Thermoformed Plastics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

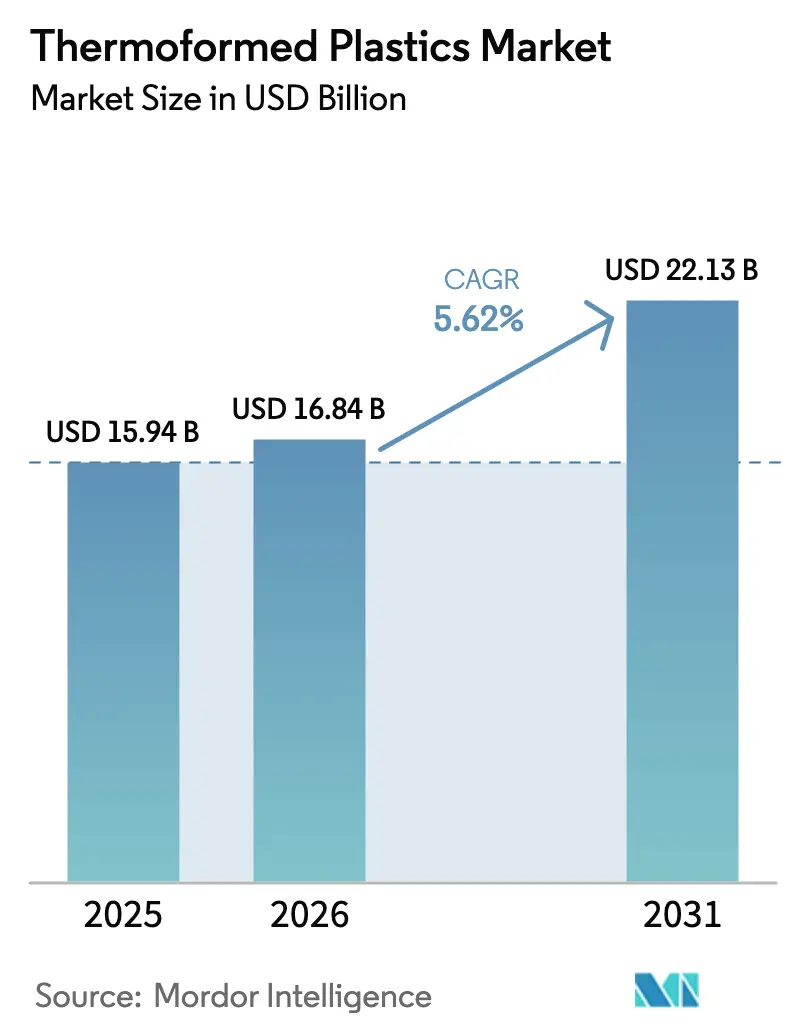

| Market Size (2026) | USD 16.84 Billion |

| Market Size (2031) | USD 22.13 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoformed Plastics Market Analysis by Mordor Intelligence

The Thermoformed Plastics Market size is expected to increase from USD 15.94 billion in 2025 to USD 16.84 billion in 2026 and reach USD 22.13 billion by 2031, growing at a CAGR of 5.62% over 2026-2031. Demand concentrates in food, beverage, healthcare, and automotive applications where thin- and thick-gauge sheets replace heavier or multi-part assemblies for cost and weight savings. Global brand owners accelerated recycled-content commitments after the European Union’s Packaging and Packaging Waste Regulation (PPWR) started phasing in minimum thresholds in 2024. Meanwhile, California’s SB 54 triggered similar momentum in North America by requiring 65% recyclability for single-use plastic packaging by 2032. Brand owners’ public sustainability goals have therefore insulated the thermoformed plastics market from cyclical feedstock price swings, although converters still face margin pressure when Brent crude volatility lifts resin costs faster than sales contracts adjust. Consolidation among mid-size processors is underway as Novolex completed its USD 6.7 billion purchase of Pactiv Evergreen in April 2025, capturing scale economies in recycled-PET procurement and cross-plant scheduling efficiencies.

Key Report Takeaways

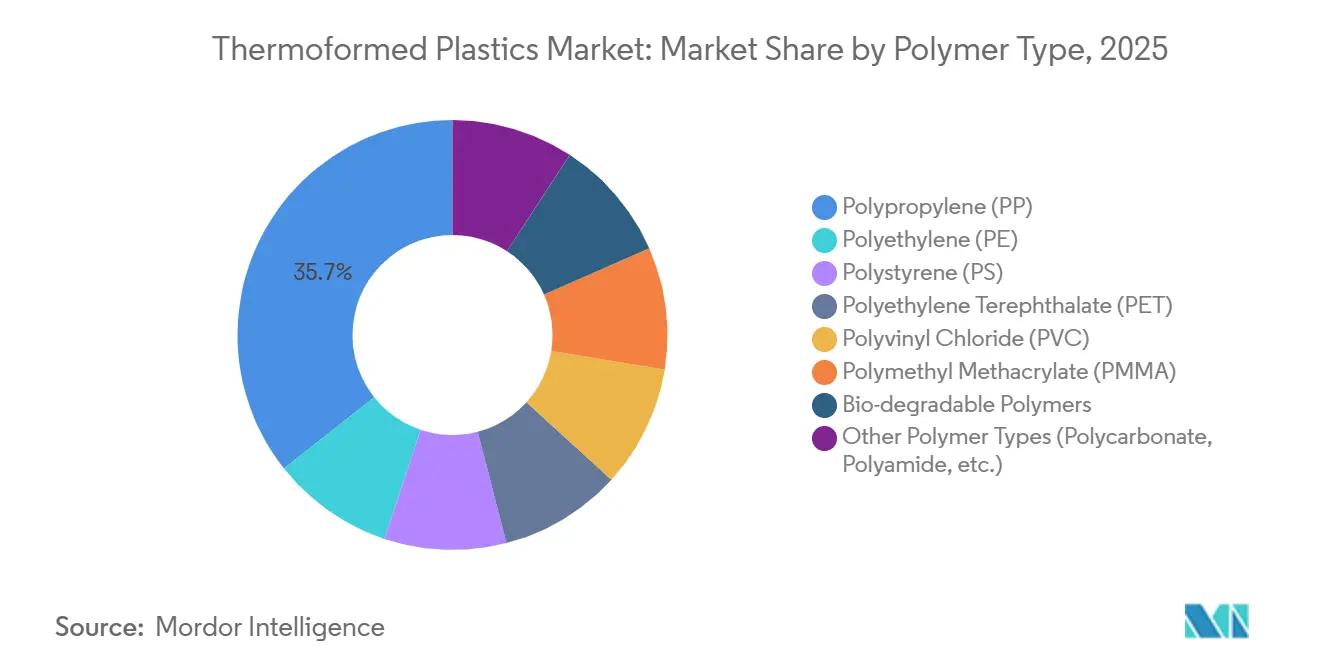

- By polymer type, polypropylene held 35.67% of the thermoformed plastics market share in 2025, while bio-degradable resins are forecast to accelerate at a 6.82% CAGR through 2031.

- By thermoforming process, vacuum forming led with 42.29% revenue share in 2025, whereas plug-assist forming is projected to post a 6.17% CAGR to 2031.

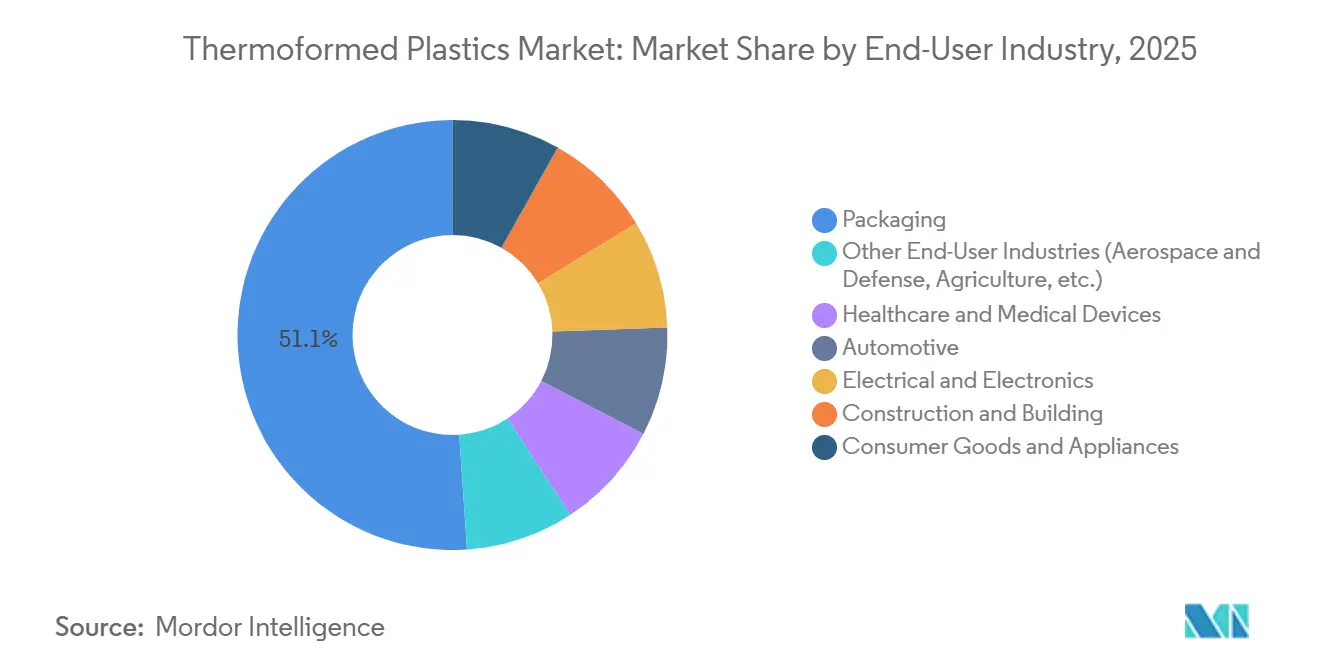

- By end-user industry, packaging accounted for 51.08% share of the thermoformed plastics market size in 2025, yet healthcare is expected to register the fastest 6.25% CAGR through 2031.

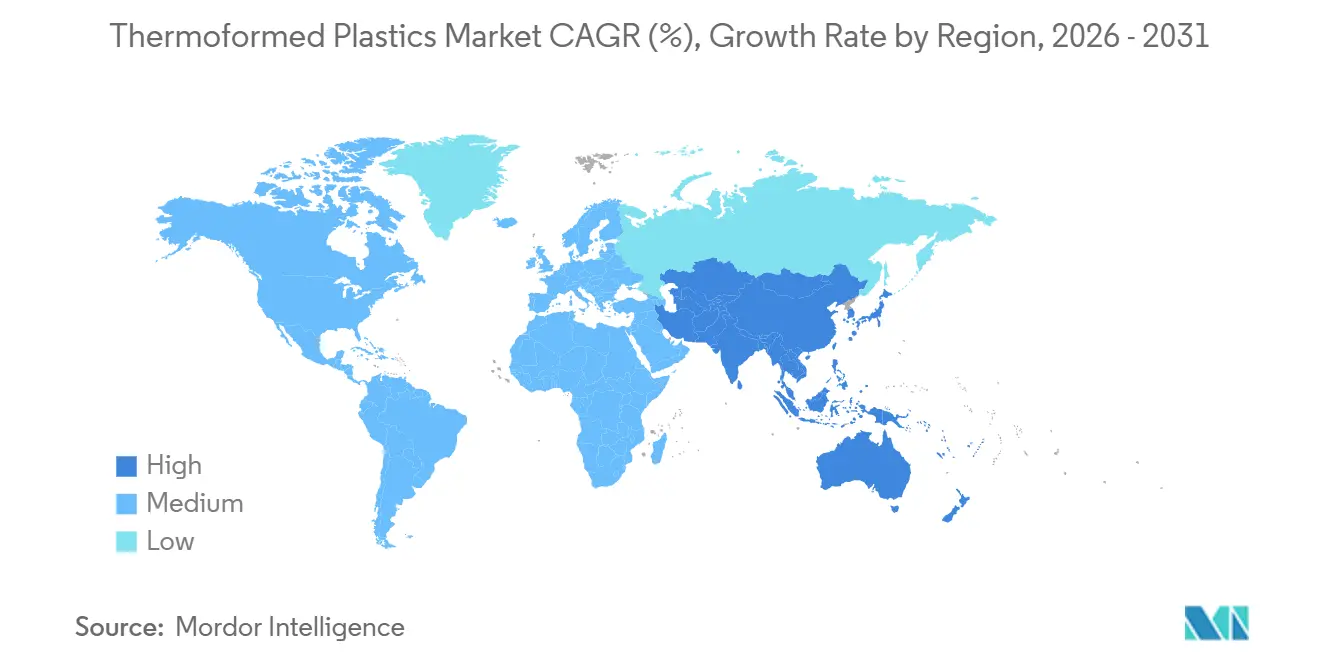

- By geography, Asia-Pacific held 39.96% share of the thermoformed plastics market size in 2025, and is anticipated to grow with the fastest CAGR of 5.94% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermoformed Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight sustainable food & beverage packaging | +1.2% | North America and EU markets | Medium term (2-4 years) |

| Rising use of disposable medical devices | +1.4% | North America, Europe, Japan, South Korea | Long term (≥4 years) |

| Cost-efficient mass production for auto interiors | +0.9% | Europe, North America, Chinese automotive hubs | Medium term (2-4 years) |

| Impact-resistant inserts for rapid e-commerce | +1.1% | North America, China, India, Brazil | Short term (≤2 years) |

| Automated poultry-farming feed-tray systems | +0.5% | China, Thailand, Vietnam, Brazil, United States | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Lightweight Sustainable Food and Beverage Packaging

California’s SB 54 requires 65% recyclability for single-use plastic packaging by 2032, prompting global quick-service restaurants to replace polystyrene with recycled-PET clamshells. Amcor disclosed that recycled-content PET thermoformed containers now contribute 22% of its rigid-packaging portfolio, up from 14% in fiscal 2023. The European PPWR, effective May 2024, mandates 30% recycled content for PET and 10% for other formats by 2030. Huhtamaki responded by commissioning a EUR 50 million recycled-PET washing line in Poland with 40,000 tonnes annual capacity in January 2025[1]Huhtamaki Oyj, “Huhtamaki Invests in Polish Recycling Line,” huhtamaki.com. Thin-gauge thermoforming reduces film thickness from 600 microns to 450 microns, trimming 25% resin per tray while maintaining drop-test integrity required for e-grocery chains that reported 8% of parcels experiencing impacts above 3 G in 2025.

Growing Consumption of Disposable Medical and Pharmaceutical Devices

The U.S. Centers for Disease Control highlighted high-level disinfection failures in 2024, steering ambulatory surgery centers toward sterile single-use trays[2]Centers for Disease Control and Prevention, “High-Level Disinfection Guidance,” cdc.gov. Sealed Air’s 2024 10-K showed 11% revenue growth in medical-device packaging, led by insulin-pen blisters complying with ISO 11607. The U.S. FDA cleared 38 new Class II devices with thermoformed housings in 2025. India’s Production-Linked Incentive program earmarked INR 34 billion (USD 408 million) for domestic medical-device makers in fiscal 2025. New carbon-loaded polypropylene trays now achieve surface resistivity below 10¹¹ ohms-per-square, preventing electrostatic failures during cardiac-device assembly.

Cost-Efficient Mass-Production for Automotive Interior Components

EU carbon-emission norms cap fleet averages at 93.6 grams CO₂ per kilometer in 2025, encouraging original equipment manufacturers to substitute steel trunk liners with thermoformed glass-fiber-reinforced polypropylene, trimming weight by 40%. Stellantis reported that 14% of interior parts in its Peugeot 3008 now use thermoformed polypropylene, up from 8% in the prior model. Plug-assist forming reduces tooling lead time to 8 weeks versus 18 weeks for injection molds, aiding faster platform launches. China’s New Energy Vehicle mandate, which targets 40% electrified sales by 2030, boosts demand for UL 94 V-0 thermoformed battery covers. In-mold decorated panels eliminate secondary painting and cut volatile organic compound emissions by 90%.

Rapid E-Commerce Growth Driving Impact-Resistant Shipment Inserts

North American parcel volumes climbed 18% year-on-year to 9.2 billion in 2025, expanding demand for HDPE protective inserts that lower electronics damage rates from 4.3% to 1.1%. Thermoformed pulp-fiber inserts launched by DS Smith in March 2025 satisfy the UK’s full-cost Extended Producer Responsibility framework. Flipkart and Amazon India adopted polypropylene mailer inserts that reduced packaging weight by 35%, saving INR 4.20 (USD 0.05) per shipment in 2025. Cold-chain biologics shipment panels made of vacuum-insulated polyurethane now maintain 2 °C to 8 °C for 96 hours, enabling direct-to-patient delivery without dry ice.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic bans and taxes | -0.8% | EU, UK, California, Canada | Short term (≤2 years) |

| Crude-linked feedstock price volatility | -0.6% | Europe and North America | Short term (≤2 years) |

| PFAS / micro-plastic contamination directives | -0.4% | Denmark, Netherlands, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Worldwide Single-Use-Plastic Regulations and Bans

The EU Single-Use Plastics Directive, fully enforced since July 2024, bars oxo-degradable resins and restricts polystyrene foodware, forcing restaurants to convert to polypropylene or PLA alternatives that cost 18% more. Canada’s Prohibition Regulations, effective December 2024, removed 42,000 tonnes of annual thermoformed polystyrene demand. California’s SB 54 sets a USD 500 million annual producer fee from 2027, penalizing multilayer trays that contaminate recycling streams. The UK Plastic Packaging Tax of GBP 210.82 per tonne on items with under 30% recycled content, in force since April 2025, eroded converters’ margins by 14%. India’s 2024 Plastic Waste Management rules ban thin plates and bowls below 50 microns, switching demand toward 120-micron PLA that composts within 180 days.

Volatility of Crude-Linked Polymer Feed-Stock Prices

Brent crude averaged USD 82 per barrel in 1H 2025, lifting European polypropylene contracts by 14% quarter-on-quarter to EUR 1,420 per ton. PET resin prices in North America whipsawed between USD 1,180 and USD 1,540 per tonne during 2024 as Gulf Coast force majeures disrupted supply. China’s domestic propylene additions cut import dependence by 8% in 2024, yet spot prices still swung 12% month-to-month due to coal-to-olefin outages. Sealed Air revealed raw-material inflation shaved USD 47 million off adjusted EBITDA by Q3 2024, prompting new quarterly pass-through clauses. Bio-based PLA continues to price at a 35% premium to virgin polypropylene, curbing substitution in cost-sensitive cutlery applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Bio-Degradable Resins Gain Despite Cost Penalty

Polypropylene retained a 35.67% share of the thermoformed plastics market in 2025 thanks to its low 0.90 g/cm³ density and 1,600 MPa flexural modulus that enable lightweight yet stiff food clamshells and automotive liners. Bio-degradable polymers such as polylactic acid and polyhydroxyalkanoates are forecast to grow at a 6.82% CAGR to 2031, outpacing the broader thermoformed plastics market because EU PPWR and California SB 54 favor compostable packaging for take-away applications. Recycled-content polyethylene terephthalate (rPET) is also expanding as Amcor lifted rPET containers to 22% of rigid-packaging sales in fiscal 2025. Polystyrene demand is eroding following the EU Single-Use Plastics Directive ban on expanded formats in July 2024. Polymethyl methacrylate and polycarbonate hold niche roles in 5G radome housings and electric-vehicle battery covers, where UV stability and UL 94 V-0 ratings outweigh higher material cost.

PET trays for fresh produce now incorporate 25% post-consumer resin on average, a figure expected to hit 40% by 2030 as bottle-to-tray recycling becomes mainstream across Germany, France, and the United Kingdom. Polyvinyl chloride remains concentrated in blister packs complying with ISO 15378; however, pharmaceutical brand owners are piloting PET-G alternatives to sidestep chlorine-content disposal hurdles. Polyamide and glass-fiber-reinforced polypropylene appear in structural thermoformed parts for battery-electric vehicles where metal substitution reduces weight by up to 45% and improves corrosion resistance over 10-year duty cycles.

By Thermoforming Process: Plug-Assist Gains on Tight Tolerances

Vacuum forming contributed 42.29% of the thermoformed plastics market share in 2025 because its USD 8,000–15,000 mold investments suit high-volume clamshells and produce trays. Plug-assist forming, however, is expected to register the quickest 6.17% CAGR through 2031 as automakers and medical-device manufacturers demand ±0.15 mm tolerances for complex geometries. Plug-assist reduces corner thinning from 35% to 12% by mechanically stretching the sheet before vacuum application, enabling draw ratios exceeding 3:1 for deep medical trays. Thin-gauge thermoforming (≤1.5 mm) commands 68% unit volume because lightweight single-use foodware prioritizes material cost. Thick-gauge methods occupy automotive and industrial niches where impact requirements exceed 30 kJ/m².

Pressure forming applies up to 100 psi compressed air, achieving sub-0.05 mm surface detail resolution suited for instrument-panel fascias that integrate functional buttons without assembly labor. Hybrid infrared-heated rotary systems now deliver 18-second cycle times, boosting overall equipment effectiveness to 87% in North American food-tray facilities. Converters are coupling inline trim-and-stack robots to slash scrap rates below 2%. Digital twins model sheet sag profiles to optimize oven zoning, saving 6% energy per cycle while meeting corporate carbon-reduction targets.

By End-User Industry: Healthcare Outpaces Packaging Growth

Packaging dominated demand with a 51.08% share in 2025, buoyed by e-commerce parcel growth and quick-service restaurant sustainability pledges. Yet, healthcare applications are poised for a 6.25% CAGR to 2031 as single-use sterile trays displace stainless-steel counterparts across ambulatory surgery centers, aligning with updated CDC disinfection guidance. Automotive interiors will extend the adoption of glass-fiber-reinforced polypropylene door panels to satisfy the 2025 EU emissions caps, while electric-vehicle battery covers create fresh volumes for flame-retardant polycarbonate.

Electrical and electronics applications gain from Asia-Pacific semiconductor investments that require electrostatic-discharge trays rated below 10¹¹ ohms-per-square. Construction uses—ABS skylights and insulated wall panels—benefit from retrofit energy-efficiency mandates in Europe, though volumes remain modest. Aerospace and defense remain niche but profitable, demanding polycarbonate radomes tested per MIL-STD-810 for −55 °C to +85 °C cycling. Agricultural seedling trays continue expanding in China, which planted over 128 million hectares in 2024, leveraging thin-gauge polypropylene that withstands 500 wash cycles.

Geography Analysis

Asia-Pacific controlled 39.96% of the thermoformed plastics market in 2025 and will post the fastest 5.94% CAGR through 2031. Growth stems from China’s 12 GW solar-module additions that require polypropylene junction-box housings and India’s INR 34 billion (USD 408 million) Production-Linked Incentive, fueling medical-device trays. Japan’s auto exports of 3.2 million units in 2024 demanded lightweight interior panels to meet 25.4 km/L fuel norms. South Korea’s DRAM dominance drives electrostatic-discharge trays in semiconductor fabs, while Thailand and Indonesia collectively added 180,000 tonnes of food-packaging capacity to serve 4,200 new quick-service restaurants.

North America captured a significant revenue share in 2025, with e-commerce parcels topping 9.2 billion and sparking demand for protective inserts. The United States represented over half of regional consumption, aided by FDA clearance of 38 Class II devices using thermoformed housings in 2025. Canada’s ban on foamed polystyrene cutlery redirected converters toward polypropylene and PLA alternatives. Mexico’s 3.1 million vehicle assemblies leveraged domestic door-panel suppliers under USMCA local-content rules exceeding 75%.

The thermoformed plastics consumption in Europe is governed by stringent regulations. The PPWR enforces 10–30% recycled-content thresholds by 2030, encouraging Huhtamaki’s EUR 50 million Polish recycling line. Germany’s 3.6 million passenger-car output increasingly favors thermoformed glass-fiber trunk liners that save 1.2 grams CO₂ per km over vehicle lifecycles. The UK’s GBP 210.82 per-ton tax on low-recycled-content plastics shaved 14% off converter margins. Russia expanded domestic PET capacity by 65,000 tonnes during 2024 to replace imports constrained by sanctions.

South America and the Middle East are witnessing rapidly growing demand for thermoformed plastics. Brazil’s 14.8 million-ton poultry sector relies on RFID-enabled feed trays to meet export bio-security audits. Argentina’s recycled-content packaging supports beef and wine exports to the EU. Saudi Arabia’s Vision 2030 funnels SAR 12 billion (USD 3.2 billion) into a 120,000-tonne polypropylene thermoforming facility due online in 2026. The UAE’s tourism-driven food-service market still imports 82% of clamshells, signaling room for domestic capacity.

Competitive Landscape

The thermoformed plastics market remains moderately fragmented. Major leading players in the market are engaged in capacity expansion and supply agreements with larger end-user industries. Smaller converters compete on process agility. Plug-assist forming with inline trim-and-stack robotics lets mid-tier firms deliver ±0.15 mm tolerances at cycle times under 20 seconds, appealing to cardiac-device original equipment manufacturers requiring ISO 11607 compliance. In-mold decoration eliminated secondary painting on Peugeot 3008 panels, reducing volatile organic compound emissions by 90% and saving USD 1.20 per part. Process automation, digital-twin oven control, and recycled-resin dosing systems now differentiate bids, enabling 2% scrap rates versus 6% three years ago.

Thermoformed Plastics Industry Leaders

Sealed Air

Amcor plc

Pactiv Evergreen Inc.

Huhtamaki Oyj

TOPPAN Packaging Americas Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex closed its USD 6.7 billion purchase of Pactiv Evergreen, creating North America’s largest thermoformed-packaging producer with 42 lines and 580,000 tons yearly capacity.

- June 2024: Sealed Air committed USD 120 million to add three clean-room thermoforming lines for insulin-pen blisters at its Charlotte, North Carolina plant, targeting Q1 2026 start-up.

- September 2024: Amcor signed a 10-year deal to supply McDonald’s with recycled-PET clamshells containing 25% post-consumer resin for 8,400 U.S. restaurants.

Global Thermoformed Plastics Market Report Scope

Thermoformed plastics are products made from thermoplastic sheets that are heated until pliable, then shaped into a 3D form using vacuum or pressure against a mold, and finally cooled to harden. This versatile process creates items like food trays, packaging, automotive parts, and appliance liners by transforming flat plastic sheets into complex shapes, often with lower tooling costs than other methods.

The thermoformed plastics market is segmented by polymer type, thermoforming process, end-user industry, and geography. By polymer type, the market is segmented into polypropylene (PP), polyethylene (PE), polystyrene (PS), polyethylene terephthalate (PET), polyvinyl chloride (PVC), polymethyl methacrylate (PMMA), bio-degradable polymers, and other polymer types (polycarbonate, polyamide, etc.). By thermoforming process, the market is segmented into vacuum forming, plug assist forming, thin-gauge thermoforming, and thick-gauge thermoforming. By end-user industry, the market is segmented into packaging, healthcare and medical devices, automotive, electrical and electronics, construction and building, consumer goods and appliances, and other end-user industries (aerospace and defense, agriculture, etc.). The report also covers market size and forecasts for thermoformed plastics in 18 countries across major regions. For each segment the market sizing and forecasts have been done on the basis of revenue (USD).

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polystyrene (PS) |

| Polyethylene Terephthalate (PET) |

| Polyvinyl Chloride (PVC) |

| Polymethyl Methacrylate (PMMA) |

| Bio-degradable Polymers |

| Other Polymer Types (Polycarbonate, Polyamide, etc.) |

| Vacuum Forming |

| Plug Assist Forming |

| Thin Gauge Thermoforming |

| Thick Gauge Thermoforming |

| Packaging |

| Healthcare and Medical Devices |

| Automotive |

| Electrical and Electronics |

| Construction and Building |

| Consumer Goods and Appliances |

| Other End-User Industries (Aerospace and Defense, Agriculture, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates (UAE) | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Polymer Type | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polystyrene (PS) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride (PVC) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Bio-degradable Polymers | ||

| Other Polymer Types (Polycarbonate, Polyamide, etc.) | ||

| By Thermoforming Process | Vacuum Forming | |

| Plug Assist Forming | ||

| Thin Gauge Thermoforming | ||

| Thick Gauge Thermoforming | ||

| By End-User Industry | Packaging | |

| Healthcare and Medical Devices | ||

| Automotive | ||

| Electrical and Electronics | ||

| Construction and Building | ||

| Consumer Goods and Appliances | ||

| Other End-User Industries (Aerospace and Defense, Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates (UAE) | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the thermoformed plastics market and how fast will it grow?

The market generated USD 16.84 billion in 2026 and is projected to reach USD 22.13 billion by 2031, reflecting a 5.62% CAGR over the forecast period.

Which polymer currently dominates demand in thermoformed plastics?

Polypropylene led in 2025 with a 35.67% share thanks to its low density, stiffness, and suitability for food clamshells and automotive liners.

How are new packaging regulations influencing thermoformed plastics adoption?

The EU PPWR and California’s SB 54 impose recycled-content and recyclability targets, prompting brand owners to shift toward recycled-PET and compostable trays, thereby supporting steady demand even when resin prices fluctuate.

Why is healthcare the fastest growing end-user segment?

Ambulatory surgery centers are switching from reusable metal to sterile single-use thermoformed trays in line with updated CDC disinfection guidance, driving a 6.25% CAGR for healthcare applications through 2031.

What advantages do thermoformed plastics offer to automakers?

Glass-fiber-reinforced polypropylene trunk liners and battery covers cut part weight by up to 40%, aiding compliance with 2025 EU fleet-average CO₂ limits while reducing tooling lead times versus injection molding.

Page last updated on: