Styrene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

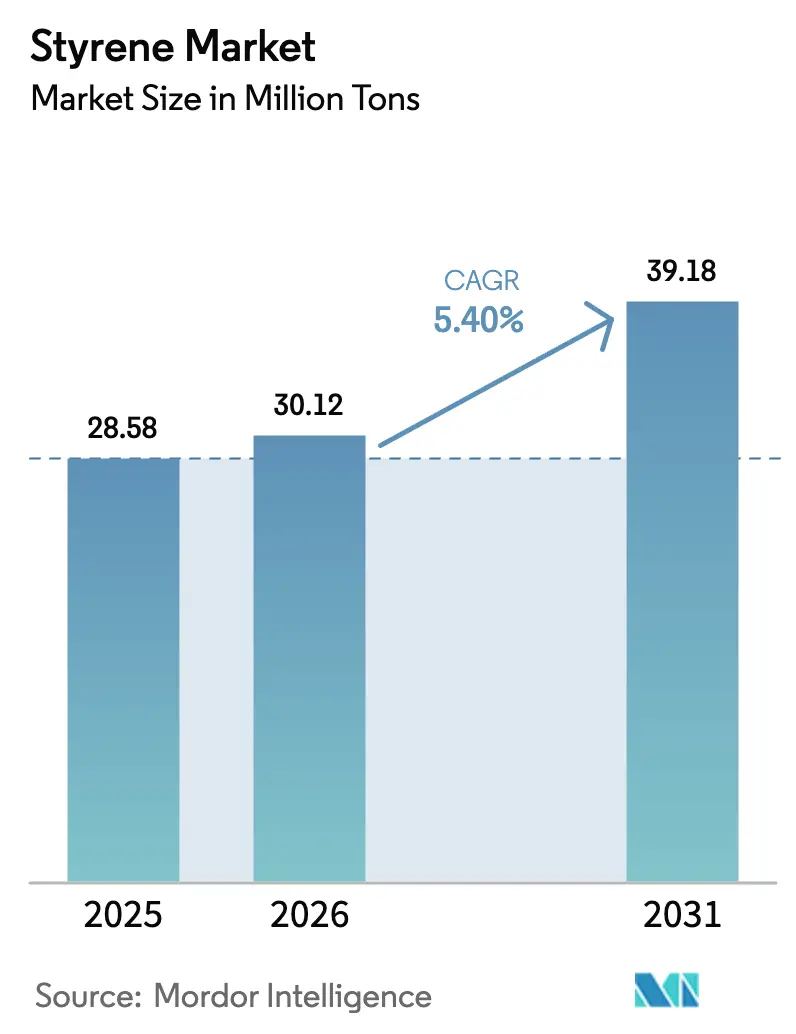

| Market Volume (2026) | 30.12 Million tons |

| Market Volume (2031) | 39.18 Million tons |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Styrene Market Analysis by Mordor Intelligence

The Styrene Market size is expected to increase from 28.58 million tons in 2025 to 30.12 million tons in 2026 and reach 39.18 million tons by 2031, growing at a CAGR of 5.40% over 2026-2031. Demand momentum persists even as single-use plastic bans, feedstock volatility, and carbon-pricing schemes reshape cost curves. Packaging retains structural importance for rigid clamshells and foam cushioning, while automotive electrification is accelerating acrylonitrile-butadiene-styrene uptake for battery enclosures and interior substrates. Breakthrough chemical-recycling deployments in Europe and North America are beginning to supply food-contact-grade monomer, enabling brand owners to meet recycled-content mandates without sacrificing performance. Asia-Pacific dominates capacity additions, yet margin leadership is migrating toward Western producers that commercialize circular solutions under FDA and EU approvals. Competitive strategies are therefore bifurcating between volume-driven integrated complexes and specialty players that monetize certifications and technical service.

Key Report Takeaways

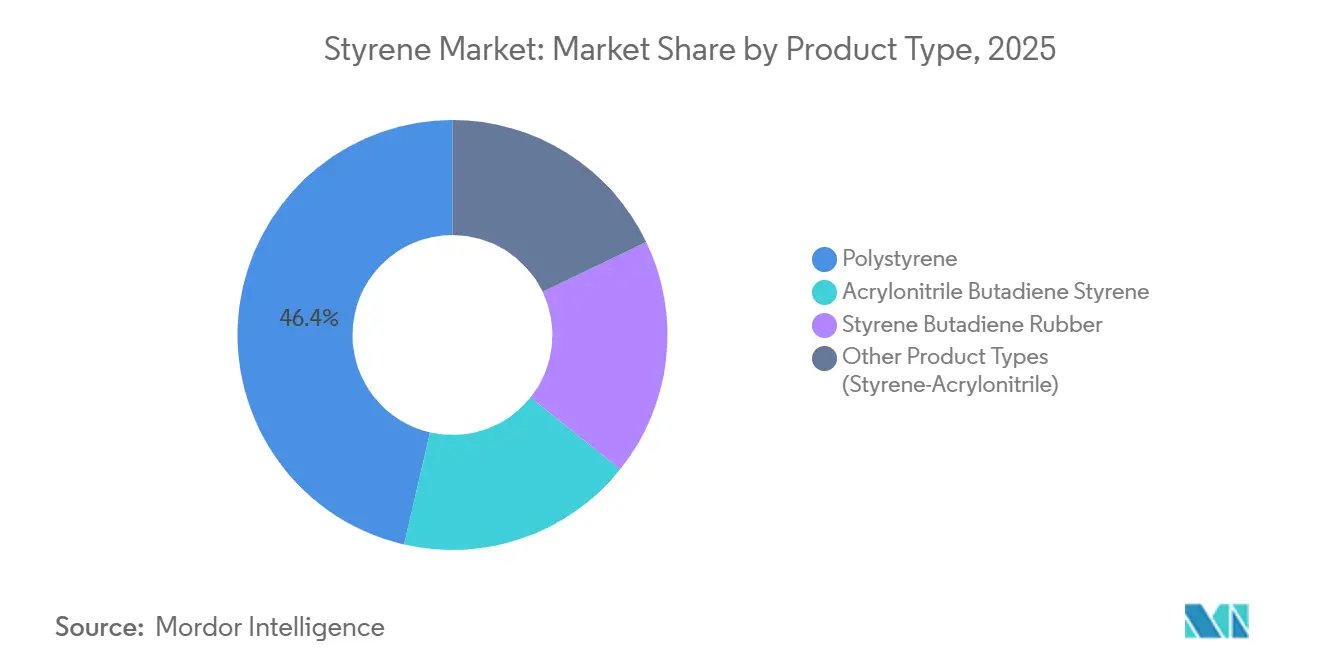

- By product type, polystyrene led with 46.38% of the styrene market share in 2025, and acrylonitrile-butadiene-styrene (ABS) is projected to grow at a 6.18% CAGR through 2031.

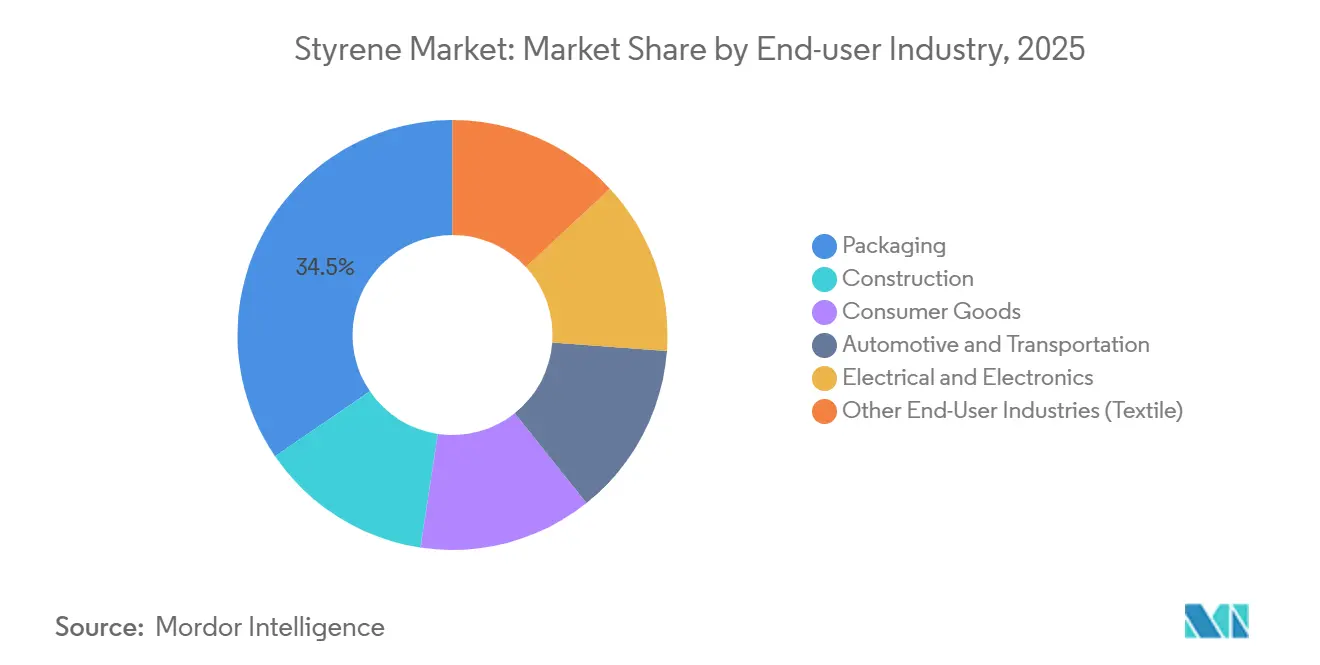

- By end-user industry, packaging absorbed 34.52% of 2025 demand, yet automotive and transportation is advancing at a 6.24% CAGR through 2031.

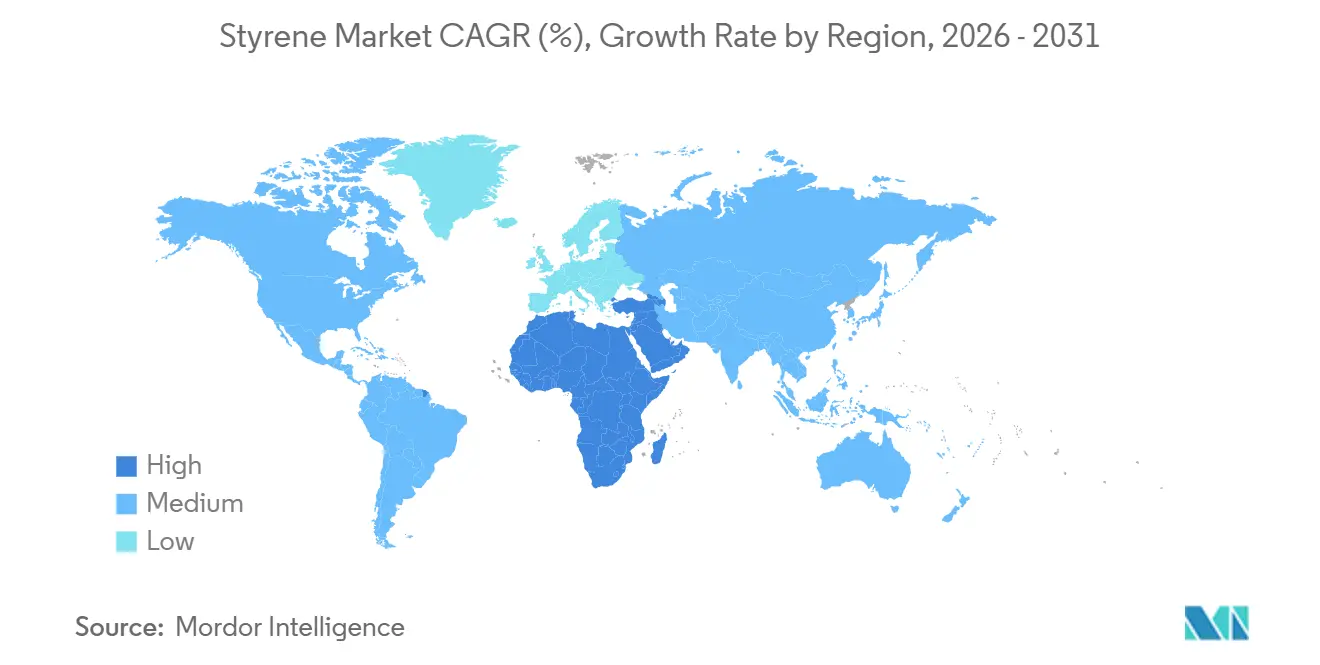

- By geography, Asia-Pacific accounted for 49.27% of 2025 consumption, while the Middle East and Africa is the fastest growing region at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Styrene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight, rigid packaging | +1.2% | Global, with EU and North America leading recycled-content adoption | Medium term (2-4 years) |

| Booming consumer-electronics housing demand | +0.9% | APAC core (China, South Korea, Vietnam), spill-over to North America | Short term (≤ 2 years) |

| Insulation push from net-zero construction codes | +1.1% | EU (EPBD 2024 compliance), North America (building-code updates), China (green-building standards) | Long term (≥ 4 years) |

| Automotive lightweighting for EV range extension | +1.3% | Global, concentrated in China, EU, and North America EV hubs | Medium term (2-4 years) |

| Breakthrough chemical-recycling capacity build-out | +0.8% | EU and North America (food-contact regulatory approval), pilot deployments in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight, Rigid Packaging

Rigid polystyrene clamshells deliver clarity and stiffness that polyethylene and polypropylene alternatives struggle to match at comparable thickness. The EU Packaging and Packaging Waste Regulation 2025/40 sets 35% recycled content by 2030 and 65% by 2040, pushing converters toward mechanically recycled polystyrene for non-food uses and chemically recycled monomer for food-contact items. INEOS Styrolution obtained U.S. FDA Food Contact Notification 2245 for pyrolysis-derived styrene, clearing the way for yogurt cups and bakery trays to meet brand targets without compromising drop-impact resistance [1]U.S. Food and Drug Administration, “Food Contact Notification 2245,” fda.gov . Agilyx’s TruStyrenyx facility completed engineering for a 100 ton-per-day depolymerization line, although final investment hinges on offtake agreements. While pyrolysis achieves more than 90% monomer purity, feedstock collection remains the bottleneck, keeping recyclers' operating rates below nameplate in most regions.

Booming Consumer-Electronics Housing Demand

Global AI-capable PC shipments are projected at 114 million units in 2025, each incorporating 150-200 grams of flame-retardant ABS for internal structures. Hyperscale operators specify UV-stabilized acrylonitrile-styrene-acrylate copolymers for 5G base-station enclosures that must endure 10-year outdoor exposure without chalking. Samsung’s Galaxy S24 family, launched January 2024, continues to rely on virgin ABS for brackets where dimensional tolerances below ±0.05 millimeters are mandatory. Supply of high-heat ABS from LG Chem and CHIMEI is tight, compelling electronics OEMs to dual-source from China despite variability in melt-flow index specifications.

Insulation Push from Net-Zero Construction Codes

The EU Energy Performance of Buildings Directive 2024/1275 requires zero on-site emissions for new buildings by 2026 and mandates life-cycle global-warming-potential disclosure from 2028. Expandable and extruded polystyrene boards achieve lambda values of 0.030-0.038 W/mK, matching polyisocyanurate foam at lower installed cost. BASF lifted Neopor EPS capacity by 50,000 tons per year at Ludwigshafen in 2024 to address Germany’s retrofit wave. Bio-attributed feedstock under the Biomass Balance approach cuts cradle-to-gate CO₂ by up to 50%, helping converters pre-qualify for public-sector tenders that now request ISO 14067 footprints.

Automotive Lightweighting for EV Range Extension

Battery packs add 200-300 kilograms to electric vehicles, and glass-fiber-reinforced ABS battery-tray covers weigh 40% less than stamped steel while meeting tensile strengths of 80-120 MPa. BASF and SABIC compete with higher-cost polyamide and polyphenylene-ether blends, but ABS maintains a unit-cost edge of EUR 2.20-2.50 per kilogram versus EUR 3.50-4.00 per kilogram. Covestro supplies UL 94 V-0 ABS for Chinese EV interiors following 2024 GB 38900 updates. SAE J2807, published in 2024, standardized thermoplastic battery-housing tests, shortening qualification cycles and encouraging metal substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use PS and EPS bans in more than 130 nations | -0.9% | Global, most stringent in EU, Canada, select U.S. states, and coastal developing economies | Short term (≤ 2 years) |

| Feedstock (benzene/ethylene) price volatility | -0.6% | Global, acute in import-dependent regions (Southeast Asia, Middle East) | Short term (≤ 2 years) |

| EU carbon-border tariffs on high-energy polymers | -0.4% | EU imports from non-ETS jurisdictions (China, India, Middle East) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Use PS and EPS Bans in More Than 130 Nations

The EU Packaging and Packaging Waste Regulation bans single-use EPS foodware from January 2029 for dine-in and January 2030 for takeaway, eliminating 180,000 tons of regional demand. New York and California restrictions remove another 35,000-40,000 tons in the United States, while Canada’s nationwide ban came into force in 2024[2]Government of Canada, “Single-Use Plastics Prohibition Regulations,” canada.ca . Quick-service restaurants migrate to molded-fiber pulp or polypropylene, raising costs 10-15% yet reducing marine-litter exposure. Small extruders lacking capital to retool are selling assets to larger converters, accelerating consolidation.

Feedstock (Benzene/Ethylene) Price Volatility

U.S. ethane crackers generate ethylene at USD 250-300 per ton, versus EUR 600-700 from European naphtha crackers, sustaining a 15-20% cash-cost gap. Forward curves show benzene contango into 2027, suggesting tighter aromatics supply as gasoline demand eases, yet margin visibility remains poor for non-integrated players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Recycling Unlocks Value Amid Regulatory Pressure

Polystyrene commanded 46.38% of 2025 volume, though its growth is projected below the overall styrene market CAGR due to food-service bans. The chemical-recycling pivot is critical; Trinseo and Recycling Technologies now convert 30,000 tons per year of post-consumer material into virgin-equivalent monomer that qualifies under EU Regulation 10/2011 and FDA FCN 2245. Acrylonitrile-butadiene-styrene heads the expansion table at a 6.18% CAGR, supported by electric-vehicle battery trays and 5G equipment housings that require UL 94 V-0 compliance. Specialty ABS grades from BASF and SABIC achieve 25-30% part-weight savings versus metal substitutes. Commodity general-purpose polystyrene faces margin compression from 1.45 million tons per year of new Chinese capacity commissioned in 2023-2024.

Recycled monomer validation by INEOS Styrolution in September 2025 demonstrates circular viability, yet collection and sorting costs of USD 150-200 per ton continue to suppress operating margins. Styrene-acrylonitrile copolymers grow in line with overall demand, primarily in transparent housings where clarity is valued. Styrene-butadiene rubber gains traction as Michelin integrates recycled styrene into tire treads, targeting 40% sustainable-material content by 2030.

By End-User Industry: Automotive Gains, Packaging Plateaus

Packaging absorbed 34.52% of 2025 output, yet automotive and transportation is expanding at a 6.24% CAGR through 2031, the swiftest among all segments. Glass-fiber-reinforced ABS battery covers weigh 40% less than steel, pushing adoption as OEMs offset battery mass. Covestro supplies ABS meeting GB 38900 fire norms for Chinese EV interiors.

Construction demand rises with EPS and XPS insulation mandated by the EU renovation wave, and BASF’s Neopor expansion positions it to capture this uptick. Electrical and electronics rely on high-heat ABS for AI PCs and 5G infrastructure, while consumer goods and textiles move in line with GDP but face polyolefin substitution. Certification hurdles (ISO 22000 for food-contact recycling and UL 94 for flame retardancy) are creating barriers to entry for smaller converters.

Geography Analysis

Asia-Pacific controlled 49.27% of 2025 volume and will retain leadership, yet capacity expansions outpace demand growth, turning China into a structural exporter. India’s annual increase rides consumer-goods manufacturing and remains 40% import-dependent, presenting opportunity for Gulf exporters. South Korea and Taiwan confront tight high-heat ABS supply, prompting electronics brands to accept longer lead times from China. Japan pilots Agilyx chemical recycling, signaling a pivot toward circularity.

North America’s growth trails Asia-Pacific as INEOS closed the Sarnia plant and LyondellBasell emphasizes circular projects over new capacity, despite the region’s ethane cost advantage. Mexico advances under USMCA-aligned auto-parts exports.

Europe lags due to energy costs and stringent bans. Versalis shuttered its Priolo cracker, and converters must secure chemically recycled or bio-attributed feedstock to meet recycled-content mandates. Renovation of Germany’s pre-1979 housing stock under EU directives does lift EPS demand, albeit conditioned on low-carbon footprints.

The Middle East and Africa delivers the highest regional CAGR at 5.91% as Saudi Arabia extends downstream integration under Vision 2030 and South Africa substitutes imports with local EPS insulation. Carbon-capture pilots seek to neutralize potential EU carbon-border levies post-2030.

Competitive Landscape

The styrene market is moderately concentrated, with the top five producers holding about 42% share, while downstream conversion remains highly fragmented. Integrated Asian and Gulf complexes leverage co-production of benzene and ethylene to maintain cash-cost leadership. Western producers shift toward circular offerings: INEOS Styrolution’s FDA-approved recycled monomer commands a 20-30% premium. BASF’s Biomass Balance route, certified ISCC PLUS, slices cradle-to-gate CO₂ by up to 50% but carries a 20-30% price premium.

Agilyx and Pyrowave license microwave and catalytic depolymerization, and Michelin’s 2025 partnership validates demand in tire-rubber applications. Trinseo emerged from Chapter 11 in 2024 with USD 225 million new equity, divested polycarbonate to Mitsubishi Chemical, and reviews latex binders to concentrate on engineered styrenics.

Overcapacity pressures in China persist: Hengli, Shenghong, and Wanhua added 1.45 million tons between 2023 and 2024, driving general-purpose polystyrene margins below USD 50 per ton. European producers idle swing lines during price troughs, and consolidation is expected as small extruders face capital barriers for certification and recycling investments.

Styrene Industry Leaders

SABIC

INEOS Styrolution

LG Chem

Trinseo

CHIMEI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: INEOS Styrolution has delivered the first commercial batch of chemically recycled styrene from Indaver’s Antwerp facility. This confirms a closed-loop production capacity of 20,000 tons per year.

- April 2025: Clariant collaborated with Technip Energies to introduce a new catalyst. This catalyst is designed to achieve significantly lower steam-to-oil ratios in styrene production.

Global Styrene Market Report Scope

Styrene is an organic compound commonly used to produce plastics, resins, and synthetic rubbers. It is a colorless liquid with a distinctive sweet smell and is highly flammable. Styrene is primarily used to manufacture polystyrene, a versatile plastic known for its insulation properties and wide range of applications, including packaging materials, disposable utensils, insulation, and consumer products.

The styrene market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into polystyrene, acrylonitrile butadiene styrene, styrene-butadiene rubber, and other product types (styrene-acrylonitrile). By end-user industry, the market is segmented into packaging, construction, consumer goods, automotive and transportation, electrical and electronics, and other end-user industries (textile). The report also covers the market size and forecasts in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Polystyrene |

| Acrylonitrile Butadiene Styrene |

| Styrene Butadiene Rubber |

| Other Product Types (Styrene-Acrylonitrile) |

| Packaging |

| Construction |

| Consumer Goods |

| Automotive and Transportation |

| Electrical and Electronics |

| Other End-User Industries (Textile) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Polystyrene | |

| Acrylonitrile Butadiene Styrene | ||

| Styrene Butadiene Rubber | ||

| Other Product Types (Styrene-Acrylonitrile) | ||

| By End-user Industry | Packaging | |

| Construction | ||

| Consumer Goods | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Other End-User Industries (Textile) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected styrene market size in 2031?

The styrene market size is forecast at 39.18 million tons by 2031.

Which regional market is growing the fastest for styrene between 2026 and 2031?

The Middle East and Africa leads with a 5.91% CAGR, driven by Saudi downstream integration and insulation demand.

Which product segment is expanding most rapidly?

Acrylonitrile-butadiene-styrene is rising at a 6.18% CAGR on electric-vehicle and 5G infrastructure applications.

How are chemical-recycling projects influencing styrene demand?

Commercial depolymerization plants in Europe and North America supply food-contact monomer, supporting demand despite single-use bans.

Page last updated on: