalization of CHF 261 million (USD 277 million). The transaction raised CHF 31 million (USD 32.9 million) to fund international expansion and deeper partnerships in the critical power solutions market.

- March 2026: Vertiv launched the PowerUPS 6000 Industrial, an IP42-rated UPS for commercial and industrial environments including manufacturing, oil and gas, and pharmaceutical sectors, operating at ambient temperatures up to 50 °C, with double-conversion efficiency of up to 97%, compatibility with VRLA, Ni-Cd, and lithium-ion battery cabinets, and certification to European standards EN 50121 and EN 50171.

- June 2025: Piller Group GmbH, through its Active Power subsidiary, supplied over 200 CleanSource battery-free UPS units for the Nebius Group data center expansion in Mäntsälä, Finland, one of Europe’s largest AI data center expansions, increasing capacity to 75 MW with a target PUE as low as 1.1.

Global Transformerless UPS Market Report Scope

The Transformerless UPS Market Report is Segmented by Power Rating (Less Than 10 KVA, 10-100 KVA, and Greater than 100 kVA), Phase (Single-Phase, and Three-Phase), End-User Industry (Data Centers, Industrial Manufacturing, Commercial Buildings, Healthcare Facilities, Telecom, and Other End-user Industries), Form Factor (Rack-Mounted, Tower, and Modular), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Less than 10 kVA |

| 10-100 kVA |

| Greater than 100 kVA |

| Single-Phase |

| Three-Phase |

| Data Centers |

| Industrial Manufacturing |

| Commercial Buildings |

| Healthcare Facilities |

| Telecom |

| Other End-user Industries |

| Rack-mounted |

| Tower |

| Modular |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Power Rating | Less than 10 kVA | |

| 10-100 kVA | ||

| Greater than 100 kVA | ||

| By Phase Type | Single-Phase | |

| Three-Phase | ||

| By End-user Industry | Data Centers | |

| Industrial Manufacturing | ||

| Commercial Buildings | ||

| Healthcare Facilities | ||

| Telecom | ||

| Other End-user Industries | ||

| By Form Factor | Rack-mounted | |

| Tower | ||

| Modular | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for transformerless UPS?

The transformerless UPS market was valued at USD 2.46 billion in 2025, is estimated at USD 2.77 billion in 2026, and is forecast to reach USD 4.98 billion by 2031 at a 12.46% CAGR.

Which end-user group currently leads demand for transformerless UPS systems?

Data centers led demand in 2025 with a 37.51% share, reflecting their need for high-efficiency and fast-response power protection in dense compute environments.

Why are modular UPS systems expanding faster than other form factors?

Modular systems are forecast to grow at 12.82% CAGR through 2031 because operators prefer staged capacity additions, faster serviceability, and lower stranded capital in uncertain load environments.

Which region is expanding the fastest?

Asia-Pacific is both the largest region, with 43.54% share in 2025, and the fastest-growing one, with a projected 12.55% CAGR through 2031.

What is holding back adoption in some projects?

The main obstacles are high upfront system and battery capex, compatibility issues in legacy high-inrush environments, cybersecurity exposure in connected controls, and tighter semiconductor supply conditions.

How are leading suppliers differentiating themselves?

Leading suppliers are competing through efficiency, certified performance, data center integration, modularity, predictive maintenance tools, and product designs tailored to industrial, telecom, and AI-driven facilities.

Page last updated on: