Turbomachinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 28.37 Billion |

| Market Size (2031) | USD 31.45 Billion |

| Growth Rate (2026 - 2031) | 2.08% CAGR |

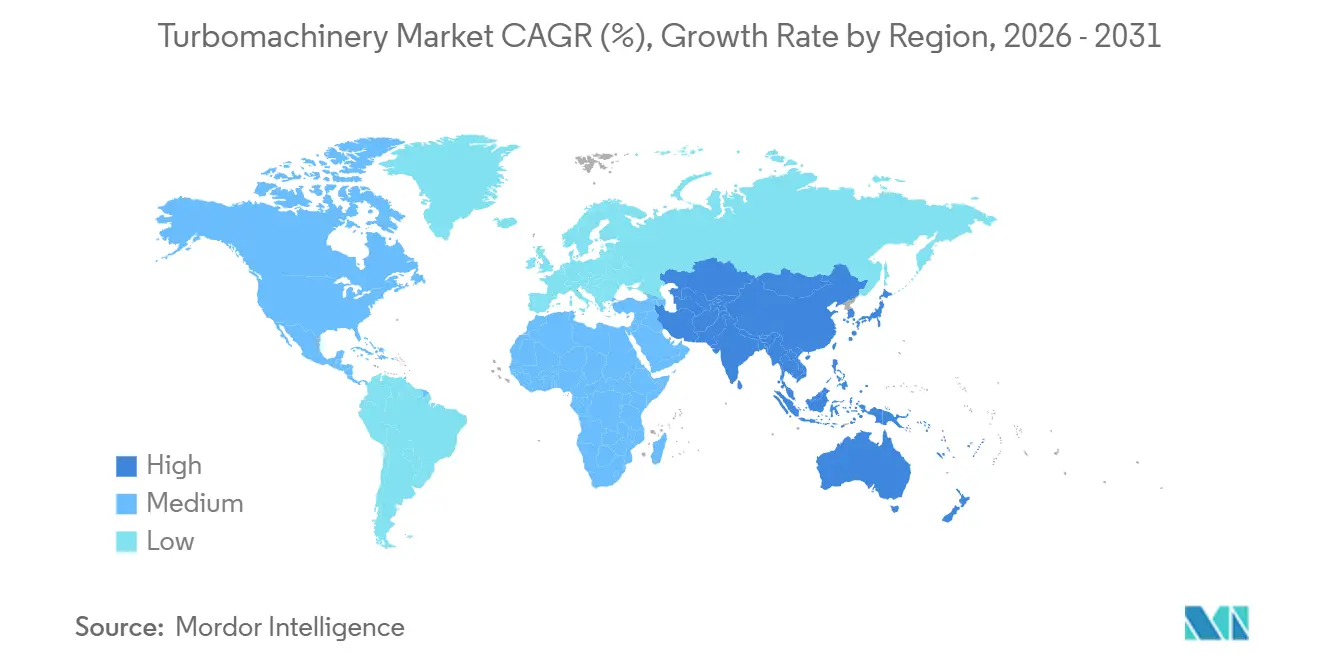

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turbomachinery Market Analysis by Mordor Intelligence

The global turbomachinery market size is expected to increase from USD 27.12 billion in 2025 to USD 28.37 billion in 2026 and reach USD 31.45 billion by 2031, and is expected to grow at a CAGR of 2.1% over 2026-2031. Steady spending across oil and gas infrastructure, power generation projects, and lifecycle services supports this measured expansion in the global turbomachinery market. A large installed base keeps overhaul, upgrades, and demand for active parts, which reduces the effect of slower project approvals on overall revenue. Liquefied Natural Gas (LNG) final investment decisions exceeded 90 billion cubic meters per year in 2025, which is feeding equipment order pipelines for compressors and gas turbines through the late 2020s [1]Source: International Energy Agency, “Gas Market Report, Q1-2026, Executive Summary,” IEA, iea.org . At the same time, data-center power demand and hydrogen-ready retrofit programs are changing Original Equipment Manufacturer (OEM) priorities, while supply tightness in forgings and hot-section components supports backlog discipline and pricing. Competition remains strongest in large-frame gas turbines, while compressors, pumps, and services show a broader supplier base across the global turbomachinery market.

Key Report Takeaways

- By equipment type, compressors held a 33.8% share in 2025, while gas turbines are projected to expand at a 3.8% CAGR through 2031.

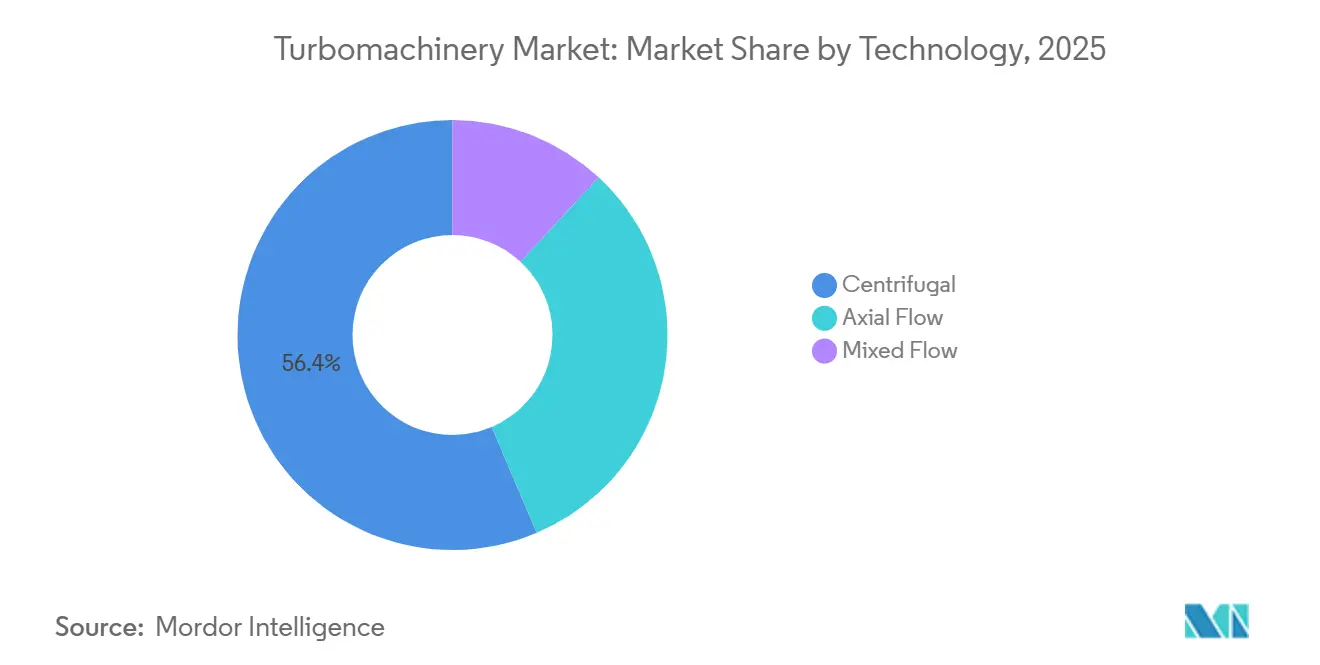

- By technology, centrifugal systems held a 56.4% share in 2025, while mixed flow technology is forecast to grow at a 3.5% CAGR through 2031.

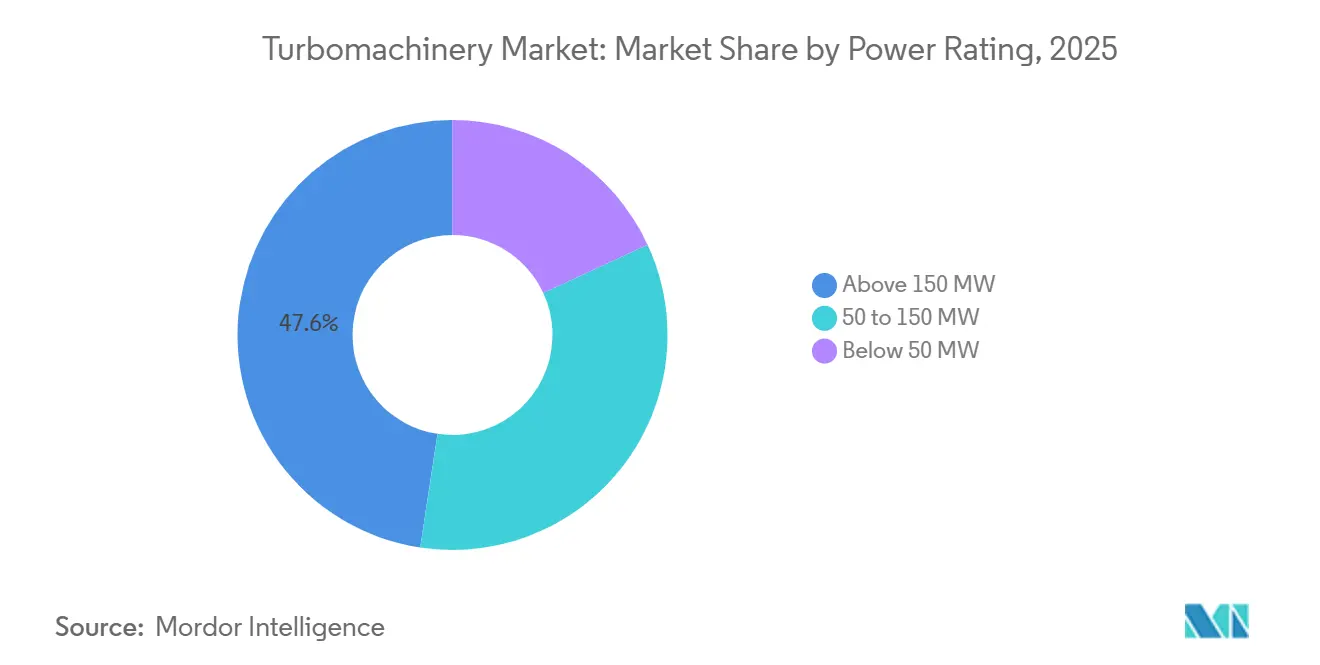

- By power rating, units above 150 MW accounted for a 47.6% share in 2025, while the 50 to 150 MW segment is projected to grow at a 3.6% CAGR through 2031.

- By end-user industry, oil and gas held a 50.8% share in 2025, while power generation is forecast to expand at a 3.9% CAGR through 2031.

- By geography, Asia-Pacific held a 36.5% share in 2025, while the region is projected to advance at a 4.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Turbomachinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG, Refining, and Petrochemical Capacity Additions | +0.6% | Global, concentrated in North America, Middle East, and Asia-Pacific | Medium term (2-4 years) |

| Energy Transition Favors High-Efficiency Rotating Equipment | +0.5% | Global, with acceleration in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Asset-Life Extension Spending Rises as Replacement Cycles Compress | +0.4% | North America, Europe, and Middle East mature basins | Medium term (2-4 years) |

| Electrification Of Compression and Process Trains Supports New OEM Cycles | +0.3% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Digital Twin-Enabled Reliability Programs Expand Service Revenue | +0.2% | Global, with OEM service hubs in North America and Europe | Medium term (2-4 years) |

| Hydrogen-Blend Readiness Spurs Retrofit Cycles | +0.2% | Europe, Japan, and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LNG, Refining, and Petrochemical Capacity Additions Drive Turbomachinery Procurement Queues

The global turbomachinery market continues to benefit from the LNG build cycle that accelerated in 2025. Global LNG supply grew by 38 billion cubic meters in 2025 and is set to expand by another 7% in 2026, with North America accounting for most new supply additions. Each new LNG train requires centrifugal compressors, gas turbine mechanical drives, and related rotating equipment that is ordered well before plant startup. Baker Hughes reinforced this order pattern in March 2026 when it was selected to supply compression and power generation equipment for ST LNG's 8.4 metric tonnes per annum (MTPA) offshore terminal in Texas [2]Source: Baker Hughes, “ST LNG Selects Baker Hughes as Technology Provider for U.S. Offshore LNG Project,” Baker Hughes Investor Relations, investors.bakerhughes.com . Refining and petrochemical expansions add another stream of demand for large compressor packages and support systems. This pipeline of LNG and downstream work keeps oil and gas at the core of the global turbomachinery market and supports multiyear OEM backlogs.

Asset-Life Extension Spending Rises as Replacement Cycles Compress

The installed base across the global turbomachinery market is now old enough that operators increasingly favor major upgrades over full replacement. ORNL documented in 2026 that delivery delays for large-frame gas turbines had stretched to 5 to 7 years because of forging and casting bottlenecks. That delay changes capital decisions, since efficiency upgrades and rotor work can lift output faster than waiting for a new unit. GE Vernova's April 2026 order in Egypt for Advanced Gas Path upgrades on two 9F gas turbines, paired with 8-year and 15-year service agreements, shows how OEMs are monetizing aging fleets [3]Source: GE Vernova, “GE Vernova Secures Order to Modernize Key Power Plants in Egypt,” GE Vernova, gevernova.com . Upgrade programs also help plant owners maintain output and efficiency without reopening full project financing cycles. This service layer gives the global turbomachinery market a steadier revenue base and makes lifecycle capability a stronger competitive differentiator.

Energy Transition Redirects Capital Toward High-Efficiency and Hydrogen-Ready Turbomachinery

The energy transition is shifting the global turbomachinery market toward high-efficiency platforms and fuel-flexible designs. Hydrogen-blend capability is moving from a technical option to a commercial requirement in several power projects. Mitsubishi Heavy Industries detailed ongoing progress toward commercial hydrogen and ammonia gas turbines in its 2025 technical review, with commercial goals set for 2030 [4]Source: Mitsubishi Heavy Industries, “Development and Validation Progress Toward Commercialization of Hydrogen/Ammonia-Fired Gas Turbines,” MHI Technical Review, mhi.com . Mitsubishi Power's January 2026 order for four M701JAC units in Qatar also showed that hydrogen-ready positioning is now part of large project procurement. The Environmental Protection Agency's (EPA's) January 2026 final rule for stationary combustion turbines adds another push for combustion-control and emissions-upgrade spending in the global turbomachinery market. This keeps new-unit demand and retrofit demand active at the same time across the global turbomachinery market.

Data-Center and AI Infrastructure Power Demand Expands Gas Turbine Addressable Market

AI infrastructure is opening a newer demand layer inside the global turbomachinery market. In July 2026, Baker Hughes and Kodiak Gas Services announced a multi-year agreement that will support 1 GW of gas-fired power capacity for U.S. data-center growth by 2030. Baker Hughes also received a February 2026 order for 10 Frame 5 gas turbines that will provide up to 250 MW for data-center projects in Georgia and Texas. These orders show that turbine demand is spreading beyond traditional utility buyers and into private power models. Private generation programs also increase the need for maintenance support, controls, and digital monitoring after installation. As more digital infrastructure sites pursue self-generation, the global turbomachinery market gains added demand for both new units and long-term service support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Project Approval Cycles Delay Order Conversion | -0.4% | North America and Europe, especially permitting-intensive jurisdictions | Medium term (2-4 years) |

| Turbine-Grade Alloy and Casting Bottlenecks Constrain Supply-Side Response | -0.4% | Global, most acute for large-frame units | Short term (≤ 2 years) |

| High Installed-Base Reliability Expectations Suppress Greenfield Velocity | -0.2% | Mature basins including North America, the North Sea, and the Middle East | Medium term (2-4 years) |

| Emissions Policy Uncertainty Can Stall End-User CapEx | -0.2% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Project Approval Cycles Limit Order-to-Delivery Conversion Rates

Long approval cycles still slow the conversion of project plans into booked orders across the global turbomachinery market. LNG, pipeline, and large compression projects often move through environmental and commercial reviews for several years before equipment contracts are released. This lag creates a mismatch between visible demand and near-term order intake, especially in permitting-intensive markets. The EU decision to phase out Russian gas imports by November 2027 increases the need for LNG-linked infrastructure, but it also concentrates project schedules and regulatory review across multiple member states. Developers therefore face tighter windows between project approval and equipment availability. The result is a larger queue of commercially attractive projects that take longer to translate into revenue for suppliers in the global turbomachinery market.

Turbine-Grade Alloy and Casting Bottlenecks Introduce Structural Supply Constraints

Supply-side constraints remain one of the clearest near-term limits on the global turbomachinery market. Oak Ridge National Laboratory (ORNL) identified large rotor forgings, hot-section blades, nickel-based superalloys, and cobalt availability as key bottlenecks behind 5-to-7-year delivery delays for large-frame gas turbines. These shortages make it harder for manufacturers to respond quickly even when end-market demand is strong. The pressure is greatest in equipment classes that depend on precision castings and long qualification cycles. It also raises the value of long-standing supplier relationships and internal process discipline. This environment favors companies with deeper manufacturing relationships and leaves smaller players with less room to scale in the global turbomachinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Compressors Anchored by LNG, Gas Turbines Expanding Fastest

Compressors accounted for 33.8% of the global turbomachinery market size in 2025, which kept them as the largest equipment segment. Their lead reflects steady demand from LNG terminals, gas-processing trains, refinery upgrades, and other continuous-duty applications. The segment also benefits from a wide operating range, from smaller distribution-network units to very large centrifugal trains used in liquefaction. This range gives suppliers exposure to both project work and recurring replacement demand. It also keeps compressors as one of the most stable anchors of the global turbomachinery market.

Gas turbines are projected to grow at a 3.8% CAGR through 2031, which makes them the fastest-growing equipment category in the global turbomachinery market. Demand is rising from power generation, grid-support requirements, and data-center self-generation, alongside traditional oil and gas mechanical-drive use. Steam turbines remain important in power and process-heat recovery applications, while hydraulic turbines and expanders stay more niche. Pumps continue to add volume through water, wastewater, and process industries, even if they do not drive the same order spikes as gas turbines or LNG compressors. Mitsubishi Heavy Industries reported that the global gas turbine market reached 57.4 GW in 2024 and that the first half of 2025 had already reached 41.7 GW, which shows why gas turbines are carrying much of the near-term upside inside the global turbomachinery market.

By Technology: Centrifugal Dominates, Mixed Flow Gains on Compact Power Applications

Centrifugal technology held 56.4% of the global turbomachinery market share in 2025, which made it the dominant technology base. Its position comes from a strong fit across LNG, gas processing, combined-cycle power, and industrial compression duties. OEMs also benefit from a mature centrifugal supply base that supports customization across power classes and pressure ratios. The design is well-suited to continuous-duty service where reliability and operating range matter more than layout novelty. This keeps centrifugal systems at the center of the global turbomachinery market.

Mixed flow technology is forecast to expand at a 3.5% CAGR through 2031, led by compact applications that need high pressure ratios without long axial layouts. These use cases include micro-gas turbines, unmanned aerial vehicle propulsion, and smaller industrial compression systems. A 2025 study in Aerotecnica Missili & Spazio found that vaneless gap optimization in mixed flow compressors extended the stable operating range, which supports broader adoption in demanding duty cycles. Axial flow technology remains important where very high mass flow and strong efficiency are needed, especially in steam turbines and large gas turbine compressor sections. This leaves the global turbomachinery industry with a clear split, where centrifugal systems dominate broad industrial service while mixed flow and axial systems defend more specialized performance needs.

By Power Rating: Above 150 MW Driven by Utility Scale, 50-150 MW Fastest as Grid Flexibility Demands Rise

Units above 150 MW represented 47.6% of the global turbomachinery market size in 2025, which made them the largest power-rating band. Large-frame combined-cycle units and industrial cogeneration blocks keep this category heavily weighted toward high-value projects. Even a limited number of project awards can create strong revenue concentration because individual unit values are so large. The segment also benefits from long service tails once a plant enters operation. This keeps the upper rating band strategically important in the global turbomachinery market.

The 50 to 150 MW segment is projected to advance at a 3.6% CAGR through 2031, supported by data-center power, industrial self-generation, and flexible peaking demand. These units fit projects that need faster ramp rates and shorter interconnection timelines than many large-frame installations. The below 50 MW band remains tied to distributed generation, industrial utilities, and smaller gas-processing compressor drives, which gives it a steady but narrower opportunity. Doosan Enerbility's March 2026 order for two 370 MW-class steam turbines for a North American combined-cycle project shows how power demand is drawing new suppliers into adjacent rating bands. The Environmental Protection Agency's (EPA) 2026 combustion turbine rule may also keep some procurement interest focused on mid-range configurations where compliance burdens can be easier to manage.

By End-User Industry: Oil and Gas Anchors Demand, Power Generation Converges

Oil and gas held 50.8% of the global turbomachinery market share in 2025, which kept it as the largest end-user base. LNG liquefaction, gas-processing compression, offshore Floating Production Storage and Offloading (FPSO) trains, and gas-lift applications continue to create the broadest equipment pull across the global turbomachinery market. Baker Hughes strengthened this position in March 2026 through a 60-month service agreement with Petrobras that covers up to 64 aeroderivative gas turbines across 19 FPSOs and the Replan refinery. The size of the installed base also makes service revenue especially sticky in this part of the global turbomachinery industry. That combination of new-unit demand and fleet support keeps oil and gas deeply embedded in the global turbomachinery market.

Power generation is forecast to grow at a 3.9% CAGR through 2031, which makes it the fastest-growing end-user segment. Data-center demand is widening procurement beyond utilities and bringing more private buyers into turbine ordering cycles. Petrochemical and chemical applications remain steady through compressor demand in crackers, ammonia loops, and air-separation units. Industrial manufacturing, marine, aerospace and defense, mining and metals, and water and wastewater add additional equipment volume even though they carry less strategic weight for OEM revenue mix. Standards such as API 617 and ISO 10816 keep procurement disciplined across major process applications in the global turbomachinery market.

Geography Analysis

Asia-Pacific held 36.5% of the market in 2025 and is projected to grow at a 4.2% CAGR through 2031, which makes it both the largest and fastest-growing regional block in the global turbomachinery market. China is shaping demand through dual-carbon compliance efforts that influence coal retirements and combined-cycle procurement. India is building domestic energy equipment manufacturing capacity, which can improve regional supply depth and future project economics. Southeast Asia adds another layer of demand as coal-to-gas transitions in countries such as Vietnam and Indonesia support new gas-fired capacity. Japan is also pushing hydrogen-linked turbomachinery deployment, and Kawasaki Heavy Industries announced in March 2026 that a next-generation hydrogen fuel supply system for gas turbine power generation had started operation from January 2026.

North America and Europe remain the next largest regional pillars of the global turbomachinery market. The IEA expects the U.S. share of global LNG supply to rise from 25% in 2025 to 33% by the end of the decade, which supports ongoing demand for compression and gas-turbine mechanical drives. North America also benefits from rising private power demand that adds a second equipment stream alongside LNG and pipeline investment. Europe is working through a faster infrastructure timetable because the region plans to phase out Russian gas imports by November 2027. GE Vernova's November 2025 order for two 9HA.01 combined-cycle blocks for Poland's Kozienice power station shows how replacement of coal-fired assets is supporting the regional role of the global turbomachinery market.

The Middle East and Africa remain a high-value zone for large-frame gas turbines, compression systems, and cogeneration equipment in the global turbomachinery market. Mitsubishi Power's January 2026 order for four M701JAC turbines for Qatar's Facility E Independent Water and Power Project (IWPP) added 2.4 GW of capacity and showed the scale of Gulf Cooperation Council (GCC) procurement. South America is building opportunity through offshore and pipeline-linked gas infrastructure, including Baker Hughes' April 2026 order for three NovaLT16 gas turbines and centrifugal compressors for Argentina's San Matias pipeline project. Baker Hughes' June 2026 lifecycle agreement for Nigeria's ANOH plant, which includes Cordant-powered iCenter digital monitoring, shows that African projects are adopting service-integrated solutions rather than stand-alone equipment purchases.

Competitive Landscape

The turbomachinery market is semi-fragmented. GE Vernova, Siemens Energy, and Mitsubishi Power remain the most visible leaders in high-output turbine projects, while the rest of the global turbomachinery market is more fragmented across compressors, pumps, and independent service work. Backlogs are being shaped as much by foundry and forging limits as by sales activity, which gives scale and manufacturing access more strategic value. This setting allows established OEMs to defend pricing, prioritize preferred customers, and attach service agreements more consistently. It also means competitive position depends on delivery credibility, installed-base reach, and fuel-flexibility claims as much as on unit efficiency.

Lifecycle services have become one of the clearest sources of advantage in the global turbomachinery market. Baker Hughes' March 2026 Petrobras agreement covering up to 64 aeroderivative turbines shows how a single customer relationship can support multiyear service revenue at fleet scale. GE Vernova's April 2026 upgrade order in Egypt shows a similar approach, with hardware modernization paired to long-term support contracts. Baker Hughes' June 2026 ANOH agreement adds digital monitoring to the service model, which deepens customer dependence after installation. These moves show that competitive strength in the global turbomachinery market increasingly comes from lifecycle depth rather than equipment sales alone.

The global turbomachinery market still leaves room for challengers when they target specific product gaps or regional openings. Doosan Enerbility's first North American steam turbine order in March 2026 shows that suppliers outside the established top tier can still enter adjacent spaces where customers want another qualified source. Hydrogen-ready designs, combustion upgrades, and digital service layers are widening the points on which suppliers can differentiate. Even so, the global turbomachinery market remains more concentrated in very large turbine platforms than it is in compression, pumps, and field services.

Turbomachinery Industry Leaders

Siemens Energy AG

General Electric Company

Mitsubishi Heavy Industries, Ltd.

Everllence SE

Baker Hughes Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Baker Hughes and Kodiak Gas Services announced a multi-year strategic agreement for NovaLT™16 and Frame 5 gas turbines plus generators, enabling 1 GW of power generation capacity by 2030 to serve U.S. data-center demand.

- June 2026: Baker Hughes was awarded a long-term lifecycle service agreement covering two NovaLT™16 gas turbines with Cordant™-powered iCenter™ digital monitoring at the greenfield ANOH Gas Processing Plant in Nigeria.

- April 2026: Baker Hughes secured its first NovaLT™16 deployment in South America, three gas turbines with centrifugal compressors, for a pipeline project transporting Vaca Muerta gas to floating LNG vessels off Argentina's Rio Negro coast.

- April 2026: GE Vernova received a Q1 2026 order from Middle Delta Electricity Production Company for AGP upgrades on two 9F gas turbines at Banha, plus 15-year and 8-year service agreements for Banha and Nubaria power plants, with upgrades expected to improve efficiency by 2%.

Global Turbomachinery Market Report Scope

Turbomachinery refers to rotating mechanical equipment that exchanges energy with a continuously flowing fluid through rotating blades or impellers. It includes power-generating machines such as gas, steam, and hydraulic turbines, as well as power-absorbing machines such as compressors, pumps, expanders, fans, and blowers. Turbomachinery is widely used across power generation, oil & gas, industrial manufacturing, water treatment, aerospace, and HVAC applications due to its ability to efficiently convert and transfer energy between fluids and mechanical systems.

The turbomachinery market is segmented by equipment type, technology, power rating, end-user, and geography. By equipment type, the market is segmented into compressors, gas turbines, steam turbines, expanders, pumps, and other turbomachinery. By technology, the market is segmented into axial flow, centrifugal, and mixed flow. By power rating, the market is segmented into below 50 MW, 50–150 MW, and above 150 MW. By end-user, the market is segmented into oil and gas, power generation, petrochemical, industrial, aerospace, marine, mining, and water. The report also covers the market size and forecasts for the global turbomachinery market across 23 countries in the major regions. For each segment, the market sizing and forecasts have been provided on the basis of value (USD).

| Compressors |

| Gas Turbines |

| Steam Turbines |

| Hydraulic Turbines |

| Expanders |

| Pumps |

| Other Turbomachinery |

| Axial Flow |

| Centrifugal |

| Mixed Flow |

| Below 50 MW |

| 50 to 150 MW |

| Above 150 MW |

| Oil and Gas |

| Power Generation |

| Petrochemical and Chemical |

| Industrial Manufacturing |

| Aerospace and Defense |

| Marine |

| Mining and Metals |

| Water and Wastewater |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Africa | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Equipment Type | Compressors | |

| Gas Turbines | ||

| Steam Turbines | ||

| Hydraulic Turbines | ||

| Expanders | ||

| Pumps | ||

| Other Turbomachinery | ||

| By Technology | Axial Flow | |

| Centrifugal | ||

| Mixed Flow | ||

| By Power Rating | Below 50 MW | |

| 50 to 150 MW | ||

| Above 150 MW | ||

| By End-User Industry | Oil and Gas | |

| Power Generation | ||

| Petrochemical and Chemical | ||

| Industrial Manufacturing | ||

| Aerospace and Defense | ||

| Marine | ||

| Mining and Metals | ||

| Water and Wastewater | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Africa | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global turbomachinery market by 2031?

The global turbomachinery market is projected to reach USD 31.45 billion by 2031, rising from USD 28.37 billion in 2026 at a 2.08% CAGR.

Which equipment category leads revenue today?

Compressors led with a 33.8% share in 2025 because LNG, gas processing, and refinery upgrades continue to generate broad and recurring demand.

Why are gas turbines growing faster than the overall space?

Gas turbines are forecast to grow at a 3.8% CAGR through 2031, supported by power generation demand, data-center self-generation, and grid-support needs.

Which end-user group contributes the most demand?

Oil and gas remained the largest end-user segment with a 50.8% share in 2025, driven by LNG, offshore production, gas processing, and related service contracts.

Which region is expected to grow fastest through 2031?

Asia-Pacific is both the largest regional segment and the fastest-growing one, with a 36.5% share in 2025 and a projected 4.2% CAGR through 2031.

How are service agreements shaping supplier competition?

Long-term service deals are becoming a major differentiator, as shown by Baker Hughes in Petrobras and Assa North Ohaji South (ANOH), and GE Vernova in Egypt, because they lock in recurring revenue beyond initial equipment sales.

Page last updated on: