Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

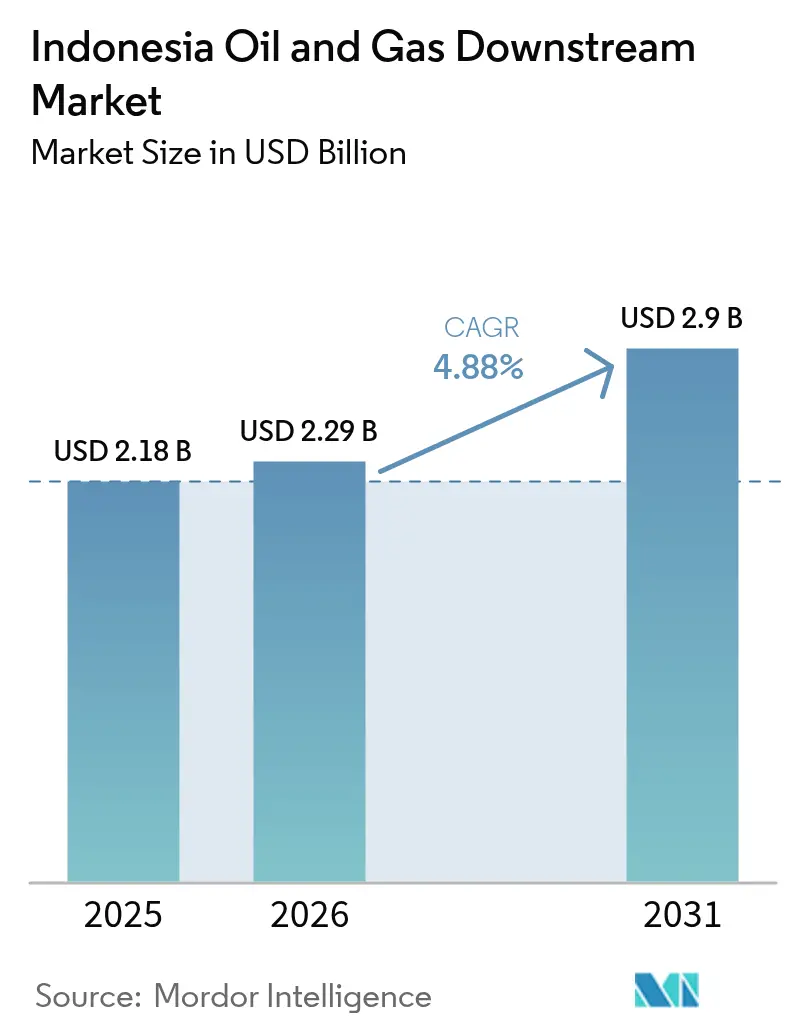

| Base Year Market Size (2025) | USD 2.18 Billion |

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 2.9 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

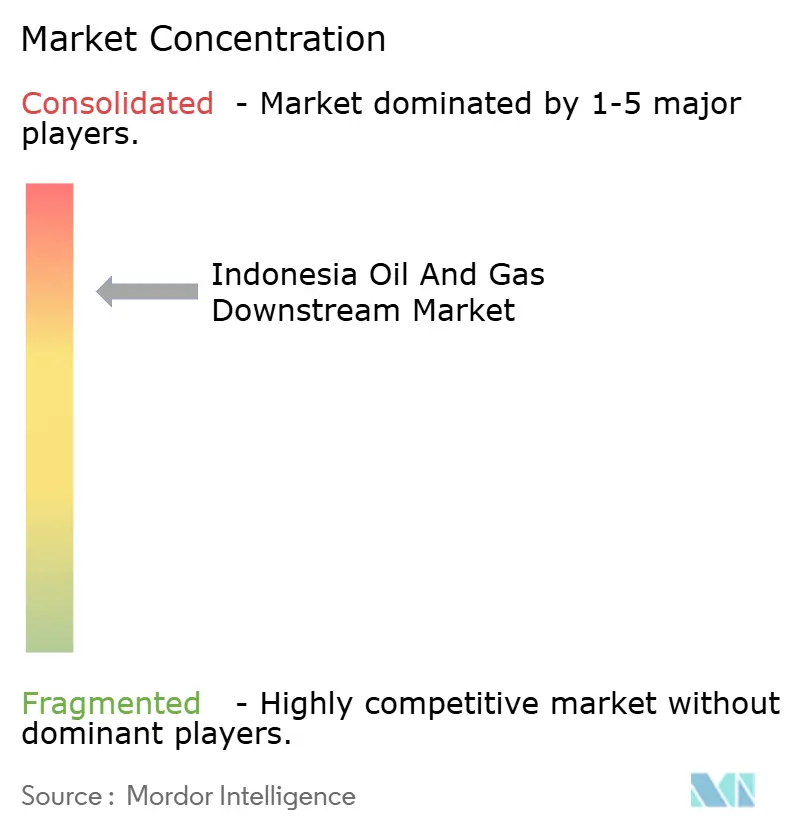

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Oil And Gas Downstream Market Analysis by Mordor Intelligence

Indonesia Oil And Gas Downstream Market size in 2026 is estimated at USD 2.29 billion, growing from 2025 value of USD 2.18 billion with 2031 projections showing USD 2.9 billion, growing at 4.88% CAGR over 2026-2031.

Strong government backing for refinery expansions, rising domestic fuel demand, and world-scale petrochemical investments underpin this trajectory. Additional momentum comes from tighter fuel-quality rules that spur refinery upgrades and from escalating biodiesel blending mandates that pull more palm-oil feedstock into downstream processing. International majors are entering through joint ventures, prompting local players to modernize assets and strengthen cost positions. Intense competition from Singapore and Malaysia presses Indonesian operators to leverage domestic feedstock advantages and state incentives for new complexes.

Key Report Takeaways

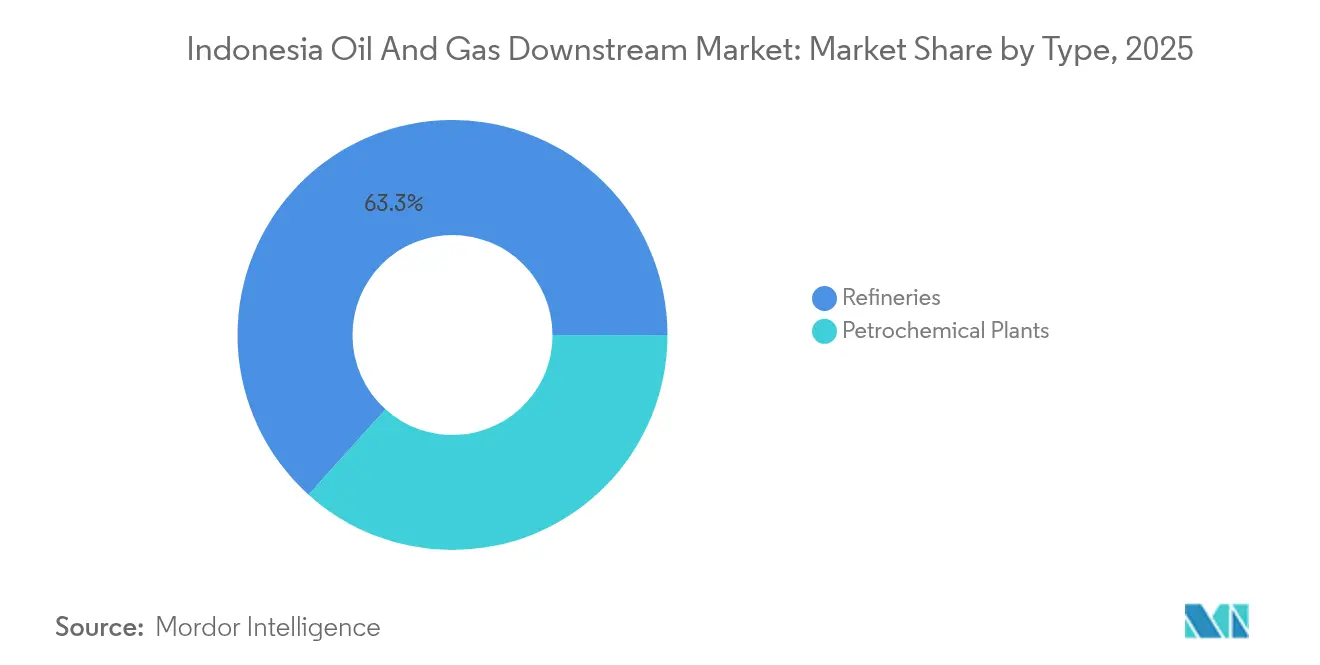

- By type, refineries controlled 63.32% of Indonesia's oil and gas downstream market share in 2025, while petrochemical plants are set to log the fastest 6.55% CAGR through 2031.

- By product type, refined petroleum products held a 57.96% share of the Indonesian oil and gas downstream market size in 2025, whereas petrochemicals are forecast to expand at a 6.6% CAGR to 2031.

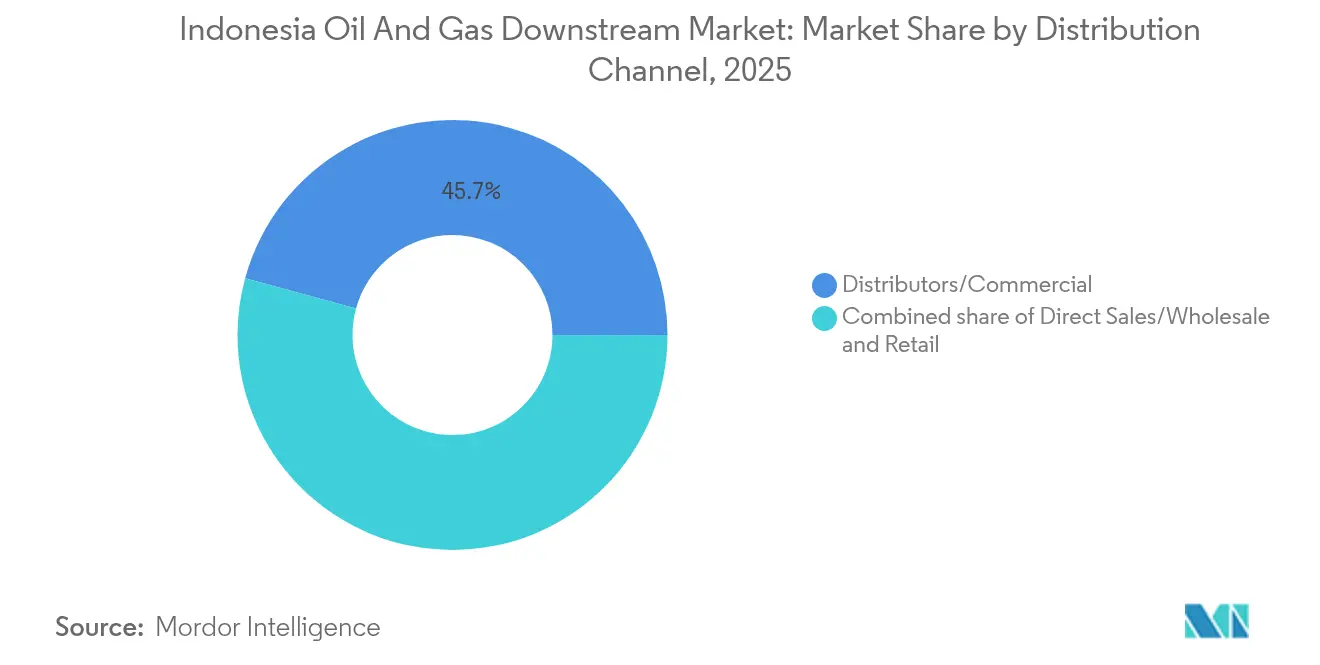

- By distribution channel, distributors and commercial sales captured a 45.74% share in 2025, yet retail channels are advancing at a 6.32% CAGR amid Pertamina's station modernization program.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push to expand domestic refining capacity | 1.50% | National, concentrated in Java, Kalimantan, Sulawesi | Medium term (2-4 years) |

| Rising domestic fuel demand from transport & industry | 0.80% | National, urban centers and industrial zones | Long term (≥ 4 years) |

| Surge in investments for world-scale petrochemical complexes | 0.90% | Java and Sumatra coastal areas | Medium term (2-4 years) |

| Implementation of B35 biodiesel blending mandate | 0.70% | National, palm oil producing regions | Short term (≤ 2 years) |

| Mandatory Euro-4 sulfur limits driving refinery upgrades | 0.60% | National, existing refinery locations | Medium term (2-4 years) |

| Airport network expansion spurring jet-fuel value-chain projects | 0.50% | Major airports and aviation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push to Expand Domestic Refining Capacity

Indonesia doubled its planned additions from 500,000 to 1 million barrels per day across 16 sites, creating regional hubs that cut logistics costs and lift energy security.[1]Indonesian Ministry of Energy and Mineral Resources, “Refinery Expansion Roadmap,” esdm.go.id Balikpapan’s upgrade, now 91% complete, illustrates the technical depth and capital outlay required for Euro-4 fuel compliance. Distributed capacity also aligns with the industrial policy that shifts value from raw exports to processed fuels. Success hinges on securing crude supplies and training personnel capable of operating advanced hydrotreaters. The program positions Indonesia to reduce import dependence while supporting future petrochemical integration.

Rising Domestic Fuel Demand from Transport & Industry

GDP growth and urbanization accelerate vehicle ownership, aviation traffic, and factory output, stretching local supply and raising import bills.[2]Bank Indonesia, “Economic Report 2024,” bi.go.id Infrastructure, such as new toll roads and industrial estates, deepens regional fuel demand. Aviation route expansion increases jet-fuel needs, which require higher-spec refiners. Sustained demand gives investors confidence despite crude price swings, yet it magnifies exposure to external oil-price shocks.

Surge in Investments for World-Scale Petrochemical Complexes

Projects like Lotte Chemical’s USD 4 billion facility in Banten and ExxonMobil’s USD 15 billion East Java complex combine scale with carbon-capture technology.[3]Lotte Chemical, “Investor Presentation 2024,” lottechem.com Investors capitalize on competitive natural-gas pricing, palm-oil feedstocks, and tax incentives. Domestic firms such as Chandra Asri join the build-out, boosting employment and technology transfer. The wave strengthens Indonesia’s bid to become a regional chemical hub, though it heightens competition for gas and skilled labor.

Implementation of B35-to-B40 Biodiesel Mandate

Nationwide B40 blending, which began in mid-2024, has increased biodiesel demand by 2.3 million tons per year, thereby boosting palm-oil utilization and reducing fossil fuel imports.[4]Indonesian Palm Oil Association, “Biodiesel Implementation Update,” gapki.id Higher blends require upgraded storage, specialized pumps, and rigorous quality controls adhering to national standards. Distributors adjust logistics while integrators explore co-locating biodiesel and traditional fuel units to optimize throughput. Success depends on synchronizing palm-oil supply with fuel sales, ensuring stable economics for both sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental & decarbonization pressures on fossil assets | -0.70% | National, concentrated in industrial areas | Long term (≥ 4 years) |

| Chronic delays & cost overruns in refinery megaprojects | -0.50% | Major refinery development sites | Medium term (2-4 years) |

| Shortage of advanced downstream technical workforce | -0.40% | National, acute in specialized facilities | Long term (≥ 4 years) |

| Margin squeeze from Singapore/Malaysia hub competition | -0.30% | Regional, affecting export-oriented facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental and Decarbonization Pressures on Fossil Assets

Indonesia’s Net Zero 2060 pledge attracts stricter emission rules and potential carbon pricing that inflate operating costs. Global lenders deploy ESG filters, limiting finance for traditional plants unless carbon-capture modules are integrated. Extended permitting and civil-society scrutiny can hold back new builds, raising the specter of stranded assets as cleaner energy alternatives scale up. Operators must weigh near-term demand against long-run climate liabilities.

Chronic Delays and Cost Overruns in Refinery Megaprojects

The Pertamina-Rosneft Tuban project, now scheduled for 2026, exemplifies the challenges of land acquisition and contractor coordination. Inflation in steel and specialized equipment pushes budgets beyond initial scopes, forcing renegotiations and eroding investor confidence. Slippage cascades into crude-supply contracts and product offtake deals, complicating cash flows and dampening sector credibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refineries Anchor Market Foundation

Refineries remained the backbone, with a 63.32% share of Indonesia's oil and gas downstream market in 2025, underpinned by government programs aimed at doubling national throughput. The Indonesian oil and gas downstream market size attributed to refineries is forecast to expand steadily through 2031 as Balikpapan and Tuban come online. Margins, however, face pressure from higher environmental compliance costs and tighter regional competition. Petrochemical plants, aided by world-scale complexes, are projected to record a 6.55% CAGR, reflecting shifting value toward higher-margin chemicals. International majors supply advanced process technology and capital, while domestic firms provide regulatory insight and local logistics.

The integration trend blurs the boundaries between refinery and chemical operations, allowing for shared feedstock optimization and an economy of scope. Combined sites capture naphtha streams for cracker units, improving overall utilization. Workforce challenges persist, as high-skill engineers often migrate abroad, prompting the development of joint training programs. Government oversight ensures safety and environmental performance, though enforcement consistency varies across provinces.

By Product Type: Petrochemicals Drive Value Creation

Refined petroleum products accounted for 57.96% of Indonesia's oil and gas downstream market share in 2025, supplying gasoline, diesel, and jet fuel to the growing transport and industrial sectors. The Indonesian oil and gas downstream market size linked to refined fuels is expected to expand slowly as efficiency gains counterbalance vehicle growth. Petrochemicals, led by ethylene and polyethylene, are expected to post the fastest 6.6% CAGR, driven by Asian demand and local feedstock advantages. Companies leverage natural-gas derivatives and palm-oil-based chemicals to tap higher value pools.

Quality standards tighten across all product lines, compelling investment in hydrocrackers and finishing units. Lubricants capture niche growth from rising automotive sales, while specialty chemicals benefit from the expansion of packaging and consumer-goods manufacturing. Digital batch tracking enhances quality assurance, bolstering export credibility to regional buyers.

By Distribution Channel: Retail Modernization Accelerates Growth

Distributors and commercial bulk sales accounted for 45.74% of total 2025 revenue, reflecting a dependence on large buyers, such as power plants and transportation fleets. Retail channels, although smaller, are projected to rise at a 6.32% CAGR as Pertamina refurbishes its stations with cashless payment, convenience retail, and alternative fuel options. The Indonesian oil and gas downstream market, tied to retail, is expected to benefit from expanding passenger-car ownership and the growth of ride-hailing services.

Bulk channels focus on custom blends and just-in-time delivery to mining and manufacturing sites scattered across the archipelago. Digital logistics platforms optimize routing and inventory for remote islands, reducing stockouts. Foreign brands assess selective entry but face local content and partnership requirements that limit their ability to roll out rapidly.

Geography Analysis

Java hosts the bulk of refining and petrochemical capacity, servicing the nation’s largest consumer base and manufacturing clusters. Sumatra supplies significant crude and palm oil output, supporting integrated biodiesel operations that feed both domestic blending mandates and export markets. The Indonesian oil and gas downstream market share concentrated in Java is expected to moderate as new assets in Kalimantan and Sulawesi come online.

Kalimantan’s planned refinery projects capitalize on the proximity to coal and gas reserves, yet infrastructure gaps and environmental constraints hinder progress. Eastern regions, such as Maluku and Papua, form part of a 16-site expansion plan that targets fuel security, although workforce shortages and higher logistics costs increase project complexity. Coastal sites are favored for petrochemical exports, while inland plants serve as part of the domestic distribution corridors.

Logistical challenges from Indonesia’s archipelagic geography necessitate marine terminals, floating storage, and multi-modal links to ensure a steady supply. Weather disruptions prompt strategic stockpiling on remote islands. Regulatory enforcement varies by province, introducing compliance uncertainty that investors factor into their risk assessments.

Competitive Landscape

PT Pertamina and its subsidiaries have the largest footprint, thanks to their vertically integrated refining, distribution, and retail networks, which underpin a moderately consolidated market. International majors such as TotalEnergies, Shell, and ExxonMobil adopt partnership models, supplying capital and advanced technology while navigating local regulations. The combined share of the five largest players hovers near 55%, maintaining significant but not dominant concentration.

Strategic moves focus on capacity upgrades, carbon capture integration, and digital process control to reduce operating costs and meet Euro 4 and future Euro 5 standards. ExxonMobil’s East Java complex couples refining with sequestration, signaling a pivot toward lower-carbon downstream assets. Shell’s predictive-maintenance rollout reduced operating expenses by 12%, demonstrating the competitive edge gained through digitalization.

Regional rivals in Singapore and Malaysia, who leverage efficient ports and lower compliance costs, are prompting Indonesian firms to utilize domestic feedstock and take advantage of government incentives. Niche entrants are exploring bio-based chemicals and sustainable aviation fuel, although scale and financing remain significant hurdles. Technology partnerships and local workforce development will shape long-term advantages.

Indonesia Oil And Gas Downstream Industry Leaders

PT Pertamina(Persero)

TotalEnergies SE

Shell plc

BP plc

PETRONAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pertamina’s Balikpapan refinery upgrade is 96.5% complete, with the key RFCC unit set to start in Q4 2025. The upgrade will raise capacity from 260,000 to 360,000 bpd and enhance product quality, including gasoline and LPG.

- September 2025: PT Pertamina plans to build a green refinery focused on producing bioavtur (sustainable aviation fuel), announced by Vice President Director Oki Muraza at the SAFE 2025 forum in Jakarta on September 10, 2025.

- August 2025: Indonesia’s state-owned Pertamina plans a USD 48 billion investment to upgrade six refineries and build a new refining-petrochemical complex, aiming to double oil output to 1.5 million bpd.

- May 2025: Lotte Chemical Indonesia, a subsidiary of South Korea’s Lotte Group, has signed a 10-year contract to supply ethylene to Asahimas Chemical for use in downstream manufacturing.

Indonesia Oil And Gas Downstream Market Report Scope

The Indonesian oil and gas downstream market report includes:

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the projected value of the Indonesia oil and gas downstream market by 2031?

The market is forecast to reach USD 2.9 billion by 2031.

Which segment is expected to grow the fastest within Indonesia's downstream sector?

Petrochemical plants are projected to post the highest 6.55% CAGR through 2031.

How much refinery capacity is Indonesia targeting through its expansion program?

The government plans to add 1 million barrels per day across 16 locations by 2030.

What is driving retail fuel channel growth in Indonesia?

Pertamina’s station modernization, cashless payments, and rising vehicle ownership support a 6.32% CAGR in retail sales.

How is Indonesia addressing environmental pressures in downstream operations?

Projects now integrate carbon-capture technology and pursue Euro-4 fuel upgrades to align with Net Zero 2060 commitments.

Page last updated on: