Thermochromic Pigments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

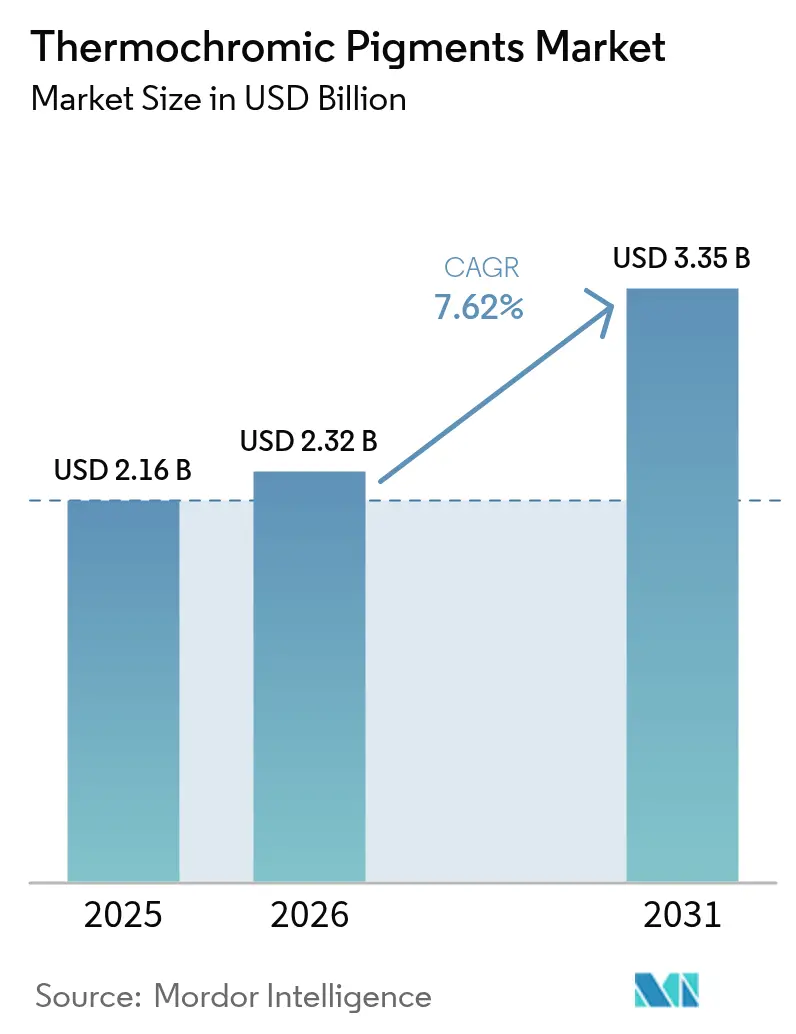

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermochromic Pigments Market Analysis by Mordor Intelligence

The Thermochromic Pigments Market size was valued at USD 2.16 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 3.35 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031). This expansion is propelled by the widening use of temperature-responsive materials in smart packaging, textiles, and security printing, while progress in microencapsulation keeps pigments stable in demanding environments. Increasing pharmaceutical demand for cold-chain indicators, the pivot toward energy-efficient building coatings, and automotive applications that blend aesthetics with thermal management add further momentum. Large regional end-users continue to integrate smart pigments into compliance seals and food packaging, reducing spoilage and enhancing consumer safety. Cost-down efforts in synthesis, combined with regulatory moves favoring visible temperature indicators, sharpen the market’s growth outlook.

Key Report Takeaways

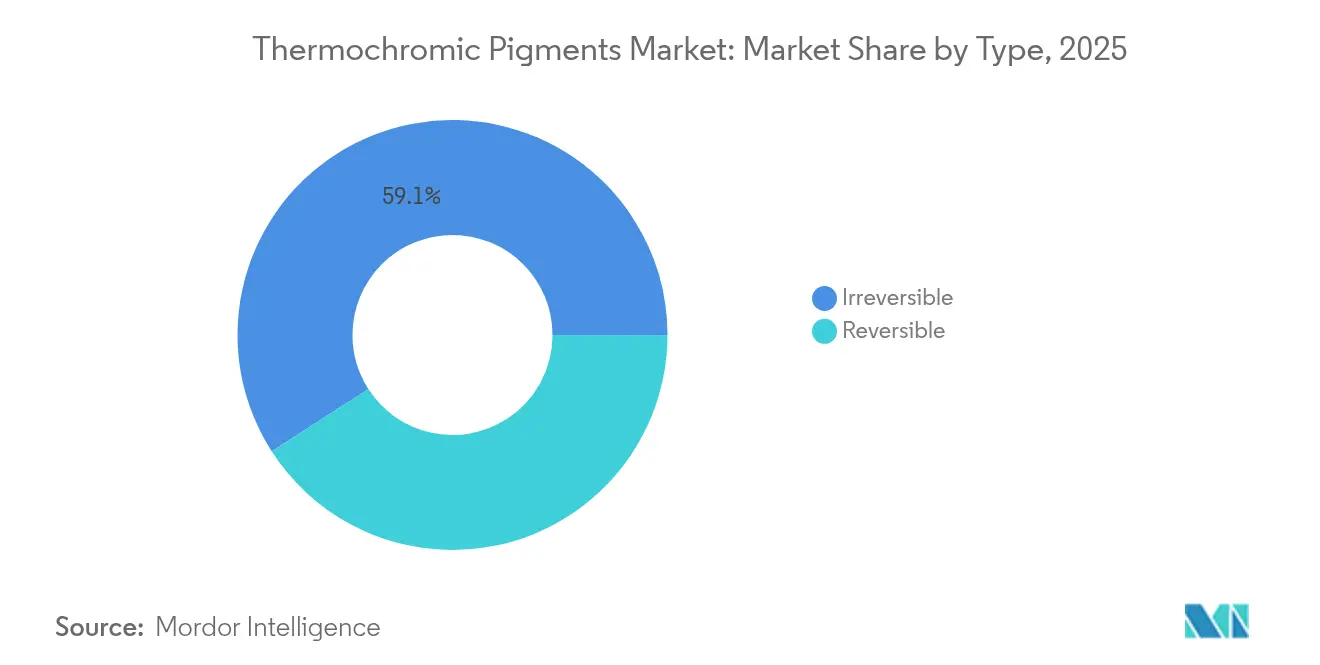

- By type, irreversible grades captured 59.10% of the thermochromic pigments market share in 2025, whereas reversible grades are projected to advance at an 8.55% CAGR through 2031.

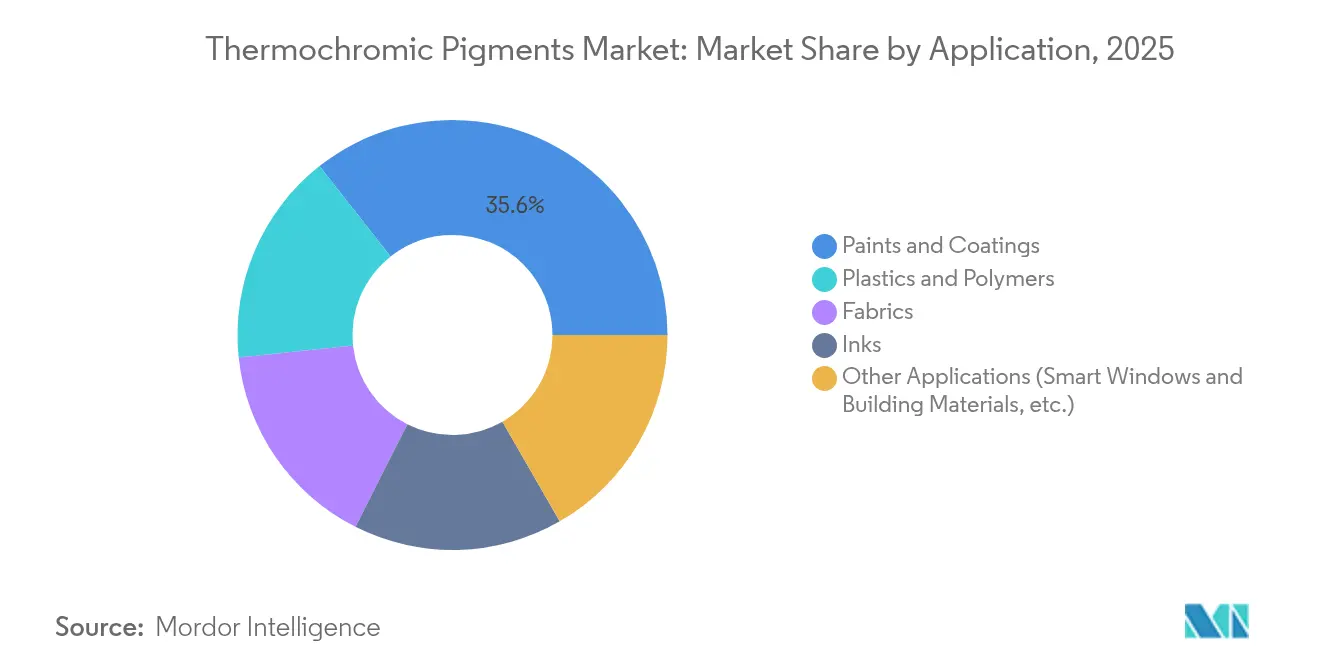

- By application, paints and coatings led with 35.62% revenue share in 2025; other applications, smart windows, and sensors, are poised for a 8.72% CAGR to 2031.

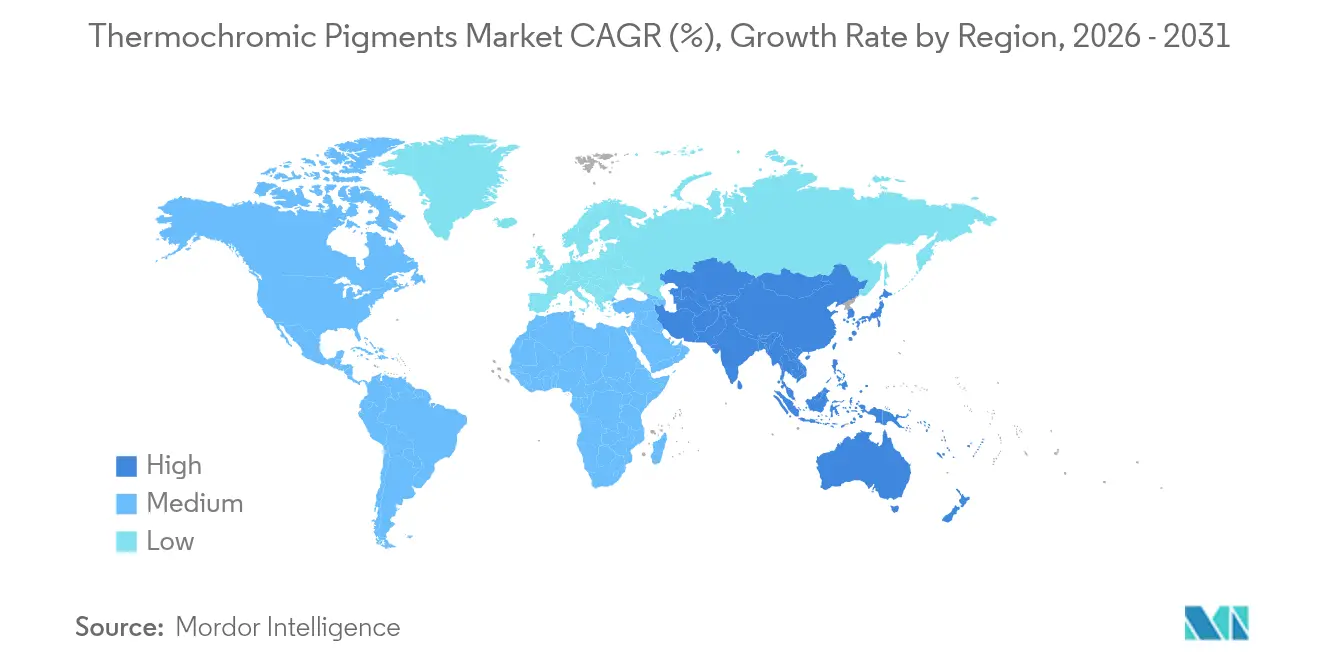

- By geography, North America held 29.35% share of the thermochromic pigments market in 2025, while Asia-Pacific is forecast to post the fastest 8.40% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermochromic Pigments Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for smart packaging | +2.1% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Rising demand from the smart textile industry | +1.8% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Growth of security inks for anti-counterfeit printing | +1.5% | Emerging markets worldwide | Short term (≤ 2 years) |

| Expansion of decorative paints and coatings | +1.3% | North America and Europe, growing in Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption of net-zero smart-window glazing | +0.9% | Europe and North America, early uptake in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Smart Packaging

Smart packaging continues to amplify demand as food and pharmaceutical suppliers adopt visible, temperature-sensitive indicators that confirm product integrity across logistics networks. Cold-chain breaks for vaccines, biologics, and ready-to-eat meals trigger irreversible color changes, offering quick, on-site verification for handlers and end users. Studies highlight that unprotected thermochromic polymer blends degrade in acidic conditions, prompting multilayer barriers and durable microcapsules that resist leaching. Regulatory agencies now insist on compliant seals for critical medications, raising baseline volumes of irreversible pigment labels in both mature and developing markets. Multinational pharma firms sourcing North American production spur early adoption, while smaller regional producers in Asia and Africa rely on visual indicators to offset inconsistent refrigeration infrastructure. The cost premium narrows as scale economies in microencapsulation improve, reinforcing the thermochromic pigments market trajectory.

Rising Demand from Smart Textile Industry

Smart textiles represent a high-growth frontier, with yarns embedding thermochromic capsules that shift hue in response to body heat, ambient temperature, or electrical input. Wet-spinning lines deposit capsules uniformly, producing fibers that cycle between colors thousands of times without fatigue. Solar-responsive fabrics reach 52.6 °C in direct sun, changing from orange to green to signal ultraviolet intensity. Integration with conductive threads enables on-demand color control via low-voltage circuits, opening avenues in sportswear, medical monitoring, and adaptive camouflage. Continuous pilot-scale production in China and South Korea lowers unit cost, while fashion houses in Europe trial limited-edition garments that merge aesthetic novelty with functional feedback. These developments underpin the long-term uplift embedded in the thermochromic pigments market.

Growth of Security Inks for Anti-Counterfeit Printing

Governments and brand owners intensify anti-counterfeit defenses, leveraging dual-readout thermochromic–fluorescent inks that combine color shifts with covert fluorescence[1]ACS Applied Materials & Interfaces, “Dual-Readout Thermochromic–Fluorescent Inks,” pubs.acs.org. Photothermal particles doped with Yb3+ activate pigments under narrowly defined near-infrared wavelengths, yielding codes that remain invisible until interrogated. The economic toll of counterfeiting, touching USD 1.8 trillion by 2022, underscores the urgency for multi-layered security. Natural pigments extracted from anthocyanidins furnish eco-friendly ink bases with high thermal stability, aligning with green procurement policies in Europe. The thermochromic pigments market thus gains from public-sector security printing and private-label brand protection.

Expansion of Decorative Paints and Coatings

In buildings, thermochromic coatings moderate solar heat gain, reflecting thermal energy in hot conditions and absorbing warmth in colder spells. Energy modeling shows potential HVAC savings of 48%. Architects deploy climate-responsive paints across façades and roofs to meet net-zero targets, while automotive OEMs apply color-shifting clear coats that also regulate cabin temperature. Silica-coated leuco dye pigments blended into cement mortars accelerate hydration, improving compressive strength without dulling color transitions. Demand accelerates across do-it-yourself channels as consumer interest in dynamic finishes rises, placing the thermochromic pigments market squarely within broader energy efficiency initiatives.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost versus conventional pigments | -1.7% | Global, acute in price-sensitive regions | Short term (≤ 2 years) |

| Narrow operational temperature range | -1.2% | Universal, especially extreme climates | Medium term (2-4 years) |

| Durability and light-fastness issues | -0.8% | Outdoor applications worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost with Respect to Conventional Pigments

Thermochromic grades often cost three to five times more than standard pigments, pressuring margins in volume-driven segments such as architectural coatings and commodity textiles. Microencapsulation demands tight process control and specialized reactors, elevating CAPEX for producers. Adoption hinges on proven return-on-investment through spoilage reduction or regulatory compliance for packagers and printers working on razor-thin budgets. Producers counter this restraint by scaling production, localizing supply chains, and adopting less expensive wall materials for microcapsules. These steps gradually close the price gap, especially as global volumes rise inside the thermochromic pigments market.

Narrow Operational Temperature Range

Many commercial systems switch within a limited −10 °C to 69 °C band, missing extreme cold in Nordic logistics or high-temperature industrial lines. Hybrid solutions stack multiple pigments or tune co-solvents, but complex formulations raise cost and complicate regulatory filings. Ongoing research and development explore polymeric matrices that broaden response windows without sacrificing color intensity. Field trials in Middle Eastern deserts and Arctic supply depots seek to validate performance, with success likely to unlock new addressable volumes for the thermochromic pigments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Irreversible variants dominate with 59.10% of the thermochromic pigments market share in 2025, reflecting their critical role in single-use pharmaceutical and food indicators. These products deliver permanent color shifts once specific thresholds are crossed, providing court-admissible evidence of temperature abuse. The segment’s large installed base across vaccine vials and blood bags ensures recurring demand, sustaining the overall thermochromic pigments market size for this category.

Reversible formulations nonetheless command attention with the highest 8.55% CAGR outlook. Continuous color cycling suits smart textiles, reusable data-loggers, and industrial process monitors. Durability gains from epoxy-silica hybrid capsules now permit more than 10,000 switch cycles without fading.

By Application: Paints and Coatings Leadership Amid Sensor Growth

Paints and coatings claim 35.62% of the thermochromic pigments market size in 2025, capitalizing on mature distribution and established performance records. Building envelope applications employ vanadium-oxide coatings that regulate indoor temperature and cut HVAC loads. Automotive suppliers embrace color-changing clear coats that signal hot-surface warnings, while consumer-goods makers apply pigments to baby spoons and mugs that reveal when contents are too hot. Coating formulators leverage UV blockers and antioxidants to extend outdoor life, solidifying leadership of this segment.

Other applications group smart windows, sensors, and construction materials, and deliver the fastest 8.72% CAGR through 2031. Smart glazing incorporates thermo-responsive layers that modulate light transmission, lifting building performance metrics. These emerging uses diversify revenue and help the thermochromic pigments market reach adjacent industries that previously relied on electronic or mechanical temperature indicators.

Geography Analysis

North America holds a 29.35% share of the thermochromic pigments market, anchored by stringent FDA mandates that demand visible temperature indicators for biologics, insulin, and specialty foods. Pharmaceutical majors cluster research and development, manufacturing, and distribution across the United States, driving early adoption and stable volumes. Canadian textile labs develop wearable sensors for elder care, and Mexican automotive plants trial thermochromic body panels to mitigate heat buildup.

Asia-Pacific posts an 8.40% CAGR from 2026-2031, the highest worldwide. Chinese fiber producers scale wet-spinning lines that integrate thermochromic capsules directly into polyester, lowering the cost per kilogram and widening access for mass-market apparel. Japan’s materials institutes are perfecting near-infrared responsive pigments suited to autonomous-electronics thermal management, and South Korea’s consumer-electronic giants are incorporating smart color films into foldable devices.

Europe remains a pivotal market, leveraging stringent building-energy codes and automotive safety regulations. German chemical firms devise catalyst-free synthesis routes that reduce solvent use, aiding environmental compliance. Fashion houses in France and Italy experiment with color-morphing couture that changes on runways under heat lamps. Though European growth is moderate compared with Asia-Pacific, regulatory certainty and green-technology funding schemes keep thermochromic pigments market penetration elevated.

Value Chain Analysis

The value chain starts with specialty inputs such as leuco dyes, color developers, and temperature-controlling solvents, then moves into microencapsulation wall materials (for example, polyurethane-type shells) and additives that improve UV resistance and compatibility in inks, polymers, and coatings. Pigment producers run emulsification and curing to form microcapsules, then compound or disperse them into masterbatches, inks, or coating systems to meet end-use requirements across packaging indicators, textiles, security printing, and building and automotive coatings. Quality control centers on particle-size distribution, capsule integrity, and calibrated switching temperatures, since end users need repeatable color change behavior for compliance and product integrity checks.

Access to specialized dye precursors and the limited number of suppliers with strong in-house microencapsulation know-how are key bottlenecks, because shell thickness and stability directly affect durability, light-fastness, and solvent resistance. Go-to-market typically mixes direct supply to industrial OEMs (packaging converters, security printers, automotive and coatings formulators) with regional distributors for smaller converters and formulators, while application labs and system compatibility testing (water-based, solvent-based, UV-cure) support customer qualification. Differentiation increasingly comes from vertical integration and formulation support that reduces scale-up failure risks, particularly where high-polarity solvents, outdoor exposure, and narrow temperature windows can erode performance.

Competitive Landscape

The thermochromic pigments market is moderately fragmented. Leading players invest heavily in microencapsulation research and development, ensuring tight particle-size distribution and superior fatigue resistance that meet demanding client specifications. They also partner with packaging automation firms to embed pigments into pre-qualified label substrates, cementing OEM stickiness. Mid-sized entrants concentrate on niche opportunities such as bio-based pigment walls and printable thermochromic circuitry. Traditional inorganic pigment suppliers explore bolt-on acquisitions or licensing deals to gain rapid entry.

Thermochromic Pigments Industry Leaders

Chromatic Technologies Inc.

SpotSee

Matsui International Company Inc.

NewColorChem

OliKrom SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

There is a clear whitespace in higher-precision, higher-processing-temperature formulations that extend thermochromic use beyond decorative effects into regulated cold-chain and industrial conversion settings. Product data published by iSuoChem in April 2026 points to tighter response precision (plus/minus 1 degree Celsius) and higher processing temperature tolerance (200 to 230 degrees Celsius), which supports opportunities in plastics compounding, durable labels, and packaging formats that face elevated heat histories during extrusion, lamination, or curing. That creates room for suppliers to offer microencapsulated systems with stronger resistance to UV, chemicals, and migration, while maintaining the calibrated switching thresholds needed for food and pharmaceutical handling.

Another near-term opportunity is combining physical color-change indicators with digital traceability for life sciences and food shippers, where buyers are standardizing on solutions that include visual pass/fail checks and chain-of-custody documentation. Building-envelope and smart glazing programs focused on passive solar regulation also keep R&D aimed at thermochromic coatings with improved durability, spectral selectivity, and tuned transition temperatures. Across these end uses, demand for non-toxic, water-based, and lower-solvent systems aligns product development with stricter chemical safety expectations and procurement screening, favoring suppliers that can document both compliance and performance consistency at scale.

Recent Industry Developments

- April 2026: SpotSee expanded its portfolio with three QR-enabled indicators, FreezeSafe QR, TiltWatch XTR QR, and ShockWatch Label QR. The additions add scannable, asset-level identification to established visual indicator formats.

- March 2026: SpotSee and Controlant announced a strategic collaboration to connect SpotSee indicator technology with Controlant's real-time monitoring for life sciences shipments. The collaboration supports blended deployments that pair simple visual checks with connected visibility and last-mile documentation.

- July 2024: Merck KGaA finalized the divestiture of its Surface Solutions business unit, including pigment solutions, to Global New Material International for USD 721 million. The transaction consolidated functional and effect pigment capabilities under GNMI, reshaping competitive positioning and product portfolio depth for customers sourcing specialty pigments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from thermochromic pigments that change color with temperature and are sold as pigment systems for use in manufacturing and printing applications, across major regions.

Scope exclusions: We exclude finished end-products that only contain the pigment (such as printed packaging or coated consumer goods) and we also exclude non-pigment thermochromic materials when they are sold as standalone functional layers.

Segmentation Overview

- By Type

- Reversible

- Irreversible

- By Application

- Plastics and Polymers

- Paints and Coatings

- Fabrics

- Inks

- Other Applications (Smart Windows and Building Materials, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and set realistic guardrails for the model before numbers were finalized. We reviewed public manufacturing and trade signals to see where thermochromic pigment consumption is likely to be concentrated, then checked end-use indicators that tend to move volumes up or down.

Key references included non-paywalled sources such as UN Comtrade for trade flows, USITC and Eurostat trade statistics for cross-checking, US EPA and ECHA pages for regulatory cues tied to chemical use, and peer-reviewed journal articles that describe pigment technology adoption and durability limits. We also used company annual reports, investor decks, product catalogs, association websites, and trusted press coverage to validate application mixes. In addition, a paid subscription for company financials and news, plus a patent database, supported tracking of capacity moves and innovation intensity. These examples are not exhaustive, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with pigment producers, distributors, formulators, and downstream users in inks, coatings, plastics, and textiles. We used these discussions to confirm typical selling formats (microencapsulated versus other deliveries), price bands by application, adoption triggers, and regional demand differences, and then to stress-test assumptions that were weak in public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 21% | Managers: 57% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable pigment demand from end-use output and conversion logic, and then it is narrowed to thermochromic penetration by application. For example, coatings and ink activity, plastics processing output, and packaging and label production trends were used to shape where pigment demand is created, followed by temperature-indicator and design-use penetration checks.

To keep totals realistic, we corroborated the result with selective bottom-up approximations such as sampled supplier revenue ranges, channel checks with distributors, and volume times average selling price calculations for common application sets. Inputs used in the model included reversible versus irreversible usage tendency, microencapsulation adoption (which shifts usable loadings), typical dosage rates in inks and coatings, application mix across plastics, textiles, and printing, and observed price movement by grade and performance. Where direct volume data was missing, gaps were handled by using proxy series like packaging output and coatings production, and then adjusting with interview-based correction factors.

For forecasting, scenario analysis was applied around adoption speed in smart packaging and temperature-sensitive labels, with supporting checks from macro indicators like manufacturing output and consumer packaging volumes. Assumptions were reviewed with experts so that price progression, penetration changes, and regional growth patterns stayed aligned with what suppliers and buyers are seeing.

Data Validation & Update Cycle

Validation is done through repeated cross-checks so that one data source does not overly drive the outcome. We compare the model output against independent signals such as trade direction, downstream production trends, and typical pricing bands, then re-check any large variances at the region and application level.

Before sign-off, anomalies are reviewed in steps, starting with unit consistency, then currency and inflation handling, and finally assumption review by a second analyst. If a major capacity change, regulation shift, or sharp raw material movement is observed, experts are re-contacted to confirm the likely market impact. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Thermochromic Pigments Market Size Versus Other Published Estimates

Published market sizes for thermochromic pigments can look far apart even when they appear to cover the same topic. In our work, the spread usually comes from what is counted as a pigment sale versus a finished product, which year is treated as the starting point, and how pricing and adoption are carried forward into the forecast window.

Trade direction checks, downstream coatings and printing activity, and interview-confirmed price bands are used to keep Mordor Intelligence's estimate tied to pigment-system revenues rather than broader smart-material or finished packaging values. Differences also come from how firms treat microencapsulated deliveries (counting only the pigment system value versus a broader formulation value), what they assume for penetration into packaging and labels, and whether currency conversion timing is aligned to the same year of pricing and volumes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.32 B (2026) | |

| Global Consultancy A | USD 2.14 B (2025) | Uses an earlier reference year and can mix in different pricing timing, which shifts the value when raw material-linked prices moved between years. |

| Industry Publisher B | USD 0.63 B (2025) | Applies a narrower scope that appears to focus on select pigment chemistries or forms, which leaves out part of the addressable pigment-system demand across coatings, plastics, and inks. |

Seen together, the estimates mainly diverge because of scope boundaries and how price and penetration are applied in the starting year. By keeping the model traceable to application demand signals and realistic price bands, the final number stays easier to explain, audit, and refresh when new capacity or adoption evidence shows up.

Key Questions Answered in the Report

What is the current thermochromic pigments market size?

The thermochromic pigments market size is valued at USD 2.32 billion in 2026 and is set to reach USD 3.35 billion by 2031 at an 7.62% CAGR.

Which region leads the thermochromic pigments market?

North America leads with 29.35% revenue share in 2025, supported by stringent pharmaceutical and food-safety regulations.

Which segment is growing fastest in the thermochromic pigments market?

The “other applications” segment, covering smart windows, sensors, and building materials, shows the quickest expansion at a 8.72% CAGR through 2031.

Why are irreversible thermochromic pigments in high demand?

Irreversible pigments hold 59.10% market share because they provide permanent evidence of temperature breaches, a necessity for vaccine, biologic and food safety compliance.

What is the main restraint for wider adoption of thermochromic pigments?

High-cost relative to conventional pigments remains the principal barrier, although scaling and process improvements are gradually narrowing the price gap.

Page last updated on: