Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

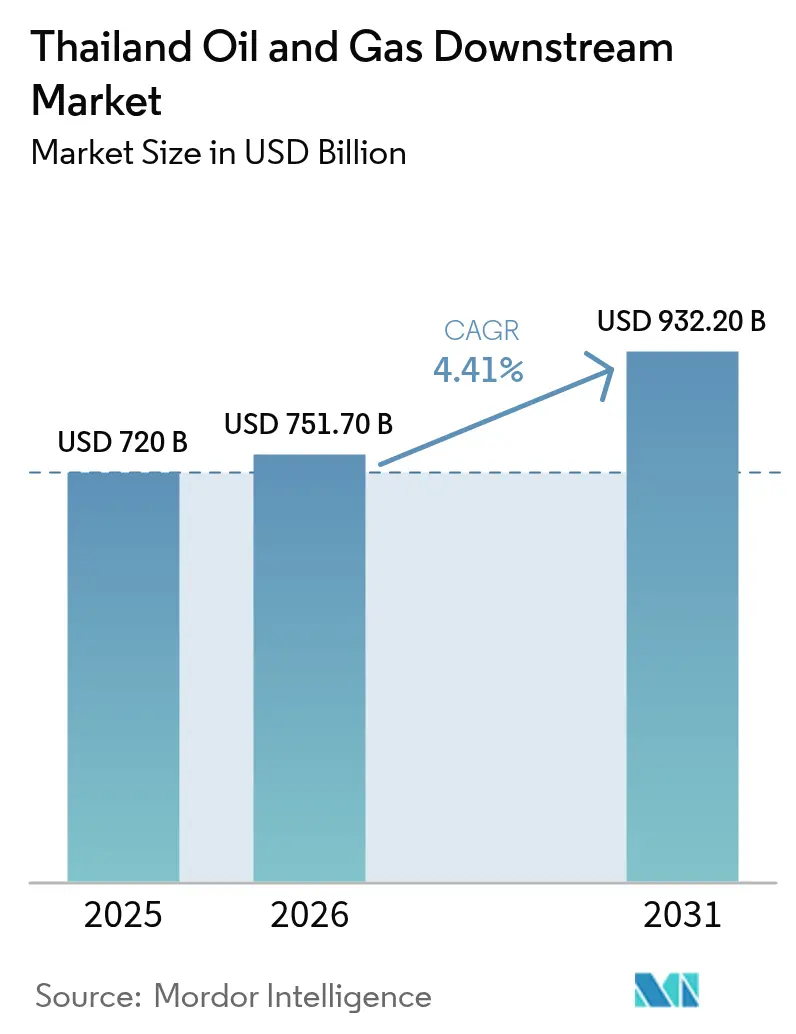

| Base Year Market Size (2025) | USD 720 Billion |

| Market Size (2026) | USD 751.7 Billion |

| Market Size (2031) | USD 932.2 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

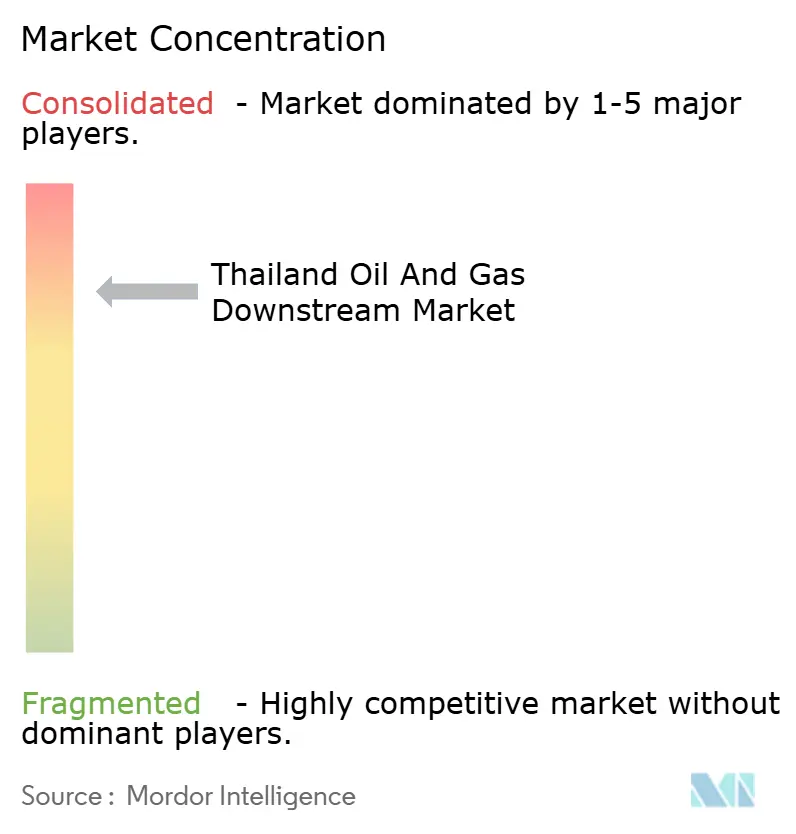

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Oil And Gas Downstream Market Analysis by Mordor Intelligence

The Thailand Oil And Gas Downstream Market size is expected to grow from USD 720 million in 2025 to USD 751.7 million in 2026 and is forecast to reach USD 932.2 million by 2031 at 4.41% CAGR over 2026-2031.

Tourism rebound, a steady e-commerce logistics boom, and government-backed clean-fuel policies underpin this moderate yet resilient growth path. Integrated refiners are already optimizing utilization rates to capture recovering jet fuel and gasoline demand, while feedstock-flexible petrochemical units are pivoting toward higher-margin specialty chemicals. Policy tailwinds, such as Euro-5 fuel specifications and a national carbon tax, are set to lift product premiums and reward operators that upgrade their desulfurization and octane-boosting units. At the same time, digitalized retail networks with EV-charging bays and data-driven loyalty apps are widening non-fuel revenue streams and partially insulating margins against long-term electrification headwinds.

Key Report Takeaways

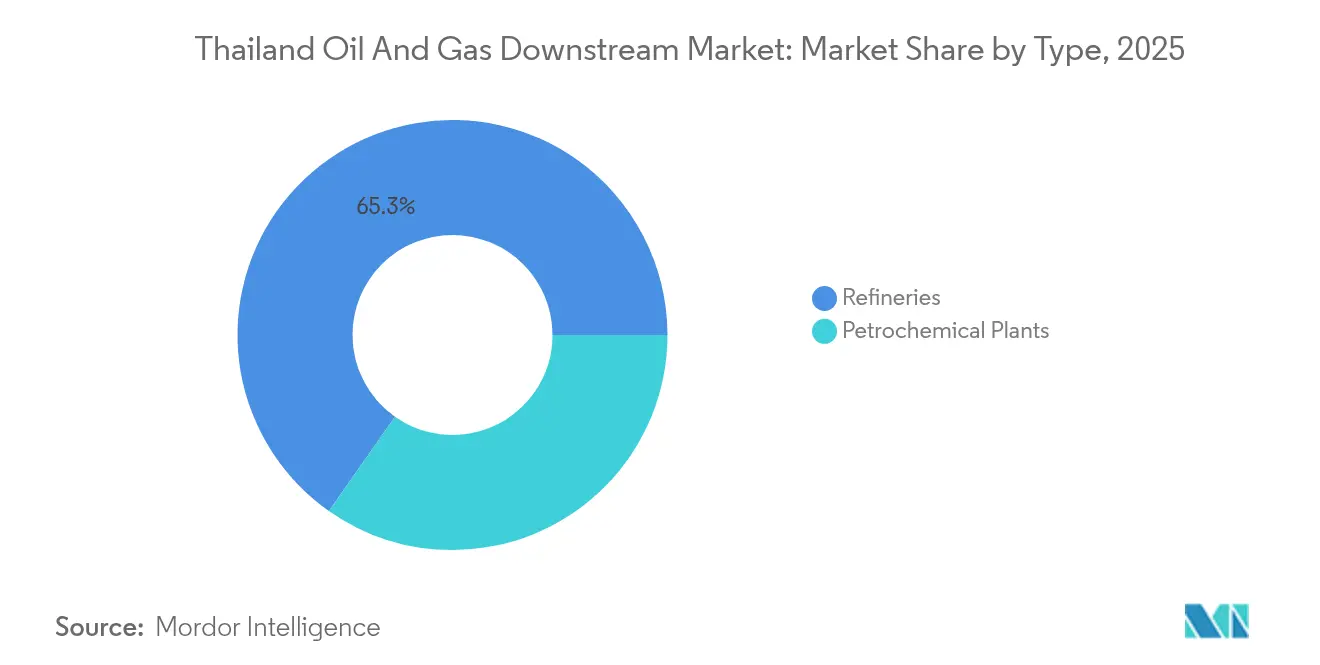

- By type, refineries commanded 65.25% of the Thailand oil and gas downstream market share in 2025, while petrochemical plants are projected to post the fastest growth rate of 4.85% through 2031.

- By product type, refined petroleum products accounted for 69.80% of the Thailand oil and gas downstream market size in 2025; petrochemicals are poised to accelerate at a 5.08% CAGR through 2031.

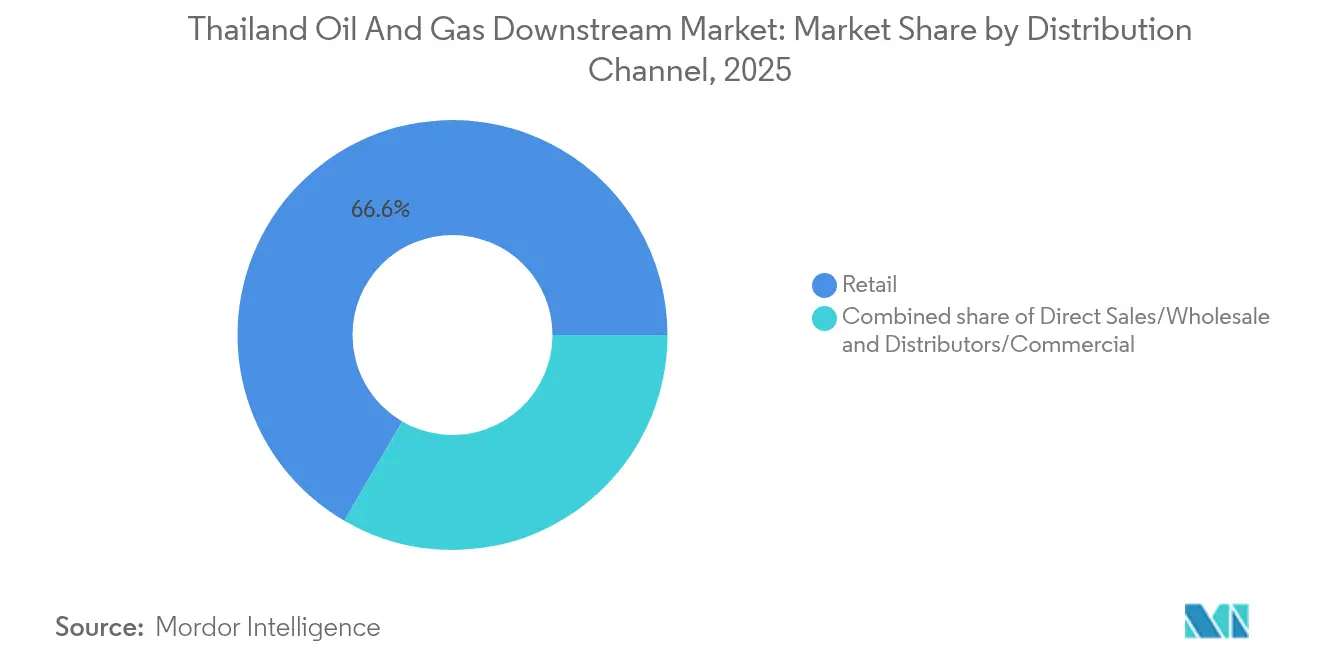

- By distribution channel, retail networks held 66.60% of the Thailand oil and gas downstream market size in 2025, whereas distributors and commercial sales are forecast to advance at a 4.62% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gradual recovery in domestic refined-product demand as tourism returns and e-commerce logistics expand | +1.2% | Bangkok, Phuket, Chiang Mai corridors | Short term (≤ 2 years) |

| Euro-5/clean-fuel upgrades unlocking higher margins post-2026 | +0.9% | Bangkok Metropolitan Region | Medium term (2-4 years) |

| State Oil Plan 2025: carbon-tax phase-in accelerating refinery efficiency projects | +0.7% | Map Ta Phut, Rayong industrial clusters | Medium term (2-4 years) |

| Rapid service-station network digitalization (EV chargers & retail platforms) boosting downstream profitability | +0.5% | Urban centers nationwide | Short term (≤ 2 years) |

| Petrochemical feedstock flexibility projects (propane/ethane) mitigating naphtha price shocks | +0.4% | Map Ta Phut and Rayong complexes | Long term (≥ 4 years) |

| Sustainable aviation fuel (SAF) investments creating a new high-value product pool | +0.3% | With export links to Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Recovery Drives Refined Product Demand Resurgence

Jet fuel liftings are nearing pre-pandemic run-rates as international arrivals climb toward the 40 million mark, reviving gasoline and diesel pull through hospitality and logistics services.[1]International Energy Agency, “Oil 2025 – Southeast Asia Demand Outlook,” iea.org Last-mile e-commerce fleets add incremental diesel line-haul demand across Bangkok’s peri-urban sprawl, extending the utilization window for mid-complexity refineries. Operators that throttled throughput during the pandemic are now executing planned turnarounds early to maximize availability during the 2025-2026 high season. Compared with peers where inbound travel lags, the Thailand oil and gas downstream market enjoys a first-mover demand recovery that supports crack spreads. The country’s current 10% EV penetration remains too low to significantly impact aggregate liquid-fuel growth before 2027, creating a multi-year cushion for refiners to recoup upgrade capital expenditures.

Euro-5 Standards Create Margin Expansion Pathway

Mandatory Euro-5 gasoline and diesel specifications, effective January 2027, will widen the pricing gap between compliant and non-compliant supplies by an estimated 5-15%. Complex refineries equipped with new resid-upgrading trains and high-capacity desulfurizers can capture this premium while also reducing carbon tax liabilities. Imported middle-distillate demand from non-compliant ASEAN peers offers an additional outlet, positioning Thailand as a clean-fuel export hub. Project timelines, such as the 400,000 barrels-per-day Clean Fuel Project, are aligned to ramp ahead of enforcement, thereby reinforcing economies of scale. Smaller standalone units face upgrade hurdles, accelerating the shift toward integrated refining and petrochemical super-sites that can recycle hydrogen and process heavier crudes at a lower marginal cost.

State Oil Plan 2025 Accelerates Efficiency Investments

The Thai Cabinet’s decision to embed a THB 200-per-tonne CO₂ carbon tax within existing excise structures will fundamentally reshape refinery cost curves starting in July 2025.[2]Royal Thai Government, “Cabinet Resolution on Energy Tax Reform,” thaigov.go.th Efficient sites with less than 27 kg CO₂/boe process emissions will experience only marginal tax exposure, whereas older hydroskimming assets may incur a 10-15% EBIT squeeze unless mitigation projects are fast-tracked. The policy is revenue-neutral to consumers yet funnels predictable cash flows into national decarbonization funds, spurring voluntary carbon market activity linked to downstream abatement. Integrated players are packaging flare-gas recovery, pre-combustion carbon capture, and renewable power purchase agreements into bundled offset plans, creating early compliance cost advantages.

Digital Transformation Enhances Retail Profitability

Mobile-first payment ecosystems and government e-wallet incentives have driven cashless fuel purchases to above 85%, enabling station operators to conduct granular loyalty analytics.[3]Nation Thailand, “Digital Fuel Retail Gains Momentum,” nationthailand.com New-build flagship sites in Bangkok and Chiang Mai co-locate 150 kW EV fast chargers, coffee franchises, and parcel lockers, pushing non-fuel gross margins above 35%. Dynamic pricing engines adjust pump prices every three hours, optimizing volumes in response to wholesale rack movements. The Thailand oil and gas downstream market, therefore, sees retail chains morphing into multi-energy micro-hubs that bridge the combustion-to-electrification transition. Operators capturing vehicle telemetry data are monetizing insights with insurers and fleet managers, creating cross-industry revenue pools that offset declining gasoline consumption per car after 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China-led petrochemical over-capacity compressing cracker/polymer spreads | -0.8% | Map Ta Phut and Rayong | Medium term (2-4 years) |

| Rising single-pool-gas feedstock costs squeezing LPG & GSP margins | -0.6% | Gas-dependent facilities nationwide | Short term (≤ 2 years) |

| Carbon-border measures (EU CBAM, CORSIA) threatening export economics for high-CO₂ fuels | -0.4% | Export-oriented refineries & petrochemical plants | Medium term (2-4 years) |

| Accelerating EV adoption eroding gasoline demand sooner than forecasts | -0.5% | Urban centers with dense charging grids | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China's Petrochemical Overcapacity Pressures Regional Margins

More than 30 million tonnes per annum (mta) of new Chinese ethylene capacity commissioned since 2024 has pulled spot monomer prices toward the bottom quartile of the global cost curve, shrinking Southeast Asian cracker margins to USD 150 per tonne.[4]The Investor, “China’s Petrochemical Push Threatens Regional Margins,” theinvestor.co.kr Thai operators reliant on naphtha feedstock see disproportionate pressure because Chinese complexes run inexpensive coal-to-olefin or ethane-based routes backed by provincial incentives. Margin compression accelerates the strategic pivot toward specialty chemicals, engineering plastics, and downstream integration, where price elasticity is lower, thereby enhancing profitability. While temporary anti-dumping duties offer limited respite, long-run competitiveness hinges on energy-efficiency retrofits and feedstock flexibility—investments already prioritized under the 2023-2027 national petrochemical roadmap.

Carbon Border Measures Threaten Export Competitiveness

The EU Carbon Border Adjustment Mechanism (CBAM) trial phase and ICAO’s CORSIA offset scheme push embedded-carbon reporting obligations onto Thai fuel and polymer exporters starting 2026. In the absence of third-party verified lifecycle assessments, shipments risk facing levies of EUR 80-100 per tonne, which erode price advantages. Export-oriented refiners are therefore fast-tracking the development of digital MRV platforms and bio-content certification to retain market access. While the Thai oil and gas downstream market still enjoys ASEAN demand pull, the loss of EU routes could strand capacity unless operators decarbonize their production or pivot volumes into emerging South Asian markets with less stringent import rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dominance of Refineries Amid Petrochemical Upswing

Refineries captured 65.25% of the Thai oil and gas downstream market share in 2025, as 1.24 million barrels per day of installed distillation capacity met resurging mobility fuel demand. The Thailand oil and gas downstream market size for refineries is projected to increase at a 3.68% CAGR through 2031, as Euro-5 compliance premiums and regional jet-fuel deficits support utilization. Petrochemical plants, growing at a 4.85% CAGR, are underpinned by investments such as PTT Global Chemical’s USD 4.4 billion “3 Steps Plus” program that adds downstream polyurethane and biodegradable PLA lines. Integrated sites leverage shared utilities and hydrogen networks, trimming operating costs by 5-7% and sharpening their strategic focus toward mixed-feed flexibility. Chinese overcapacity remains the chief headwind; however, Thai complexes counter with specialty niches, including bio-ethylene and high-purity ABS, which command resilient premiums.

A parallel differentiation track is unfolding around carbon intensity. New-build hydrocrackers paired with gas-fired cogeneration units emit 12-15% less CO₂ per barrel than decade-old hydroskimmers, thereby cushioning carbon-tax exposure. Retrofits bundling waste-heat recovery and flue-gas desalination further lower compliance costs, attracting green-finance-linked loans at sub-LIBOR spreads. Collectively, these moves help sustain the Thai oil and gas downstream market’s refinery core, even as petrochemical earnings outgrow fuel sales.

By Product Type: Refined Fuels Lead While Petrochemicals Accelerate

Refined products accounted for 69.80% of Thailand's oil and gas downstream market size in 2025, buoyed by a doubling of jet fuel demand from 2022 lows and domestic diesel demand from e-commerce fleets. Structural tailwinds include regional tightening of fuel quality and Myanmar's pipeline export flows, which together keep middle-distillate cracks attractive until at least 2027. Petrochemicals, advancing at a 5.08% CAGR, increasingly tilt toward high-value elastomers and engineering resins supplied to Southeast Asian electronics and automotive clusters. Operators such as IRPC raised their polyolefin nameplate capacity to 931 kta in mid-2024, capturing polypropylene demand linked to consumer goods packaging.

Lubricants form a niche subsector, generating steady mid-single-digit growth through premium synthetics for ride-hailing fleets and industrial MRO segments. Sustainable aviation fuel—though only 0.2 % of national jet demand in 2024—registers the fastest volume growth trajectory, backed by offtake deals with regional carriers under CORSIA. The evolving product mix diversifies earnings and mitigates volatile refinery gross refining margins, reinforcing the shift in Thailand's oil and gas market toward value-added outputs.

By Distribution Channel: Retail Networks Retain Scale Advantages

Retail outlets captured 66.60% of the Thailand oil and gas downstream market size in 2025, owing to 13,500 active service stations that embed fuel sales within convenience store footprints. Digital payments, loyalty apps, and cross-selling of food services increased the non-fuel margin contribution above 35% for leading chains, mitigating pressure from flat to declining per-car gasoline volumes after 2028. Distributors and commercial bulk sales, which are growing at a 4.62% CAGR, benefit from industrial restocking in Eastern Economic Corridor zones and mining fuel contracts in neighboring Laos and Cambodia.

Wholesale channels focused on bunker fuel and aviation deliveries offer scale but suffer higher spot-price volatility, pushing traders toward longer-term offtake agreements indexed to Singapore swaps. Integrated players—owning refineries, terminals, and retail—optimize arbitrage by dynamically diverting barrels among channels based on margin signals. In aggregate, distribution-channel diversification reinforces revenue resilience and sustains the profitability of Thailand's oil and gas downstream market as mobility electrifies.

Geography Analysis

Eastern Thailand anchors the Thai oil and gas downstream market, with Map Ta Phut, Rayong, and Sattahip hosting 75% of the nation's refining and petrochemical throughput, thanks to deep-water jetties and extensive pipeline grids that link to Bangkok's vast fuel demand centers. The zone's clustering reduces logistics costs by 18% versus standalone inland assets and supports integration synergies across fuels, olefins, and aromatics. Northern provinces, such as Chiang Mai, see steady fuel uplift from tourism-led mobility, although limited industrial bases keep throughput shares below 5%. Central Thailand, driven by Bangkok's 11 million residents and Thailand's highest vehicle density, accounts for more than 40% of the nation's gasoline demand, thereby anchoring retail margins and sustaining large terminal capacities.

Cross-border flows deepen geographic relevance. Pipeline exports to Laos and tank-truck deliveries into Cambodia translate into roughly 85 kbd of refined-product offtake, cushioning domestic demand cyclicality. On the import side, crude oil delivered via the Strait of Malacca exposes the Thailand oil and gas downstream market to shipping disruptions; hence, the government maintains strategic petroleum reserves equivalent to 180 days of net imports. Renewable power expansion, aimed at 51% of generation by 2037, will reduce gas-oil demand in the power sector while leaving transportation fuels structurally tight until EV adoption surpasses a 30% fleet share, projected for 2032.

Geographic concentration also heightens environmental scrutiny. Provinces hosting large complexes have implemented real-time SOx and NOx monitoring, tying emissions breaches to immediate production curbs. Operators are increasingly securing renewable electricity PPAs from wind and solar farms in Nakhon Ratchasima to lower their Scope 2 emissions, leveraging grid access to green their value chains. The combined geography-driven advantages and constraints create a nuanced landscape in which strategic siting, infrastructure redundancy, and community engagement all play a crucial role in determining long-term competitiveness.

Competitive Landscape

Thailand's downstream sector is moderately consolidated, with the PTT Group, Thai Oil, Bangchak, IRPC, and PTT Global Chemical collectively accounting for approximately 58% of the country's distillation capacity and over 60% of its polymer output. International majors such as Shell and TotalEnergies operate through JV refineries or branded retail networks, adding marketing sophistication and premium-fuel positioning. Integrated value chains, from crude import to retail, give incumbents scale economies that deliver 4-6 USD/barrel operating cost advantages over prospective entrants. Capital-intensive Euro-5 upgrades and the 2025 carbon tax further raise entry hurdles, solidifying incumbents' competitive moat.

Technology deployment is reshaping hierarchy. PTT is piloting a 45 MW green-hydrogen electrolyzer at Rayong, scheduled to start up in 2026, while Thai Oil integrates post-combustion carbon capture into its clean-fuel revamp. Digital twins and predictive maintenance are rolling out across catalytic reformers, slashing unplanned downtime by 25% and boosting effective capacity. On the retail front, Bangchak's "B-eV" platform is bundling subscription-based charging with insurance tie-ups, widening revenue scope beyond fuel. Mid-tier independents leverage strategic alliances to access these technologies via shared services, reflecting a collaborative rather than purely competitive industry ethos.

M&A prospects remain active as smaller standalone refiners navigate compliance and capital expenditures. Rumors of foreign strategic stakes in gas fractionation and aromatics units surface periodically, yet national-interest considerations and energy-security objectives temper full asset sales. Overall, the Thailand oil and gas downstream market balances scale-driven incumbency with innovation-led repositioning, a duality that shapes competitive dynamics over the next decade.

Thailand Oil And Gas Downstream Industry Leaders

PTT Public Company Limited (incl. Thai Oil, IRPC, OR)

Bangchak Group (Bangchak + BSRC)

Esso (Thailand) PCL

Star Petroleum Refining PCL (Chevron)

SCG Chemicals & PTTGC (petrochemical-heavy)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Thai Cabinet approved a THB 200-per-tonne CO₂ carbon tax on oil and petroleum products, creating ASEAN’s first downstream carbon-pricing mechanism.

- February 2024: Thai Oil shareholders endorsed a THB 63.02 billion budget increase for the Clean Fuel Project, lifting capacity to 400,000 bpd and enabling Euro-5 compliance.

- November 2024: SCG pledged an additional USD 700 million to Vietnam’s Long Son complex for the conversion of U.S. ethane feedstock, illustrating Thai companies’ regional expansion.

- June 2024: The Thailand Board of Investment cleared Braskem-SCG’s THB 19.3 billion bio-ethylene plant with 200 kta capacity, the nation’s largest bio-petrochemical investment.

Thailand Oil And Gas Downstream Market Report Scope

Downstream operations are oil and gas processes that occur after the production phase to the point of sale. These processes are the final step in the path that oil and gas take from being in the ground to being in the hands of consumers.

The Thai oil and gas downstream market is segmented by refineries, petrochemical plants, and fuel retail and marketing. The market sizing and forecasts have been done based on refining capacity (thousand barrels per day).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the current value of the Thailand oil and gas downstream market?

The Thailand oil and gas downstream market size reached USD 751.7 million in 2026 and is projected to grow to USD 932.2 million by 2031.

How fast is the sector growing between 2025 and 2031?

Aggregate revenue is forecast to rise at a 4.41% CAGR, supported by tourism-led fuel demand and clean-fuel policy incentives, over the 2026-2031 period.

Which segment is expanding the quickest?

Petrochemical plants are expected to post the fastest 4.85% CAGR through 2031, outpacing the refinery segment.

How will Euro-5 standards affect refiners?

Compliance will enable a 5-15 % product premium and favor operators that have already funded desulfurization and octane-boosting upgrades.

What impact does the new carbon tax have on operators?

Facilities with lower carbon intensity gain a cost advantage, while older hydroskimmers could face a 10-15 % EBIT squeeze without efficiency retrofits.

Are EVs a major threat to fuel demand in Thailand?

EV adoption hit 10% in 2023 and will only materially dent gasoline demand after 2027, giving refiners a multi-year window to diversify revenue streams.

Page last updated on: