Stretcher Chairs Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

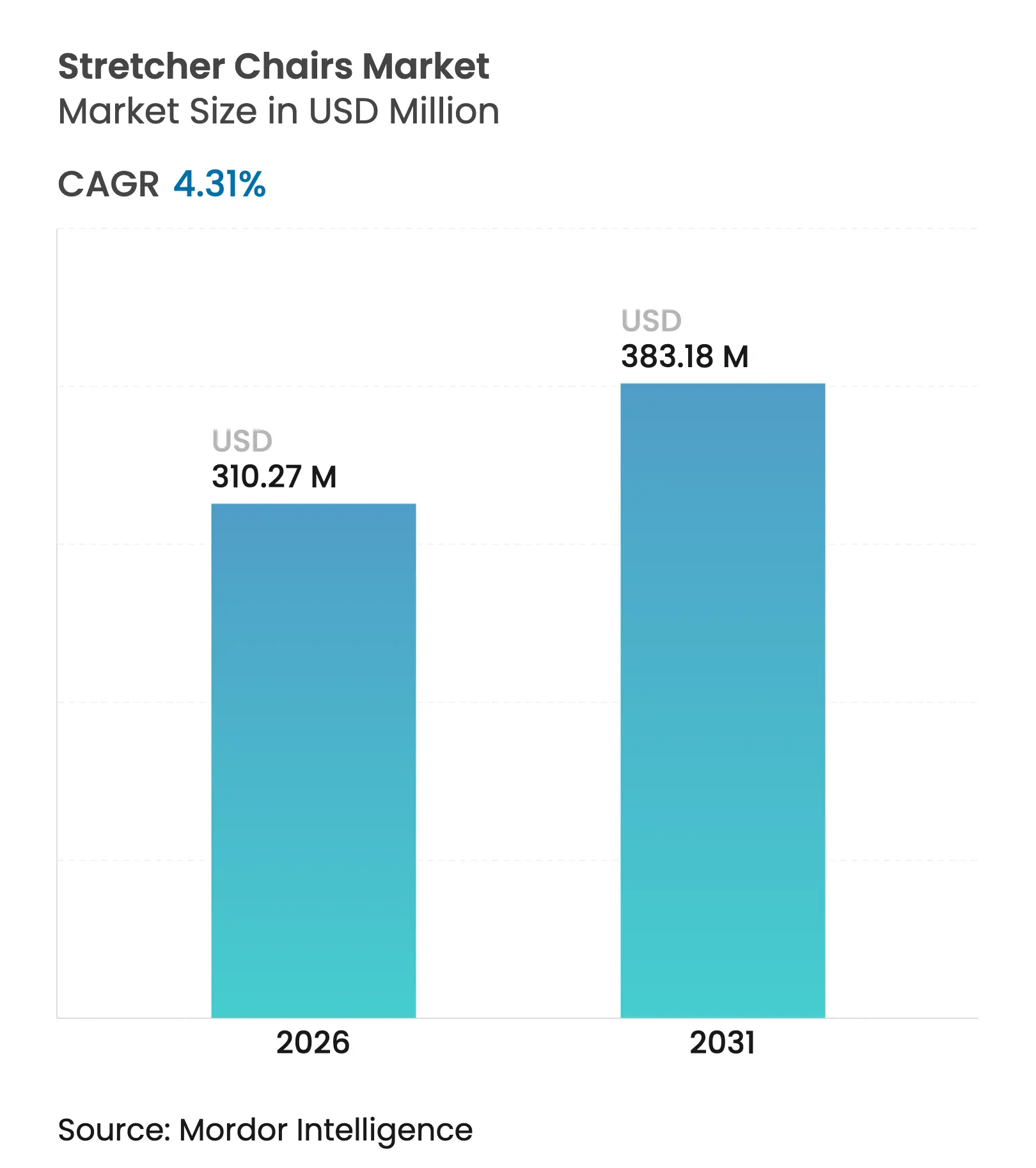

| Market Size (2026) | USD 310.27 Million |

| Market Size (2031) | USD 383.18 Million |

| Growth Rate (2026 - 2031) | 4.31 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Stretcher Chairs Market Analysis by Mordor Intelligence

medical stretcher chairs market size in 2026 is estimated at USD 310.27 million, growing from 2025 value of USD 297.44 million with 2031 projections showing USD 383.18 million, growing at 4.31% CAGR over 2026-2031. This steady progression reflects health-system priorities that blend patient-centric mobility, caregiver ergonomics, and tightening regulatory mandates. Accelerating ambulatory surgical center (ASC) growth, wider adoption of “no-lift” hospital policies, and technology upgrades in actuation systems all reinforce demand. Powered variants gain traction as facilities quantify reductions in musculoskeletal injuries, while bariatric-capable models command premium pricing amid rising obesity prevalence. At the same time, manufacturers navigate stricter FDA quality system amendments taking effect in 2026 and variable Medicare reimbursement that can prolong purchase cycles.[1]U.S. Food & Drug Administration, “Quality System Regulation Amendments,” fda.gov The overall momentum positions the medical stretcher chairs market to benefit from both demographic shifts and health-facility modernization programs.

Key Report Takeaways

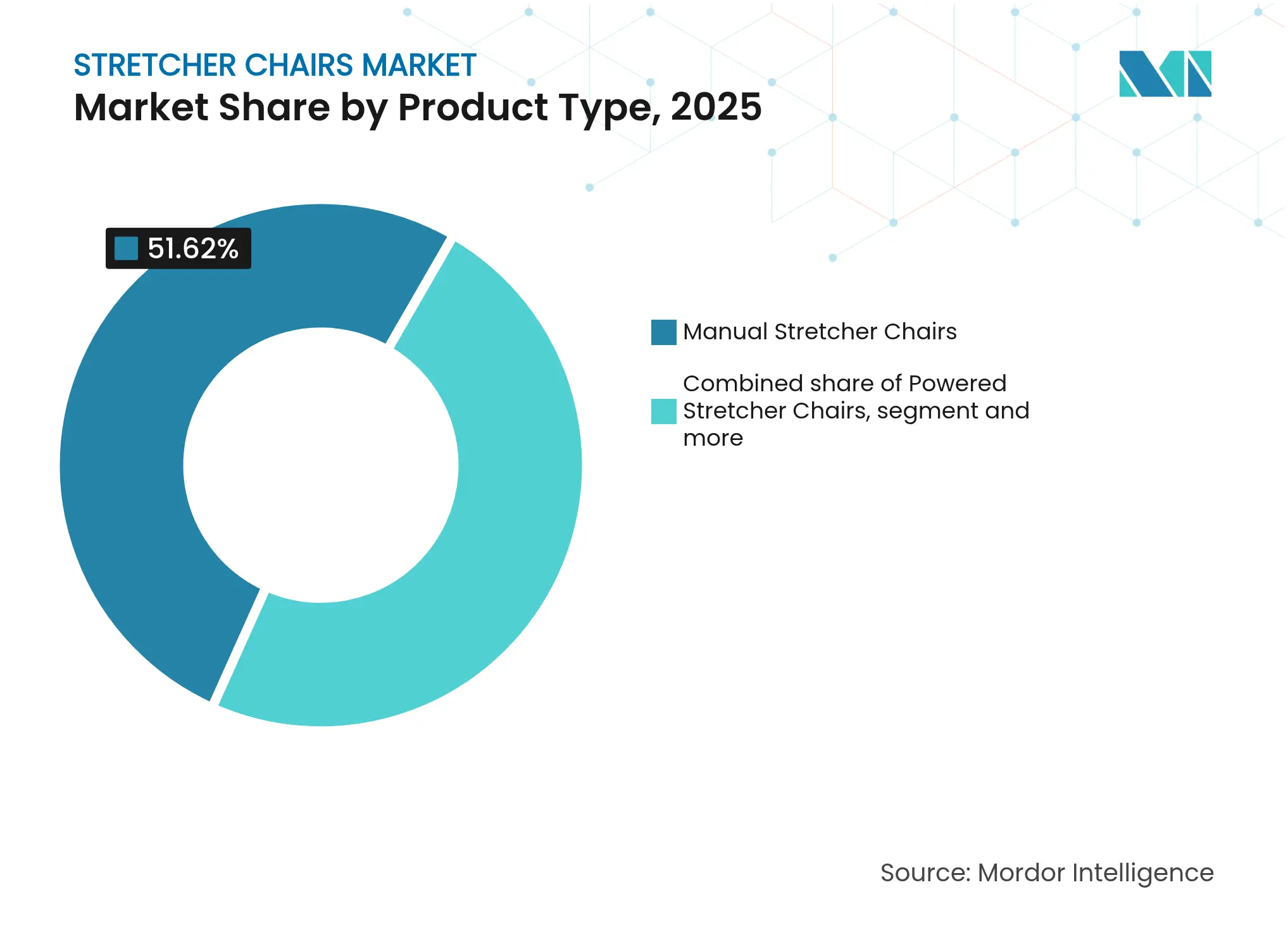

- By product type, manual stretcher chairs led with 51.62% of the medical stretcher chairs market share in 2025; powered variants are projected to grow at a 5.20% CAGR through 2031.

- By actuation technology, hydraulic systems commanded 42.95% share of the medical stretcher chairs market size in 2025, while electric motor systems are advancing at a 5.06% CAGR to 2031.

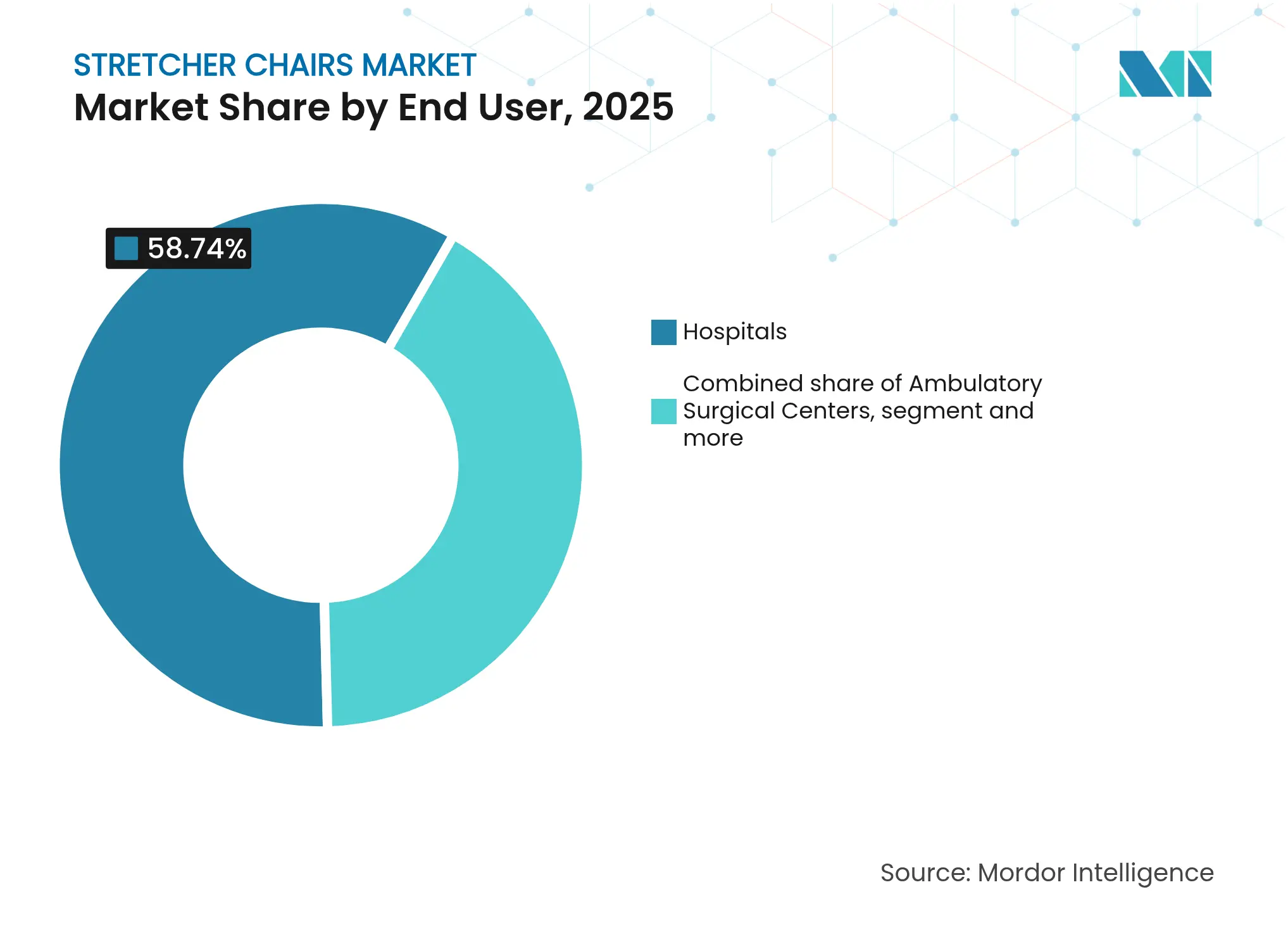

- By end user, hospitals retained 58.74% revenue share in 2025; ASCs are the fastest-growing segment at a 5.37% CAGR.

- By distribution channel, online and e-commerce platforms are forecast to expand at a 5.72% CAGR, the highest among all channels.

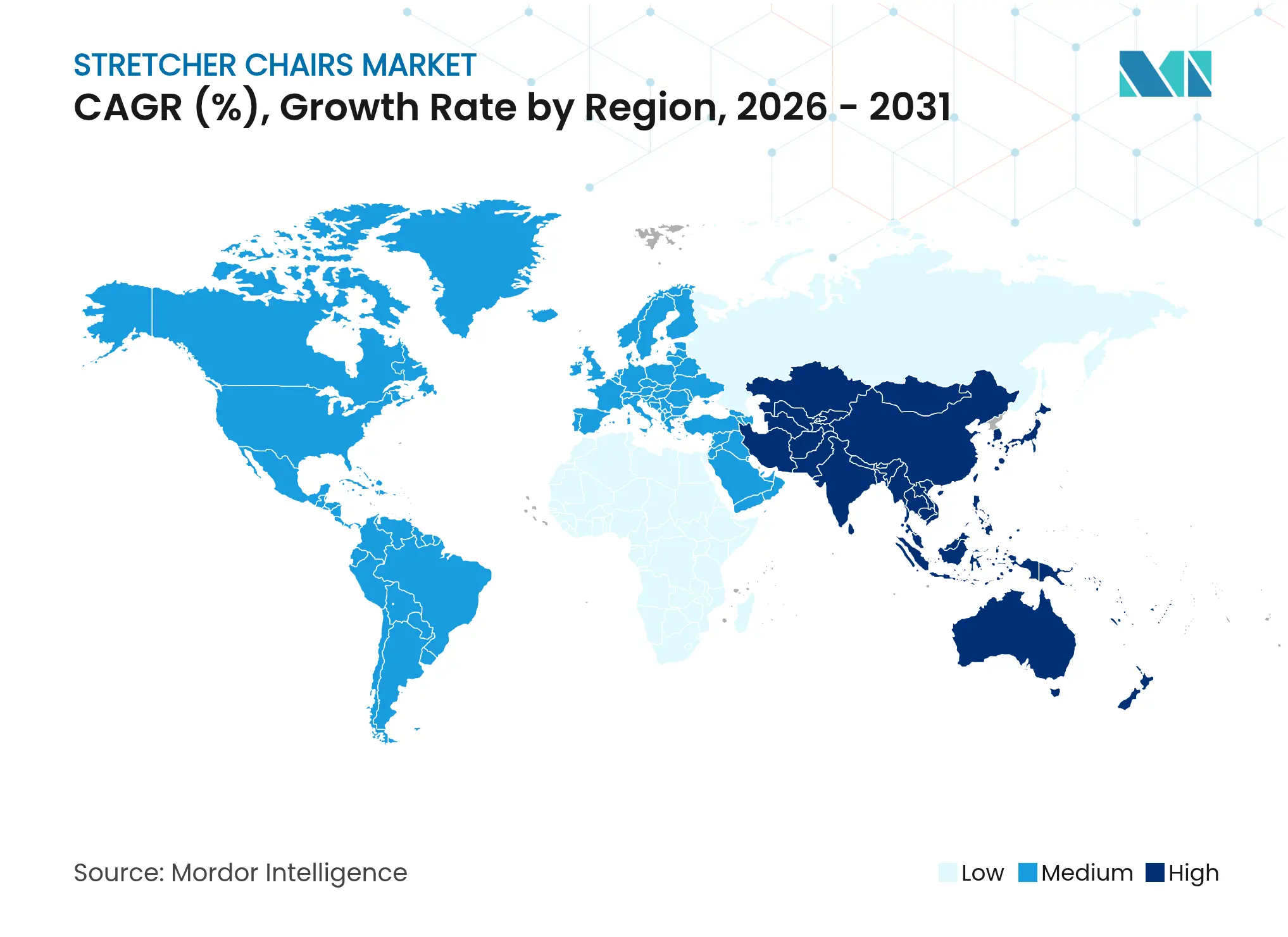

- By geography, North America accounted for 40.73% of the medical stretcher chairs market in 2025, whereas Asia-Pacific is set to grow at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stretcher Chairs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increase in number of accidents & trauma Increase in number of accidents & trauma | +0.8% | Global, higher in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Global, higher in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Rise in geriatric population Rise in geriatric population | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Expansion of ambulatory surgical centers Expansion of ambulatory surgical centers | +1.0% | North America & Europe, emerging in APAC | Short term (≤ 2 years) | |||

Hospital “no-lift” safety initiatives Hospital “no-lift” safety initiatives | +0.7% | North America & EU, regulatory spillover to APAC | Medium term (2-4 years) | |||

Integration with imaging-table systems Integration with imaging-table systems | +0.6% | Global, led by advanced markets | Long term (≥ 4 years) | |||

Demand for bariatric-capable chairs Demand for bariatric-capable chairs | +0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rise in Geriatric Population

The proportion of individuals aged 65 and older is climbing sharply, a demographic transition that elevates day-to-day mobility demands across hospitals, outpatient centers, and long-term-care sites. Facilities respond by specifying stretcher chairs with low transfer heights, integrated vital-sign monitoring, and cushioning that minimizes pressure-injury risk. Compliance imperatives also intensify: updated U.S. Access Board equipment rules require 17-inch transfer heights so most wheelchair users can self-transfer, a standard that accelerates adoption of height-adjustable powered models. For vendors, the aging trend secures multi-year demand visibility and reinforces the medical stretcher chairs market’s orientation toward ergonomic innovations that improve dignity and throughput.

Expansion of Ambulatory Surgical Centers

ASCs are expanding by 16.2% from 2023–2027, supported by Medicare site-neutral payments and relaxed certificate-of-need statutes.[2]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy 2025,” medpac.gov High patient-turnover environments favor stretcher chairs with rapid cleaning surfaces and modular accessories that align with same-day surgery workflows. Equipment capable of seamless imaging integration and lateral tilting further shortens room cycles. The resulting procurement wave positions ASCs as the fastest-growing customer group within the medical stretcher chairs market, prompting manufacturers to tailor service packages and training modules to specialized outpatient requirements.

Hospital “No-Lift” Safety Initiatives

State regulations such as California AB 1136 and OSHA guidance obligate health systems to reduce manual lifting, a mandate that heightens interest in powered stretcher chairs delivering electric height adjustment and drive-assist features. Post-implementation reports cite up to 73% fewer caregiver injuries, a payoff that justifies higher capital cost. AORN’s 2024 perioperative guidelines likewise compel individualized ergonomic plans that favor motorized mobility aids. As hospitals codify safe-patient-handling metrics into purchasing scorecards, the medical stretcher chairs market gains durable support from worker-safety budgets as well as patient-experience programs.

Demand for Bariatric-Capable Chairs

More than 40% of U.S. adults meet obesity criteria, a reality shifting equipment designs toward 500 kg capacity frames, wide surfaces, and high-torque actuators. Liability fears tied to patient-handling injuries amplify urgency, driving facilities to add bariatric lines beyond their immediate caseload needs. Provider Magazine notes that new bariatric units also require updated evacuation plans and doorway modifications, raising total capital exposure but amplifying the imperative to acquire certified solutions. In response, vendors introduce reinforced chassis, track-assist steering, and dual-battery architecture, carving a premium subsegment that lifts average selling prices and margins across the medical stretcher chairs market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital cost of powered chairs High capital cost of powered chairs | -1.1% | Global, more pronounced in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:Global, more pronounced in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Limited reimbursement policies Limited reimbursement policies | -0.9% | North America & Europe, variable in APAC | Medium term (2-4 years) | |||

Regulatory delays for imaging compliance Regulatory delays for imaging compliance | -0.4% | Global, concentrated in advanced markets | Long term (≥ 4 years) | |||

Supply-chain gaps in high-load actuators Supply-chain gaps in high-load actuators | -0.6% | Global, acute in specialized regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Cost of Powered Chairs

Powered stretcher chairs cost roughly 3–5 times more than manual units, challenging budgets of small clinics and facilities in emerging economies. Although reductions in injury claims can offset purchase expense, many administrators must still stage acquisitions over multiple fiscal cycles or shift toward leasing. Vendors counter hesitation by bundling preventative-maintenance contracts and extended batteries that lower lifetime service calls. Over the near term, however, capital intensity will temper conversion speed and carve price-sensitive niches inside the broader medical stretcher chairs market.

Limited Reimbursement Policies

Coverage for advanced stretcher chairs under Medicare’s DMEPOS fee schedule remains inconsistent, particularly for features such as imaging-table compatibility and smart telemetry. Manufacturers are pressed to secure specific HCPCS coding before product launch while educating payers on clinical value. In Europe and Asia-Pacific, reimbursement variance across national programs can lengthen approval timelines and fragment demand. Limited coverage therefore dampens uptake in home-health and long-term-care settings, restraining full potential of the medical stretcher chairs market during the forecast horizon.

Segment Analysis

By Product Type: Manual Dominance Faces Powered Disruption

Manual units accounted for 51.62% of the medical stretcher chairs market in 2025 thanks to cost advantages and minimal training needs. Powered models, however, are accelerating at a 5.20% CAGR as facilities prioritize caregiver safety and compliance metrics. This migration is reflected in the medical stretcher chairs market size for powered variants, which is projected to expand faster than any other product category through 2031. Early conversions often begin in emergency departments and surgical suites, but replacement cycles are now spreading to imaging wings and outpatient clinics.

Powered designs integrate joystick steering, battery health indicators, and usage analytics that feed directly into hospital asset-management systems. Their higher upfront price is counterbalanced by fewer worker compensation claims and shorter transfer times, reinforcing total-cost propositions. Manufacturers are also introducing hybrid systems that allow manual fallback during battery depletion, reducing risk perception among procurement teams. Collectively, these dynamics underpin a gradual yet durable shift that will redefine product-mix composition inside the medical stretcher chairs market.

Note: Segment shares of all individual segments available upon report purchase

By Actuation Technology: Hydraulic Stability Versus Electric Precision

Hydraulic platforms held 42.95% of the medical stretcher chairs market share in 2025 due to proven load-bearing reliability and smooth motion. Electric motor systems, though, are expanding at a 5.06% CAGR, propelled by precision positioning, lower energy usage, and seamless integration with digital infrastructures. Facilities seeking data-rich maintenance programs opt for electric actuators because onboard sensors feed real-time diagnostics to central dashboards.

Electromechanical research indicates 35–50% energy savings compared with hydraulics, a benefit aligned with hospital sustainability goals. Battery advances also mitigate prior concerns over duty cycles. Hybrid configurations, pairing hydraulic lifting with electric tilting, gain popularity in bariatric contexts where fail-safe margin remains paramount. As a result, the medical stretcher chairs market size for electric solutions is expected to close the gap on hydraulics during the forecast period, although both technologies will coexist to address varying acuity and budget tiers.

By End User: Hospital Dominance Amid ASC Acceleration

Hospitals generated 58.74% of medical stretcher chairs market revenues in 2025, reflecting broad procedural ranges and higher patient acuity. Yet ASCs are advancing at a 5.37% CAGR through 2031, capitalizing on reimbursement policies that reward same-day procedures. This dual-channel dynamic pressures suppliers to deliver configurable platforms: robust enough for emergency departments yet nimble enough for small-footprint ASC suites.

In hospitals, demand skews toward multi-function chairs that move seamlessly from imaging to recovery, minimizing equipment swaps and infection-control breaches. ASCs, by contrast, specify quick-clean upholstery and compact turning radii that enhance room turnover. Specialty clinics and home-health providers add further granularity with lightweight transport and fold-down models. The expanding spectrum of users therefore widens design requirements, lifting overall innovation velocity inside the medical stretcher chairs market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates E-commerce Growth

Direct institutional contracts still dominate high-value orders, yet online platforms are projected to rise at a 5.72% CAGR, the fastest of all channels. Procurement teams increasingly rely on e-catalogs that display 3-D models, regulatory certificates, and real-time inventory. Transparent pricing and shorter quotation cycles favor online conversions, especially for standardized SKUs destined for satellite clinics.

Distributors retain importance for bundled supply agreements that align mobility equipment with consumables and servicing. Meanwhile, manufacturers pursue omnichannel strategies: virtual demonstrations coupled with local service partners ensure installation quality without sacrificing digital convenience. This hybrid approach further widens access, particularly in emerging Asia-Pacific markets where end users lack on-site biomedical engineers. Consequently, channel evolution reinforces overall growth momentum of the medical stretcher chairs market while reallocating margin structures across the supply chain.

Geography Analysis

North America led with 40.73% share of the medical stretcher chairs market in 2025. Uptake is driven by OSHA-backed safety mandates, Medicare payment incentives favoring ASCs, and the 2024 CDC Safe Patient Handling framework that standardizes mobility protocols. Hospitals invest heavily in powered solutions to meet state “no-lift” laws, whereas bariatric models gain prominence amid obesity rates exceeding 40%. Robust aftermarket service networks and established capital-budget cycles sustain recurring demand even as capital scrutiny intensifies.

Asia-Pacific is poised for the fastest 6.15% CAGR through 2031, buoyed by healthcare infrastructure projects in China, India, and Southeast Asia. Government insurance expansions broaden equipment budgets, while private operators add high-acuity specialty centers that specify advanced mobility solutions. Local manufacturing clusters reduce component costs, but regional buyers still import premium actuators and control modules. Harmonization of ASEAN medical device regulations lowers entry barriers for multinational suppliers, amplifying competitive depth within the regional medical stretcher chairs market.

Europe maintains steady adoption on the back of aging demographics, unified MDR compliance, and national initiatives that reward ergonomic upgrades in long-term care. Hospitals prioritize stretcher chairs certified to EN 60601-2-52 bed safety standards, while procurement frameworks in the United Kingdom and Nordic countries increasingly apply lifecycle carbon-footprint scoring. Brexit-related customs checks have elongated lead times for U.K. buyers, nudging some toward regional sourcing strategies. Sustainability metrics combined with stringent worker-safety regulations underpin a consistent, if slower, contribution to overall medical stretcher chairs market expansion.

Competitive Landscape

Market Concentration

The competitive arena is moderately concentrated, with a core group of multinational manufacturers controlling a significant portion of global shipments. These leaders differentiate through platform architectures that support modular accessories, imaging integration, and cloud-based asset monitoring. For example, Stryker’s Prime Connect ecosystem links stretcher chair telemetry directly to nurse-call systems, offering fall-prevention alerts and predictive maintenance.

Supply-chain resilience is an emerging battleground. Access to high-load actuators and PTFE-based low-friction bearings became constrained in 2024, exposing smaller firms to production delays. Larger players mitigate risk via multisourcing and vertical integration of casting and powder-coat operations. Regulatory acumen provides further advantage as FDA’s 2026 quality system amendments tighten documentation thresholds; companies with dedicated compliance teams secure faster 510(k) clearances, reinforcing market share positions inside the medical stretcher chairs market.

M&A activity underscores the value of scale. MIGA Holdings’ November 2024 acquisition of Invacare’s North American business consolidates distribution reach, while Drive DeVilbiss Healthcare’s Mobility Designed purchase adds advanced industrial design talent. Start-ups gravitate toward niches—imaging-compatible trolleys or ultra-light evacuation chairs—yet often license their innovations to majors to overcome global service-network deficits. Competitive intensity is therefore shaped by technology pipelines, regulatory readiness, and after-sales coverage rather than price alone, sustaining a balanced but dynamic medical stretcher chairs market.

Stretcher Chairs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stryker introduced the Xpedition powered stair chair with a 500-pound capacity and track-drive system for single-operator safety.

- November 2024: MIGA Holdings LLC completed its acquisition of Invacare’s North American business, expanding portfolio depth and service infrastructure.

- June 2024: Drive DeVilbiss Healthcare acquired Mobility Designed, adding user-centric design expertise to its mobility portfolio.

- March 2024: Stryker debuted Stair-TREAD evacuation solutions at Criticare 2024, addressing emergency egress requirements in multi-story facilities.

Table of Contents for Stretcher Chairs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increase in number of accidents & trauma

- 4.2.2Rise in geriatric population

- 4.2.3Expansion of ambulatory surgical centers

- 4.2.4Hospital “no-lift” safety initiatives

- 4.2.5Integration with imaging-table systems

- 4.2.6Demand for bariatric-capable chairs

- 4.3Market Restraints

- 4.3.1High capital cost of powered chairs

- 4.3.2Limited reimbursement policies

- 4.3.3Regulatory delays for imaging compliance

- 4.3.4Supply-chain gaps in high-load actuators

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Powered Stretcher Chairs

- 5.1.2Manual Stretcher Chairs

- 5.1.3Others

- 5.2By Actuation Technology

- 5.2.1Electric Motor

- 5.2.2Hydraulic

- 5.2.3Pneumatic

- 5.2.4Mechanical

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Ambulatory Surgical Centers

- 5.3.3Specialty Clinics

- 5.3.4Home-Care Settings

- 5.3.5Others

- 5.4By Distribution Channel

- 5.4.1Direct Institutional Sales

- 5.4.2Medical Supply Distributors

- 5.4.3Online / E-commerce

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Stryker Corporation

- 6.3.2GF Health Products, Inc.

- 6.3.3Winco Mfg LLC (Champion Manufacturing Inc.)

- 6.3.4Wy’East Medical

- 6.3.5IBIOM Instruments Ltée

- 6.3.6Productos Metálicos del Bages (Promeba)

- 6.3.7NovyMed International

- 6.3.8UFSK-International OSYS

- 6.3.9LINET Group SE

- 6.3.10Drive DeVilbiss Healthcare (Medical Depot, Inc. )

- 6.3.11Invacare Corporation

- 6.3.12Ferno-Washington

- 6.3.13TransMotion Medical

- 6.3.14Midmark Corporation

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Stretcher Chairs Market Report Scope

As per the scope of the report, stretcher chairs are used to conveniently carry patients from one place to another within and outside of a healthcare center. The Stretcher Chairs market is segmented by Product (Powered Chairs, Manual Chairs), by End-User (Hospitals, Ambulatory Surgical Centers, and Others), and by Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.