Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.91 Billion |

| Market Size (2026) | USD 4.97 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 1.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Textile Market Analysis by Mordor Intelligence

The Thailand Textile Market size is expected to grow from USD 4.91 billion in 2025 to USD 4.97 billion in 2026 and is forecast to reach USD 5.37 billion by 2031 at 1.56% CAGR over 2026-2031.

Domestic tourism, Board of Investment (BOI) incentives for machinery upgrades, and fast-growing e-commerce are sustaining moderate growth even as wage inflation and cheaper imports weigh on margins. Large, vertically integrated mills are adopting automated looms and digital printing to lower unit costs, while small and medium enterprises (SMEs) focus on short runs for domestic brands. Technical-textile demand from automotive and medical clusters is widening the customer base, and local polyester and viscose capacity is shortening raw-material lead times. The Thailand textile market is therefore repositioning from volume-driven apparel to value-oriented industrial applications.

Key Report Takeaways

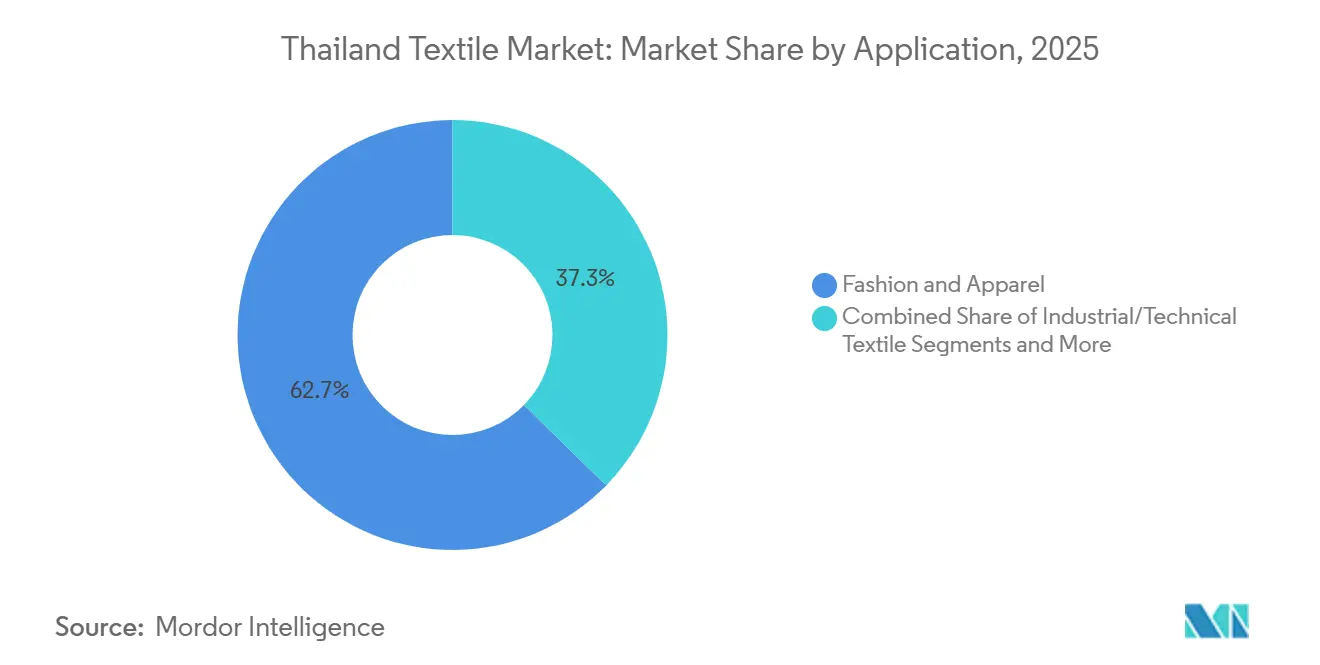

- By application, Fashion and Apparel led with 62.67% revenue share in 2025; Industrial/Technical Textiles are forecast to expand at a 1.95% CAGR through 2031.

- By raw material, Natural Fibers held 61.86% of the Thailand textile market share in 2025, while Synthetic Fibers are projected to grow at a 1.86% CAGR to 2031.

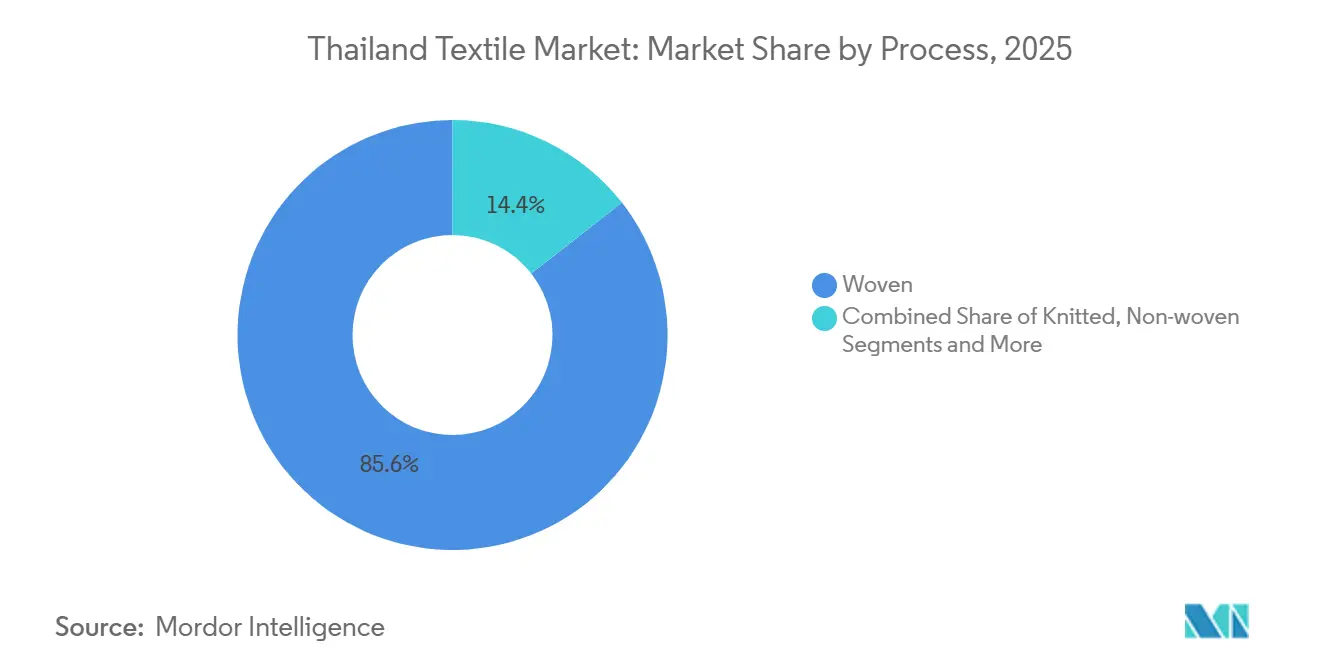

- By process, Woven fabrics captured 85.56% of 2025 output; Nonwovens are advancing at a 1.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic tourism–led apparel rebound | +0.4% | Bangkok, Phuket, Chiang Mai | Short term (≤ 2 years) |

| BOI incentives for machinery modernization | +0.3% | Samut Prakan and Pathum Thani industrial zones | Medium term (2-4 years) |

| E-commerce–driven quick-response supply chains | +0.3% | Urban hubs with strong logistics | Short term (≤ 2 years) |

| Local synthetic and viscose fiber capacity | +0.2% | Rayong and Chonburi petrochemical corridors | Medium term (2-4 years) |

| Technical-textile demand from automotive and medical clusters | +0.2% | Eastern Economic Corridor | Long term (≥ 4 years) |

| Blockchain traceability for ESG compliance | +0.1% | Export-oriented firms in central Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Domestic Tourism–Led Apparel Rebound

Tourist spending rebounded to 88% of 2019 levels in 2025, driving a 22% jump in casual-wear and resort apparel sales. Pratunam and Chatuchak wholesalers responded by sourcing smaller, more varied fabric lots, which lifted mill utilization rates in central Thailand. Regional shopping festivals added new outlets for immediate sales, bypassing traditional distributors. E-wallet campaigns by the Tourism Authority continue to spur purchases of locally made garments, keeping factory order books steady into 2026. The sustained flow of visitors is thus anchoring near-term fabric demand despite export headwinds.[1]Tourism Authority of Thailand, “Tourism Statistics 2025,” TourismThailand.org.

Government BOI Incentives for Machinery Modernization

The Smart & Sustainable Textile scheme grants eight-year tax holidays and 50% import-duty waivers on advanced looms, digital printers, and water-treatment systems. Forty-seven approved projects totaling USD 343 million aimed to trim energy use by up to 30% per meter of cloth by end-2025. Indorama’s melt-spinning upgrades alone cut its energy intensity by 15%, underscoring the immediate payoff for large mills. SMEs lacking collateral still struggle to co-invest, widening the productivity gap within the Thailand textile market. Over the medium term, higher capital intensity is expected to contain labor-cost pressures[2]Thailand Board of Investment, “Textile Industry Incentives,” BOI.go.th.

E-Commerce–Driven Quick-Response Supply Chains

Online fashion sales hit USD 2.5 billion in 2025, and platforms now demand 15-day replenishment cycles. Leading mills have adopted make-to-order workflows, digital pattern libraries, and AI demand forecasting, which lowered fabric waste by 12-15%. Speed-to-market rather than price is becoming the deciding factor for activewear and streetwear orders, allowing domestic producers to offset Vietnam’s wage advantage. Quick-response capability is therefore reshaping the competitive playbook across the Thailand textile market[3]Electronic Transactions Development Agency, “E-Commerce Statistics 2025,” ETDA.or.th.

Local Availability of Synthetic & Viscose Fiber Capacity

Rayong and Chonburi host 1.2 million t/year of polyester staple and 450,000 t/year of viscose capacity that supply mills within 10 days, compared with three weeks for imported fiber. Proximity to petrochemical feedstocks cuts logistics costs by up to 10% and shields spinners from freight volatility. Thai Rayon’s viscose and Indorama’s PET lines underpin a resilient raw-material pipeline, encouraging fabricators to shift blends toward synthetics with performance add-ons. Ready fiber supply thus reinforces the Thailand textile market’s pivot to higher-margin technical fabrics.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor costs & skilled-labour shortages | -0.3% | National, acute in Bangkok metropolitan region and central industrial zones | Short term (≤ 2 years) |

| Cheaper apparel imports from China & Vietnam | -0.2% | National, concentrated in retail and e-commerce channels | Medium term (2-4 years) |

| Tight SME credit caused by elevated NPL ratios | -0.2% | National, most severe for SMEs in Samut Prakan, Pathum Thani, Nakhon Pathom | Short term (≤ 2 years) |

| Water-stress regulations on dyeing/finishing effluents | -0.1% | National, concentrated in dyeing clusters in Samut Prakan, Nakhon Pathom, Ayutthaya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs and Skilled-Labor Shortages

Minimum wages increased to USD 11.50 per day in 2025, lifting total labor expenses by 21% versus 2023. Younger workers continue to migrate into electronics and automotive assembly, leaving 23,000 textile vacancies unfilled. Automation eases pressure in spinning and weaving, yet dyeing and final inspection remain human-intensive. Enrollment in industry-backed vocational programs reached only 1,800 students in 2025, well below the 5,000 annual entrants needed to stabilize the workforce. Unless training pipelines expand, rising wage floors will squeeze the Thailand textile market’s cost competitiveness.

Cheaper Apparel Imports from China & Vietnam

Apparel imports surged 14% in 2025 to USD 3.2 billion, with China and Vietnam supplying 68% of the volume. Chinese fast-fashion players Shein and Temu price basic garments 30-40% below Thai producers, eroding shelf space in mass-market retail. Vietnam’s duty-free access to the EU and UK diverts brand orders away from Thailand, especially for cut-make-trim contracts. Domestic mills must therefore pivot toward technical, sustainable, or design-led niches to escape pure price competition that imperils the Thailand textile market’s apparel segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Technical Textiles Gain as Apparel Plateaus

Fashion and apparel retained a 62.67% Thailand textile market share in 2025, anchored by tourism-driven casual wear demand and quick-response orders from e-commerce platforms. Industrial and technical textiles captured 18% of revenue and are forecast to post the fastest 1.95% CAGR, propelled by airbags, medical nonwovens, and geotextiles required in the Eastern Economic Corridor. Apparel volume growth flattens after 2027 as low-priced imports from China and Vietnam erode margins, yet domestic mills still rely on the segment for scale and working-capital turnover.

Manufacturers are reallocating loom hours toward specification-driven fabrics that command up to 25% higher average selling prices, while retaining short-run apparel lines for cash flow. ISO 13485-certified nonwoven producers already supply Thai and ASEAN hospitals, proving that compliance unlocks premium contracts. Airbag-grade nylon yarn from the Toyobo-Indorama venture illustrates how automotive clusters pull in local content under just-in-time schedules. Over the forecast horizon, technical uses are expected to lift their slice of the Thailand textile market size to roughly USD 1 billion, offsetting the commoditization of mass-market clothing.

By Raw Material: Synthetic Fibers Close the Gap

Natural fibers held 61.86% of 2025 revenue, with cotton alone accounting for 48% because consumers favor breathable fabrics in Thailand’s tropical climate. Synthetic fibers are set to expand at a 1.86% CAGR, buoyed by domestic polyester and viscose capacity that trims logistics costs by 8-10% and stabilizes supply. Polyester’s wrinkle resistance and viscose’s silk-like drape increasingly satisfy activewear and mid-priced fashion brands, narrowing cotton’s dominance.

Recycled PET output reached 50,000 t in 2025, but adoption is limited by a 10-15% price premium over virgin resin. If sorting infrastructure improves and brands honor sustainability price points, recycled inputs could accelerate synthetic penetration and reshape raw-material dynamics within the broader Thailand textile market. Specialty high-performance fibers such as aramid remain niche and imported, yet pilot trials with Chulalongkorn University on phase-change yarns hint at future diversification.

By Process/Technology: Nonwovens Emerge Amid Woven Dominance

Woven fabrics commanded 85.56% of output in 2025, reflecting legacy apparel and home-textile production that still relies on shuttle and air-jet looms. BOI incentives are catalyzing upgrades to rapier and water-jet systems that cut energy use up to 22% per meter, improving competitiveness even as wages rise. Knitted goods comprise 9% of revenue, centered on T-shirts and activewear, but utilization fell to 68% in 2025 due to weak exports.

Nonwovens, though under 10% of volume, will clock the fastest 1.89% CAGR on sustained hygiene and medical demand. Spunbond and melt-blown capacity in Rayong and Samut Prakan already supplies regional diaper and mask producers, while hydro-entangled lines feed wet-wipe brands. Automotive seat and cabin-filter contracts are fostering early adoption of 3-D spacer fabrics, signaling how advanced processes can chip away at woven dominance and add higher-margin revenue to the Thailand textile market share mix.

Geography Analysis

Greater Bangkok and nearby Samut Prakan generated just over half of the Thailand textile market size in 2025, helped by dense weaving, dyeing, and garment hubs linked to Suvarnabhumi Airport and Laem Chabang Port. Mills here reload e-commerce warehouses within one day, a speed that keeps fashion labels loyal even as wages rise. Access to designers, freight forwarders, and skilled operators keeps capacity use high, so the area is projected to expand at a steady 1.4% CAGR through 2031.

The Eastern Economic Corridor (Rayong, Chonburi, and Chachoengsao) delivered 22% of sector revenue in 2025 and is the fastest-growing pocket, on track for a 2.1% CAGR. Integrated polyester and nylon plants supply airbag and nonwoven producers within the same estates, cutting raw-material lead times by up to ten days. BOI tax holidays and bonded-zone status add further pull for Japanese joint ventures that need ISO-level quality controls. As technical fabrics gain ground, the corridor’s Thailand textile market share is expected to reach about 26% by 2031.

Northern provinces such as Chiang Mai and Lamphun focus on premium silk and cotton hand-weaves that sell at 40-50% price premiums in tourist boutiques. Artisan cooperatives meet resort-wear orders in small lots, cushioning the region from mass-market price swings. Exports to Laos, Myanmar, and Cambodia rose 7% in 2025 to USD 420 million, filling gaps left by Chinese suppliers that target larger Western contracts. The north’s niche products give it an 8% slice of the Thailand textile market size and are forecast to grow at a 1.6% CAGR, ensuring continued relevance despite its smaller volume base.

Regulatory Landscape

Thailand textile producers operate under the Ministry of Industry's standards and conformity regime administered by the Thai Industrial Standards Institute (TISI) under the Industrial Product Standards Act. For finished textile products, TISI standards set chemical safety requirements, including limits for substances such as formaldehyde and azo dyes (for example, the TIS 2346 series). Compliance is typically demonstrated through product testing at designated or ISO/IEC 17025-accredited laboratories, alongside factory quality-system assessment via TISI inspection and licensing.

On the investment and industrial policy side, the Thailand Board of Investment (BOI) continues to shape capital spending through promotion categories and conditions, with updates to the investment promotion framework published in the Royal Gazette on 22 January 2026 (based on 5 June 2025 notifications). These updates are relevant for mills planning automation, digital printing, and environmental upgrades, as promotion eligibility and requirements can affect project economics and location choices, especially where waste-treatment infrastructure and process controls are needed for dyeing and finishing operations.

Value Chain Analysis

Thailand maintains an integrated textile value chain spanning fiber and polymer inputs, spinning, weaving/knitting and nonwovens, dyeing/printing/finishing, garmenting, and distribution through wholesalers and increasingly e-commerce fulfillment. Domestic man-made fiber availability supports shorter lead times, with viscose staple fiber supplied by Thai Rayon Public Company Limited (reported capacity of 151,000 tons per year) and large synthetic fiber production concentrated in the Rayong and Chonburi petrochemical corridor. These inputs feed yarn and fabric operations serving both apparel and technical-textile demand.

Upstream and midstream processes are being reshaped by modernization incentives and sustainability requirements, pushing investment into efficient looms, digital workflows, and water-treatment systems, while SMEs remain more exposed to financing and compliance costs. Downstream, domestic brands, tourist retail, and online platforms have increased the emphasis on quick-response replenishment, tightening coordination between fabric mills, dye houses, and cut-make-trim units. At the same time, environmental constraints and limited textile-waste recycling capacity create bottlenecks that elevate the value of compliant dyeing/finishing partners and circular material initiatives.

Competitive Landscape

The top 10 companies capture roughly 35% of sector revenue, leaving a long tail of SMEs that compete on quick-turn apparel and private-label orders. Japanese joint ventures such as Thai Toray and Toyobo-Indorama dominate technical-grade polyester and nylon, leveraging parent R&D and certifications like IATF 16949 to secure multi-year automotive contracts. Indorama Ventures integrates PET resin through to finished yarn, mitigating raw-material volatility and deepening margins.

Domestic names (Thanulux, Textile Prestige, and Luckytex) differentiate through design agility and shorter lead times for domestic brands and regional retailers. Pilot projects with Chulalongkorn University are testing phase-change materials and antimicrobial finishes that could open new niches in workwear and healthcare. Digital printing adoption remains under 8% of fabric output, yet early movers have landed premium European orders that underscore how on-demand customization can command higher prices within the Thailand textile market.

Recycled fibers, smart textiles with embedded sensors, and blockchain-enabled traceability are emerging battlegrounds. Large mills with stronger balance sheets can absorb the upfront tech costs, while SMEs risk being locked out of global supply chains if they cannot meet rising ESG standards. Market consolidation is therefore plausible as smaller operators partner with or are acquired by larger, compliance-ready players.

Thailand Textile Industry Leaders

Thanulux PCL

Textile Prestige PCL

Nan Yang Textile Group

Thai Textile Industry PCL

Erawan Textile Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest whitespace in Thailand is higher-value textiles that align with current investment promotion and buyer compliance needs: performance fabrics for workwear and activewear, medical and hygiene nonwovens, and specification-driven materials linked to automotive and industrial supply chains in the Eastern Economic Corridor. BOI promotion criteria that emphasize automation, R&D intensity (including thresholds such as at least 0.5% of revenue over the first three years for qualifying projects), and environmental protection measures are channeling investment toward smart-factory upgrades, digital printing, and process control. This reinforces the shift from commodity apparel fabric toward technical and value-added output.

Opportunities also extend to traceability and circular inputs where export-facing customers and ESG screening are tightening. Practical evidence of product-side differentiation shows up in 2026 releases by Nan Yang Textile Group focused on moisture-management and stretch performance, reflecting continued development of higher-spec fabric portfolios for professional and functional end uses. Alongside this, state-led initiatives such as the June 2026 program to develop a Silk Yarn Bank and standardize Thai silk-dyeing guidelines point to niche upgrading pathways for premium natural fibers, complementing industrial-scale moves in synthetics and technical textiles.

Recent Industry Developments

- May 2026: Nan Yang Textile Group announced Versatile Workshift, a fabric line designed for professional workwear leveraging its Dri-Balance Performa moisture-management technology. The release expands its performance credentials and supports Thai suppliers in meeting rising demand for functional fabrics in corporate PPE and uniform markets.

- April 2026: Nan Yang Textile Group launched Dynamic Performance fabric collection, engineered for multi-directional stretch and moisture management under its Dri-Balance technology platform. The development broadens its technical fabric portfolio and supports higher-margin segments such as functional apparel and industrial end uses.

- November 2024: Thanulux PCL completed the full divestment of its textile and garment business and was reclassified by the Stock Exchange of Thailand into the financials industry group. The exit highlights structural pressure on commodity-focused apparel manufacturing and underscores the advantage held by remaining producers that invest in automation, compliance, and technical textiles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Thailand textile market is defined as the value of textile materials and textile products sold into Thailand across key end uses such as apparel, home textiles, and industrial uses, counted in current USD for the stated year.

Scope exclusions: It excludes downstream retail markups for finished apparel brands and also excludes textile machinery and equipment sales.

Segmentation Overview

- By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others (Protective, Sports Textiles, etc.)

- By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon / Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- Natural Fibers

- By Process / Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond / Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to build the first set of demand and supply signals that a Thailand textile model needs. We relied on public and official sources such as Thailand customs trade statistics, the World Bank and IMF macro series, UN Comtrade trade flows, and ILO labor indicators to understand output capacity, trade intensity, and demand sensitivity.

To shape the industry view, we also reviewed listed company annual reports and investor presentations, Thailand ministry updates, and association websites that describe textile manufacturing, policy direction, and export performance. A paid subscription database for company financials and a shipment-level import and export database were used selectively to sanity check revenue ranges and product mix assumptions where public data was unclear. The sources listed here are illustrative only, and many other public documents and data points were checked for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what the desk data could not fully explain, especially the split between domestic consumption and export-linked production, and how pricing moved across fibers and fabric types. We spoke with manufacturers, traders, distributors, and downstream buying teams, and then checked assumptions around capacity utilization, order cycles, and the realistic pass-through of raw material costs across Thailand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | |

| Mid tier: 42% | Functional/Unit leaders: 42% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

The market size was built using a top-down approach where Thailand production, trade, and apparent consumption signals are reconstructed by textile category and then converted into value using realistic average price bands. The model starts with textile output and trade balances, which are then adjusted using loss factors and product mapping so the same yardage or tonnage is not counted twice.

A bottom-up cross-check was then used to keep totals grounded, using sampled supplier revenues, channel checks on typical fabric pricing, and volume to value conversions for common product lines. When company disclosures were missing, gaps were handled with peer averages and capacity-based proxies, followed by a re-check with interview feedback. Key inputs that drive the model include export and import values by textile codes, capacity utilization and operating days in mills, cotton and polyester price movements, wage and energy cost pressure (as it affects output), and the share of demand coming from apparel manufacturing versus technical and home textiles.

For forecasting, we used scenario analysis supported by short time series smoothing on the main drivers, because the market is influenced by trade cycles and input cost swings. Assumptions on export demand, domestic manufacturing activity, and raw material pricing were refreshed with expert views so the forward path stays practical rather than overly optimistic.

Data Validation & Update Cycle

Validation was done through multiple checks so the final value is consistent with real-world signals. We compared the modeled totals against independent indicators such as Thailand textile export trends, changes in import dependence, and the direction of key fiber prices to see whether the implied market movement made sense.

If unusual jumps appeared, the inputs were reviewed, the category mapping was rechecked, and respondents were recontacted when the variance could not be explained by a known event. Before sign-off, the model and assumptions go through an internal analyst review, and then the report is refreshed annually, with interim updates when material events change trade flows, pricing, or operating rates. Right before delivery, one more pass is done so clients receive the latest updated view.

Mordor Intelligence's Thailand Textile Market Size Compared Against Other Published Estimates

Published market values for Thailand textiles can look different across sources, even when they use similar labels. Differences usually come from what is counted as textiles, whether the estimate leans on trade values or factory output, and how prices are converted and updated over time.

By tracking export and import values, capacity utilization signals, and then refreshing fiber-linked price assumptions with respondent checks, Mordor Intelligence keeps the Thailand textile total tied to an apparent consumption view rather than broad garment retail value add. Some estimates also extend the scope into apparel and fashion retail revenue or use a longer forecast horizon with a single growth rate, which can shift the reported base year size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.91 B (2025) | |

| Industry Publisher A | USD 5.20 B (2025) | This estimate appears to use a broader revenue pool with less clarity on whether apparel retail value add is excluded, which can inflate totals when compared with a textiles-only factory and trade linked scope. |

| Market Platform B | USD 4.97 B (2026) | The headline number is presented for a different year, and the sizing narrative leans more on forecast framing, so direct comparison can be affected by currency timing, price base used, and the assumed year-on-year price progression. |

The spread across the table is mostly explained by scope boundaries and year alignment, followed by how pricing is carried through the model. When the category boundary is kept tight and the year and price base are made explicit, the resulting market size becomes easier to reconcile with trade and production signals and easier to repeat in future updates.

Key Questions Answered in the Report

How large is the Thailand textile market in 2026?

The Thailand textile market size reached USD 4.97 billion in 2026 and is forecast to grow at a 1.56% CAGR through 2031.

Which application segment is expanding fastest?

Industrial/Technical Textiles are projected to record the highest CAGR at 1.95% between 2026-2031, driven by automotive airbags and medical nonwovens.

What is driving machinery modernization?

BOI tax holidays and import-duty waivers on automated looms and digital printers are encouraging mills to upgrade equipment and cut energy costs.

How are labor costs affecting competitiveness?

A daily minimum wage of USD 11.50 has lifted labor expenses by 21% since 2023, prompting greater automation and a pivot to higher-margin technical fabrics.

Which fibers are gaining share?

Synthetic fibers, particularly polyester and viscose, are growing fastest thanks to local raw-material capacity that shortens lead times and lowers logistics costs.

What role does blockchain play in the sector?

Export-oriented mills are piloting blockchain to trace cotton and viscose origins, meet EU deforestation rules, and secure premium orders from ESG-focused brands.

Page last updated on: