Electrochromic Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

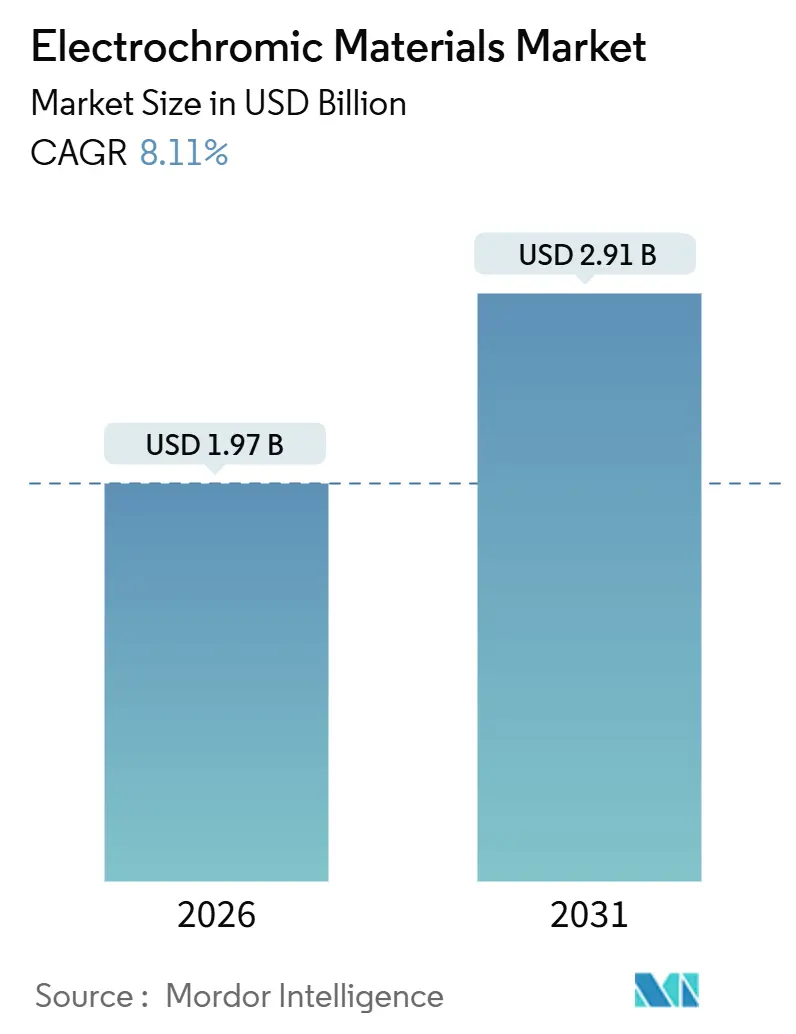

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

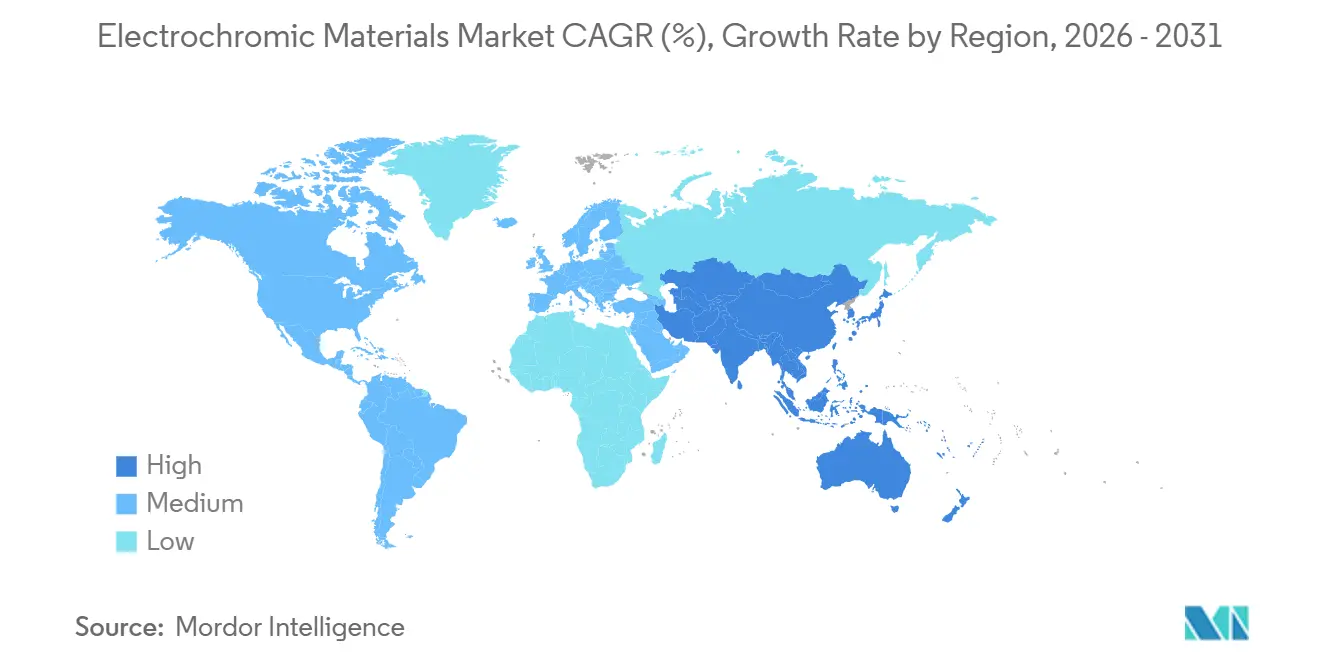

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrochromic Materials Market Analysis by Mordor Intelligence

The Electrochromic Materials Market size is estimated at USD 1.97 billion in 2026, and is expected to reach USD 2.91 billion by 2031, at a CAGR of 8.11% during the forecast period (2026-2031). Stricter building-energy codes in Europe and the United States, expanding tariff barriers that favor local production, and fast-switching automotive and retail-display use cases are refocusing procurement from optional sustainability upgrades to mandated performance components. Buildings now specify dynamic glazing to meet carbon-reduction targets at lower lifetime cost than mechanical shading, while automakers integrate electrochromic sunroofs and instrument clusters to offset battery-induced weight and heat loads. Supply-chain reshoring continues as Section 301 duties on Chinese glass and the EU Critical Raw Materials Act drive additional North American and European capacity. Despite high upfront prices, payback periods keep shortening as electricity tariffs rise and financing programs reward near-zero-energy envelopes. Competitive intensity stays moderate, with the top five suppliers controlling roughly 60% of revenue but facing new polymer-film challengers that promise roll-to-roll cost parity.

Key Report Takeaways

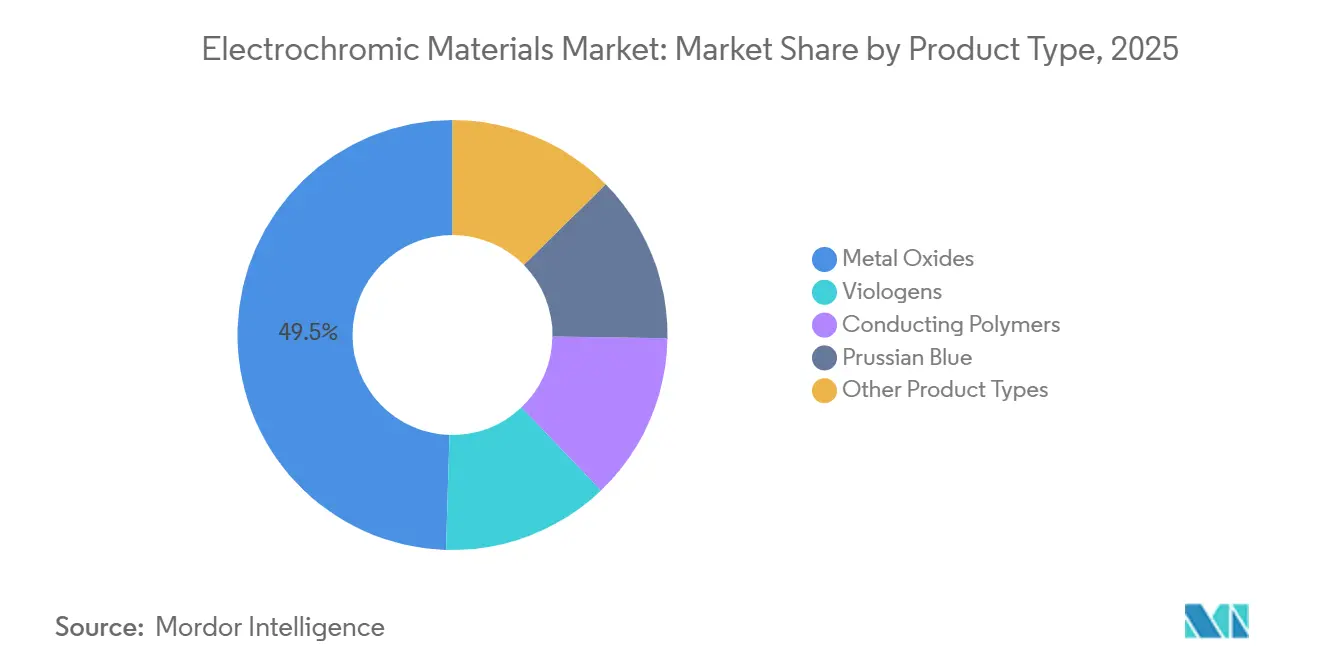

- By product type, metal oxides led with a 49.51% electrochromic materials market share in 2025; conducting polymers are advancing at a 10.71% CAGR to 2031.

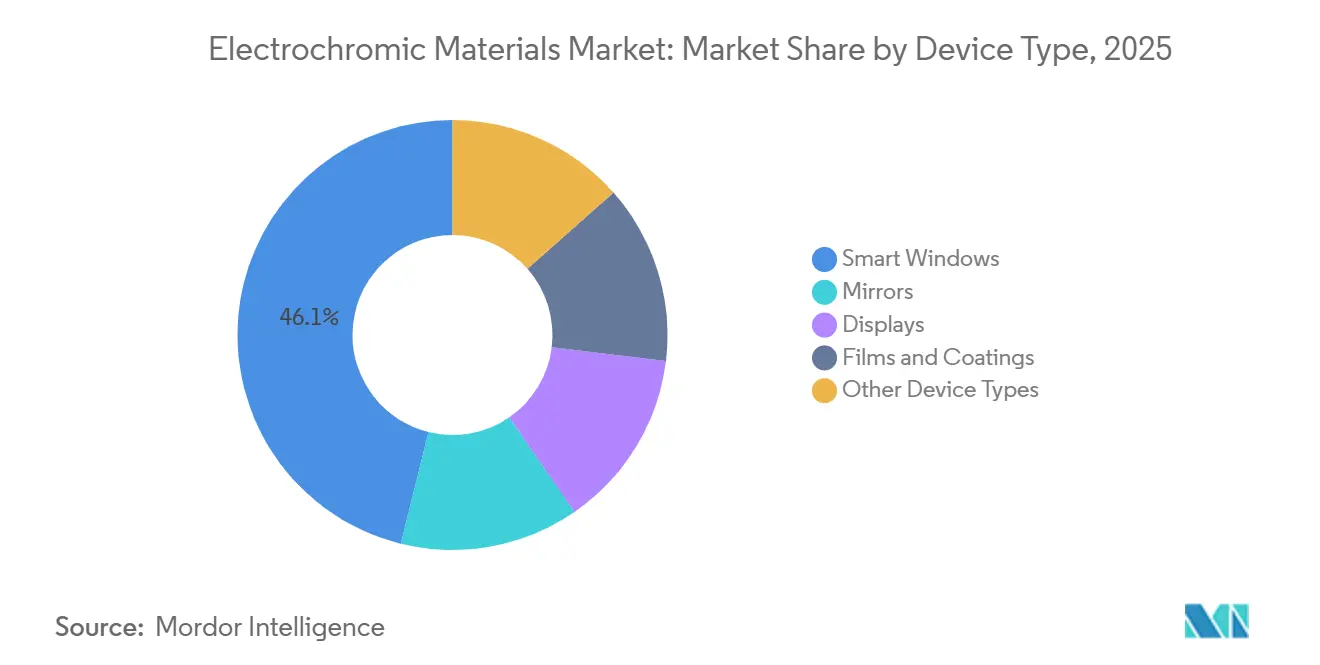

- By device type, smart windows captured 46.13% of revenue in 2025, while displays are set to grow at an 11.12% CAGR through 2031.

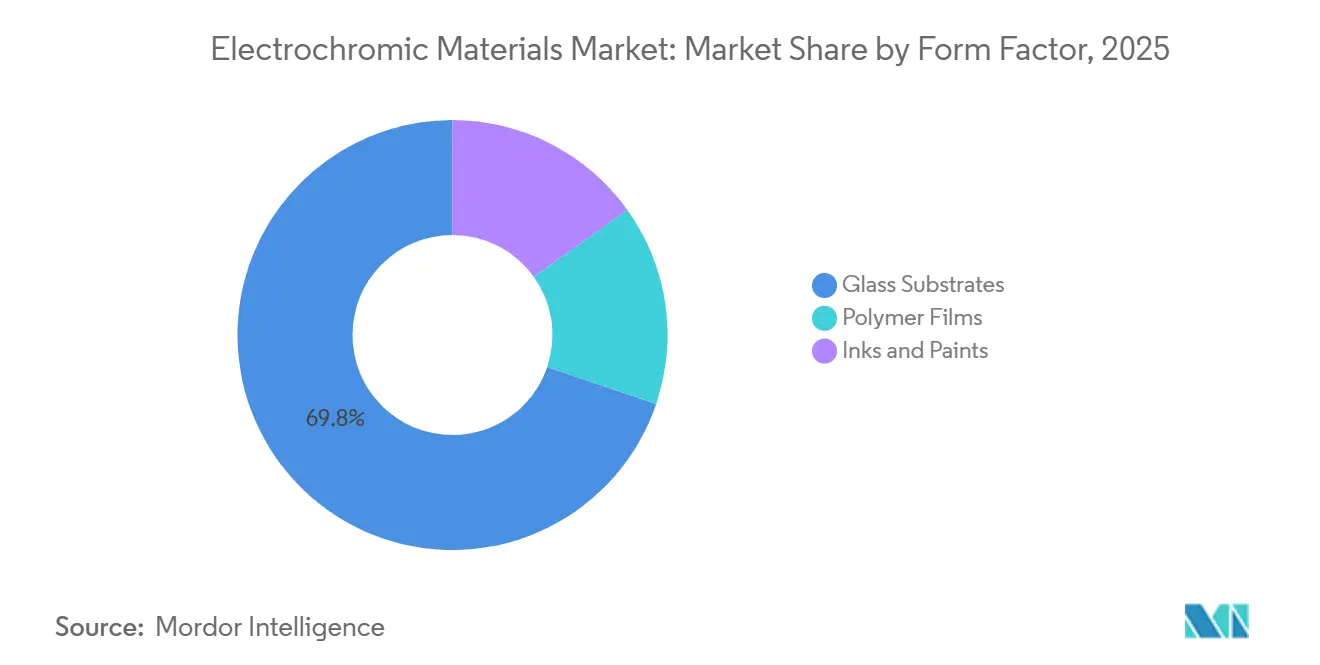

- By form factor, glass substrates accounted for 69.80% of the electrochromic materials market size in 2025; polymer films will expand at a 10.98% CAGR between 2026-2031.

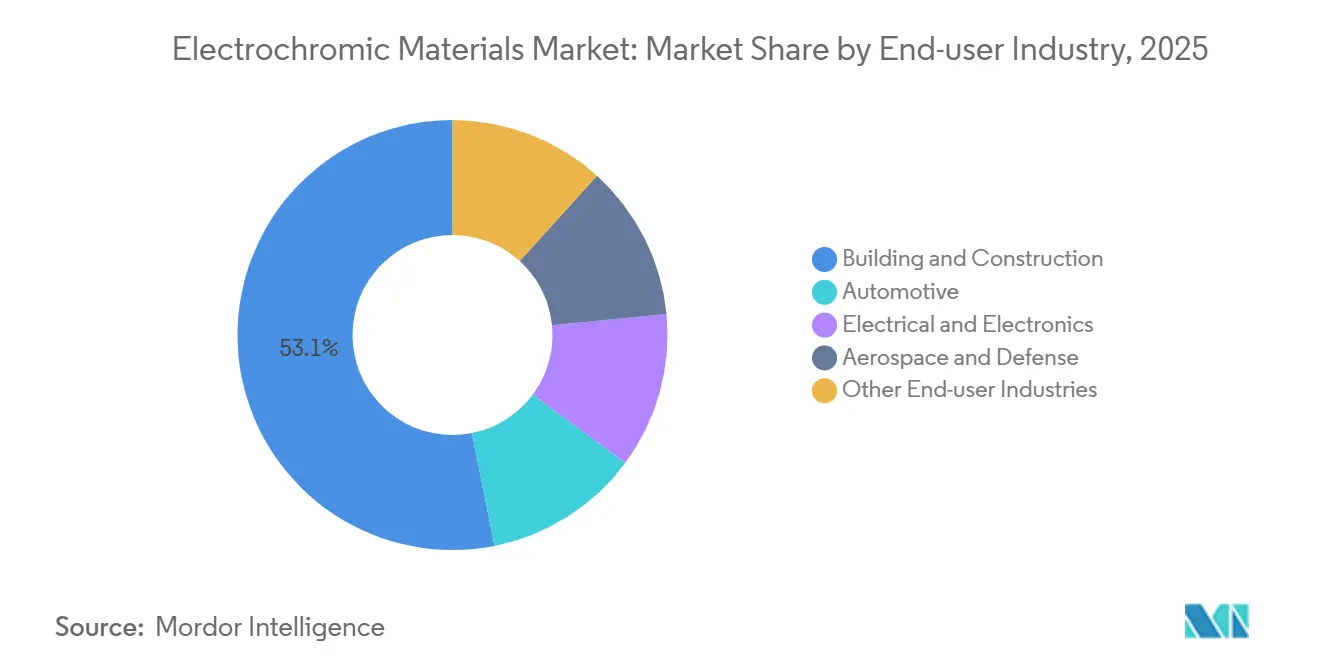

- By end-user industry, building and construction held 53.12% revenue in 2025 and is forecast to post a 10.88% CAGR, outpacing automotive.

- By geography, Europe retained 33.45% regional revenue in 2025; Asia-Pacific is projected to register the fastest 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrochromic Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Efficiency Regulations Accelerating Smart-Window Adoption | +2.1% | Europe, North America, APAC (China, Japan, South Korea) | Medium term (2-4 years) |

| Automotive Demand for Auto-Dimming Mirrors and Panoramic Sunroofs | +1.8% | Global, with concentration in North America, Europe, China | Short term (≤ 2 years) |

| Aerospace Window Upgrades for Weight and Glare Reduction | +0.9% | Global, led by North America (Boeing, Airbus supply chains) | Long term (≥ 4 years) |

| Self-Powered Electrochromic Smart Windows Integrating Solar Harvesters | +1.4% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Tariff-Driven Reshoring of Electrochromic Material Supply Chains | +1.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations Accelerating Smart-Window Adoption

European, U.S. and U.K. building codes now recognize dynamic glazing as a primary compliance route rather than a discretionary feature, compressing payback periods and triggering large scale retrofits[1]U.S. Environmental Protection Agency, “ENERGY STAR Version 7.0 Final Criteria,” energystar.gov . France’s RE2020 grants a 15% carbon-offset credit for façades that reduce HVAC runtime by 20%, a threshold met by electrochromic glass. ENERGY STAR Version 7.0 created a “dynamic performance” tier that only electrochromic or suspended-particle devices satisfy. NREL field work in 2024 showed that Phoenix office retrofits cut simple payback to 7.2 years as peak-demand charges escalated. The UK Future Homes Standard mandates 75% lower operational carbon from 2025, indirectly boosting electrochromics as insulation-only packages become insufficient.

Automotive Demand for Auto-Dimming Mirrors and Panoramic Sunroofs

Premium electric vehicles now rely on film-based electrochromic roofs that switch in under 90 seconds, addressing legacy glare complaints. GM’s 2024 patent for zone-specific windshields illustrates the shift toward segmented dimming that preserves driver sightlines while shading passengers. Large-format prototypes exceeding 1.5 m × 1.6 m confirm manufacturing scale-up, yet penetration in mass-market trims remains below 5% because the USD 800-1,200 adder competes with battery-range upgrades.

Aerospace Window Upgrades for Weight and Glare Reduction

Boeing 787 operational data indicate a 15 kg per aircraft weight drop versus mechanical shades, trimming annual fuel cost by USD 3,000 at 2024 prices. Airlines credit electrochromic dimming for fewer premium-cabin glare complaints on trans-Pacific sectors. FAA endurance certification of 50,000 switching cycles narrows the supplier field, reinforcing high-margin contracts for qualified vendors.

Self-Powered Electrochromic Smart Windows Integrating Solar Harvesters

Perovskite-assisted stacks demonstrated 12.3% conversion efficiency while preserving 45% visible-light transmission, eliminating external wiring for retrofit sites. NREL’s luminescent concentrator prototype generated 18 mW/m², delivering two switch cycles per hour without grid power. Thermoelectric layers scavenging temperature gradients broaden applicability for off-grid cabins and heritage buildings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost Versus Conventional Coated Glass | -1.5% | Global | Short term (≤ 2 years) |

| Cycling-Stability and Durability Challenges | -0.8% | Global, particularly harsh-climate regions (Middle East, Nordic countries) | Medium term (2-4 years) |

| Digital Rear-View Mirrors Eroding Automotive EC Mirror Demand | -0.6% | North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Unit Cost Versus Conventional Coated Glass

Installed prices averaging USD 85 per ft² dwarf the USD 22 per ft² baseline for low-e double glazing, limiting adoption to Class-A and high-end residential projects[2]Lawrence Berkeley National Laboratory, “Window Technology Cost Benchmark,” windows.lbl.gov . Only 12% of U.S. developers specify electrochromics for speculative offices, though build-to-suit projects accept higher capex when operational savings accrue to tenants. Bankruptcy of View Inc. in 2024 highlights the cash-burn risk of volume-driven cost reduction without scale.

Cycling-Stability and Durability Challenges

W₃O₈ systems typically retain 80% modulation after 50,000-100,000 cycles, equating to 7-14 years of daily switching, below envelope life expectations. Conducting-polymer films degrade faster under 85 °C/85% RH stress, losing 40% contrast after 10,000 cycles. Hermetic edge-seals and dual-cathode stacks push lab performance beyond 200,000 cycles, yet absence of an IEC durability standard complicates warranty underwriting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metal Oxides Hold Scale, Polymers Rewrite Flexibility Rules

Metal oxides maintained 49.51% revenue in 2025, anchored by tungsten-trioxide’s 60-70% light-modulation range and more than 50,000 cycle life. Hierarchically porous W₃O₈ films achieved sub-5 s switching, opening dashboard opportunities previously reserved for faster chemistries. Conducting polymers grow at 10.71% as OEMs and retrofitters adopt roll-to-roll PEDOT and PANI layers that cut manufacturing costs 40% and bend onto curved pillars. However, additional ultraviolet-barrier coatings add USD 8-12 per m², tempering the near-term price narrative. Viologen and Prussian blue niches persist where less than 1 s response or anti-glare performance outweighs lifetime concerns.

The electrochromic materials market now evaluates substrate flexibility as rigorously as contrast ratio. Ricoh’s curved A-pillar film shows how PEDOT overcomes brittle-oxide cracking, whereas tungsten systems excel in 30-year façade warranties. Hybrid composites under investigation promise oxide-level durability with polymer-style processability, yet synthesis complexity and licensing hurdles stall large-scale launch.

By Device Type: Smart Windows Dominate, Displays Accelerate

Smart windows captured 46.13% revenue in 2025 on the back of multi-thousand-square-meter building orders, but displays will post an 11.12% CAGR thanks to sunlight-readable automotive clusters and outdoor retail signage. Electrochromic displays maintain 10:1 contrast under 100,000 lux, outperforming transflective LCDs, and crown-labeled prototypes transition fully in less than 2s. Mirrors lose share as camera-based rear vision scales, yet after-market commercial vehicles still specify auto-dimming glass. Retrofit films and coatings furnish a new volume tier as Polytronix cuts install costs to USD 40 ft². Multi-function panels that fuse dimming with edge LEDs blur device boundaries and raise content per square meter.

By Form Factor: Glass Remains Anchor, Polymer Films Unlock Retrofit

Glass substrates held 69.80% in 2025, backed by proven 92% performance retention after 10 years in Arizona field tests. They dominate new-build façades where 25-year warranties outweigh weight penalties. Polymer films, expanding at 10.98% CAGR, slash unit mass to 1.2 kg/m² and enable self-adhesive retrofits. Municipal pilots such as New York City’s 50,000 m² curtain-wall trial registered a 22% peak-cooling cut without façade disruption. Ink-based coatings service low-cycle military and anti-counterfeiting uses where USD 5 per m² material costs trump longevity.

Glass and film paths will coexist: rigid units for premium curtain walls, lightweight laminates for automotive roofs, and peel-and-stick sheets for existing towers constrained by tenant occupancy or historical façades.

By End-user Industry: Buildings Drive Volume, Automotive Re-balances Priorities

Building and construction commanded 53.12% revenue in 2025 and will pace ahead at a 10.88% CAGR as Germany’s KfW subsidy, France’s embodied-carbon cap and EU public-building renovation mandates converge. A Frankfurt office retrofit cut cooling energy 28% and secured a 12% rent premium. The electrochromic materials market size in commercial real estate is consequently projected to maintain moderate growth through 2031. Automotive’s share slips as EV makers allocate budget to battery range and camera mirrors encroach on legacy dimming units. Aerospace and defense demand is also growing due to FAA certification barriers and USD 1,200 per-window pricing. Electronics and wearables stay experimental but receive persistent R&D as foldable devices require bend-tolerant displays.

Geography Analysis

Europe delivered 33.45% revenue in 2025, propelled by the EPBD recast that obliges 3% annual public building retrofits and Germany’s KfW Efficiency House 40 incentives. France’s RE2020 and the U.K.’s Future Homes Standard push electrochromic uptake by setting carbon ceilings that static glazing cannot breach. Nordic passive-house adopters exploit EC glass for winter gain and summer shading, while Italy and Spain lag as lower electricity tariffs prolong payback.

Asia-Pacific, advancing at an 11.12% CAGR, benefits from China’s import-substitution push under Made in China 2025, Japanese OEM integration of electrochromic roofs, and South Korean display giants turning to sunlight-readable e-paper. India’s 2024 Energy Conservation Building Code offers a voluntary dynamic-glazing credit, setting the groundwork for future demand. Singapore’s Green Mark Platinum pathway rewards 20% HVAC energy cuts, fostering early municipal adoption.

In North America, California’s Title 24 updates and New York’s Local Law 97 impose carbon penalties that favor dynamic glazing, while federal net-zero mandates create a captive demand pipeline through 2030. Section 301 tariffs increase landed costs for Chinese imports by 25%, spurring Saint-Gobain’s USD 45 million Minnesota expansion. Canada’s Pan-Canadian Framework backs provincial code harmonization, with British Columbia and Ontario specifying EC glass in public infrastructure. Latin American and Middle-East uptake remains project-driven in prestige office towers and megacity developments like Saudi Arabia’s NEOM.

Regulatory Landscape

Adoption of electrochromic materials is shaped by building-energy policy and performance testing requirements that influence which products qualify for glazing programs in both buildings and vehicles. In Europe, the Energy Performance of Buildings Directive (Directive (EU) 2024/1275, consolidated through 2026) reinforces national building renovation plans and the long-term shift toward a zero-emission building stock by 2050, which supports compliance-driven pull for dynamic glazing in retrofits and public-building upgrades. On the chemicals side, access for organic electrochromic chemistries is governed under the EU REACH framework administered by ECHA, covering substances and intermediates used in systems such as viologen derivatives and requiring registration and transparency for qualifying volumes.

Standardization is also tightening the testing and qualification pathways that suppliers must meet for both architecture and vehicles. ISO 18543:2021 provides an international durability and accelerated ageing framework for electrochromic glazings in building applications, while ASTM E2141-21 is a widely referenced US method for accelerated aging of electrochromic devices in sealed insulating glass units. In road vehicles, China issued GB/T 46023.1-2025 for organic electrochromic glazing, which took effect on February 1, 2026 and sets more formal compliance expectations for smart automotive glazing supply chains and component qualification.

Value Chain Analysis

The value chain begins with raw materials and specialty inputs, including tungsten-based oxides, lithium-based electrolytes, viologens, conductive polymers such as PEDOT/PANI, plus barrier and interlayer films. This is followed by chemical synthesis and formulation, thin-film deposition (sputtering and coating, and roll-to-roll for films), and cell stack integration. Downstream steps then include lamination into glass units or flexible substrates, edge sealing and electrical interconnection, and device-level assembly into smart windows, mirrors, sunroofs, and displays. Reliability and qualification testing, including accelerated aging and cycling, acts as a gating step for architectural warranties and automotive programs, shaping supplier selection and limiting rapid substitution.

Commercialization and scale depend on partnerships between material suppliers, device developers, and Tier-1 or glazing integrators. One example is the Mativ Holdings, Inc. and Miru Smart Technologies collaboration, which includes a May 2025 first commercial purchase order for an advanced TPU interlayer film used in Miru eWindow devices and a January 2026 equity investment intended to accelerate commercial production for automotive platforms. Distribution routes differ by form factor, with architectural glass typically moving through fabricator and façade-contractor networks, while automotive programs concentrate volume through OEM and Tier-1 procurement that prioritizes consistent switching performance, curvature-capable substrates, and robust sealing processes.

Competitive Landscape

The top five players - Gentex, Saint-Gobain, ChromoGenics, View and Guardian - control roughly 60-65% of revenue, placing the electrochromic materials market at a moderate-concentration midpoint. Gentex holds more than 90% of auto-dimming mirrors due to vertically integrated gel-electrolyte lines that compress cost curves unreachable for newcomers. Saint-Gobain leverages a 3,000-fabricator network to integrate EC units into curtain walls, yet faces retrofit-film competition from Crown Electrokinetics, whose DynamicTint targets the existing stock underserved by panel suppliers. Cost-leadership strategies emerge in Asia as KIBING’s 1.2 million m² Shandong line undercuts import pricing.

Innovation emphasis shifts from 70% contrast plateaus to form-factor versatility and self-powered stacks. Halio (Saint-Gobain-backed) patents dual-ion layers to drive sub-3-minute switching, while EControl-Glas integrates edge LEDs for dual-use façades. Supply-security moves accelerate: AGC’s 2024 tungsten contract with a Portuguese mine hedges against China’s 85% refining dominance. Industry consolidation is likely as polymer-film capex and warranty-backed durability trials exceed the financial reach of niche entrants unless they partner with automotive or building-materials majors.

Electrochromic Materials Industry Leaders

GENTEX CORPORATION

Saint-Gobain

View, Inc.

ChromoGenics

Guardian Glass

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is emerging at the intersection of compliance-led building renovation and product differentiation around aesthetics, durability, and embodied-carbon documentation. EPBD-driven renovation planning in Europe, along with tightening energy-performance compliance routes in the United States and United Kingdom, is moving electrochromics from optional upgrades toward specification-grade façade components. Design objections remain a practical barrier in some segments, so product progress such as neutral-color electrochromic glass is directly relevant to premium commercial projects. Procurement patterns also reflect localization incentives and tariff frictions that favor regional capacity and shorter lead times for coated substrates, interlayers, and assembled units.

Automotive offers a parallel route where standardized qualification and supply agreements can turn prototypes into repeatable programs. China introducing GB/T 46023.1-2025 on February 1, 2026 creates a formal test and requirement framework for organic electrochromic automotive glazing, which can reduce sourcing ambiguity for OEMs and speed supplier onboarding. On the demand side, evidence of momentum includes ChromoGenics securing a 4,000 m2 ConverLight dynamic glass order for a Hong Kong development (June 2026) and Mativ expanding its relationship with Miru via an equity investment to accelerate eWindow commercialization for automotive platforms (January 2026), reinforcing a shift toward higher-volume programs tied to validated manufacturing routes and qualified material stacks.

Recent Industry Developments

- April 2026: Gentex signed a cooperation agreement with Antolin to bring next-generation electrochromic dimmable sun visors to the European automotive market. The partnership links Gentex electrochromic capability with a major interior-systems supplier, moving dimmable components beyond mirrors and toward integrated cabin systems for OEM platforms.

- January 2026: Mativ Holdings announced an equity investment in Miru Smart Technologies and expanded their partnership to accelerate commercialization of Miru eWindow electrochromic technology for automotive markets. The agreement strengthens upstream material supply and industrialization support for compound-curved devices that require specialized interlayers and scalable production processes.

- January 2025: SageGlass (Saint-Gobain) launched RealTone, an electrochromic glass offering positioned around more neutral aesthetics by reducing the traditional blue hue. This product-direction emphasis targets a frequent architectural adoption barrier and supports specification in premium facades where color fidelity is central to design approval.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers materials that reversibly change tint or light transmittance when a small voltage is applied. Revenue in this study is for the electrochromic material layer and related material forms sold into commercial devices.

Scope exclusions: it excludes non-electrochromic smart glazing technologies such as suspended particle devices, PDLC, and photochromic or thermochromic materials.

Segmentation Overview

- By Product Type

- Metal Oxides

- Viologens

- Conducting Polymers

- Prussian Blue

- Other Product Types

- By Device Type

- Smart Windows

- Mirrors

- Displays

- Films and Coatings

- Other Device Types

- By Form Factor

- Glass Substrates

- Polymer Films

- Inks and Paints

- By End-user Industry

- Building and Construction

- Automotive

- Electrical and Electronics

- Aerospace and Defense

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a clear demand map for where electrochromic materials are actually consumed, then matching it with supply-side signals. We use public sources such as USGS mineral statistics, UN Comtrade trade flows, US DOE building energy publications, NREL technical reports, and standards and code references from groups such as ISO or ASTM, which help define use cases and adoption constraints.

To keep the model grounded, we also review company annual reports and investor presentations, check patent databases for filing trends, and review reputable press coverage for new capacity, product launches, and building code changes. Paid subscriptions are used only where public disclosure is thin, mainly for company financials and shipment or contract tracking. These desk sources are not exhaustive, and many additional public documents were reviewed to compile data, validate assumptions, and close open questions.

Primary Interviews and Surveys

Primary work is used to stress-test what desk research cannot confirm well, mainly real adoption pace, typical pricing movement for material systems, and qualification timelines by end use. We spoke with a mix of material suppliers, device and component stakeholders, and downstream buyers across APAC, EMEA, and the Americas, so gaps from secondary data could be addressed and key assumptions triangulated before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 41% |

| Mid tier: 50% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 17% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where building and automotive demand pools are reconstructed from installation activity, glazing and mirror penetration, and regional construction and vehicle output indicators, then converted into material value using intensity factors and price bands that reflect current market ranges. To reduce drift, we corroborate totals with selective bottom-up approximations such as sampled supplier revenue splits, channel checks by form factor (glass substrates, polymer films, inks and paints), and spot checks of average selling price ranges for common material systems.

Key inputs used in the model include smart window and retrofit adoption rates by region, floor space additions and energy code tightening signals, automotive mirror and glazing fitment trends, material yield and scrap assumptions during coating, and observed price progression as volumes scale. For forecasting, we run scenario analysis around construction cycles and qualification timing, supported by expert views on how quickly projects move from pilots to larger rollouts. Where bottom-up visibility is incomplete, conservative fill factors are applied and then revisited during validation so the gaps do not inflate the market.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals such as end-use installation activity, trade movements for key inputs, and the pace of announced project pipelines. If a region or application shows an unusual jump, we revisit the underlying drivers, re-check the conversion math, and re-contact selected interviewees to confirm whether it is real demand or a timing artifact.

Before sign-off, the workbook goes through multi-step analyst reviews where assumptions, units, and currency conversions are re-verified, followed by a final variance check against prior iterations. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity changes, policy shifts, or demand shocks. Right before delivery, a final pass is completed so clients receive the most current view.

Mordor Intelligence's Electrochromic Materials Market Size Compared With Other Published Estimates

Published market values for electrochromic materials can differ because teams do not always count the same material boundary, and they also choose different years and pricing logic for smart windows versus mirrors and displays. The benchmark table provides a quick view of the spread and why it varies.

The table shows a noticeable gap versus two other published values, and in Mordor Intelligence's model the figure is tied to electrochromic materials revenue supplied into devices, while excluding adjacent smart glazing technologies like SPD and PDLC, which can raise totals when bundled. Differences can also come from whether a source assumes an aggressive retrofit adoption curve, uses global average prices without regional mix shifts, or converts currencies using a different timing window. When these assumptions are not checked with end-user or installer feedback, the final value can move meaningfully.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.97 B (2026) | |

| Trade Publisher A | USD 2.58 B (2024) | Uses a combined "materials and devices" framing and reports an earlier year, which can blend device value with materials and make comparisons to materials-only scopes uneven. |

| Industry Outlook B | USD 2.30 B (2025) | Applies a longer horizon forecast and a broader industry definition with simplified price escalation, which can lift the near-term number if faster adoption is assumed. |

Taken together, the comparison points to scope and pricing assumptions as the biggest drivers of variation, not only arithmetic differences. Our approach stays traceable to end-use demand pools, realistic penetration and yield factors, and interview-led checks on adoption timing, which keeps the estimate explainable and repeatable.

Key Questions Answered in the Report

How large is the electrochromic materials market?

It reached USD 1.97 billion in 2026 and is forecast to attain USD 2.91 billion by 2031.

What is the expected CAGR for electrochromic materials through 2031?

The market is projected to grow at an 8.11% CAGR between 2026 and 2031.

Which end-user segment drives most revenue?

Building and construction leads with 53.12% revenue in 2025 and the fastest 10.88% CAGR outlook.

Why are polymer-film electrochromics gaining ground?

Roll-to-roll processing cuts manufacturing cost and weight, enabling retrofit films and curved automotive applications.

Page last updated on: