Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.68 Billion |

| Market Size (2026) | USD 16.40 Billion |

| Market Size (2031) | USD 20.34 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Packaging Market Analysis by Mordor Intelligence

The Thailand packaging market size was valued at USD 15.68 billion in 2025 and is estimated to grow from USD 16.4 billion in 2026 to reach USD 20.34 billion by 2031, at a CAGR of 4.4% during the forecast period (2026-2031). The growth trajectory reflects Thailand’s dual role as a regional food-export powerhouse and a rising e-commerce hub, both of which stimulate demand for cost-efficient, sustainable packs. Capital inflows worth THB 721 billion (USD 20.6 billion) approved by the Board of Investment in 2024 channel fresh spending into food processing, automation, and, by extension, packaging lines. Converters are already redesigning portfolios to meet the draft Packaging Act’s anticipated extended producer responsibility targets, which favour lighter, mono-material structures over heavy, rigid formats. Meanwhile, daily parcel volumes topping 7 million accelerate the adoption of mailers and stand-up pouches that curb freight charges and minimize damage.

Key Report Takeaways

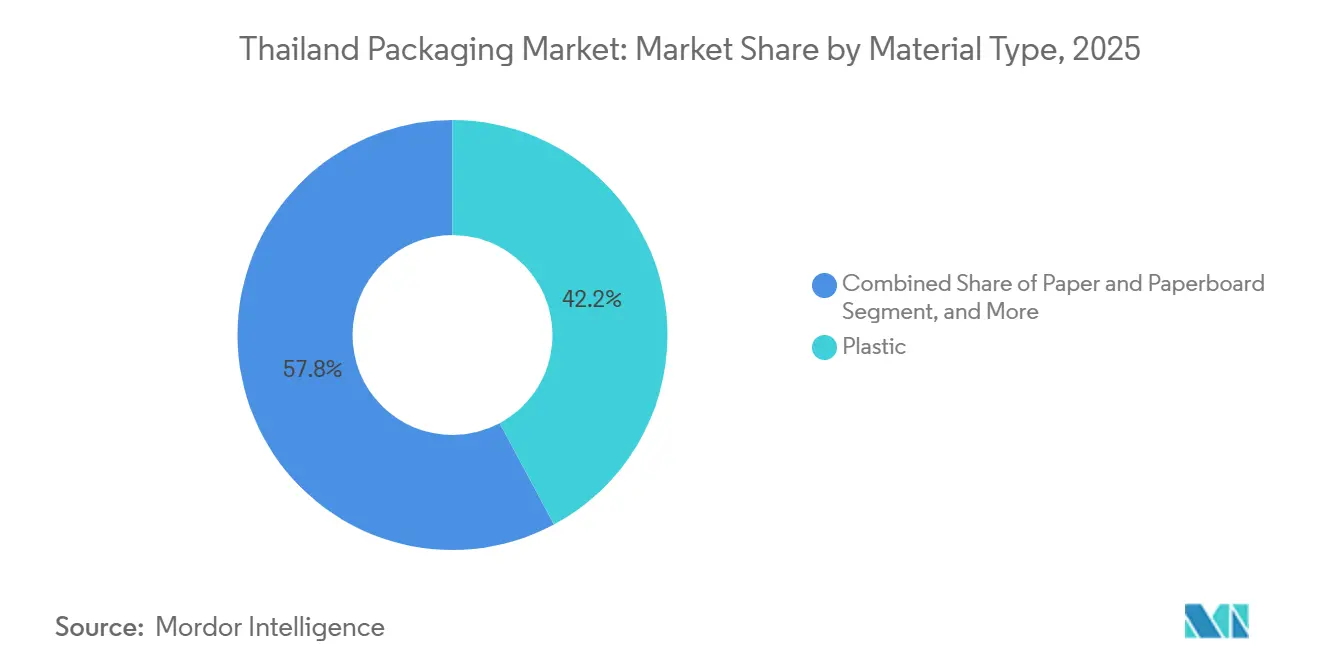

- By material type, plastic captured 42.18% of Thailand packaging market share in 2025, while recycled polyethylene terephthalate is forecast to expand at a 4.92% CAGR through 2031.

- By product type, pouches accounted for the fastest growth at a 5.01% CAGR, whereas bags led with 28.24% revenue share of the Thailand packaging market size in 2025.

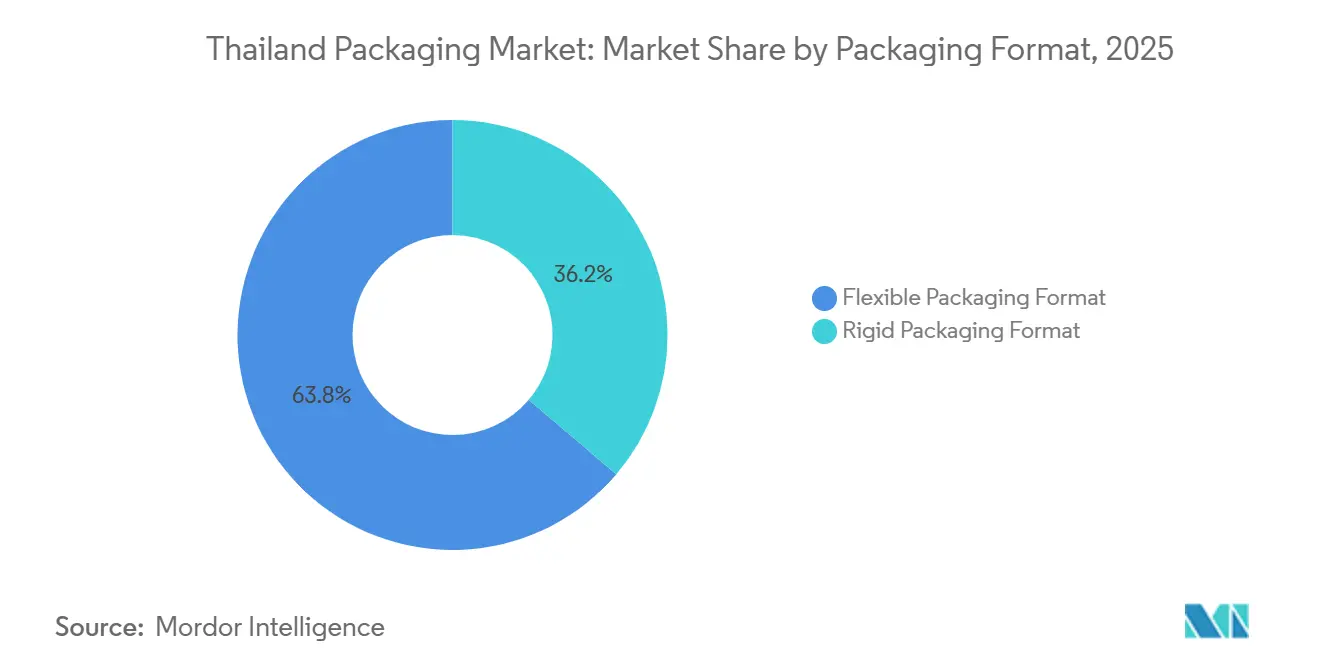

- By packaging format, flexible packs dominated with 63.78% value in 2025 and are projected to widen their lead by growing at 5.25% through 2031.

- By end-user industry, food held 35.39% of 2025 revenue, yet cannabis-infused food and beverage is poised to record a 4.98% CAGR once regulatory clarity returns.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Food and Beverage Output | +1.20% | National, with concentration in Central and Eastern regions | Medium term (2-4 years) |

| Growth of E-commerce and Parcel Volumes | +1.00% | National, with urban density in Bangkok, Chiang Mai, Phuket | Short term (≤ 2 years) |

| Demand for Convenient and Flexible Packs | +0.80% | National, accelerated in urban centers | Medium term (2-4 years) |

| Sustainability and Circular-Economy Mandates | +0.70% | National, with early adoption in export-oriented sectors | Long term (≥ 4 years) |

| BOI Incentives for Packaging Automation | +0.50% | National, with priority zones in Eastern Economic Corridor | Medium term (2-4 years) |

| Cannabis-Infused Food and Beverage Requires Child-Safe Packs | +0.20% | National, regulatory uncertainty limits near-term impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Food and Beverage Output

Thailand shipped USD 32.8 billion worth of food products in 2024, a performance that lifts packaging demand because shelf-stable exports need multilayer barrier films that preserve flavour during long transit.[1]Thai Food Processors Association, “Thailand Food Exports Reach USD 32.8 Billion in 2024,” THAIFOODPROCESSORS.ORG Capacity-utilization in domestic food factories climbed to 78% in 2025, sustaining orders for corrugated shippers, stand-up pouches, and aseptic cartons.[2]Office of Industrial Economics, “Food Manufacturing Capacity Utilization Reaches 78% in 2025,” OIE.GO.TH Hotels, restaurants, and institutional buyers spent USD 35.4 billion in 2025 as tourism rebounded, strengthening local pull for ready-to-eat meal kits that rely on microwaveable trays.[3]United States Department of Agriculture Foreign Agricultural Service, “Hotel-Restaurant-Institutional Market Totals USD 35.4 Billion in 2025,” FAS.USDA.GOV The dual export-domestic engine allows converters to transfer resin cost swings into pricing without volume loss. Consequently, rising food throughput is expected to add 1.2 percentage points to the Thailand packaging market CAGR between 2026 and 2031.

Growth Of E-Commerce and Parcel Volumes

Courier leader Kerry Express handled 7 million-8 million parcels daily during 2025, reflecting a double-digit volume climb since 2022.[4]Baker McKenzie, “Thailand’s Draft Packaging Act and Extended Producer Responsibility Framework,” BAKERMCKENZIE.COM Each parcel uses a polyethylene mailer or corrugated box, and the shift toward same-day service favours pre-formed, lightweight solutions that shorten pack-to-ship cycles. National gross-merchandise value touched THB 100 billion (USD 2.9 billion) in 2025, with fashion and health-and-beauty goods recording the highest reorder rates. Parcel carriers now request recyclable or biodegradable mailers to meet corporate climate pledges, spurring demand for paper-based bubble mailers and compostable air pillows. As the last-mile network saturates Bangkok and expands to provincial hubs, e-commerce will continue to contribute about 1 percentage point to market growth through 2028.

Demand For Convenient and Flexible Packs

Single-serve pouches, resealable bags, and portion-controlled formats increased their slice of flexible-packaging value from 22% in 2022 to 28% in 2025, mirroring smaller household sizes and on-the-go eating habits. Retail chains widen chilled and ambient meal-kit shelves, relying on multi-compartment pouches that separate sauces from proteins and capture a 15%-20% price premium over rigid trays. Modern-trade stores already represent 65% of packaged-food sales and are growing at 6% annually, further tilting demand toward value-added flexible packs. Converters integrate laser scoring, tamper-evident seals, and QR-code traceability to justify higher margins. The convenience trend is projected to lift the Thailand packaging market CAGR by 0.8 percentage points in the medium term.

Sustainability And Circular-Economy Mandates

Thailand’s draft Packaging Act, slated for 2027 enforcement, will obligate producers to fund collection and recycling proportional to tonnage placed on the market. SCG Packaging aligned early, pledging a 100% recyclable portfolio by 2030 and net-zero emissions by 2050. The Asian Development Bank estimates a USD 1.2 billion annual upside in plastic-waste valorisation if consumer participation exceeds 40%. First movers adopting mono-material films and ISO 14001 processes will capture shelf space from laggards once EPR fees start. Accordingly, sustainability mandates are set to add 0.7 percentage points to long-term market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-Use-Plastic Bans and Eco Taxes | -0.60% | National, with stricter enforcement in Bangkok and tourist zones | Short term (≤ 2 years) |

| Volatile Petrochemical Resin Prices | -0.50% | National, with spillover from regional crude-oil markets | Short term (≤ 2 years) |

| Shortage of Food-Grade rPET Feedstock | -0.30% | National, import dependency on Japan and South Korea | Medium term (2-4 years) |

| Low-Cost Import Competition From Vietnam and China | -0.40% | National, concentrated in corrugated and flexible-film segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Use-Plastic Bans and Eco Taxes

A nationwide prohibition on oxo-degradable bags, polystyrene food boxes, and plastic straws took effect on 1 January 2025, with fines up to THB 100,000 (USD 2,857) per infraction. Retailers pivoted to paper straws and bagasse containers that cost 20%-40% more, squeezing food-service margins. The ban removed roughly 50,000 metric tons of annual polystyrene demand, forcing extruders to idle lines or retool toward polypropylene. Planned eco-tax surcharges of THB 2-THB 5 per kilogram (USD 0.06-USD 0.14) on virgin resin could deepen the cost burden. Combined, these factors shave 0.6 percentage points from the Thailand packaging market CAGR in the near term.

Volatile Petrochemical Resin Prices

Polypropylene spot prices oscillated between USD 950 and USD 1,150 per metric ton during 2025, a 15%-20% quarterly swing triggered by crude-oil volatility and outages in regional crackers. PET bottle-grade resin peaked at USD 1,050 per metric ton in Q2 2025 before sliding back to USD 920 at year-end. Converters, hedged with 30-60-day supply contracts, struggled to pass spikes through annual deals, eroding gross margins by up to 300 basis points and inflating working-capital needs. Consequently, resin turbulence subtracts 0.5 percentage points from projected CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Content Reshapes Plastic Dominance

Plastic captured 42.18% of value in 2025, yet recycled PET is racing ahead at a 4.92% CAGR, underlining the pivot to circular feedstock as global brands chase 25%-50% post-consumer-resin targets. The Thailand packaging market size for rPET bottles alone is projected to grow faster than virgin equivalents because Indorama Ventures commissioned a 50,000 metric-ton food-grade line in late 2025. Polypropylene and high-density polyethylene grow in the low-4% range but face eco-tax headwinds, while polystyrene demand collapsed post-ban.

Paper and paperboard represented about 28% of 2025 value, buoyed by 5.2% output growth at domestic mills that meet surging e-commerce box orders. Metal held 18%, its advance tied to Thai Beverage Can and Ball Corporation investments in lightweight aluminium technology. Glass followed at 12%, with BG Container Glass banking on furnace-upgrade efficiencies but conceding share to lighter PET bottles. Altogether, material dynamics demonstrate how sustainability premiums and logistics economics reshape the Thailand packaging market.

By Product Type: Pouches Outpace Bags in Flexible Segment

Bags accounted for 28.24% of 2025 revenue, yet pouches grow quicker at 5.01% as consumers favour resealable, shelf-standing formats. The Thailand packaging market share for pouches benefits from 12%-15% converter margins, higher than commodity bag lines, because of zipper and spout features. Films and wraps rise 4.7% thanks to export palletization and greenhouse farming in the Eastern Economic Corridor.

Rigid plastics bottles, jars, and caps collectively post a 4.2% CAGR, aided by beverage and personal-care demand. Tethered caps add USD 0.01-USD 0.02 each yet prevent littering and meet forthcoming EPR rules. Corrugated boxes, folding cartons, and molded-fiber takeaway packs round out paper products, leveraging the January 2025 foam ban to win food-service contracts. The product landscape signals a continuing tilt toward value-added formats within the Thailand packaging market.

By Packaging Format: Flexible Dominance Widens on Cost and Sustainability

Flexible packs delivered 63.78% of 2025 value and should extend to nearly two-thirds by 2031, growing at 5.25%. Each stand-up pouch or mailer uses up to 80% less material weight and slashes freight carbon, advantages magnified by 7-8 million daily parcels. Thailand packaging market share gains for flexible converters also stem from their 14%-16% EBITDA margins versus 10%-12% for rigid lines.

Rigid formats keep relevance in beverages and pharmaceuticals, yet single use bans and heavier EPR fees cap growth at 4%. Once the Packaging Act imposes weight-based levies, analysts expect another 50-100 basis-point swing toward flexible options. The format contest will thus hinge on recyclability credentials and design-for-reuse innovations.

By End-User Industry: Food Leads, Cannabis Uncertainty Clouds Outlook

Food commanded 35.39% of 2025 value, riding record exports of ready-to-eat meals and coconut water that need aseptic cartons, MAP pouches, and microwaveable trays. Beverage ranked second with 22%, propelled by aluminium-can expansion catering to energy drinks. Pharmaceutical packs grew 4.8% on blister, vial, and child-resistant-closure adoption, while cosmetics leaned on refillable compacts for a 4.6% CAGR.

Industrial and agriculture segments move in the high-3% to low-4% bracket as petrochemical and greenhouse investments rise. Cannabis-infused products, although a small base, still boast a 4.98% forecast CAGR contingent on policy reset after the late-2024 recriminalization that stranded child-resistant-closure inventory. End-use diversity cushions the Thailand packaging market against cyclical jolts.

Geography Analysis

The Central and Eastern regions, home to Bangkok and the Eastern Economic Corridor, generate the bulk of Thailand packaging market revenue because they host food-processing clusters, petrochemical complexes, and the highest parcel densities. E-commerce fulfilments centers near Bangkok’s ring roads amplify demand for corrugated shippers and polyethylene mailers. Meanwhile, coastal ports in Chonburi and Rayong drive export flows that favour moisture-barrier films and seaworthy stretch wraps.

Northern hubs such as Chiang Mai and Chiang Rai exhibit rising consumption of on-the-go snacks and ready-to-drink beverages, expanding local need for stand-up pouches and lightweight cans. Logistics operators extend same-day delivery to these secondary cities, thereby multiplying parcel mailer requirements. The Northeast, historically agrarian, starts to adopt silage films and fertilizer bags as greenhouse projects spread under government irrigation initiatives.

In the South, Phuket and Hat Yai record high tourist turnover that accelerates single-serve beverage sales, pushing aluminium-can lines toward full capacity. The border trade with Malaysia channels corrugated boxes and returnable glass bottles into cross-border supply chains. Altogether, geographical dispersion balances the Thailand packaging market, ensuring growth is not overly reliant on any single province.

Competitive Landscape

Thailand’s packaging arena is moderately concentrated: the top five suppliers control roughly 40%-45% of market value yet compete alongside 200 smaller converters. SCG Packaging leverages vertical integration with petrochemical affiliates to secure resin at stable pricing and co-develop recyclable designs with multinational brand owners. BG Container Glass banks on furnace modernization to trim gas use by 8% and raise throughput 15%, offsetting glass’s weight disadvantage. TPAC Packaging specializes in custom PET bottles and has implemented predictive-maintenance sensors that lift line uptime by 10%.

International players intensify rivalry. Amcor rolled out mono-material polyethylene snack pouches and pilots in-store film collection bins in Bangkok and Phuket. Huhtamaki introduced a compostable bagasse clamshell that wins contracts from quick-service restaurants affected by the foam ban. Sealed Air markets fiber-based and mono-material cushioning that satisfies courier recyclability mandates. Ball Corporation scales lightweight two-piece cans to trim aluminium input by 10%, curbing exposure to metal price spikes.

Smaller firms still find room by offering agile, short-run services and specialty tooling for pharma, cosmetics, and child-resistant formats. However, upcoming EPR fees and ISO 14001 requirements may raise compliance costs, accelerating consolidation as under-capitalized players exit or merge. Technology adoption digital twins, vision inspection, and automated plate-mounting will likely separate winners from laggards over the next five years.

Thailand Packaging Industry Leaders

SCG Packaging Public Co. Ltd

BG Container Glass Public Co. Ltd

TPAC Packaging Public Co. Ltd

Thai Beverage Can Co. Ltd

TBPI Public Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kasikornbank prioritizes ESG loans for packaging automation within corporate-lending portfolio.

- November 2024: SCG Chemicals rolls out SCGC Green Polymer, an eco-polymer family aligned with circular-economy targets.

- September 2024: Indorama Ventures sets up joint-venture rPET plants totaling 100 kt/year capacity to meet 30% recycled-content rules.

- July 2024: PTG Energy releases Sustainability Report 2023, outlining waste-to-power initiatives influencing lubricant-pack needs.

Thailand Packaging Market Report Scope

The Thailand Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, Container Glass), Product Type (Paper and Paperboard Product, Plastic Product, Metal Product, Container Glass Product), Packaging Format (Rigid, Flexible), End-User Industry (Food, Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, Automotive, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polypropylene (PP) |

| HDPE and LDPE | |

| PET | |

| PVC | |

| PS | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-Use Paper Products | ||

| Other Paper and Paperboard Types | ||

| Plastic Product | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-Grade Products | ||

| Other Rigid Plastics | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics | ||

| Metal Product | Cans | |

| Caps and Closures | ||

| Aerosol Containers | ||

| Other Metal Products | ||

| Container Glass Product | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-User Industry

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-User Industries |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polypropylene (PP) | ||

| HDPE and LDPE | |||

| PET | |||

| PVC | |||

| PS | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-Use Paper Products | |||

| Other Paper and Paperboard Types | |||

| Plastic Product | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-Grade Products | |||

| Other Rigid Plastics | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics | |||

| Metal Product | Cans | ||

| Caps and Closures | |||

| Aerosol Containers | |||

| Other Metal Products | |||

| Container Glass Product | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Pharmaceutical and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-User Industries | |||

Key Questions Answered in the Report

What is the projected value of the Thailand packaging market by 2031?

Forecasts indicate the market will reach USD 20.34 billion by 2031, supported by food exports, e-commerce, and sustainability mandates.

Which packaging format is growing faster in Thailand?

Flexible formats lead with a 5.25% CAGR through 2031, widening their share beyond the current 63.78%.

How significant is recycled PET in Thailand's packaging landscape?

Recycled PET is the fastest-growing plastic substrate at a 4.92% CAGR, fueled by brand commitments to integrate up to 50% post-consumer resin.

What impact do single-use plastic bans have on local converters?

The January 2025 bans eliminated 50,000 metric tons of polystyrene demand and raised costs 20%-40% for alternative materials, trimming near-term margins.

Who are the leading companies in Thailand's packaging sector?

SCG Packaging, BG Container Glass, TPAC Packaging, Thai Beverage Can, and Amcor together hold roughly 40%-45% of market value.

How is e-commerce shaping packaging demand?

Daily parcel volumes above 7 million drive adoption of lightweight mailers and stand-up pouches, adding around 1 percentage point to overall CAGR in the short term.

Page last updated on: