Next-generation Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

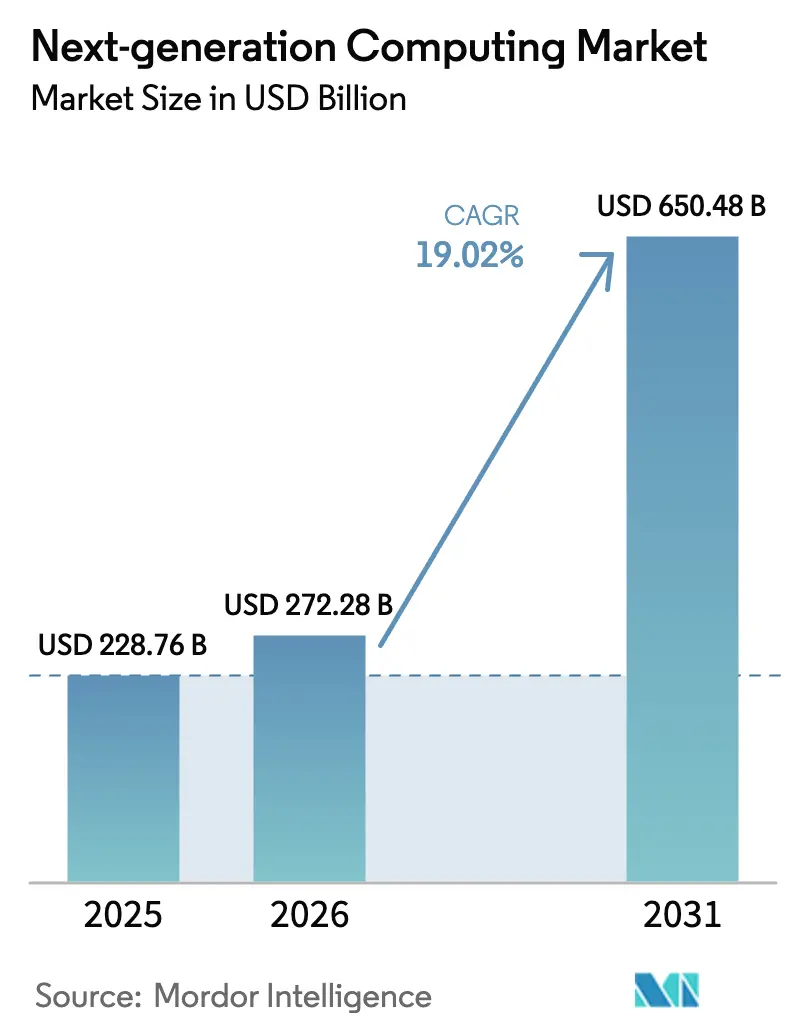

| Market Size (2026) | USD 272.28 Billion |

| Market Size (2031) | USD 650.48 Billion |

| Growth Rate (2026 - 2031) | 19.02% CAGR |

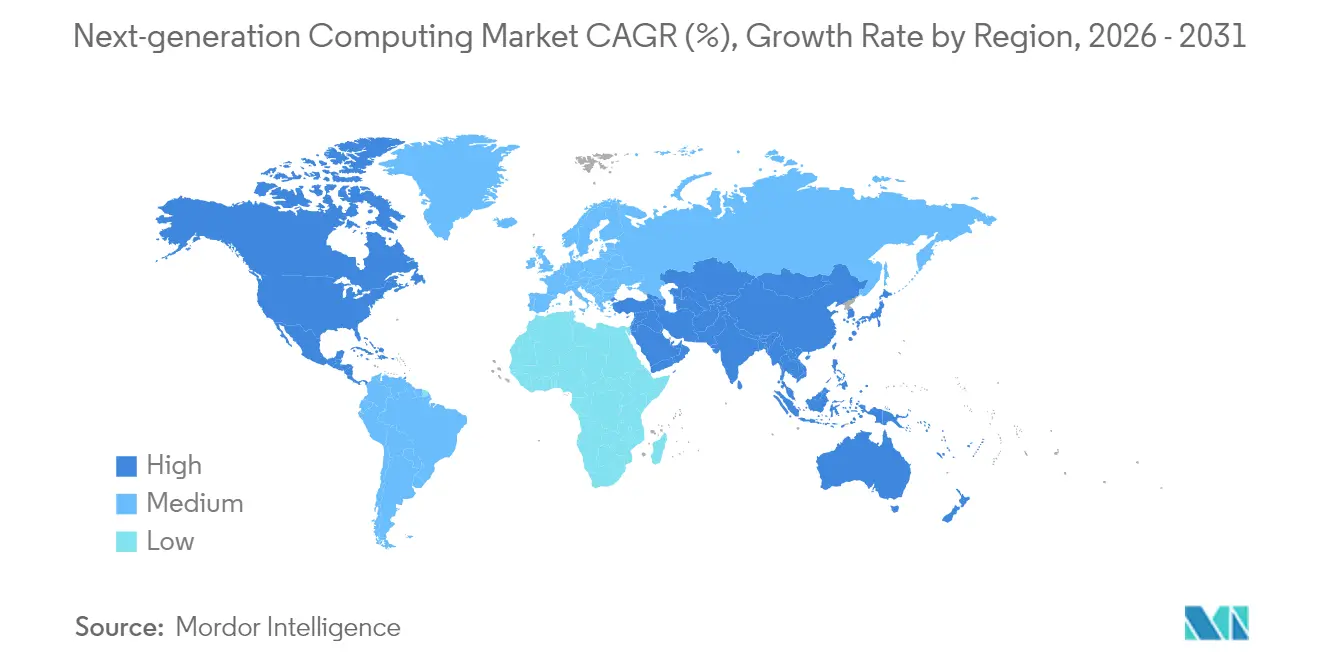

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-generation Computing Market Analysis by Mordor Intelligence

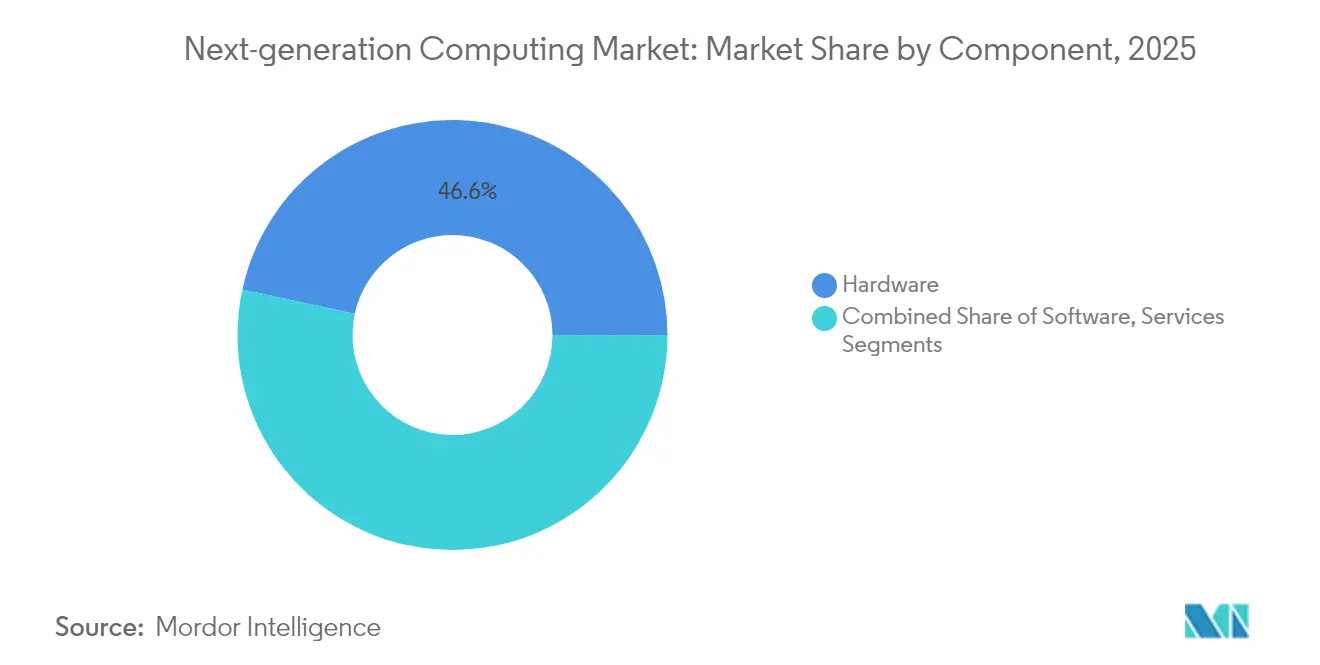

The next-generation computing market size is expected to grow from USD 228.76 billion in 2025 to USD 272.28 billion in 2026 and is forecast to reach USD 650.48 billion by 2031 at 19.02% CAGR over 2026-2031. The expansion has been fuelled by record demand for generative-AI infrastructure, stepped-up public funding for quantum programmes, and tighter integration of edge and cloud resources that lower latency for industrial Internet of Things (IoT) use cases. Hardware components retained leadership with a 47.2% revenue contribution in 2024, helped by successive GPU and application-specific-integrated-circuit (ASIC) launches that improved performance per watt. Services nevertheless paced the fastest, as rising implementation complexity required specialist providers to integrate heterogeneous clusters across on-premise and cloud estates. Traditional high-performance computing (HPC) architectures still hold 41.2% revenue, though quantum computing solutions are projected to record a 35.2% CAGR, signalling an unmistakable pivot toward non-classical approaches. North America kept a 41.2% hold on the next-generation computing market, while Asia-Pacific emerged as the most buoyant region with a 23.1% CAGR thanks to quantum research incentives and hyperscale cloud build-outs.

Key Report Takeaways

- By component, hardware produced 46.60% of 2025 revenue in the next-generation computing market, whereas services are on course to expand 23.78% CAGR through 2031.

- By computing paradigm, HPC led with 40.70% of the next-generation computing market share in 2025; quantum computing is projected to post a 34.05% CAGR.

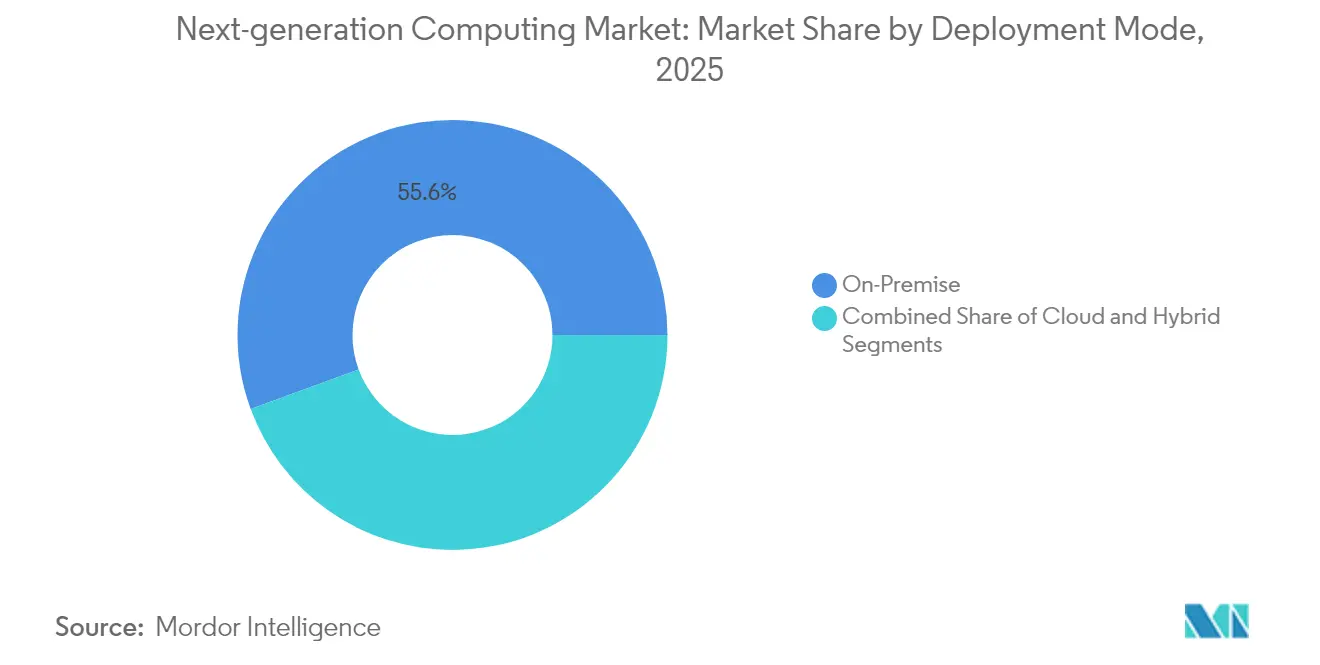

- By deployment mode, on-premise installations captured 55.60% of spending in 2025; cloud deployments carry the highest 27.4% CAGR outlook.

- By end-user sector, BFSI commanded 20.80% revenue, while healthcare and life sciences hold the fastest 31.05% CAGR trajectory.

- By region, North America generated 40.80% of 2025 revenue, and Asia-Pacific will deliver the quickest 22.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Next-generation Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge for generative-AI compute scaling | +5.2% | Global with a focus on North America and East Asia | Medium term (2–4 years) |

| Government funding waves for quantum-tech hubs | +3.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Edge-to-cloud convergence for ultra-low-latency IoT | +2.7% | Global with early adoption in industrial economies | Medium term (2–4 years) |

| Falling GPU TCO via cloud credits and open-IP chiplets | +1.9% | Global | Short term (≤ 2 years) |

| Liquid-cooling breakthroughs enabling dense HPC racks | +1.3% | North America, Europe, East Asia | Medium term (2–4 years) |

| Secondary market for de-commissioned AI accelerators | +0.8% | Global with concentration in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand surge for generative-AI compute scaling

Fiscal-2025 datacenter revenue at a leading GPU vendor more than doubled year-over-year, confirming that large language models (LLMs) and image generators now dominate silicon demand. Blackwell-class processors integrated 208 billion transistors, enabling trillion-parameter inference with a fraction of prior-generation energy draw. Cloud providers responded by releasing dedicated AI instances that bundle low-latency networking and pooled high-bandwidth memory, allowing medium-sized firms to access exa-scale capacity on demand. System integrators simultaneously re-engineered board-level power delivery and introduced software stacks that finesse scheduling across thousands of GPUs, flattening barriers to entry. These steps combined to accelerate capital flows into the next-generation computing market and to reinforce hardware refresh cycles.

Government funding waves for quantum-tech hubs

The United States Department of Energy opened USD 625 million in fresh awards for quantum research in January 2025. [1]United States Department of Energy, “Funding Opportunity Announcement: Quantum Information Science,” energy.gov Similar UK allocations of GBP 121 million (USD 164.34 million) supported national testbeds and business accelerators. Funding clusters anchor universities, national labs, and private suppliers into long-term partnerships, share prototyping risk, and catalyse workforce development through fellowship programmes. In parallel, Japan and India enlarged their sovereign quantum budgets to build supply-chain resilience around dilution refrigerators, photonics, and control electronics. These initiatives triggered patent filings in qubit connectivity, cryogenic packaging, and error-mitigation algorithms, adding durable momentum to the next-generation computing market.

Edge-to-cloud convergence for ultra-low-latency IoT

Roughly one-fifth of the 157 zettabytes created by connected devices in 2025 was processed outside central data centers, a proportion set to rise as 5G moves to 5.5G deployments. Industrial firms embedded AI accelerators into factory gateways, allowing vision systems to reject defects in under ten milliseconds. Cloud providers extended lightweight Kubernetes distributions for single-node clusters, permitting identical microservices to shift seamlessly between edge and core. Network-equipment vendors contributed Time-Sensitive Networking and private-5G slices to guarantee deterministic packet delivery. Collectively, these advances tightened feedback loops in autonomous vehicles, smart grids, and telemedicine, swelling the next-generation computing market with new workload classes.

Falling GPU TCO via cloud credits and open-IP chiplets

Hyperscalers used targeted credit programmes that cut initial AI-instance bills by up to 30%, luring developers who might otherwise buy on-premise gear. On the silicon side, modular chiplet architectures let vendors stitch independently verified logic, memory, and I/O tiles inside one package, improving yield and lowering die cost. An RDNA 4-based GPU family showcased 40% higher performance per compute unit than its predecessor, while retaining compatible drivers, reducing migration expense. Start-ups also prototyped chiplets on older nodes linked to advanced interposers, bringing acceptable performance to mid-market buyers. Cheaper entry points broadened the buyer base and lengthened the tail of the next-generation computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quantum-skilled talent shortage | –2.1% | Global with severe impact in emerging markets | Medium term (2–4 years) |

| High CAPEX and integration risk for heterogeneous clusters | –1.8% | Global | Short term (≤ 2 years) |

| Grid-power and permitting bottlenecks for hyperscale DCs | –1.6% | North America, Europe, parts of Asia-Pacific | Medium term (2–4 years) |

| Export-control limits on advanced HBM and GPU shipments | –1.2% | Global but concentrated in China and Russia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Quantum-skilled talent shortage

A 2025 survey of quantum-technology stakeholders showed 45% citing workforce scarcity as their primary adoption barrier. Quantum algorithm design blends physics, mathematics, and computer science, yet mainstream curricula rarely cover all three. Enterprises attempted to close gaps via internal boot camps and joint university chairs, but ramp-up time often exceeded project deadlines. While government scholarships expanded PhD enrolment, near-term supply remained tight, delaying planned roll-outs in cryptography, optimisation, and material-science workloads and moderating overall expansion of the next-generation computing market.

Grid-power and permitting bottlenecks for hyperscale DCs

Total global data center electricity draw is expected to cross 29,000 TWh by 2030, with generative-AI workloads alone absorbing 1.5% of global power demand. Regions such as Northern Virginia, Dublin, and Frankfurt faced multi-year wait-lists for new grid interconnects, forcing operators to postpone cluster deployments. Equipment vendors reacted by releasing 800V high-voltage DC powertrains that reduce copper use and losses. [2]HPCwire, “NVIDIA 800 V HVDC Architecture Will Power the Next Generation of AI Factories,” hpcwire.comSome operators also trialled underground thermal energy storage and liquid cooling to shave peak consumption. Permit streamlining remains crucial; until resolved, site-location decisions will skew toward regions offering renewable capacity, influencing geographic dispersion in the next-generation computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware primacy under service-led acceleration

The next-generation computing market size tied to hardware reached USD 106.59 billion in 2025, powered by the adoption of GPUs, tensor processing units, and photonic interconnects. Exascale-class boards integrated six HBM stacks, doubling bandwidth and allowing 10× larger model training batches. Memory producers committed capacity expansions to meet a projected fifteen-fold increase in HBM demand for HPC and AI by 2035, safeguarding component supply. Power-efficient optical links also entered mainstream server boards, cutting latency between accelerator pods to microsecond levels.

Services, although smaller, grew faster by handling architecture design, secure deployment, and life-cycle management. Managed quantum workloads, AI-pipeline optimisation, and proactive cooling analytics formed new fee lines. Cloud providers bundled professional services hours into platform subscriptions, creating annuity-style revenue. This hybrid revenue mix improved resilience in the next-generation computing market during hardware supply oscillations and cultivated customer lock-in around specialised toolchains.

By Computing Paradigm: Quantum momentum reshapes dominant HPC

HPC still delivered the bulk of 2024 revenue, thanks to well-established procurement cycles in weather modelling, fluid dynamics, and financial risk grids. Vendors launched exascale systems that combined x86 or Arm CPUs with next-generation GPUs on NVLink-over-Ethernet fabrics, offering single-precision throughput beyond seven exaflops. Such leaps sustained the next-generation computing market even as alternative paradigms matured.

Quantum computing exhibited the steepest growth curve. D-Wave released a 5,000-plus-qubit annealer geared for combinatorial optimisation, while trapped-ion and neutral-atom providers attracted venture funding for error-corrected prototypes. Early hybrid pilots saw quantum kernels accelerate Monte Carlo simulation convergence in high-finance risk models. Given its 34.05% CAGR outlook, quantum will progressively erode classical-only budgets, solidifying its role in the overall next-generation computing market.

By Deployment Mode: On-premise dominance meets cloud elasticity

On-premise clusters accounted for 55.60% of 2025 spending in the next-generation computing market because defence, finance, and genomics labs require deterministic performance and regulatory control. Tier-1 banks retrofitted private GPU superpods with micro-channel liquid cooling that reduced floor-space needs by half. Sovereign cloud regulations in Europe further encouraged in-country hardware.

Cloud installations, however, posted the swiftest gains, with enterprise usage nearing universality by 2025. Hyperscalers expanded accelerator density via four-GPU mezzanine cards and liquid-cooled chassis offered as on-demand SKUs. Enterprises leveraged these remotely accessible clusters for model-training bursts, then pulled inference workloads on-premise to manage cost. Hybrid and multi-cloud orchestration frameworks fused identity management and data locality governance, mitigating vendor lock-in and widening the customer funnel for the next-generation computing market.

By End-User Industry: BFSI scale balanced by healthcare agility

Financial institutions represented 20.80% of 2025 revenue in the next-generation computing market. Algorithmic-trading desks required microsecond response times, achieving them with co-located FPGA edge nodes. Banks also trialled quantum-safe cryptography to future-proof data vaults, adding incremental spending on post-quantum key-exchange appliances.

Healthcare and life sciences are expected to deliver a 31.05% CAGR. Radiology departments deployed AI inference at point-of-image acquisition, slashing diagnosis wait times. Large bio-pharma firms ran de-novo drug-discovery pipelines that used protein-folding LLMs trained on hundreds of millions of sequences. Quantum machine-learning pilots at leading medical centres investigated cardiovascular-surgery risk prediction, showcasing how clinical outcomes can shape capital budgeting and broaden societal value in the next-generation computing market.

Geography Analysis

North America generated 40.80% of 2025 revenue in the next-generation computing market. The United States alone accounted for roughly three-quarters of regional spend, buoyed by public financing, deep venture capital, and dominant cloud incumbents. National laboratories operated pathfinder quantum testbeds that integrate neutral-atom arrays with exascale supercomputers, cementing leadership. Energy-efficient data-centre innovations emerged from cross-industry consortia, reflecting policy focus on sustainability.

Asia-Pacific will post the fastest 22.45% CAGR. China, Japan, and India expanded semiconductor park incentives and subsidised quantum-research fellowships. Hyperscale operators pledged to double colocation white-space in Singapore, Sydney, and Mumbai to meet AI demand. Parallel 5G-Advanced roll-outs created new edge-computing nodes, deepening workload localisation and strengthening regional relevance of the next-generation computing market. Australia and South Korea joined multilateral alliances on quantum standards, adding technical pluralism to the region.

Europe preserved a unified industrial strategy combining digital sovereignty and environmental stewardship. Germany’s Fraunhofer institutes advanced neuromorphic prototypes targeting sub-watt inference, while French labs piloted photonic-based quantum routers. The EU’s fit-for-55 climate package spurred data-centre operators to sign long-term renewable-energy purchase agreements, aligning regulatory compliance with investor pressure. These initiatives elevated Europe’s role as a sustainability vanguard within the next-generation computing market.

Competitive Landscape

The competitive arena remained moderately concentrated; the five largest vendors controlled majority of overall revenue share, yet niche innovators proliferated. NVIDIA kept nearly 80% of the enterprise AI-accelerator sub-segment through continuous GPU, interconnect and software-stack updates. AMD challenged with modular chiplet-based GPUs that promise competitive throughput at lower cost, while Intel refined Ponte Vecchio multicore tiles for HPC. Start-ups such as Cerebras Systems used wafer-scale engines for specialised natural-language-model inference, diversifying supplier options.

Quantum hardware competition intensified. IonQ acquired a controlling stake in cryptography specialist ID Quantique to bundle quantum-safe networking with trapped-ion processors. [4]Photonics Media, “IonQ to Acquire ID Quantique,” photonics.com Neutral-atom provider QuEra closed a large funding round to build fault-tolerant arrays exceeding one million physical qubits. Superconducting-qubit pioneers collaborated with microwave-component manufacturers to slash control-system overheads. These moves collectively expanded the supplier base, enlarging the total addressable portion of the next-generation computing market.

Horizontal alliances broadened solution scope. Eaton and Siemens Energy developed 50% lower-emission power-plant architectures targeting hyperscale campuses, tackling the grid-level footprint that could otherwise restrain expansion. Systems integrators partnered with photonics foundries to package co-packaged optics, solving bandwidth ceilings in next-generation Ethernet fabrics. Such cross-disciplinary ventures redirected competition from single-component races toward vertically integrated stacks that encompass silicon, software and sustainability, solidifying holistic value propositions in the next-generation computing market.

Next-generation Computing Industry Leaders

Amazon Web Services Inc.

Alphabet Inc. (Google Cloud)

Microsoft Corp.

IBM Corp.

NIVIDIA Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eaton and Siemens Energy presented joint power-management blueprints for hyperscalers.

- June 2025: DuPont rolled out advanced substrate chemistries for AI servers.

- May 2025: Delta debuted 92%-efficient AI-datacenter solutions.

- May 2025: IonQ moved to acquire ID Quantique for quantum-safe networking.

- May 2025: NVIDIA introduced an 800V HVDC architecture for AI factories.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the next-generation computing market as revenue from hardware, foundational system software, and managed services that enable high-performance, edge, quantum, optical, and neuromorphic workloads across enterprise and public-cloud settings.

Scope exclusion: consumer PCs and dedicated gaming consoles are not considered.

Segmentation Overview

- By Component

- Hardware

- Processors and Accelerators

- Memory and Storage

- Interconnect and Networking

- Thermal and Power Solutions

- Software

- Services

- Hardware

- By Computing Paradigm

- High-Performance Computing (HPC)

- Quantum Computing

- Optical/Photonic Computing

- Neuromorphic Computing

- Edge / Near-Edge Computing

- Cloud-Native Accelerated Computing

- Hybrid and Other Emerging

- By Deployment Mode

- Cloud

- On-Premise

- Hybrid

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Automotive and Transportation

- Energy and Utilities

- Aerospace and Defense

- Media and Entertainment

- IT and Telecom

- Retail and e-Commerce

- Manufacturing and Industrial

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with chip architects, cloud operators, quantum start-ups, and CIOs in North America, Europe, and Asia. Their insights on price points, deployment mix shifts, and funding triggers validated desk findings and closed information gaps.

Desk Research

We drew on open datasets from the United States Bureau of Economic Analysis, OECD Digital Economy Outlook, UN Comtrade advanced-processor codes, and peer-reviewed exascale papers on IEEE Xplore. Company 10-Ks, investor decks, patent filings via Questel, plus proprietary feeds from D&B Hoovers and Dow Jones Factiva enriched revenue mapping. These examples illustrate our breadth; many other sources supported data checks and contextual depth.

Market-Sizing & Forecasting

After collating national data-center outlays, parsing cloud disclosures, and charting GPU invoice trends, we arrive at the base-year spend. A top-down model links those pools with HPC node shipments, then selective bottom-up supplier roll-ups test and refine totals. Key drivers include tensor-core pricing swings, qubit counts per rack, edge cabinet installations, energy tariffs, and sovereign-cloud rules. Forecasts through 2030 use multivariate regression plus scenario analysis, with assumptions vetted by senior interviewees. Where vendor detail is thin, median peer margins bridge gaps before calibration.

Data Validation & Update Cycle

Outputs face variance checks against independent ratios and time-series logic, followed by internal peer review. Reports refresh every year, material events spark interim revisions, and a final analyst pass ensures clients receive the latest view.

Why Mordor's Next-generation Computing Baseline Earns Trust

Published market values often differ because each firm selects distinct technology bundles and refresh cadences, and because some rely on static average selling prices rather than live procurement signals.

Key gap drivers we observe include narrower component coverage, constant-currency assumptions that ignore rapid GPU price moves, and infrequent model updates adopted elsewhere, whereas our team revisits inputs annually and tri-validates them with buyer conversations.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 228.76 B (2025) | Mordor Intelligence | |

| USD 160.97 B (2024) | Global Consultancy A | Excludes optical and neuromorphic tech; relies on 2023 vendor filings |

| USD 152.13 B (2024) | Trade Journal B | Keeps currency fixed, omits recent GPU cost inflation |

| USD 281.20 B (2025) | Research Publisher C | Combines user opex with supplier revenue, inflating totals |

Taken together, the comparison shows that Mordor Intelligence, by selecting a transparent scope, revisiting variables yearly, and double-checking numbers through direct market dialogue, delivers a balanced, reproducible baseline that decision-makers can depend on.

Key Questions Answered in the Report

What is the projected next-generation computing market size in 2031?

The next-generation computing market size is expected to reach USD 650.48 billion by 2031, up from USD 272.28 billion in 2026.

Which component category is expanding fastest?

Services are expanding the quickest, with a 23.78% CAGR to 2031 as enterprises seek integration, optimisation and managed-operations expertise.

How large is the opportunity for quantum computing within the next-generation computing market?

Quantum solutions are forecast to grow at a 34.05% CAGR, making them the most dynamic computing paradigm over the period.

Why does on-premise deployment still dominate the next-generation computing market?

Security mandates and deterministic performance requirements kept 55.60% of 2025 spending on on-premise clusters, especially in finance, defence and genomics research.

Which region will record the fastest growth?

Asia-Pacific will record the fastest expansion, at a 22.45% CAGR, driven by quantum research funding and hyperscale cloud capacity doubling.

What is the chief restraint on quantum-technology adoption?

A global shortage of quantum-skilled professionals is the biggest bottleneck, trimming the overall CAGR by an estimated 2.1%.

Page last updated on: