Tablet Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

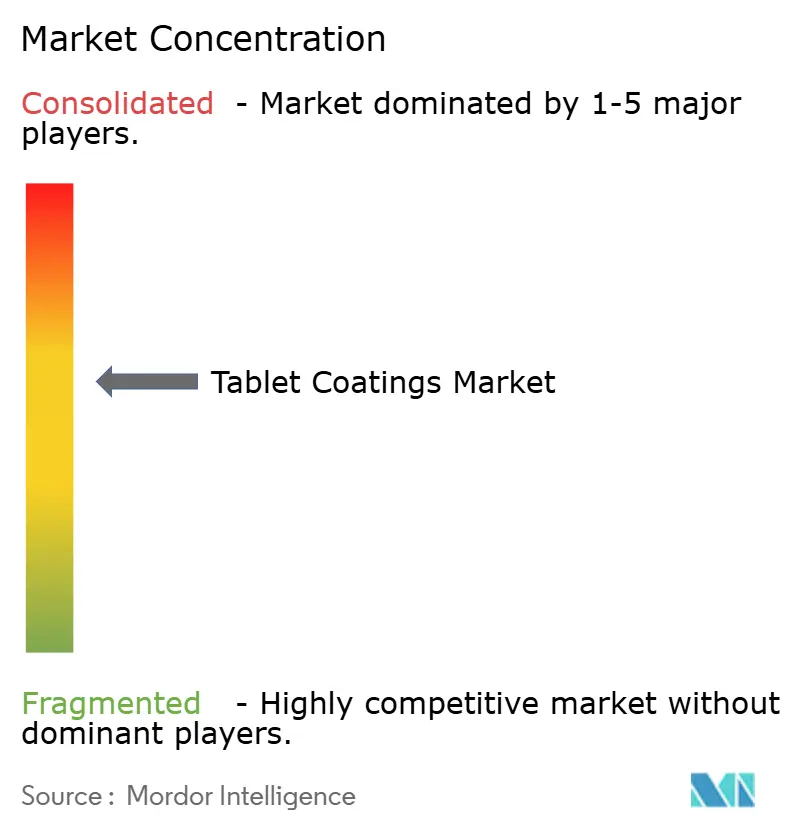

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tablet Coatings Market Analysis by Mordor Intelligence

tablet coatings market size in 2026 is estimated at USD 1.04 billion, growing from 2025 value of USD 0.986 billion with 2031 projections showing USD 1.33 billion, growing at 5.12% CAGR over 2026-2031. Robust capital spending by drug makers, a pivot toward continuous manufacturing, and tightening quality expectations are the prime forces behind this steady expansion. Film-coated tablets hold more than half of current demand, while enteric technologies register the quickest unit growth as companies pursue targeted delivery. Asia-Pacific’s share already tops one-third of global value and continues to grow thanks to aggressive capacity additions in India and China. Heightened scrutiny of titanium dioxide is reshaping formulation strategies, yet regulatory bodies in the United States, Europe, and Asia simultaneously encourage adoption of advanced, more sustainable coating systems. Against this backdrop, the tablet coatings market offers suppliers a multi-year runway for incremental volume as well as premium, technology-rich opportunities.

Key Report Takeaways

- By coating type, film-coated tablets led with 52.74% revenue share in 2025, whereas enteric-coated products are forecast to post the fastest 6.73% CAGR to 2031.

- By polymer, cellulose ethers commanded 38.25% share of the tablet coatings market size in 2025; acrylic acid polymers are projected to expand at an 7.86% CAGR through 2031.

- By formulation component, plasticizers delivered 41.88% of 2025 revenue, while colorants are on track for a 6.95% CAGR to 2031.

- By process, conventional pan equipment held 40.92% of the 2025 tablet coatings market share, with continuous systems advancing at an 7.98% CAGR.

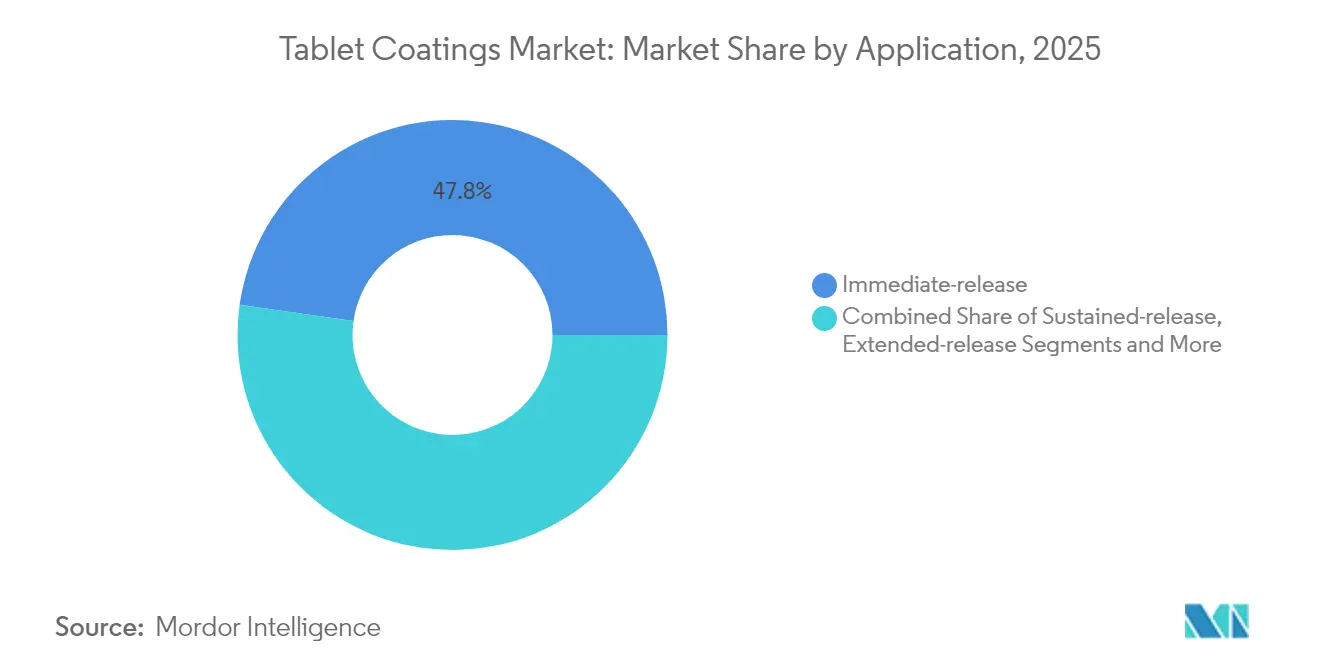

- By application, immediate-release coatings accounted for 47.76% of 2025 value; sustained-release solutions are expected to grow at 7.46% to the end of the decade.

- By end-user, pharmaceutical manufacturers retained 61.83% share in 2025, yet CDMOs/CMOs are slated for the highest 8.02% CAGR.

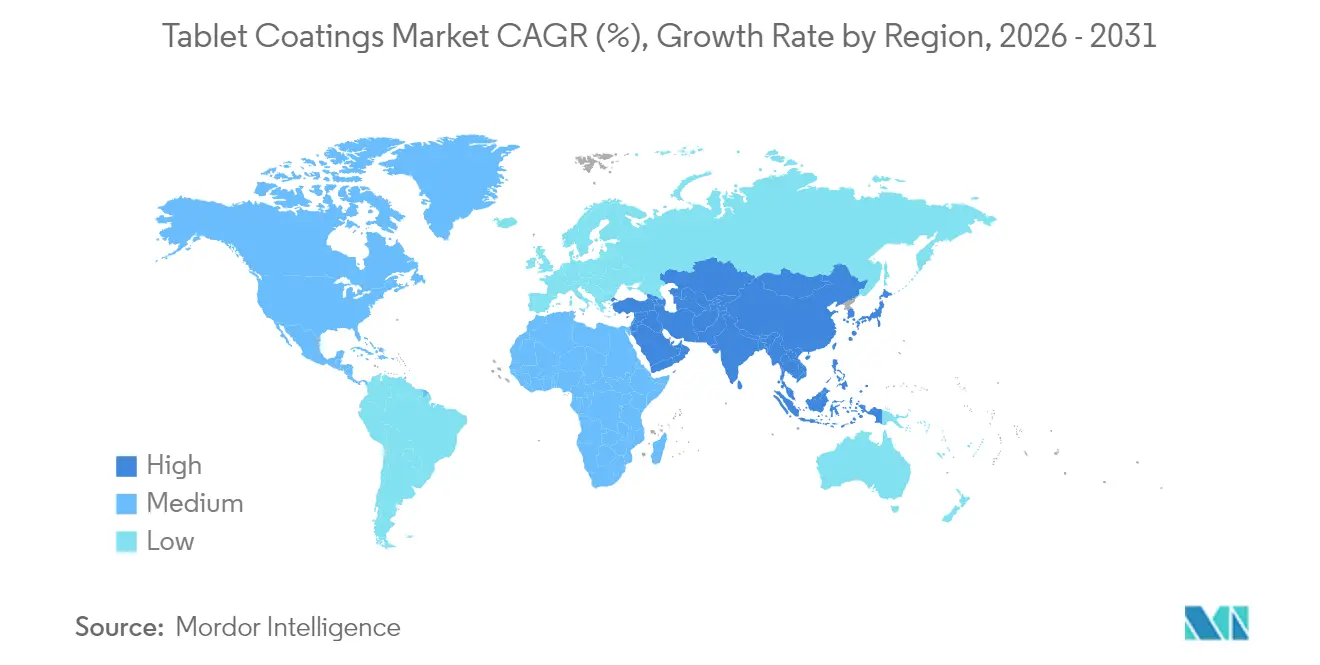

- By geography, Asia-Pacific dominated at 33.67% share in 2025 and is simultaneously the fastest-growing region with an 7.72% CAGR projection.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tablet Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expeditious growth of the global pharmaceutical manufacturing base | +1.8% | Global (APAC & North America concentration) | Medium term (2–4 years) |

| Rapid adoption of orphan drugs & nutraceuticals | +1.2% | Global (North America & Europe lead) | Long term (≥ 4 years) |

| Growing demand for taste-masking & aesthetic coatings for pediatric and geriatric compliance | +0.9% | Global (developed markets first) | Short term (≤ 2 years) |

| Shift toward continuous manufacturing in solid-dose formulations | +0.7% | North America & EU extending to APAC | Medium term (2–4 years) |

| Personalized medicine driving demand for mini-tabs & micro-encapsulation | +0.5% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Accelerated regulatory approvals shortening time-to-market for reformulated tablets | +0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expeditious Growth Of The Global Pharmaceutical Manufacturing Base

Drug makers have launched an unprecedented wave of bricks-and-mortar expansion. PCI Pharma Services earmarked USD 365 million for coating-friendly lines in the United States and Europe, while CordenPharma allocated EUR 900 million to peptides that rely on sophisticated protective layers. In Asia, WuXi STA activated a 169-acre active-ingredient campus and tripled peptide capacity, reflecting the region’s appetite for complex solid forms. These multimillion-dollar moves immediately lift baseline consumption of coating polymers, pigments, and plasticizers. They also spur downstream investments such as Lotte Fine Chemical’s USD 740 million cellulose pact with Colorcon, which aims to secure a leadership position in excipient supply. As more biologicals make the leap to oral dosage, demand extends beyond conventional barrier films into moisture-tight or enteric layers engineered for fragile APIs. For suppliers, the expanding factory footprint translates into recurring raw-material volumes, steady retrofits of aging pans, and adoption of inline quality controls that favor premium, ready-to-use powders.

Rapid Adoption Of Orphan Drugs & Nutraceuticals

Record orphan-drug approvals and booming nutraceutical launches broaden the coating toolbox. Vertex, Gilead, and peer innovators each spent more than USD 4 billion in 2024 to secure rare-disease candidates that often demand pH-dependent release or micro-layered actives for low-dose accuracy. On the supplement side, Colorcon debuted Nutrapure, the first aqueous clear organic film system, crafted to satisfy clean-label consumers without compromising stability. Evonik’s EUDRAGUARD® line delivers probiotic-friendly enteric functionality, showing how pharmaceutical-grade science migrates into wellness products. Hovione’s pact with Zerion Pharma extends high-surface-area Dispersome carriers to vitamin blends, highlighting the cross-pollination of Rx and OTC technologies. With the FDA now offering clearer notification rules for new dietary ingredients, novel coatings can reach shelves faster while capturing premium margins.

Growing Demand For Taste-Masking & Aesthetic Coatings For Pediatric And Geriatric Compliance

Palatable dosage forms materially improve adherence. University of California – San Diego confirmed that a single timed-release capsule wrapped in pH-responsive layers could replace multiple daily pills for chronic disease sufferers.[1]UCSD News Staff, “Timed-Release Capsule Could Replace Multiple Pills,” UC San Diego, phys.orgClinical trials show in-situ coating boosts swallowability in 87% of children and enhances perceived taste in 85% of cases, quantifying real-world benefits. Formulators now lean on electronic-tongue analytics to perfect polymer blends, isolating sugar, fat, and pH variables that correlate with sensory scores.[2]George Brown, “Suitability of E-tongue Sensors,” Springer Nature, link.springer.com The University of Nottingham’s multi-material ink-jet 3D printing takes personalization further by embedding color coding and dose titration in a single print job. As regulators finalize guidance on alternative colorants, brand owners seize the chance to refresh visual identity while simultaneously hitting compliance targets.

Shift Toward Continuous Manufacturing In Solid-Dose Formulations

Cost and quality pressures are pushing tablet lines from batch to continuous flow. The FDA’s January 2025 advanced-manufacturing guidance creates a preferential review lane for equipment such as GEA’s ConsiGma, which integrates dosing, granulation, drying, and film coating in one skid. Hovione installed a next-generation continuous tableting suite in Lisbon that halves development time and slashes material use during scale-up. Syntegon’s Settle Plate Changer automates viable monitoring, cutting manual interventions by 80% and ensuring data-rich coating runs. For excipient vendors, continuous lines favor ready-to-use aqueous dispersions that dissolve quickly and exhibit tight viscosity windows, reinforcing demand for premium high-purity grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent & divergent regional GMP requirements | -1.1% | Global (EU-US-APAC) | Medium term (2–4 years) |

| Time- and cost-intensive coating process validation | -0.8% | Global | Short term (≤ 2 years) |

| Rising scrutiny of titanium-dioxide use | -0.6% | EU-led, potential global ripple | Medium term (2–4 years) |

| Supply-chain volatility in specialty polymers | -0.4% | Global (polymer-producing hubs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent & Divergent Regional GMP Requirements

Regulatory labyrinths complicate execution. Europe’s 2024 draft medicines law adds layers of supply-chain traceability, while the FDA’s CFR 211.110 revision mandates scientifically justified sampling plans.[3]European Pharmaceutical Review Staff, “GMP Update 2024/2025,” ECA Academy, gmp-journal.com Asia-Pacific introduces country-specific modules despite PIC/S harmonization, forcing manufacturers to compile overlapping dossiers for India, China, and Japan. For coaters, each jurisdiction can demand fresh validation of inlet air temperature, spray pattern, and cleaning cycles. The added paperwork inflates launch budgets and slows global rollout, blunting some CAGR upside predicted for the tablet coatings market.

Time- and Cost-Intensive Coating Process Validation

Every new film layer requires demonstration of uniformity, stability, and leachable safety. Stability testing alone can span six to 12 months under ICH conditions, delaying revenue capture. Pilot-scale batches consume kilograms of API, which is especially costly for high-potency oncology products. Real-time-release testing reduces some burden but still necessitates complex multivariate models and regulator concurrence. These hurdles encourage companies to favor well-characterized, ready-to-use systems, yet smaller firms often lack funds for upfront validation, limiting broad adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Type: Film-Coated Dominance Drives Innovation

Film-coated tablets contributed 52.74% of 2025 revenue, underscoring how a single layer can combine moisture protection, UV shielding, and brand color in one economical pass. The tablet coatings market size for enteric-coated formats is projected to rise at 6.73% CAGR as biologic actives and probiotics demand intestine-directed release. Over the next five years, film formulations will integrate digital watermark pigments for anti-counterfeiting and low-foaming surfactants to support continuous lines. Concurrently, sugar-coat demand will stay niche, serving mainly pediatric syrups converted into chewable cores.

Continuous processing magnifies film-coat advantages because the step’s short residence time aligns well with ready-to-use aqueous systems. Hovione’s Lisbon installation links continuous granulation to direct pan coating, demonstrating 30% faster cycle times versus batch. Enteric players innovate with plasticizer-free acrylic dispersions that cut preparation time by 70%, led by Evonik’s EUDRAGIT FL 30 D-55. Suppliers see rising orders for functional films combining delayed and sustained-release layers in single-step processes, saving floor space and validation hours.

By Polymer: Cellulose Ethers Lead Amid Acrylic Innovation

Cellulose ethers owned 38.25% of 2025 demand thanks to a decades-long safety record and universal compendial listings. Acrylics, however, show an 7.86% forward CAGR, positioning them as the fastest polymer class in the broader tablet coatings market. Pharmaceutical buyers value acrylics for superior film strength under low solids and for ease of pH tuning, both key for continuous spray. Lotte Fine Chemical’s partnership with Colorcon aims to enlarge cellulose output dramatically, a sign core users still prioritize supply security for traditional grades.

Next-generation acrylics integrate quaternary-amine groups for colon targeting, while bio-based celluloses gain momentum in sustainability audits. The tablet coatings market share that acrylics capture will also benefit from regulatory pressures on TiO2 because many acrylic dispersions mask core discoloration without added opacifiers. Polymer producers invest in green-chemistry solvent recovery and energy-efficient reactors to lower scope-1 emissions, aligning with ESG mandates from top-20 pharma customers.

By Formulation Component: Plasticizers Dominate While Colorants Accelerate

Plasticizers represented 41.88% of revenue in 2025 because nearly every film requires flexibility to resist edge chipping. Yet colorants, at a 6.95% projected CAGR, will outpace all other additives as companies revamp branding and compliance with new FDA color guidance fda.gov. The tablet coatings market size for colorants is set to expand further as traceability tools embed QR-readable patterns directly into thin films.

Sorbitol and triethyl citrate remain top plasticizers, but their dosage is dropping as polymer science advances toward inherently pliable backbones. Titanium-dioxide-free opacifiers based on calcium carbonate are gaining traction, although higher loadings are required to reach equivalent hiding power, which nudges solvent demand upward. Multifunctional anti-tack agents that double as gloss enhancers help formulators reduce ingredient count and validation burden.

By Process/Equipment: Conventional Pan Coating Leads Amid Continuous Innovation

Conventional pans still held 40.92% of 2025 throughput, reflecting broad installed bases in generics plants. Continuous lines, posting an 7.98% forward CAGR, are the headline story in the tablet coatings market. Early adopters report 30% less waste and real-time release testing that short-circuits days-long lab waits. Syntegon’s SPC-1000 and GEA’s ConsiGma exemplify platforms that integrate environmental monitoring, PAT, and cleaning validation into digital twins, cutting change-over from hours to minutes.

Perforated pans find use where heat-sensitive actives need gentle drying, and fluidized beds thrive in pellet and multiparticulate niches. Equipment OEMs now ship plug-and-play skids with cloud-ready sensors so users can benchmark coating uniformity across sites, a key element in global tech-transfer programs.

By Application: Immediate-Release Dominates While Sustained-Release Accelerates

Immediate-release layers accounted for 47.76% of 2025 spending; routine taste masking and brand coloration keep this share high. Sustained-release coatings, forecast at 7.46% CAGR, reflect chronic disease realities and payer preference for once-daily dosing. The tablet coatings market share for extended-release profiles is growing in cardiometabolic therapy where steady plasma levels improve outcomes.

3D-printed prototypes demonstrate pulsatile release by stacking dissimilar polymers in concentric rings. pH-responsive delayed-release designs are increasingly combined with time-based diffusion barriers, yielding hybrid systems that maintain acid protection yet offer afternoon drug pulses. Such complexity elevates the value of process-analytical-technology-enabled coaters capable of monitoring layer thickness in microns.

By End-User: Pharmaceutical Manufacturers Lead While CDMOs Accelerate

Originator and generic drug makers generated 61.83% of 2025 demand, leveraging captive formulary control to optimize coatings. CDMOs/CMOs, with an 8.02% CAGR outlook, are expanding fastest as big pharma outsources older molecules and niche therapies. Adare Pharma Solutions upgraded its Italian site for high-potency coatings, while Serán BioScience broke ground on a USD 200 million Oregon facility tailored for continuous lines.

The tablet coatings industry model is thus bifurcating: large pharma retains strategic pipelines yet relies on partners for volume flexibility and specialized polymer know-how. Nutraceutical houses adopt pharmaceutical standards via turnkey systems such as Roquette’s plant-based ReadiLYCOAT™, further stretching end-user diversity.

Geography Analysis

Asia-Pacific controlled 33.67% of 2025 revenue and is projected for an 7.72% CAGR, making it both the largest and the fastest region in the tablet coatings market. India’s CRDMO operators collectively announce multi-year capex aimed at doubling coated-tablet output by 2030, supported by government production incentives. China’s modernization drive includes WuXi STA’s peptide complex that triples spray-drying and film-coating capacity; Korean player SK pharmteco injects USD 260 million into small-molecule lines, underscoring regional momentum. These investments pull in coating raw materials ranging from hydroxypropyl methylcellulose to specialized color blends.

North America retains its innovation edge. The FDA’s 2025 guideline on continuous processing triggers fresh equipment orders, while USD 160 billion in projected pharmaceutical capex provides a steady pipeline for retrofit opportunities. PCI Pharma’s USD 365 million upgrade and Hovione’s USD 170 million New Jersey expansion highlight the commitment to higher-value coating technologies.

Europe wrestles with regulatory unknowns surrounding TiO2 but compensates through technology leadership and large-scale peptide projects. CordenPharma’s EUR 900 million commitment underlines continued confidence, and Evonik’s restructuring channels resources into high-growth drug-delivery coatings. The upcoming EMA opinion on TiO2 may catalyze a wave of reformulations, providing suppliers of calcium-carbonate opacifiers and polymeric whiteners with new revenue streams.

Competitive Landscape

The tablet coatings market remains moderately concentrated. Colorcon tops the leaderboard, cementing position via a USD 740 million cellulose distribution alliance with Lotte Fine Chemical. BASF leverages a broad excipient catalog, while Evonik focuses on specialty acrylics that cut preparation time by 70%. Continuous innovation is vital. Jabil’s acquisition of Pharmaceutics International adds 360,000 ft² of CDMO space, signaling rising demand for turnkey coating services. Integer Holdings acquired Precision Coating to blend device surface expertise with pharma coatings, hinting at cross-sector convergence.

Partnerships drive technical depth. Hovione and Zerion Pharma formed a venture to scale Dispersome carriers, while Colorcon launches Nutrapure, targeting clean-label supplement makers. Sustainability is another competition axis; suppliers race to offer TiO2-free whites and biodegradable polymers in advance of potential mandates. Digitalization equally separates leaders, as companies integrate PAT, MES, and cloud analytics into equipment offerings, cutting downtime and providing predictive maintenance insights to clients.

Tablet Coatings Industry Leaders

Merck KGaA

Kerry Group PLC

Ashland Global Holdings

BASF SE

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Colorcon’s Opadry Complete Film Coating System wins the Market Impact Award at CPHI China 2025, acknowledging innovation and customer trust.

- April 2025: Ashland expands its Brazilian plant for Aquarius coatings and adds a microbial-protection suite to reinforce global supply resilience.

- February 2025: Roquette unveils a platform combining Tabshield and ReadiLYCOAT ready-to-use systems to serve Rx, nutraceutical, and OTC markets.

- June 2024: Hovione debuts a continuous tableting line in Lisbon, co-developed with GEA, optimized for potent APIs and minimal material use.

Global Tablet Coatings Market Report Scope

As per the scope of the report, tablet coating is the process of applying a coating material to the surface of the tablet to achieve the desired properties of the dosage form. Tablet coating is a significant step involved in the manufacturing process of tablet dosage forms. This coating process involves the deposition of thin and uniform polymer-based formulations onto the surface of solid dosage forms such as tablets, capsules, powders, granules, or pallets.

the tablet coatings market is segmented by coating type (film-coated, sugar-coated, enteric-coated, and other coating types), polymer (cellulose ether polymers, vinyl alcohol polymers, acrylic acid polymers, and other polymers), formulation (plasticizer, colorant, and solvent (vehicle)), application (immediate-release, sustained-release, and extended-release), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Film-coated |

| Sugar-coated |

| Enteric-coated |

| Functional coatings |

| Other coating types |

| Cellulose ethers |

| Acrylic acid polymers |

| Vinyl alcohol polymers |

| Polyethylene glycol & derivatives |

| Other polymers |

| Plasticizers |

| Colorants |

| Solvents / Vehicles |

| Opacifiers & anti-tack agents |

| Conventional pan coating |

| Perforated pan coating |

| Fluidized-bed coating |

| Continuous coating systems |

| Immediate-release |

| Sustained-release |

| Extended-release |

| Delayed / enteric release |

| Pharmaceutical manufacturers |

| Nutraceutical & dietary-supplement companies |

| CDMOs & CMOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Coating Type | Film-coated | |

| Sugar-coated | ||

| Enteric-coated | ||

| Functional coatings | ||

| Other coating types | ||

| By Polymer | Cellulose ethers | |

| Acrylic acid polymers | ||

| Vinyl alcohol polymers | ||

| Polyethylene glycol & derivatives | ||

| Other polymers | ||

| By Formulation Component | Plasticizers | |

| Colorants | ||

| Solvents / Vehicles | ||

| Opacifiers & anti-tack agents | ||

| By Process / Equipment | Conventional pan coating | |

| Perforated pan coating | ||

| Fluidized-bed coating | ||

| Continuous coating systems | ||

| By Application | Immediate-release | |

| Sustained-release | ||

| Extended-release | ||

| Delayed / enteric release | ||

| By End-User | Pharmaceutical manufacturers | |

| Nutraceutical & dietary-supplement companies | ||

| CDMOs & CMOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the tablet coatings market?

The tablet coatings market is valued at USD 1.04 billion in 2026 and is projected to reach USD 1.33 billion by 2031.

Which coating type generates the highest revenue?

Film-coated tablets hold 52.74% of 2025 revenue, making them the leading coating type.

Why is Asia-Pacific considered pivotal for market growth?

Asia-Pacific commands 33.67% share and posts the fastest 7.72% CAGR due to aggressive pharmaceutical manufacturing expansion in India, China, and South Korea.

How are regulations influencing titanium dioxide usage?

The European Medicines Agency is assessing TiO2 safety, and potential restrictions are pushing formulators toward calcium-carbonate and polymeric opacifiers.

What drives the surge in continuous manufacturing adoption?

Regulatory incentives from the FDA, coupled with demonstrable cost and quality benefits, are accelerating the shift from batch to continuous coating lines.

Page last updated on: