Stem Cell Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

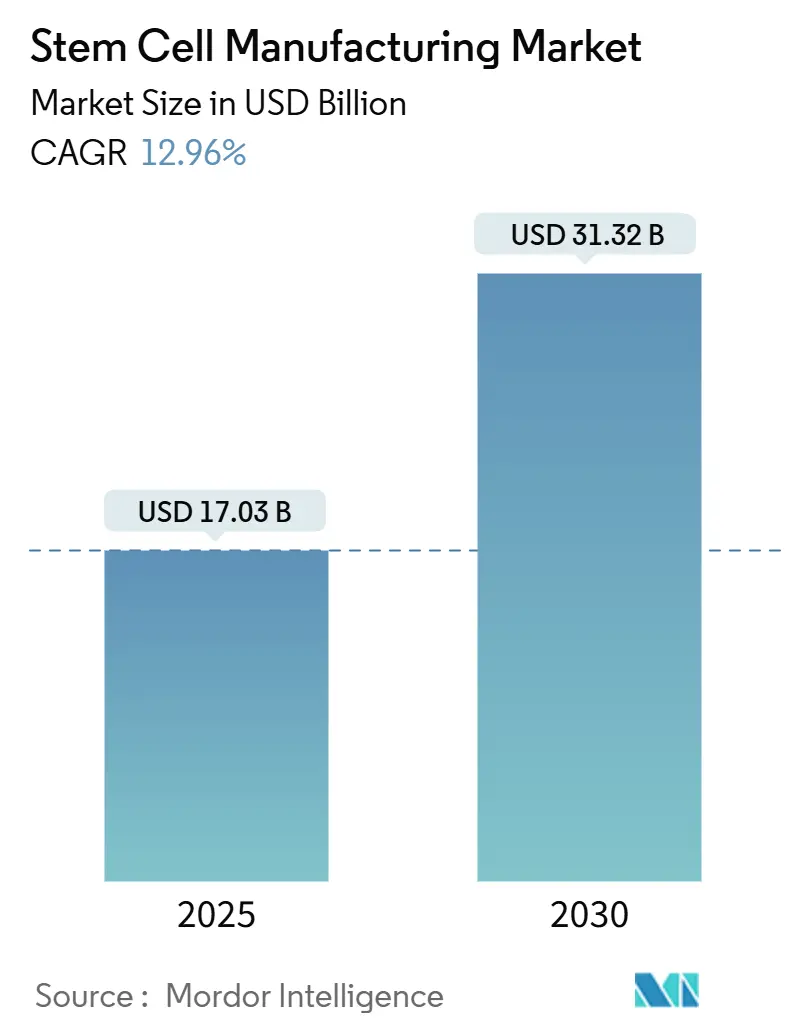

| Market Size (2025) | USD 17.03 Billion |

| Market Size (2030) | USD 31.32 Billion |

| Growth Rate (2025 - 2030) | 12.96% CAGR |

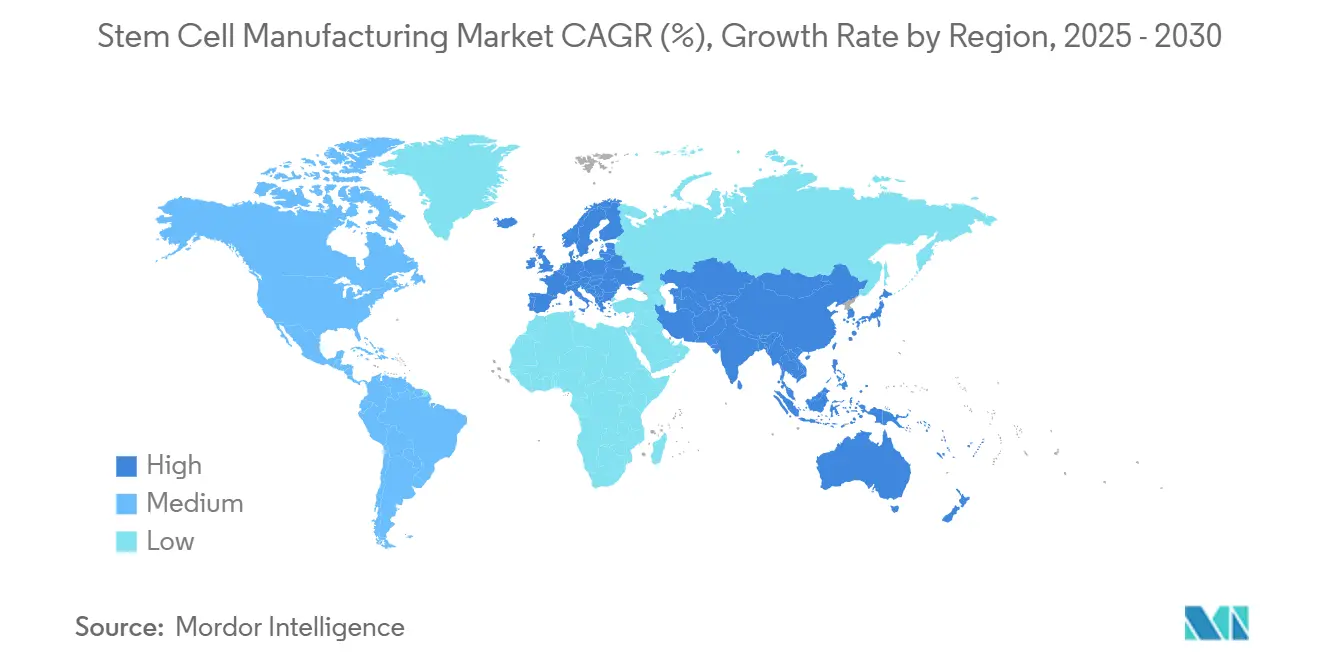

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stem Cell Manufacturing Market Analysis by Mordor Intelligence

The Stem Cell Manufacturing Market size is estimated at USD 17.03 billion in 2025, and is expected to reach USD 31.32 billion by 2030, at a CAGR of 12.96% during the forecast period (2025-2030). Rising adoption of automated, closed-system bioreactors, regulatory harmonization in major economies, and the need for large-batch production to serve regenerative therapies collectively underpin this growth trajectory. Consumables remain the single largest revenue contributor, reflecting their recurring use in every production run, while instruments are scaling fastest as manufacturers deploy robotics and advanced analytics to counter talent shortages. North America retains leadership through strong FDA frameworks and sustained public–private funding, whereas Asia Pacific posts the quickest expansion on the back of policy modernization in Japan and China.[1]Source: Takamasa Hirai et al., “Country-specific regulation and international standardization of cell-based therapeutic products,” cell.com The transition from manual workflows toward single-use technologies is lowering contamination risk and enabling distributed manufacturing close to clinical sites. However, bottlenecks in fetal bovine serum supply and a global skills crunch in bioprocess engineering pose near-term operational challenges.

Key Report Takeaways

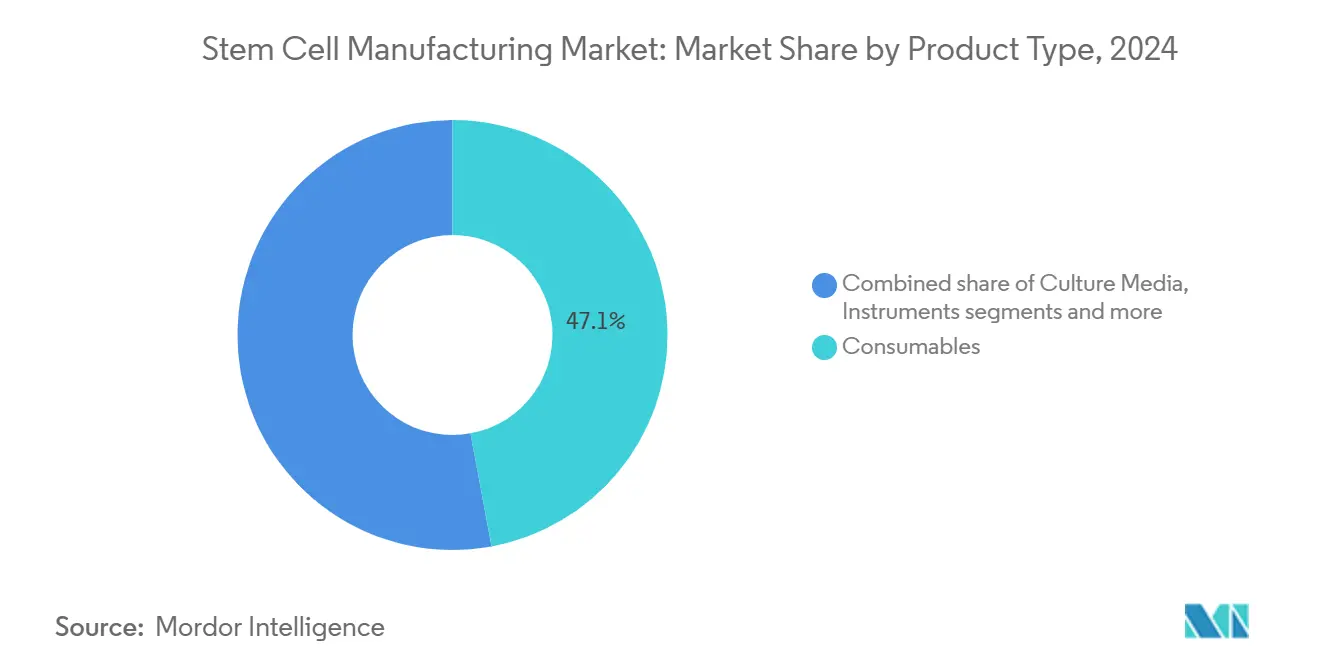

- By product type, consumables held 47.12% of the stem cell manufacturing market share in 2024, while instruments are projected to expand at a 13.85% CAGR through 2030.

- By application, stem cell therapy accounted for 51.75% of the stem cell manufacturing market size in 2024; stem cell banking is poised for the highest growth at 14.63% CAGR to 2030.

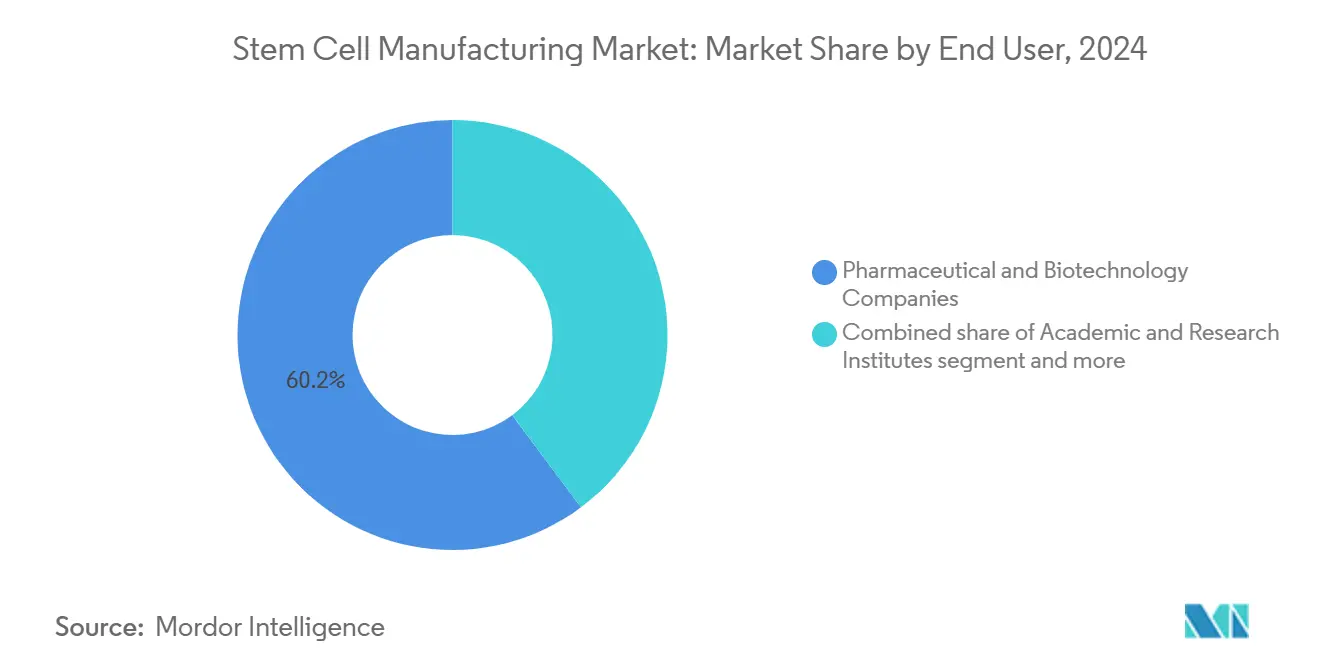

- By end user, pharmaceutical and biotechnology companies commanded 60.23% revenue share in 2024, whereas academic and research institutes are forecast to rise at a 13.92% CAGR through 2030.

- By geography, North America led with 41.32% market share in 2024, while Asia Pacific is the fastest-growing region at a 14.22% CAGR to 2030.

Global Stem Cell Manufacturing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automated, closed-system bioreactors & single-use tech | +2.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Growing public–private funding for stem-cell R&D | +2.1% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Rising chronic-disease burden fueling regenerative demand | +1.9% | Global, with highest impact in aging populations | Long term (≥ 4 years) |

| Growing public awareness about therapeutic potency | +1.4% | APAC & emerging markets, spillover to established regions | Medium term (2-4 years) |

| Favorable regulatory and policy support | +1.2% | Japan, EU, with gradual expansion to other regions | Short term (≤ 2 years) |

| Strategic collaborations and market expansion | +0.8% | Global, concentrated in biotech hubs | Medium term (2-4 years) |

Source: Mordor Intelligence

Automated, Closed-System Bioreactors Transform Manufacturing Paradigms

Industrial deployment of automated, closed-system bioreactors is redefining production economics across the stem cell manufacturing market. Lonza’s Cocoon platform cuts human intervention by up to 70% while maintaining GMP compliance, directly alleviating the global shortage of skilled operators. Job postings for bioprocess engineers climbed 400% between 2019 and 2023, yet remain difficult to fill, underscoring the urgency of automation.[2]Source: UC Davis Continuing Education, “Career Outlook: Cell and Gene Therapy,” cpe.ucdavis.edu Single-use assemblies reduce cross-contamination and lower facility footprints, enabling distributed production models that place manufacturing closer to point-of-care delivery. The University of Technology Sydney’s 3D-printed microfluidic harvester integrates multiple steps into one device, shrinking cost per batch and improving cell viability. Collectively, these innovations anchor a long-term uplift in capacity that underpins the market’s 12.96% CAGR outlook.

Growing Public-Private Funding Accelerates Commercial Translation

Escalating government initiatives and industry alliances continue to channel capital into advanced facilities and workforce programs. The National Institute for Innovation in Manufacturing Biopharmaceuticals (NIIMBL) sponsors collaborative projects that de-risk scale-up challenges while offering experiential training to new technicians. Biofoundry models, often housed within academic settings, are shortening iteration cycles and enabling small firms to access state-of-the-art infrastructure without heavy capital outlay. These funding streams improve technology readiness levels and bring novel therapies closer to commercial launch, solidifying the long-term demand base across the stem cell manufacturing market.

Rising Chronic-Disease Burden Creates Sustained Demand Pull

Chronic conditions such as cardiovascular disorders, diabetes, and neurodegenerative diseases are escalating sharply among aging populations, intensifying demand for regenerative solutions that conventional pharmacology cannot adequately address. The FDA’s approval of Lantidra for Type 1 diabetes in 2024 signaled regulatory willingness to endorse living-cell products for mainstream indications. Concurrently, Japan’s expedited conditional approval pathway fast-tracks therapies with promising early data, compressing timelines and incentivizing manufacturing expansion. The combination of demographic pressure and progressive regulation is strengthening investor confidence, catalyzing new plant builds and equipment upgrades throughout the stem cell manufacturing market.

Public Awareness Drives Market Acceptance and Investment

Education initiatives spearheaded by organizations like the International Society for Cell & Gene Therapy (ISCT) are elevating general understanding of cell-based treatments, translating scientific advances into tangible patient demand. Government-backed outreach in markets such as South Korea and Singapore positions regenerative medicine as a national priority, stimulating enrollment in clinical trials and encouraging insurance payors to consider reimbursement pathways. Expanding vocational curricula and apprenticeships, exemplified by the Canadian Alliance for Skills and Training in Life Sciences (CASTL), are simultaneously addressing workforce gaps and cementing public trust. Heightened awareness stabilizes revenue forecasts and supports long-term capital planning for manufacturers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GMP operational costs | -1.8% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Complex regulatory and ethical hurdles | -1.2% | EU & emerging markets, moderate impact in US/Japan | Long term (≥ 4 years) |

| Shortage of cell-manufacturing bioprocess engineers | -1.0% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Supply-chain bottlenecks for GMP growth factors and vectors | -0.9% | Global, with regional variations in severity | Medium term (2-4 years) |

Source: Mordor Intelligence

High GMP Operational Costs Constrain Market Entry

Building and running GMP-compliant facilities requires USD 10–50 million in upfront investments, with operating expenses consuming 15–25% of annual revenue, challenging small firms and emerging nations. Larger incumbents leverage economies of scale and diversified product portfolios to absorb these costs, widening competitive gaps. Bio-Techne’s transition to animal-free reagents illustrates how vendors must continuously invest in compliance-driven process upgrades while balancing cost containment. Contract manufacturing organizations (CMOs) specializing in cell therapies are beginning to democratize access, yet capacity remains limited relative to demand.

Complex Regulatory Frameworks Slow Global Market Development

Divergent regulatory classifications, such as the European Union’s Advanced Therapy Medicinal Products (ATMP) rules, extend development timelines and inflate submission costs. For combination products blending cells with devices, pathway ambiguity persists, creating additional uncertainty. Efforts by the FDA’s CoGenT Global pilot aim to harmonize approaches, but practical convergence remains nascent. Emerging economies face capacity gaps in regulatory expertise, slowing domestic approvals despite strong therapy demand, thus tempering the overall stem cell manufacturing market CAGR.

Segment Analysis

By Product Type: Consumables Hold the Lion’s Share While Instruments Accelerate

In 2024, consumables accounted for 47.12% of the stem cell manufacturing market share, underscoring the indispensability of media, reagents, and single-use assemblies to every production run. Recurrent demand ensures stable cashflows, allowing suppliers to invest in serum-free and chemically defined formulations that mitigate contamination risk and combat the looming fetal bovine serum shortage. Instruments, although smaller in absolute revenue today, are projected to register a 13.85% CAGR through 2030 as facilities install closed-system bioreactors, automated cell sorters, and AI-enabled monitoring probes. The stem cell manufacturing industry is witnessing a surge in strategic alliances between equipment vendors and therapy developers, enabling real-time process optimization and reducing batch failures.

Emerging platform technologies exemplify the transformational nature of the instrument segment. Ori Biotech’s IRO system delivers 70% labor reduction and 50% cost savings, highlighting how smart hardware can reset production cost baselines. Integration of machine learning models into bioreactors allows dynamic adjustment of feed rates and oxygenation, elevating reproducibility. Consumable suppliers are responding by bundling sensors and pre-sterilized bags, creating end-to-end kits that simplify validation. Collectively, these trends diversify revenue pools and enhance resilience across the stem cell manufacturing market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Therapeutic Programs Dominate While Banking Gains Momentum

Therapeutic applications represented 51.75% of the stem cell manufacturing market size in 2024, buoyed by the FDA’s expectation of 10–20 cell-based approvals annually by 2025. Developers prioritize scalable allogeneic platforms that serve global patient populations, propelling demand for high-volume, GMP-grade batches. Tissue engineering solutions, aided by 3D-bioprinting advances, further expand clinical pipelines targeting musculoskeletal and dermal indications. Meanwhile, drug discovery and toxicology workflows use induced pluripotent stem cells (iPSCs) to generate disease-specific models, creating parallel demand streams for smaller yet recurrent batch sizes.

Stem cell banking, though holding a smaller revenue base today, is forecast to post a 14.63% CAGR, driven by public cord-blood initiatives and diversification into adipose and dental pulp sources. Automated cryopreservation systems ensure >90% post-thaw viability, elevating confidence among clinicians. The stem cell manufacturing industry benefits from banking’s annuity-style revenue model: one-time collection fees translate into multi-decade storage income, stabilizing cashflows during fluctuating therapy approval cycles. As reimbursement frameworks evolve, stored cellular assets could serve as the raw material for personalized therapies, reinforcing demand for banked inventories and downstream manufacturing services.

By End User: Pharmaceutical Leaders Leverage Scale While Academia Accelerates Innovation

Pharmaceutical and biotechnology firms captured 60.23% of 2024 revenue, capitalizing on established quality systems and regulatory infrastructures to run multi-product cell therapy suites. Large incumbents integrate stem cell platforms into existing biologics plants, extracting economies of scope and expediting tech-transfer timelines. CMOs embedded within this cohort address capacity bottlenecks by offering turnkey GMP capabilities to venture-backed biotech entrants.

Academic and research institutes, supported by programs such as the NSF-funded Center for Cell Manufacturing Technologies (CMaT), are the fastest-growing end-user class with a 13.92% CAGR. Beyond basic science, universities run pilot-scale GMP suites that de-risk early-phase clinical materials while training a new technical workforce. This dual role enhances translational throughput and tempers the talent deficit constraining the broader stem cell manufacturing market. Hospitals and specialized clinics adopt point-of-care micro-factories to prepare autologous doses onsite, albeit at a modest growth rate, given reimbursement complexities and space constraints. Together, these dynamics foster a heterogeneous customer landscape that demands configurable manufacturing solutions.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 41.32% revenue share in 2024, driven by the world’s largest cluster of cell therapy developers, abundant venture capital, and FDA pathways such as RMAT and accelerated approval that shorten commercialization lead times. The region also houses the highest concentration of CMOs, offering flexible capacity to smaller sponsors. Yet the acute shortfall of bioprocess engineers—vacancies outpace qualified candidates three-to-one—could restrain build-out plans unless workforce initiatives gain further traction. Partnerships among community colleges, NIIMBL, and industry accelerate technician training, but competition from mRNA and viral-vector facilities intensifies hiring pressures.

Asia Pacific is the fastest-growing territory, projected to log a 14.22% CAGR as Japan’s conditional approval scheme[3]Source: Japan PMDA, “Regulatory Frameworks of Regenerative Medicines,” pmda.go.jp and China’s sizeable provincial subsidies encourage rapid scaling of local plants. South Korea’s authorization of 16 cell-based products, including three stem cell therapies, underscores regulatory maturity and positions the peninsula as an exporter of manufacturing know-how. Furthermore, cost-competitive labor and land in China and India lure multinational firms to establish satellite facilities, diversifying supply chains. However, disparate approval procedures among ASEAN members still create time-to-market frictions that multinational sponsors must navigate carefully.

Europe commands a significant but more regulated market environment. The European Medicines Agency’s ATMP framework sets stringent quality benchmarks, which extend development timelines yet elevate global confidence in product safety. Implementation of the European Pharmacopoeia chapter on cell-based products offers clearer analytical standards, easing some validation uncertainties. Funding from Horizon Europe and national programs continues to support infrastructure upgrades, while public skepticism toward animal-derived components accelerates adoption of chemically defined media. Smaller regions such as the Middle East and Africa and South America observe emergent local initiatives—Brazilian and South African centers now pilot stem cell transplant programs—yet limited capital and skills infrastructures temper near-term scale-up prospects.

Competitive Landscape

Top Companies in Stem Cell Manufacturing Market

Competitive intensity across the stem cell manufacturing market is moderate. Thermo Fisher Scientific and Lonza leverage vertically integrated portfolios encompassing consumables, instruments, and contract services, which fosters customer loyalty through one-stop solutions. Continuous investment in single-use bioreactors and closed-system fill/finish lines positions these players at the forefront of automation. Mid-sized innovators such as Ori Biotech employ disruptive hardware to slash labor costs by 70%, appealing to early-stage developers seeking lean capex models.

Traditional life-science equipment firms including Beckman Coulter are entering the segment with purification platforms tailored for cell-based batches, intensifying pricing pressure and speeding technological convergence. Contract manufacturers expand geographically—Lonza in Houston and WuXi in Shanghai—providing global clients with multi-jurisdictional production footprints that ease regulatory submissions. Meanwhile, smaller regional CMOs focus on niche processes like exosome isolation, carving defensible positions through specialization.

Overall, differentiation hinges on automation depth, regulatory track record, and capacity scalability. Companies that couple modular hardware with robust digital twins can offer guaranteed batch reproducibility, a decisive advantage as therapy sponsors prepare for late-stage trials. Intellectual-property light barriers and knowledge-intensive operations favor alliances: equipment suppliers partner with therapy developers to co-create optimized workflows, while reagent vendors bundle consumables with software analytics. The ecosystem thus coalesces around platform partnerships that accelerate market penetration and enhance stickiness across the stem cell manufacturing market.

Stem Cell Manufacturing Industry Leaders

-

Lonza Group AG

-

Fujifilm Holdings Corporation (Cellular Dynamics)

-

Merck KGaA

-

STEMCELL Technologies

-

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: STEMCELL Technologies acquired Cellular Highways Ltd., expanding into advanced microfluidic cell-sorting systems targeting fragile cell populations.

- May 2025: REPROCELL introduced StemEdit human iPSC non-HLA class I and class I/II knockout lines to streamline allogeneic therapy development.

- July 2024: Bioserve India launched REPROCELL stem cell product lines in India to strengthen domestic regenerative-medicine research.

Global Stem Cell Manufacturing Market Report Scope

As per the scope of the report, a stem cell is a cell with the unique ability to develop into particular cell types in the body. In the future, they may be used to replace cells and tissues that have been damaged or lost due to disease. The Stem Cell Manufacturing Market is Segmented by Type (Products (Culture Media, Consumables, Instruments, Stem Cell Lines and Services), Application (Stem Cell Therapy, Drug Discovery and Development, and Stem Cell Banking), End User (Pharmaceutical and Biotechnology Companies, Cell Banks and Tissue Banks, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product Type | Culture Media | ||

| Consumables | |||

| Instruments | |||

| Stem Cell Lines | |||

| Services | |||

| By Application | Stem Cell Therapy | ||

| Drug Discovery and Toxicology | |||

| Stem Cell Banking | |||

| Tissue Engineering and Regenerative Medicine | |||

| By End User | Pharmaceutical and Biotechnology Companies | ||

| Academic and Research Institutes | |||

| Cell and Tissue Banks | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Culture Media |

| Consumables |

| Instruments |

| Stem Cell Lines |

| Services |

| Stem Cell Therapy |

| Drug Discovery and Toxicology |

| Stem Cell Banking |

| Tissue Engineering and Regenerative Medicine |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Cell and Tissue Banks |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the stem cell manufacturing market?

The stem cell manufacturing market is valued at USD 17.03 billion in 2025 with a forecast to reach USD 31.32 billion by 2030.

Which product segment generates the highest revenue today?

Consumables lead with 47.12% market share owing to their recurring use in every cell culture run.

Why are automated bioreactors considered critical for future growth?

Automated, closed-system bioreactors cut human intervention by up to 70%, mitigate contamination risk, and alleviate the global shortage of skilled bioprocess engineers.

Which geographic region will grow fastest through 2030?

Asia Pacific, buoyed by regulatory modernization and cost-efficient manufacturing capacity, is projected to expand at a 14.22% CAGR.

How do stem cell banks contribute to market expansion?

Stem cell banking offers annuity-style revenues and supports future personalized therapies, driving a 14.63% CAGR within the application segment.

What are the primary hurdles to new market entrants?

High GMP facility costs, complex multinational regulations, and supply chain constraints for critical reagents are the main barriers.

Page last updated on: June 23, 2025