Sulphur Coated Urea Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

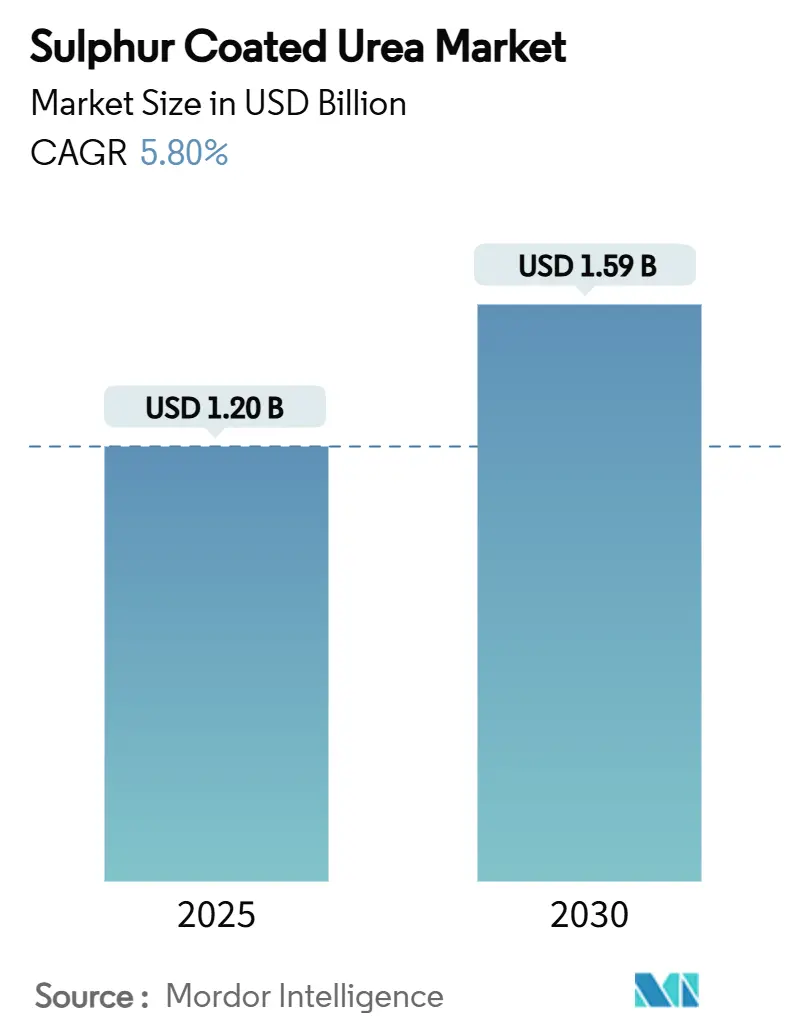

| Market Size (2025) | USD 1.20 Billion |

| Market Size (2030) | USD 1.59 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

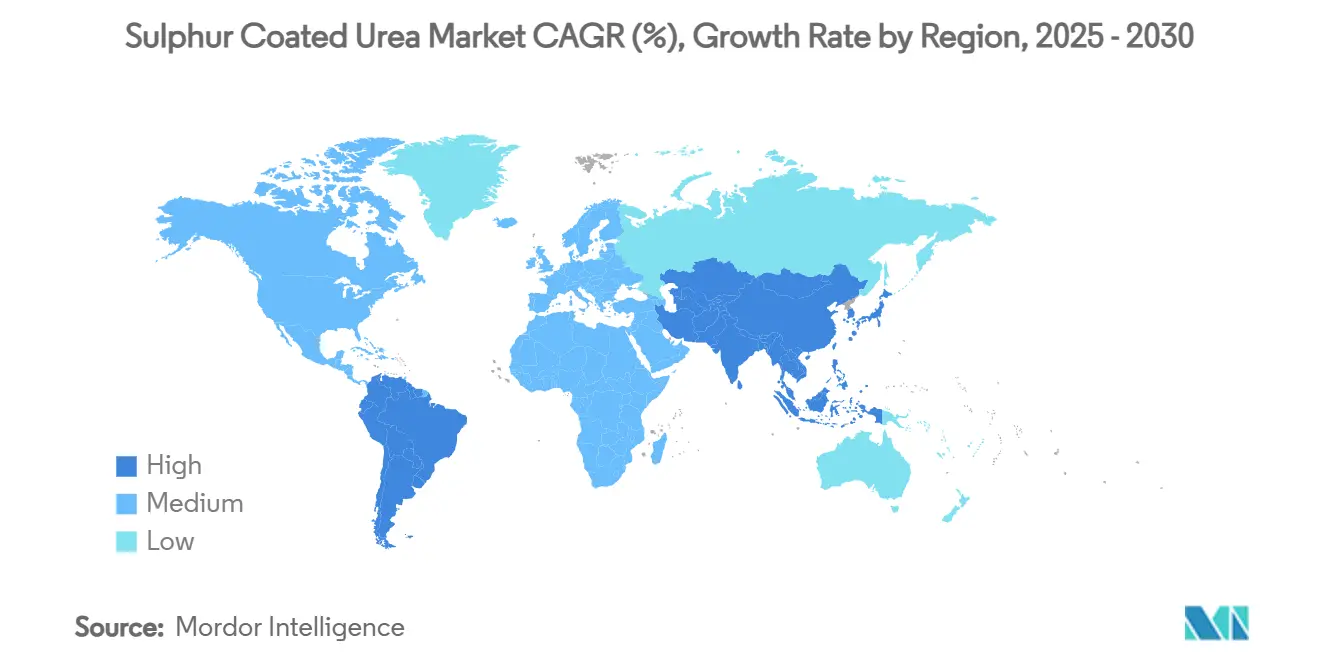

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulphur Coated Urea Market Analysis by Mordor Intelligence

The sulfur-coated urea market size is estimated at USD 1.20 billion in 2025 and is projected to reach USD 1.59 billion by 2030, growing at a 5.8% CAGR. The upward trajectory reflects agriculture’s shift from volume-driven to efficiency-driven nutrient strategies, as growers align nitrogen release with crop uptake windows rather than relying on calendar-based applications. Environmental mandates, the monetization of carbon credits, and the rising adoption of precision agriculture collectively encourage large farms, turf managers, and specialty crop producers to upgrade from conventional urea to controlled-release formulations. Regulatory actions, such as the European Union’s microplastic restrictions and Canada’s 30% reduction target for fertilizer emissions, remove lower-cost polymer-coated options from the market, thereby funneling demand toward sulfur-based coatings[1]Source: European Commission, “Regulation 2023/2055,” eur-lex.europa.eu. Competitive intensity remains pronounced, as regional suppliers continue to expand beyond their home markets. However, the top five players still captured the majority of the revenue share in 2024, signaling moderate concentration.

Key Report Takeaways

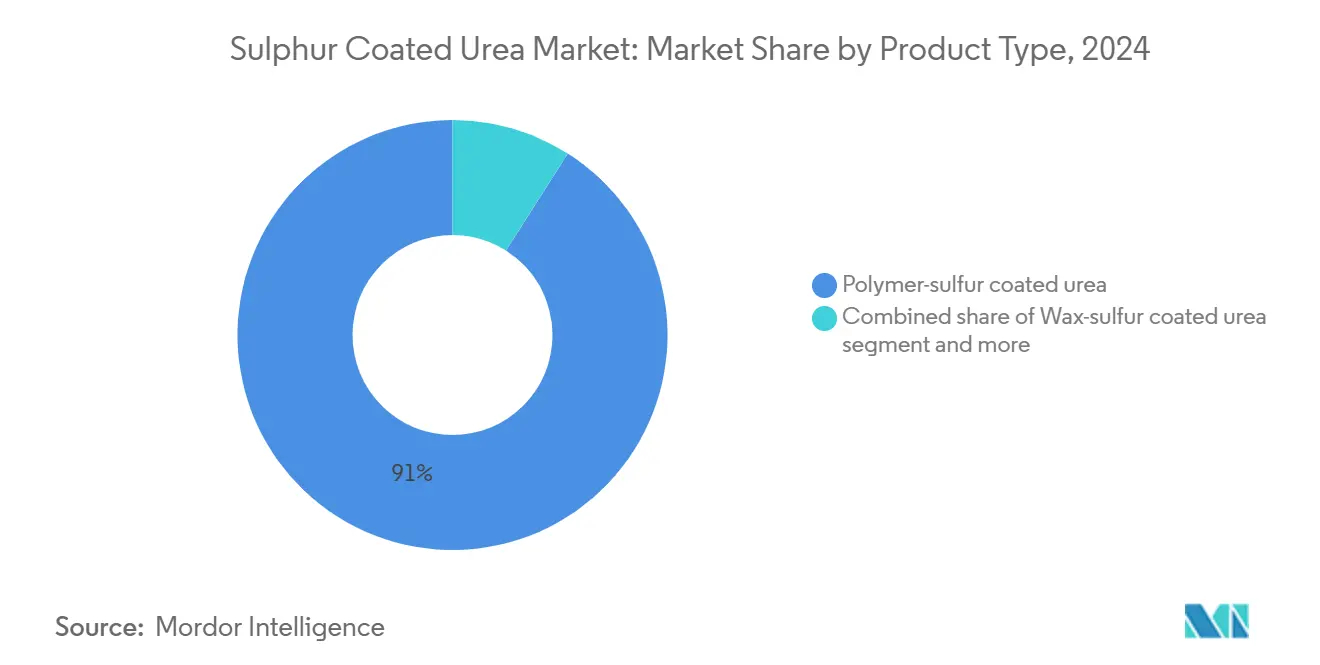

- By product type, polymer-sulfur coated urea held 91% of the sulfur-coated urea market share in 2024, and the wax-sulfur coated urea formulations are projected to rise at a 7.8% CAGR through 2030.

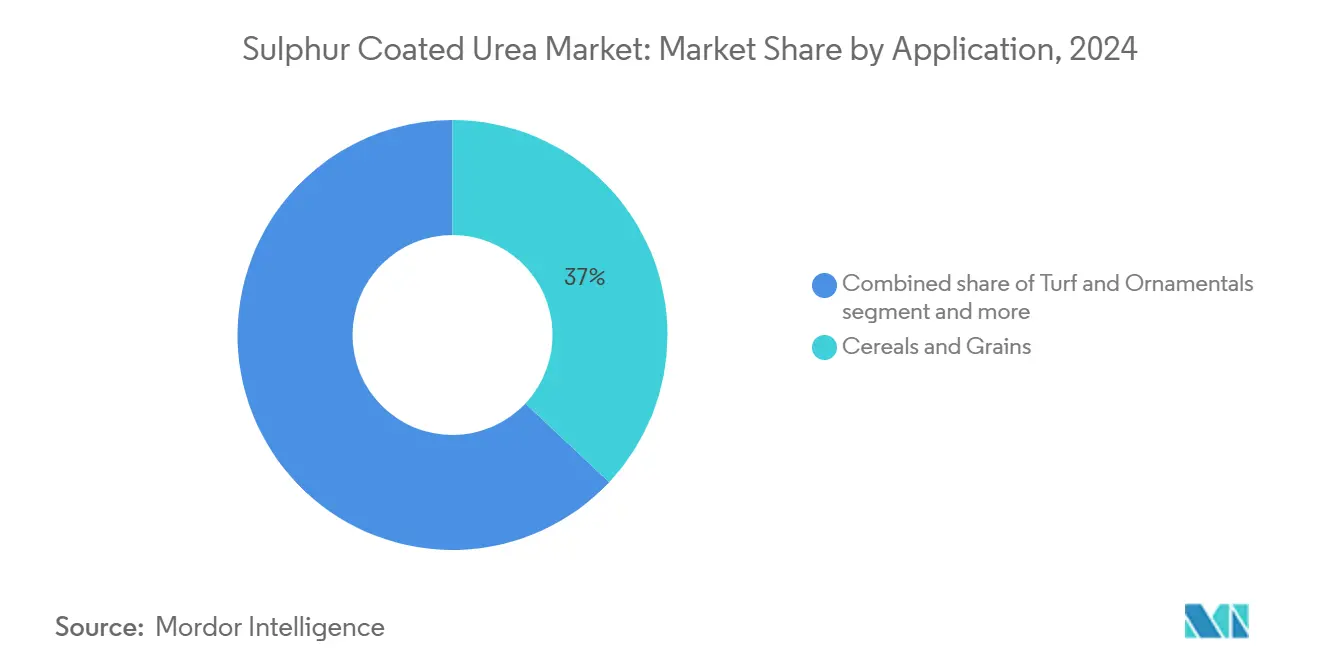

- By application, cereals and grains led with a 37% contribution to the sulfur-coated urea market size in 2024, while turf and ornamentals are advancing at an 8.5% CAGR to 2030.

- By geography, North America accounted for 34% of 2024 revenue; however, the Asia-Pacific region shows the highest regional CAGR at 6.9% through 2030.

- The top five companies, including Nutrien Ltd., Yara International ASA, and The Mosaic Company, collectively commanded a majority share of the sulfur-coated urea market in 2024.

Global Sulphur Coated Urea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for enhanced-efficiency fertilizers | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Precision-agriculture adoption raises demand for controlled-release inputs | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Turf and ornamental industry’s shift to low-leaching nitrogen sources | +0.7% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of sulfur recovery from refineries ensures feedstock availability | +0.6% | Global, concentrated in refining regions | Medium term (2-4 years) |

| Declining micro-encapsulation costs improve product economics | +0.5% | Global, led by bio-based polymer innovations | Long term (≥ 4 years) |

| Carbon-credit monetization for reduced nitrous-oxide emissions | +0.4% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Enhanced-Efficiency Fertilizers

Governments now treat environmental compliance as a path to competitive advantage. The European Union’s Fertilizer Products Regulation introduces labeling and performance standards that deter low-grade coatings and favor proven sulfur-based technologies. In Canada, the federal goal of cutting fertilizer greenhouse-gas emissions 30% by 2030 reframes sulfur-coated urea as a compliance instrument rather than a premium input[2]Source: The Grower, “High-efficiency, slow-release fertilizers are being developed,” thegrower.org. Commodity groups such as the Saskatchewan Wheat Development Commission publicly endorse enhanced-efficiency nitrogen, signaling mainstream acceptance among growers[3]Source: Saskatchewan Wheat Development Commission, “Enhanced efficiency nitrogen fertilizers,” saskwheat.ca. Together, these actions lock in baseline demand growth and encourage research and development investment across the sulfur-coated urea market.

Precision-Agriculture Adoption Raises Demand for Controlled-Release Inputs

Variable-rate technology (VRT) has moved beyond early adopter farms because investment payback periods now stand at 2 to 5 years per Australian case study. Consultancies estimate fertilizer volumes could decline 5% by 2040 under widespread VRT, but the reduction largely targets conventional urea, not controlled-release forms. Sulfur-coated formulations deliver predictable release curves that align with zone-specific nutrient prescriptions, making them indispensable within precision-agriculture programs. The combination between precision hardware and controlled-release chemistry is accelerating adoption across large-acreage row-crop farms in the United States and Europe.

Turf and Ornamental Industry’s Shift to Low-Leaching Nitrogen Sources

Golf courses cut overall nitrogen use 41% between 2006 and 2025, but demand for slow-release nitrogen remained intact because superintendents need season-long feeding with minimal leaching. Sports-turf managers prefer sulfur-coated urea due to steadier growth patterns that translate into smoother playing surfaces and reduced mowing frequencies. As public pressure grows to protect groundwater, municipalities increasingly restrict quick-release nitrogen, tilting procurement toward controlled-release products. This preference supports premium pricing and stabilizes margins in the sulfur-coated urea market.

Expansion of Sulfur Recovery from Refineries Ensures Feedstock Availability

United States refiners boosted elemental-sulfur recovery 72% over the past decade and now extract more than half of the sulfur contained in crude oil. Modern Claus process upgrades raise recovery efficiencies above 99%. More stable sulfur output lowers raw-material price volatility, enabling fertilizer manufacturers to plan multi-year coating expansions. The recent tariffs on Canadian sulfur imports into the United States (25% on 850,000 tons a year) highlight ongoing supply-chain risk. Companies with diversified sourcing stand to gain market share during supply disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premium versus conventional urea limits adoption in emerging markets | −0.8% | Asia-Pacific, Africa, South America | Short term (≤ 2 years) |

| Volatile elemental-sulfur supply tied to oil and gas cycles | −0.6% | Global, concentrated in import-dependent regions | Medium term (2-4 years) |

| Looming micro-plastic restrictions on polymer coatings | −0.4% | Europe, expanding to North America | Long term (≥ 4 years) |

| Limited compatibility with fertigated irrigation systems | −0.3% | Mediterranean, Middle East, water-scarce regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Premium Versus Conventional Urea Limits Adoption in Emerging Markets

In price-sensitive regions, sulfur-coated urea can cost two to three times more than granular urea, curbing uptake among smallholders who operate on narrow margins. Heavy subsidies on conventional fertilizers in India dilute price signals, discouraging farmers from switching despite balanced-nutrient policies. Chinese growers apply fertilizers at 298.79 kg per hectare, 1.33 times above safety benchmarks, yet still favor cheaper inputs over controlled-release options. Unless manufacturing scale lowers costs or bundled advisory services prove yield benefits, adoption in emerging markets will lag.

Volatile Elemental-Sulfur Supply Tied to Oil and Gas Cycles

European sulfur shortages triggered a 50% price hike in 2024 to EUR 158.5-174.5 per ton (USD 172-189 per ton) due to refinery downtime and sweeter crude slates. North American tariffs on Canadian sulfur amplify risks for producers without diversified feedstock. The sulfur-coated urea industry, therefore, sees margin pressure or must hold larger inventories during oil-price swings, complicating long-term contracts with distributors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polymer-Sulfur Coated Urea Dominance Faces Wax-Based Disruption

Polymer-sulfur-coated urea formulations captured 91% of the sulfur-coated urea market share in 2024, leveraging established manufacturing lines and field-proven release profiles. Wax-sulfur-coated urea is growing at the fastest rate, with a 7.8% CAGR, as bio-wax blends meet microplastic regulations without compromising performance. Plant-oil polyurethane shells and starch hybrids further erode the price-performance gap versus legacy polymers, encouraging product line expansions among majors and mid-sized regional players[4]Source: Journal of Plant Nutrition and Fertilizers, “Plant oil-based polyurethane coated fertilizer,” plantnutrifert.org.

The “Others” category (resin blends and metal-organic frameworks) held a limited share in 2024, but it functions as a research and development sandbox where firms pilot next-generation, fully biodegradable coatings. While these novel encapsulants improve the uniformity of nutrient release, production costs remain high due to limited scale, which restrains their commercial rollout[5]Source: European Commission, “Commission Regulation 2023/2055,” eur-lex.europa.eu . Over the forecast horizon, polymer-sulfur products will continue to dictate pricing benchmarks; however, accelerated regulatory timelines could enable wax-based entrants to approach a significant sulfur-coated urea market share by 2030.

By Application: Cereals Drive Volume While Turf Commands Premium

Cereals and grains absorbed 37% of global demand in 2024. Adoption is strongest in corn and wheat systems that benefit from synchronized nitrogen release, reducing volatilization and leaching losses while sustaining yields. Farmers in the United States Corn Belt and Western Canada increasingly blend sulfur-coated urea with commodity urea to balance early-season and late-season nitrogen supply, spreading cost premiums across the fertilization calendar.

Turf and ornamentals represent the fastest expanding end use, advancing at an 8.5% CAGR. Golf course managers in North America view season-long, steady growth as essential to playability and aesthetics, supporting a price premium that can exceed 40% over conventional urea. Fruit and vegetable applications are also growing because controlled-release formulations minimize fertilizer burn and enhance quality grades, which are critical to export markets where cosmetic standards dictate pricing. Oilseeds and pulses command a limited share, primarily in Brazil and Canada, where producers target nitrogen-use efficiency to comply with new greenhouse-gas protocols embedded in carbon-credit programs.

Geography Analysis

North America dominated the sulfur-coated urea market with 34% revenue share in 2024, led by large cereal acreages and substantial turfgrass sectors. Precision agriculture penetration reaches 70% of corn and soybean hectares, aligning with controlled-release uptake in states such as Iowa and Illinois. Implementation of carbon-reduction credit programs further entrenches demand. Supply risks remain, as 25% tariffs on Canadian sulfur imports can inflate feedstock costs and squeeze producer margins in the United States.

Asia-Pacific is the fastest-growing region with a 6.9% CAGR through 2030. China’s tightening nutrient discharge rules and subsidy reform reinforce the shift from bulk urea to enhanced-efficiency fertilizers. India’s Fertilizer Subsidy Scheme revisions encourage balanced NPK use, although high sulfur-coated urea premiums temper near-term adoption. Southeast Asian nations are trialing controlled-release products in oil-palm and rubber plantations to mitigate leaching on high rainfall soils, opening fresh revenue pools for global suppliers.

Europe captured a prominent share of the 2024 revenue after North America, but faces sulfur supply shortages that raise manufacturing costs. New European Union rules phasing out non-biodegradable polymer coatings will likely accelerate product reformulation toward wax-sulfur blends, requiring rapid capital expenditure from producers. South America is forecasted to show a significant CAGR, driven by the expansion of Brazilian soybean and corn acreage, as well as aggressive low-carbon fertilizer projects, such as the USD 1 billion Durango plant planned in Mexico. Middle East and Africa remain nascent but hold upside as governments promote desert agriculture using precision drip irrigation, provided manufacturers deliver fertigation-compatible controlled-release formulations.

Competitive Landscape

The sulfur-coated urea industry exhibits moderate consolidation, with the top producers capturing the majority of the 2024 revenue, led by Nutrien Ltd., Yara International ASA, and The Mosaic Company. Nutrien Ltd. leverages its integrated ammonia, sulfur, and distribution assets, all reinforced by a USD 2 billion clean-ammonia facility slated to start up in 2027 in Louisiana. Yara International ASA continues to invest in digital agronomy platforms that bundle controlled-release fertilizers with decision-support tools, differentiating itself on service rather than solely on product chemistry. The Mosaic Company pivots toward strategic partnerships in South America to secure distribution amid rising regional demand.

Research and development intensity is rising as firms pursue biodegradable coatings to comply with upcoming microplastic bans. Nutrien’s memorandum with CoteX Technologies illustrates a partnership model that accesses novel polymer science without incurring prolonged in-house development costs. Chinese incumbents Kingenta Ecological Engineering Co., Ltd. and Hubei Yihua Chemical Industry Co., Ltd. exploit lower production costs to target export markets, often via licensing deals that grant access to Western distribution. Patent filings around bio-based encapsulants and metal-organic frameworks surged 22% between 2023 and 2024, indicating a technology arms race that may redraw competitive boundaries over the next five years.

Regional supply security continues to influence competitive dynamics. Producers with captive sulfur streams from refineries or natural-gas operations enjoy margin stability when sulfur prices spike. In contrast, merchant buyers face cost shocks, prompting discussions of long-term offtake agreements and regional hedging strategies. Strategic moves also involve downstream integration, such as CF Industries Holdings Inc. collaborating with POET LLC to showcase low-carbon ammonia use in ethanol-linked corn production, thus expanding the addressable controlled-release fertilizer market.

Sulphur Coated Urea Industry Leaders

Nutrien Ltd.

Yara International ASA

The Mosaic Company

ICL Group Ltd.

Koch Fertilizer LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fermaca Dreams announced a USD 1 billion investment in a green fertilizer plant in Durango, Mexico, targeting 600,000 metric tons of annual urea output.

- July 2024: NEXTCHEM received a pre-FEED contract for FertigHy’s 500,000-ton low-carbon fertilizer plant. The project broadens Europe’s pipeline of lower-emission nitrogen sources that can be further enhanced through sulfur coating, aligning with continental emission-reduction mandates and sustaining demand for controlled-release products.

- November 2023: Nutrien and CoteX Technologies entered a memorandum of understanding to commercialize biodegradable coating technology for nitrogen fertilizers.

Global Sulphur Coated Urea Market Report Scope

| Polymer-sulfur coated urea |

| Wax-sulfur coated urea |

| Others |

| Cereals and grains |

| Oilseeds and pulses |

| Fruits and vegetables |

| Turf and ornamentals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Polymer-sulfur coated urea | |

| Wax-sulfur coated urea | ||

| Others | ||

| By Application | Cereals and grains | |

| Oilseeds and pulses | ||

| Fruits and vegetables | ||

| Turf and ornamentals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the sulfur-coated urea market?

The sulfur-coated urea market size is USD 1.20 billion in 2025 and is projected to reach USD 1.59 billion by 2030, growing at a 5.8% CAGR.

Which product type holds the largest share?

Polymer-sulfur coated urea dominates with 91% market share in 2024, driven by established manufacturing scale and reliable nutrient-release profiles.

Why is Asia-Pacific the fastest-growing region?

Regulatory pressure to cut fertilizer losses in China and balanced-nutrient policies in India are pushing adoption, resulting in a 6.9% CAGR for the region through 2030.

How do carbon credits influence adoption?

Programs from the American Carbon Registry and other bodies allow farmers to monetize nitrous-oxide reductions, offsetting premium prices for controlled-release fertilizers and spurring demand growth.

What challenges could slow market expansion?

High price premiums versus conventional urea, volatile sulfur feedstock supply, microplastic regulations, and incompatibility with some fertigation systems can all restrain uptake in specific geographies.

Which companies lead the competitive landscape?

Nutrien Ltd., Yara International ASA, and Mosaic Company collectively commanded a 46.2% sulfur-coated urea market share during 2024, benefiting from integrated supply chains and active R&D into biodegradable coatings.

Page last updated on: