Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

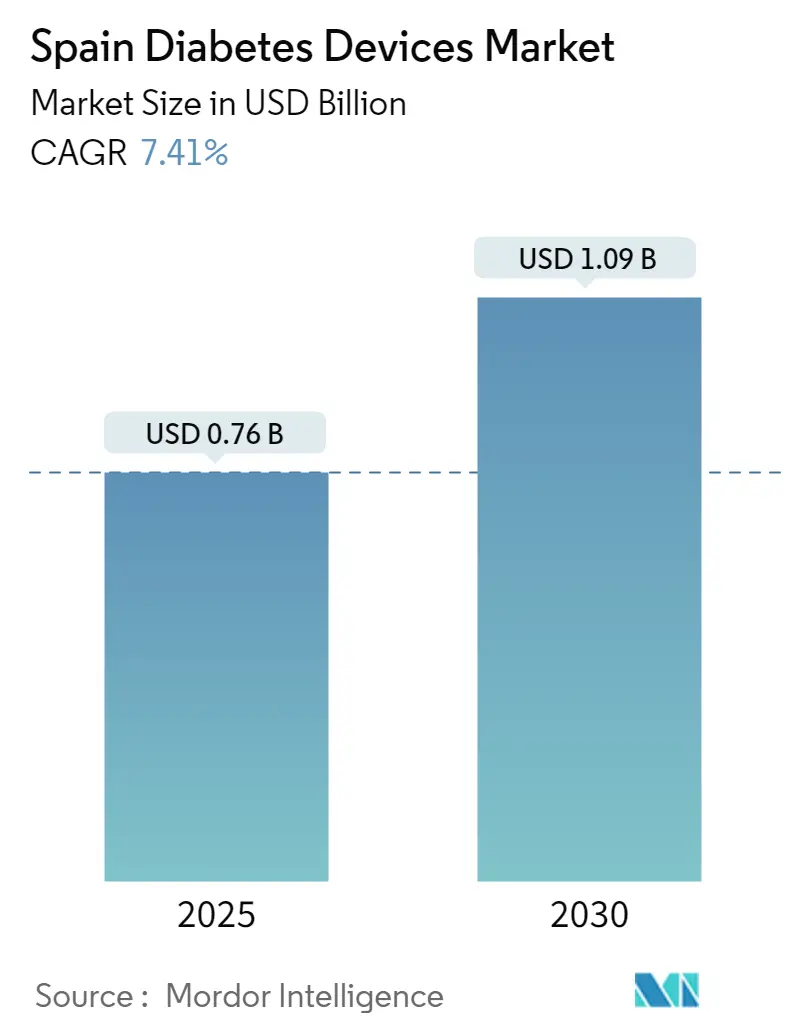

| Market Size (2025) | USD 0.76 Billion |

| Market Size (2030) | USD 1.09 Billion |

| Growth Rate (2025 - 2030) | 7.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Diabetes Devices Market Analysis by Mordor Intelligence

The Spain diabetes devices market is valued at USD 760 million in 2025 and is projected to reach USD 1,090 million by 2030, expanding at a 7.41% CAGR. Growth stems from rising diabetes prevalence, wider continuous glucose monitoring (CGM) reimbursement, and integration with Spain’s national e-prescription platform. The shift from reactive treatment to proactive monitoring is accelerating demand for Bluetooth-enabled glucometers, smart insulin pens, and hybrid closed-loop pumps. Multinational producers are strengthening local partnerships to navigate Spain’s decentralized procurement, while regional distributors are using their familiarity with autonomous community tenders to gain share. Retail pharmacies, bolstered by Grupo Cofares’ expansion, now serve as full-service diabetes hubs offering device education and refill services. Across the Spain diabetes devices market, cybersecurity certification hurdles and price caps on consumables temper pricing power but also motivate manufacturers to highlight product safety and cost-effectiveness.

Key Report Takeaways

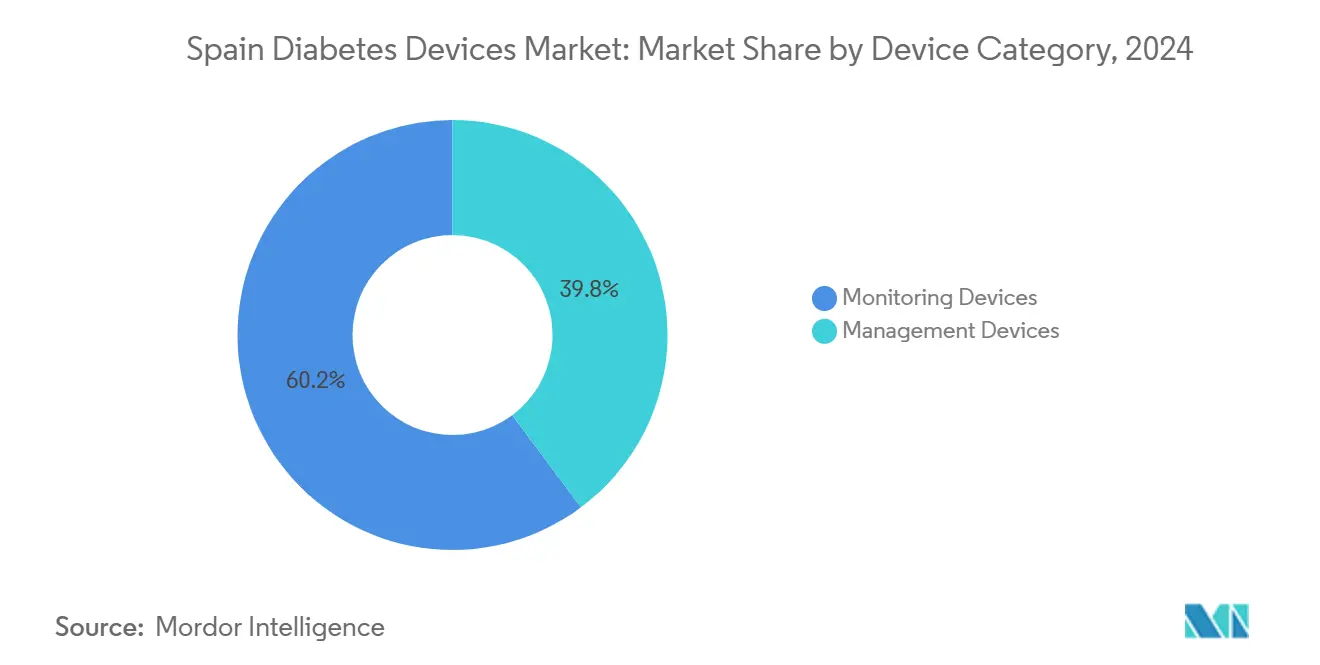

- By device category, Monitoring Devices led with 60.24% revenue share in 2024; Continuous Glucose Monitoring is projected to advance at an 8.41% CAGR to 2030.

- By end-user, hospitals held 46.12% of the Spain diabetes devices market share in 2024, while home-care settings are set to expand at a 7.81% CAGR through 2030.

- By distribution channel, retail pharmacies accounted for 55.35% share of the Spain diabetes devices market size in 2024 and remain pivotal as online pharmacies log the fastest growth at 8.23% CAGR.

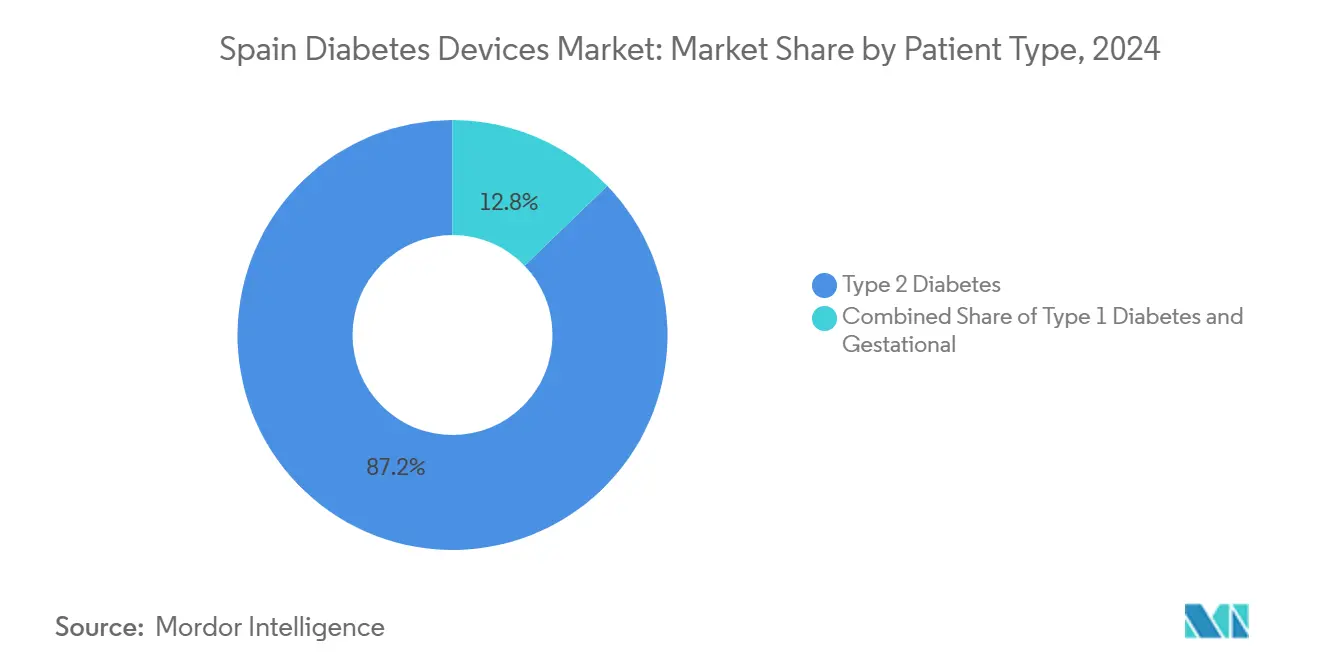

- By patient type, Type 2 diabetes dominated with 87.29% share of the Spain diabetes devices market size in 2024; Type 1 diabetes shows the highest projected CAGR at 7.92% to 2030.

- By device connectivity, non-connected products retained 78.64% share in 2024; Bluetooth/Wireless devices post the strongest growth at 9.16% CAGR.

Spain Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing‐linked Diabetes Prevalence Spike in Southern & Coastal Spain | +1.5% | Southern regions (Andalusia, Valencia) and coastal areas (Canary Islands) | Long term (≥ 4 years) |

| Roll-out of Primary-Care–Driven CGM Reimbursement (2024) | +1.2% | National, with early adoption in Catalonia, Basque Country, and Madrid | Medium term (2-4 years) |

| Surge in Hybrid‐Closed-Loop Clinical Trials at Spanish University Hospitals | +0.9% | Urban centers with university hospitals (Barcelona, Madrid, Valencia, Seville) | Medium term (2-4 years) |

| Employer-backed diabetes-wellness programs | +0.7% | Catalonia & Madrid | Medium term (2-4 years) |

| Retail-pharmacy Penetration of Smart Pens via Grupo Cofares | +1.1% | National, with concentration in urban areas | Short term (≤ 2 years) |

| Growth of e-Prescription Platform Enabling Auto-Refills | +0.8% | National, with varying implementation rates across autonomous communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing-linked diabetes prevalence spike

Spain’s coastal and southern regions report diabetes rates well above the national average, driven by an aging population that peaks at age 80 [1]Edelmiro L. Menéndez Torre, “Prevalence of Diabetes Mellitus in Spain,” Endocrinología, Diabetes y Nutrición, elsevier.es. Concentrated prevalence translates into higher per-capita device demand, prompting suppliers to align inventory and after-sales support with autonomous-community programs targeting seniors. Regional initiatives such as Madrid Salud’s ALAS program illustrate how localized prevention strategies can normalize glucose levels in 35% of pre-diabetic participants, underscoring unmet demand for continuous monitoring in older cohorts. The Spain diabetes devices market consequently sees sustained baseline growth as each successive age bracket enters high-risk status. Manufacturers are tailoring simple-interface glucometers and larger-font CGM displays to meet geriatric usability needs, while pharmacies in Andalusia and Valencia boost stock of easy-load test strips to address dexterity challenges in elderly users.

Primary-care CGM reimbursement rollout

The 2024 national policy authorizing CGM funding through primary-care clinics removed specialist gatekeeping and opened access for insulin-treated Type 2 patients. Catalonia’s phased launch showed 69% uptake among contacted candidates, a pattern now replicated in Basque Country and Madrid [2]María González, “Real-World Study of Medtronic 780G Hybrid Closed-Loop System,” Endocrinología, Diabetes y Nutrición, elsevier.es. Health-economic analyses project annual savings of EUR 580 per patient from reduced severe hypoglycemia, motivating additional autonomous communities to widen eligibility. Suppliers positioned within the Spain diabetes devices market are reallocating marketing budgets from endocrinology centers toward primary-care physician education. Demand for factory-calibrated CGMs that integrate with standard electronic health records is rising, and Spanish distributors are vying for exclusive tenders that bundle sensors with cloud dashboards for general practitioners.

Hybrid closed-loop clinical trials at university hospitals

Barcelona and Madrid university hospitals have become national reference centers for hybrid closed-loop (HCL) research. Trials of the Medtronic 780G system improved time-in-range from 69% to 74% and lowered HbA1c from 7.6% to 7.0% over six months [3]F. Gómez-Peralta, “Impact of Continuous Glucose Monitoring in Clinical Practice,” Diabetes Therapy, link.springer.com. Findings fast-track inclusion of HCL technologies in regional formularies, accelerating diffusion beyond tertiary centers. Publications in Spanish journals give regional budget holders the evidence needed to authorize procurement, thereby uplifting the Spain diabetes devices market. Device makers now sponsor clinician-training workshops across Seville and Valencia to shorten rollout lag after regulatory clearance.

Retail-pharmacy smart-pen penetration

Grupo Cofares’ 38% pharmacy coverage allows rapid deployment of Bluetooth-enabled smart pens, shifting insulin delivery closer to patients’ daily routines. Community pharmacists, guided by the 7th Medical-Pharmaceutical Congress recommendations, counsel users on pairing pens with CGM apps, ensuring data continuity between refills. This consumer-centric route reduces reliance on hospital dispensation and lifts adherence among Type 2 patients managed mainly in primary care. Early sales trends confirm that when pens are stocked alongside test-strip packs, patients accept incremental device costs due to perceived convenience. The Spain diabetes devices market is thus recording faster unit turnover through retail shelves than through hospital pharmacies.

Growth of e-prescription platform enabling auto-refills

Spain’s Receta Electrónica now supports auto-refill prompts that sync with CGM sensor lifecycles and pump infusion-set schedules. Integration with community pharmacy software yields smoother supply continuity, dropping sensor lapse days and trimming adverse event risk. Real-world pilots indicate a 15% rise in on-time consumable pickups where auto-refill alerts are active. The platform’s expansion strengthens data capture for healthcare administrators, who use adherence analytics to fine-tune regional budgets. Device makers embed barcode identifiers aligned with e-prescriptions, simplifying pharmacy inventory tracking and fostering long-term loyalty within the Spain diabetes devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent AEMPS Cyber-security Certification for Connected Pumps | -1.2% | National | Medium term (2-4 years) |

| Low CGM Uptake in Rural Castilla-La Mancha & Extremadura | -0.8% | Rural areas, particularly Castilla-La Mancha and Extremadura | Long term (≥ 4 years) |

| Pricing Reference System Caps on Test-Strips | -0.6% | National | Short term (≤ 2 years) |

| Fragmented Regional Procurement Delays (17 Autonomous Communities) | -0.9% | National, with varying impact across autonomous communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent AEMPS cybersecurity certification for connected pumps

Spain’s regulator demands advanced penetration-testing evidence before connected insulin pumps gain market entry. Certification adds 6–12 months to launch schedules and lifts compliance costs, discouraging smaller innovators. While patients eventually benefit from stronger data protection, delayed product availability suppresses near-term pump sales within the Spain diabetes devices market. Multinationals respond by staging Spanish rollouts after initial clearance in other EU states, reallocating early promotional spending to neighboring markets. The extra scrutiny also obliges distributors to provide detailed cybersecurity training to biomedical engineers in public hospitals.

Low CGM uptake in rural Castilla-La Mancha and Extremadura

Sparse specialist clinics, limited broadband, and lower average incomes keep continuous monitoring penetration at roughly half the urban rate. A study on rural home-healthcare logistics revealed logistical hurdles to routine device servicing and patient education [4]Cristian Castillo, “Home Healthcare in Spanish Rural Areas,” Socio-Economic Planning Sciences, sciencedirect.com. Resulting disparities compel regional authorities to trial mobile-clinic initiatives, but capital constraints slow progress. Manufacturers running pilot programs with telehealth startups hope to prove remote onboarding feasible, yet until coverage improves, subdued rural demand constrains overall Spain diabetes devices market growth.

Pricing reference system caps on test strips

Spain’s reference pricing reduces test-strip margins by roughly 15%. Lower profitability limits promotional budgets for advanced strips that reduce blood-sample volumes or improve accuracy. Manufacturers therefore prioritize CGM sensors, leaving basic glucometer innovation stagnant. Pharmacies continue to sell high volumes, but suppressed prices shrink the revenue pool, moderating the Spain diabetes devices market size trajectory.

Fragmented regional procurement delays

Each autonomous community sets independent tender cycles, creating asynchronous adoption of new technologies. The resulting 3-6 month lag compared with centralized systems cuts into cumulative five-year revenue. Suppliers maintain separate sales teams for high-priority regions such as Catalonia and Basque Country, raising operational costs. Harmonization efforts remain slow, so procurement fragmentation will persist as a structural drag on the Spain diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: monitoring dominance, management momentum

Monitoring Devices held 60.24% of the Spain diabetes devices market in 2024, reinforced by standardized glucose-testing protocols across all autonomous communities. CGM sub-segment momentum continues at an 8.41% CAGR as funding grows and clinical evidence validates cost savings. The Spain diabetes devices market size for Monitoring Devices is forecast to reach USD 690 million by 2030, demonstrating sustained volume and value expansion.

Management Devices—including pumps and smart pens—represent a smaller but strategically significant share. Hybrid closed-loop systems trialed in Spanish hospitals prove significant glycemic improvements, prompting more regions to reimburse advanced pumps. Retail pharmacy availability of smart pens has lowered access barriers; coupled with automated dosing algorithms, these devices reduce user burden and boost adherence. Suppliers bundle cloud dashboards with pens to capitalize on the emergent data-driven care model, further enlarging their footprint within the Spain diabetes devices market.

By End-User: hospital anchor, home-care acceleration

Hospitals commanded 46.12% of the Spain diabetes devices market share in 2024 thanks to their gatekeeper role for complex device initiation. Central pharmaco-therapeutic committees still approve pump and CGM prescriptions, influencing subsequent outpatient trajectories. In-hospital adoption of professional CGMs for acute management supports continued unit placements.

Home-care settings grow fastest at 7.83% CAGR, underpinned by telemedicine expansion encouraged by Spain’s Digital Health Strategy. Lockdown-era studies showed improved time-in-range despite fewer clinic visits, validating remote monitoring benefits doi.org. The Spain diabetes devices market size generated by home-care users is projected to surpass USD 350 million by 2030, lifting overall sector resilience.

By Distribution Channel: retail reach, online surge

Retail pharmacies provide 55.35% of 2024 revenue, demonstrating unmatched geographic presence and reimbursement integration. Their advisory role expands as pharmacists receive continuous-education credits for diabetes device counseling. Bundled service models—such as sensor starter packs plus training—grow wallet share within the Spain diabetes devices market.

Online pharmacies, progressing at 8.23% CAGR, attract tech-savvy urban consumers who value doorstep delivery of consumables. Integration with Receta Electrónica has enabled seamless co-payment processing, while courier services guarantee cold-chain compliance for insulin. Hospital pharmacies remain indispensable for initial pump allocations and professional CGM rentals but face competition on recurrent sales as distributors incentivize community channels.

By Patient Type: Type 2 volume, Type 1 innovation

Type 2 patients generate 87.29% of revenue, dictating baseline demand. As CGM and smart-pen evidence accrues for this cohort, public payers gradually sponsor advanced devices, enlarging absolute volumes. Type 1 patients adopt new technology earlier and represent the innovation showcase, propelling HCL system trials that influence broader device design. With a 7.92% CAGR, their spending power significantly outpaces population growth, sustaining premium-tier activity within the Spain diabetes devices market.

By Device Connectivity: non-connected hold, wireless rise

Non-connected devices led with 78.64% share in 2024 due to lower cost and entrenched reimbursement. Reference-pricing pressures keep basic glucometers ubiquitous. Yet Bluetooth/Wireless-connected devices race ahead at 9.16% CAGR, energized by app-based coaching and remote clinician dashboards. The Spain diabetes devices market share for connected devices could exceed 30% by 2030 as autonomy-oriented younger users and digitally literate seniors opt for integrated data flows.

Geography Analysis

Spain’s decentralized healthcare architecture produces marked regional contrasts. Southern autonomous communities such as Andalusia and Valencia combine high prevalence with sizeable elderly populations, driving elevated per-capita test-strip and CGM sensor consumption. The Canary Islands top prevalence charts at 12%, prompting local authorities to subsidize CGM starter kits for seniors at community health centers. These initiatives propel the Spain diabetes devices market in coastal zones ahead of national averages.

Urban hubs—Madrid, Barcelona, Valencia, and Seville—concentrate specialist hospitals and university research, making them early adopters of hybrid closed-loop pumps and AI-driven dosage apps. Madrid’s 600,000 adults with diabetes form a dense demand cluster; procurement teams there prioritize interoperability with the regional health record, stimulating suppliers to localize software in Spanish and Catalan.

Rural provinces, notably Castilla-La Mancha and Extremadura, lag in CGM uptake due to broadband gaps and fewer trained endocrinologists. Mobile telehealth vans piloted in Segovia show promise but require sustained funding. Until such programs scale, limited device exposure curbs the Spain diabetes devices market size contribution from these areas.

Basque Country and Navarre leverage higher public health spending per capita to integrate diabetes devices into chronic-care pathways faster than the national mean. Catalonia’s chronic-disease package adds stepwise CGM funding; its unified health-information platform supports data-driven reimbursement decisions, providing a blueprint other regions aim to replicate. These leading communities collectively account for a disproportionate share of premium device sales, enhancing overall Spain diabetes devices market growth.

Competitive Landscape

The Spain diabetes devices market is moderately concentrated, with Abbott, Medtronic, and Dexcom leading monitoring revenues, while Medtronic and Ypsomed command pump installations. Strategic alliances redefine rivalry: Medtronic’s partnership with Abbott aligns glucose sensing with interoperable pumps, promising seamless data handoffs that meet Spain’s e-prescription standards. Ypsomed’s 80.8% pump sales jump underscores rising interest in automated dosing; its focus on open-protocol Bluetooth connectivity resonates with hospitals requiring flexible integrations.

Domestic player Insulcloud exploits cloud analytics to meet local procurement criteria for interoperable solutions, offering real-time dashboards that mesh with autonomous community telehealth portals. Menarini Diagnostics leverages established lab-diagnostic relationships to bundle glucometers with HbA1c testing services, anchoring its presence in public-clinic tenders. Fragmented procurement rewards adaptive distributors who localize bids, train clinicians, and guarantee region-specific spare-parts logistics, fostering a vibrant mid-tier segment within the Spain diabetes devices market.

Regulatory rigor shapes competition: AEMPS cybersecurity mandates challenge smaller entrants lacking dedicated compliance teams, but established multinationals capitalize on their audit experience to secure early approvals. Companies also differentiate via post-sale support, offering 24-hour helplines in Spanish, Catalan, and Basque to satisfy regional language requirements. As e-prescription data matures, analytics-based adherence programs become a new battleground, prompting device makers to embed AI algorithms that flag supply gaps and suggest proactive interventions.

Spain Diabetes Devices Industry Leaders

Dexcom Inc.

Ascensia Diabetes Care

Eli Lilly and Company

Tandem Diabetes Care

Ypsomed AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Dexcom launched the real-time CGM system Dexcom ONE+ in Spain, offering factory calibration and direct smartphone display.

- November 2022: The Eversense E3 continuous glucose monitor (CGM) was approved by the FDA and it received a CE Mark approval in Europe for people with diabetes aged 18 and older.

- June 2022: Senseonics received a CE mark for a 6-month CGM implant. Ascensia Diabetes Care, which signed up to sell Eversense in 2020, was expected to distribute the diabetes device in countries including Germany, Italy, and Spain, where it was laying the groundwork for launch through sales conferences and changes to its distribution model.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain diabetes devices market as the aggregate value of monitoring devices (self-monitoring blood-glucose meters, test strips, lancets, and continuous glucose monitoring sensors, transmitters, receivers) and management devices (insulin pumps, cartridges, syringes, and disposable or reusable pens) sold in Spain to hospitals, pharmacies, and home-care users.

Scope exclusion: we do not track glucose-responsive drugs or standalone diabetes software without a paired hardware component.

Segmentation Overview

- By Device Category

- Monitoring Devices

- Self-Monitoring Blood Glucose (SMBG)

- Glucometer Devices

- Test Strips

- Lancets

- Continuous Glucose Monitoring (CGM)

- Sensors

- Transmitters & Receivers (Durables)

- Self-Monitoring Blood Glucose (SMBG)

- Management Devices

- Insulin Pump Systems

- Pump Device

- Pump Reservoir

- Infusion Set

- Patch Pump

- Insulin Delivery Pens

- Disposable Pens

- Reusable Smart Pens

- Insulin Syringes

- Insulin Cartridges

- Insulin Pump Systems

- Monitoring Devices

- By End-User

- Hospitals

- Specialty Clinics

- Home-Care Settings

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Patient Type

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational / Other

- By Device Connectivity

- Bluetooth / Wireless-Connected

- Non-Connected

Detailed Research Methodology and Data Validation

Primary Research

We interviewed endocrinologists, procurement chiefs at public hospitals across five Autonomous Communities, retail-pharmacy chains, and local importers. Their inputs refined channel splits, typical sensor replacement cycles, and average selling prices, then validated early model outputs.

Desk Research

Mordor analysts first mapped the universe of devices and reimbursement rules using freely accessible sources such as Spain's Ministry of Health tender bulletins, AEMPS device registries, the International Diabetes Federation atlas, and periodic datasets from the National Statistics Institute. Trade-association white papers (e.g., FENIN medical devices barometer) and peer-reviewed Spanish Endocrinology Society journals supplied prevalence and adoption fingerprints. Subscription databases like D&B Hoovers and Dow Jones Factiva helped us size corporate revenue streams and flag abnormal swings. This list is illustrative, not exhaustive, as many other public and paid references were consulted.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build converted Spain's adult diabetes population into device demand pools. Values were stress-tested through selective bottom-up supplier roll-ups on insulin pumps and CGM sensors. Key variables include: (1) CGM reimbursement rollout timing, (2) year-on-year growth in diagnosed diabetics (~2.5%), (3) test-strip reference-price caps, (4) average sensor ASP erosion, and (5) hospital share of insulin-pump placements. Multivariate regression, supported by expert consensus, projects these drivers to 2030, and gaps in bottom-up data are bridged by calibrated uptake ratios from matched EU peers.

Data Validation & Update Cycle

Outputs pass multi-layer variance checks before senior review, then are benchmarked against independent shipment totals and tender volumes. The model refreshes annually, with interim revisions triggered by material policy or technology events.

Building Confidence in Our Spain Diabetes Devices Baseline

Published estimates differ because firms choose varying device lists, price definitions, and update cadences.

Key gap drivers here include divergent inclusion of test-strip reimbursements, differing CGM sensor life assumptions, and whether authors roll drug-device combos into device revenue. Mordor's model reports current-year figures in constant 2024 USD, uses quarterly MoH tender prices, and is refreshed every twelve months, which explains observed spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.76 B (2025) | Mordor Intelligence | - |

| USD 0.77 B (2023) | Regional Consultancy A | Older base year; excludes pharmacy margin adjustments |

| USD 0.77 B (2024) | Global Consultancy B | Treats smart pens software fees as devices |

| USD 0.44 B (2022) | Industry Data-book C | Limits scope to SMBG and insulin pumps only |

In summary, the Spain market value we publish balances transparent variable selection with disciplined refresh cycles, giving decision-makers a dependable, repeatable baseline that sits between optimistic pipeline-heavy views and conservative legacy-device tallies.

Key Questions Answered in the Report

How big is the Spain Diabetes Devices Market?

The Spain Diabetes Devices Market size is expected to reach USD 0.76 billion in 2025 and grow at a CAGR of 7.41% to reach USD 1.09 billion by 2030.

Which product segment is expanding fastest?

Continuous Glucose Monitoring systems are the fastest-growing segment, posting an 8.4% CAGR through 2030 as primary-care reimbursement broadens coverage.

Who are the key players in Spain Diabetes Devices Market?

Dexcom, Abbott, Novo Nordisk, Medtronic and Sanofi are the major companies operating in the Spain Diabetes Devices Market.

Where is CGM uptake lowest, and why?

Rural Castilla-La Mancha and Extremadura show persistently low adoption because of sparse specialist coverage, limited broadband, and lower household incomes, widening the urban–rural care gap.

Page last updated on: