Tobacco Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.33 Billion |

| Market Size (2031) | USD 22.76 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

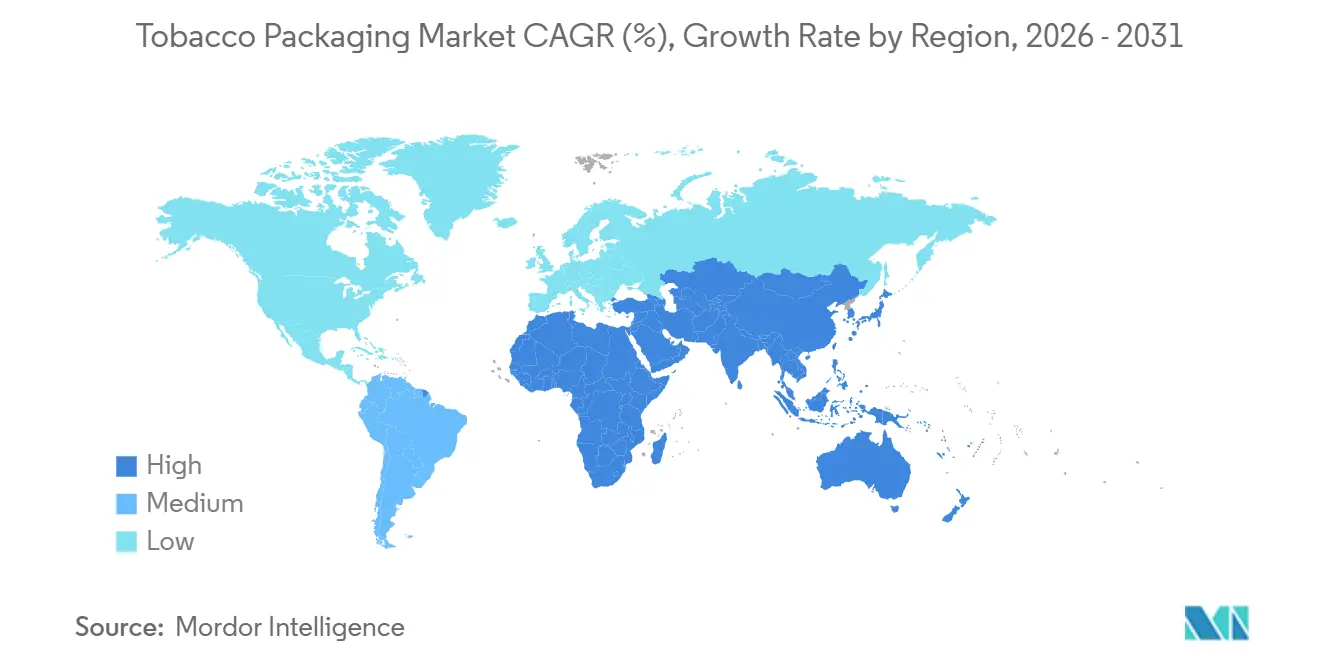

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

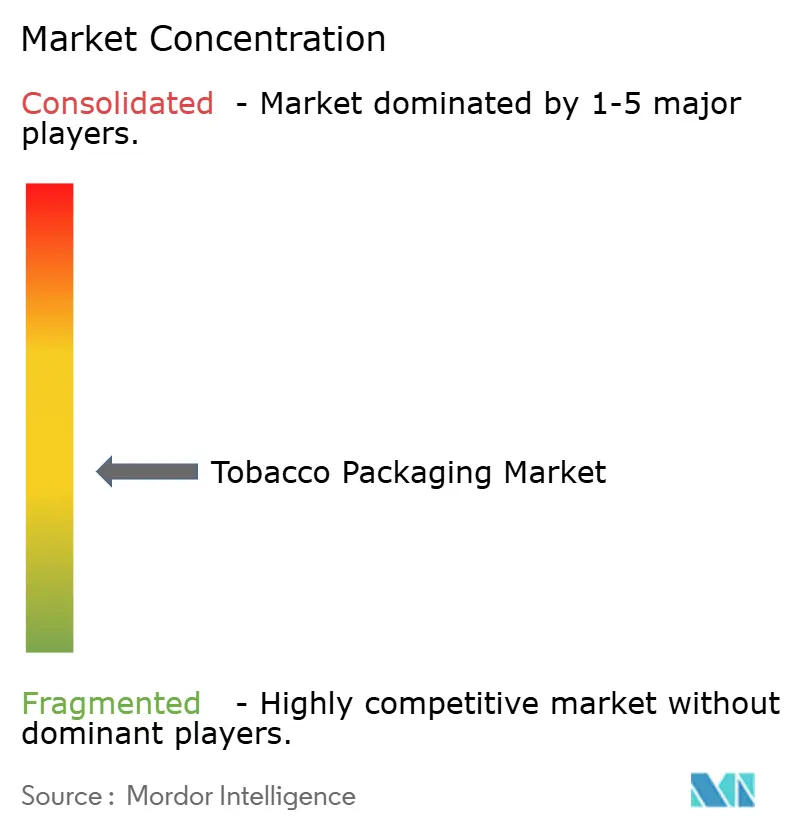

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tobacco Packaging Market Analysis by Mordor Intelligence

The tobacco packaging market size was valued at USD 18.71 billion in 2025 and estimated to grow from USD 19.33 billion in 2026 to reach USD 22.76 billion by 2031, at a CAGR of 3.32% during the forecast period (2026-2031). Growth is being reshaped by the roll-out of plain‐packaging laws that strip branding from outer cartons, compelling converters to differentiate through anti-counterfeit features, sustainable substrates, and fully automated production lines. Paper and paperboard continue to dominate because they align with extended producer responsibility fees and perform reliably on high-speed machinery, yet bioplastics and compostables are the fastest-growing materials as European Single Use Plastics rules tighten. Asia-Pacific remains the demand anchor on account of China’s multi-trillion-stick output and India’s mandatory serialization scheme, while the Middle East is emerging as the quickest regional opportunity thanks to new graphic-warning rules that require thicker boards and UV-stable inks. Competitive dynamics are shifting as British American Tobacco and Philip Morris International backward-integrate into pack assembly, pressuring independent converters to scale up or specialize.

Key Report Takeaways

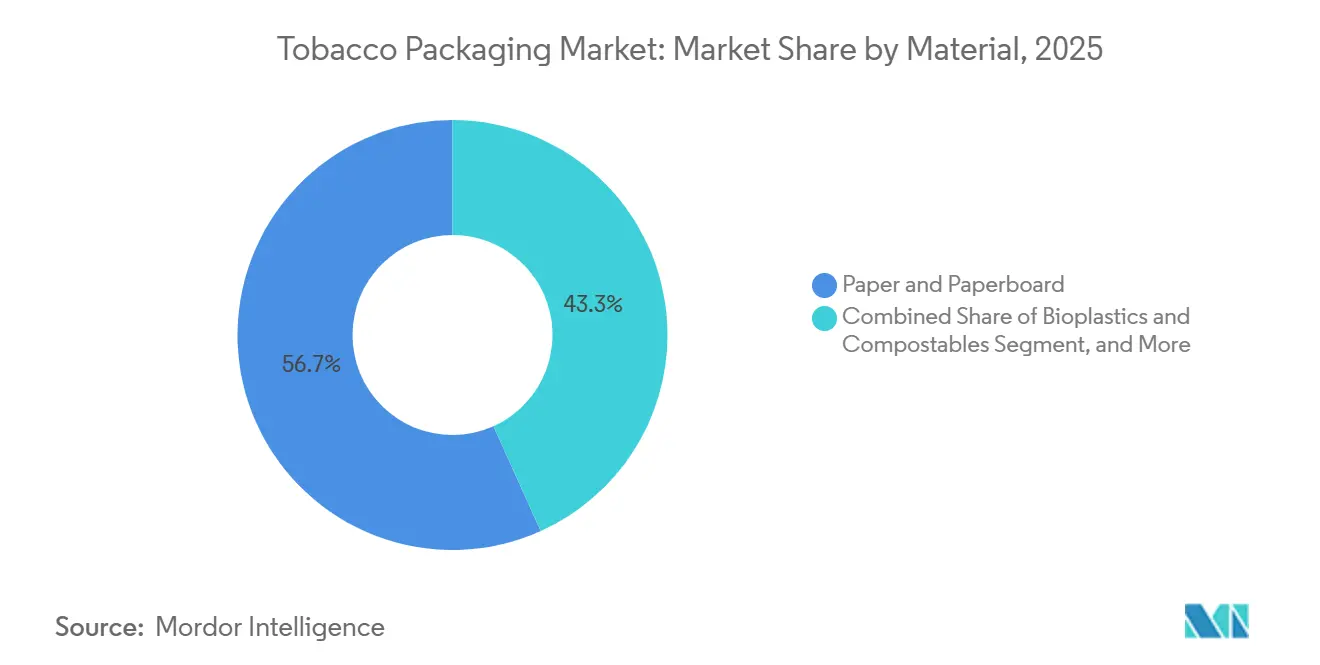

- By material, paper and paperboard led with 56.73% of the tobacco packaging market share in 2025, whereas bioplastics and compostables are projected to advance at a 4.33% CAGR through 2031.

- By packaging type, primary packs accounted for 48.26% of the tobacco packaging market in 2025, while high-end luxury rigid boxes are expected to expand at a 4.19% CAGR through 2031.

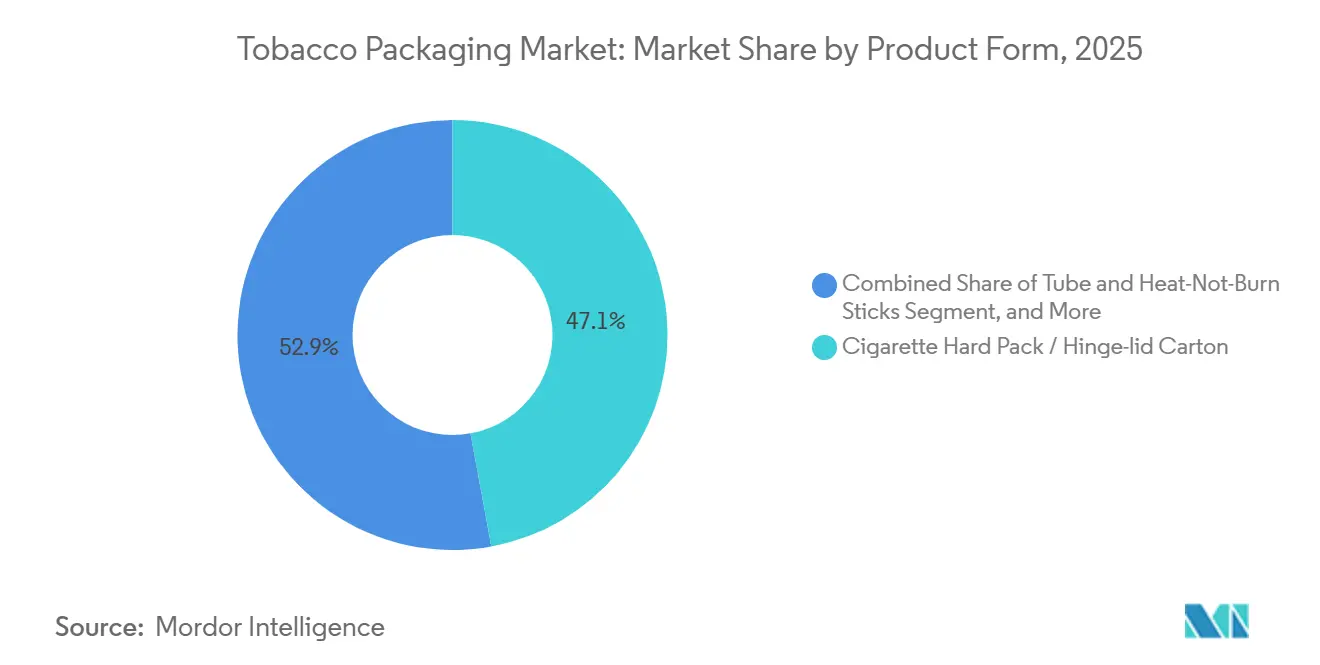

- By product form, cigarette hard packs and hinge-lid cartons captured 47.12% of the tobacco packaging market share in 2025, yet tube formats for heat-not-burn sticks are forecast to grow at a 4.16% CAGR between 2026-2031.

- By tobacco type, smoking tobacco dominated with a 63.44% share of the tobacco packaging market size in 2025, and next-generation products are set to climb at a 4.11% CAGR to 2031.

- By geography, Asia-Pacific accounted for 46.79% of revenue in 2025, while the Middle East is the fastest-growing region, advancing at a 4.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Tobacco Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Plain-Pack Mandates and Graphic Warnings | +0.9% | Europe, Australia, Canada, Middle East, South America | Medium term (2-4 years) |

| Paperboard Shift for Sustainability and Cost | +0.7% | Europe and North America lead, Asia-Pacific catching up | Long term (≥ 4 years) |

| Unit-Level Anti-Counterfeit Tech Adoption | +0.6% | Europe, India, Brazil, Turkey, Middle East, Africa | Medium term (2-4 years) |

| Automation-Ready Pack Formats for HTP and E-cig | +0.5% | Japan, South Korea, Europe, North America | Short term (≤ 2 years) |

| Cultural-Event Limited-Edition Packs | +0.3% | United States, China, Middle East | Short term (≤ 2 years) |

| Eco-Modular Pack Lines for SKU Agility | +0.4% | Global, early in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Plain-Pack Mandates and Graphic Warnings

Plain-pack laws in 28 nations now force 65% to 90% surface coverage with health images, erasing embossing and foil that once justified premium pricing.[1]European Commission, “Tobacco Products Directive Revision,” ec.europa.eu Saudi Arabia and the United Arab Emirates introduced 75% graphics in 2025, which pushed converters to adopt UV-resistant inks and thicker paperboard, adding 8% to substrate costs. With visual branding removed, tobacco firms redirect budgets toward point-of-sale displays and digital platforms, but demand for covert security tags rises because standardized packs are easier to counterfeit. The legislation, therefore, simultaneously commoditizes appearance and amplifies traceability requirements, rewarding suppliers that integrate track-and-trace within plain designs. Converters unable to pivot to compliance-driven features risk margin erosion as contracts shift to technically advanced rivals.

Paperboard Shift for Sustainability and Cost

Paper and paperboard held a 56.73% share in 2025, thanks to fee structures under European extended producer responsibility schemes that penalize unrecyclable plastic. Smurfit WestRock’s 2024 merger unlocked 500,000 tonnes of dedicated folding-carton capacity, cutting per-unit costs by up to 9%.[2]Smurfit Kappa and Westrock, “Merger Investor Presentation,” smurfitkappa.com Mondi followed up in 2025 with a water-based barrier that removed polyethylene lamination and reduced material weight by 18%. While Asia-Pacific still uses metallized films for humidity control, export-oriented plants in Vietnam and Indonesia have shifted to coated paperboard to keep access to the European Union market. Over the long term, converters that master PFAS-free coatings and achieve recyclability at scale will capture price premiums even as overall substrate costs fall.

Unit-Level Anti-Counterfeit Tech Adoption

The European Union Tobacco Products Directive established unique codes on every pack from 2024 forward, a framework that India, Brazil, and Turkey replicated, covering 1.8 trillion cigarettes annually. India’s Central Board of Indirect Taxes and Customs mandated QR serialization in 2025, forcing manufacturers to retrofit 47 lines with vision systems.[3]Central Board of Indirect Taxes and Customs, “Tobacco QR Serialization,” cbic.gov.in Serialization adds USD 0.015-0.025 per pack but creates a moat for vendors such as Authentix and SICPA that supply patented taggants. Smaller converters unable to license secure technology are locked out of high-compliance markets, provoking a bifurcation in global supply: sophisticated lines for regulated regions and low-cost lithography for markets where enforcement remains weak. The traceability trend, therefore, elevates technical capability above print aesthetics as the new source of competitive advantage.

Automation-Ready Pack Formats for HTP and E-cig

Heat-not-burn and pouch categories require tighter tolerances than combustible cigarettes, demanding servo cartoners and ultrasonic sealing lines that cost USD 2-4 million each but lift throughput to 650 packs per minute. Philip Morris International’s IQOS ILUMA tubes integrate RFID chips for device pairing, compelling converters to add injection-molding stations and electronics testing. Japan Tobacco International’s Ploom X Advanced uses a magnetic slide box assembled in 14 steps, illustrating how next-gen products shift value toward assembly complexity. Converters that invested in robotic pick-and-place and vision alignment, including Sonoco and Huhtamaki, reported double-digit order growth in 2025. Those reliant on legacy folder-gluers are losing share as tobacco firms award contracts to partners who can deliver device-level tolerances.

Restraints Impact Analysis of Tobacco Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Excise Taxes Shrink Consumption | -0.8% | United Kingdom, Australia, Canada, France, South Africa, Philippines | Short term (≤ 2 years) |

| Global Plain-Pack Roll-Out Erodes Branding ROI | -0.6% | Europe, Australia, Canada, New Zealand, Thailand, Saudi Arabia, UAE | Medium term (2-4 years) |

| PFAS and Plastics Bans Tightening | -0.4% | European Union, United States, Canada | Long term (≥ 4 years) |

| Illicit Single-Stick Sales Bypass Legal Packs | -0.5% | Sub-Saharan Africa, Southeast Asia, South America, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Excise Taxes Shrink Consumption

The United Kingdom raised duties by 10% in 2025, driving a 5.2% decline in legal cigarette sales. Australia’s indexation pushed the excise component of a pack above AUD 30 (USD 20) the same year, accelerating the switch to roll-your-own pouches. Canada followed with CAD 4-per-carton hikes plus provincial surcharges, contracting volumes by 4.8%. As smokers downtrade or shift to illicit markets, converters face lower run lengths and rising unit costs, eroding margins in plants designed for billion-stick scale. Many are diversifying into cannabis or pharmaceutical folding cartons to cushion utilization swings.

Global Plain-Pack Roll-Out Erodes Branding ROI

Thailand, Saudi Arabia, and 26 other jurisdictions mandated drab-brown packs with uniform fonts by end-2025, collapsing the spread between standard and luxury substrates from USD 0.12 to 0.03 per pack. Thailand Tobacco Monopoly cut the number of substrate SKUs from 47 to 3 as a result. Brand owners now route marketing spend to retail signage or augmented reality, reducing the strategic importance of print embellishment. Converters that once sold holographic foils and embossed varnish at premium margins must now compete on price and delivery reliability, accelerating consolidation among mid-tier suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tobacco Packaging Market Segment Analysis

By Material:

Paperboard Strength With Bioplastic MomentumPaper and paperboard accounted for 56.73% of 2025 revenue, making them the single largest slice of the tobacco packaging market. Converters favor these substrates because they glide through folding-carton lines at 800 packs per minute and qualify for curbside recycling programs that help brand owners avoid extended producer responsibility penalties. Metals and traditional plastics still play niche roles as moisture barriers, yet their combined share remained below one-third due to cost and regulatory headwinds that continue to build. Bioplastics and compostables, although small today, are rising at a 4.33% CAGR as evolving import standards in Europe incentivize tobacco groups to shift from BOPP films toward polylactic acid sleeves and cellulose trays.

Profit pools are therefore shifting from commodity paperboard toward coated grades that deliver PFAS-free, high-gloss, or oxygen-barrier performance without losing recyclability. Suppliers that master water-based coatings or fiber-based laminates can secure premium contracts even when plain-pack rules suppress decorative print. In humid Asian climates, metallized film retains an edge for pouch overwraps, but fee structures in France and Germany are narrowing its price advantage. By the end of the forecast window, leading converters are expected to offer a dual product line, with high-volume recycled paperboard for cigarettes and specialized bioplastic tubes for heated tobacco sticks, positioning themselves for both compliance and margin protection.

By Packaging Type:

Primary Packs Steady, Rigid Boxes AscendantPrimary packs accounted for 48.26% of spending in 2025, led by hinge-lid cartons and soft packs with tamper-evident seals and child-resistant closures. Cost, speed, and regulatory conformity keep the format resilient even as global cigarette volumes contract. Secondary sleeves and transit shippers have moved toward single-color print to meet plain-pack mandates, compressing their unit value and pushing converters to drive savings through faster make-readies and digital workflows. Luxury rigid boxes, though accounting for only 6% of revenue, are growing at 4.19% and punching above their weight in profitability; cigar and limited-edition cigarette launches use magnetic closures, wood veneers, or laser etching to justify per-unit prices 20-plus times higher than those of a standard folding carton.

The bifurcation in demand compels converters to partition their asset base. High-speed folder-gluers and automated pick-and-place modules keep primary pack costs down at billion-stick scale, while short-run hand-assembly cells cater to premium lines that require tactile finishes. Modular equipment that swaps from cartons to rigid boxes in under an hour is becoming a critical differentiator as tobacco companies trim SKU counts yet still pursue seasonal tie-ins. Providers who can guarantee both mass throughput and bespoke craftsmanship occupy the most defensible competitive tier.

By Product Form:

Hard Packs Hold Scale, Tubes Rapidly ExpandCigarette hard packs and hinge-lid cartons accounted for 47.12% of 2025 revenue, cementing their place as the workhorse formats in the tobacco packaging market. Structural integrity, familiarity to consumers, and compatibility with packer speeds approaching 800 units per minute keep them indispensable in regions like Europe and North America. Soft packs stay relevant in price-sensitive areas but lose share where large pictorial warnings crease the foil laminate. Tube and heat-not-burn stick formats, which today account for only 6% of revenue, show a 4.16% CAGR through 2031, propelled by device ecosystems such as IQOS and Ploom that mandate precision-molded polypropylene or hybrid paper-plastic sleeves.

These tubes embed RFID chips, induction heaters, or moisture-control liners, lifting packaging costs per thousand by double-digit percentages while unlocking new consumer experiences and data-tracking capabilities. The shift pushes converters to add injection molding, ultrasonic sealing, and automated test stations, traditionally found in electronics plants. Firms that already operate multi-process campuses can cross-train staff and amortize tooling, gaining a time-to-market edge. As heated and oral products edge toward one-fifth of nicotine consumption in developed markets, mastery of tube assembly will move from nice-to-have to table stakes.

By Tobacco Type:

Smoking Dominant While Reduced-Risk Gains PaceSmoking Tobacco retained 63.44% of spending in 2025, preserving the lion’s share of the tobacco packaging market size despite regulatory headwinds. Cigarette sales remain in the trillions of annual sticks, ensuring steady, if low-growth, demand for hard and soft packs. Yet next-generation products, which package heated sticks, nicotine pouches, and e-cigarette pods, are expanding at a 4.11% CAGR and grabbing investment dollars as excise regimes remain more favorable. Packaging complexity jumps markedly in this arena: blister cards must pass child-resistance tests, pouch cans require tamper-evident seals, and heated-stick tubes integrate electronics authentication.

Smokeless and chewing formats keep a loyal base in India and parts of the United States, but tax hikes on gutkha pouches are nudging converters to seek higher-margin volumes elsewhere. Cigar and cigarillo packs, at roughly 14% of revenue, remain insulated from commoditization because cedar linings, humidity packs, and lacquered finishes deliver durable price premiums. Over the forecast horizon, converters that field a balanced portfolio spanning commodity cigarette cartons and feature-rich next-generation formats will secure the broadest customer roster and the greatest resilience to policy swings.

Geography Analysis

APAC Tobacco Packaging Market

Asia-Pacific accounted for 46.79% of 2025 revenue, confirming its position as the largest regional share of the tobacco packaging market. China’s 2.4 trillion-stick output and India’s 1.1 trillion-unit production underpin this scale advantage, while relatively slow adoption of plain-pack rules keeps design complexity and per-pack value higher than in Europe. India’s 2025 serialization mandate pushed converters to install vision inspection on more than 40 lines, nudging average conversion cost per thousand packs up by 6%. In parallel, Vietnam and Indonesia adopted coated paperboard grades to meet the requirements of European import buyers, signaling that external regulation is shaping substrate choice even in non-regulated jurisdictions. Regional specialists, therefore, balance low-cost carton runs for domestic brands with higher-spec contracts for export-oriented manufacturers.

Europe and North America Tobacco Packaging Market

Europe accounted for 26% of 2025 turnover, even though cigarette volumes contracted by about 4% under a mix of excise hikes and flavor bans. The region’s revenue resilience stems from PFAS restrictions and extended producer responsibility fees that reward converters who can deliver recyclable, barrier-coated paperboard. Mondi and Smurfit Westrock lead on this front, leveraging patented water-based coatings that pass recyclability tests without compromising moisture protection. North America held an 18% share; U.S. cigarette demand fell, yet nicotine-pouch packaging jumped 19%, lifting unit value as blister cards and molded cans require child-resistant features. Converters with both carton and rigid-plastic capacity are capturing this dual-track growth.

MEA and South America Tobacco Packaging Market

The Middle East and Africa collectively accounted for 10% of 2025 sales, but the region posted the fastest growth rate at 4.39% CAGR. Gulf Cooperation Council states now enforce 75% pictorial warnings, prompting a switch to thicker boards and UV-stable inks that raise per-pack substrate cost by up to 12%. Conversely, illicit single-stick trade in sub-Saharan corridors strips 12% to 18% of addressable demand, limiting volume despite rising population. South America closed 2025 with a 6% share; Brazil’s July 2024 track-and-trace law forced 89 lines to install serialization hardware, consolidating capacity among top domestic players and opening space for European converters to export compliant cartons. Geography, therefore, shapes strategy: suppliers must blend high-volume, cost-driven operations in Asia with compliance-led premium niches in Europe, North America, and the Gulf to smooth earnings across regulatory cycles.

Regulatory Landscape

Tobacco packaging regulation continues to converge on plain-pack presentation and larger, rotated health warnings under the WHO Framework Convention on Tobacco Control (WHO FCTC) Article 11, which sets a minimum expectation of at least 30% warning coverage (and recommends 50% or more). Australia remains among the most stringent, requiring health warning images covering at least 75% of the front and 90% of the back of cigarette packs and cartons. In the US, the FDA finalized new cigarette health warnings covering 50% of the front and back of packs, with enforcement timelines extending into late 2025 to early 2026.

Canada is adding packaging-structure complexity through the Tobacco Products Appearance, Packaging and Labelling Regulations (TPAPLR). By July 31, 2026, manufacturers must sell and distribute cigarette packages that include a health information message on an extended upper slide-flap to retailers and distributors. By October 31, 2026, retailers must sell compliant packages to consumers, and Canada also requires vertical-orientation cartons to carry health warnings on the four largest exterior surfaces from July 2026. In Europe, standardized packaging is expanding to adjacent categories, including Belgiums plain packaging requirement for cigarette papers effective June 1, 2026, which increases the compliance burden beyond conventional cigarette cartons and influences inks, finishes, and inventory changeovers across suppliers.

Value Chain Analysis

The tobacco packaging value chain runs from upstream fiber and polymer producers through paperboard mills, film and foil suppliers, ink, adhesive and coating formulators, and security material providers (tax stamps, taggants, holograms), into converting and pack-assembly operations covering folding cartons, overwrap, labels, rigid boxes, tubes, and molded components. Specialized prepress and tooling partners support regulated print quality and security features, for example Saueressig Group supplying gravure cylinders and embossing rollers used for tobacco branding and covert or overt authentication. Downstream, tobacco manufacturers and contract packers integrate packaging with high-speed machinery, then route product via wholesalers and regulated retail, where pack format, labeling, and track-and-trace compliance drive SKU management and distribution practices.

Regulation and product mix are reshaping where value accumulates in this chain. Plain-pack mandates reduce the value of decorative finishes while raising demand for compliant warning layouts, durable inks, and precision converting that can hold tolerances at high packer speeds. Serialization and traceability requirements such as unique codes and security features shift purchasing toward approved technology stacks and verified suppliers, which raises barriers for smaller converters without the relevant licensing or integration capability. At the same time, tobacco companies supplier programs focused on upstream sustainability, including Philip Morris Internationals Sustainability Accelerator in 2025 and British American Tobaccos deforestation-free pulp and paper supply-chain goal by 2025, increase auditing, material specifications, and documentation requirements for paper and paperboard inputs, affecting sourcing, qualification cycles, and cost-to-serve for packaging converters.

Competitive Landscape

The tobacco packaging market is moderately concentrated, with the top five converters accounting for roughly 38% of global capacity in 2025. Amcor, Smurfit Kappa, WestRock, Mondi, and International Paper, along with Innovia Films, are investing heavily in automation and PFAS-free coatings, positioning themselves to win long-term supply deals with multinational tobacco companies. Yet regional specialists in China, India, and Indonesia undercut global rivals on landed cost by up to 22% through labor arbitrage and proximity to leaf-processing hubs, keeping price pressure intense on commodity cigarette cartons.

Strategic bifurcation is widening. In the mass-market segment, success hinges on billion-stick scale, high-speed folder-gluers, and digital micro-runs that can toggle among 200 SKUs per shift without tooling downtime. Conversely, next-generation products demand precision molding, RFID embedding, and ultrasonic sealing, capabilities that carry 25% to 40% price premiums and higher EBITDA margins. Sonoco, Huhtamaki, and Shenzhen Jinjia have captured share here by coupling injection molding with vision inspection that verifies electronic integration at 1,200 packs per minute.

Brand owners' backward integration is accelerating consolidation pressure. British American Tobacco bought a 35% stake in a Romanian folding-carton plant in 2024, while Philip Morris International opened a dedicated tube-molding facility in Poland in 2025. These moves secure captive capacity and tighten the market for independent converters. In response, mid-tier players are merging to gain purchasing power and R&D scale, or pivoting into luxury rigid boxes where gross margins exceed 30%. The competitive chessboard is therefore fluid, favoring suppliers that offer both cost-optimized cigarette cartons and high-spec solutions for reduced-risk products.

Tobacco Packaging Industry Leaders

Amcor plc

Smurfit Westrock plc

International Paper Company

Mondi Group

Innovia Films Ltd.

- *Disclaimer: Major Players sorted in no particular order

Tobacco Packaging Market Companies Covered in this Report

- Amcor plc

- Smurfit Westrock plc

- International Paper Company

- Mondi Group

- Innovia Films Ltd.

- Philip Morris International Inc.

- Sonoco Products Company

- Siegwerk Druckfarben AG & Co. KGaA

- Japan Tobacco International

- Treofan Film International

- Stora Enso Oyj

- ITC Limited

- British American Tobacco plc

- Shenzhen Jinjia Group Co. Ltd.

- Huhtamaki Oyj

- Uflex Ltd.

- DS Smith plc

- Jindal Poly Films Ltd.

- Oji Holdings Corp.

- SCHUR Flexibles Holding

Market Opportunities and Future Outlook

Compliance-driven pack redesign and traceability remain a primary whitespace for converters and component suppliers that can industrialize frequent artwork rotations, warning-panel changes, and new pack structures without interrupting throughput. A near-term example is Canadas TPAPLR transition, which requires manufacturers to distribute cigarette packages with health information messages on extended upper slide-flaps by July 31, 2026, and retailers to sell compliant packages to consumers by October 31, 2026. This timeline creates demand for new carton and inner-pack layouts, additional print real estate, and tighter change-control over inventories. The UK Tobacco and Vapes Act 2026 also expands regulatory levers by empowering the Secretary of State to set requirements around packaging materials, texture, size, and opening mechanisms, reinforcing the commercial value of modular tooling, fast changeovers, and proven compliance systems.

Sustainability-led material substitution is opening parallel opportunities in smokeless and next-generation formats where plastic reduction is being industrialized. In April 2026, Future Materials Sweden ordered two Scala machines from PulPac to initiate industrial-scale production of fiber-based snus cans at a new facility in Ljungby, following development work announced with PulPac and partners to replace traditional plastic cans with dry molded fiber. Premium and specialty tobacco packaging is also adopting cross-category structures to protect unit economics under standardized branding, including pharmaceutical-style blister concepts introduced in March 2026 for premium longfiller cigars that shift value toward barrier performance, sealing integrity, and pack-protection engineering rather than external graphics.

Recent Industry Developments in Tobacco Packaging Market

- February 2026: Smurfit Westrock announced a EUR 600 million investment in its French operations, planned over three to five years, to modernize facilities including the Epernay and Vernon plants. The program supports efficiency upgrades and sustainability-linked improvements that can strengthen the companys competitiveness in regulated folding-carton and specialty paperboard applications used by tobacco customers.

- April 2025: Amcor completed its combination with Berry Global, creating a larger packaging platform with integration plans that include USD 650 million in identified synergies by fiscal 2028. The expanded footprint and purchasing leverage can influence pricing and capacity availability across materials used in tobacco packaging, from films and laminates to specialized barrier solutions.

- May 2024: Smurfit Westrock Security Concepts was contracted to supply traceability codes and security features (tax stamps) for tobacco products in Ireland under EU Tobacco Products Directive compliance requirements. The award highlights the shift of value toward regulated identifiers and authentication capabilities that sit alongside cartons and overwrap in the tobacco packaging ecosystem.

Tobacco Packaging Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the value of packaging used to contain, protect, and sell tobacco products, counted across primary, secondary, and bulk or transit formats. It includes the main materials and pack formats used for cigarettes, smokeless tobacco, cigars, and next-generation products.

Scope exclusions: Packaging machinery, standalone printing services not tied to pack supply, and logistics services are not counted in this market value.

Segments Covered in This Report

- By Material

- Paper and Paperboard

- Plastics

- Metals

- Glass and Ceramics

- Bioplastics and Compostables

- By Packaging Type

- Primary

- Secondary

- Bulk / Transit

- High-End Luxury Rigid Boxes

- By Product Form

- Cigarette Soft Pack

- Cigarette Hard Pack / Hinge-lid Carton

- Pouch and Sachet

- Tube and Heat-Not-Burn Sticks

- By Tobacco Type

- Smoking Tobacco

- Smokeless Tobacco

- Next-Generation Products

- Cigars and Cigarillos

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context for tobacco products and the packaging rules that shape pack formats. We refer to public sources such as the World Health Organization (WHO) tobacco control materials, World Bank macro indicators, UN Comtrade trade statistics for packaging inputs, and United Nations population and income series to understand consumption direction by region.

Next, we use a mix of company annual reports, investor presentations, and press releases to map packaging materials, pack format shifts, and capacity or footprint changes. Patent databases are checked to see where innovation is moving (for example, barrier films, anti-counterfeit features, and special inks). We also use customs or shipment-level import-export databases to validate material flows in high-trade corridors. These desk sources are not exhaustive, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were completed with packaging converters, material suppliers, brand-side procurement, and channel participants who track pack demand and pricing. The respondent input was used to confirm what is counted as tobacco packaging in each region, and then to test assumptions including pack mix, material substitution, and typical price movements by format.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 16% | Managers: 54% | Americas: 22% |

Market-Sizing & Forecasting

Sizing uses a top-down and bottom-up logic, where the main build begins from a demand pool view and is then checked using supplier and channel signals. The top-down side links tobacco product output and consumption direction to packaging intensity, which is converted into value using format-wise price assumptions.

Key inputs typically include cigarette versus alternative format mix, the split between soft packs and hinge-lid cartons, the share of pouches and sachets in smokeless formats, material mix shifts between paperboard and plastics, and regulatory packaging requirements that can change board thickness, ink use, and feature adoption. When gaps appear by country, the model is filled using proxy indicators such as trade flows of packaging materials and regional averages, which are validated in interviews.

For forecasting, we rely on scenario analysis supported by expert views, since regulation and illicit trade controls can shift mix faster than long-run trends. Growth is then carried forward with calibrated assumptions on pack demand, price progression, and the pace of feature upgrades (like track and trace or anti-counterfeit elements). Totals are adjusted when bottom-up checks suggest an out-of-line result.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals, such as tobacco consumption direction, material trade trends, and announced packaging upgrades, and then checking for outliers by region and product form. When a number appears off, we re-check assumptions behind pack mix, price timing, and currency conversion before the estimate is finalized.

Each report goes through multi-step internal reviews, where calculations, definitions, and key inputs are inspected and reconciled. The work is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes or sharp raw material price moves. Before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Tobacco Packaging Market Sizing Compared With Other Published Estimates

Published market values for tobacco packaging can differ across sources, even when they cover the same industry in broad terms. The spread usually comes from timing choices, which packaging formats are counted, and how average selling prices are rolled forward year by year.

In a refresh-led read, the divergence often traces back to when currency conversion is locked, whether pricing uses spot material swings or smoother pass-through assumptions, and how cross-checks are done against pack mix changes such as soft pack versus hinge-lid cartons and the rise of pouches and next-generation formats. In this study, the latest annual refresh and consistent currency timing used for ASP roll-forward and variance checks are key reasons the 2026 value differs, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.33 B (2026) | |

| Global Consultancy A | USD 20.85 B (2024) | Uses an earlier base year and can capture a different pack mix snapshot, so later-year price progression and currency timing are not directly aligned with a 2026 build. |

| Market Publisher B | USD 21.06 B (2025) | Anchors the estimate in 2025 and may apply smoother price growth across formats, which can lift totals if pack feature upgrades and material substitution are not re-validated each refresh. |

The table shows that year selection alone can shift the headline number, and that pricing mechanics matter when pack formats and materials are changing. By keeping scope boundaries clear across primary, secondary, and bulk packaging, and then pressure-testing ASP and mix assumptions in updates, we keep the final value traceable to practical inputs.

Key Questions Answered in the Report

What is the projected value of global tobacco packaging in 2031?

The tobacco packaging market is forecast to reach USD 22.76 billion by 2031, rising from USD 19.33 billion in 2026.

Which material leads current packaging demand?

Paper and paperboard dominates with 56.73% revenue share in 2025 due to cost efficiency and recyclability.

Which region offers the fastest growth opportunity?

The Middle East is set to grow at a 4.39% CAGR through 2031 as new graphic-warning mandates require higher-spec substrates.

How are plain-pack rules affecting converters?

Plain-packaging eliminates decorative finishes, compresses margins, and shifts focus toward anti-counterfeit features and low-cost production.

What segment is expanding fastest by product form?

Tube and heat-not-burn stick formats is advancing at a 4.16% CAGR, powered by IQOS and similar platforms.

How concentrated is the supplier landscape?

The top five converters hold around 38% of capacity, indicating moderate concentration and ongoing consolidation pressure.

Page last updated on: