1,6-Hexanediol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

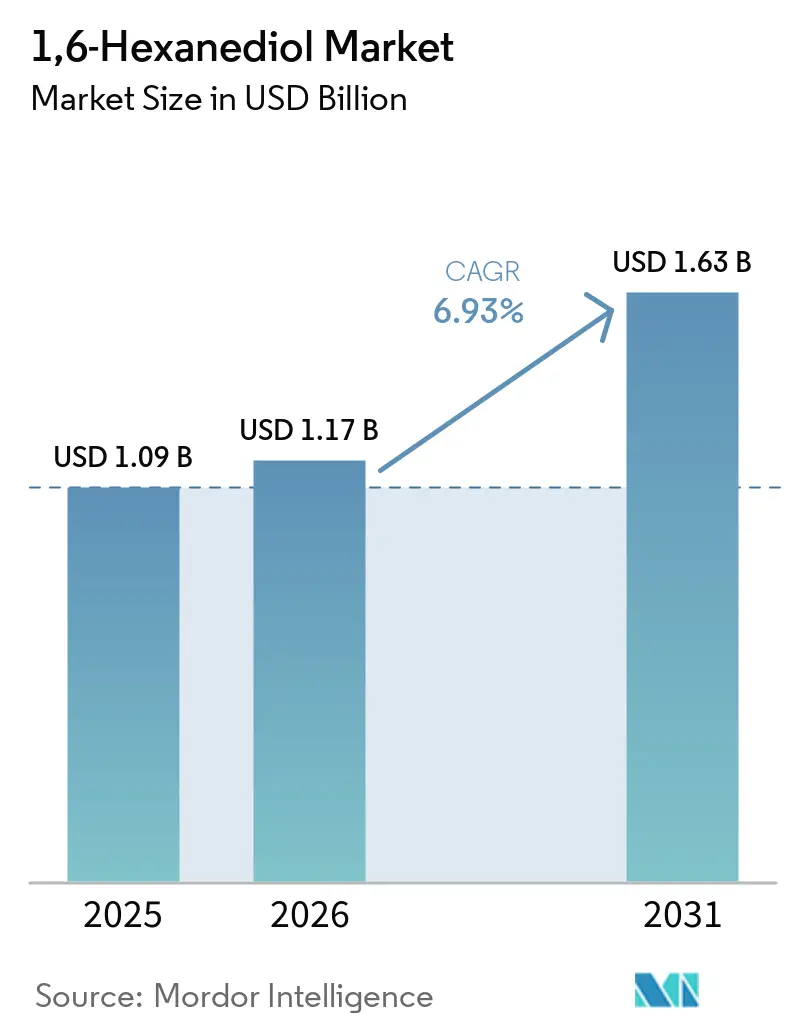

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

1,6-Hexanediol Market Analysis by Mordor Intelligence

The 1,6-Hexanediol Market size was valued at USD 1.09 billion in 2025 and estimated to grow from USD 1.17 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 6.93% during the forecast period (2026-2031). Strong polyurethane demand for wind-turbine blades, rapid uptake of UV-curable coatings, additive-manufacturing growth, and the push toward bio-based C6 diols collectively elevate consumption volumes, while purity upgrades open premium-price niches in optical and pharmaceutical uses. Cyclohexane remains the dominant raw material, yet adipic-acid innovations and biomass routes signal a gradual feedstock transition. High-purity grades command price premiums as AR/VR lens makers and semiconductor fabs tighten impurity thresholds. Regionally, Asia-Pacific anchors nearly half of global demand, propelled by integrated petrochemical complexes and downstream manufacturing clusters; North America and Europe, in turn, steer sustainability and regulatory advances that re-shape technology choices. Moderate fragmentation persists, but capacity additions by BASF, Evonik, and UBE Corporation indicate an intensifying contest for share in high-value segments.

Key Report Takeaways

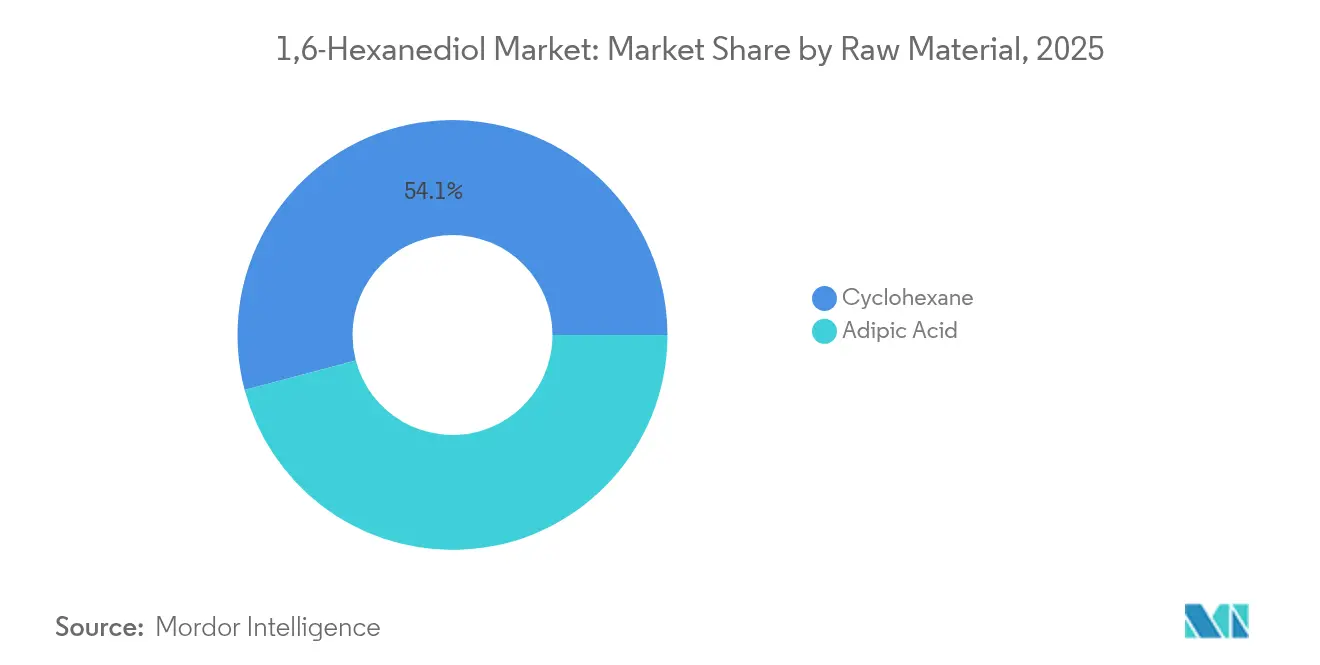

- By raw material, cyclohexane led with 54.12% revenue share in 2025; adipic acid is projected to expand at a 7.18% CAGR through 2031.

- By manufacturing process, the two-step cyclohexanone - adipic-acid hydrogenation route accounted for 83.75% of the 1,6-hexanediol market share in 2025, and also has the highest projected CAGR at 7.42% through 2031.

- By purity grade, greater than or equal to 99% high-purity products captured 60.85% of the 1,6-hexanediol market size in 2025 and are advancing at a 7.72% CAGR through 2031.

- By application, polyurethane held 36.98% of the 1,6-hexanediol market size in 2025; “Other Applications” anchored by 3D-printing photopolymers is growing fastest at an 7.92% CAGR to 2031.

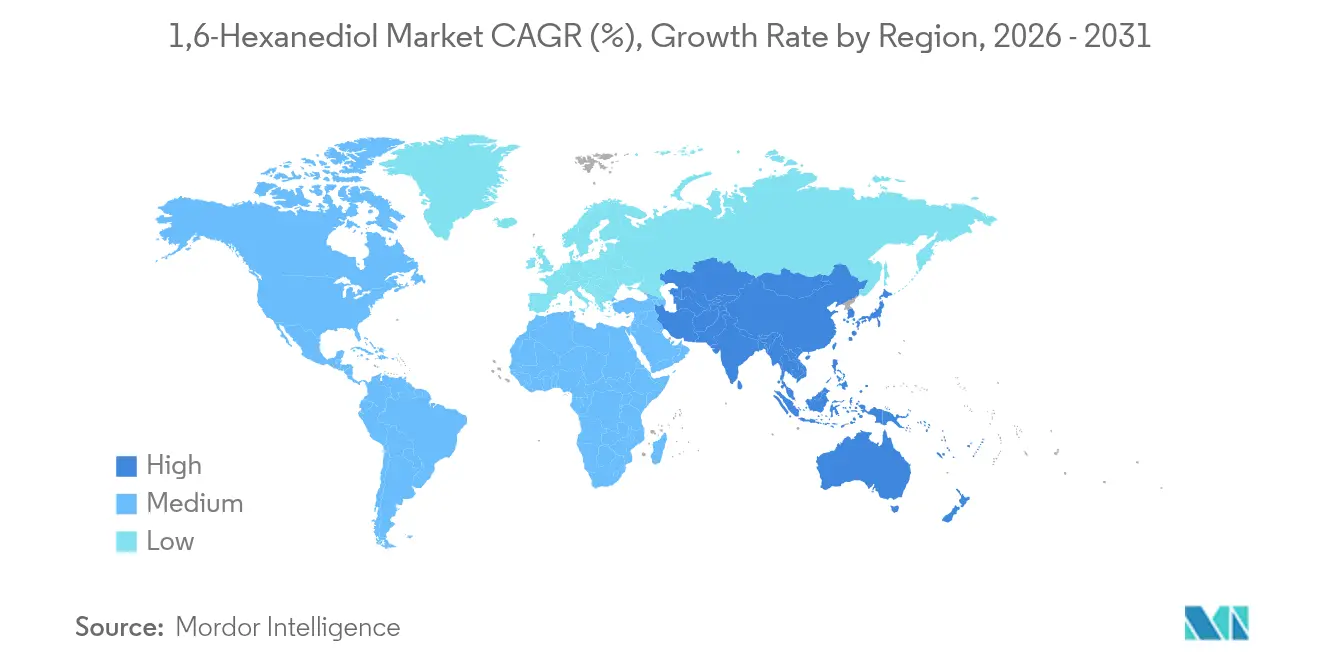

- By geography, Asia-Pacific represented 47.05% of 2025 revenues and is forecast to expand at a 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 1,6-Hexanediol Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising polyurethane demand in wind-turbine blade composites | +1.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Expanding powder and UV-curable industrial coatings market | +1.8% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Growth in TPU-based 3D-printing filaments | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Transition toward bio-based C6 diols from oil-seed feedstocks | +1.1% | Europe and North America regulatory-driven | Long term (≥ 4 years) |

| High-refractive-index optical polymers for AR/VR lenses | +0.7% | APAC manufacturing hubs, global demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Polyurethane Demand in Wind-Turbine Blade Composites

Global onshore and offshore wind installations specify longer blades and higher tip speeds, heightening fatigue and weathering requirements for composite matrices. Polyurethanes extended with 1,6-hexanediol supply superior elastomeric toughness, enabling thinner profiles without sacrificing durability. Equipment OEMs prioritize recyclability, and recyclable polyurethane chemistries incorporating the diol increasingly displace epoxy systems in prototype blades. Government clean-energy mandates and corporate net-zero targets sustain multiyear procurement pipelines for turbine components, converting material innovations into near-term volume orders. Lifecycle models show polyurethane blades may reduce mass by 10% versus epoxy, yielding logistics and tower-load benefits that outweigh marginal cost increases. Coupled with service-life extensions, these technical gains lift demand for high-functionality polyurethanes and, by extension, the 1,6-hexanediol market.

Expanding Powder and UV-Curable Industrial Coatings Market

Manufacturers adopt UV-curable and powder-coating lines to cut VOC emissions and accelerate takt times. Oligomers synthesized from 1,6-hexanediol demonstrate high crosslink density, reaching tensile strengths above 63 MPa while curing within seconds under LED lamps. Manufacturers adopt UV-curable and powder-coating lines to cut VOC emissions and accelerate takt times. Oligomers synthesized from 1,6-hexanediol demonstrate high crosslink density, reaching tensile strengths above 63 MPa while curing within seconds under LED lamps. Asia-Pacific appliance and furniture plants scale continuous powder-coat lines, and North American automakers retrofit bumpers and trim operations with UV tunnels, enlarging the addressable base. Capital payback improves as energy-intensive ovens are eliminated, aligning cost savings with sustainability targets. These factors converge to elevate coating-grade diol demand ahead of broader industrial output growth.

Growth in TPU-Based 3D-Printing Filaments

Additive manufacturing moves from prototyping to series production, and TPU filaments formulated with 1,6-hexanediol polyols satisfy flexibility, rebound, and abrasion-resistance criteria for medical orthotics, athletic footwear midsoles, and aerospace ducting. Closed-cell lattices printed via fused-filament fabrication achieve plateau stresses scaling predictably with density, facilitating part-specific energy-absorption tuning. Digital-light-processing platforms further expand use of photoactive urethanediol itaconates, offering isocyanate-free, bio-based routes with elastic moduli near 1 GPa. As printer OEMs qualify industrial TPU grades, procurement volumes shift from kilogram test runs to tonne-scale supply contracts, unlocking a fresh growth channel for the 1,6-hexanediol market.

Transition Toward Bio-Based C6 Diols from Oil-Seed Feedstocks

Regulators and brand owners push Scope 3 decarbonization, prompting chemical firms to pilot fermentation and catalytic-upgrading routes from vegetable oils, lignocellulosics, and algae. Microalgae strains with 55-57% oleic content deliver oil yields of 136.5 g/L, enabling competitive feedstock economics for downstream C6 diols. LANXESS’ mass-balancing certification under ISCC+ demonstrates traceability for renewable feedstock claims and eases customer adoption hurdles. Separately, two-step hydrogenation of biomass-derived 2,5-furandicarboxylic acid yields 99% adipic acid, setting the stage for fully bio-sourced 1,6-hexanediol. Early premiums narrow as capacity scales, positioning bio-based volumes for double-digit growth through the decade.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in adipic-acid and cyclohexane prices | -1.4% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Availability of functional substitutes (1,5-Pentanediol, 1,4-Butanediol) | -0.9% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| N₂O-emission regulations on adipic-acid producers | -0.8% | Europe and North America regulatory zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Adipic-Acid and Cyclohexane Prices

Feedstock swings threaten margins because 1,6-hexanediol pricing lags spot adipic acid and benzene cycles. China’s new 11.8 million tons/year aromatics complexes narrow integrators’ costs but also amplify global oversupply, triggering price troughs that unsettle independent producers[1]Tullo, Alexander H., “China’s Aromatics Building Boom Rattles the Petrochemical Industry,” cen.acs.org . Producers respond through term-contract hedging and selective backward integration, yet inventory risk persists, particularly for Asian exporters reliant on merchant adipic acid. Although refinery consolidation and capacity rationalization promise medium-term stability, near-term volatility compels balance-sheet conservatism and may delay discretionary capacity additions in the 1,6-hexanediol market.

N₂O-Emission Regulations on Adipic-Acid Producers

Adipic-acid oxidation emits roughly 0.25 kg N₂O per kg product, translating into 47.4 Mt CO₂e in 2024. The EU Emissions Trading System prices N₂O, while the U.S. tightens EPA new-source performance standards, compelling investments in thermal and catalytic abatement units that cut emissions by over 80% but add capital, operation, and maintenance costs. Compliance raises adipic-acid cash costs, indirectly inflating 1,6-hexanediol input prices. Smaller plants face retrofit economics that favor closure, nudging the industry toward larger, integrated sites. In China, policy scenarios project up to 62.6% abatement by 2030, reinforcing the long-term cost shift.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Cyclohexane Dominance Amid Bio-Based Transition

Cyclohexane accounted for 54.12% of 2025 volumes as vertically integrated petrochemical complexes guarantee feed continuity and scale economies that anchor the 1,6-hexanediol market size for this segment. Technology upgrades, including VPO composite catalysts that push 60.6% cyclohexane conversion with 85% adipic-acid selectivity, temper N₂O emissions and sustain competitiveness.

Adipic-acid feedstock usage climbs faster at 7.18% CAGR as microreactor oxidation achieves 93% yields with shortened residence times and reduced off-gas streams. Bio-derived adipic acid sourced from FDCA furthers the renewable pivot, but costs remain above cyclohexane routes. Fermentation-based diols, though currently a niche, draw venture funding and pilot-line expansions that could erode cyclohexane’s share beyond 2030 if carbon-pricing schemes intensify. Consequently, raw-material dynamics embody the wider transition forces shaping the 1,6-hexanediol market.

By Manufacturing Process: Two-Step Hydrogenation Maintains Technological Leadership

The two-step cyclohexanone - adipic-acid hydrogenation route generated 83.75% of 2025 output, anchoring a 1,6-hexanediol market share entrenched by decades of catalyst refinement and plant debottlenecking. This pathway’s learning-curve advantages keep cash-cost leadership despite energy-price volatility, fostering a 7.42% CAGR to 2031 as brownfield upgrades stretch capacity. Integration with hexamethylenediamine facilities, such as BASF’s Chalampé complex, enhances by-product valorization and utilities sharing.

Direct one-step hydrogenation of caprolactone simplifies unit operations but battles lower selectivity and shorter catalyst life, limiting uptake to specialty plants targeting ultra-high-purity grades. Bio-fermentation and catalytic upgrading deliver the highest growth, albeit from a low base, as producers trial sugar-to-diol routes in Europe and North America. Evonik’s specialty amine unit in Nanjing uses green electricity and advanced automation, illustrating how digitalization and renewable power can close cost gaps in emerging processes.

By Purity Grade: High-Purity Applications Drive Premium Growth

More than or equal to 99% high-purity material captured 60.85% of 2025 revenues and is projected to expand at a 7.72% CAGR. AR/VR headset demand for high-refractive-index lenses and semiconductor moisture-barrier films elevates specification and trace-impurity demands, extending batch-certification protocols and driving premium pricing. Lens-grade supply contracts often stipulate more than 5 ppm water and acid values below 30 ppm, spurring investment in continuous crystallization and vacuum-distillation modules.

Industrial-grade 1,6-hexanediol serves flexible foam, coating, and plasticizer formulations where tolerance for trace carbonyls remains higher. Producers therefore prioritize process-control automation and in-line FTIR monitoring to deliver tighter quality windows without inflating cost structure. This bifurcation reinforces a value-over-volume dynamic that tilts future profits toward the high-purity end of the 1,6-hexanediol market.

By Application: Polyurethane Leadership with Photopolymer Upside

Polyurethanes absorbed 36.98% of the 2025 demand, underpinned by construction insulation, mobility seating cushions, and emerging wind-blade elastomers. Even so, novel isocyanate-reactive chain extenders using the diol prolong the segment’s margin lead.

The “Other Applications” bucket, primarily 3D-printing photopolymers, registers the fastest 7.92% CAGR. Layer-cured lattices in footwear and customized orthoses validate commercial scale, while dental and consumer electronics casings round out early adopter sets. This diversification positions the 1,6-hexanediol market for structural resilience even as its legacy polyurethane franchise plateaus.

Geography Analysis

Asia-Pacific generated 47.05% of global revenue in 2025, and a 7.86% CAGR outlook. China’s integrated aromatics hubs anchor cost leadership, yet stricter emission norms push producers to adopt catalytic N₂O abatement and invest in bio-based pilot lines. Japan and South Korea channel demand into high-purity grades used in optical polymers and battery binders, reinforcing the region’s value density. ASEAN nations scale polyurethane foam plants for appliance insulation and footwear, but remain net importers of the diol.

North America is leveraged by wind-turbine blade buildouts and additive-manufacturing expansion, driving incremental volumes. UBE Corporation’s USD 500 million Louisiana project to produce carbonate solvents and upstream diol intermediates underscores overseas capital inflows tied to U.S. clean-energy incentives.

Europe, while battling cost disadvantages, preserves a technological-leadership niche through process-intensification and sustainability innovation. BASF’s Chalampé start-up and Alsachimie joint-venture consolidation broaden feedstock optionality while embedding Scope 3 reporting into customer contracts.

South America, and the Middle East and Africa's petrochemical diversification in Saudi Arabia and Brazil’s polyurethane downstream build-out hint at higher long-term growth runways.

Competitive Landscape

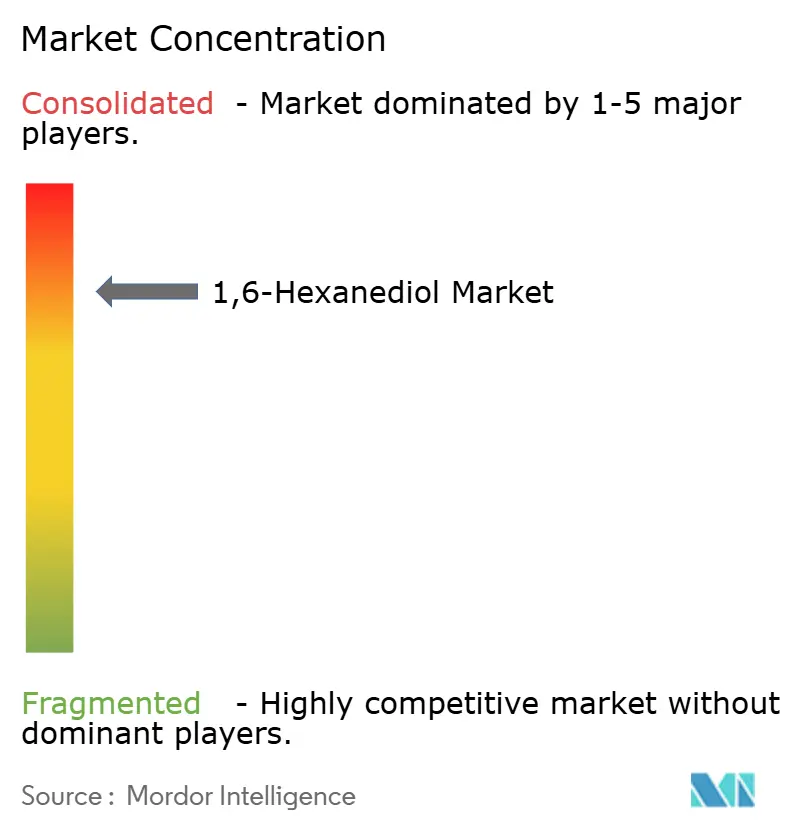

The 1,6-hexanediol industry presents consolidation amongst major players. Strategic moves gravitate toward mergers and acquisitions, and joint ventures that deliver geographic diversification or technology boosts. Chinese producers, supported by provincial incentives, undertake debottlenecking and pilot bio-based lines to hedge against carbon-border adjustment mechanisms. Across the board, emission-abatement retrofits, catalyst-efficiency drives, and digital twins for predictive maintenance dominate capex agendas. Competitive intensity is also visible in customer-service models. Suppliers roll out blockchain-enabled batch traceability, offer Scope 3 calculators, and extend technical-service labs to co-develop low-VOC coatings and 3D-printing resins.

1,6-Hexanediol Industry Leaders

LANXESS

BASF

PETRONAS Chemicals Group Berhad

Prasol Chemicals Ltd.

UBE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: BASF announced that the Carbon Trust verified the cradle-to-gate product-carbon footprint of BASF 1,6-hexanediol as lower than the market average for fossil-based equivalents.

- April 2023: LANXESS announced that its 1,6-hexanediol (HDO) production received Scopeblue certification, awarded to products with over 50% sustainable raw material content or a carbon footprint less than half of conventional alternatives.

Global 1,6-Hexanediol Market Report Scope

The 1,6-Hexanediol is widely used in the production of industrial polyester and polyurethane. It helps in improving the hardness and flexibility of polyesters. The 1,6-Hexanediol market is segmented by raw material, application, and geography. By raw material, the market is segmented into cyclohexane and adipic acid. By application, the market is segmented into polyurethane, coatings, acrylates, adhesives, polyester resins, plasticizers, and others. The report also covers the market size and forecasts for the 1,6-hexanediol market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Cyclohexane |

| Adipic Acid |

| Two-step Cyclohexanone - Adipic-Acid Hydrogenation |

| Direct One-step Hydrogenation of Caprolactone |

| Bio-fermentation and Catalytic Upgrading |

| Greater than equal to 99% (High-Purity) |

| Less than 99% (Industrial-Grade) |

| Polyurethane |

| Coatings |

| Acrylates |

| Adhesives |

| Polyester Resins |

| Plasticizers |

| Other Applications (3D-Printing Photopolymers, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Cyclohexane | |

| Adipic Acid | ||

| By Manufacturing Process | Two-step Cyclohexanone - Adipic-Acid Hydrogenation | |

| Direct One-step Hydrogenation of Caprolactone | ||

| Bio-fermentation and Catalytic Upgrading | ||

| By Purity Grade | Greater than equal to 99% (High-Purity) | |

| Less than 99% (Industrial-Grade) | ||

| By Application | Polyurethane | |

| Coatings | ||

| Acrylates | ||

| Adhesives | ||

| Polyester Resins | ||

| Plasticizers | ||

| Other Applications (3D-Printing Photopolymers, etc.) | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current 1,6-hexanediol market size and expected growth?

The market is valued at USD 1.17 billion in 2026 and is forecast to reach USD 1.63 billion by 2031, registering a 6.93% CAGR during the forecast period (2026-2031).

Which raw material dominates 1,6-hexanediol production?

Cyclohexane remains the leading feedstock, accounting for 54.12% of 2025 volumes due to integrated petrochemical economics.

Why are high-purity grades gaining share?

AR/VR optics, semiconductors, and pharmaceutical intermediates require ≤99% purity, driving a 7.72% CAGR for this premium segment through 2031.

How are sustainability trends shaping the 1,6-hexanediol market?

Bio-based C6 diol pathways, mass-balance certification, and N₂O-abatement mandates are reshaping feedstock choices, cost structures, and investment priorities.

Which region shows the fastest growth in demand?

Asia-Pacific leads with a 7.86% CAGR through 2031, underpinned by large-scale chemical complexes and expanding downstream manufacturing.

Page last updated on: