Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

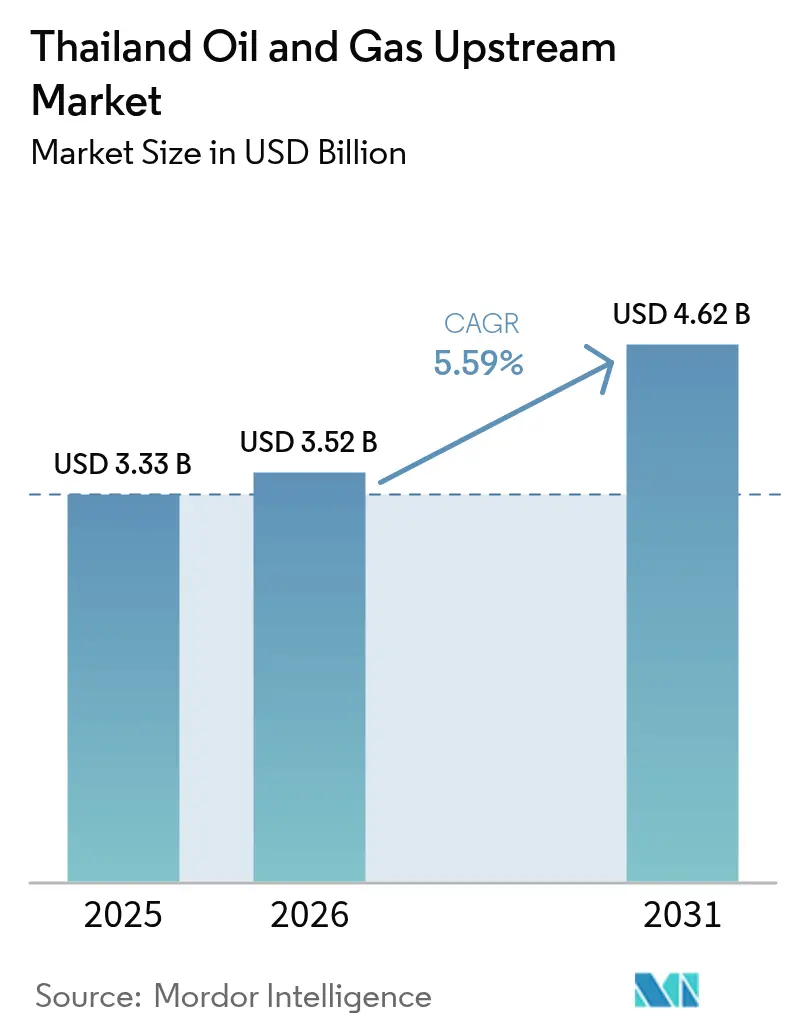

| Base Year Market Size (2025) | USD 3.33 Billion |

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Thailand Oil And Gas Upstream Market size was valued at USD 3.33 billion in 2025 and estimated to grow from USD 3.52 billion in 2026 to reach USD 4.62 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031).

Rising domestic gas output from the Erawan and Bongkot clusters, flexible production-sharing fiscal terms, and government-backed CCS pilots together anchor the growth trajectory. LNG price fluctuations in 2024 widened the landed-gas cost gap compared to domestic production, encouraging operators to accelerate projects that shorten payback periods. Meanwhile, deeper-water prospects and AI-enabled seismic reprocessing have revived exploration spending, and tighter energy-security policies are elevating domestic upstream projects from purely commercial assets to cornerstones of national strategy. Market leaders are channeling capital into brownfield upgrades, subsea tiebacks, and carbon-handling infrastructure, collectively driving incremental volumes at lower unit costs.

Key Report Takeaways

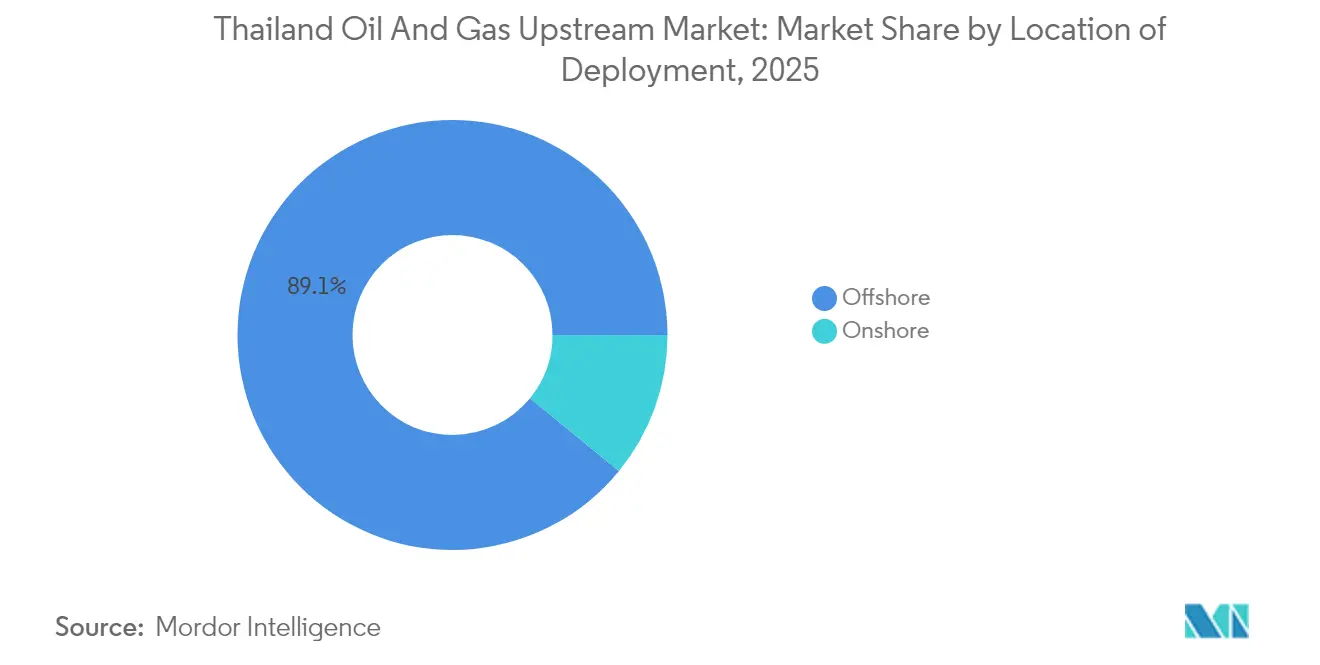

- By location of deployment, offshore operations held a 89.10% share of the Thailand oil and gas upstream market size in 2025 and are expected to advance at a 5.78% CAGR through 2031.

- By resource type, natural gas accounted for 77.85% of Thailand's oil and gas upstream market share in 2025, while crude oil is projected to grow at a 5.66% CAGR through 2031.

- By well type, conventional drilling captured 84.60% of the Thailand oil and gas upstream market size in 2025; unconventional wells are poised for a 5.95% CAGR through 2031.

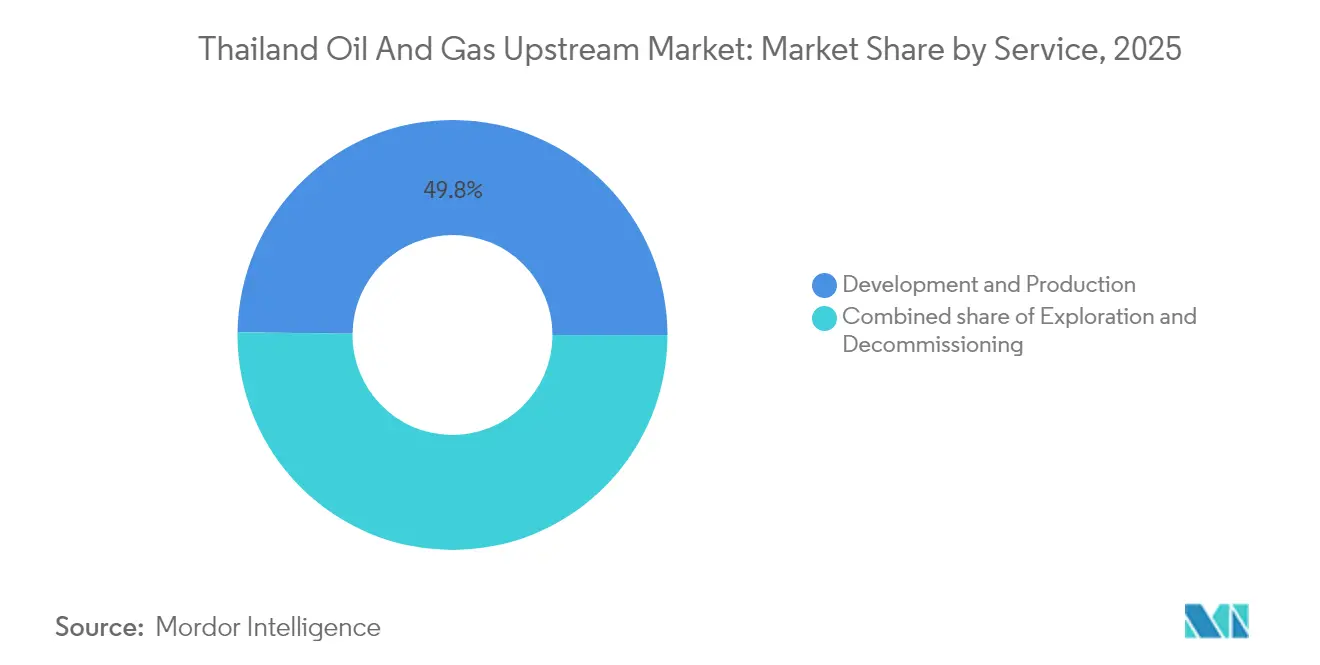

- By service, development and production activities represented 49.80% of 2025 revenue, whereas exploration services are on track for a 6.2% CAGR to 2031.

- PTTEP, Chevron, TotalEnergies, and Mubadala Energy collectively controlled over 80% of the national gas volumes in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ramp-up of Erawan/Bongkot gas clusters | +1.2% | Gulf of Thailand offshore blocks | Short term (≤ 2 years) |

| 24th & 25th licensing rounds plus PSC overhaul | +0.8% | Nationwide (onshore focus) | Medium term (2-4 years) |

| LNG-price volatility pushing domestic upstream | +0.7% | Nationwide with regional spillover | Short term (≤ 2 years) |

| CCS/EGR pilots unlocking stranded reserves | +0.6% | Gulf of Thailand mature fields | Long term (≥ 4 years) |

| AI-augmented reprocessing of legacy seismic | +0.5% | All exploration blocks | Medium term (2-4 years) |

| Modular tie-backs of marginal gas pockets | +0.4% | Gulf of Thailand satellite fields | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ramp-up of Erawan/Bongkot Gas Clusters

PTTEP closed its USD 2.8 billion acquisition of Chevron’s domestic portfolio in 2024 and immediately began a drilling and facilities-upgrade campaign aimed at lifting combined output from Erawan and Bongkot to 800 MMSCFD by 2026.[1]Investor Relations, “Fourth-Quarter 2024 Presentation,” PTTEP, pttep.com Integrated control has trimmed per-unit development costs an estimated 15–20% by sharing compression, processing, and logistics assets across neighboring blocks. Alignment with Thailand’s Single Pool Gas Price policy secures predictable long-term margins, enabling enhanced recovery methods in deeper horizons that could stretch field life by up to 10 years. PTTEP’s AI & Robotics Ventures unit deploys predictive-maintenance drones and edge-analytics sensors that have already reduced unplanned downtime across both complexes.

24th & 25th Licensing Rounds Plus PSC Overhaul

The 2024 regulatory reboot introduced production-sharing contracts beside legacy concessions, balancing state revenue capture with investor upside. Eight blocks awarded under the 24th round attracted USD 2.1 billion in committed spending, while the 25th round released 16 onshore areas tailored for unconventional techniques. The PSC construct raises government take during price peaks yet cushions operators during troughs, a feature that is especially attractive for tight-margin, marginal fields. Streamlined environmental approvals now include standardized timelines, reducing the average exploration start-up delay by almost 40% compared to the pre-2024 practice.

LNG-Price Volatility Pushing Domestic Upstream

Asian spot LNG swung between USD 8–15 /MMBtu in 2024, amplifying Thailand’s gas-import bill and prompting policymakers to fast-track domestic field developments. Operators responded by reprioritizing brownfield infill wells and subsea tiebacks with paybacks of under three years. PTT’s offtake portfolio shifted toward indexed domestic supply contracts that hedge exposure to global shocks, underscoring the strategic value of local barrels even when breakevens exceed long-term LNG contract prices.

CCS/EGR Pilots Unlocking Stranded Reserves

Thailand approved full-cycle carbon-storage legislation in 2024, and PTTEP’s Arthit pilot targets injection of 2.5 million t/y CO₂ while lifting an extra 1.5 TCF of gas via pressure support starting 2027.[2]Statistics Division, “2024 Petroleum Balance Sheet,” Department of Mineral Fuels Thailand, dmf.go.th Success would establish engineering templates for 15-plus mature fields, potentially extending their economic life by 10-15 years and aligning with the nation’s 2065 carbon neutrality pledge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining output from mature shallow-water fields | -0.9% | Gulf of Thailand legacy concessions | Short term (≤ 2 years) |

| Lengthy EIA & community-consultation cycles | -0.6% | Nationwide, notably onshore | Medium term (2-4 years) |

| High-CO₂ content in new discoveries | -0.5% | Deep-water Gulf blocks | Medium term (2-4 years) |

| Petroleum-engineering talent flight to renewables | -0.4% | Bangkok and regional hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Output from Mature Shallow-Water Fields

Legacy fields drilled between 1980 and 2010 are exhibiting annual decline rates of 8–12% as reservoir pressure drops.[3]“Field Decline Analysis Workshop 2024,” Society of Petroleum Engineers Thailand Section, spe.org Although water-injection and compression upgrades can soften the descent, cost-effective replacement volumes of 200–300 MMCFD each year are still required merely to maintain a flat supply. Remaining reserves reside in tighter compartments, demanding horizontal wells and selective stimulation, both of which are capital-intensive under today’s service-cost inflation.

Lengthy EIA & Community-Consultation Cycles

Mandatory impact assessments for offshore projects within 12 nautical miles of shore draw multi-stakeholder reviews involving fishing, tourism, and environmental groups.[4]“National EIA Guidelines,” Office of Natural Resources and Environmental Policy and Planning, onep.go.th Recent approvals averaged 18–24 months, doubling project lead times compared to regional peers and hindering cash-flow schedules for smaller independents. Onshore unconventional schemes face even wider opposition, further complicating surface-access negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Dominance Spurs Tech Shifts

Offshore acreage accounted for 89.10% of Thailand's oil and gas upstream market size in 2025 and is expected to grow at a 5.78% CAGR through 2031. Production is anchored in shallow Gulf waters, where PTTEP integrates Bongkot, Erawan, and Arthit through cross-field pipelines and shared gas-processing trains, thereby driving down unit operating expenses (opex). Deeper plays now entering appraisal may tilt the Thailand oil and gas upstream market toward subsea completion systems and dynamic positioning rigs, lifting capex requirements yet lengthening asset life.

Onshore prospects, which account for just 10.90% of current output, benefit from the new PSC fiscal regime. Exploration focuses on the Khorat Plateau, where tight-sand formations mirror productive analogs in neighboring countries. While infrastructure lags coastal hubs, modular processing skids and trucked LNG could bridge early commercialization gaps until pipeline connectivity improves.

By Resource Type: Gas Infrastructure Anchors Value Chain

Natural gas supplied 77.85% of 2025 volumes thanks to power-sector baseload demand and firm offtake contracts with EGAT. The long-term saturation of gas pipelines and processing plants across the Eastern Seaboard solidifies gas as the price setter for competing liquid barrels. Crude’s 5.66% CAGR outlook stems from deeper-water finds holding higher oil cuts and from brownfield secondary-recovery programs aimed at lifting aggregate liquids yield. High CO₂ ratios in some deep prospects complicate economics, yet upcoming CCS facilities could neutralize these penalties and attract new capital.

By Well Type: Conventional Techniques Face Digital Disruption

Conventional wells retained 84.60% of Thailand's oil and gas upstream market share in 2025, delivering initial gas rates of 15–25 MMCFD at water depths of 30–80 m. Digital twins and real-time downhole sensors keep lifting costs under USD 1.3 per MMBtu. Unconventional programs—still <5% of activity—record a 5.95% CAGR as operators test horizontal drilling and fracture methods optimized for Southeast Asian rock mechanics. Early pilot wells displayed rate-of-penetration gains of 22% after integrating automated bit guidance and AI drilling analytics.

By Service: Exploration Renaissance Takes Shape

Development and production work captured 49.80% of 2025 spending, reflecting ongoing platform upgrades, compression add-ons, and artificial-lift rollouts. However, exploration services are growing at a rate of 6.2% annually as reprocessed seismic data and fresh PSC acreage spark interest in frontier leads. Decommissioning—still in its nascent stages—will scale sharply after 2028, when more than 30 fixed platforms reach the end of their design life, opening tenders for heavy-lift vessels and rigless plug-and-abandon equipment tailored to shallow-water Gulf environments.

Geography Analysis

Thailand's upstream heartland is the central Gulf basin, where Bongkot, Erawan, and Arthit alone supply over 75% of daily gas. Proximity to the Eastern Economic Corridor keeps transport tariffs low and facilitates back-flushing of processed gas liquids into petrochemical feedstocks. To the west, the joint development area with Myanmar contributes roughly 15% of the nation's gas through bilateral transit pipelines; recent political turbulence across the border underscores the strategic value of Thailand-controlled reserves.

Emergent deep-water zones south of existing hubs introduce thicker pay zones but also elevated CO₂ concentrations that require in-situ separation or post-processing. Planned CCS hubs could economically absorb that CO₂, opening the way for higher liquids-rich targets and diversifying the Thailand oil and gas upstream market. Onshore, the Khorat Plateau remains under-drilled. Seismic inversion data suggest 5–8 TCF of tight-gas potential; however, public perception risks and water-use constraints will likely dictate staged pilot approaches before full-field development.

Regulatory Landscape

Thailand upstream petroleum activities are regulated primarily by the Department of Mineral Fuels (DMF) under the Petroleum Committee, with the Petroleum Act, B.E. 2514 (1971), as amended, and the Petroleum Income Tax Act, B.E. 2514 (1971) forming the core legal framework. Petroleum resources belong to the state, and companies participate through awarded concessions or newer contractual structures such as production-sharing contracts (PSCs), alongside service-contract mechanisms. Together, these frameworks define rights to explore, develop, and produce, as well as fiscal obligations.

In March 2026, the government held public hearings on a draft bill to amend the Petroleum Act. The draft includes provisions to address carbon capture and storage (CCS) use in petroleum reservoirs, updated decommissioning obligations, and revised production terms up to 20 years. This amendment process links regulatory priorities to energy-security and cost-volatility concerns, while also formalizing end-of-life and carbon-management requirements for ageing Gulf of Thailand assets.

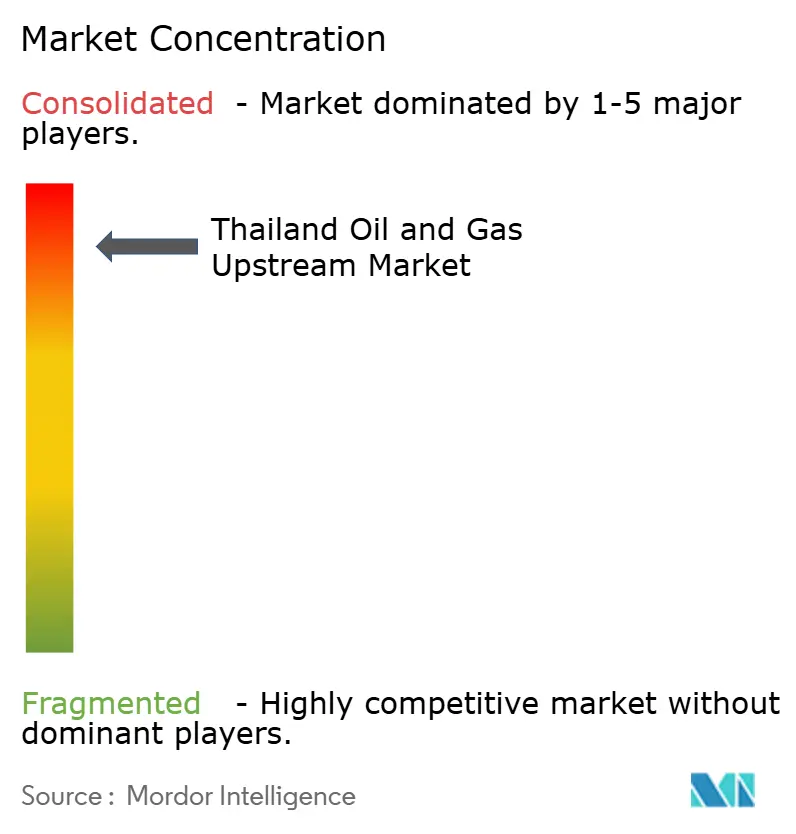

Competitive Landscape

PTTEP supplied more than 80% of Thailand’s gas in 2024 and operated 15 offshore blocks, leveraging state backing and integrated midstream assets to consolidate scale advantages. Chevron, TotalEnergies, and Mubadala Energy maintain minority stakes, often as technical partners in complex brownfield expansions, rather than as leaders in greenfield projects. Service competition is more balanced. Schlumberger, Baker Hughes, and Halliburton rotate turnkey drilling campaigns, while TechnipFMC and Subsea 7 pursue subsea EPC scopes linked to deep-water tie-backs.

Opportunities for niche entrants center on carbon-management technology, unconventional resource stimulation, and end-of-life decommissioning. The switch to PSCs lowers entry barriers by allowing shared-risk structures that align cash flow with reservoir performance, positioning the Thailand oil and gas upstream industry for a more diversified operator mix post-2027.

Thailand Oil And Gas Upstream Industry Leaders

-

PTTEP

-

Chevron Thailand E&P

-

Valeura Energy

-

Mitsui Oil Exploration (MOECO)

-

Mubadala Energy Thailand

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In Thailand, upstream opportunities are centered on (i) accelerated development and debottlenecking of existing Gulf of Thailand gas hubs and (ii) new acreage access under the licensing framework. PTTEP has disclosed a 2026 budget of USD 7,726 million within a 2026-2030 investment plan of USD 33,279 million, which provides visible capital backing for brownfield drilling, facilities upgrades, and reliability projects tied to domestic supply.

Alongside that, Cabinet approval in August 2025 for the transfer of a 40% participating interest in G1/61 (Erawan) to PTTEP, resulting in sole investorship, creates a clearer decision chain for development sequencing and contractor mobilization on one of Thailand's key gas blocks. White-space for exploration is also widening beyond the mature central Gulf basin, with DMF signaling plans in January 2026 to call for bids in the Andaman Sea and expand frontier activity for seismic, appraisal drilling, and offshore services. Carbon-management capability is another investable gap, with Thailand pairing efforts to reduce production gaps and LNG import exposure with CCS-focused provisions discussed in 2026, and PTTEP's Arthit CCS pilot (final investment decision announced for a project designed to capture up to 1 million tonnes of CO2 per year, with start targeted in 2028) reinforcing demand for CO2 handling, monitoring, and subsurface assurance solutions that can be replicated across mature fields.

Recent Industry Developments

- June 2026: Valeura Energy completed an eight-well drilling campaign at the Nong Yao field (Block G11/48) in the Gulf of Thailand, including its first multi-lateral development well in the country (NYB-02ST1). The campaign indicates a shift toward more complex well architectures to lift recovery and manage development costs in mature, shallow-water assets.

- July 2025: PTTEP agreed to acquire a 50% participating interest in MTJDA Block A-18 from Chevron subsidiaries for USD 450 million. The transaction deepens PTTEP's exposure to joint-development area gas supply and reinforces its operated portfolio around established offshore infrastructure.

- July 2024: Chevron handed over a wellhead platform topside to Carigali-PTTEPI Operating Company (CPOC) for reuse in the Malaysia-Thailand Joint Development Area. Reusing major offshore hardware reduces capital intensity and can shorten execution cycles for incremental developments linked to existing gas hubs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Thailand oil and gas upstream market is defined as the value of activities that support exploring, developing, producing, and decommissioning oil and gas assets within Thailand, across onshore and offshore areas.

Scope exclusions: We exclude midstream and downstream operations such as transportation pipelines, LNG regasification, refining, petrochemicals, and fuel retailing.

Segmentation Overview

-

By Location of Deployment

- Onshore

- Offshore

-

By Resource Type

- Crude Oil

- Natural Gas

-

By Well Type

- Conventional

- Unconventional

-

By Service

- Exploration

- Development and Production

- Decommissioning

Data Sources, Market Sizing, and Validation

Desk Research

To start the model, we built a clean picture of Thailand upstream activity using public datasets that are broadly consistent year to year. Sources used include official energy statistics and bulletins, hydrocarbon licensing and field updates published by regulators, and central bank or national accounts series that help align currency timing and inflation adjustments.

We also reviewed upstream-relevant disclosures and project updates from company annual reports, investor presentations, and releases from industry associations and reputable business press. Where the public record is thin, paid subscriptions were used selectively for company financials and intelligence, news and financials, and patent databases, mainly to cross-check timelines, capex cues, and major project milestones. The desk sources listed here are illustrative, and we also referenced other public documents and datasets to fill gaps and test the assumptions.

Primary Interviews and Surveys

After the desk work was drafted, we validated the demand signals through expert interviews and structured surveys with upstream operators, service firms, and advisors who track Thailand developments closely. Because offshore activity and gas-led projects can shift quickly based on approvals and work programs, we used respondents across job roles to confirm unit costs, activity levels, and the timing of execution across Thailand onshore and offshore.

Distribution of primary research fieldwork respondents was designed to capture both cost drivers and execution timing signals that affect upstream spend mapping.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | |

| Mid tier: 56% | Functional/Unit leaders: 32% | |

| Smaller Players: 18% | Managers: 52% |

Market-Sizing & Forecasting

Sizing was built using both a top-down and bottom-up logic, with the top-down pathway anchored on Thailand upstream activity indicators. In practice, production volumes, active field development signals, and published work-program direction were converted into spend pools, and then mapped to upstream service groupings.

To keep totals realistic, we corroborated them with selective bottom-up checks such as sampled project spend by field phase, channel checks on typical service rates, and volume multiplied by average cost ranges where activity could be observed. Key inputs included oil and gas production trends, offshore versus onshore activity mix, drilling and well intervention intensity, decommissioning schedules, and movements in input costs that influence service pricing. Where company or field level detail was missing, we bridged gaps using proxy ratios from comparable Thai projects and then tightened them through expert feedback.

For forecasting, we used scenario analysis so outlooks could reflect changes in work-program timing, policy signals, and commodity-price expectations without forcing a single path. The scenario paths were then reconciled against what interviewees expected for offshore ramp-ups, maintenance cycles, and the pace of late-life asset retirement.

Data Validation & Update Cycle

Before sign-off, results are triangulated against independent signals such as production direction, known project milestones, and service activity commentary, and then checked for year-over-year jumps that do not align with sector realities. If a variance looks large, we re-check assumptions, review currency conversion timing, and, where needed, re-contact primary sources for clarification.

Each report is refreshed annually, and interim updates are made when material events occur, such as a major award, delay, or regulatory change that shifts upstream activity. Right before delivery, we do a final pass to ensure the latest public updates are reflected and the model logic remains consistent.

Mordor Intelligence's Thailand Oil and Gas Upstream Market Size Compared Against Other Published Estimates

Published market sizes for Thailand upstream often differ because the counted spend is not defined the same way across studies, and because base-year timing, currency conversion, and pricing logic are handled differently.

In this market, the biggest gaps usually come from whether decommissioning is counted as part of upstream services, whether unconventional categories are included in a country where they are limited, and whether values reflect realized activity levels or broader investment intentions. Some estimates also use aggressive price escalation for service rates, while others hold costs flat even when offshore work scopes tighten.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.33 B (2025) | |

| Global Consultancy A | USD 5.10 B (2024) | Uses a wider upstream definition that can fold in adjacent technologies and broader activity, and the earlier base year can inflate value when currency timing and service cost movements are not aligned to the same window. |

| Trade Publisher B | USD 10.00 B (2024) | Appears to describe upstream exploration in a way that can mix investment ambition with realized activity, which can overstate spend when project timelines, offshore ramp-ups, and decommissioning schedules are not validated to current work programs. |

The spread is mainly explained by how tightly the model sticks to Thailand realized upstream activity and which service buckets are counted, with decommissioning treated as in-scope and non-upstream value-chain items kept out, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the Thailand oil and gas upstream market?

It was USD 3.52 billion in 2026 and is projected to rise to USD 4.62 billion by 2031.

How fast is offshore production expected to grow?

Offshore volumes should increase at a 5.78% CAGR through 2031 as deeper-water and tie-back projects come online.

Which resource type dominates Thailand's upstream portfolio?

Natural gas supplies 77.85% of output, driven by long-term offtake contracts with power generators.

What fiscal changes were introduced in the latest licensing rounds?

The 24th and 25th rounds added production-sharing contracts that balance government take with investor incentives.

How is Thailand addressing high-CO2 reservoirs?

Commercial CCS pilots, starting with the Arthit field in 2027, will inject captured CO? to enhance recovery while storing emissions.

Who leads the domestic upstream sector?

PTTEP commands more than 80% of national gas production and holds operatorship of 15 offshore blocks.

Page last updated on: