Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

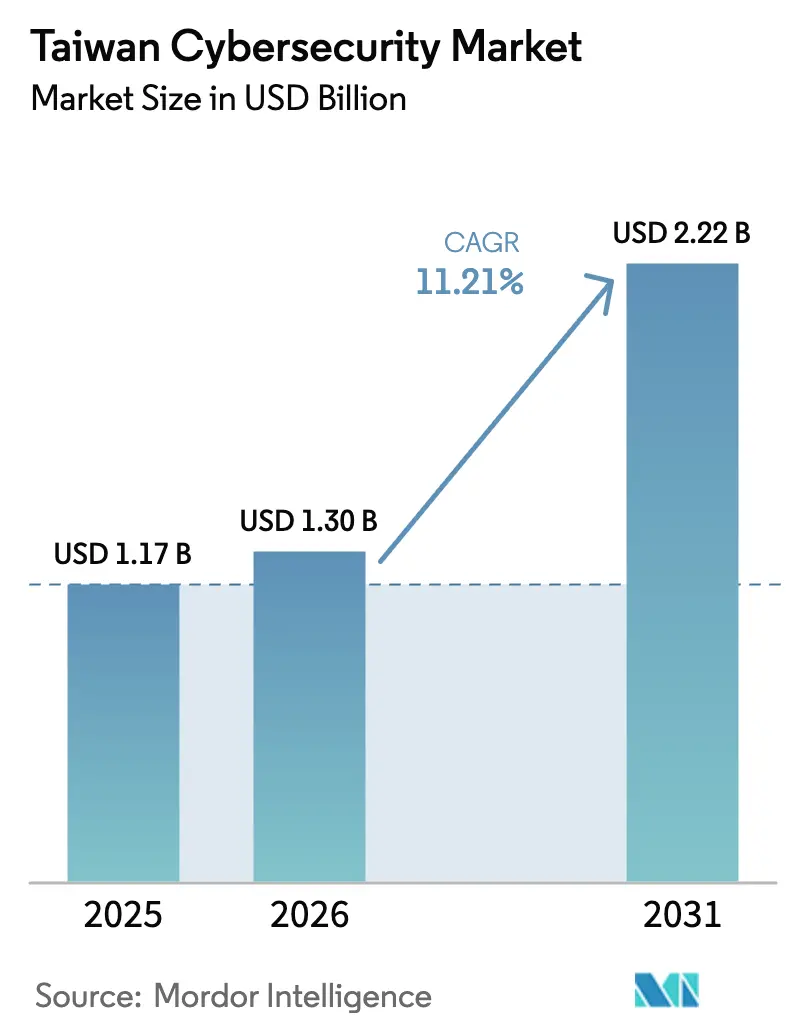

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

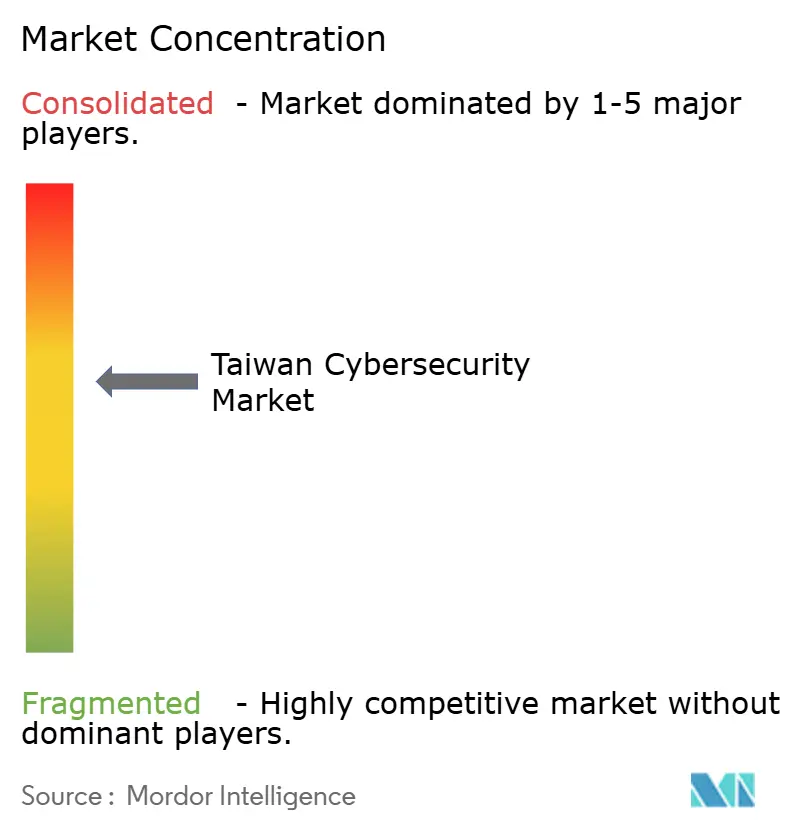

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Cybersecurity Market Analysis by Mordor Intelligence

The Taiwan cybersecurity market size is expected to grow from USD 1.17 billion in 2025 to USD 1.3 billion in 2026 and is forecast to reach USD 2.22 billion by 2031 at 11.21% CAGR over 2026-2031. Geopolitical tensions, supply-chain reliance on semiconductors, and an average of 2.4 million daily cyberattacks drive continuous spending across government and industry. Regulatory enforcement—most notably the Cyber Security Act 2.0—elevates compliance from voluntary best practice to legal obligation with fines up to NT$10 million for non-reporting of incidents, tilting budgets toward managed security services. Private 5G roll-outs inside science parks, post-quantum cryptography migration guidelines, and zero-trust frameworks in banking anchor future-proof investment patterns. Simultaneously, a chronic talent shortfall of about 80,000 specialists inflates demand for automation and outsourced security operations. Cost-sensitive SMEs nevertheless remain hesitant, leaving a sizable but fragmented addressable base for the Taiwan cybersecurity market.

Key Report Takeaways

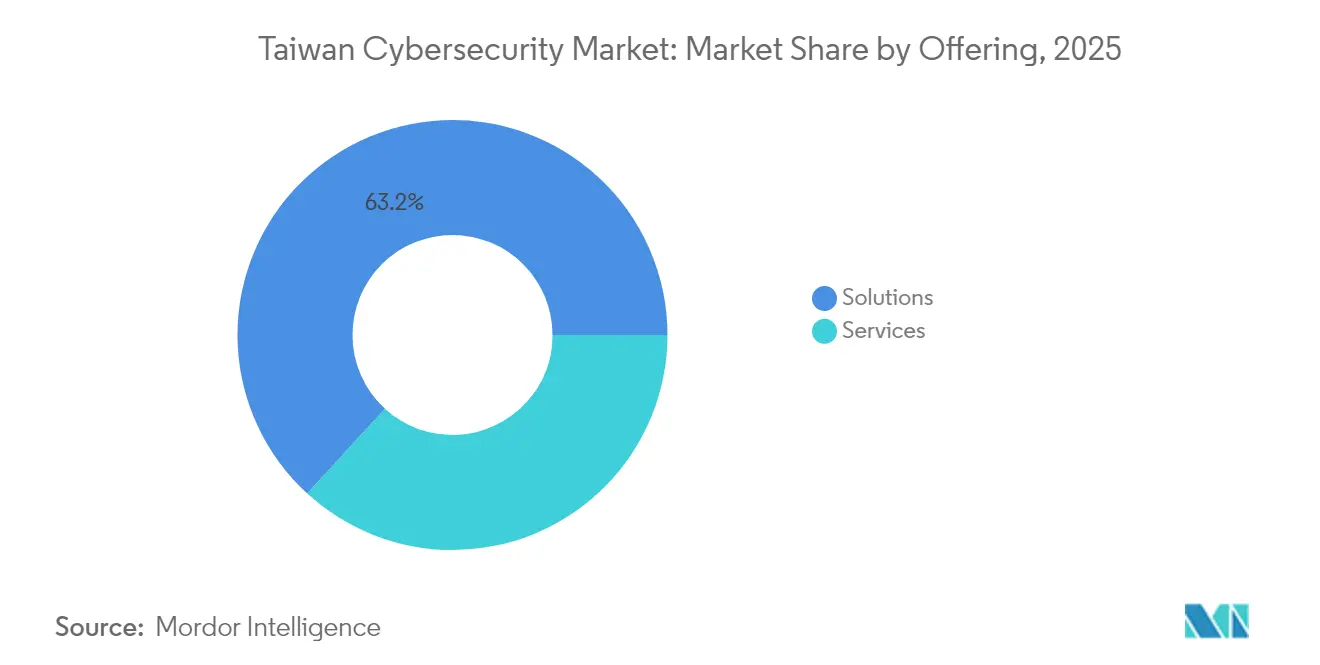

- By offering, solutions commanded 63.20% of the Taiwan cybersecurity market share in 2025; managed services are forecast to expand at a 14.23% CAGR through 2031.

- By deployment mode, on-premise held 56.20% of the Taiwan cybersecurity market size in 2025; cloud is projected to grow at 16.34% CAGR to 2031.

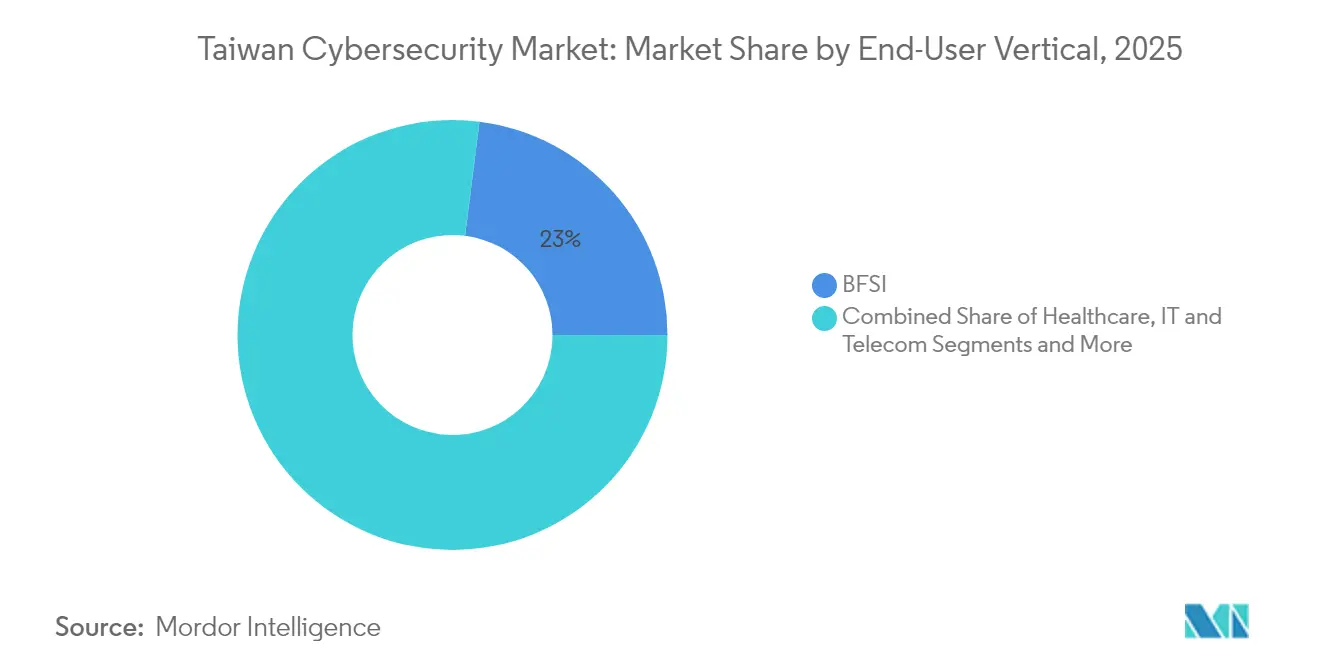

- By end-user vertical, BFSI led with 23.00% revenue share in 2025, while healthcare is advancing at a 15.02% CAGR to 2031.

- By enterprise size, large enterprises captured 71.60% share of the Taiwan cybersecurity market in 2025; SMEs record the fastest growth at 12.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-manufacturing OT–IT convergence secures IP | +2.1% | National, Hsinchu Science Park focus | Medium term (2-4 years) |

| Cyber Security Act 2.0 and critical-infrastructure resilience mandates | +2.8% | National, six critical sectors | Short term (≤ 2 years) |

| 5G private-network roll-outs in science parks boost edge security | +1.7% | Kaohsiung and regional parks | Medium term (2-4 years) |

| FinTech sandbox accelerating zero-trust adoption in BFSI | +1.4% | Taipei financial district | Short term (≤ 2 years) |

| Semiconductor supply-chain security demands from US/EU clients | +2.3% | National with global linkages | Long term (≥ 4 years) |

| Surge in ransomware on gaming and semiconductor sectors | +1.9% | Sector-specific clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-manufacturing OT–IT convergence secures IP

Convergence blurs once-separate networks, exposing legacy equipment to internet-borne threats. TXOne Networks’ 2024 survey indicated that 94% of Taiwanese factories logged OT incidents linked to IT vectors, underscoring the urgency for industrial-grade security platforms. For instance, Inventec’s fully virtualized 5G private network raised straight-through production rates from 70% to 85%, yet introduced new vulnerabilities for automated guided vehicles that now require micro-segmenting defenses. Vendors are therefore integrating real-time anomaly detection, immutable logs, and downtime-free patching features to fit strict production-quality metrics.

Cyber Security Act 2.0 and critical-infrastructure resilience mandates

Legislative amendments broaden coverage from 4 to 6 sectors and impose NTD 10 million penalties for unreported breaches, prompting immediate procurement of incident-response platforms and 24/7 SOC services[1]Chang-Lin Wang, “Legislature passes Cyber Security Act 2.0 amendments,” Technice, technice.com.tw. The Ministry of Digital Affairs further requires annual third-party audits, accelerating demand for consulting and vulnerability assessment. Organizations unable to self-staff SOC teams increasingly outsource to domestic MSSPs to meet stringent response-time benchmarks.

5G private-network roll-outs in science parks boost edge security

Far EasTone Telecom’s 5G smart-patrol deployment for Kaohsiung police showcased how network slicing enforces application isolation while maintaining latency below 10 ms. Closed architectures like HTC Reign Core allow customizable bandwidth to critical workloads, addressing intellectual-property leakage concerns prevalent in RandD labs within the Taiwan cybersecurity market.

FinTech sandbox accelerating zero-trust adoption in BFSI

The Financial Supervisory Commission’s sandbox permits rapid piloting of AI fraud detection and blockchain remittances while mandating “never-trust, always-verify” controls. E.SUN Bank’s Fraud Prevention Laboratory now correlates biometrics, device posture, and behavioral analytics, cutting false-positive transaction flags by 27% in 2025. Large banks are therefore issuing multi-factor hard tokens and deploying micro-service gateways to secure open-banking APIs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented SME base with low cyber-insurance uptake | -1.8% | Traditional manufacturing belts | Medium term (2-4 years) |

| Appliance-centric procurement slows SaaS migration | -1.3% | Government and large enterprise | Long term (≥ 4 years) |

| Cross-border data-transfer curbs for foreign MSSPs | -0.9% | National | Short term (≤ 2 years) |

| Shortage of bilingual cyber talent raises service costs | -1.6% | Taipei and Hsinchu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented SME base with low cyber-insurance uptake

Over 98% of the corporate landscape consists of SMEs that rarely exceed 1% of revenue on cyber spending. A 2025 Digital Development Department audit found sizable capability gaps in sectors such as food processing, where only 22% of firms perform annual penetration testing. Limited appetite for cyber-insurance perpetuates underinvestment, forcing providers to tailor low-cost bundles that combine endpoint security, awareness training, and simplified incident cover.

Appliance-centric procurement slows SaaS migration

Government agencies still favor hardware security modules and appliance firewalls due to data-sovereignty concerns. This stance postpones cloud-native adoption, lengthens refresh cycles, and escalates total cost of ownership. For example, a state-run bank procured 650 physical devices in 2025 to maintain an air-gapped environment despite equivalent SaaS alternatives that deliver automatic patching and elastic scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions dominance amid services acceleration

Solutions held 63.20% of the Taiwan cybersecurity market share in 2025. Demand centered on unified threat management, endpoint protection, and secure-web gateways. Yet the services category is the growth engine: managed services are forecast at 14.23% CAGR to 2031 as organizations confront a talent deficit exceeding 80,000 professionals. Vendors now bundle MDR, threat hunting, and compliance reporting into subscription models that align with operating rather than capital budgets.

Professional services also gain traction. CyCraft’s AI-powered red-team engagements demonstrated 38% faster breach discovery versus manual assessments, prompting large retailers to allocate incremental budgets for continuous testing. Meanwhile, endpoint and cloud workload protection within the solutions bucket are the preferred entry points for SMEs because they can be deployed rapidly with minimal on-site integration.

By Deployment Mode: Cloud gains momentum despite on-premise preference

On-premise maintains 56.20% share of the Taiwan cybersecurity market size in 2025, reflecting entrenched data-residency rules in government and finance. However, economic pressure and evolving attack surfaces push hybrid models. Cloud deployments grow at 16.34% CAGR and now account for most green-field projects, especially analytics-heavy SIEM replacements. The sovereign-cloud initiatives of Chunghwa Telecom and Far EasTone supply compliant hosting that alleviates regulatory hurdles.

Use cases such as secure access service edge (SASE) and cloud access security brokers (CASB) showcase rapid uptake because they unify remote-work protection for distributed teams. GECP’s private-cloud migration in 2025 lowered mean-time-to-detect by 46% while halving log-storage costs, a trend that encourages even cautious sectors to pilot cloud-native defenses.

By End-User Vertical: BFSI leadership with healthcare acceleration

BFSI contributes 23.00% revenue, driven by stringent sandbox regulations and zero-trust mandates. Financial institutions now combine real-time AI analytics with multi-factor authentication to mitigate account takeover. For example, CTBC Bank’s open-banking API gateway blocked 1.9 million suspicious calls in 2025 without service disruption.

Healthcare grows fastest at 15.02% CAGR, catalyzed by 5G telemedicine and escalating ransomware attacks. The Ministry of Digital Affairs dispatched emergency teams to Mackay Memorial Hospital after a March 2025 breach, spurring sector-wide vulnerability assessments. Hospitals now prioritize network segmentation, immutable backups, and AI-driven anomaly detection to safeguard electronic medical records.

By End-User Enterprise Size: Large-enterprise dominance with SME momentum

Large enterprises command 71.60% of the Taiwan cybersecurity market in 2025. They integrate SOAR, deception grids, and quantum-safe VPNs, setting reference architectures adopted downstream. TSMC expanded its Supply Chain Security Association to 620 vendors in 2025, imposing baseline requirements that spread best practice across tiers.

SMEs, although smaller in spend, are the growth frontier at 12.26% CAGR. Subsidized audits and training improved baseline security awareness for 77.6% of SMEs completing the 2025 maturity assessment. Local MSSPs respond with pay-as-you-grow bundles that include EDR, phishing simulation, and cyber-insurance gateways.

Geography Analysis

Northern Taiwan anchors about 59.40% of the Taiwan cybersecurity market, with Taipei and Hsinchu housing financial headquarters and semiconductor fabs that demand layered defenses. Daily hostile probes from state-sponsored actors average 2.4 million, reinforcing a survival-driven mindset toward cyber readiness. The government’s NT$8.8 billion resilience program allocates grants across energy, healthcare, and finance but prioritizes deployments in population-dense urban hubs where critical infrastructure densities are highest.

Central Taiwan benefits from cluster manufacturing in Taichung, spurring adoption of OT security appliances that factor in latency-sensitive CNC machinery. Kaohsiung’s Asia New Bay Area 5G AIoT Hub positions the south as a testbed for edge-security startups, attracting venture capital and public-private pilots for autonomous logistics.

International collaboration further shapes regional demand. SEMI’s semiconductor-specific cybersecurity standards headquartered in Hsinchu guide fabs across the island, while joint Taiwan-Japan research on post-quantum crypto opens export channels for domestic IP. US defence engagement programs channel funding into threat-sharing platforms that enhance situational awareness island-wide. These dynamics collectively broaden the Taiwan cybersecurity market while reinforcing local sovereignty requirements that favor domestic providers.

Competitive Landscape

Competition is balanced between global majors and agile domestic specialists inside the Taiwan cybersecurity market. Fortinet, Palo Alto Networks, and Trend Micro retain enterprise penetration due to robust channel ecosystems yet face pricing pressure from local firms offering Mandarin interfaces and compliance mapping out of the box. CyCraft’s XecGuard AI model, launched July 2025, improves defensive accuracy by 19.4%, elevating the domestic vendor’s profile in managed detection services.

Strategic investments illustrate a consolidation wave: Chunghwa Telecom injected NTD 65 million into CyCraft to form a “national team,” blending carrier data telemetry with AI analytics for sovereign threat intelligence. TXOne Networks strengthens its OT niche by embedding anomaly sensors in PLC firmware through partnerships with Advantech. Meanwhile, F5 and ASUS have launched post-quantum toolkits, anticipating regulatory pushes for quantum resilience.

White-space opportunities remain around SME packages, AI model security, and cross-border compliance advisory. Onward Security leverages Common Criteria certification labs to win IoT security testing contracts, while BTQ Technologies pilots lattice-based algorithms inside HSMs for financial clients. The top five suppliers held about 43% collective revenue in 2024, indicating moderate concentration and room for disruptive entrants.

Taiwan Cybersecurity Industry Leaders

Adlink Technology

Egis Technology Inc.

AuthenTrend

CureLAN Technology Co

CyCraft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CyCraft Technology and APMIC unveiled XecGuard, a 3-billion-parameter AI defense model, achieving 19.4% uplift against prompt-injection attacks.

- July 2025: F5 Networks released post-quantum cryptography solutions tailored for Taiwanese enterprises.

- June 2025: ASUS secured US CAVP certification for its proprietary post-quantum algorithm.

- May 2025: Taiwan’s Cabinet approved a NT$8.8 billion four-year cybersecurity resilience plan.

Taiwan Cybersecurity Market Report Scope

IT advancement, communication technologies, and smart energy grids are changing the landscapes of almost every country's critical infrastructure and business networks. However, with rapidly changing technology comes rapidly advancing threats. Cybersecurity solutions help an organization to monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information, using spyware and malware, and by phishing to maintain data confidentiality. The market sizing for the study has been provided based on the end-user spending on Cybersecurity solutions and services.

Taiwan cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

Key Questions Answered in the Report

What is the current value of the Taiwan cybersecurity market?

The Taiwan cybersecurity market size stands at USD 1.3 billion in 2026.

How fast is the Taiwan cybersecurity market expected to grow?

The market is projected to register an 11.21% CAGR and reach USD 2.22 billion by 2031.

Which industry vertical spends the most on cybersecurity in Taiwan?

Banking, financial services, and insurance contribute the largest share at 23.00% of 2025 revenue.

What legislation most influences cybersecurity spending in Taiwan?

The Cyber Security Act 2.0, which imposes fines up to NTD 10 million (USD 0.34 Million) for unreported incidents, is the primary regulatory driver.

Page last updated on: