Surface Acoustic Wave Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

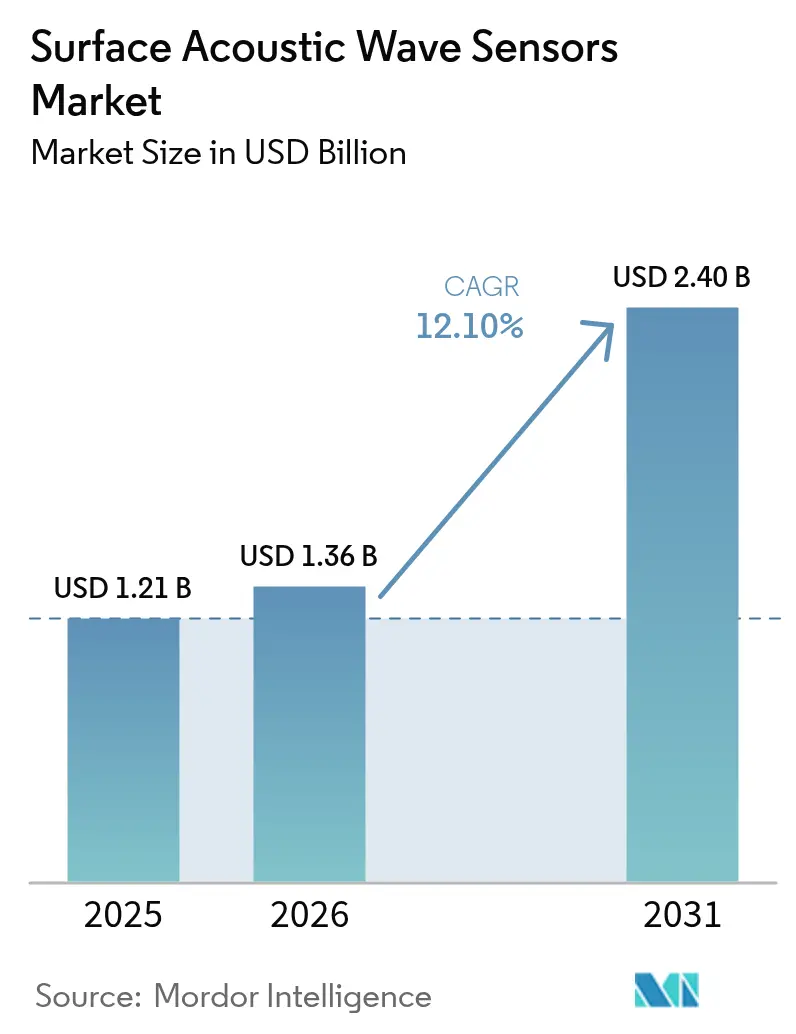

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 2.4 Billion |

| Growth Rate (2026 - 2031) | 12.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surface Acoustic Wave Sensors Market Analysis by Mordor Intelligence

The Surface Acoustic Wave Sensors Market size was valued at USD 1.21 billion in 2025 and estimated to grow from USD 1.36 billion in 2026 to reach USD 2.4 billion by 2031, at a CAGR of 12.10% during the forecast period (2026-2031). This brisk trajectory is driven by the technology’s low-power wireless architecture, the rollout of 5G infrastructure, and the rising demand for robust sensing solutions within electric vehicles (EVs). Battery-free operation enables permanent installation in rotating or sealed assemblies, reducing maintenance costs for aerospace engines and industrial turbines. Consumer electronics manufacturers continue to specify SAW filters to preserve signal integrity in compact form factors, while policymakers in major auto markets now mandate direct tire-pressure monitoring systems that favor high-temperature SAW devices. Established quartz and lithium tantalate supply chains provide tier-one component manufacturers with scale economies, enabling them to maintain competitive average selling prices despite substrate innovations. At the same time, niche suppliers that master langasite processing secure premium margins in ultra-high-temperature aerospace programs.[1]Boeing, “Innovation and Technology Demonstrators,” boeing.com

Key Report Takeaways

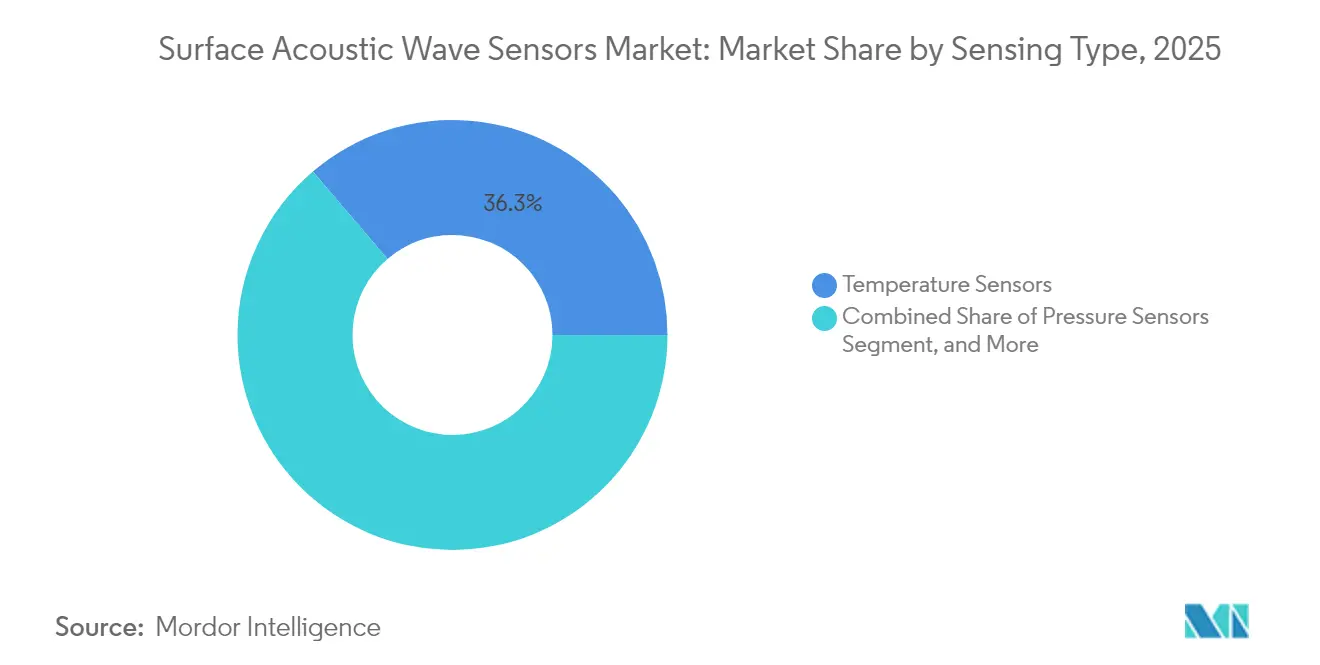

- By sensing type, temperature devices held 36.25% of the surface acoustic wave sensors market share in 2025, whereas pressure sensors are projected to expand at a 13.95% CAGR through 2031.

- By end-user, consumer electronics dominated the surface acoustic wave sensors market with a 32.15% revenue share in 2025, while automotive applications are projected to grow at a 13.65% CAGR to 2031.

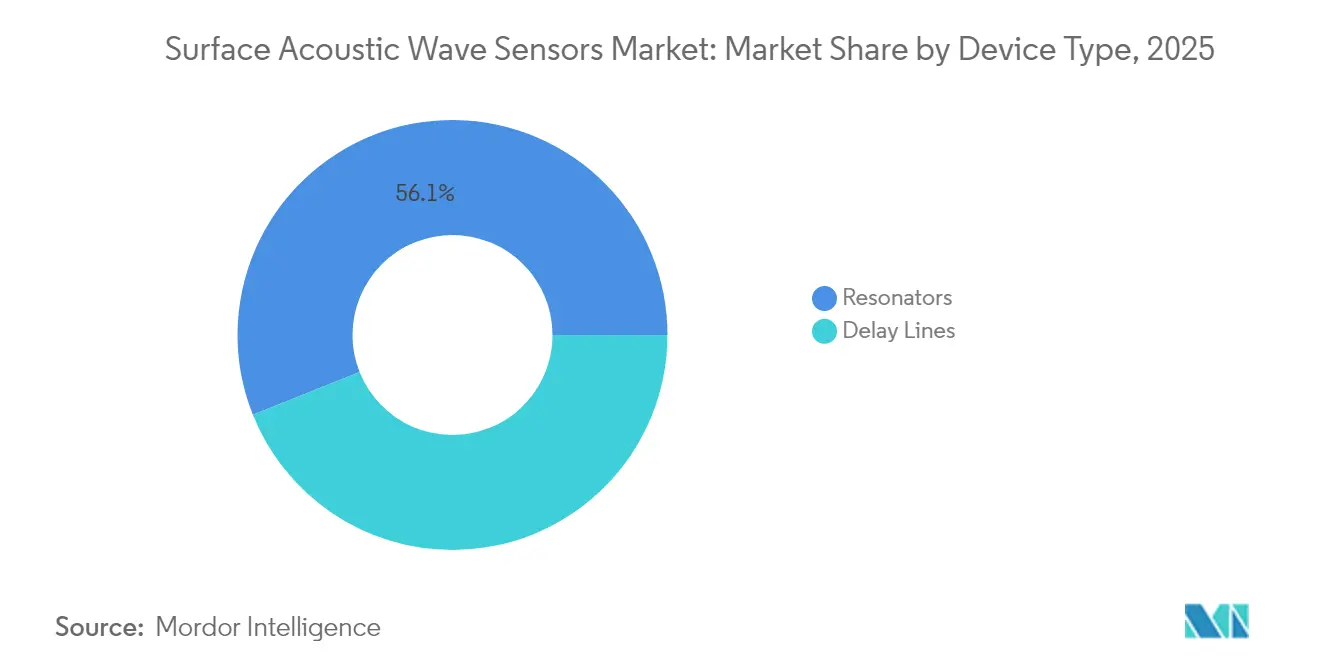

- By device type, resonators accounted for 56.05% of the 2025 surface acoustic wave sensor market size, while delay lines are the fastest-growing segment at a 12.82% CAGR.

- By material substrate, quartz wafers accounted for a 36.85% share of the surface acoustic wave sensors market in 2025, and langasite substrates are forecast to grow at a 13.42% CAGR over the period.

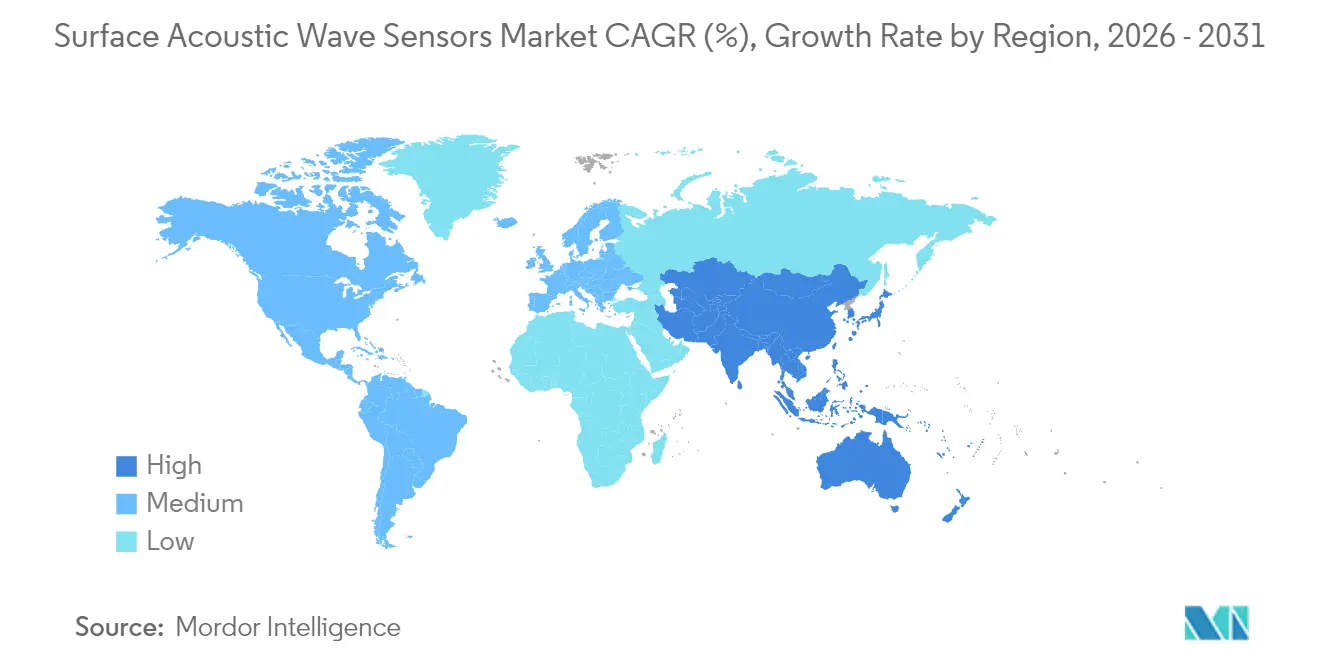

- By geography, North America led the surface acoustic wave sensors market with a 36.95% share in 2025, whereas the Asia Pacific region is expected to record the fastest regional CAGR of 13.24% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surface Acoustic Wave Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wireless and Passive Sensor Architecture Enabling Battery-less Deployment | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Low Manufacturing Cost Through Established Piezoelectric Substrate Supply Chains | +1.8% | Asia Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Automotive TPMS and EV Thermal Management Demand for High-Temperature SAW Sensors | +2.3% | Global, with early gains in China, Germany, United States | Medium term (2-4 years) |

| Expansion of 5G and IoT Infrastructure Requiring Miniaturized, High-Frequency Sensing Solutions | +2.7% | Asia Pacific and North America | Short term (≤ 2 years) |

| Adoption of Ultra-High-Temperature Langasite SAW Sensors in Aerospace Turbine Monitoring | +1.4% | North America and Europe | Long term (≥ 4 years) |

| Emergence of Portable SAW Biosensors for Rapid Point-of-Care Diagnostics | +1.6% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wireless and Passive Sensor Architecture Enabling Battery-less Deployment

Passive SAW tags harvest interrogation energy, eliminating the need for batteries that constrain lifetime and add weight. This feature slashes the total cost of ownership for industrial users by up to 60% as scheduled cell replacement and hazardous-area access are no longer required. Rotating turbine disks, aircraft engine blades, and high-voltage busbars can now host embedded sensors that operate for decades without power interruptions. Radio read ranges approaching several meters simplify data acquisition and cut cabling costs in retrofits. Because the sensor does not radiate continuously, spectrum congestion and electromagnetic compatibility issues are minimal, which eases compliance approvals for large IoT networks.

Low Manufacturing Cost Through Established Piezoelectric Substrate Supply Chains

Quartz, lithium tantalate, and lithium niobate crystal growth matured in the frequency-control sector, so 150 mm wafers with 1 µm thickness tolerance now cost below USD 2 in high-volume supply agreements.[2]TDK Corporation, “TDK Announces Strategic Investment in Advanced Sensor Technologies,” tdk.com Front-end lines already optimized for SAW filters in smartphones can be retooled to add sensor patterns without incurring heavy capital expenditures, thereby pushing gross margins higher for vertically integrated producers. Japanese foundries deploy full automation, which lifts yields above 95%, a decisive factor for price-sensitive automotive programs shipping millions of units each year. As a result, SAW sensors penetrate mid-tier consumer devices that previously relied on discrete MEMS parts.

Automotive TPMS and EV Thermal Management Demand for High-Temperature SAW Sensors

Direct TPMS mandates in vehicles registered after 2024 create a captive channel for SAW devices that can withstand rim temperatures and centrifugal stresses over the product's lifetime.[3]Continental AG, “Continental Develops Next-Generation Automotive Sensors,” continental.com In parallel, battery-electric platforms operate at near 800 V, which elevates inverter and pack temperatures above 150 °C. Quartz-based sensors remain accurate within ±1 °C from –40 °C to 200 °C, thereby avoiding thermal drift that can degrade lithium-ion health. Passive interrogation sidesteps wiring through rotating wheels or sealed packs, simplifying harness design. Suppliers able to certify devices under ISO 26262 reach design-win decisions faster within automaker safety workflows.

Expansion of 5G and IoT Infrastructure Requiring Miniaturized, High-Frequency Sensing Solutions

Millimeter-wave bands require frequency filters with quality factors exceeding 10,000. SAW resonators achieve an insertion loss of under 1 dB up to 6 GHz, outperforming BAW in low-power handheld devices. Small-outline packages sized below 1 cm³ embed both sensing and trimming networks, which fit space-constrained IoT nodes. Telecom carriers demand stability from –40 °C to 125 °C to keep base stations running in harsh climates, and SAW devices meet this specification without external compensation. The concurrent boom of connected edge devices multiplies unit volumes, cementing economies of scale for wafer fabs in Japan, Taiwan, and soon China.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compatibility and Installation Challenges in Existing Industrial Networks | -1.9% | Global, with concentration in mature industrial regions | Short term (≤ 2 years) |

| Performance Limitations of SAW Devices in Liquid-Phase Sensing Environments | -1.3% | Global, particularly in chemical and pharmaceutical industries | Medium term (2-4 years) |

| Intensifying Competition from Bulk Acoustic Wave and MEMS Sensors at >3 GHz Bands | -2.1% | Asia Pacific and North America | Medium term (2-4 years) |

| Supply Risk of Specialty Piezoelectric Materials amid Geopolitical Constraints | -1.7% | Global, with concentration in defense and aerospace applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compatibility and Installation Challenges in Existing Industrial Networks

Factory control systems built on legacy fieldbus or proprietary RF protocols often lack gateways that recognize SAW tag modulation schemes. Retrofitting lines can require shutdowns costing millions per day, which dissuades plant managers. Frequency overlaps with RFID create certification hurdles that lengthen commissioning schedules. Integrators sometimes add Honeywell-branded bridges that translate sensor IDs to PLC codes, but the extra hardware raises project budgets by 25–30%.[4]Honeywell International, “Honeywell Industrial Sensor Integration Solutions,” honeywell.com Skills shortages in radio network planning compound the hesitation, stalling adoption in otherwise attractive brownfield plants.

Performance Limitations of SAW Devices in Liquid-Phase Sensing Environments

Acoustic waves lose energy through viscous damping when sensors are in contact with water or chemicals, reducing sensitivity by up to 40% compared to gas-phase performance. Protective parylene or SiC coatings add cost and can alter frequency responses, making repeat calibration necessary in pharmaceutical tanks. Fouling by biofilms or suspended solids shortens maintenance intervals, eroding the passive-lifetime advantage. Until waveguide encapsulation methods mature, MEMS capacitive or optical sensors remain the preferred choice for critical liquid concentration monitoring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensing Type: Temperature Dominance Faces Pressure Challenge

Temperature devices generated 36.25% of the 2025 surface acoustic wave sensors market size, reflecting the widespread need for precise thermal tracking in process plants and HVAC installations. Their ability to measure wide ranges without drift secures designs for EV battery modules, industrial furnaces, and data center cooling loops. Pressure sensors are growing at a faster rate, benefiting from global TPMS legislation and the aerospace trend toward weight reduction through wireless tire and brake sensing. SAW gas-phase chemical sensors capture early contracts in environmental stations that must detect ppm-level emissions. Humidity and mass devices serve smart-building controls and semiconductor deposition lines, forming steady but smaller revenue pools.

Temperature sensors serve as the benchmark for material innovation; quartz resonates stably across ambient temperature swings, while langasite versions enable turbine exhaust placement. Competitive differentiation hinges on packaging metal-ceramic hermetic seals that provide decades of protection against steam or corrosives. Pressure variants leverage identical wafer processes but adopt rugged cavities and diaphragms, letting foundries amortize tooling across product families. As automotive volumes climb, price erosion will test newcomers lacking scale. Nevertheless, the mandate wave keeps the segment on a double-digit growth curve, narrowing the lead that temperature devices currently hold.

By End-User Industry: Consumer Electronics Leadership Challenged by Automotive Growth

Consumer electronics accounted for 32.15% of the 2025 surface acoustic wave sensors market share thanks to their entrenched role as front-end filters in smartphones, tablets, and wearables. Flagship handset vendors now integrate over 25 SAW or SAW-hybrid filters per device to isolate 5G sub-6 GHz bands while conserving battery life. Yet, the automotive segment advances at a 13.65% CAGR, driven by electrification, direct TPMS mandates, and the shift to redundant safety architectures that favor discrete passive sensors. Aerospace and defense buyers pay premiums for radiation-tolerant langasite parts that stay operational above 1000 °C in hypersonic propulsion tests.

Healthcare interest is growing as point-of-care diagnostics transition from centralized labs to clinics. SAW biosensors offer label-free detection within minutes, capturing attention during pandemic-preparedness drills. Industrial users adopt SAW torque and vibration tags for predictive maintenance programs that align with Industry 4.0 roadmaps. Cross-industry diversity smooths revenue cycles, but tier-one suppliers must tailor qualification plans to each vertical’s certification code, from ISO 26262 in vehicles to FAA FAR-25 in aviation.

By Device Type: Resonators Maintain Edge Despite Delay Line Growth

Resonators held 56.05% of the 2025 surface acoustic wave sensors market size because frequency-stabilized references remain essential in every RF architecture. 5G macro-cells require dozens of high-Q resonators to manage phase noise budgets and meet spectral-mask rules, which keeps demand high even as handset builds fluctuate. Delay lines follow at a lower volume but climb at a 12.82% CAGR due to adoption in short-range radar, gesture-recognition modules, and ultrasonic flaw detectors. Their ability to encode precise time-of-flight data in compact footprints underpins emerging driver-monitoring systems and automated warehouse robots.

Resonators compete primarily on phase noise and aging drift; suppliers utilize electrode-aperture optimization and temperature-compensation algorithms to minimize parts-per-billion deviations. Delay line vendors focus on low insertion loss across wide bandwidths to support FMCW radar chirps. Packaging is moving toward system-in-package offerings that mount multiple SAW elements on a common ceramic substrate to reduce assembly steps. This convergence promises to blur the historic line between sensor and filter, opening hybrid revenue streams for device makers positioned in both camps.

By Material Substrate: Quartz Dominance Challenged by Langasite Innovation

Quartz generated 36.85% of the 2025 surface acoustic wave sensors market share due to its widespread use in growth, slicing, and lapping processes across global fabs. Wafer yields exceed 95%, and long-term aging remains below 10 ppm per year, which suits mission-critical clocks. Langasite, however, expands at a 13.42% CAGR as jet-engine and space-propulsion programs demand sensors that can survive beyond 1000 °C without undergoing phase transitions. Lithium tantalate and niobate secure mid-volume niches where coupling efficiency trumps cost, such as in high-center-frequency biosensors that must detect single-digit colony counts.

Hybrid substrates stack thin lithium niobate films on quartz carriers, combining coupling gains with thermal stability. While manufacturing complexity rises, system-level savings emerge by trimming external compensation circuits. Foundries that already deposit epitaxial piezo layers for RF filters pivot seamlessly into the sensor arena, consolidating procurement. End-users weigh price against survivability; commercial telecom picks quartz, whereas turbine OEMs commit to langasite and accept the premium.

Geography Analysis

North America retained a 36.95% share of the surface acoustic wave sensors market in 2025, anchored by defense spending that values radiation resistance and battery-free operation in avionics and missile guidance. Federal research grants under SBIR streamline technology maturation, while long FAA certification cycles protect incumbents once type approval is reached. The region’s mature semiconductor base, primarily located in Arizona and Texas, enables rapid design iterations and tight quality control loops. Leading primes such as Boeing increasingly specify passive SAW tags for engine-core instrumentation because they eliminate slip rings inside rotating assemblies.

The Asia Pacific is advancing at a 13.24% CAGR due to 5G rollouts and the relocation of automotive electronics lines to China and South Korea. Beijing’s “Made in China 2025” drive channels subsidies into local wafer fabs that now ship quartz blanks rivaling those of Japan in quality. South Korea leverages its handset ecosystem to absorb SAW filters in every premium smartphone. Japanese majors maintain an edge in substrate R&D and hold design-in positions at tier-one automakers, such as Toyota, but price pressures from Chinese firms narrow their margins. India begins installing SAW-based smart meters in urban utilities, albeit from a low base.

Europe relies on its auto and industrial automation clusters to grow demand at a steady mid-single-digit pace. Germany’s EV build-out needs pack-level temperature sensors rated beyond 150 °C, while France’s nuclear fleet orders radiation-tolerant devices for reactor monitoring. Regulatory frameworks such as UNECE R141 and EU battery directives indirectly boost SAW uptake by tightening safety specifications. Aerospace programs at Airbus and Rolls-Royce evaluate langasite sensors for blade-tip clearance measurement, opening future opportunities despite the region’s cautious qualification ethos.

Regulatory Landscape

Wireless SAW sensors and tags generally follow regional radio rules for unlicensed/ISM spectrum. As a result, product compliance is often assessed against ETSI radio equipment standards (for example, EN 300 220/330/440 families) in Europe and Federal Communications Commission (FCC) requirements in the United States, with design constraints driven by band-specific power and bandwidth limits (including common sub-GHz allocations around 434 MHz, 868 MHz, and 915 MHz, and 2.4 GHz). In the United States, the National Telecommunications and Information Administration (NTIA) flagged receiver interference immunity concerns in August 2025, reinforcing focus on coexistence performance for RF systems that can include SAW-based components.

On the component standardization side, IEC Technical Committee TC 49 publishes test and quality frameworks used across global supply chains for piezoelectric and acoustic-wave devices. Key anchors include IEC 60747-14-11:2021 for semiconductor sensors (including SAW-based integrated sensors), IEC 63041-2:2017 for piezoelectric chemical/biochemical sensors, and IEC 60862-1:2015 as the generic specification for SAW filters, which received a corrigendum in March 2026. For suppliers serving automotive and communications programs, aligning device qualification, reliability testing, and documentation to these IEC specifications supports cross-region acceptance and can reduce re-qualification work across OEM platforms.

Value Chain Analysis

The value chain begins with piezoelectric material production and wafer preparation, using quartz and other piezoelectric substrates (lithium tantalate, lithium niobate, and langasite for extreme-temperature use). Device design follows, along with photolithography and metallization of interdigital transducers, wafer-level testing, and packaging, which is often hermetic metal-ceramic formats for harsh environments. High-volume manufacturing lines originally optimized for SAW RF components act as an upstream enabler for scaling SAW sensors, while specialty boule growth and processing capability becomes a differentiator for langasite-based devices.

Downstream, SAW sensor vendors and module houses supply tier-one integrators and OEMs across automotive (including TPMS and EV thermal monitoring), consumer electronics RF front ends, industrial automation, and aerospace and defense. Adoption depends on application engineering, including antenna design, reader or interrogator tuning, and network integration, followed by compliance testing for RF operation. From there, the market moves through distribution either directly to large OEMs or via electronics distributors and solution partners. Integration and qualification steps, such as automotive functional safety workflows and aerospace certification expectations, can extend time-to-revenue, increasing the role of design-in support, reference designs, and calibrated reader ecosystems in securing program wins.

Competitive Landscape

The surface acoustic wave sensors market shows moderate fragmentation. TDK Electronics, Murata Manufacturing, and Skyworks Solutions leverage vertically integrated quartz and lithium tantalate supply chains, which anchor pricing and secure pricing leverage in high-volume telecom orders. They reinforce the moat by filing patents for temperature-compensated topologies and by co-designing ASICs that simplify user calibration. Honeywell directs resources toward aerospace and industrial niches where qualification hurdles discourage fast followers and where life-cycle contracts exceed two decades.

Mid-tier firms, such as CTS Corporation and Pro-Micron, carve out territories in automotive TPMS and factory automation by partnering with regional tier-one companies and offering application-specific packaging. SENSeOR and Transense Technologies focus on extreme-temperature and torque-sensing use cases, earning premium unit prices despite lower annual volumes. Entry barriers for new players are tightening as MEMS vendors move up in frequency and as foundries raise minimum wafer-start commitments, although startups that master langasite boule growth can still disrupt the ultra-high-temperature segment. The rising wave of system-in-package adoption favors incumbents that own both substrate and flip-chip assembly lines, further consolidating influence over bill-of-material decisions across the supply chain.

Surface Acoustic Wave Sensors Industry Leaders

TDK Electronics AG

Murata Manufacturing Co., Ltd.

Honeywell International Inc.

API Technologies Corp.

Vectron International (Microchip Technology Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In the near term, whitespace exists in battery-free sensing deployments where cabling and maintenance access drive lifecycle cost, particularly for rotating machinery and sealed or high-temperature assemblies. Demand pull is already visible in automotive safety requirements and EV thermal management use cases. The substrate roadmap also supports expansion into harsher environments, with langasite-based SAW devices positioned for ultra-high-temperature turbine monitoring. This aligns with supplier investments such as TDKs announced USD 150 million commitment in September 2025 to add langasite crystal furnace capacity in Japan. As automotive volumes expand, qualification-ready, application-specific packaging, including rugged pressure devices for TPMS and stable temperature devices for packs and inverters, creates room for suppliers that pair sensor elements with integrated calibration and reader interoperability.

Technology roadmapping and research activity are also pointing to adjacent opportunity areas beyond classic RF filtering. The 2026 Guided Elastic Waves Roadmap, released in March 2026, broadened the discussion from standalone SAW devices to a wider guided elastic wave architecture spanning industrial sensing, life sciences, and advanced physics domains. That direction supports vendor R and D prioritization in miniaturization, integration, and extreme-environment reliability. Research published in 2026 also benchmarked passive wireless SAW sensors and highlighted clustering around bands such as 434 MHz for harsh-environment operation, while flexible SAW sensor developments, reviewed in 2026, enabled conformal sensing formats for wearables and structural health monitoring where rigid packages constrain adoption. These evidence points translate into product opportunities around standardized interrogator interfaces, robust coatings and packaging for new media exposures, and hybrid modules that combine sensing with RF front-end performance needs in compact IoT nodes.

Recent Industry Developments

- March 2026: The International Electrotechnical Commission issued a corrigendum to IEC 60862-1:2015, the generic specification for surface acoustic wave (SAW) filters, tightening the reference baseline used by global qualification and test programs. This supports more consistent conformance for suppliers that reuse SAW filter process platforms for sensor-grade devices and documentation across multi-region customer audits.

- September 2025: Honeywell introduced new sensing technology positioned to strengthen semiconductor manufacturing processes, extending its industrial sensing portfolio used in high-value fabs. This reinforcement of demand for robust, high-reliability sensing and process-control architectures intersects with SAW-enabled platforms in harsh and interference-sensitive environments.

- November 2024: TDK Electronics AG highlighted Acoustic Data Link (ADL) work using piezo transducers to transmit energy and sensor data through metal structures, with commercial partners testing the approach for pressure and leakage detection. This expands the design space for battery-free sensing in sealed assets where RF propagation is constrained, complementing passive SAW architectures used in industrial and aerospace installations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from surface acoustic wave (SAW) sensors that convert a physical or chemical change into a measurable signal, and that are sold into end-use industries such as automotive, industrial, and electronics across major regions.

Scope exclusions: We exclude non-SAW acoustic technologies (for example, bulk acoustic wave devices) and general sensing modules where the SAW element is not the primary sensing component.

Segmentation Overview

- By Sensing Type

- Pressure Sensors

- Torque Sensors

- Temperature Sensors

- Humidity Sensors

- Chemical Sensors

- Mass Sensors

- Other Sensors

- By End-User Industry

- Automotive

- Aerospace and Defense

- Consumer Electronics

- Healthcare

- Industrial

- Other End-User Industries

- By Device Type

- Resonators

- Delay Lines

- By Material Substrate

- Quartz

- Lithium Tantalate

- Lithium Niobate

- Langasite

- Other Materials

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the first market structure and to keep units, pricing logic, and end-use adoption signals consistent. We reviewed public sources such as US Census trade data, UN Comtrade, and national statistics portals, and we then checked technical references like IEEE publications and other peer-reviewed journals on SAW device performance limits.

To connect the technical picture to demand, we also relied on company filings, investor presentations, press releases, and association material from electronics and automotive ecosystems. A paid subscription for company financials and another for patent coverage were used selectively to sanity-check product focus, shipment direction, and R and D intensity without forcing the model to any single source. This list is not exhaustive, and other public references were used throughout the study for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work centered on interviews and structured surveys with SAW component participants and downstream users, so ASP ranges and adoption timing could be verified in plain terms. We spoke with product, sourcing, engineering, and operations roles, and we kept the coverage spread across Americas, EMEA, and APAC to reflect regional manufacturing concentration and end-market demand signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 52% |

| Mid tier: 42% | Functional/Unit leaders: 38% | EMEA: 30% |

| Smaller Players: 19% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where electronics and sensor demand signals are reconstructed into a SAW-appropriate demand pool using adoption rates by end use, and then converted into value using realistic average selling price (ASP) bands. The totals are cross-checked with selective bottom-up approximations, such as sampled supplier revenue splits, typical ASP by device type (resonators versus delay lines), and volume proxies tied to high-use applications like automotive sensing.

Inputs that mattered in the model included penetration of wireless and passive sensing in harsh environments, EV and broader automotive sensor content growth, 5G and RF front-end related pull for SAW components, and substrate and material availability (for example, quartz and lithium tantalate). We also incorporated qualification-cycle timing that can slow or accelerate design-ins. Where the bottom-up cross-check showed gaps, we filled missing pieces through conservative interpolation using adjacent application shares, then validated again through follow-up calls.

Forecasting was mainly done with scenario analysis supported by simple trend smoothing on the strongest drivers, because adoption follows design cycles rather than only GDP-like indicators. Assumptions on ASP movement and mix shift were reviewed with interviewees and applied consistently across regions before the final numbers were locked.

Data Validation & Update Cycle

Each model output was checked against independent signals, including application-level adoption ranges, implied ASP bands, and regional manufacturing intensity, and then reviewed for large jumps that could not be explained by the stated drivers. If a variance looked unusual, we traced it back to the input and re-contacted respondents when clarification was needed.

A multi-step analyst review was followed before sign-off so calculation errors, unit mismatches, and double counting risks could be removed early. Reports are refreshed annually, and interim updates are made when material events change demand, supply, or pricing. Before delivery, we run a final pass to ensure the latest public developments and validated assumptions are reflected.

Mordor Intelligence's Surface Acoustic Wave Sensors Market Size Compared Against Other Published Estimates

Published market sizes for SAW sensors often differ because scope and counting rules are not the same, even when the label sounds identical. Differences typically come from what is included as a SAW sensor, how device types are treated, and how pricing and currency timing are handled.

Some estimates roll SAW sensors together with adjacent acoustic components or use broader module-level revenue that captures more than the sensing function. In Mordor Intelligence sizing, only SAW sensor revenues are counted, and categories like non-SAW acoustic technologies and general modules are kept out unless the SAW sensing element is the clear, primary value driver.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.21 B (2025) | |

| Regional Consultancy A | USD 1.26 B (2025) | Uses a slightly broader inclusion of SAW-related components and applies higher near-term pricing in automotive-heavy demand mixes, which lifts the 2025 value even with a similar growth direction. |

| Industry Publisher B | USD 2.69 B (2025) | Appears to bundle SAW sensors with wider device and configuration groupings at the module level, which can introduce double counting across applications and inflate revenue captured under the SAW label. |

The spread in the table is mainly explained by scope control and how value is assigned to the SAW element versus a broader module. By keeping unit economics tied to device type and validating adoption assumptions through primary checks, our estimate stays traceable to a repeatable set of drivers rather than a catch-all component bucket.

Key Questions Answered in the Report

What revenue figure is forecast for the surface acoustic wave sensors market by 2031?

The market is projected to reach USD 2.4 billion in 2031 based on a 12.10% CAGR during the forecast period (2026-2031).

Which sensing type currently leads in unit demand?

Temperature devices command 36.25% share, owing to widespread use in industrial and HVAC systems.

Why are SAW sensors favored in direct TPMS?

They tolerate rim temperatures, operate without batteries, and comply with new mandates for continuous tire-pressure reporting.

How fast is the Asia Pacific region growing?

Asia Pacific is on a 13.24% CAGR path, propelled by 5G infrastructure and expanding automotive electronics capacity.

Which substrate is gaining traction for ultra-high-temperature applications?

Langasite is expanding at 13.42% CAGR because it withstands temperatures above 1000 °C, making it suitable for turbine monitoring.

What level of market concentration characterizes this sector?

With the top five vendors holding roughly 55% of sales, the landscape is moderately consolidated.

Page last updated on: