High-temperature Thermoplastic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

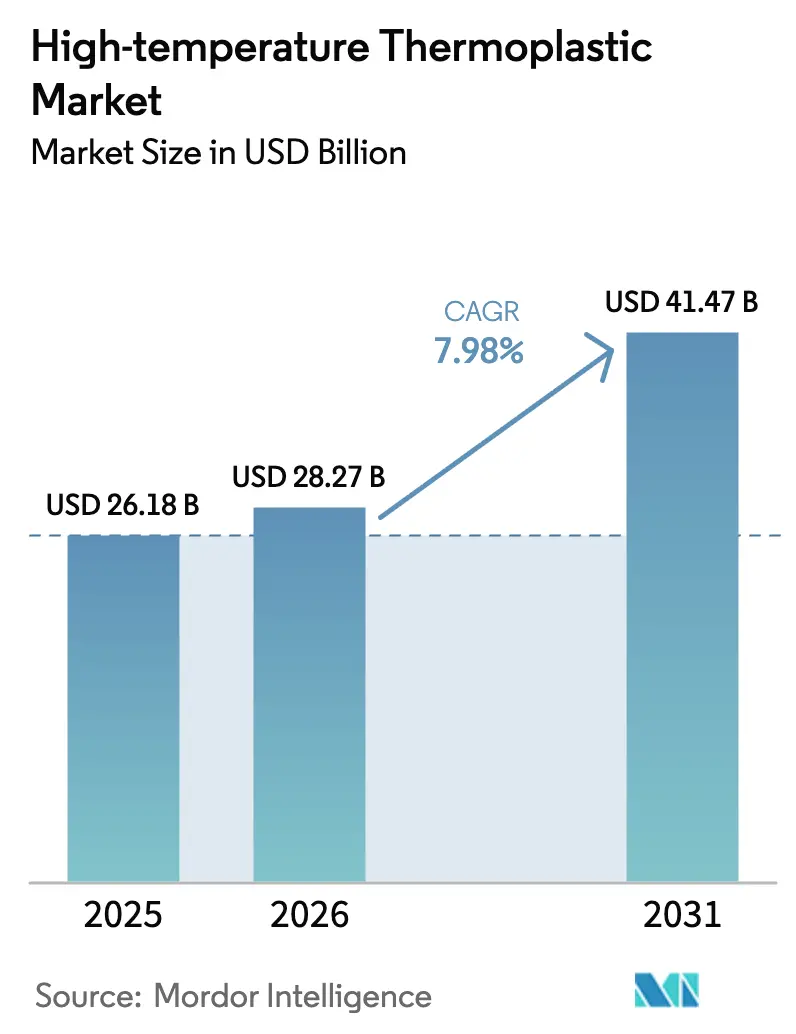

| Market Size (2026) | USD 28.27 Billion |

| Market Size (2031) | USD 41.47 Billion |

| Growth Rate (2026 - 2031) | 7.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-temperature Thermoplastic Market Analysis by Mordor Intelligence

High-temperature Thermoplastic market size in 2026 is estimated at USD 28.27 billion, growing from 2025 value of USD 26.18 billion with 2031 projections showing USD 41.47 billion, growing at 7.98% CAGR over 2026-2031. Demand accelerates because these polymers tolerate continuous temperatures above 200 °C while retaining strength, an essential property for electric vehicle batteries, miniaturized electronics, and lightweight aerospace structures. Electrification, 5G roll-outs, and record aircraft build rates combine to pull larger production volumes through the supply chain. Supply-side readiness also improves as key resin producers open additional capacity in Asia-Pacific, shortening lead times for regional converters and original equipment manufacturers. Even so, cost volatility in specialty monomers and energy continues to challenge smaller participants that lack the scale to hedge input swings. The result is a balanced but vibrant industry that rewards technology leadership, regionalized manufacturing, and closed-loop product development.

Key Report Takeaways

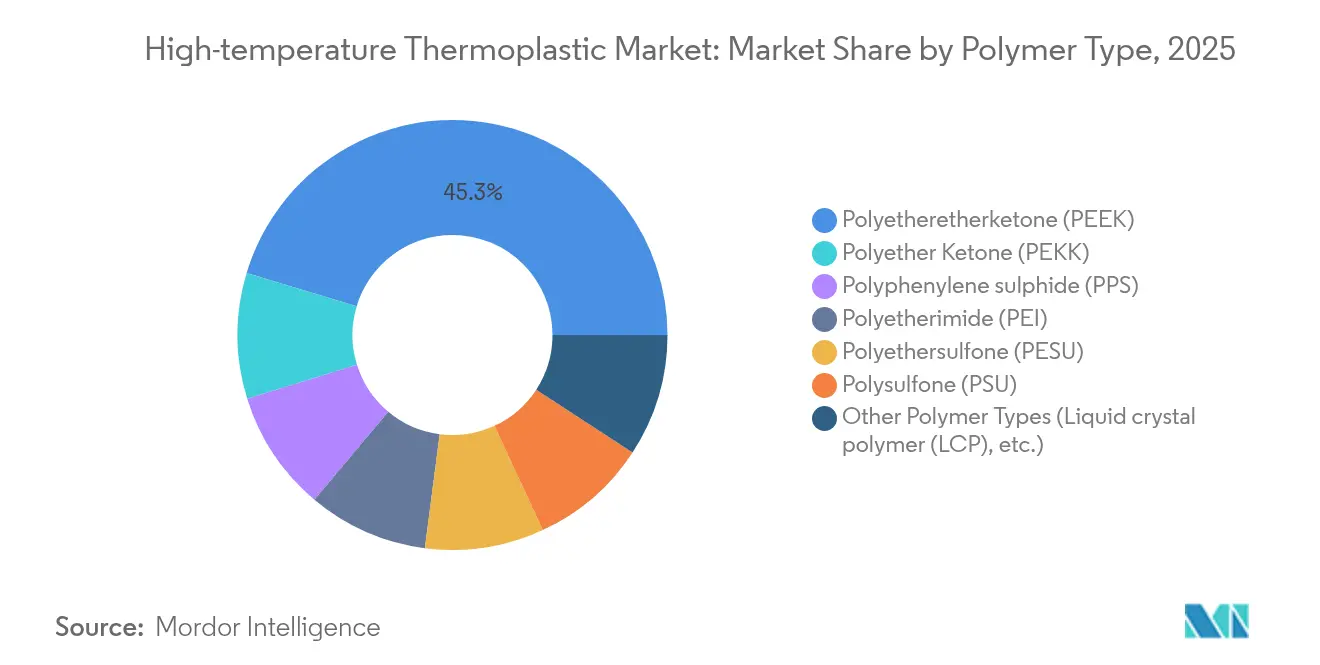

- By polymer type, PEEK captured 45.35% of high-temperature thermoplastic market share in 2025, while PEKK is projected to advance at an 10.78% CAGR through 2031.

- By molecular structure, semi-crystalline grades held 71.10% share of the high-temperature thermoplastic market size in 2025; amorphous grades post the fastest 7.67% CAGR to 2031.

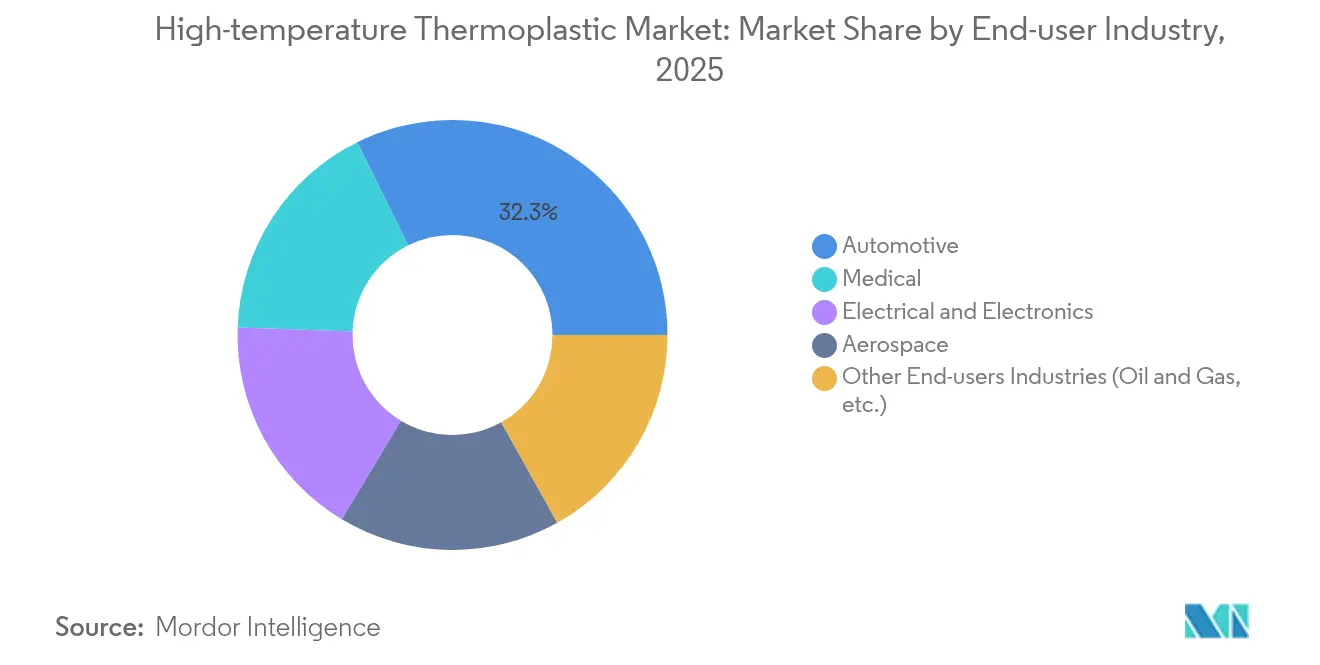

- By end-user industry, the automotive segment led with 32.30% revenue share in 2025; medical and healthcare is forecast to grow at a 9.72% CAGR through 2031.

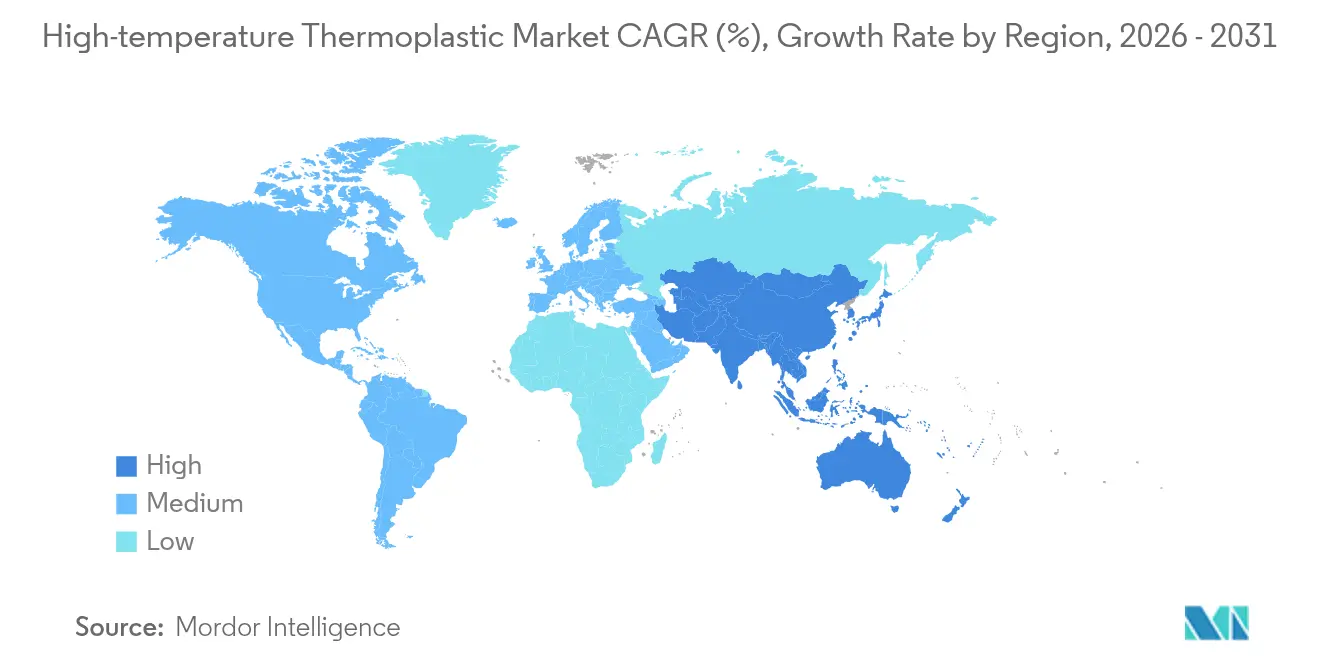

- By region, Asia-Pacific commanded 39.05% of the high-temperature thermoplastic market in 2025 and is poised to rise at an 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-temperature Thermoplastic Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight automotive components | +2.1% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growth electronics miniaturisation and high-heat PCB applications | +1.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Growing demand from the aerospace and defense industry | +1.5% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| High usage in 3D printing and additive manufacturing | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand from healthcare industry | +0.9% | Global, with premium markets leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight Automotive Components

Electric vehicles require resin grades that endure battery pack temperatures, flame exposure, and constant vibration. SABIC’s NORYL NHP8000VT3 delivers a CTI PLC0 rating that helps protect 800-volt power-train architectures against tracking failure. The 2024 Bluebus e-bus integrated a thermoplastic battery housing, trimming mass versus an aluminum shell while exceeding fire-safety limits. Tesla specified roughly 9 kg of PEEK per Optimus-Gen2 humanoid robot and removed 10 kg of total weight, proving the polymer’s versatility beyond vehicles. Automakers pursuing longer range and faster charging combine those examples to confirm a structural shift toward advanced thermoplastics.

Growth in Electronics Miniaturization and High-Heat PCB Applications

Shrinking form factors raise component heat flux, pushing board temperatures above 300 °C during assembly reflow. Polyimide film maintains dimensional stability and matches copper’s coefficient of thermal expansion, reducing delamination in high-density circuits. The IEEE Heterogeneous Integration Roadmap flags high-temperature thermoplastics as critical die-attach and under-fill materials for chiplet packaging, enabling further transistor scaling[1]IEEE Publications, “Heterogeneous Integration Roadmap 2025,” ieee.org. As data-center operators chase higher rack power and 5G radios proliferate, board makers specify polymers that survive rapid thermal cycling without embrittlement. Asia-Pacific foundries already line up additional laminator lines, indicating a near-term pull that benefits regional resin suppliers.

Growing Demand from the Aerospace and Defense Industry

Commercial and defense airframers move toward thermoplastic composite ribs, clips, and skins to support rate ramp-ups targeting 100 single-aisle jets per month. Arkema and Hexcel produced the first qualified PEKK-based primary structure in 2024, proving industrial readiness for flight parts. Boeing’s 155,000 ft² Advanced Composite Fabrication Center in Arizona will reach steady-state output in late 2025, reinforcing North American leadership. PEEK and PEI already meet FAR 25.853 without added flame retardants, eliminating secondary treatments and speeding assembly. Certification hurdles deter new entrants, yet once cleared they lock in multi-decade revenue streams, enhancing the driver’s long-term potency.

High Usage in 3D Printing and Additive Manufacturing

EOS lasers sinter PEKK powders into aircraft brackets with repeatable porosity control, while Markforged feeds continuous-fiber thermoplastics for robotic end-effectors at small lot sizes. Hot-isostatic pressing improves 3D-printed PEEK composites by 46% in flexural strength and 30% in inter-laminar shear, narrowing the gap with injected parts. Custom implants tailored to patient anatomy, plus flight-ready ducting with integral stiffeners, make additive a strong mid-term accelerator.

Rising Demand from Healthcare Industry

Orthopedic and cranial implants rely on PEEK for biocompatibility and radiolucency. Evonik’s VESTAKEEP Fusion, which embeds biphasic calcium phosphate, raised osteoblast attachment by more than 30% versus standard PEEK. Single-use surgical tools favor amorphous PSU and PESU for steam-sterilization cycles and clear sight-lines. Global aging populations and minimally invasive procedures lock in steady growth, positioning healthcare as a durable long-term volume contributor.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw-material and compounding cost | -1.4% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Recycling and circular-economy challenges | -0.8% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Capital-intensive high-temperature processing equipment | -0.6% | Global, with higher barriers in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material and Compounding Cost

Specialty monomers face tight balances and geopolitical disruptions. Composite resin producer AOC raised prices by EUR 200 per ton for vinyl ester blends in 2024, passing energy hikes through the chain. Medical device firms coping with PTFE shortages were forced to verticalize fluoropolymer extrusion to secure supply. High-temperature twin-screw extruders and mold-temperature control units rated above 400 °C require capital that smaller firms cannot easily deploy. Until unit costs go down, price-sensitive segments will continue to substitute with engineering plastics or aluminum.

Recycling and Circular-Economy Challenges

Closed-loop recovery of PEEK, PEKK, and PPS remains complex because residual glass or carbon fibers degrade molecular weight. Researchers achieved depolymerization of PEEK with sulfur nucleophiles to clean monomer streams, but scale-up is unproven[2]Nature Communications Chemistry, “Selective Depolymerization of PEEK,” nature.com. Röchling allocated EUR 10 million to its Sustainability Centre to mechanically reprocess 10,000 tons of waste a year, yet still must blend recycled flake with virgin resin for critical properties. Regulatory pushes for minimum recycled content intensify in Europe and North America, creating compliance costs and, in some applications, performance compromises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: PEEK Dominance Faces PEKK Innovation

PEEK held 45.35% of the high-temperature thermoplastic market share in 2025. Tensile strength near 115 MPa and continuous-use temperature around 260 °C keep the polymer on most qualified parts lists. Aerospace seat frames, spinal cages, and semiconductor wafer-handling components rely on that track record. PEKK’s lower crystallization speed supports layer-by-layer fusion in additive manufacturing, a trait that underpins its 10.78% CAGR. Arkema’s licensing deal with SEQENS enables back-integration of anode-grade raw materials, thereby reducing exposure to supply shocks.

Second-tier materials advance as well. Liquid-crystal polymer grades with a glass transition temperature above 280 °C meet the next-generation connector pin density requirements in 5G base stations. Ultra-high-molecular-weight polybenzimidazole is used in downhole seals at 350 °C, but it is sold in kilograms rather than tonnes. Collectively, these specialty niches limit commoditization, sustaining premium margins across the high-temperature thermoplastic market.

By Molecular Structure: Semi-Crystalline Strength Versus Amorphous Versatility

Semi-crystalline grades accounted for 71.10% of the overall high-temperature thermoplastic market in 2025, as their ordered domains confer high modulus, excellent barrier properties, and long-term creep resistance. Carbon–fiber–reinforced PEKK panels with a 60% fiber volume fraction maintain an eighty-plus gigapascal flexural modulus at 150 °C. Such traits are essential for aerospace wing access doors and electric-vehicle skid plates that are subjected to rock strikes. Amorphous cousins grow 7.67% CAGR on the back of optical and processing advantages.

PESU powder dissolves in dimethylacetamide, enabling the application of spray-coated anti-corrosion layers on steel vessels. Lower melt viscosity lets molders fill thin-wall connectors without voids, cutting cycle time. Advances in plasma surface activation now improve adhesion across both structures, widening part-design freedom. Dual-matrix hybrids, which combine amorphous PEI skins with semi-crystalline PEEK cores, are expected to arrive in 2025 prototypes, aiming to optimize both clarity and stiffness in a single component.

By End-User Industry: Automotive Leadership Challenged by Medical Innovation

Automotive applications consumed 32.30% of the total volume in 2025. Battery enclosures made from continuous-fiber PEEK/CF laminates meet the UL 94 V0 standard with a margin and weigh 30% less than aluminum boxes. Syensqo’s Ajedium PEEK dielectric film squares the circle on high dielectric strength and low dissipation factor for 800-V inverter busbars. The medical and healthcare sector’s 9.72% CAGR stems from growth in image-compatible implants and sterilizable single-use tools. PEEK spinal cages machined to patient scans reduce operating time, while PSU trocar cannulas withstand more than 1,000 steam cycles.

Aerospace demand rides Boeing and Airbus build-rate targets. Military rotorcraft retrofit programs specify PEKK clamps because the polymer does not galvanically corrode adjacent carbon fiber. Oil and gas operators still purchase PPS valve seats for sour-gas service, yet new field investments lag behind the pace of electric-mobility spending. Diverse requirements across end-users keep the supply base balanced, smoothing revenue against cyclical swings in any one sector.

Geography Analysis

Asia-Pacific’s 39.05% 2025 share stems from vertically integrated supply chains that connect monomer synthesis, compounding, and part fabrication within a day’s trucking distance. The region is expected to post the fastest 8.45% CAGR to 2031. Government incentives for new-energy vehicles in China, India, and Thailand boost demand for PEEK battery frames and PPS coolant fittings. Japanese OEMs are pioneering PEI-based connector blocks for ultrafast chargers, thereby expanding the domestic converter base.

North America maintains a resilient position. The aerospace backbone of Washington state and Alabama anchors steady polymer off-take, while the Texas chemical corridor supplies key monomers. Post-pandemic reshoring policies are encouraging battery manufacturers to invest in Michigan and Georgia, where processors are installing new 450-ton presses.

Competitive Landscape

The high-temperature thermoplastic market exhibits a high degree of concentration. Victrex, Syensqo, SABIC, and Arkema defend their shares through extensive patent estates and multi-regional plants that offer local service, as well as redundancy. Competition is increasingly shifting to processing innovation rather than basic chemistry. Supply-chain disruptions push producers to regionalize compounding and stock safety inventories. SABIC expanded Ultem resin output in Singapore by 50%, securing Asian supply for autos and electronics.

High-temperature Thermoplastic Industry Leaders

Arkema

Solvay

SABIC

Victrex plc

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hexcel unveiled a PEKK/carbon thermoplastic over-wing emergency-exit component under the HELUES aerospace project, showing rate-capable out-of-autoclave forming.

- March 2025: SABIC introduced EXTEM RH resin that withstands 260 °C reflow soldering for optics, connectors, and data-infrastructure housings.

Global High-temperature Thermoplastic Market Report Scope

The high-temperature thermoplastic report includes:

| Polyetheretherketone (PEEK) |

| Polyether Ketone (PEKK) |

| Polyphenylene sulphide (PPS) |

| Polyetherimide (PEI) |

| Polyethersulfone (PESU) |

| Polysulfone (PSU) |

| Other Polymer Types (Liquid crystal polymer (LCP), etc.) |

| Amorphous |

| Semi-crystalline |

| Automotive |

| Electrical and Electronics |

| Aerospace |

| Medical |

| Other End-users Industries (Oil and Gas, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Polymer Type | Polyetheretherketone (PEEK) | |

| Polyether Ketone (PEKK) | ||

| Polyphenylene sulphide (PPS) | ||

| Polyetherimide (PEI) | ||

| Polyethersulfone (PESU) | ||

| Polysulfone (PSU) | ||

| Other Polymer Types (Liquid crystal polymer (LCP), etc.) | ||

| By Molecular Structure | Amorphous | |

| Semi-crystalline | ||

| By End-user Industry | Automotive | |

| Electrical and Electronics | ||

| Aerospace | ||

| Medical | ||

| Other End-users Industries (Oil and Gas, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current high-temperature thermoplastic market size?

The high-temperature thermoplastic market size reached USD 28.27 billion in 2026 and is forecast to reach USD 41.47 billion by 2031.

Which region leads the high-temperature thermoplastic market?

Asia-Pacific leads with 39.05% revenue share in 2025 and is projected to grow at an 8.45% CAGR through 2031.

Which polymer dominates the high-temperature thermoplastic market?

PEEK held 45.35% market share in 2025, driven by its track record in aerospace, medical, and industrial parts.

Why are high-temperature thermoplastics important for electric vehicles?

They enable lighter battery housings and withstand continuous exposure above 200 °C, improving range and safety.

What is the fastest-growing end-use segment?

Medical and healthcare applications are set to expand at a 9.72% CAGR to 2031 due to stricter biocompatibility and minimally invasive surgery trends.

Page last updated on: