Supercritical Fluid Chromatography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

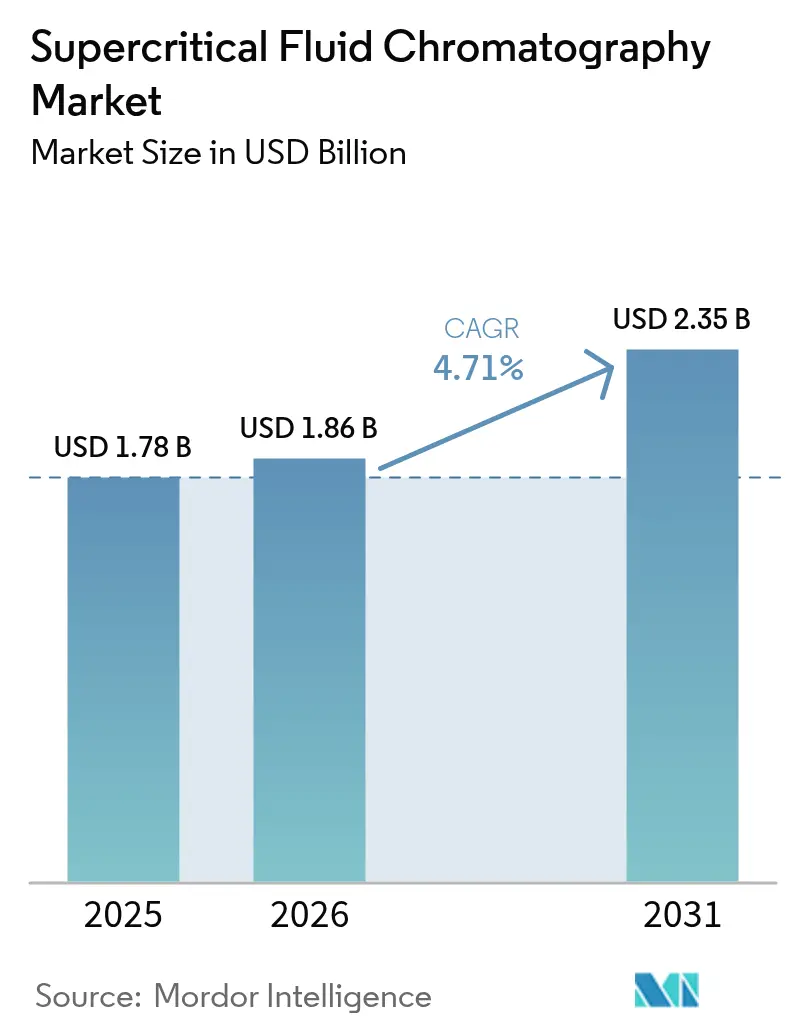

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supercritical Fluid Chromatography Market Analysis by Mordor Intelligence

Supercritical fluid chromatography market size in 2026 is estimated at USD 1.86 billion, growing from 2025 value of USD 1.78 billion with 2031 projections showing USD 2.35 billion, growing at 4.71% CAGR over 2026-2031. Rising green-chemistry mandates, widening pharmaceutical adoption for chiral separations, and broader use in lipidomics and cannabis testing underpin this expansion. The FDA’s 2024 implementation of ICH Q2(R2) and Q14 solidified regulatory legitimacy for the technique, encouraging capital investment by both innovator drug firms and contract research organizations (CROs). Integrated LC–SFC platforms that toggle between liquid and supercritical modes shorten method-transfer times, while cloud-enabled software simplifies compliance reporting. Demand also benefits from North American and European initiatives targeting solvent-use reductions, driving preference for CO₂-based mobile phases over organic-solvent-intensive HPLC. Skills shortages and detector limits with highly polar compounds remain growth brakes, but continued column innovation and AI-assisted method development are steadily easing these hurdles.

Key Report Takeaways

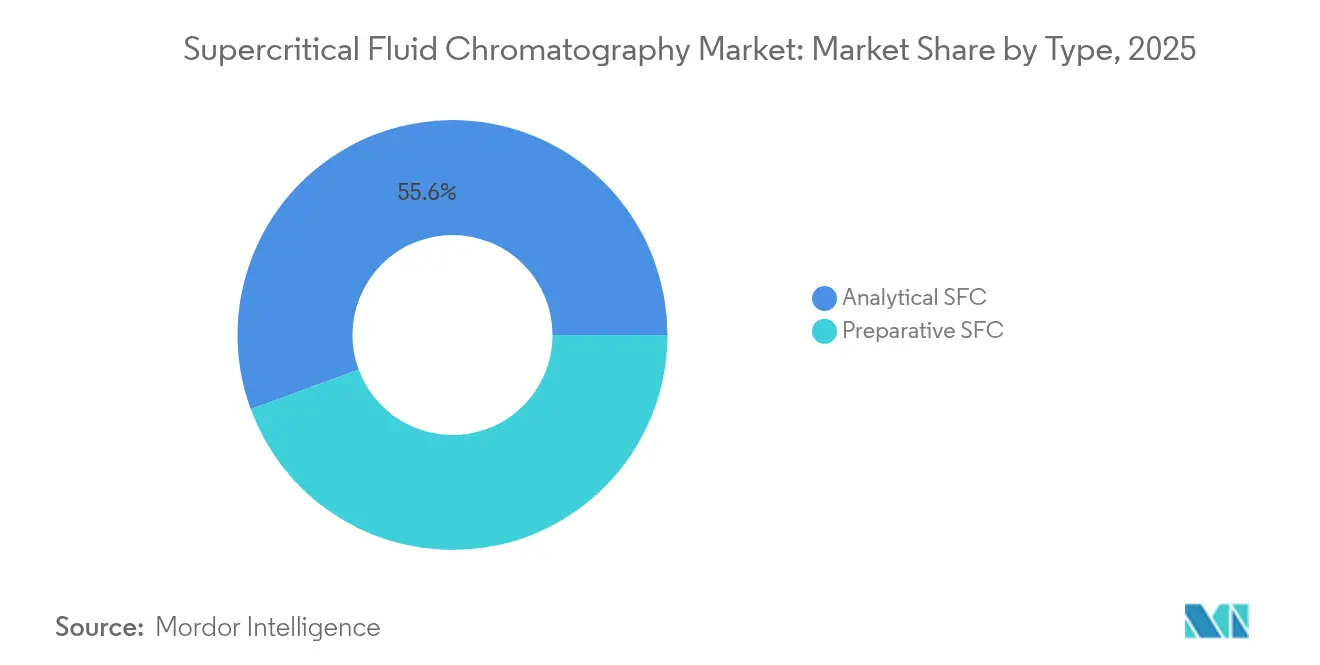

- By type, analytical SFC led with 55.62% of supercritical fluid chromatography market share in 2025, while preparative SFC is projected to expand at a 4.62% CAGR through 2031.

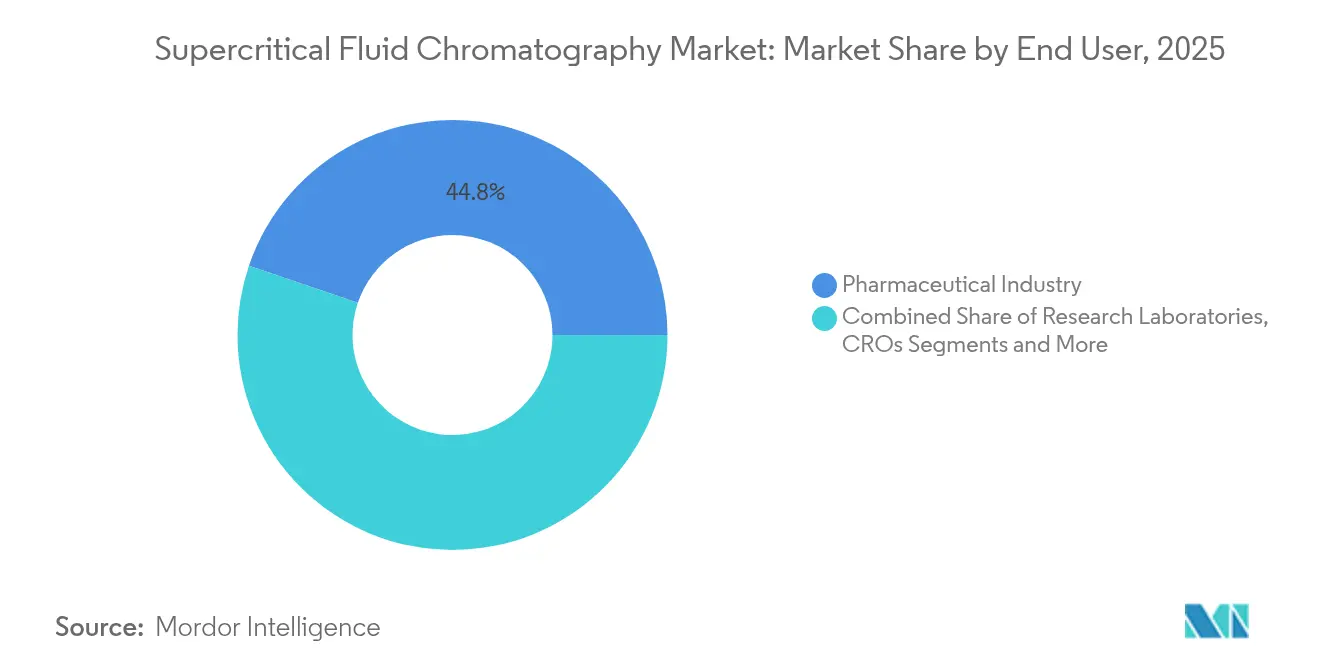

- By end-user, the pharmaceutical segment commanded a 44.78% share of the supercritical fluid chromatography market in 2025; CROs / CDMOs represent the fastest-growing cohort, with a 5.18% CAGR to 2031.

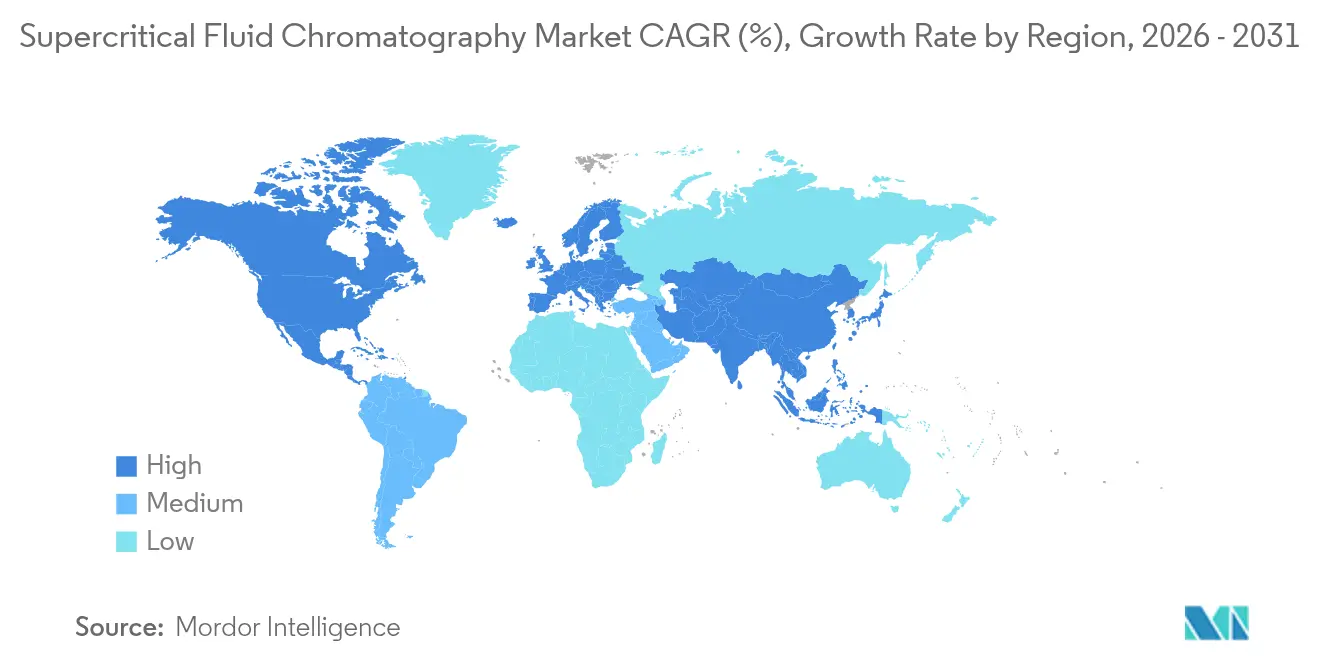

- By geography, North America accounted for 36.05% of the supercritical fluid chromatography market share in 2025, whereas Asia-Pacific is set to grow the quickest at 4.98% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supercritical Fluid Chromatography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Green Analytical Chemistry Mandates | +1.20% | Global, with early adoption in EU & North America | Medium term (2-4 years) |

| Growing Biopharma Demand For Chiral Separations | +0.90% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Rapid Screening Needs In Cannabis And Natural-Product QC | +0.60% | North America core, spill-over to emerging markets | Short term (≤ 2 years) |

| Rising Adoption Of Integrated LC–SFC Instrument Platforms | +0.80% | Global, concentrated in pharmaceutical hubs | Medium term (2-4 years) |

| Increasing Research Funding For Lipidomics And Metabolomics Workflows | +0.70% | Global, with concentration in academic centers | Long term (≥ 4 years) |

| Data-Driven Process Analytical Technology Integration In Continuous Manufacturing | +0.50% | North America & EU, early adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Green Analytical Chemistry Mandates

Heightened sustainability policies in Europe and the United States are reshaping laboratory investment priorities. Modern SFC systems cut organic-solvent use by up to 95% compared with HPLC, yet deliver equivalent resolution for pharmacopeial assays.[1]Ahmed M. Et al., “Green Analytical Chemistry Metrics,” Future Journal of Pharmaceutical Sciences, journals.elsevier.com Modified GAPI scoring, now common in European method-selection protocols, awards high ratings to CO₂-based separations, prompting pharmaceutical QA groups to fund SFC upgrades. Equipment vendors report that green-metric compliance is now a decisive factor in over half of new instrument tenders, signaling a persistent capital-spending tailwind for the supercritical fluid chromatography market.

Growing Biopharma Demand for Chiral Separations

Enantiomer-specific drug development drives continuous demand for high-throughput chiral screening. Advances in polysaccharide-based stationary phases let SFC resolve multi-stereocenter APIs that frustrate traditional HPLC, cutting lead-optimization cycles by several weeks. Multiple FDA-approved chiral drugs during 2022-2024 relied on SFC data packages. CROs now market “SFC-first” discovery platforms, citing success rates above 80% for single-method chiral separations, stimulating recurring consumables sales across the supercritical fluid chromatography market.

Rapid Screening Needs in Cannabis and Natural-Product QC

Enantiomer-specific drug development drives continuous demand for high-throughput chiral screening. Advances in polysaccharide-based stationary phases let SFC resolve multi-stereocenter APIs that frustrate traditional HPLC, cutting lead-optimization cycles by several weeks. Multiple FDA-approved chiral drugs during 2022-2024 relied on SFC data packages. CROs now market “SFC-first” discovery platforms, citing success rates above 80% for single-method chiral separations, stimulating recurring consumables sales across the supercritical fluid chromatography market.

Rising Adoption of Integrated LC–SFC Instrument Platforms

Pharmaceutical laboratories favor hybrid systems that switch between reversed-phase LC and SFC without replumbing. Sub-2-minute mode-switching and AI-guided solvent selection deliver orthogonal selectivity and reduce instrument footprints.[2]Nguyen P. Et al., “Hybrid LC–SFC Stationary Phases,” Journal of Separation Science, onlinelibrary.wiley.com As biopharma firms push continuous-manufacturing pilots, such flexibility is becoming a standard URS line item, boosting integrated platform uptake across the supercritical fluid chromatography market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Detector Compatibility For Highly Polar Analytes | -0.80% | Global, particularly affecting emerging applications | Medium term (2-4 years) |

| High Capital Cost Versus UHPLC Alternatives | -0.60% | Emerging markets, cost-sensitive segments | Short term (≤ 2 years) |

| Shortage Of Skilled Supercritical Fluid Chromatography Analysts | -0.50% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Limited Availability Of Advanced Chiral Columns In Emerging Regions | -0.30% | APAC emerging markets, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Detector Compatibility for Highly Polar Analytes

Electrospray efficiency declines when decompressed CO₂ dilutes post-column flow, limiting trace-level detection of polar metabolites. Although make-up solvent interfaces improve sensitivity, they introduce cost and complexity that delay adoption in budget-constrained labs. Environmental analysts therefore maintain dual LC and SFC workflows, tempering incremental instrument orders in several supercritical fluid chromatography market subsegments.

High Capital Cost Versus UHPLC Alternatives

A complete SFC stack can cost USD 200,000-400,000, roughly double a top-spec UHPLC. Smaller pharma firms and universities are often unable to justify the spend unless throughput exceeds 500 samples per month. Until vendors broaden mid-tier offerings, price elasticity will cap penetration in the lower-volume tiers of the supercritical fluid chromatography industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Analytical SFC Dominates Precision-Oriented Workstreams

In 2025, analytical configurations captured 55.62% of the supercritical fluid chromatography market share, reflecting widespread use in method-development and QC labs that require sub-ppm impurity profiling. The supercritical fluid chromatography market size for analytical platforms is projected to expand from USD 1.04 billion in 2026 to USD 1.28 billion by 2031 at a 4.26% CAGR. Robust validation guidance in ICH Q2(R2) reinforces long-term procurement commitments, while sub-2-µm particle compatibility delivers UHPSFC performance close to UHPLC.

Preparative systems, although smaller in absolute revenue, will outpace analytical units with a 4.62% CAGR. Gram-scale chiral purification for IND-enabling studies and growing natural-product processing underpin this trajectory. Larger column diameters and CO₂ recycling loops have reduced per-gram solvent cost, anchoring SFC within continuous-manufacturing skids for oncology APIs, thereby lifting the preparative segment within the supercritical fluid chromatography market.

By Component: Instruments Propel Innovation, Columns Track Application Breadth

The instruments sub-segment accounts for more than two-thirds of the supercritical fluid chromatography market revenue in 2025, energized by feature updates that integrate AI-driven method-suggestion engines and remote diagnostics. Automated modifier-blend modules now cut method-development time by 30%, a compelling value proposition for CROs aiming to shorten study timelines. Columns and consumables follow as the fastest-growing component group, recording a 4.92% CAGR to 2031. Hybrid silica-based stationary phases that operate seamlessly under LC and SFC conditions facilitate laboratory migration without wholesale method redevelopment. Meanwhile, software and services are carving a distinct revenue niche as compliance teams outsource GxP-validation scripting, intensifying recurring revenue patterns in the supercritical fluid chromatography industry.

By End-User: Pharma Remains Core, Outsourcing Accelerates

Pharmaceutical companies held 44.78% of the supercritical fluid chromatography market size in 2025, leveraging the technique for chiral purity assays and late-stage process control. Regulatory alignment and solvent-reduction goals sustain capital expenditure in large-molecule analytics. CROs and CDMOs recorded the highest projected CAGR at 5.18% through 2031. These service providers capitalize on SFC’s orthogonal selectivity to complement LC–MS data in regulatory submissions, often bundling the capability as a premium add-on. Academic and governmental research laboratories are next in line, buoyed by lipidomics grant clauses stipulating SFC access, thereby broadening the supercritical fluid chromatography market beyond purely commercial settings.

Geography Analysis

North America retained leadership with 36.05% of the supercritical fluid chromatography market share in 2025. The FDA’s clear validation pathway, combined with expanding cannabis-testing requirements, drives routine SFC adoption in both regulated QC and third-party testing labs. Continuous-manufacturing pilots in monoclonal antibody plants further stoke demand for integrated PAT-ready SFC modules.

Europe follows closely, anchored by stringent solvent-reduction policies and Horizon research funding that underscores SFC’s environmental credentials. EMA alignment with ICH Q14 has normalized SFC inclusion in CTD dossiers, ensuring sustained instrument refresh cycles among generic-drug makers. Elite universities in Germany and the Netherlands are upgrading core facilities with UHPSFC-MS units to meet lipidomics project loads, enriching the supercritical fluid chromatography market ecosystem.

Asia-Pacific is set to grow fastest at 4.98% CAGR, propelled by China’s expanding API-export base and Japan’s push for green-chemistry metrics in GMP audits. Shimadzu’s Nexera UC Prep roll-out offers localized service networks, easing adoption risks for first-time users and amplifying preparative-scale penetration. Nonetheless, limited regional supply of specialty chiral columns and a scarcity of SFC-trained analysts temper near-term volumes, leaving a capacity gap that global consumables vendors are racing to fill.

Regulatory Landscape

Regulatory acceptance for supercritical fluid chromatography (SFC) in regulated pharmaceutical testing is anchored in method validation and lifecycle expectations under ICH Q2(R2) and ICH Q14, which the FDA implemented in 2024 and which are used to support analytical procedures included in submissions and commercial quality control. In the United States, SFC methods for drug manufacturing and release testing also need to align with cGMP requirements under 21 CFR Parts 210 and 211, shaping documentation, change control, and routine suitability practices.

Standard-setting activity continues to formalize SFC practice. In April 2026, the United States Pharmacopeia (USP) published a prospectus for a new General Chapter dedicated to SFC, covering principles, instrumentation, qualification, and method validation, with applicability spanning pharmaceuticals as well as dietary supplements and herbal products. In Europe, EMA alignment with ICH Q14 supports inclusion of SFC workflows in CTD dossiers, reinforcing cross-region method-transfer discipline for global manufacturers and CROs/CDMOs.

Value Chain Analysis

The SFC value chain begins with upstream inputs, including high-purity CO2 supply, modifiers and solvents, and specialty consumables such as chiral stationary-phase columns. Instrument OEMs then integrate these into engineered subassemblies like high-pressure pumps, valves, and back-pressure regulation components. Core OEM nodes include Waters, Agilent, Shimadzu, and JASCO, while specialty service providers and application labs support adoption through method development, purification services, and operator training (examples include Lotus Separations, Reach Separations, and ABsys SFC). Midstream, software, validation documentation, and field service (IQ/OQ, Part 11-aligned data workflows, and instrument qualification) are often central, since regulated end users frequently procure SFC as a turnkey, compliance-ready capability.

Downstream, systems and consumables are used across pharmaceutical QC, CRO and CDMO laboratories, and selected adjacent testing environments, with repeat demand driven by columns and consumables as methods move into routine use. Bottlenecks tend to concentrate on uptime and qualified service coverage, since instrument downtime can disrupt QC release schedules, and reliance on specific back-pressure regulator technologies can create single-source vulnerabilities. Distribution and sustainment typically rely on authorized service networks to keep compliance artifacts current (including ISO 17025 and 21 CFR Part 11-aligned controls where relevant), making local technical support and validated software packages as important as the core instrument hardware in purchasing decisions.

Competitive Landscape

The supercritical fluid chromatography market shows moderate concentration. Waters, Agilent, and Shimadzu collectively account for an estimated 55-60% revenue share, leveraging broad installed bases and in-house column chemistries to reinforce customer lock-in. Waters’ Q4 2024 instrument surge came partly from PAT-ready SFC modules bundled with BioResolve columns, underscoring synergy between hardware and consumables.

Agilent is foregrounding AI-powered ChemStation upgrades that auto-suggest SFC screening conditions, a bid to lower expertise hurdles for mid-tier labs. Shimadzu differentiates on the preparative scale, marketing gas–liquid separation technology that eliminates external chillers and trims utility costs at kilogram purification volumes. Smaller specialists such as Sepiatec and Aurora SFC offer modular skids for cannabis labs and metabolomics cores, although limited-service footprints constrain their reach.

Strategic alliances are intensifying. Agilent collaborates with Daicel on next-gen chiral phases, while Waters’ OEM program embeds its CO₂ pumps in third-party PAT rigs. Competitors increasingly bundle compliance e-learning and IQ/OQ kits, reflecting customer demand for turnkey validation. The supercritical fluid chromatography industry thus pivots on integrated ecosystems rather than single-component differentiation.

Supercritical Fluid Chromatography Industry Leaders

Shimadzu Scientific Instruments

JASCO

Fluitron, Inc.

Thar Process, Inc.

SFT, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The continued shift of SFC from specialist deployments into standardized, regulated workflows is creating a clear opportunity as formal guidance and compendial standardization expand. The USP prospectus published in April 2026 for a new General Chapter on SFC, covering instrumentation, qualification, and method validation, provides a concrete pathway for broader, more uniform adoption across pharmaceutical, dietary supplement, and herbal product testing, and it can reduce friction in method transfer between R&D and GMP quality control.

Application whitespace is also expanding beyond core API chiral separations into materials and product-safety testing that benefits from CO2-based separations and SFC-MS coupling. In April 2026, Talanta reported an approach combining stir-bar sorptive extraction with online supercritical fluid extraction and SFC-MS to analyze migrating plastic additives from medical devices, highlighting a route for SFC workflows in medical-device related analytics. On the technology side, integrated LC-SFC (unified chromatography) platforms and preparative-scale infrastructure upgrades, including CO2 supply and bulk delivery systems, create room for vendors and service providers to bundle compliance-ready hardware, validated software, and consumables into higher-uptime packages that address skilled-analyst constraints and routine QC reliability needs.

Recent Industry Developments

- February 2026: Thar Process launched a new line of CO2 bulk delivery systems for preparative supercritical fluid chromatography (SFC) and pilot-scale supercritical fluid extraction (SFE) users. The launch targets a practical constraint for scale-up, improving continuity of CO2 supply and supporting higher-throughput, longer-duration operations in purification workflows.

- May 2025: Shimadzu Asia Pacific entered a strategic partnership with Core Separations, naming it the exclusive distributor for industrial-scale SFC and SFE systems across Southeast Asia and South Asia (excluding India). The move strengthens regional access to larger-format systems and service coverage, which can accelerate adoption in industrial purification and process environments beyond traditional analytical labs.

- January 2024: Thar Process released the SuperDry 9000 supercritical CO2 lyophilization system aimed at R&D and clinical-scale biopharmaceutical applications. The product broadens supercritical CO2 processing capabilities adjacent to SFC/SFE ecosystems, reinforcing supplier positioning with biopharma customers building solvent-reduction and CO2-based processing toolkits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the supercritical fluid chromatography market is counted as the revenues generated from SFC instruments and the supporting items needed to run SFC separations, across labs and industrial users, in all major regions.

Scope exclusions: Services that are not directly tied to SFC systems (such as general lab consulting) and broad chromatography equipment that is not SFC-based are not counted.

Segmentation Overview

- By Type

- Preparative SFC

- Analytical SFC

- By Component

- Instruments

- Columns & Consumables

- Software & Services

- By End-User

- Research Laboratories

- Pharmaceutical Industry

- CROs & CDMOs

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear picture of where SFC is being used and how that use is changing over time, so later assumptions were anchored to real activity. Public sources were used for this, including the US FDA guidance library for analytical method expectations, USP and other pharmacopeia references for method standards, peer-reviewed journals covering chiral separations and lipidomics workflows, and government trade statistics portals that show instrument and component flows at a high level.

We also reviewed company filings, investor decks, and product documentation to understand how vendors describe SFC systems, columns, and related consumables, and which end users are actively buying them. A paid subscription for company financials and news was used only to speed up cross-checks on revenue exposure and major product launches, and a paid patent database was used to scan where method and column innovation is heading. The desk sources named above are illustrative and not exhaustive, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what share of chromatography budgets can realistically shift to SFC and where it stays limited due to method fit, detector needs, and analyst familiarity. We spoke with a mix of instrument and column suppliers, distributors, pharmaceutical and biotech labs, CRO and CDMO users, and research laboratories, then validated assumptions across APAC, EMEA, and the Americas so regional adoption differences were not averaged away.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 49% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 15% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where installed base, annual placements, and replacement cycles for SFC instruments were reconstructed by region and then converted into value using typical selling prices and mix. Once the demand pool was shaped, we cross-checked it using selective bottom-up approximations, including sampled supplier revenue splits, distributor channel checks, and a sanity check that ties consumables and software attachment to instrument activity.

The model key inputs included instrument shipment momentum, average selling price movements by system class (analytical versus preparative), column and consumable replacement frequency, share of chiral separations and high throughput workflows that favor SFC, and regional lab funding and pharma manufacturing trends that affect capital purchases. Where bottom-up splits were incomplete, gaps were handled by using proxy ratios from similar chromatography purchase patterns and then re-tested with interview feedback before finalizing.

Forecasts were prepared using scenario analysis supported by simple multivariate relationships, where adoption is linked to pharma pipeline activity, lab investment cycles, and the pace of method standardization. Assumptions were kept transparent so a client can trace each year's change back to a small set of drivers, and adjust them if their internal view differs.

Data Validation & Update Cycle

Outputs were validated through multiple checks, starting with comparing implied instrument volumes and attachment rates against independent signals like product launches, tender activity, and reported lab expansion trends. If the model produced sudden jumps, we revisited the price, mix, or replacement assumptions and re-contacted sources when the variance could not be explained by a clear event.

Each major spreadsheet block is reviewed by another analyst before sign-off, and the full storyline is tested for internal consistency so growth drivers align with the numeric trajectory. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, large acquisitions, or sharp shifts in lab spending. Before delivery, we do a final evidence pass so clients receive the latest updated view.

Mordor Intelligence's Supercritical Fluid Chromatography Market Sizing Compared With Other Published Estimates

Different published market sizes for SFC can look far apart because scope boundaries are not always the same, and because some models assume faster adoption than what end users are currently budgeting for. Currency timing, the treatment of consumables and software, and how the base year is picked can also shift the final number even when the story sounds similar.

Instrument shipment signals, consumables attachment patterns, and interview-validated adoption limits across pharma, CROs, and research labs are the checks that keep Mordor Intelligence's estimate tied to SFC specific demand, rather than counting broader chromatography spending that does not require supercritical CO2 based separation. The biggest gaps usually come from whether kits and reagents are bundled into the total, how quickly preparative use is assumed to scale, and whether price changes are applied without aligning them to purchase cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.86 B (2026) | |

| Global Market Publisher A | USD 1.42 B (2025) | Uses a different base year and applies a high long range growth rate, which can lift totals if adoption is projected faster than lab budget cycles. Component scope is described mainly as instruments and consumables, with limited clarity on software and service revenue treatment. |

| Market Research Group B | USD 1.63 B (2025) | Uses a wider product list that includes kits and reagents and a broad end user map, which can pull in spend that is not consistently SFC specific. The forecast window and CAGR basis differ, so the year to year comparability to a 2026 base is not direct. |

The spread in values becomes easier to explain once the year, component inclusions, and adoption pace assumptions are laid side by side. By keeping the model linked to observable instrument activity and realistic attachment behavior, our number stays traceable to inputs that can be rechecked and updated as the market evolves.

Key Questions Answered in the Report

What is the current size of the supercritical fluid chromatography market?

The market stands at USD 1.86 billion in 2026 and is projected to reach USD 2.35 billion by 2031.

Which segment leads the supercritical fluid chromatography market?

Analytical SFC dominates, holding 55.62% of 2025 revenue and benefiting from ICH-validated QC applications.

Why is Asia-Pacific the fastest-growing region?

Expanding API manufacturing, supportive regulatory harmonization, and localized instrument launches drive a 4.98% CAGR outlook.

What are the main restraints to broader adoption?

High capital costs versus UHPLC and detector sensitivity limitations for highly polar analytes are the chief barriers.

How are green-chemistry mandates influencing purchase decisions?

EU and North American regulations reward CO₂-based separations, encouraging laboratories to upgrade to SFC to reduce solvent waste.

Page last updated on: