Sulphur Recovery Technologies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 2.51% CAGR |

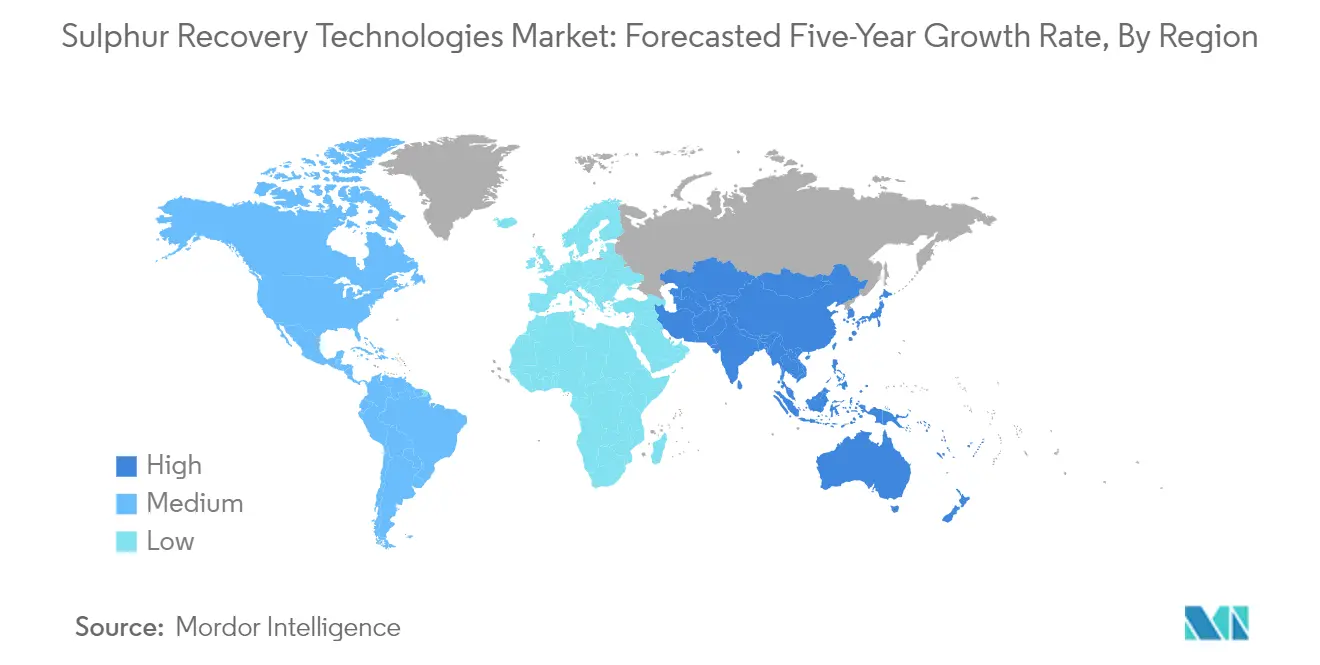

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

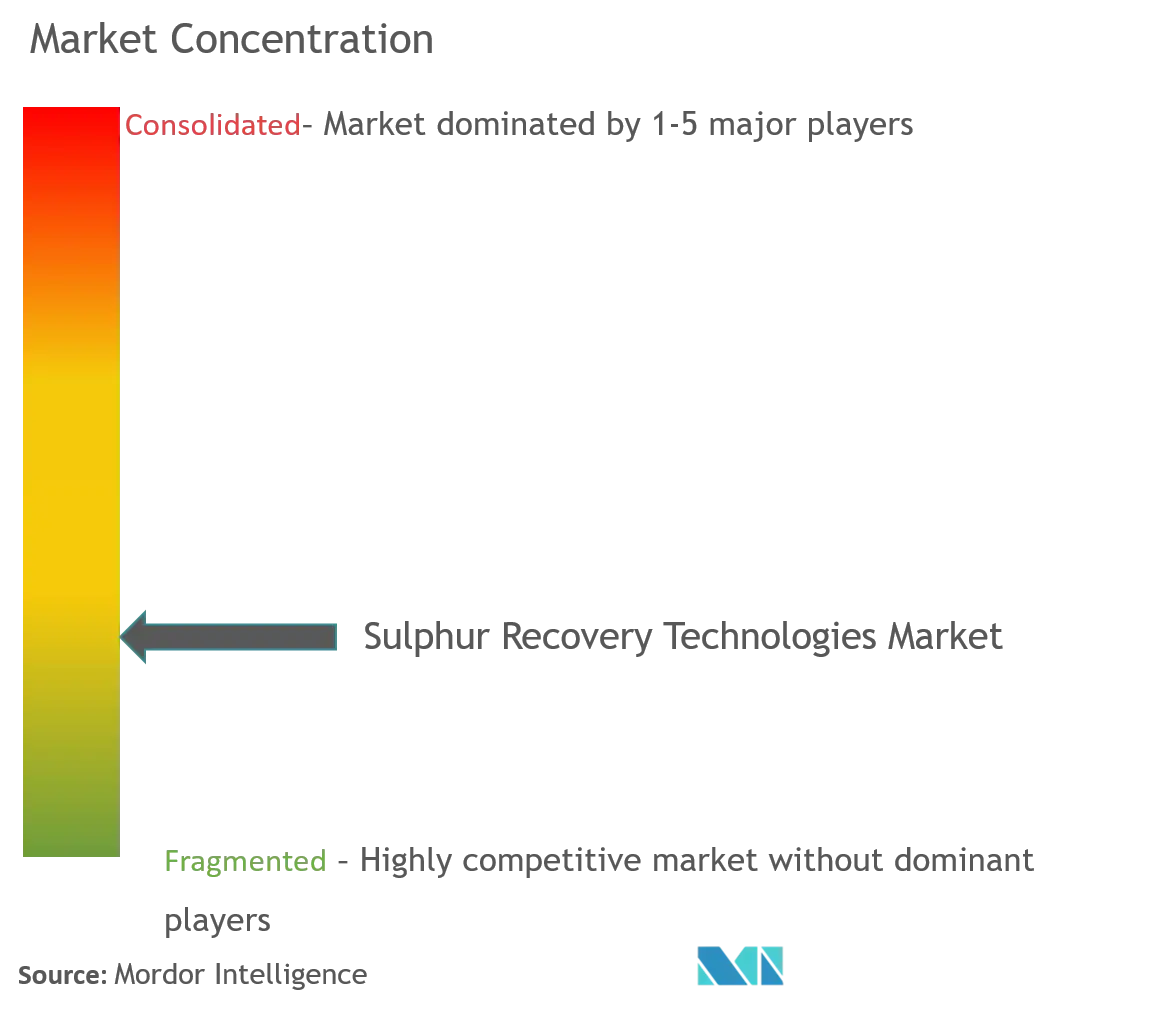

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulphur Recovery Technologies Market Analysis by Mordor Intelligence

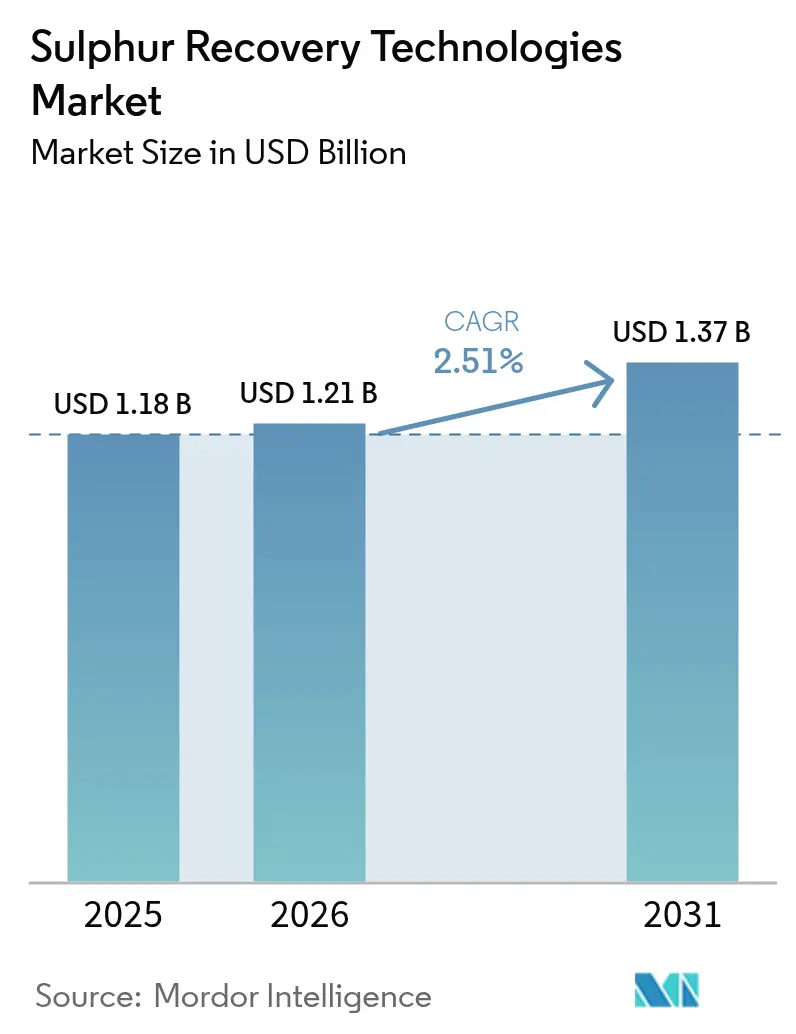

The Sulphur Recovery Technologies Market size was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.21 billion in 2026 to reach USD 1.37 billion by 2031, at a CAGR of 2.51% during the forecast period (2026-2031).

The sulfur recovery technology landscape is experiencing significant transformation amid growing industrial activities and environmental consciousness. Global energy and industrial process-related carbon dioxide emissions reached approximately 35.1 billion metric tons in 2023, representing a 1.6% increase from the previous year, highlighting the urgent need for effective emission control technologies. This surge in emissions has prompted industries to adopt more sophisticated sulfur recovery unit solutions, particularly in regions with stringent environmental regulations. The implementation of the International Maritime Organization (IMO) rules has further catalyzed the adoption of advanced sulfur recovery unit technologies, especially in the maritime sector, where vessels must now comply with a 0.50% m/m sulfur content limit in fuel oil.

The industry is witnessing substantial technological advancements and infrastructure developments across various sectors. In May 2024, Bharat Coal Gasification & Chemicals Limited (BCGCL) launched a significant tender worth INR 117.82 billion for its Coal to Ammonium Nitrate project in Odisha, incorporating advanced sulfur recovery unit units. Similarly, Saudi Aramco announced plans to implement 99 projects over the next three years, with 58 specifically focused on oil, gas, and petrochemical facilities, including comprehensive sulfur recovery unit upgrades across the country. These developments reflect the industry's commitment to enhancing sulfur recovery technology capabilities while maintaining operational efficiency.

The power generation sector is undergoing notable transformations in sulfur emission management. According to the US Environmental Protection Agency's 2023 data, SO2 emissions from US power plants decreased by 24% compared to 2022, demonstrating the effectiveness of modern sulfur recovery technology. The implementation of flue gas desulfurization (FGD) systems in power plants has become increasingly prevalent, particularly in regions utilizing high-sulfur coal for power generation. This trend is especially significant in Asia-Pacific, where coal remains a dominant energy source.

The petrochemical and refining sectors continue to drive innovation in sulfur recovery technology. China's annual oil refining capacity rose to 936 million tonnes in 2023, necessitating advanced sulfur recovery technology solutions to meet environmental standards. In April 2024, Aramco awarded a USD 7.7 billion engineering, procurement, and construction (EPC) contract for expanding the Fadhili gas plant, which includes upgrading the existing sulfur recovery unit to produce 2,300 metric tons of sulfur production daily. These developments underscore the industry's focus on expanding capacity while maintaining stringent environmental compliance through advanced sulfur recovery technology.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sulphur Recovery Technologies Market Trends and Insights

Growing Environmental Concerns and Strict Norms on Pollution

The global push for stricter environmental regulations has become a primary driver for the sulfur recovery unit technologies market, particularly evident in the maritime industry's transformation. In October 2023, the Australian Maritime Safety Authority implemented stringent regulations mandating that domestic ships must utilize fuel oil with no more than 0.50% m/m sulfur content, while completely prohibiting the transport of fuel oil exceeding this threshold unless carried as cargo. This regulatory framework has been further strengthened by the International Maritime Organization's (IMO) expansion of Emission Control Areas (ECAs), with the Mediterranean Sea ECA set to come into force in May 2025, and the recent approval of proposals to designate the Canadian Arctic and Norwegian Sea as ECAs. These developments demonstrate the growing global commitment to reducing sulfur emissions in marine operations.

The power generation sector has witnessed remarkable progress in emission reduction efforts, highlighting the increasing importance of sulfur recovery unit technologies. According to the US Environmental Protection Agency's 2023 data, SO2 emissions from US power plants decreased by 24% compared to 2022, marking a dramatic 96% reduction in annual SO2 emissions from 1990 to 2023. This significant achievement is complemented by major industry investments, such as Technip Energies' January 2023 contract to enhance sulfur recovery facilities at Aramco's Riyadh Refinery. The project, which includes installing three new tail gas treatment units and upgrading existing sulfur recovery units, aims to achieve a recovery efficiency exceeding 99.9%, demonstrating the industry's commitment to meeting increasingly stringent environmental standards.

The urgency to address environmental concerns is further emphasized by the rising global energy-related CO2 emissions, which reached approximately 35.1 billion metric tons in 2023, representing a 1.6% increase from 2022. This upward trend in emissions has prompted governments worldwide to implement more stringent environmental regulations, particularly focusing on sulfur emissions from industrial operations. For instance, in February 2024, the US Environmental Protection Agency revealed that power plants subject to both the Cross-State Air Pollution Rule and the Acid Rain Program collectively emitted 0.65 million tons of SO2 in 2023, marking a significant reduction of 11.2 million tons from 1995 levels. These developments underscore the critical role of gas desulfurization and hydrogen sulfide removal technologies in meeting increasingly stringent environmental standards and supporting global sustainability goals.

Segment Analysis: By Application

Refineries Segment in Sulphur Recovery Technologies Market

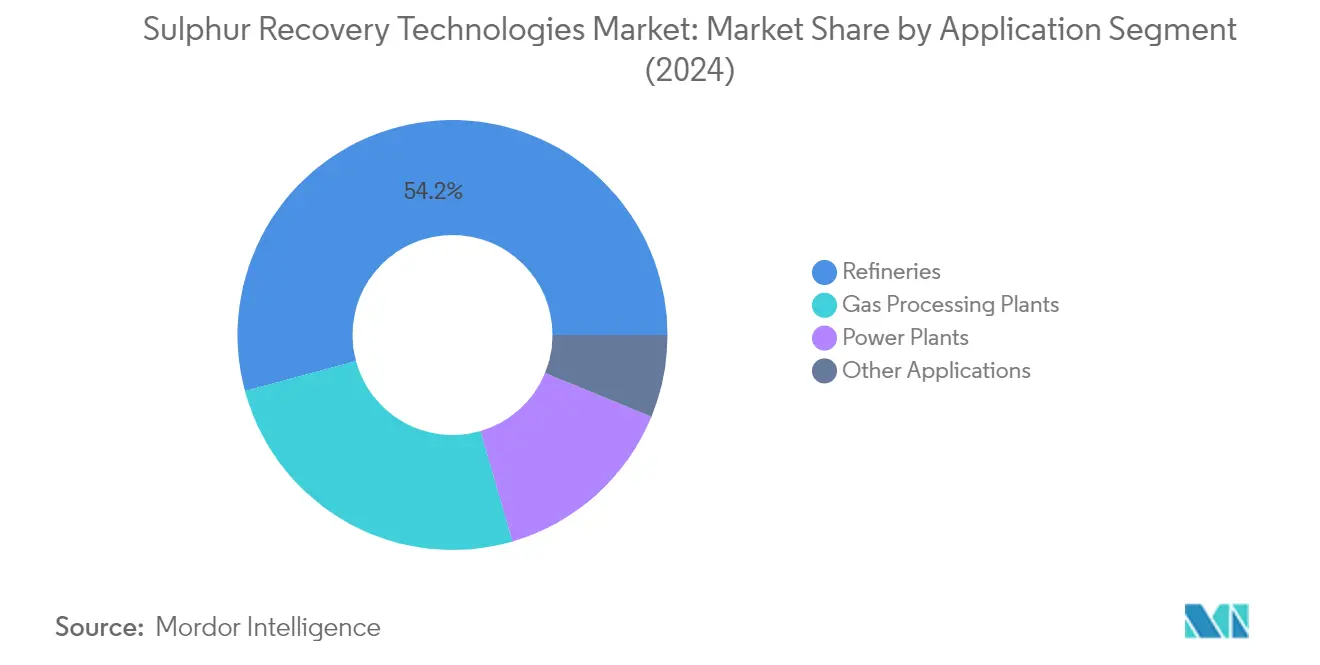

The refineries segment dominates the global sulphur recovery unit technologies market, commanding approximately 53.42% of the total market share in 2025, while also exhibiting the highest growth rate with a projected growth of nearly 2.9% from 2026 to 2031. This segment's prominence is driven by stringent environmental regulations requiring refineries to implement advanced sulphur recovery units (SRUs) for reducing emissions. Major investments in refinery expansions and upgrades, particularly in regions like Asia-Pacific and the Middle East, have further strengthened this segment's position. The implementation of IMO 2020 regulations restricting sulphur content in marine fuels has also catalyzed the adoption of sulphur processing technologies in refineries worldwide. Additionally, the growing focus on producing cleaner fuels with lower sulphur content has necessitated the installation and upgrading of SRUs in refineries globally.

Remaining Segments in Sulphur Recovery Technologies Market

The gas processing plants segment represents the second-largest application area for sulphur recovery technologies, followed by power plants and other applications. Gas processing plants utilize these technologies to remove sulphur contaminants from sour gas treatment streams, ensuring compliance with environmental regulations while producing valuable by-products. The power plants segment, particularly coal-fired facilities, employs flue gas desulfurization systems to meet emission standards and reduce environmental impact. Other applications include waste-to-energy plants, geothermal facilities, chemical plants, and petrochemical operations, where sulphur recovery technologies play a crucial role in emission control and process optimization. The growing emphasis on environmental sustainability and stricter emission regulations continues to drive the adoption of acid gas treatment technologies across these segments.

Sulphur Recovery Technologies Market Geography Segment Analysis

North America represents a mature and well-established market for sulphur recovery technology, holding approximately 25.60% of the global market share in 2025. The region's market is characterized by stringent environmental regulations and advanced technological adoption, particularly in the United States and Canada. The presence of extensive oil and gas infrastructure, including refineries and industrial gas treatment plants, drives the continuous demand for sophisticated sulphur recovery unit solutions. The United States leads the regional market with its robust refining sector, while Canada maintains some of the highest sulphur recovery rates globally. The market is witnessing a transformation as traditional refinery expansion gives way to emerging opportunities in renewable energy sources like geothermal, biomass, and waste-to-energy plants. These alternative energy sources, while generally cleaner burning, still require sulphur recovery unit technologies for environmental compliance. The region's focus on technological advancement and environmental stewardship continues to shape the market landscape, with companies investing in upgrading existing facilities to meet increasingly stringent emission standards.

The Asia-Pacific region has emerged as a powerhouse in the global sulphur recovery technologies market, demonstrating approximately 2.05% growth from 2019 to 2025. This dynamic market is driven by rapid industrialization and expanding refining capacities across major economies like China and India. The region's market landscape is characterized by significant investments in new refineries and modernization of existing facilities, particularly in China, which has been actively expanding its refining infrastructure. The implementation of stricter environmental regulations, especially regarding sulphur content in fuels, has catalyzed the adoption of advanced recovery technologies. India's aggressive expansion in its refining sector, coupled with Japan and South Korea's technological advancement in sulphur recovery processes, further strengthens the regional market. The region's commitment to reducing environmental impact while meeting growing energy demands has led to increased implementation of sophisticated sulphur recovery units across various industrial applications.

The European sulphur recovery technologies market is projected to grow at approximately 1.95% during 2026-2031, reflecting the region's mature yet evolving market dynamics. The market is characterized by its strong emphasis on environmental sustainability and technological innovation, particularly in countries like Germany, France, and the United Kingdom. European refineries and industrial facilities are at the forefront of implementing advanced sulphur recovery solutions, driven by the European Union's stringent environmental regulations and emission standards. The region's focus on clean energy transition and industrial decarbonization has led to increased investments in upgrading existing sulphur recovery units and implementing new technologies. The market benefits from the presence of leading technology providers and a strong research and development ecosystem. The integration of digital technologies and automation in sulphur recovery processes further distinguishes the European market, as facilities seek to optimize efficiency and reduce operational costs while maintaining high environmental standards.

The South American sulphur recovery technologies market is experiencing significant transformation, primarily driven by developments in key countries like Brazil, Argentina, and Colombia. The region's market is characterized by ongoing investments in refinery expansion projects and modernization initiatives, particularly in Brazil's downstream sector. The implementation of stricter environmental regulations and the need to process higher sulphur content crude oil has intensified the demand for advanced recovery technologies. The market is witnessing increased activity in waste-to-energy projects and biomass processing facilities, which require sophisticated sulphur recovery solutions. The region's commitment to reducing environmental impact while expanding its industrial capabilities has led to the adoption of more efficient sulphur recovery technologies. The presence of significant oil and gas reserves, coupled with growing investment in processing infrastructure, continues to shape the market landscape, creating opportunities for technology providers and industrial operators alike.

The Middle East & Africa region represents a crucial market for sulphur recovery technologies, driven by its extensive oil and gas processing infrastructure and ongoing investments in refining capabilities. The market is particularly dynamic in countries like Saudi Arabia and the United Arab Emirates, where significant investments in refinery upgrades and expansions are driving demand for advanced sulphur recovery solutions. The region's focus on modernizing its processing facilities and meeting international environmental standards has led to increased adoption of sophisticated recovery technologies. The presence of large-scale petrochemical projects and the processing of high-sulphur crude oil necessitates advanced recovery solutions. The market is further characterized by continuous technological upgrades and capacity expansions in existing facilities. African nations, particularly Nigeria, are witnessing growing investments in refining infrastructure, creating new opportunities for sulphur recovery technology providers. The region's commitment to reducing environmental impact while maintaining its position as a global energy hub continues to drive market growth.

Competitive Landscape

Top Companies in Sulphur Recovery Technologies Market

The global sulfur recovery technologies market is led by established players, including WorleyParsons Limited, Shell PLC, Bechtel Corporation, Fluor Corporation, and Air Liquide SA. These companies are driving innovation through advanced sulfur purification and recovery solutions, with a particular focus on improving efficiency and environmental compliance. The industry witnesses continuous product development in areas such as Claus tail-gas treatment units, amine gas treatment systems, and integrated sulfur recovery technologies solutions. Companies are strengthening their market positions through strategic partnerships and technology licensing agreements, particularly in emerging markets. Operational excellence is being achieved through digitalization initiatives and the integration of smart technologies in sulfur recovery technologies units. Geographic expansion remains a key focus, with companies establishing regional centers of excellence and forming local partnerships to better serve diverse market needs.

Consolidated Market with Strong Regional Players

The sulfur recovery technologies market exhibits a moderately consolidated structure, characterized by the presence of both global engineering conglomerates and specialized technology providers. Global players like Shell and WorleyParsons dominate through their comprehensive portfolio of technologies and extensive geographical presence, while regional specialists maintain strong positions in specific markets through their focused expertise and local relationships. The market has witnessed significant consolidation through strategic acquisitions, such as the Brimstone Group's acquisition of Brimstone Sulphur Symposium and Merichem Technologies' acquisition of Chemical Products Industries, indicating a trend toward technology and capability enhancement.

The competitive dynamics are shaped by high entry barriers due to technological complexity and stringent regulatory requirements, favoring established players with proven track records. Market participants are increasingly focusing on building long-term relationships with end-users through comprehensive service offerings that include not only technology provision but also maintenance, optimization, and upgrade services. The industry structure is further characterized by strategic alliances between technology providers and engineering firms to offer integrated solutions, particularly for large-scale projects in emerging markets.

Innovation and Sustainability Drive Future Success

Success in the sulfur recovery technologies market increasingly depends on companies' ability to deliver innovative, environmentally compliant solutions while maintaining cost competitiveness. Incumbent players are strengthening their market positions by investing in research and development to improve recovery efficiency and reduce environmental impact. Companies are also focusing on developing modular and flexible solutions that can accommodate varying feedstock qualities and operating conditions. The ability to provide comprehensive digital solutions, including remote monitoring and predictive maintenance capabilities, is becoming a crucial differentiator in the market.

For new entrants and challenger companies, success lies in identifying and serving underserved market segments and developing specialized solutions for specific applications. The high concentration of buyers in certain regions and industries necessitates strong relationship management capabilities and local presence. Companies must also address the growing threat of substitute technologies, particularly in regions with stringent environmental regulations. The regulatory landscape, especially regarding emissions standards and safety requirements, continues to shape competitive strategies, with successful companies demonstrating the ability to anticipate and adapt to evolving compliance requirements while maintaining operational efficiency.

Sulphur Recovery Technologies Industry Leaders

Enersul Limited Partnership

WorleyParsons Limited

Bechtel Corporation

Fluor Corporation

Shell Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Bharat Coal Gasification & Chemicals Limited (BCGCL), a joint venture of Coal India Ltd and BHEL, floated a tender for INR 117.82 billion for a selection of lump sum turnkey (LSTK-2) of its Coal to Ammonium Nitrate project in Odisha. The project is expected to be executed through four packages, where LSTK-2, 3, and 4 are expected to be outsourced through floating tenders, and LSTK 1 will be done by BHEL. The LSTK-2 package is expected to include raw gas purification, including a CO shift unit, rectisol unit, sulfur recovery unit, and liquid nitrogen wash unit.

- May 2024: Saudi Arabia’s national oil company, Saudi ARAMCO, announced plans to launch 99 projects over the next three years to increase the production of oil and gas, improve capacity treatment, and modernize other related facilities. Out of the 99 projects, 58 are related to oil, gas, and petrochemical projects. Out of 58 projects, some of these include a gas lift program at the Marjan field, dry gas handling at Shaybah, and sulfur recovery unit upgrades across the country.

Global Sulphur Recovery Technologies Market Report Scope

Sulfur recovery technology refers to recovering elemental sulfur from hydrogen sulfide. This process is applied in various industries, such as crude oil refineries, gas processing units, power plants, etc.

The sulfur recovery technologies market is segmented by application and geography. By application, the market is segmented into refineries, gas processing plants, power plants, and others. The report also covers the market sizes and forecasts across major regions. The market sizes and demand forecasts are provided in value terms (USD) for all the above segments.

| Refineries |

| Gas Processing Plants |

| Power Plants |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| Asia-Pacific | India |

| China | |

| South Korea | |

| Japan | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| NORDIC | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Nigeria | |

| Oman | |

| South Africa | |

| Egypt | |

| Algeria | |

| Rest of Middle East & Africa |

| Application | Refineries | |

| Gas Processing Plants | ||

| Power Plants | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Asia-Pacific | India | |

| China | ||

| South Korea | ||

| Japan | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| NORDIC | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Nigeria | ||

| Oman | ||

| South Africa | ||

| Egypt | ||

| Algeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How big is the Sulphur Recovery Technologies Market?

The Sulphur Recovery Technologies Market size is expected to reach USD 1.21 billion in 2026 and grow at a CAGR of 2.51% to reach USD 1.37 billion by 2031.

What is the current Sulphur Recovery Technologies Market size?

In 2026, the Sulphur Recovery Technologies Market size is expected to reach USD 1.21 billion.

Who are the key players in Sulphur Recovery Technologies Market?

Enersul Limited Partnership, WorleyParsons Limited, Bechtel Corporation, Fluor Corporation and Shell Plc are the major companies operating in the Sulphur Recovery Technologies Market.

Which is the fastest growing region in Sulphur Recovery Technologies Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Sulphur Recovery Technologies Market?

In 2025, the Asia Pacific accounts for the largest market share in Sulphur Recovery Technologies Market.

What years does this Sulphur Recovery Technologies Market cover, and what was the market size in 2025?

In 2025, the Sulphur Recovery Technologies Market size was estimated at USD 1.18 billion. The report covers the Sulphur Recovery Technologies Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Sulphur Recovery Technologies Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: