Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

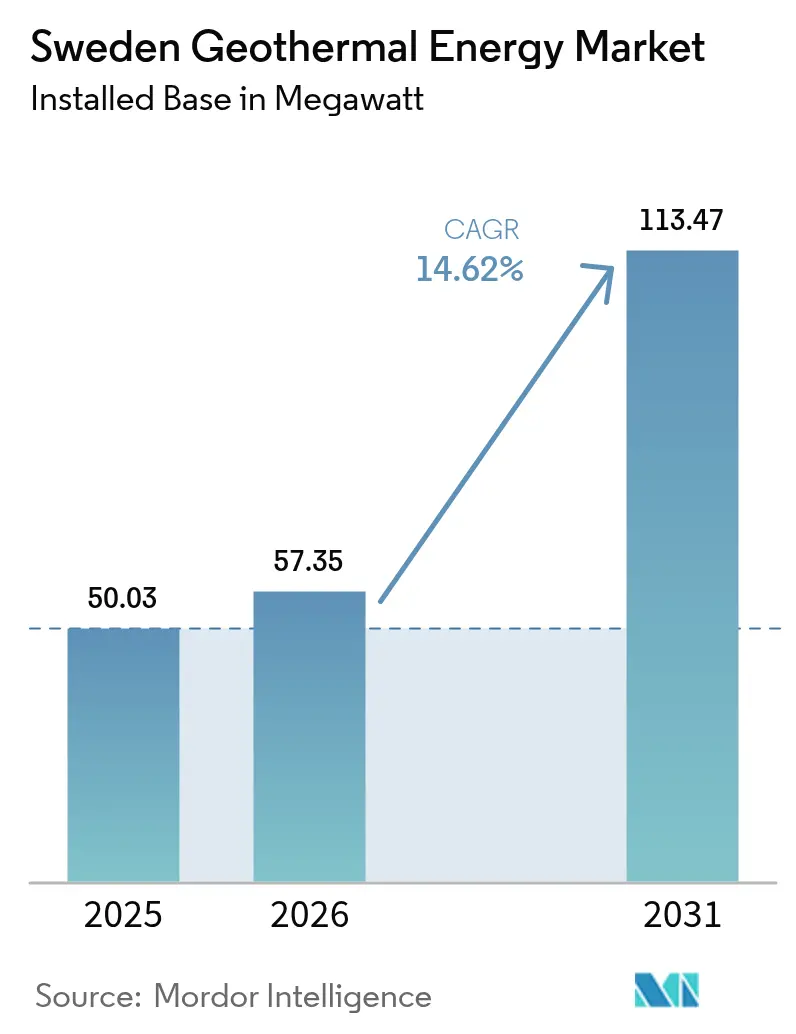

| Base Year Market Size (2025) | 50.03 megawatt |

| Market Volume (2026) | 57.35 megawatt |

| Market Volume (2031) | 113.47 megawatt |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Geothermal Energy Market Analysis by Mordor Intelligence

The Sweden Geothermal Energy Market size was valued at 50.03 megawatt in 2025 and estimated to grow from 57.35 megawatt in 2026 to reach 113.47 megawatt by 2031, at a CAGR of 14.62% during the forecast period (2026-2031).

Strong policy alignment with the 2045 net-zero target, rising fossil-fuel heating costs, and premium green-heat incentives converge to accelerate adoption across residential, commercial, and municipal segments. Ground-source heat pumps create an accessible entry point, while closed-loop and Enhanced Geothermal Systems (EGS) establish a pathway to deeper resources able to supply baseload thermal and, eventually, electric output. A maturing financing ecosystem, illustrated by Baseload Capital’s EUR 53 million raise, lowers perceived risk and signals growing institutional confidence. Meanwhile, public-sector procurement and corporate 24/7 renewable-heat power-purchase agreements (PPAs) add long-term revenue visibility that underpins capital-intensive drilling programs.

Key Report Takeaways

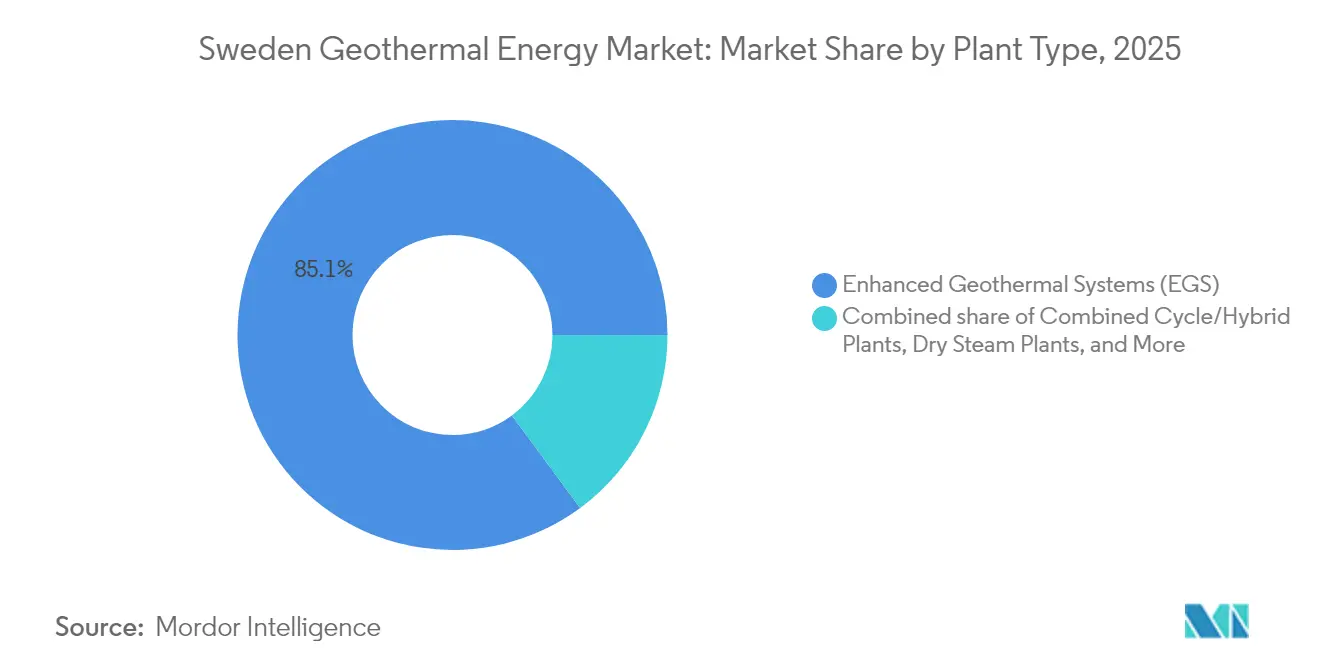

- By plant type, enhanced geothermal systems (EGS) led with 85.12% of geothermal energy market share in 2025; combined cycle/hybrid plants are projected to expand at a 24.35% CAGR through 2031.

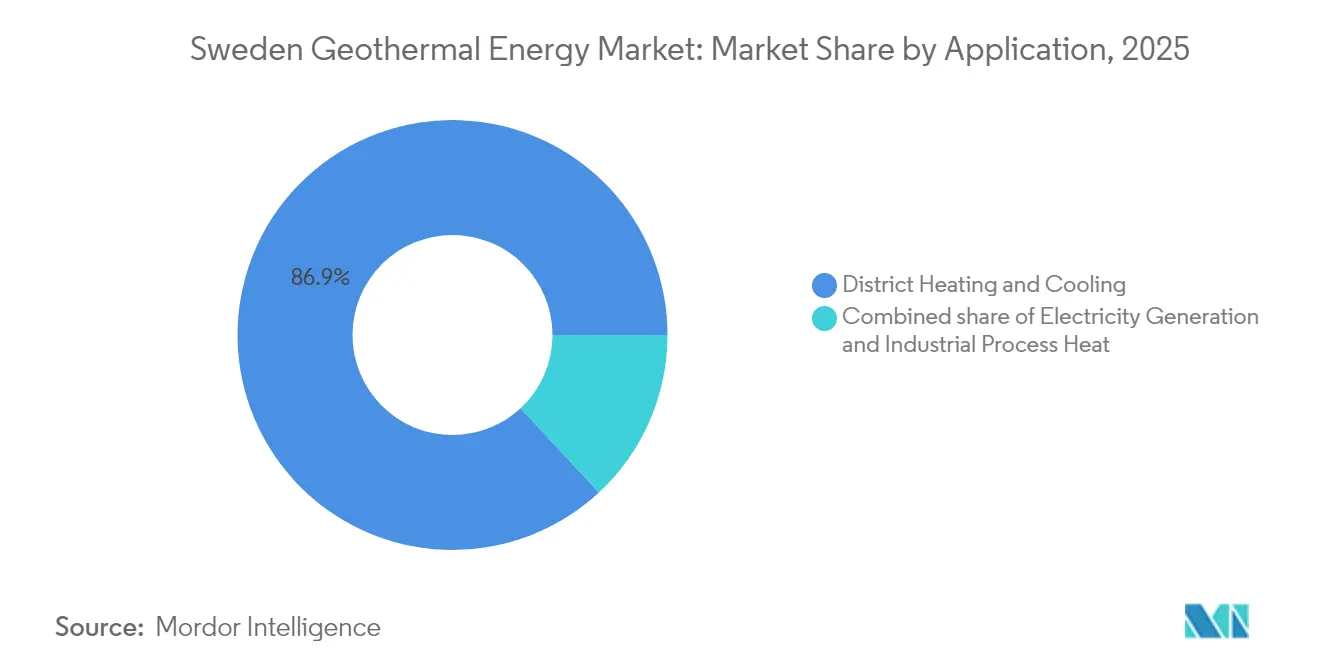

- By application, district heating and cooling captured 86.92% revenue share in 2025; electricity generation is forecast to advance at a 27.55% CAGR to 2031.

- Baseload Capital, Climeon, and LKAB together accounted for a major share of installed capacity within the geothermal energy market in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Geothermal Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding green-heat subsidies under Sweden's Climate Policy Framework | 2.8% | National, with higher uptake in southern municipalities | Medium term (2-4 years) |

| Stringent building-energy codes boosting ground-source heat-pump retrofits | 2.4% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Corporate 24/7 renewable-heat PPAs led by data-centre operators | 2.1% | Stockholm, Gothenburg, and industrial clusters | Medium term (2-4 years) |

| Rapid cost declines in closed-loop geothermal drilling rigs | 1.7% | National, with early adoption in Southern Sweden | Long term (≥ 4 years) |

| Repurposing idle mines for low-enthalpy geothermal fluid extraction | 1.5% | Northern Sweden mining regions | Long term (≥ 4 years) |

| District-heating decarbonisation mandates in ≥30 municipalities | 1.3% | Urban centers with existing district heating networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Green-Heat Subsidies Under Sweden's Climate Policy Framework

Enhanced investment grants of up to SEK 30,000 per installation, combined with the May 2025 increase in ROT tax deductions to 50% of labour costs, cut total out-of-pocket expenses for residential systems by nearly 40%.[1]Government Offices of Sweden, “Enhanced ROT Tax Deduction Rules,” regeringen.se Municipal schemes in Lund and Växjö complement national grants, rewarding district-heating companies that integrate shallow geothermal loops into new low-temperature grids. Tying eligibility to verifiable efficiency gains sharpens the focus on ground-source technologies, which deliver the required seasonal COP performance. The looming 2025 application deadline spurs near-term demand while embedding geothermal heat in Sweden’s longer-term decarbonisation roadmap.

Stringent Building-Energy Codes Boosting Ground-Source Heat-Pump Retrofits

Revised regulations mandate high efficiency in major renovations, effectively sidelining oil and gas boilers for most urban buildings. Single-family homes, which consume 35% of national heating energy, provide attractive drilling sites, while large commercial assets adopt integrated heating-cooling loops that maximise annual capacity factors. Because compliance is required within planned refurbishment cycles, installers benefit from a transparent three-to-five-year retrofit pipeline, stabilising order books and supporting workforce expansion. Performance-based rules allow architects to weigh competing low-carbon options, yet ground-source pumps often prevail on life-cycle cost.

Corporate 24/7 Renewable-Heat PPAs Led by Data-Centre Operators

Stockholm Data Parks and Multigrid sell recovered server-heat to municipal networks at EUR 0.03 per kWh, almost 55% below the average Swedish district-heat tariff in 2024. EcoDataCenter’s SEK 18 billion campus in Östersund pairs geothermal heating with food-grade greenhouse operations, locking in low operational costs and landmark Scope 1 emission cuts. These long-tenor PPAs underpin bankability for large geothermal loops and open the door for similar deals in steel, pulp, and chemical clusters seeking continuous renewable process heat.

Rapid Cost Declines in Closed-Loop Geothermal Drilling Rigs

Atlas Copco’s X-Air+ compressor range cuts fuel use 30% versus prior models, while HARDAB’s rod-handling rig lowers crew requirements to a single operator.[2]Atlas Copco, “X-Air+ Compressors for Geothermal Drilling,” atlascopco.com Closed-loop designs sidestep permeability risk, broadening the resource base into Sweden’s crystalline shield. Cost parity with gas boilers emerges by 2028 for mid-scale projects, catalysing adoption in municipalities lacking sedimentary formations. Localisation of rig manufacturing adds supply-chain resilience and turns Sweden into an export hub for Nordic-grade geothermal equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High exploratory-drilling CAPEX amid hard-bedrock conditions | -2.2% | National, particularly severe in central/northern regions | Short term (≤ 2 years) |

| Reservoir-temperature uncertainty outside Southern Sweden | -1.9% | Central and northern Sweden | Medium term (2-4 years) |

| Scarcity of specialised geothermal drilling crews | -1.6% | National, with acute shortages in remote areas | Short term (≤ 2 years) |

| Public concern over micro-seismicity near urban clusters | -1.0% | Stockholm, Gothenburg, and major urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Exploratory-Drilling CAPEX Amid Hard-Bedrock Conditions

The 3,702 m Lund deep well cost more than EUR 5.5 million yet yielded only 85 °C bottom-hole temperature, underscoring the cost risk in crystalline rock. Typical hard-rock costs of EUR 1,500 per metre dwarf the EUR 600 European average, squeezing smaller developers. Multi-well EGS designs compound budgets, prompting a pivot toward closed-loop or mine-water solutions that mute resource risk and curtail up-front capital intensity.

Reservoir-Temperature Uncertainty Outside Southern Sweden

Heat-flow gradients drop to 15 °C per kilometre across vast parts of central Sweden, versus 25 °C in Scania, complicating bankability models.[3]Geothermal Energy Journal, “Temperature Gradient Variability across the Fennoscandian Shield,” geothermal-energy-journal.springeropen.com Extensive geophysical surveys add months to project timelines, and lenders demand conservative production forecasts. Public-sector mapping campaigns promise incremental de-risking, yet until completed, developers lean on phased drilling and hybrid revenue streams, such as pairing shallow geothermal loops with solar thermal collectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plant Type: EGS Dominates Sweden's Geothermal Landscape

Enhanced Geothermal Systems (EGS) held 85.12% of installed capacity in 2025, making them Sweden’s clear front-runner. Their strength comes from the nation’s hard crystalline bedrock, which favors engineered reservoirs over traditional hydrothermal methods. Combined-cycle and hybrid plants are the rising stars, moving at a 24.35% CAGR to 2031 as operators pair geothermal wells with other renewables and thermal storage to smooth output. Binary-cycle units serve lower-temperature wells, while flash-steam projects remain rare because Sweden lacks the very hot resources they need. Closed-loop designs are starting to supplement EGS by removing fluid-circulation risks and opening new sites that once looked uneconomic.

EGS benefits from know-how built in Sweden’s mining and oil-and-gas industries. Work at the Äspö Hard Rock Laboratory, for example, refines hydraulic-fracturing techniques tailored to crystalline rock and adds real-time monitoring that keeps seismic risks in check. Developers also lean on digital controls to watch reservoir performance and adjust flows on the fly, cutting operating costs and environmental impacts. Growing interest in hybrid layouts, where a single plant feeds both the power grid and district-heating pipes, shows how Sweden aims to squeeze more value from every megawatt of heat.

By Application: District Heating Anchors Market Growth

District heating and cooling systems commanded 86.92% of geothermal use in 2025. Sweden’s vast municipal pipe networks already warm more than half of its city homes, so plugging in geothermal heat needs little new hardware. Electricity production is smaller today, but it is the fastest mover with a 27.55% CAGR through 2031 as better low-temperature turbines make power generation viable. Industrial process heat occupies a modest but important slice, especially among factories chasing carbon-cutting goals. Direct-use niches, such as greenhouses, fish farms, and seasonal storage, keep expanding as operators look for steady, long-run revenue.

District-heating projects give developers quick cash flow, while power plants promise future upside as technology costs fall. Mälarenergi’s 13 GWh underground thermal-storage retrofit highlights the scale of spending now going into district systems. More than 30 cities have set fossil-free heat targets, locking in demand for new geothermal loops. Because the pipes are already in the ground, project timelines shorten and financing risk drops. Interest is also rising in combined-heat-and-power setups that sell both kilowatts and hot water, diversifying income and boosting overall plant returns.

Geography Analysis

Southern counties, Scania, Halland, and Västra Götaland, account for 62.55% of installed geothermal capacity owing to higher temperature gradients, dense population, and extensive district-heat piping. Stockholm alone hosts 180,000 ground-source bores, underpinning a regional geothermal energy market valued at USD 154.74 million in 2026. Emerging closed-loop pilots in Blekinge tap 140 °C resources at 5 km depth, showcasing technical viability for domestic baseload.

Central Sweden, anchored by Uppsala and Örebro, exhibits a slower rollout because crystalline bedrock elevates drilling costs. Yet policy-backed energy-poverty programs fund 45 kW micro-loops for schools and elder-care homes, demonstrating social-equity benefits. Local universities add geothermal labs that shorten innovation cycles and create specialised talent, gradually lowering soft-cost premiums.

Northern provinces present unique mine-water potential. Kiruna’s decommissioned shafts hold 9 million m³ of 28 °C water, enough to cover 60% municipal heat load via high-lift pumps. LKAB’s SEK 31 billion decarbonisation plan aligns demand with supply, positioning the region for dual-purpose energy-and-storage hubs. Grid constraints are minimal, allowing excess summer solar to charge subterranean heat stores for winter recovery. Municipal authorities fast-track permits, keen to replace peat and oil boilers before 2030.

Competitive Landscape

Sweden’s geothermal energy market remains moderately fragmented, though visible consolidation has started. Baseload Capital’s equity round, ThinkGeoEnergy’s project-originations, and Ormat-SLB’s 2024 collaboration illustrate inbound capital and technology flow. Home-grown innovators such as Climeon supply Organic Rankine Cycle modules that turn low-grade heat streams into 150–300 kW electric blocks, creating a domestic supply chain alongside HARDAB rigs and Atlas Copco compressors.

Competitive intensity hinges on drilling efficiency, reservoir modelling, and integrated EPC delivery. Firms able to guarantee turnkey performance win municipal tenders that favour single-point accountability. Partnerships between utilities and equipment vendors proliferate: Göteborg Energi signed a framework agreement with HARDAB to swap ageing biomass with 50 MW of closed-loop geothermal by 2029, bundling maintenance into a 15-year service contract. Technology licensing further accelerates know-how diffusion; Swedish rig patents are now adopted in Iceland and the Baltics, raising export revenues while expanding economies of scale.

White-space persists in mine-water heat and seasonal thermal storage. Tektonik Nordic pioneers sand-filled pit reservoirs linked to 8 MW pump stations, while Thermia pilots trans-critical CO₂ heat pumps that raise outlet temperatures to 110 °C, letting district-heat operators abandon peak gas boilers. Intellectual-property barriers remain modest, so first movers focus on capturing the best sites and building long-term offtake contracts before subsidy tapering begins after 2028.

Sweden Geothermal Energy Industry Leaders

WSP Global Inc.

Climeon AB

Baseload Capital AB

MalmbergGruppen AB

Rototec AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kärnfull Next secured land for a small modular reactor cluster in Valdemarsvik, creating future synergies with geothermal district-heating loops.

- September 2024: Baseload Capital closed a EUR 53 million Series B round to accelerate geothermal deployments in Sweden and abroad.

- September 2024: ELIQUO Water Group acquired Malmberg Water AB, strengthening hydro-geothermal and water management capabilities.

- June 2024: Ormat and SLB signed a global partnership to integrate drilling and reservoir technology in geothermal projects.

Sweden Geothermal Energy Market Report Scope

The Sweden geothermal energy market report includes:

By Plant Type

| Dry Steam Plants |

| Flash Steam Plants |

| Binary Cycle Plants |

| Combined Cycle/Hybrid Plants |

| Enhanced Geothermal Systems (EGS) |

By Application

| Electricity Generation |

| District Heating and Cooling |

| Industrial Process Heat |

| By Plant Type | Dry Steam Plants |

| Flash Steam Plants | |

| Binary Cycle Plants | |

| Combined Cycle/Hybrid Plants | |

| Enhanced Geothermal Systems (EGS) | |

| By Application | Electricity Generation |

| District Heating and Cooling | |

| Industrial Process Heat |

Key Questions Answered in the Report

What is the current size of Sweden’s geothermal energy market?

Sweden’s geothermal capacity stands at 57.35 MW in 2026, reflecting the sector’s early-stage but fast-growing status.

How fast is the market expected to grow?

Installed capacity is projected to reach 113.47 MW by 2031, equal to a robust 14.62% compound annual growth rate during the forecast period (2026-2031).

Which geothermal plant type is most common in Sweden today?

Enhanced Geothermal Systems (EGS) dominate with 85.12% market share.

How do government incentives affect project economics?

Grants of up to SEK 30,000 per installation and a 50% ROT tax deduction on labour costs can trim residential system payback periods by nearly 40%.

Which Swedish regions offer the greatest near-term opportunity?

Southern counties such as Scania and Västra Götaland lead deployment thanks to higher geothermal gradients, dense district-heating networks, and easier drilling conditions.

What are the main hurdles facing developers?

High exploratory-drilling CAPEX in hard bedrock and subsurface temperature uncertainty outside the south slow project financing and can delay time to revenue.

Page last updated on: