Central and Eastern Europe Freight and Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

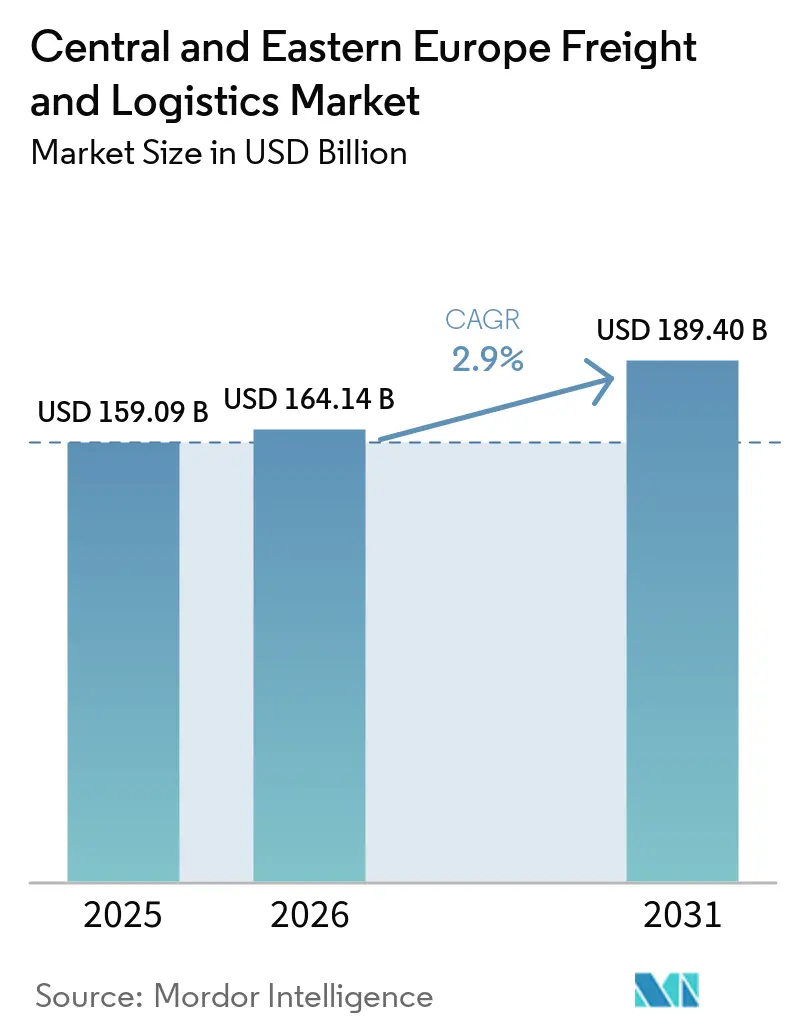

| Base Year Market Size (2025) | USD 159.09 Billion |

| Market Size (2026) | USD 164.14 Billion |

| Market Size (2031) | USD 189.40 Billion |

| Growth Rate (2026 - 2031) | 2.90% CAGR |

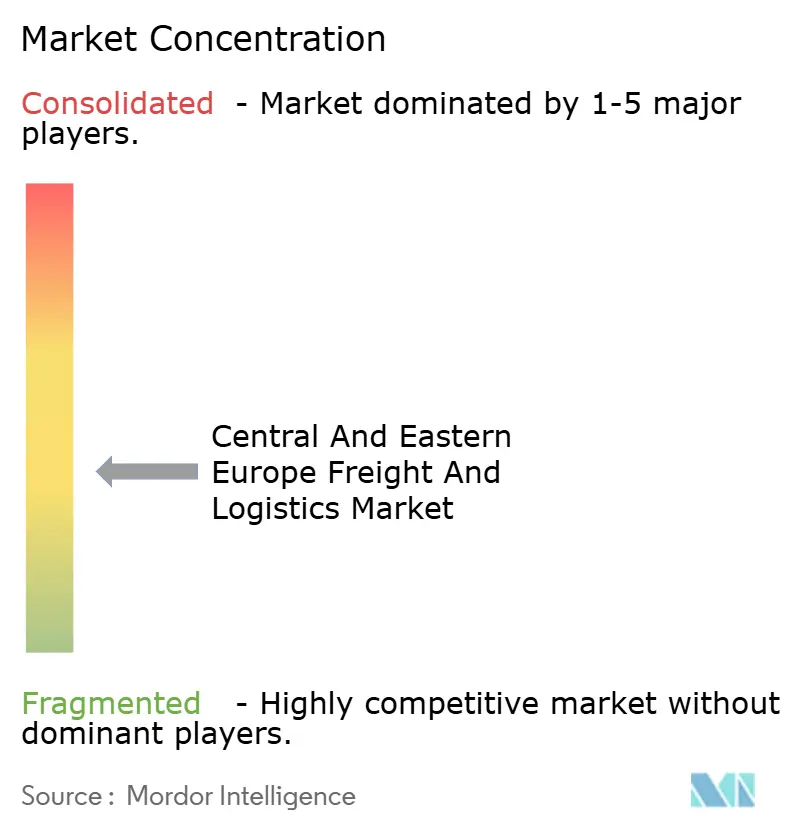

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central and Eastern Europe Freight and Logistics Market Analysis by Mordor Intelligence

The Central and Eastern Europe freight and logistics market size is estimated to be USD 159.09 billion in 2025, with USD 164.14 billion in 2026, and projected to reach USD 189.40 billion by 2031, growing at a CAGR of 2.9% from 2026 to 2031.

Defense-related infrastructure upgrades, EU-mandated alternative-fuel corridors, and fast-growing digital commerce are reshaping capacity allocation across every logistics mode, prompting carriers to accelerate fleet renewal and network redesign. NATO’s military-mobility program is standardizing heavy-lift handling and cutting civilian border wait times by up to 40%. Simultaneously, the EU Alternative Fuels Infrastructure Regulation (AFIR) obliges CEE states to install 3,600 heavy-duty charging points and 1,000 LNG stations by 2030, triggering multi-billion-euro corridor investments. Emerging Baltic-Adriatic mega-hubs now reduce north-south lead times by as much as one-third, diverting Asia-Europe trade from more congested Rhine-Alpine routes. High-value project cargo for hyperscale data-center builds, and CBAM-driven steel re-routing through Black Sea ports extend the demand runway for specialized carriers and freight forwarders focused on regulatory compliance services.

Key Report Takeaways

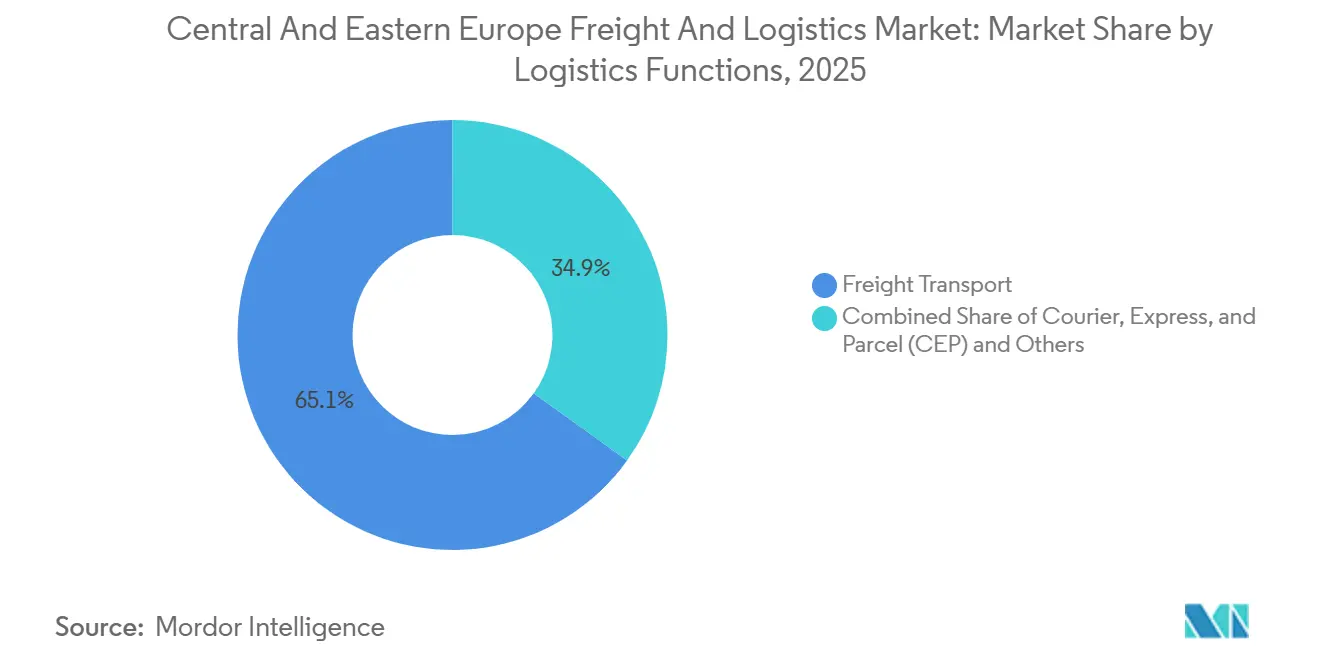

- By logistics function, freight transport held 65.08% of the Central and Eastern Europe freight and logistics market size in 2025, while courier, express, and parcel (CEP) posted the fastest 3.35% CAGR through 2031.

- By freight transport mode, road captured 74.82% of the Central and Eastern Europe freight and logistics market share in 2025, and air freight leads growth at a 4.44% CAGR to 2031.

- By CEP service, domestic deliveries represented 65.48% of the Central and Eastern Europe freight and logistics market in 2025, while international CEP is on track for 3.49% CAGR to 2031.

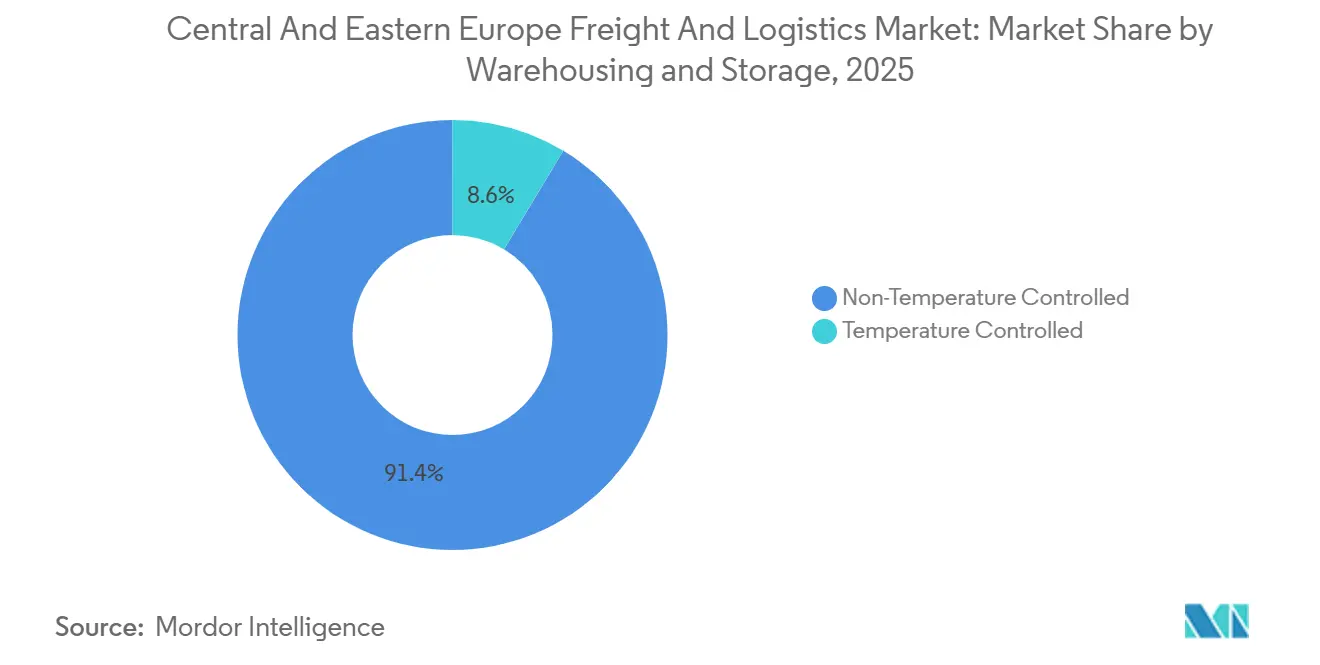

- By warehousing and storage, non-temperature-controlled facilities controlled 91.39% of the Central and Eastern Europe freight and logistics market in 2025, and temperature-controlled storage advances at a 2.70% CAGR through 2031.

- By freight forwarding mode, sea and inland waterways retained 50.09% share in 2025, but air forwarding is accelerating at 3.86% CAGR to 2031.

- By end user, wholesale and retail trade commanded 30.58% of the Central and Eastern Europe freight and logistics market in 2025 and is projected to expand at 3.12% CAGR through 2031.

- By country, Poland dominated with 32.72% of the Central and Eastern Europe freight and logistics market in 2025, whereas Bulgaria is set to grow fastest at 3.24% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Central and Eastern Europe Freight and Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NATO Military-Mobility Cargo Surge Fuelling Contract-Logistics Demand | +0.6% | Poland, Baltic states, Romania, with spillover to Slovakia, Hungary | Medium term (2-4 years) |

| Roll-out of LNG/EV/HVO Heavy-Vehicle Corridors under EU AFIR | +0.5% | CEE-wide TEN-T corridors, with early deployment in Poland, Czech Republic | Long term (≥ 4 years) |

| Baltic-Adriatic Intermodal Mega-Hubs Slashing Door-to-Door Lead-Times | +0.5% | Poland, Czech Republic, Slovenia, Austria border regions | Medium term (2-4 years) |

| Data-Centre Construction Boom Creating High-Value Project Logistics | +0.4% | Poland, Romania, Hungary, with emerging activity in Bulgaria | Short term (≤ 2 years) |

| CBAM-Induced Re-routing of Steel & Aluminium via Black Sea Ports | +0.3% | Romania, Bulgaria, with impact on Danube corridor countries | Medium term (2-4 years) |

| Tier-2 Balkan Q-Commerce Uplift Driving Same-day CEP Volumes | +0.3% | Serbia, Bulgaria, Albania, North Macedonia, Bosnia and Herzegovina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

NATO Military-Mobility Cargo Surge Fuelling Contract-Logistics Demand

NATO’s pledge to deploy 300,000 troops rapidly across its eastern flank made dual-use road, rail, and port upgrades a strategic imperative. Bridge reinforcement, wider rail platforms, and customs pre-clearance systems already cut civilian freight transit by up to 40% on key corridors. Contract-logistics firms have secured multi-year agreements worth EUR 50-100 million (USD 58- 118 million) to store and reposition armored vehicles and oversized generators. Standardized heavy-lift procedures initially written for defense equipment are now applied to wind-turbine and industrial-machinery projects, widening the addressable market. Gauge-harmonization efforts along the Baltic-Black Sea axis further eliminate time-consuming bogie exchanges, enhancing rail competitiveness and unlocking additional Central and Eastern Europe freight and logistics market opportunities[1]NATO, “Military Mobility,” nato.int.

Roll-out of LNG/EV/HVO Heavy-Vehicle Corridors under EU AFIR

AFIR obliges member states to place e-truck charging every 60 km and LNG refueling every 150 km on core TEN-T routes by 2030, underpinning more than EUR 10 billion (USD 11.7 billion) of public-private investment. Poland alone targets 450 heavy-duty chargers by 2027, with Romania installing 12 LNG stations on its north-south arteries. Early adopters report 15-20% lower total cost of ownership over five-year cycles once carbon-pricing exposure is factored in. Hauliers gain network certainty, prompting accelerated diesel fleet retirement and boosting demand for renewable HVO especially in the Czech Republic and Slovakia where local production reduces supply risk. Corridor interoperability allows carriers to schedule alternative-fuel trucks across multiple borders, reinforcing modal flexibility and bolstering the Central and Eastern Europe freight and logistics market’s decarbonization trajectory.

Baltic-Adriatic Intermodal Mega-Hubs Slashing Door-to-Door Lead Times

Upgraded terminals in Gliwice and Koper now accommodate 1,000-meter trains and automate box handling, reducing truck dwell to under 30 minutes and slicing end-to-end transit by 25-35%. Competitive alternatives to Rhine-Alpine lanes are shifting Asia-Europe volumes eastward, heightening hub-and-spoke consolidation that lifts vehicle utilization 20-30%. Mega-hub density supports rail’s modal-shift ambitions, counters driver shortages, and opens new revenue streams for intermodal forwarders. Infrastructure certainty also draws investment in value-added facilities such as bonded warehouses and temperature-controlled cross-docks near hub gates, expanding Central and Eastern Europe freight and logistics market service breadth[2]European Commission, “TEN-T Corridor Coordinators,” transport.ec.europa.eu.

Data-Center Construction Boom Creating High-Value Project Logistics

More than EUR 2 billion (USD 2.5 billion) flowed into Polish hyperscale builds during 2024-2025, with 150 MW under construction in Bucharest and fresh capacity planned for Budapest. Each site requires 200-300 oversized transport moves, including 100-ton transformers and 80-ton cooling units. Project-logistics specialists provide route surveys, heavy-lift cranes, and temperature-controlled staging that mitigate urban infrastructure constraints. Operators increasingly demand carbon-neutral deliveries, accelerating uptake of electric and HVO-powered trucks along project lanes. The specialized nature of this cargo yields premium margins and propels the Central and Eastern Europe freight and logistics market toward higher-value services.

Restraints Impact Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distance-Based Road-User Charges Raising SME Carrier Opex | -0.5% | Poland, Czech Republic, Hungary, with potential expansion to Romania, Bulgaria | Short term (≤ 2 years) |

| Wagon & Container Shortages on East-West Rail Corridors | -0.4% | Poland, Czech Republic, Slovakia, with impact on Germany-bound freight | Medium term (2-4 years) |

| Stricter 2025 Danube Emission Caps Elevating Barge Freight Rates | -0.3% | Danube corridor countries: Romania, Bulgaria, Serbia, Hungary, Slovakia | Short term (≤ 2 years) |

| Cyber-security Breaches Driving Up Insurance & Contingency Costs | -0.3% | CEE-wide, with particular impact on digitally-integrated logistics providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Distance-Based Road-User Charges Raising SME Carrier Opex

Electronic tolling rolled out on all Polish roads over 3.5 tons in 2024 lifted per-kilometer fees 18-22%, adding EUR 3,000-5,000 (USD 3,510- 5,900) to annual SME budgets. Quarterly rate revisions tied to vehicle-emissions classes inject pricing volatility that scale players absorb more easily than family firms. Czech plans to extend distance tolling to secondary roads in 2026 will broaden the cost impact and accelerate consolidation. Many small carriers seek routing software to squeeze empty miles but struggle to finance subscriptions, intensifying exit risk. These headwinds temper the Central and Eastern Europe freight and logistics market growth outlook during the near term[3]European Commission, “Road Tolls and Distance Charging,” europa.eu.

Wagon & Container Shortages on East-West Rail Corridors

A Europe-wide deficit of 15,000-20,000 intermodal wagons and chronic imbalance between westbound and eastbound flows add EUR 150-250 (USD 175-295) per TEU for repositioning. Procurement lead times stretch to 24 months, and leasing liquidity in CEE lags Western Europe, constraining rail capacity just as policy support grows. Dynamic surge pricing erodes rail’s cost edge and nudges shippers back to road despite rising tolls. Digital pooling platforms show promise but still grapple with technical-spec harmonization across 15+ operators. Without swift asset expansion, rail’s share risks stagnation, limiting the Central and Eastern Europe freight and logistics market’s modal-shift targets through 2028[4]European Commission, “Rail Transport and Logistics,” transport.ec.europa.eu .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Freight Transport Dominance Meets Rapid CEP Upswing

Freight transport captured 65.08% of the 2025 value, anchoring the Central and Eastern Europe freight and logistics market even as contract-logistics providers diversify into defense and renewable-energy projects. A wide road network, upgraded under NATO programs, enhances domestic trunk efficiency, while rail bottlenecks underscore the segment’s resilience. Warehouse and storage service revenue rises on the back of data-center equipment staging and temperature-controlled pharmaceutical demand.

CEP’s 3.35% CAGR through 2031 reflects explosive mid-tier city q-commerce orders that scale micro-fulfillment footprints fivefold between 2024 and 2027. CEP platform growth spills over to freight forwarding as importers demand customs and carbon-audit expertise for steel, aluminum, and consumer electronics. Other services, notably consultancy for AFIR and CBAM compliance, secure long-term retainers with manufacturers optimizing Scope 3 footprints. Automation, 5G-enabled transparency, and predictive maintenance trim warehouse operating costs 10-15% and reinforce cross-functional synergies, sustaining the Central and Eastern Europe freight and logistics market momentum.

By Freight Transport Mode: Road Pre-eminence Under Cost Pressure

Road held 74.82% of the Central and Eastern Europe freight and logistics market size, yet distance-based tolls and diesel volatility incentivize fleet electrification and LNG swaps along AFIR corridors. Early adopters enjoy 15-20% TCO savings, boosting the Central and Eastern Europe freight and logistics market for alternative-fuel trucks.

Air freight advances fastest at 4.44% CAGR as data-center timelines and pharma shipments require premium speed. Rail’s policy-driven upside is checked by wagon shortages, while Black Sea port upgrades increase sea route attractiveness for CBAM-affected metals. Danube emission caps raise inland waterway rates 15-25%, prompting mixed modal choices. NATO road and rail refurbishments trim civilian lead times by up to 25%, reinforcing cross-border supply-chain reliability. Intermodal mega-hubs spur a 20-30% uptick in rail utilization on the Baltic-Adriatic spine, deepening diversification within the Central and Eastern Europe freight and logistics market.

By End User Industry: Retail Omnichannel Outpaces Manufacturing

Wholesale and retail trade commanded 30.58% of the Central and Eastern Europe freight and logistics market in 2025 and is projected to grow at a CAGR of 3.12% through 2031, maintaining its lead due to omnichannel strategies focused on rapid delivery and urban warehousing. The segment continues to expand as retailers adopt automation, AMRs, and micro-fulfillment solutions. Manufacturing remains a key contributor, supported by nearshoring and gigafactory developments, while construction and agriculture benefit from infrastructure investments and improved cold-chain capabilities.

Defense procurement and data-center megaprojects sit within “Others,” now a double-digit contributor as militaries outsource storage and distribution to civilian partners. Scope 3 reduction pressures push shippers to prioritize providers with carbon-accounting platforms, nudging all end users toward greener services within the Central and Eastern Europe freight and logistics market.

By Courier, Express, and Parcel (CEP): Domestic Density, International Momentum

Domestic CEP retained 65.48% value in the Central and Eastern Europe freight and logistics market share, leveraging postal-network reach and rising e-grocery frequency. International parcels, expanding at 3.49% CAGR, profit from customs harmonization and marketplace fulfillment roll-outs that reduce border friction. Q-commerce apps lift urban parcel counts 150-180% in Serbian and Bulgarian tier-2 cities, compelling providers to convert retail ground floors into 200-500 m² dark stores.

Electric cargo bikes and small vans become mandatory in low-emission zones, aligning with AFIR charging deployment. Cybersecurity spend rises 40-60% as ransomware attacks spike, elevating insurance premiums yet solidifying consumer trust. Algorithmic route planning slashes empty mileage 18%, sustaining margins despite EUR 2-4 delivery price caps and strengthening the Central and Eastern Europe freight and logistics market’s urban last-mile leadership.

By Warehousing and Storage: Automation Upskills Commodity Space

Non-temperature-controlled sites covered 91.39% of Central and Eastern Europe freight and logistics market, but growth tilts toward temperature-controlled facilities at 2.70% CAGR as pharma and fresh-food e-commerce scale. Grade-A warehouses adopt ASRS and AMRs, cutting labor 40%, while solar roofs and smart HVAC secure 10-15% rent premiums for green-certified buildings. Defense mobility creates demand for high-security depots with biometric access and 24/7 surveillance.

Data-center contractors lease short-term staging near build sites, reinforcing specialization trends. Urban infill projects repurpose light industrial shells into micro-fulfillment nodes, expanding the Central and Eastern Europe freight and logistics industry footprint inside city cores without breaching zoning caps. Automation’s cost curve now suits 20,000 m² assets, half the former threshold, broadening uptake across secondary markets.

By Freight Forwarding Mode: Compliance Consulting Adds New Revenue

Sea and inland waterways held 50.09% of Central and Eastern Europe freight and logistics market, but air forwarding’s 3.86% CAGR shows shippers value speed for critical electronics and cold chain. CBAM shifts Turkish and Middle-Eastern steel via Constanța, Burgas, and Varna, reducing transport carbon by up to 30%. Freight forwarders monetize compliance by charging EUR 50,000-150,000 (USD 58,500-177,000) for supply-chain carbon audits and routing redesign.

Danube Stage-V retrofits push barge rates higher, moderating waterway competitiveness and advising blended rail-sea solutions. Digital control towers grant customers real-time visibility, and API connectivity trims paperwork costs. Cyber-security upgrades become gating criteria for shipper RFPs, integrating IT resilience into the Central and Eastern Europe freight and logistics market value proposition.

Geography Analysis

Poland commanded 32.72% of 2025 revenue, reinforcing the strength of the Poland freight and logistics market through its Baltic-Adriatic hub status and NATO funding that accelerates dual-use road and rail upgrades. Distance-based tolls lifted Polish SME carrier costs, but 450 EV charging points due by 2027 and EUR 2 billion (USD 2.36 billion) of data-center investments offset cost drag through higher-margin project logistics. The Central and Eastern Europe freight and logistics market size for Poland, therefore, remains resilient even under margin stress. Czech Republic and Romania follow; the former leverages proximate German demand and high-capacity rail, the latter capitalizes on Black Sea port volumes linked to CBAM trade shifts.

Bulgaria grows quickest at 3.24% CAGR through 2031, fueled by 30% capacity expansions at Burgas and Varna and e-commerce penetration in Plovdiv and Varna. Hungary emerges as a data-center node with 150 MW under construction, while Slovakia doubles down on automotive supply-chain nodes. Baltic states, although smaller, sit on NATO’s critical north-south corridor and receive above-average infrastructure subsidies that shorten lead times and enhance resilience. Western Balkan markets, Serbia, Albania, and North Macedonia, log fast parcel growth, installing 200 micro-fulfillment sites by 2027 from 50 in 2024.

Black Sea and Danube dynamics reshape routing as CBAM encourages shorter, lower-carbon legs, reinforcing Romanian and Bulgarian port relevance. Simultaneously, Baltic-Adriatic mega-hubs redefine Eurasian landbridge competitiveness by trimming transit 25-35%. Distance-based toll proliferation drives modal re-optimization, particularly among cross-border retailers importing fast-moving consumables. Collectively, these developments diversify revenue streams and consolidate the Central and Eastern Europe freight and logistics market as a strategic NATO-EU interface.

Competitive Landscape

The top 10 operators account for roughly 35-40% of sector revenue, indicating moderate concentration. DSV’s 2026 assimilation of DB Schenker’s regional assets creates scale leadership with EUR 150 million (EUR 175 million) synergy upside from shared depots and integrated IT. DHL allocated EUR 500 million (USD 590 million) to 200 micro-fulfillment sites, targeting tier-2 q-commerce, while PKP CARGO secures a EUR 200 million (USD 234 million) NATO rail services contract that locks in priority track access.

White-space opens for mid-caps specializing in CBAM carbon audits, data-center project logistics, and defense kit warehousing capabilities that traditional integrators lack in depth. AI-driven route optimization, adopted by GEODIS in early 2026, reduces Czech empty runs 18%, illustrating how tech provides a 10-15% cost edge. Rhenus and UPS expand AFIR-aligned LNG fleets and pharma cold-chain hubs, tapping emission-conscious shippers.

Cybersecurity emerges as a price-of-entry; insurers demand stringent protocols, disadvantaging under-invested rivals. Consolidation accelerates when toll expansion and retrofit mandates squeeze SME liquidity, likely raising the Central and Eastern Europe freight and logistics market concentration by 2-3 points by 2030.

Central and Eastern Europe Freight and Logistics Industry Leaders

DHL Group

DSV A/S (Including DB Schenker)

Kuehne+Nagel

United Parcel Service of America, Inc. (UPS)

Raben Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group expanded its partnership with Westwing for sustainable e-commerce logistics, including operations via its Poland logistics center.

- February 2026: FedEx opened a 3,700 m² Vilnius sorting hub to strengthen cross-border e-commerce handling across the Baltics.

- February 2026: DHL Supply Chain extended its integrated-logistics partnership with Volkswagen Slovakia for an additional five years.

- June 2025: DACHSER purchased Brummer Group to reinforce temperature-controlled food logistics across Austria and neighboring CEE states.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Central & Eastern Europe (CEE) freight and logistics market as all revenue earned from commercial movement, storage, and ancillary handling of goods across road, rail, air, inland waterway, and courier-express-parcel networks inside thirteen EU and accession economies stretching from Poland to Albania. According to Mordor Intelligence, this value reached USD 159.09 billion in 2025.

Scope exclusion: Passenger transport, private captive fleets, and hyper-local bike courier services sit outside this boundary.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

- Geography

- Albania

- Bulgaria

- Croatia

- Czech Republic

- Estonia

- Hungary

- Latvia

- Lithuania

- Poland

- Romania

- Slovak Republic

- Slovenia

- Rest of CEE

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed freight forwarders, 3PL executives, warehouse developers, and policy officers across Poland, Czechia, Romania, and the Baltics. These conversations validated truckload rate swings, cross-border dwell times, and e-commerce parcel volumes, filling gaps where public data lagged.

Desk Research

We first canvassed open datasets from Eurostat's structural business statistics, the World Bank's Logistics Performance Index, and UNCTAD port call records, which anchor historic turnover, throughput, and trade flows. Country transport ministries, such as Poland's GDDKiA and Romania's MTI, supply annual ton-km and warehouse stock additions, while the International Union of Railways publishes intermodal train-kilometer trends. Company 10-Ks and investor decks round out rate and volume signals. Subscription tools like D&B Hoovers and Dow Jones Factiva help us corroborate operator revenues and news on capacity additions. This list is illustrative; many other sources were tapped for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down build starts with national transport output and warehouse receipts, which are then re-mapped to our service taxonomy and adjusted for double counting. Select bottom-up sense checks, such as sampled average selling price times pallet moves at leading depots and lane-level truck counts, calibrate totals. Key model inputs include diesel price indices, retail e-sales growth, automotive export tonnage, rail intermodal share, and EU-funded corridor completions. We forecast through 2030 using multivariate regression supported by primary-expert consensus on GDP and modal shift assumptions, and we patch data holes with rolling three-year averages where micro-series are missing.

Data Validation & Update Cycle

Outputs pass anomaly scans against external trade, fuel, and leasing benchmarks before a second analyst review. Reports refresh yearly, with mid-cycle revisions when material events, such as new Schengen border rules, arise. A final pre-publication pass ensures clients receive the latest view.

Why Mordor's Central And Eastern Europe Freight & Logistics Baseline Earns Trust

Published estimates often diverge because firms choose different service baskets, currencies, and refresh rhythms.

Below we contrast our 2025 baseline with other widely cited figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 159.09 Bn (2025) | Mordor Intelligence | - |

| USD 121.91 Bn (2024) | Regional Consultancy A | Omits warehousing & CEP, narrower country list |

| €300 Bn (2024) | Trade Journal B | Blends real-estate asset values with freight turnover |

The comparison shows that when scope creep or omissions are stripped away, Mordor's disciplined mix of transparent inputs, regular refresh, and dual-path validation delivers a balanced, reproducible baseline decision-makers can rely on.

Key Questions Answered in the Report

How large is the Central and Eastern Europe freight and logistics market expected to become by 2031?

It is forecast to reach USD 189.40 billion by 2031, expanding at a 2.9% CAGR from 2026 to 2031.

Which logistics function is growing fastest across CEE?

Courier, express, and parcel services show the quickest trajectory with a 3.35% CAGR through 2031 thanks to quick-commerce penetration.

Why are NATO investments influencing civilian freight flows?

Dual-use road and rail upgrades funded for military mobility cut civilian border wait times up to 40%, improving network reliability for commercial carriers.

What are the principal challenges facing the industry?

Chronic driver shortages, border congestion linked to new EU travel systems, under-developed cold-chain infrastructure, and uneven Grade-A warehousing supply.

How will AFIR affect long-haul trucking costs?

Alternative-fuel corridors lower total cost of ownership 15-20% over five years for fleets switching to LNG, electric, or HVO trucks.

Which country is the fastest-growing CEE logistics market?

Bulgaria leads with a projected 3.24% CAGR to 2031, driven by Black Sea port expansion and robust q-commerce demand.

Page last updated on: