Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

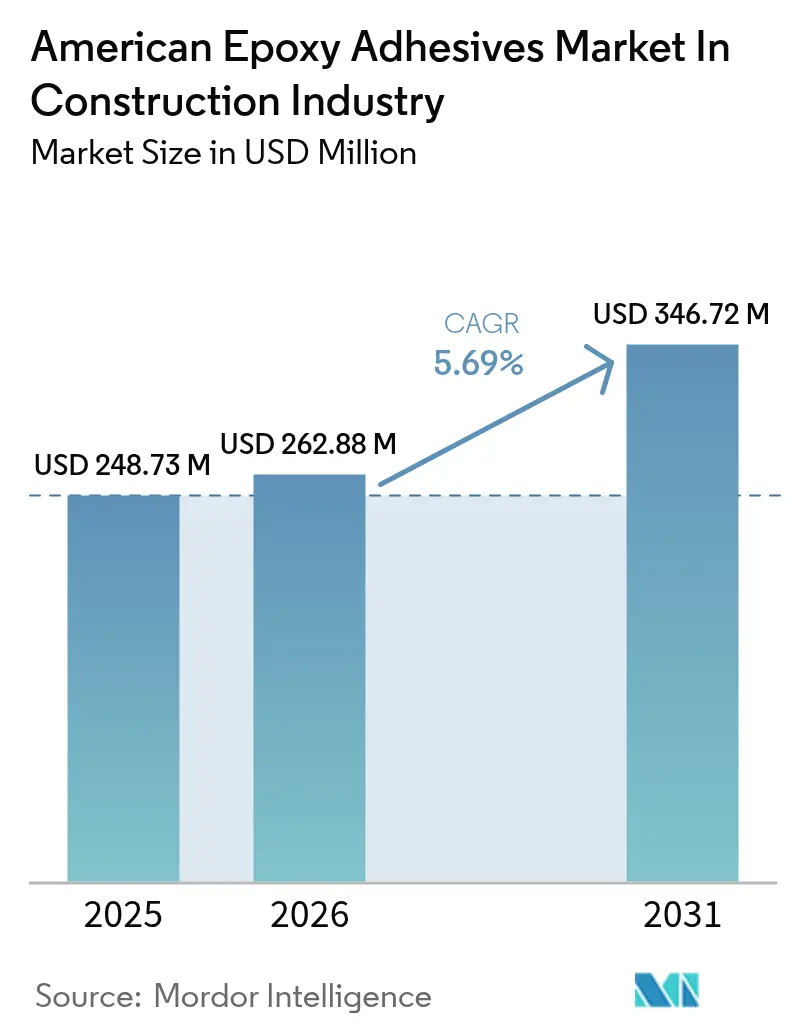

| Base Year Market Size (2025) | USD 248.73 Million |

| Market Size (2026) | USD 262.88 Million |

| Market Size (2031) | USD 346.72 Million |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

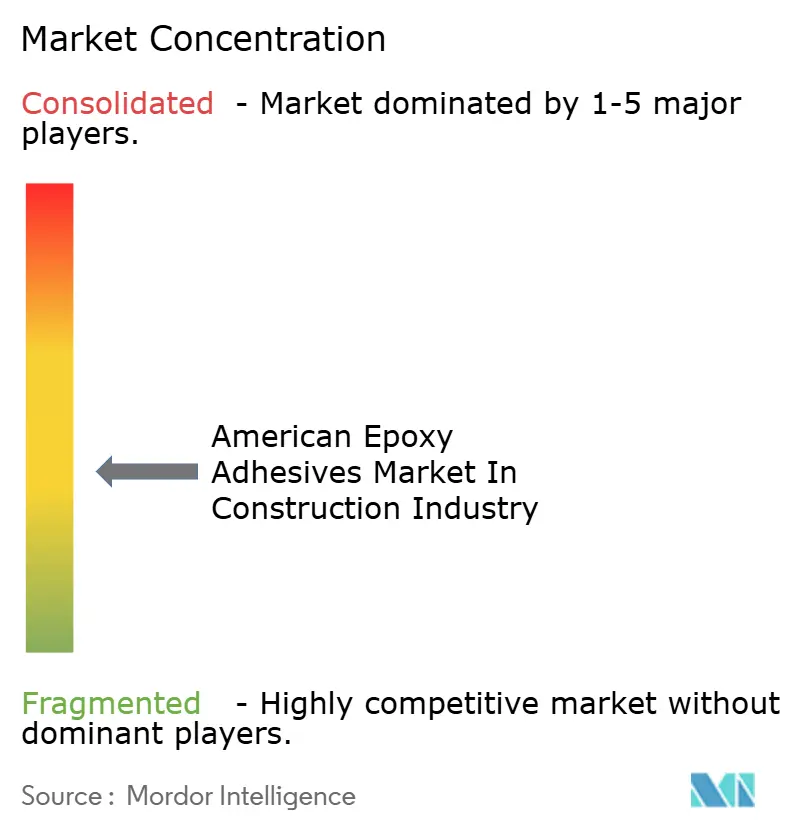

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

American Epoxy Adhesives for Construction Market Analysis by Mordor Intelligence

The American Epoxy Adhesives Market size in Construction Industry market size in 2026 is estimated at USD 262.88 million, growing from 2025 value of USD 248.73 million with 2031 projections showing USD 346.72 million, growing at 5.69% CAGR over 2026-2031. Robust public-works budgets, widespread code acceptance of structural bonding, and the need for lightweight, corrosion-resistant joints are reshaping how contractors assemble bridges, data centers, and modular housing. Federal infrastructure outlays in the United States and Canada continue to favor epoxy injection and overlay systems that strengthen aging concrete. Developers of prefabricated buildings increasingly specify one-component epoxies whose latent catalysts eliminate on-site mixing, saving labor even as cure performance improves. Contractors are also embracing UV-cured chemistries because handheld LED lamps polymerize joints in seconds, shortening installation cycles and keeping building envelopes on schedule. Against those growth vectors, formulators confront raw-material volatility and freshly proposed volatile-organic-compound limits that compel expensive reformulation toward water-borne or high-solids platforms.

Key Report Takeaways

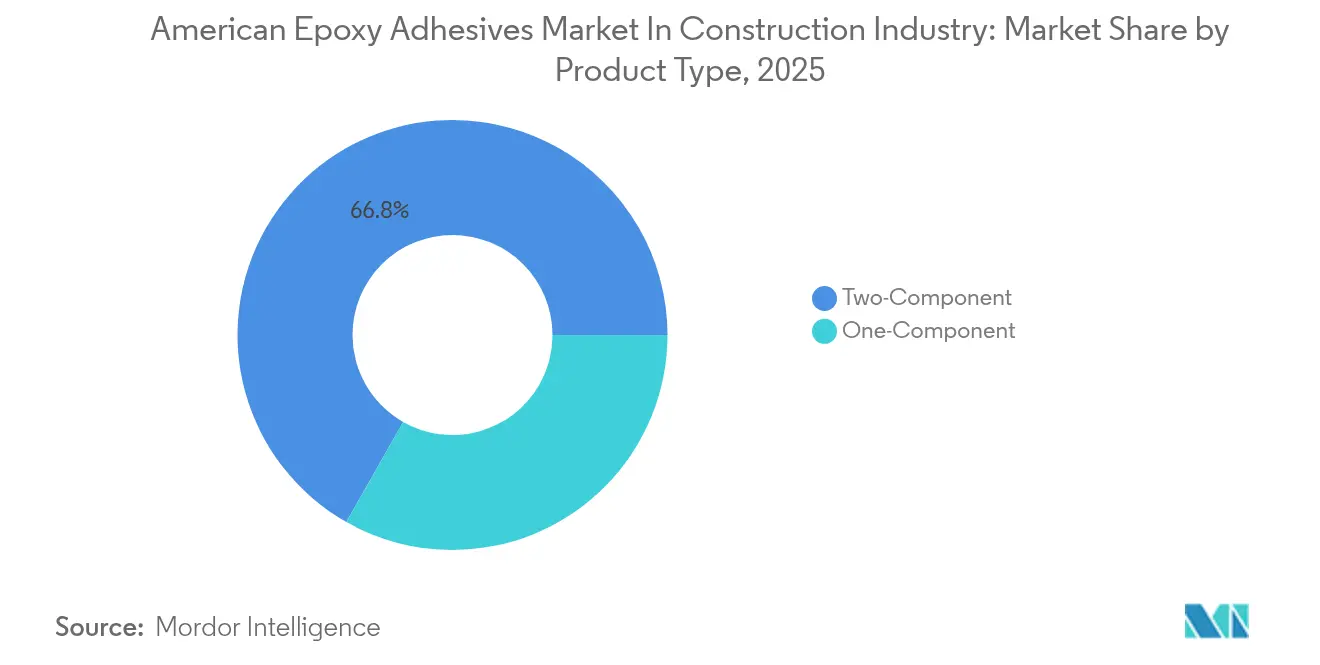

- By product type, two-component systems led with a 66.78% American epoxy adhesives market share in 2025, while one-component grades are forecast to grow at a 6.08% CAGR through 2031.

- By technology, reactive chemistries accounted for 47.95% of revenue in 2025; UV-cured formulations are projected to register the fastest 6.19% CAGR to 2031.

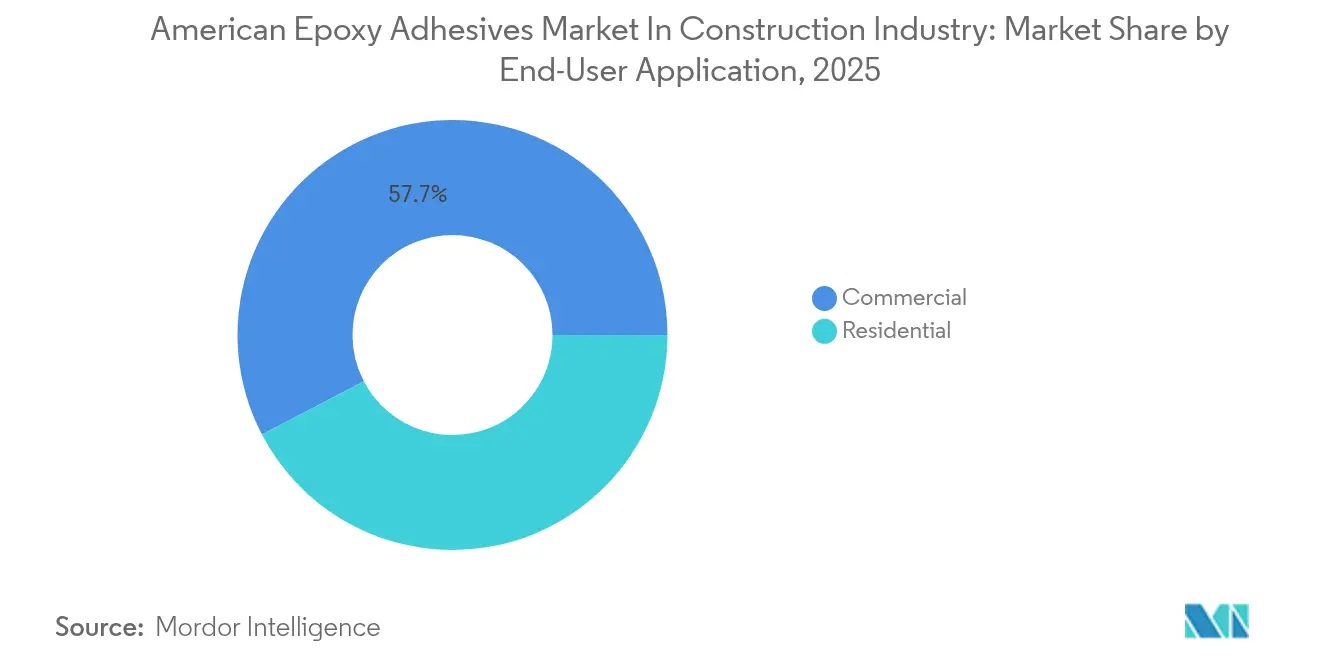

- By end-user application, commercial construction captured 57.66% of demand in 2025, whereas residential use is advancing at a 5.86% CAGR to 2031.

- By geography, North America dominated with 71.62% revenue share in 2025, but South America is poised for the highest 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

American Epoxy Adhesives for Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-led construction boom across the Americas | +1.8% | North America (IIJA, CHIPS Act); South America (Brazil PPP, Argentina energy corridors) | Medium term (2–4 years) |

| Rapid adoption of prefabricated and modular building systems | +1.3% | North America (urban infill, affordable housing); Chile (seismic-resistant modules) | Short term (≤ 2 years) |

| Shift from mechanical fastening to high-performance bonding | +1.1% | Global, with early penetration in U.S. commercial and Canadian transit projects | Long term (≥ 4 years) |

| 3-D concrete printing requiring structural epoxy formulations | +0.9% | North America (pilot projects in Texas, California); Mexico (social housing trials) | Long term (≥ 4 years) |

| Brazil's PPP tax incentives accelerating epoxy demand in civil works | +0.7% | Brazil (federal and state concessions); spillover to Uruguay, Paraguay | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Boom Across the Americas

Infrastructure spending is steering the American epoxy adhesives market toward higher-performance formulations. The U.S. Infrastructure Investment and Jobs Act allocates significant funds to road and bridge upgrades and prioritizes epoxy injection over full deck replacement, lifting demand for low-viscosity resins that penetrate micro-cracks. Canada’s Investing in Canada Infrastructure Program earmarks funding for transit projects that mandate prefabricated modules bonded with structural epoxies. South American concessions funded by the Inter-American Development Bank, with epoxy grouts anchoring turbine bases and pipeline joints in corrosive soils. As projects migrate from temperate to equatorial climates, formulators must widen service-temperature windows and extend pot life to accommodate hot-weather placement. Longer open times also minimize waste in large bridge-deck pours, improving job economics while maintaining bond reliability.

Rapid Adoption of Prefabricated and Modular Building Systems

Prefabrication is propelling growth across the American epoxy adhesives market as factory-controlled environments enable robotic dispensing of precise bead geometries. U.S. modular housing starts climbed in 2024, each using one-component film adhesives that cure at 120 °C and remove the risk of on-site mixing errors. Sika’s 2024 annual report shows prefab-related adhesive sales rising, supported by partnerships with volumetric manufacturers in Texas and Ontario. Factory automation shortens cycle time, but it also demands epoxies with predictable cure profiles that synchronize with takt-time rhythms. Suppliers must co-develop with module builders, validating joints under shipping vibration and crane-lift loads to win repeat business.

Shift from Mechanical Fastening to High-Performance Bonding

Designers are replacing bolts and welds with adhesives to eliminate thermal bridges and distribute stress more evenly across joints. The American Institute of Steel Construction published a 2024 design guide for epoxy-bonded steel-to-concrete beams, granting engineers load tables that accelerate specification. Henkel reported growth in its Loctite structural line as curtain-wall fabricators adopted bonded glazing that improves thermal resistance by 0.15 W/m²·K. Canada’s 2024 National Building Code now allows adhesive-only attachment of exterior insulation up to 12 stories, provided lap-shear strength meets 1 MPa after 28 days—thresholds easily surpassed by reactive epoxies. To capitalize, suppliers continue funding third-party testing and code-body engagement that turn engineering skepticism into formal specification clauses, deepening penetration across the American epoxy adhesives market.

3-D Concrete Printing Requiring Structural Epoxy Formulations

Additive construction, while eliminating the need for formwork, faces challenges with weak interlayer interfaces. A study published in Cement and Concrete Composites in 2024 highlighted that untreated layers achieve merely a fraction of their intended monolithic tensile strength. However, the application of a thin epoxy primer can restore this strength to its full potential. In Texas, ICON Technology has been printing hundreds of homes, utilizing a two-component epoxy with a limited pot life. This allows them to effectively bond layers that are deposited over extended periods. Echoing this, the U.S. Army Corps of Engineers, in 2024, validated similar epoxy formulations in a prototype barracks, underscoring military interest in both portable printers and field-cured adhesives. Pilot projects in Mexico have shown promise, revealing that epoxy priming can lead to a reduction in concrete waste by minimizing the demolition of defective prints. Given these advancements, suppliers are urged to fine-tune viscosity for optimal substrate wetting, all while ensuring a swift strength build-up. This balance is crucial to support subsequent layers within the tight print cycles, positioning them for an early-mover advantage in the burgeoning American epoxy adhesives market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in bisphenol-A and epichlorohydrin raw-material prices | -0.9% | Global, with acute exposure in North America due to import dependence | Short term (≤ 2 years) |

| Stringent VOC and chemical-exposure regulations in United States and Canada | -0.6% | North America (EPA NESHAP, SCAQMD Rule 1168); limited near-term impact in South America | Medium term (2–4 years) |

| Shortage of certified applicators for two-component systems | -0.4% | North America (high labor turnover); emerging concern in Brazil, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Bisphenol-A and Epichlorohydrin Raw-Material Prices

In 2024, Bisphenol-A prices in Asia experienced significant swings. Meanwhile, contracts for epichlorohydrin on the U.S. Gulf Coast rose, driven by tight propylene supplies. This surge in epichlorohydrin prices has put pressure on margins for formulators bound by 60-day supply contracts. Dow Chemical, in Q4 2024, faced a decline in epoxy-resin profitability, attributing it to feedstock inflation outpacing increases in selling prices. In response, major producers are either backward-integrating or entering into multiyear offtake agreements. On the other hand, niche players are venturing into bio-based resins. These resins, though pricier, offer a buffer against fluctuations in petrochemical prices. The ongoing volatility in the market is keeping working capital requirements elevated. This, in turn, is tempering the risk appetite of smaller entrants, leading to a slight deceleration in the CAGR of the American epoxy adhesives market.

Stringent VOC and Chemical-Exposure Regulations in the United States and Canada

The U.S. EPA has proposed an amendment to 40 CFR Part 63, reducing VOC limits for structural adhesives. This move aligns federal regulations with California’s Rule 1168[1]U.S. Environmental Protection Agency, “Proposed VOC Limits for Adhesives,” epa.gov. As a result of this compliance, there's a noticeable shift towards water-borne or high-solids technologies. However, this transition comes at a cost: raw material prices increase, and there's an added expense for performance validation. In Canada, a 2024 prohibition on bisphenol-A in adhesives for schools and hospitals introduces another financial strain[2]Environment and Climate Change Canada, “Bisphenol-A Restrictions,” canada.ca . Suppliers are now pivoting to bisphenol-F or bisphenol-S epoxies, which come at a premium. H.B. Fuller highlights that a significant portion of its North American portfolio is already in line with the new EPA limit, a notable increase from 2023. This underscores the disproportionate challenge faced by smaller formulators. While the regulatory changes seem to favor larger players, they also dampen short-term growth prospects in the U.S. epoxy adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Two-Component Systems Maintain Lead While One-Component Grades Accelerate

Two-component epoxies controlled 66.78% of revenue in 2025, a dominance underpinned by ambient-temperature cure and greater than 25 MPa lap-shear strength, making them indispensable for bridge overlays and curtain-wall anchoring. Contractors absorb the mixing burden because failure costs dwarf labor premiums. However, one-component grades are expanding at a 6.08% CAGR as latent catalysts deliver factory-friendly cure schedules that integrate with panel-press ovens. Henkel’s Loctite EA 9497 film adhesive allows Ontario modular builders to bond steel frames without metering pumps, eliminating common field errors. Moisture-cure and frozen pre-mix products occupy niche roles where cold-chain logistics or slow strength development limit broader uptake.

One-component systems appeal to residential builders needing simple cartridge application, though elevated cure temperatures currently confine them to climate-controlled plants or warm seasons. Arkema’s 90 °C cure epoxy targets cross-laminated timber production lines, demonstrating how temperature reductions can unlock broader field usage. Looking ahead, automation and prefab adoption are expected to shave some percentage points from the two-component share by 2031 as the American epoxy adhesives market shifts toward heat-activated or film formats that merge reliability with process simplicity.

By Technology: UV-Cured Formulations Disrupt Reactive Mainstays

Reactive epoxies claimed 47.95% of the technology mix in 2025, prized for solvent-free curing and robust gap-filling on heavy civil jobs. Yet UV-cured chemistries are advancing fastest at 6.19% CAGR, spurred by LED-lamp prices that fell between 2022 and 2024 and photoinitiators that now penetrate 6 mm bond lines. Solvent-borne epoxies continue to decline under tightening VOC rules, while water-borne grades gain share despite slower dry times as contractors chase low-odor installations in occupied buildings.

The American epoxy adhesives market size for UV-cured grades is projected to expand faster than any other technology cohort, given the dual tailwinds of regulatory pressure and manufacturing efficiency. However, reactive systems will remain entrenched in bridge and foundation work where deep section cure and high modulus remain critical. Suppliers therefore maintain parallel development tracks, balancing rapid-cure innovation with improvements in traditional amine-cure platforms to preserve core infrastructure revenue.

By End-User Application: Commercial Demand Dominates, Residential Segment Climbs

Commercial projects absorbed 57.66% of volume in 2025 as data centers, warehouses, and hospitals specified fire-rated assemblies and seismic-rated curtain walls that demand code-listed epoxies. In 2023, the U.S. data-center pipeline saw significant growth, as operators turned to low-smoke epoxies for their cable races. Logistics facilities require floor joints that maintain bond strength at –30 °C, stimulating the development of epoxy-polyurethane hybrids. Residential applications are climbing at a 5.86% CAGR as single-family and multifamily builders adopt engineered lumber and prefab walls bonded with structural adhesives.

Brazil’s restarted Minha Casa Minha Vida program is adding affordable units that specify epoxy-bonded precast panels, lifting South American volume. To satisfy fast-moving framing crews, suppliers now offer grab times of less than 5 minutes, pushing research and development toward rheology modifiers that maintain early tack without sacrificing long-term strength. These shifts suggest residential share will inch upward as builders seek labor-saving assembly methods consistent with tight production schedules.

Geography Analysis

North America held 71.62% of revenue in 2025, bolstered by performance-based codes endorsing adhesive-only structural connections. This was further supported by a network of ASTM-accredited training centers, ensuring a consistent influx of certified applicators. The U.S. alone accounted for a significant portion of the American epoxy adhesives market, fueled by substantial allocations for surface transportation. These funds predominantly directed epoxies towards bridge repairs and anchor installations. California’s seismic retrofit initiative, targeting masonry buildings, mandates epoxy anchors. These anchors are designed to transfer shear loads into newly installed steel frames, guaranteeing a robust demand trajectory through 2030. Canada, contributing to the regional revenue, sees transit projects like Toronto’s Ontario Line necessitating epoxy-grouted track fastenings. These fastenings are engineered to withstand impressive load cycles. Meanwhile, Mexico, propelled by the rise of near-shoring logistics hubs, experiences tempered adoption of premium two-component systems due to price sensitivity.

South America is the growth engine, advancing at a 6.04% CAGR. This momentum is largely driven by significant investments from Brazil, Argentina, and Chile into their transport and energy infrastructures. Brazil’s Law 14,801 has effectively reduced financing costs for Public-Private Partnerships (PPPs). This legislative push has facilitated highway concessions to finalize in 2024. Notably, each of these concessions mandates the use of thixotropic epoxies for their precast tunnel segments. Highlighting the adhesive's volume potential, the São Paulo Metro Line 6 utilizes adhesive per segment across its rings. In Argentina, the Vaca Muerta shale pipeline and the electrification of Buenos Aires' rail system are deploying epoxy-bonded composite insulators. These insulators are specifically designed to withstand high-salinity environments. Chile has introduced a new code mandating prefab seismic modules. These modules must feature adhesive joints that can endure 8.0-magnitude shake-table tests, thereby amplifying the demand for high-modulus epoxies.

While North America anticipates a moderate CAGR, this represents a deceleration from the surge witnessed between 2020 and 2024. In contrast, South America is witnessing an uptick, accelerating from a previous growth rate to the current one. This shift is attributed to the maturation of reforms and an influx of commodity investments. Given this landscape, suppliers in North America face the challenge of safeguarding their margins amidst fierce competition. Simultaneously, they are urged to amplify local manufacturing and establish service teams fluent in Spanish or Portuguese in South America, aiming to harness the region's pronounced growth in the expansive American epoxy adhesives market.

Competitive Landscape

The American Epoxy Adhesives for Construction Market remains moderately fragmented. Pricing pressure intensified in 2024 as Chinese imports undercut commodity paste prices. Strategic playbooks converge on three levers: backward resin integration to hedge feedstock swings, geographic expansion into South America via acquisitions or toll blending, and portfolio premiumization with low-VOC or bio-based grades carrying price premiums. White-space opportunities cluster in residential prefabrication, where robotic dispensing and heat-cure one-component films integrate seamlessly into production lines. 3-D concrete printing also beckons, with suppliers racing to embed epoxy primers directly into print heads to automate an otherwise manual process. Patent filings reveal growing interest in epoxy-polyurethane hybrids that marry strength with flexibility and in photoinitiators that enable UV cure through pigmented panels, foreshadowing the next phase of technology competition in the American epoxy adhesives market.

American Epoxy Adhesives for Construction Industry Leaders

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

RPM International Inc.

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: H.B. Fuller opened a new manufacturing facility in Cairo and expanded its United Arab Emirates site to serve more than 30 market segments. The Vice President mentions that the facility ensures efficient and seamless distribution to customers across North America.

- May 2024: H.B. Fuller Company announced the acquisition of ND Industries Inc., a leading provider of specialty adhesives and fastener locking and sealing solutions. H.B. Fuller aims to fast-track its key growth objectives through a strategic acquisition. This move aligns with the company's approach of channeling capital towards the most lucrative segments in the functional coatings, adhesives, sealants, and elastomers (CASE) sector. With this acquisition, H.B. Fuller is set to enhance its portfolio by incorporating ND Industries’ Vibra-Tite brand products, complementing its current offerings of epoxy products.

American Epoxy Adhesives for Construction Market Report Scope

Construction adhesives, specialized bonding agents, join, seal, and secure materials such as wood, metal, concrete, and drywall. They offer durable, long-lasting bonds, often serving as a more efficient or aesthetically pleasing alternative to traditional fasteners. The American Epoxy Adhesives for Construction Market is segmented by product type, technology, end-user application, and geography. By product type, the market is segmented into one-component and two-component. By technology, the market is segmented into reactive, solvent-borne, UV-cured adhesives, and water-borne. By end-user application, the market is segmented into residential and commercial. The report also covers the market size and forecasts for the epoxy adhesives market in the construction industry in 6 countries across the American region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Product Type

| One-Component |

| Two-Component |

By Technology

| Reactive |

| Solvent-borne |

| UV Cured Adhesives |

| Water-borne |

By End-User Application

| Residential |

| Commercial |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

| By Product Type | One-Component | |

| Two-Component | ||

| By Technology | Reactive | |

| Solvent-borne | ||

| UV Cured Adhesives | ||

| Water-borne | ||

| By End-User Application | Residential | |

| Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 valuation of the American epoxy adhesives market?

The sector is valued at USD 262.88 million in 2026, with expansion underway toward USD 346.72 million by 2031.

Which product type leads current demand?

Two-component systems command 66.78% of 2025 revenue due to superior ambient-temperature cure and high tensile strength.

Which technology is growing fastest?

UV-cured epoxies are advancing at a 6.19% CAGR, aided by falling LED-lamp prices and rapid cure cycles.

Where is the highest geographic growth?

South America is forecast to grow at a 6.04% CAGR, led by Brazilian PPP infrastructure and Argentine energy corridors.

How are raw-material swings affecting suppliers?

Bisphenol-A and epichlorohydrin volatility trimmed large producers’ epoxy margins in 2024.

Page last updated on: