Total Ankle Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

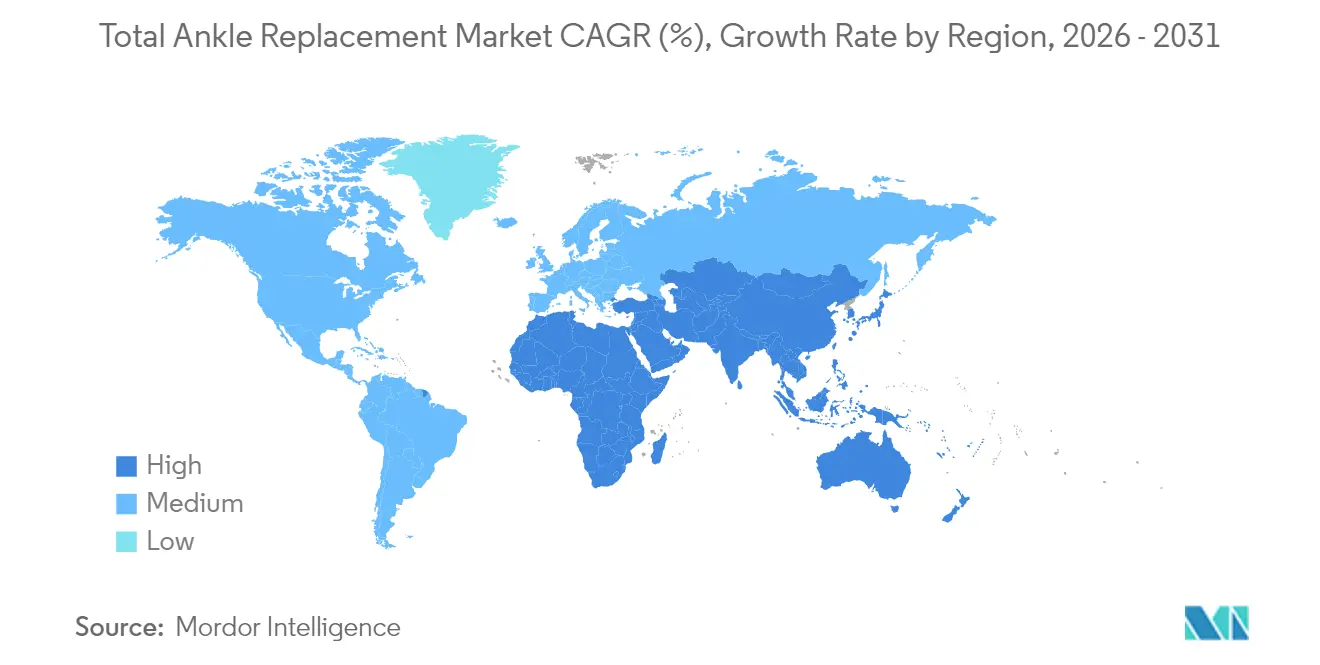

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

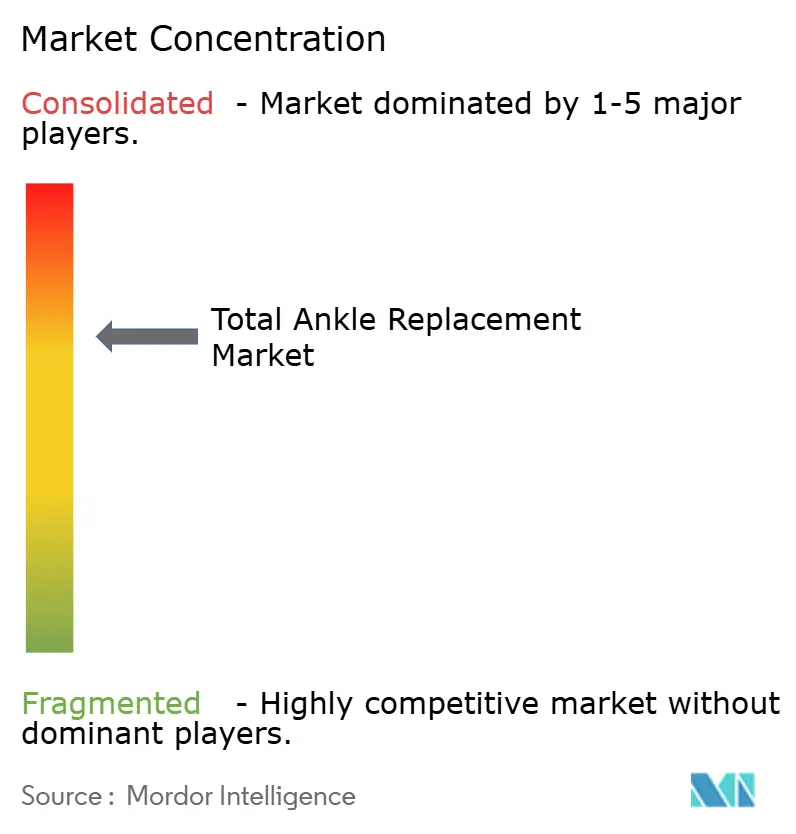

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Total Ankle Replacement Market Analysis by Mordor Intelligence

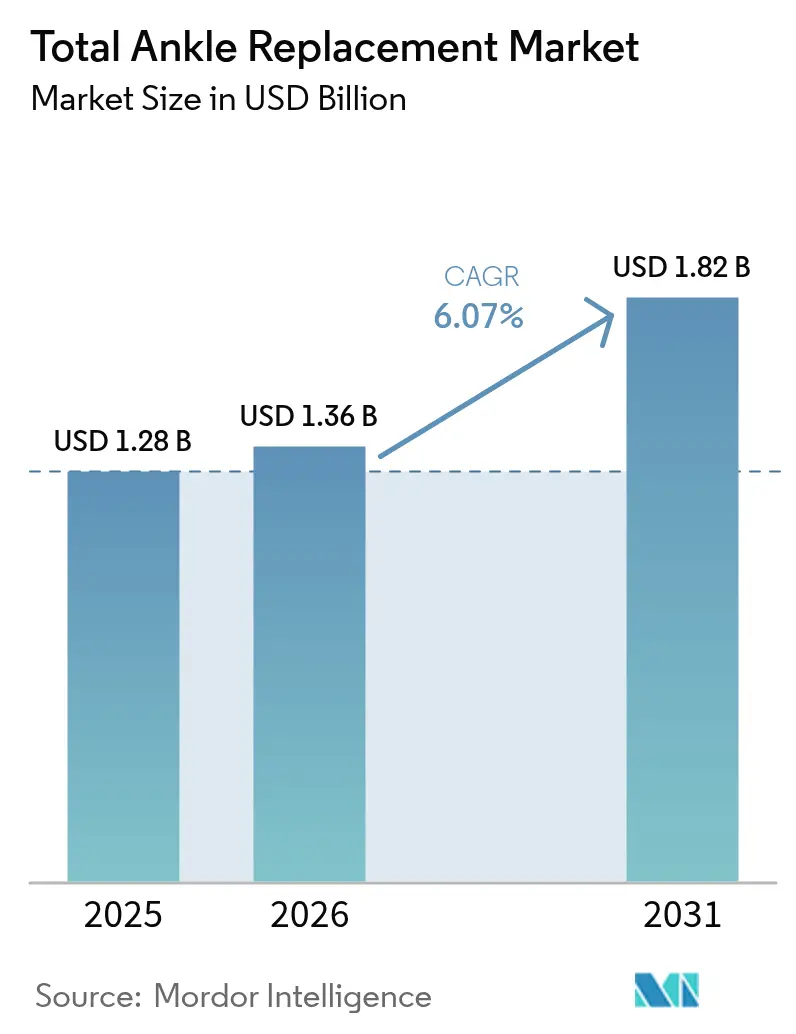

The Total Ankle Replacement Market size was valued at USD 1.28 billion in 2025 and estimated to grow from USD 1.36 billion in 2026 to reach USD 1.82 billion by 2031, at a CAGR of 6.07% during the forecast period (2026-2031).

This growth shows the procedure’s transformation from a niche therapy to a mainstream option for end-stage ankle arthritis as fourth-generation implants extend survivorship, reduce revision risk, and allow surgeons to select designs that mimic native ankle biomechanics. Adoption is rising as patient-specific 3D-printed components, smart instrumentation, and robotic guidance improve accuracy, while clinical guidelines now recommend motion-preserving surgery for younger and more active cohorts. Outpatient migration advances because CMS removed total ankle arthroplasty from the inpatient-only list in 2024, prompting hospitals and ambulatory surgical centers to re-organize care pathways around same-day discharge protocols. Competitive pressure remains high after Zimmer Biomet’s USD 1.1 billion acquisition of Paragon 28 in 2025, and manufacturers continue to bundle implants with digital planning software, artificial-intelligence-enabled sensors, and value-based service agreements to protect share. Reimbursement remains a critical factor; although commercial payers increasingly recognize the procedure’s cost-utility versus fusion, emerging markets still wrestle with high device prices, limited surgeon training, and inconsistent insurance coverage.

Key Report Takeaways

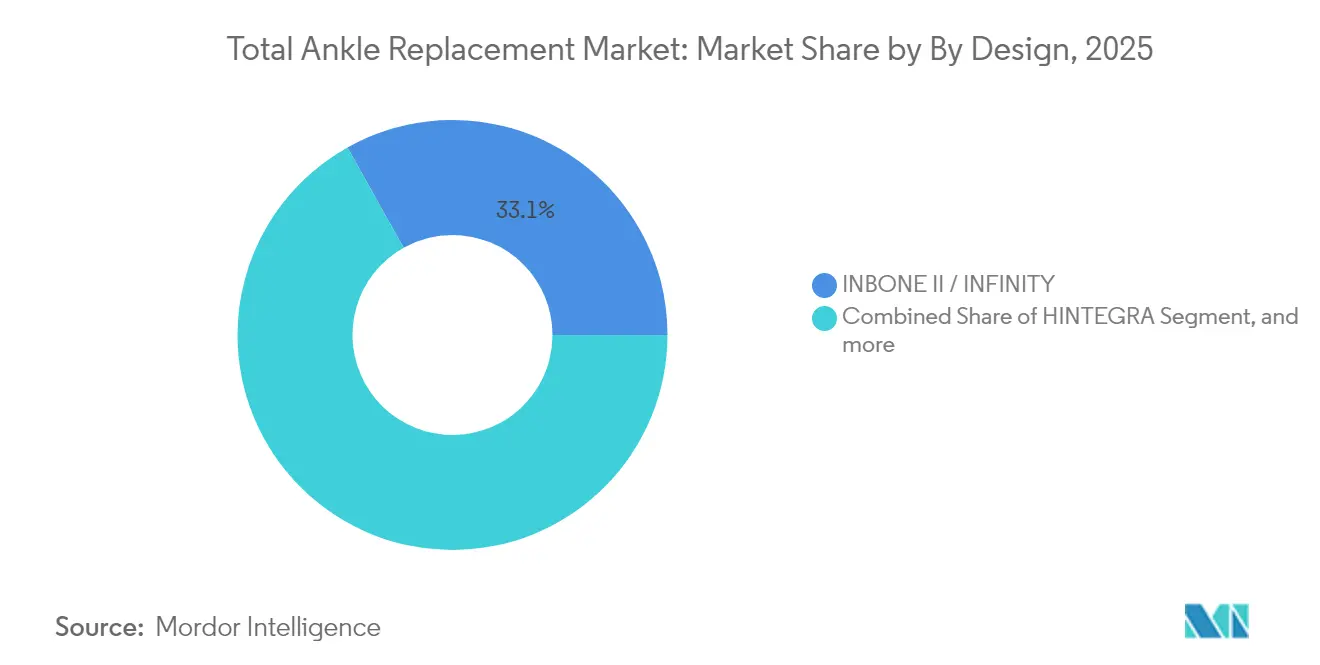

- By design, INBONE II/INFINITY held 33.12% of total ankle replacement market share in 2025, while CADENCE is forecast to expand at an 8.63% CAGR through 2031.

- By bearing type, mobile-bearing systems captured 52.98% revenue share in 2025; hybrid or semi-constrained platforms are projected to grow at an 11.18% CAGR to 2031.

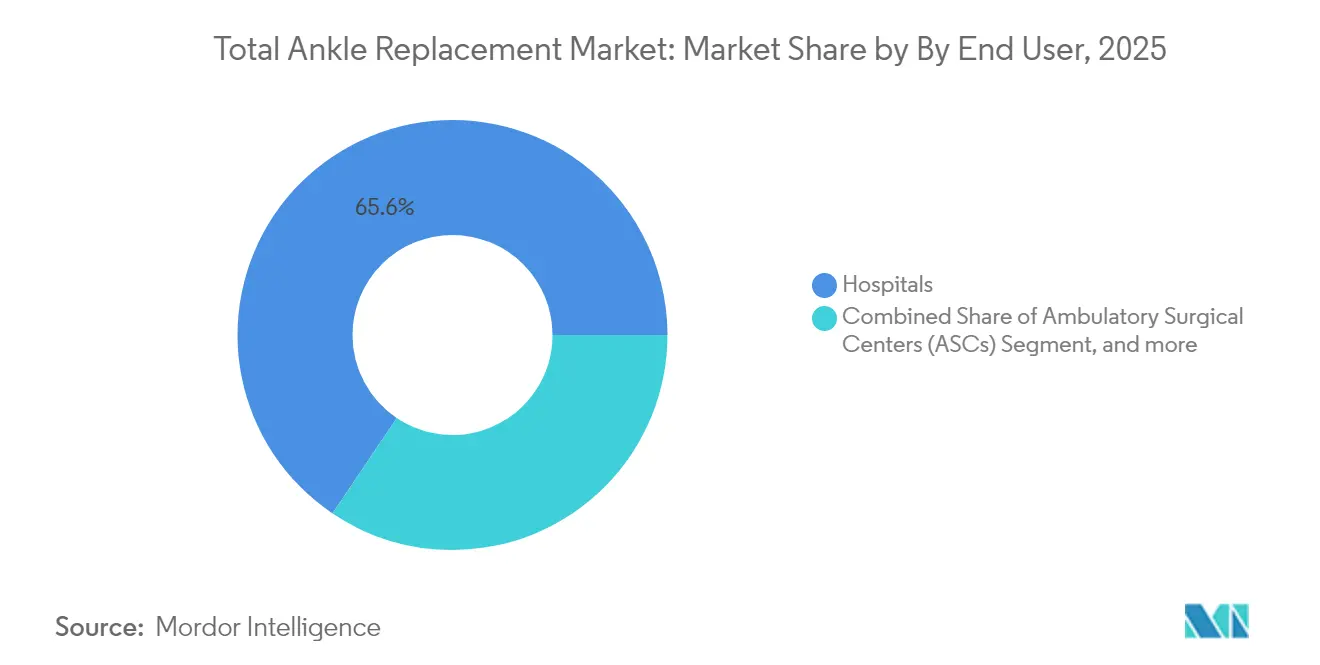

- By end user, hospitals accounted for a 65.58% share of the total ankle replacement market size in 2025, whereas ambulatory surgical centers are advancing at a 9.41% CAGR through 2031.

- By geography, North America led with 42.71% revenue share in 2025, while Asia-Pacific is set to register the fastest 10.35% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Total Ankle Replacement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of ankle osteoarthritis and aging population | +1.8% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Surge in minimally invasive, image-guided, and robotic TAR procedures | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Favourable reimbursement expansion | +0.9% | Primarily North America, selective European markets | Short term (≤ 2 years) |

| Additive-manufactured, patient-specific implants gain FDA clearances | +0.7% | Global, led by United States approvals | Medium term (2-4 years) |

| Growing demand from younger sports-injury cohort | +0.5% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Outpatient TAR adoption in ASC settings | +0.3% | United States mainly | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Ankle Osteoarthritis & Aging Population

The demographic shift toward older, more active adults elevates the incidence of ankle osteoarthritis and fuels the total ankle replacement market. Trauma is the leading etiology, so the disease burden grows as sports participation and road traffic injuries increase. Clinical studies show postoperative return-to-sport rates climbing from 31.1% to 85.4%, confirming that modern implants maintain mobility and independence among seniors.[1]Michal Mor, “Sports Activity After Total Ankle Arthroplasty,” Journal of Clinical Medicine, mdpi.com Multinational health systems, therefore, position total ankle arthroplasty as a quality-of-life intervention rather than a last resort, embedding it into arthritis care pathways and driving long-term demand.

Surge in Minimally-Invasive, Image-Guided & Robotic TAR Procedures

Navigation and robotic platforms translate lessons from knee arthroplasty to the ankle by improving resection accuracy, minimizing soft-tissue disruption, and shortening learning curves. About 13% of United States knee replacements already use robotics, and leading orthopedic centers now deploy similar workflows for ankles.[2]Jonathan Vigdorchik, “Robotic Assistance in Ankle Arthroplasty,” JBJS Open Access, jbjs.org Robotics supports lateral approaches that conserve bone and mitigate subsidence, while intraoperative sensors quantify implant alignment in real time. These advantages widen candidacy to deformity cases previously slated for fusion and enhance the appeal of outpatient protocols, together accelerating the total ankle replacement market.

Favourable Reimbursement Expansion

CMS raised ambulatory surgical center reimbursement by 2.9% for 2025, boosting total ASC payments to USD 7.4 billion and removing financial disincentives for same-day ankle arthroplasty.[3]CMS, “ASC Payment System Final Rule,” cms.gov Cost-effectiveness models calculated an incremental cost-utility ratio of USD 11,800 per QALY versus fusion, comfortably inside payer thresholds. Commercial insurers follow Medicare’s lead, recognizing downstream savings from preserved joint motion and lower adjacent-joint degeneration. Although reimbursement cuts to physician fees continue elsewhere, the broader payment environment remains net positive for procedure growth.

Additive-Manufactured, Patient-Specific Ankle Implants Gain FDA Clearances

Clearances for restor3d, 3D Systems, and MedCAD devices between 2023 and 2025 validate the regulatory pathway for bespoke implants that match individual bone morphology. One multicenter cohort reported 96.3% device survivorship with patient-specific total talus replacements.[4]FDA, “Restor3d Total Talus Clearance,” fda.gov Porous titanium and vitamin E-infused polyethylene lower wear and loosen risk, and pre-navigated cutting guides shorten operative time. As printing costs fall, companies leverage digital libraries for rapid production, giving surgeons on-demand options that strengthen brand loyalty and stimulate replacement cycles across the total ankle replacement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surgical-site complications and revision burden | -1.4% | Global, stronger in emerging markets | Medium term (2-4 years) |

| High device and procedure costs limit adoption in emerging markets | -0.8% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Absence of long-term global implant registry data | -0.6% | Global, more critical for new entrants | Medium term (2-4 years) |

| Joint-preserving alternatives delaying TAR | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surgical-Site Complications & Revision Burden

Long-term datasets reveal 10-year revision rates near 10.9% and 20-year rates at 13.5%, materially higher than hip or knee arthroplasty. Periprosthetic infection risks run from 1% to 14%, and ankle soft-tissue envelopes complicate wound healing. The FDA flagged the Hintermann H3 system in 2024 for failure rates exceeding 16.1%, underscoring vigilance requirements. Surgeons respond by tightening indications, extending preoperative optimization, and limiting bilateral cases, all of which temper procedure volume growth within the total ankle replacement market.

High Device & Procedure Costs Limit Adoption in Emerging Markets

The procedure costs USD 20,200 more than fusion, with implants alone exceeding USD 8,000 in some markets. Emerging payers rarely reimburse premium instrumentation, forcing providers either to shift costs to patients or to default to fusion. Limited fellowship programs, restricted CT imaging, and scarce revision expertise further slow penetration. Manufacturers must therefore develop tiered portfolios and local training academies to unlock latent demand and widen the total ankle replacement market footprint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: INBONE Systems Lead While CADENCE Drives Innovation

INBONE II and INFINITY platforms combined for a 33.12% revenue share in 2025, giving them the most significant stake in the total ankle replacement market. Their modular tibial stems provide customizable fixation ranging from short metaphyseal posts to long intramedullary segments, an approach that improves initial stability in revision and osteoporotic cases. Seven-year survivorship of 95.9% underscores dependable mid-term performance, and global users passed 48,000 implants by 2024. Competitive differentiation centers on integrated patient-specific guides and streamlined instrumentation sets that cut setup time and radiation exposure, advantages prized in ambulatory settings. Parallel clinical programs collect fluoroscopic kinematic data that illustrate near-native sagittal and coronal plane motion, bolstering evidence packages for payer submissions and further fortifying leadership in the total ankle replacement market.

CADENCE rose on an 8.63% CAGR trajectory through 2031, propelled by breakthroughs in polyethylene formulation, talar dome curvature, and streamlined lateral approach instrumentation. Early outcome registries show 98% patient satisfaction at two years, and surgeons report simplified bone resections that trim learning curves for community hospitals. VANTAGE, STAR, and SALTO Talaris retain loyal followings, each leveraging distinct bearing philosophies and regional reimbursement footholds. Paragon 28’s 3D-printed APEX system adds porous trabecular surfaces and vitamin E stabilized liners to resist oxidation and wear. Over the forecast, design innovations will hinge on smart sensor integration and MRT-compatible alloys that let clinicians monitor implant health remotely, fueling repeat procedures and secondary revenue streams for manufacturers.

By Bearing Type: Mobile Systems Dominate as Hybrid Designs Gain Momentum

Mobile-bearing constructs captured 52.98% share in 2025, reflecting surgeon faith in implants that allow polyethylene inserts to self-align under load and reduce edge stresses. Finite-element analyses verify that stress distribution reaches physiologic patterns when cartilage overlay thickness is tuned to 0.5 mm, an insight guiding next-generation mobile bearings. Fixed designs remain valuable for compromised bone stock or ligamentous insufficiency, yet concerns about constrained kinematics limit widespread adoption.

The hybrid segment, blending inherent rotational mobility with built-in stability features, expands at an 11.18% CAGR, highlighting the market’s search for balanced solutions. Companies now pair hybrid talar components with ultracongruent inserts to harmonize contact pressures, attracting surgeons who once vacillated between mobile and fixed platforms. As personalized gait analytics become routine, bearing selection will increasingly derive from preoperative motion datasets, embedding decision support tools deeper into the total ankle replacement market sales process.

By End User: Hospital Dominance Challenged by ASC Growth

Hospitals held 65.58% of the total ankle replacement market size in 2025, leveraging operating-room infrastructure, intensive-care backup, and residency training pipelines. Academic centers drive early adoption of robotics, and bundled-payment pilots anchor risk-sharing contracts. Even so, ambulatory surgical centers advance at a 9.41% CAGR as insurers prefer lower facility fees and patients seek same-day recovery.

Device makers responded with single-tray systems and disposable saws that align with ASC sterility protocols, shaving turnover time by 12 minutes per case. Quality registries show 30-day readmission parity between settings, reinforcing payer confidence. Specialty orthopedic clinics serve as preoperative hubs for imaging, gait analysis, and shared-decision counseling, then hand patients to either hospitals or ASCs for surgery, integrating services across the care continuum and broadening channel access within the total ankle replacement market.

Geography Analysis

North America generated 42.71% of revenue in 2025 and anchors global clinical guideline development, driven by CMS coverage, high surgeon density, and consumer willingness to pay for premium implants. United States physicians perform more than 11,000 ankle replacements annually and frequently combine procedures such as ligament reconstruction to optimize alignment. Canada contributes through publicly funded specialist centers in Ontario and Alberta, whereas Mexico’s private sector captures medical tourists from Central America seeking motion-preserving procedures.

Europe remains the second-largest cluster, with Germany, France, and the United Kingdom leading volumes under stringent CE-mark requirements and cost-utility thresholds. National health systems conduct health-technology assessments that scrutinize long-term revision rates, encouraging manufacturers to publish peer-reviewed survivorship data. Scandinavian countries share registry insights that influence broader European reimbursement negotiations.

Asia-Pacific is the fastest-growing region at a 10.35% CAGR to 2031 as aging populations and rising disposable income heighten demand for advanced orthopedic care. China ramps fellowship programs in Shanghai and Beijing, Japan leverages universal insurance to cover select technologies, and India’s tier-1 hospitals attract domestic medical tourists. The combination of heavy trauma incidence and large diabetes populations increases arthritis burden, creating a fertile expansion corridor for the total ankle replacement market. Middle East and Africa plus South America show nascent uptake as private hospital chains import expertise, though currency fluctuations and out-of-pocket dynamics temper near-term procedure counts.

Competitive Landscape

The total ankle replacement market features moderate consolidation yet intense innovation rivalry. Zimmer Biomet closed the USD 1.1 billion Paragon 28 acquisition in April 2025, gaining the APEX 3D system, Smart 28 instrumentation, and a focused ankle sales force that complements Zimmer’s global network. Stryker sustains leadership through Infinity’s 98.8% two-year survivorship and the 2024 launch of Ankle Truss and Osteotomy Truss adjunct systems that expand revision toolbox breadth. Smith+Nephew reported 5.3% underlying revenue growth in 2024 and released patient-matched guides that integrate CT mapping with intraoperative navigation, simplifying component alignment and boosting surgeon adoption.

Niche players chase white-space by focusing on patient-specific implants, additive manufacturing, and sensorized polyethylene inserts that monitor load and temperature. Restor3d leverages machine-learning design algorithms to optimize lattice structures, whereas 3D Systems targets orthoplastic trauma surgeons with an end-to-end digital workflow. Competitive dynamics now extend beyond hardware to software ecosystems, remote monitoring platforms, and value-based contracting models that tie payments to long-term functional scores. Regulatory scrutiny intensifies after the FDA’s 2024 safety communication, prompting firms to invest heavily in post-market surveillance and real-world data generation. As a result, top manufacturers bundle cloud registries and longitudinal outcome analytics with implant sales, raising switching costs and shaping purchase decisions across the total ankle replacement market.

Total Ankle Replacement Industry Leaders

Zimmer Biomet

Exactech, Inc.

Enovis

Smith + Nephew

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Zimmer Biomet completed its acquisition of Paragon 28 for USD 1.1 billion, creating a dedicated sales channel for foot and ankle solutions and positioning the company to access the rapidly growing ambulatory surgery center market. The acquisition integrates Paragon 28's innovative APEX 3D Total Ankle Replacement System and Smart 28 surgical tools with Zimmer Biomet's global distribution network and manufacturing capabilities.

- March 2025: MedCAD secured FDA 510(k) clearance for its AccuStride foot and ankle system, marking a significant advancement in patient-specific instrumentation for total ankle replacement procedures. The clearance enables market entry for the device that meets FDA safety and effectiveness standards for surgical precision enhancement.

- October 2024: Exactech successfully performed its inaugural total ankle replacement surgery utilizing the Vantage Ankle 3D and 3D+ tibial implants. These 3D-printed ankle implants, akin to all 3D-printed orthopedic solutions, offer the advantage of customization, streamlining the surgical process for physicians.

- August 2024: Enovis Corporation introduced its Scandinavian Total Ankle Replacement (STAR Ankle), now enhanced with the new e+ Polyethylene. The implant's vitamin E-infused e+ Polyethylene insert promises heightened durability, stability, and longevity. Coupled with the recent launch of STAR Patient Specific Instrumentation (PSI), the STAR+ Experience underscores Enovis' dedication to ongoing enhancements, prioritizing patient satisfaction and outcomes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the total ankle replacement market as the global revenue generated from new, fully integrated prosthetic systems that replace the entire talocrural joint for patients with end-stage arthritis or traumatic damage. The definition covers primary tibial and talar components plus the single-use instruments supplied to hospitals and ambulatory surgical centers.

For clarity, we exclude revision implants, partial ankle arthroplasty, fusion hardware, and aftermarket service kits.

Segmentation Overview

- By Design

- HINTEGRA

- STAR

- SALTO / SALTO Talaris

- INBONE II / INFINITY

- CADENCE

- Other Designs

- By Bearing Type

- Mobile-Bearing Systems

- Fixed-Bearing Systems

- Hybrid / Semi-constrained

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Orthopaedic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate secondary signals, Mordor analysts interviewed foot-and-ankle surgeons, specialty distributors, and reimbursement advisors across North America, Western Europe, China, India, and the GCC. These conversations refined conversion rates from fusion to replacement, confirmed ASP bands by care setting, and stress tested growth assumptions.

Desk Research

During desk work, we gathered baseline procedure volumes, demographic shifts, and reimbursement rules from open sources such as the National Center for Health Statistics, CMS Medicare claims, Eurostat discharges, the Australian Orthopaedic Association Joint Registry, and American Orthopaedic Foot & Ankle Society abstracts.

Company 10-Ks, Questel patent analytics, tender notices from Tenders Info, and clinical trial registries then highlighted pipeline flow, while D&B Hoovers ranges helped us anchor typical average selling prices. This list is illustrative, and we relied on many additional public and paid references for data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model begins with symptomatic ankle arthritis prevalence by country, multiplies by surgery eligibility and uptake, and applies verified ASP ranges, which we then cross check against sampled customs shipment data. Select bottom-up approximations, such as supplier roll-ups for high-volume hospitals, help refine totals.

Key variables feeding the model include aging population growth, obesity incidence, surgeon density, reimbursement expansion, and implant price trends. Forecasts rely on multivariate regression blended with ARIMA smoothing when regulatory or technology inflection points arise. Gaps from incomplete shipment disclosure are bridged through triangulation with registry counts and survey confirmed utilization multipliers.

Data Validation & Update Cycle

Before sign-off, two independent analysts run anomaly checks, compare outputs with orthopedic import statistics, and convene a review panel. Reports refresh annually, with interim updates triggered by recalls, guideline shifts, or payment changes so our clients receive the latest view.

Why Our Total Ankle Replacement Baseline Earns Trust

Published market values often differ because variations in device mix, care setting coverage, currency conversion points, and refresh cadence influence totals.

We outline the main gap drivers below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.28 B (2025) | Mordor Intelligence | - |

| USD 0.75 B (2024) | Global Consultancy A | Instrument sets excluded; conservative price deck |

| USD 0.71 B (2023) | Regional Consultancy B | Historical charges used; sub-global scope |

| USD 1.12 B (2024) | Trade Journal C | Fusion devices included alongside replacements |

The comparison shows that when scope alignment, ASP calibration, and timely refresh are applied together, Mordor's balanced approach delivers a dependable baseline that decision makers can trace to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the total ankle replacement market?

The total ankle replacement market is valued at USD 1.36 billion in 2026 and is expected to reach USD 1.82 billion by 2031.

How fast is the total ankle replacement market growing?

The market grows at a 6.07% CAGR during the 2026-2031 forecast period.

Which design platform leads the total ankle replacement market share today?

INBONE II/INFINITY holds 33.12% of global revenue in 2025, making it the leading design family.

Why are ambulatory surgical centers important for future growth?

ASC settings support same-day discharge, reduce facility costs, and benefit from CMS reimbursement increases, driving a 9.41% CAGR among ASCs through 2031.

Which region will expand the fastest by 2031?

Asia-Pacific is forecast to grow at a 10.35% CAGR, propelled by aging populations, higher healthcare spending, and expanding access to specialist orthopedic care.

What technology trends shape competition in the total ankle replacement industry?

Patient-specific 3D-printed implants, robotic guidance, and sensorized liners are the core technologies differentiating products and influencing purchasing decisions.

Page last updated on: