Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

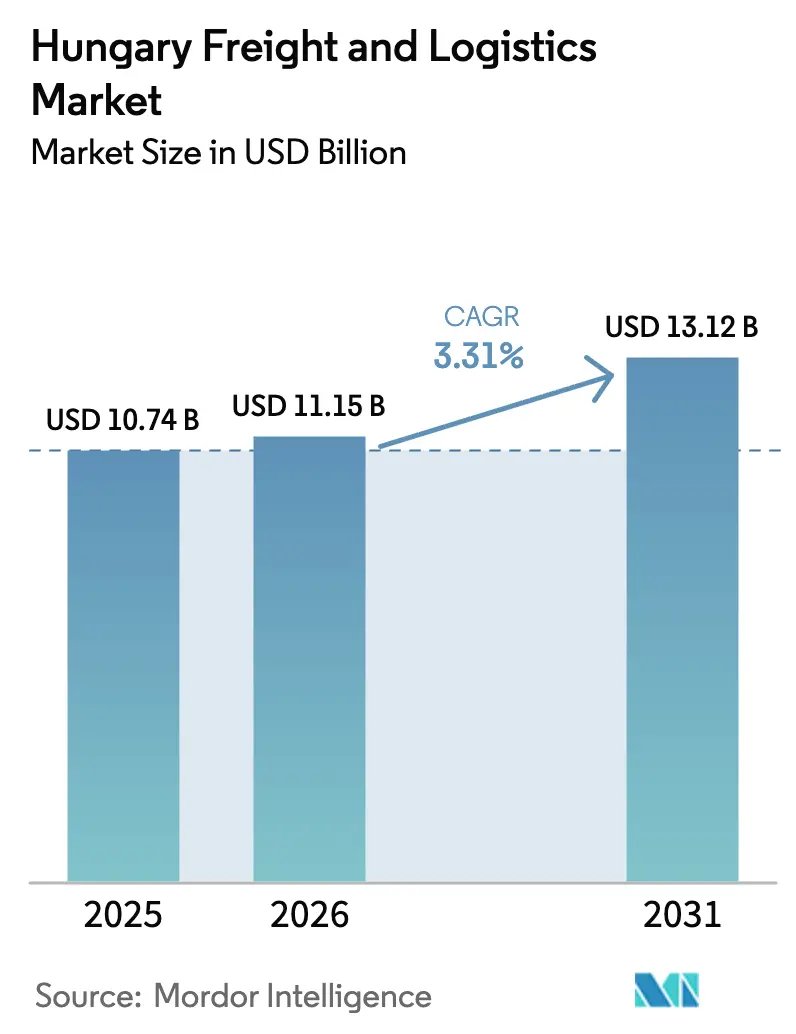

| Base Year Market Size (2025) | USD 10.74 Billion |

| Market Size (2026) | USD 11.15 Billion |

| Market Size (2031) | USD 13.12 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Freight And Logistics Market Analysis by Mordor Intelligence

The Hungary Freight And Logistics Market size is estimated at USD 11.15 billion in 2026, and is expected to reach USD 13.12 billion by 2031, at a CAGR of 3.31% during the forecast period (2026-2031).

The Hungary freight and logistics market benefits from its gateway role on the Rhine-Danube and Orient-East Med corridors, steady EU Cohesion Fund inflows, and expanding e-commerce volumes that lift courier, express, and parcel activity. Ongoing motorway and rail upgrades raise service reliability, while a wave of automotive and battery investments anchors long-haul freight volumes. Competitive intensity is moderate, as multinational integrators fight regional specialists for temperature-controlled contracts and just-in-time automotive flows. Labor scarcity, fuel-price volatility, and temporary rail works temper growth, yet digital freight platforms and intermodal hubs continue to unlock productivity.

Key Report Takeaways

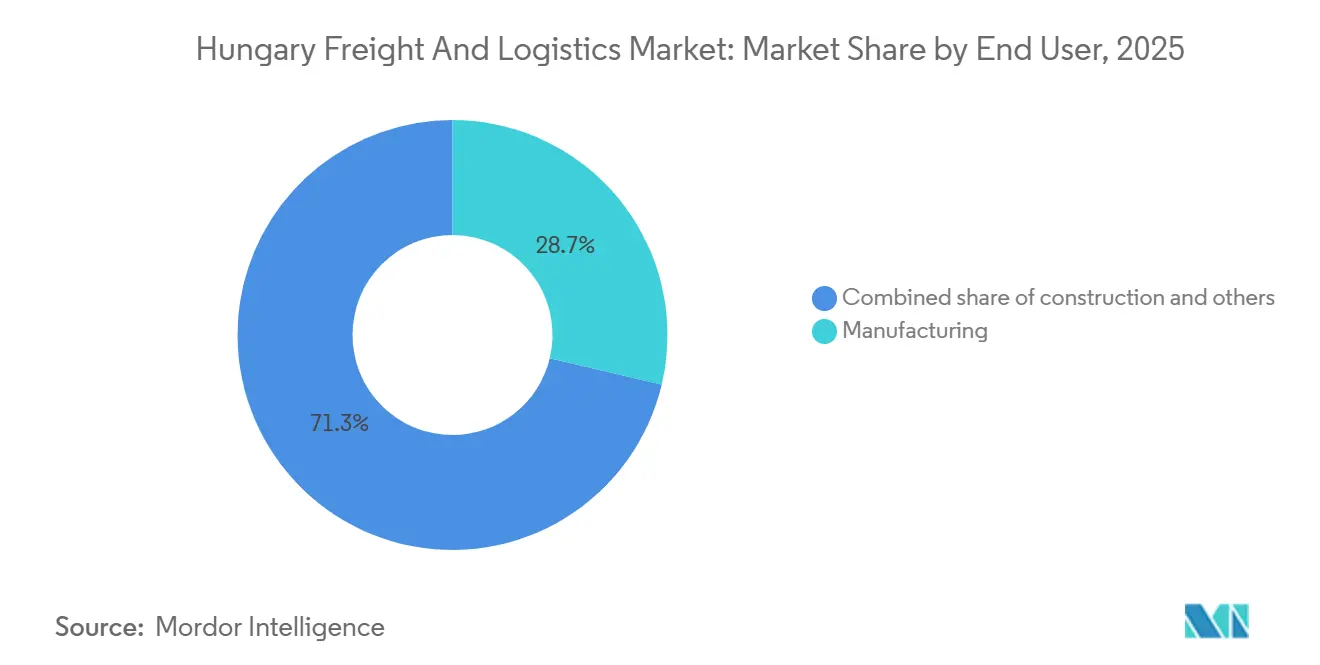

- By end user industry, manufacturing led with 28.72% of the Hungary freight and logistics market share in 2025; Wholesale and Retail Trade is forecast to expand at a 3.74% CAGR through 2031.

- By logistics function, freight transport accounted for 44% of the Hungary freight and logistics market size in 2025, while CEP services are advancing at a 4% CAGR through 2031.

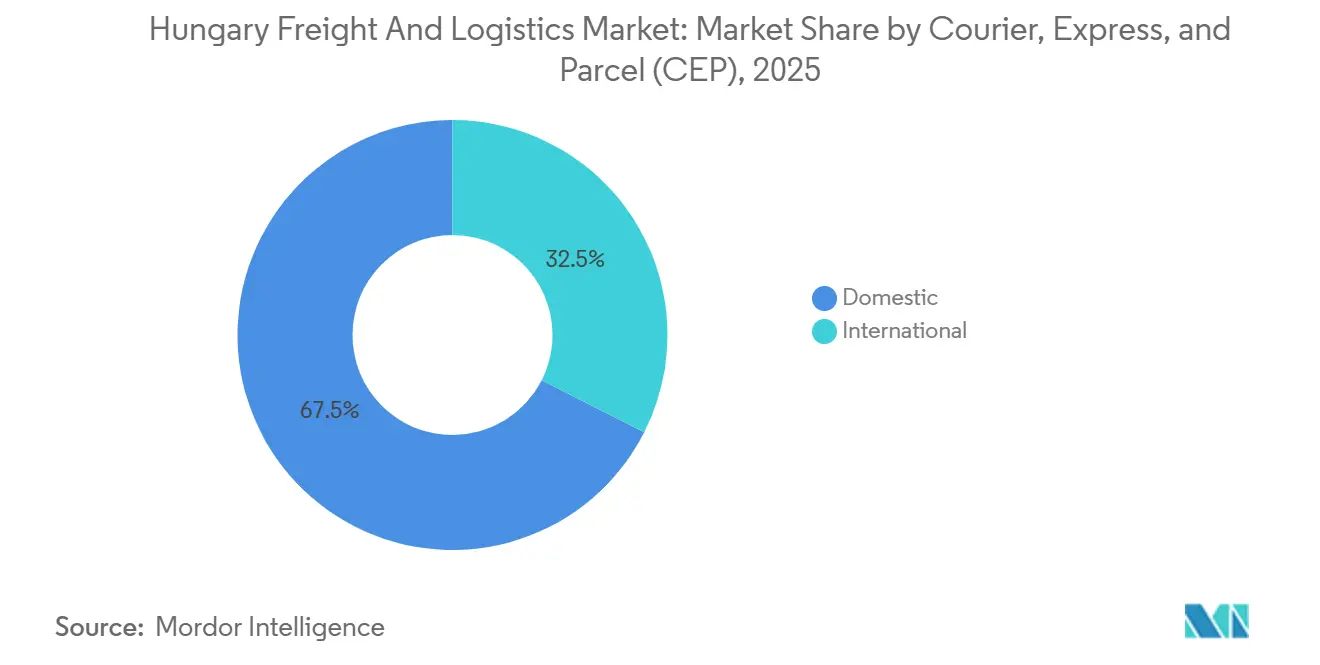

- By CEP destination, domestic shipments captured 67.53% of volume in 2025; international parcels are projected to grow at a 3.83% CAGR through 2031.

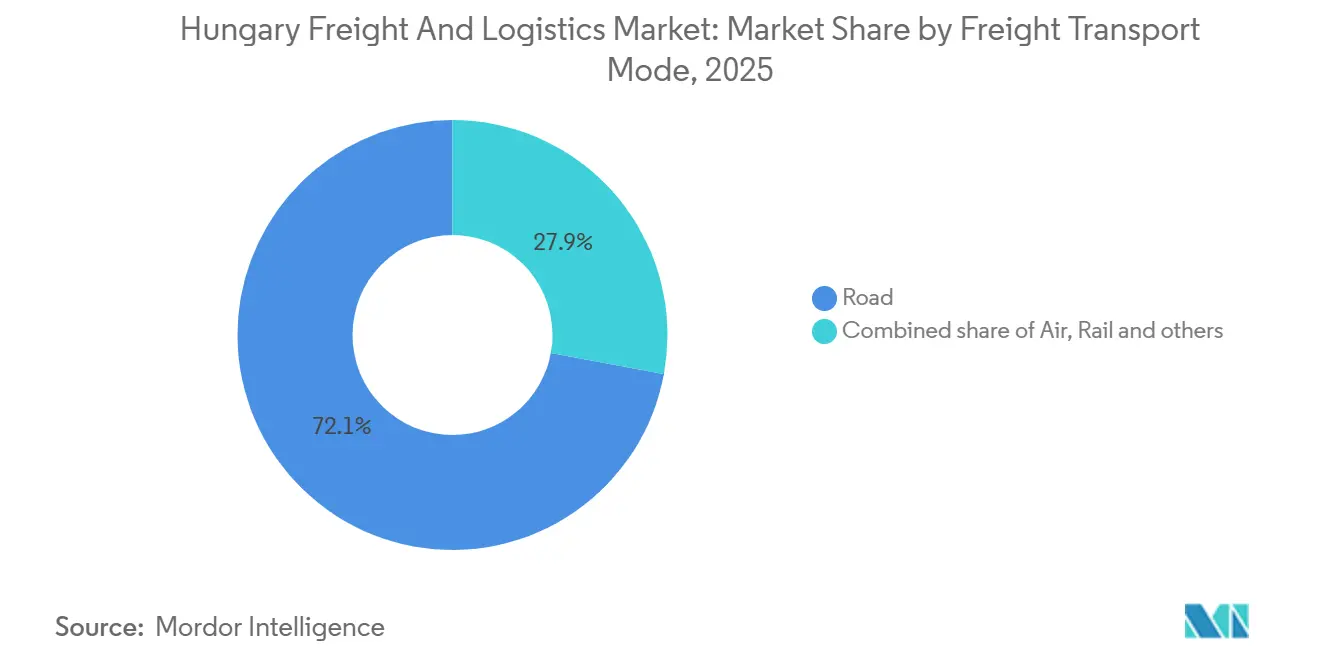

- By freight transport mode, road haulage commanded 72% revenue share in 2025, whereas air cargo is forecast to grow at a 4% CAGR through 2031.

- By warehousing and storage, non-temperature controlled facilities commanded 90.31% of the revenue share in 2025; temperature controlled space is accelerating at a 3.52% CAGR between 2026 and 2031.

- By freight forwarding mode, sea and inland waterways led with 69.87% revenue share in 2025; air forwarding is projected to post a 3.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hungary Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Strategic position as EU land-bridge & corridor investments | +0.9% | National, with concentration in Budapest, Győr, Debrecen corridors | Medium term (2-4 years) |

| E-commerce boom spurring last-mile demand | +0.7% | National, urban clusters (Budapest, Debrecen, Szeged) lead adoption | Short term (≤ 2 years) |

| Road & rail upgrades via EU Cohesion Funds | +0.6% | National, priority on TEN-T core network segments | Long term (≥ 4 years) |

| Automotive-battery near-shoring logistics demand | +0.8% | Regional, concentrated in Debrecen, Győr, Kecskemét industrial zones | Medium term (2-4 years) |

| Budapest Airport Cargo City expansion | +0.2% | National, spillover to regional distribution hubs | Short term (≤ 2 years) |

| Digital freight-platform adoption | +0.1% | National, early gains in cross-border lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strategic Position as EU Land-Bridge & Corridor Investments

Hungary’s central position along the Rhine-Danube and Orient-East Med corridors makes it a key transit point between Western Europe and the Balkans. Backed by EUR 370 million (USD 431 million) in EU grants for road, rail, and terminal upgrades, the country is boosting freight capacity. The Budapest-Belgrade double-track line will cut transit times by 40% and shift cargo from road to rail, easing M5 congestion. Greater reliability for automotive and retail flows is driving hub consolidation around Budapest, where developers are adding speculative warehouses near the ring road. Despite short-term congestion during construction, Hungary is strengthening its role as a key European logistics bridgehead.[1]European Commission, “TEN-T Infrastructure,” EC.EUROPA.EU.

E-commerce Boom Spurring Last-Mile Demand

Hungarian e-commerce revenue is forecast to reach EUR 4.8 billion (USD 5.6 billion) by 2028, an 8.2% CAGR that outpaces overall freight growth[2]Statista Analysts, “E-commerce Hungary Outlook,” STATISTA.COM. A 67% cross-border shopping rate pushes integrators to design networks that balance domestic density with pan-regional sortation, driving parcel locker rollouts and micro-fulfillment nodes. GLS Hungary already handles 25 million annual parcels through 1,000 lockers and 50 depots with a 99.7% delivery success rate, a performance rooted in automation and route optimization. Such reliability encourages retailers to promise next-day service nationwide, increasing shipment frequency and shrinking average consignment size. Urban emission zone plans in Budapest accelerate the shift toward electric vans, prompting fleet renewal and charging-hub investment. Consequently, the Hungary freight and logistics market receives a steady influx of high-margin CEP revenue that counterbalances lower-yield bulk transport.

Road & Rail Upgrades via EU Cohesion Funds

Hungary’s EUR 21.7 billion (USD 25.3 billion) Cohesion Fund envelope finances 450 kilometers of motorway rehabilitation, 300 kilometers of rail electrification, and three intermodal terminals, though inflationary pressures extend build schedules by up to 18 months. The M4 extension to the Romanian border opened late-2025 sections that cut eastbound transit times for automotive suppliers. While rail tonnage dipped during corridor works, long-term capacity gains will restore shipper confidence once double-track segments open. Operators that pre-book slots or lease block trains secure a competitive advantage, especially for heavy components moving to Debrecen and Gyor. The Hungary freight and logistics market, therefore, accepts short-term disruptions as a trade-off for durable speed gains and modal diversification.

Automotive-Battery Near-Shoring Logistics Demand

BMW, CATL, and BYD have committed more than EUR 10 billion (USD 11.66 billion) to Hungarian plants, which together add thousands of daily inbound and outbound shipments. BMW Debrecen alone requires 120 just-in-time truck movements per day, while CATL imports lithium compounds via the Port of Koper for rail transfer to Debrecen. These flows demand temperature-controlled containers, bonded warehousing, and real-time visibility, lifting average revenue per shipment. Waberer’s reserved 50 dedicated tractors to safeguard service levels on the corridor, illustrating how asset commitment secures automotive contracts. As battery plants ramp, demand shifts toward outbound finished-module distribution into Western Europe, boosting intermodal rail volumes. The Hungary freight and logistics market thus captures a structural upgrade from commodity bulk to high-value engineered freight.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Driver shortage & rising labor cost | -0.5% | National, acute in cross-border long-haul segments | Short term (≤ 2 years) |

| Fuel-price & toll volatility | -0.3% | National, disproportionate impact on small owner-operators | Short term (≤ 2 years) |

| Urban emission zones restricting access | -0.1% | Budapest, potential expansion to Debrecen, Szeged | Medium term (2-4 years) |

| Rail bottlenecks during corridor works | -0.2% | National, concentrated on TEN-T core network | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Driver Shortage & Rising Labor Cost

Europe faces a projected shortfall of 745,000 truck drivers by 2028, and Hungarian vacancy rates are already near 1.6%, impeding fleet expansion[3]International Road Transport Union, “Driver Shortage Crisis Worsens,” IRU.ORG. Average gross earnings in the sector grew 9.2% year on year to USD 2,100 in 2025, compressing margins for small fleets that cannot amortize wage hikes across large networks. Operators decline profitable contracts or subcontract at thinner spreads when seats go unfilled, shifting bargaining power toward drivers and agencies. Larger integrators deploy driver-assist systems and work-life scheduling tools to retain staff, but capital outlays raise entry barriers for newcomers. The Hungary freight and logistics market, therefore, experiences gradual consolidation as under-capitalized carriers exit or merge.

Fuel-Price & Toll Volatility

Diesel excise duty hovers near USD 37.50 per hectoliter net, and the CO₂-linked HU-GO toll added up to USD 0.17 per kilometer for older trucks in 2025. Combined with Europe’s highest VAT rate of 27%, pump prices exceed regional averages, straining owner-operators that lack hedging tools. Variable toll surcharges reduce pricing transparency, prompting shippers to request fuel-adjustment clauses that erode carrier negotiating power. Some micro-fleets mothball Euro V assets early, further tightening capacity. The Hungary freight and logistics market thus confronts cost pass-through challenges that favor operators with scale and procurement leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Anchors Demand, Retail Trade Accelerates

Manufacturing captured 28.72% of the Hungary freight and logistics market share in 2025, driven by automotive, electronics, and pharmaceuticals. Just-in-time assembly at BMW Debrecen and Audi Gyor relies on synchronized inbound steel, semiconductors, and battery cells that transit via both rail and road. Pharmaceutical flows add stringent GDP compliance, pushing carriers to certify warehouses and train staff to secure multi-year contracts. Meanwhile, Wholesale and Retail Trade, the fastest-growing sub-segment, expands at 3.74% CAGR as omni-channel merchants extend fulfillment centers outside Budapest to shorten same-day delivery radii. The Hungary freight and logistics market therefore shifts toward higher service differentiation, with asset-light brokers retreating to commodity cargo as shippers audit carrier certifications.

Retail’s rise stems from cross-border e-commerce habits and disposable-income growth that lifts parcel density. CEP operators overlay parcel lockers on grocery stores, enabling click-and-collect models that reduce failed deliveries. Manufacturing retains absolute tonnage dominance, yet its share declines modestly as consumer-driven flows multiply. Agriculture and construction remain cyclical, linked to harvest yields and public-works budgets, contributing surge demand periods rather than year-round stability. As capital projects conclude, freed capacity redeploys into automotive exports, keeping the Hungary freight and logistics market balanced across industrial and consumer sectors.

By Logistics Function: Freight Transport Dominates, CEP Surges

Freight transport represented 44% of the Hungary freight and logistics market size at USD 4.51 billion in 2025, covering road, rail, air, and inland waterways. Road haulage absorbs just-in-time automotive and supermarket replenishment, while rail shares remain under pressure until corridor upgrades finish. CEP services expand at a 4% CAGR, leveraging dense urban locker networks and automated sortation to achieve sub-24-hour delivery norms. Digitized labels and real-time tracking reduce manual touches, supporting profit margins despite wage inflation.

Warehousing captures 11% of market revenue, with vacancy below 4% in Greater Budapest as e-commerce tenants sign five-year leases for 15,000 m² blocks. Freight forwarding handles 48 billion TKM, benefiting from the Hungary freight and logistics market bridge role for East-West flows. Other services such as customs brokerage and packaging face commoditization, leading to vendor consolidation onto digital platforms that auction shipments to pre-vetted carriers.

By Courier, Express, and Parcel Destination: Domestic Volume, International Growth

Domestic parcels held a 67.53% share in 2025 as Hungary’s 9.7 million residents generated sufficient density for next-day economics. Parcel lockers multiply in suburban malls, allowing two-hour collection windows that improve customer experience and lower last-mile costs. International parcels grow faster at 3.83% CAGR because Hungarian shoppers purchase fashion and electronics from Germany, Italy, and China. Integrators price cross-border consignments at a 30-40% premium, reflecting customs clearance and extended tracking requirements.

Return logistics challenge profitability, as EU rules require transparent duties and recycling of packaging waste. Providers invest in automated customs portals that pre-clear shipments before departure, speeding linehaul transit. The Hungary freight and logistics market thus prizes network flexibility that satisfies both domestic density and international reach without duplicating infrastructure.

By Warehousing and Storage: Ambient Dominates, Cold Chain Expands

Non-temperature-controlled space captured 90.31% market share in 2025, serving automotive parts, fast-moving consumer goods, and general merchandise[4]Cushman & Wakefield Research, “Hungary Market Insights,” CUSHMANWAKEFIELD.COM. Demand clusters within 30 kilometers of the M0 ring road, where occupiers secure highway access and labor pools. Vacancy tightened to 3.5% in Q3 2024, pushing headline rents upward by high-single-digit percentages. Temperature-controlled capacity advances at 3.52% CAGR, propelled by pharmaceutical near-shoring and fresh-food e-commerce. Raben’s Dunaharaszti site combines chilled, 14-18 °C, and ambient chambers, enabling multi-temperature consolidation that reduces secondary handling.

Cold-chain expansion concentrates in Debrecen’s pharma cluster and Budapest Airport’s Cargo City, where GDP compliance and airport proximity justify the 40-50% construction premium. Institutional investors seek inflation-protected leases, driving speculative builds with flexible mezzanine layouts. The Hungary freight and logistics market thus experiences bifurcation between commoditized big-box sheds and premium regulated facilities.

By Freight Transport Mode: Road Reigns, Air Freight Accelerates

Road haulage commanded 72% modal share in 2025, favored for flexibility and reliable transit on the 1,300-kilometer motorway network. Diesel excise and toll surcharges pressure margins, yet operators offset costs through high asset utilization and drop-and-hook systems at automotive plants. Air cargo tonnage at Budapest Airport rose 49% year on year to 200,000 tonnes in H1 2025, on track for 450,000-tonne capacity by 2027. Electronics prototypes, pharmaceuticals, and e-commerce returns favor air because linehaul reliability outweighs rate premiums.

Rail volume dipped during TEN-T works but regains competitiveness once double-track electrified segments open post-2027, enabling 1,200-meter trains that carry 76 TEUs each. Inland waterways remain a niche on the Danube, handling mainly bulk commodities and repositioned empty containers. The Hungary freight and logistics market, therefore, relies on road for capacity and on air for high-value urgency until rail modernization concludes.

By Freight Forwarding Mode: Inland Waterways Lead, Air Gains Share

Sea and inland waterways contributed 69.87% of forwarding revenue in 2025 because Adriatic ports and Danube barge traffic dominate containerized imports. Most flows transit Hungary without domestic origin or destination, limiting local value-added but supporting haulage into Austria and Slovakia. Air forwarding expands at a 3.46% CAGR, anchored by pharmaceuticals and electronics that require sub-24-hour door-to-door delivery. Kuehne + Nagel’s Budapest branch integrates cargo capacity, customs brokerage, and scheduled van routes, capturing end-to-end control for OEMs.

Road and rail forwarding split the remainder, with digital freight platforms matching spot loads and leveraging Hungary’s September 2024 e-CMR adoption for paperless documentation. Waterway competitiveness stagnates due to an empty-container imbalance and aging lock infrastructure south of Budapest. The Hungary freight and logistics market thus prizes forwarding models that bundle mode-neutral capacity with compliance expertise.

Geography Analysis

Budapest, Gyor, and Debrecen together generated about 65% of Hungary's freight and logistics market revenue in 2025, reflecting their combined industrial base, population, and hub infrastructure. Budapest offers airport cargo capacity and Danube barges, attracting integrators and 3PL headquarters. Gyor’s Audi engine plant has surpassed five million units of cumulative production, sustaining feeder part movements and a near-zero vacancy rate below 2% for industrial space. Debrecen emerges as the fastest-growing node as BMW and CATL investments trigger 200 daily truck calls and stimulate cold-chain and bonded-zone demand.

Eastern corridors strengthen following M4 motorway extensions to the Romanian border, shifting share toward Szolnok and Nyíregyháza. Completion of the Budapest-Belgrade rail line in 2027 will shorten Adriatic transit for Kecskemét and Szeged suppliers by 40%, lifting rail’s regional share. Warehouse dynamics diverge: Greater Budapest vacancy remains tight in Q3 2025, while secondary cities hold above 8%, offering expansion options for cost-sensitive retailers. Cross-border lanes to Austria and Slovakia account for roughly 40% of tonnage but face 10-15% compliance-cost increases from the EU Mobility Package social provisions.

EU funds prioritize TEN-T core nodes, skewing grant allocation toward Budapest and Debrecen. Peripheral counties lobby for last-mile projects, but fiscal space narrows as inflation lifts construction costs. The Hungary freight and logistics market thus consolidates along an east-west spine, with secondary hubs gaining only when supported by specific industrial anchors or subsidy schemes.

Competitive Landscape

The top ten operators command roughly 35-40% of Hungary's freight and logistics market revenue, leaving ample space for regional specialists and digital entrants. DSV’s USD 14.3 billion acquisition of DB Schenker, cleared in April 2025, creates a European giant with deeper contract-logistics capacity, yet faces a 12-month IT integration that risks customer churn. Waberer’s International secured a 62.5% stake in GySEV Cargo, closing in late 2025, giving the domestic champion rail traction that aligns with EU Green Deal modal-shift incentives.

Digital freight platforms partner with traditional forwarders to pool capacity and provide eFTI-ready data, accelerating after Hungary acceded to the e-CMR convention in 2024. DHL Supply Chain renewed a long-term lease at CTPark Budapest East, adding automation that reduces pick times and raises labor productivity. Hellmann Worldwide teamed with Trans.eu in October 2025 to digitize tendering and onboard 100 Hungarian carriers, illustrating how mid-tier players leverage technology to offset scale gaps. Temperature-controlled niches attract capital, as Raben and Logicor build GDP-compliant facilities that command 30-40% rent premiums. Consequently, the Hungary freight and logistics market rewards scale, compliance expertise, and digital transparency, while price-focused micro-fleets either specialize in rural lanes or exit through consolidation.

Hungary Freight And Logistics Industry Leaders

Waberer’s International Nyrt.

Magyar Posta Zrt.

Rail Cargo Hungaria Zrt

DHL Logistics Hungary

DSV Solutions Kft.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Waberer’s Group acquired the remaining 33.075% stake in Hungarian Post Insurance, diversifying revenue and supporting integrated service bundles.

- October 2025: Hellmann Worldwide Logistics partnered with Trans.eu to digitize freight processes and connect with more than 100 Hungarian carriers, reducing empty miles and improving visibility.

- July 2025: DHL Supply Chain extended its lease at CTPark Budapest East, undertaking facility upgrades to support continued automotive and retail contracts.

- April 2025: DSV finalized the takeover of DB Schenker, unifying operations under the DSV brand and expanding contract-logistics footprints in Hungary.

Hungary Freight And Logistics Market Report Scope

By End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

By Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

Key Questions Answered in the Report

What is the current value of the Hungary freight and logistics market?

The market is valued at USD 11.15 billion in 2026 and is forecast to reach USD 13.12 billion by 2031.

How fast is the Hungary freight and logistics market growing?

Aggregate revenue is projected to advance at a 3.31% CAGR between 2026 and 2031.

Which end-user segment contributes the largest share?

Manufacturing leads with 28.72% share due to automotive, electronics, and pharmaceutical production.

Which logistics function is expanding the quickest?

Courier, express, and parcel services are growing at about 4% CAGR, outpacing other functions.

What infrastructure projects most influence future growth?

The Budapest–Belgrade double-track rail line and ongoing motorway expansions under the EU Cohesion Fund substantially raise capacity and speed post-2027.

Page last updated on: