Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

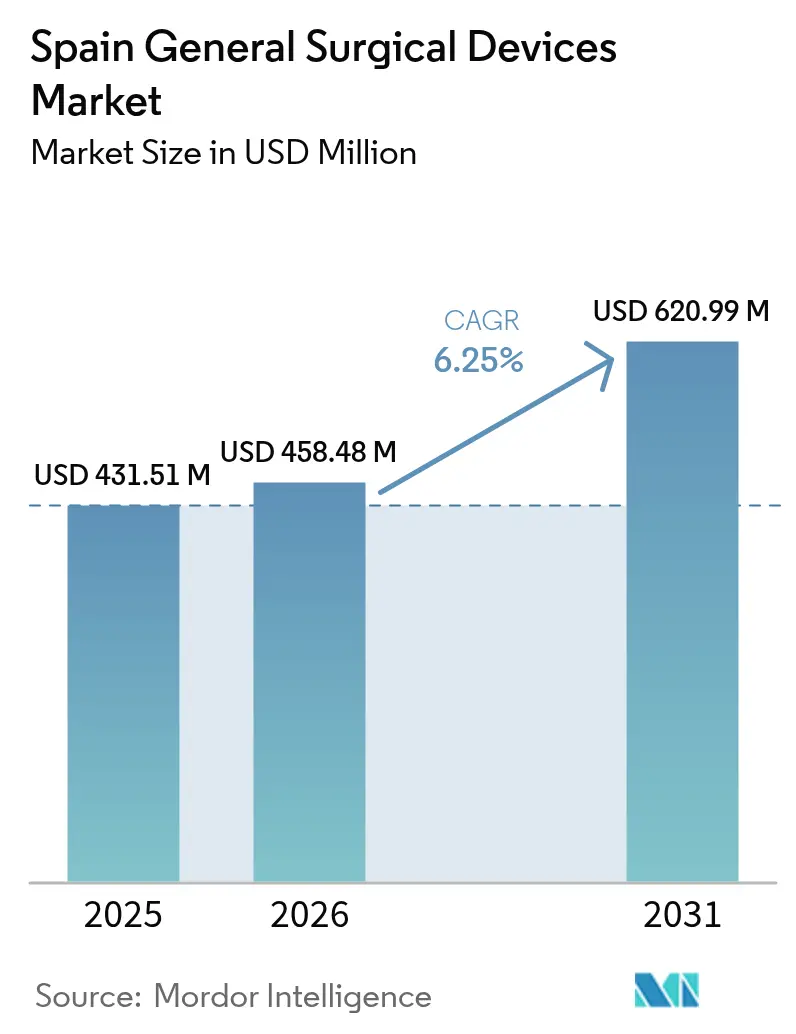

| Base Year Market Size (2025) | USD 431.51 Million |

| Market Size (2026) | USD 458.48 Million |

| Market Size (2031) | USD 620.99 Million |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain General Surgical Devices Market Analysis by Mordor Intelligence

The Spain General Surgical Devices Market size was valued at USD 431.51 million in 2025 and estimated to grow from USD 458.48 million in 2026 to reach USD 620.99 million by 2031, at a CAGR of 6.25% during the forecast period (2026-2031). Budget expansion by the Spanish Ministry of Health, rising volumes of minimally invasive procedures, and steady investments from European recovery funds underpin near-term growth. Demand is reinforced by an aging population, a higher prevalence of chronic diseases, and a policy push that directs 69% of Madrid’s health budget toward hospital care. Rapid adoption of single-use electrosurgical instruments aims to curb surgical site infections, which affect 4.51% of Spanish operative cases. Growth is further lifted by inbound surgical tourism. On the supply side, the shortage of advanced laparoscopy-trained surgeons and recurrent electrosurgical generator recalls temper the five-year outlook.

Key Report Takeaways

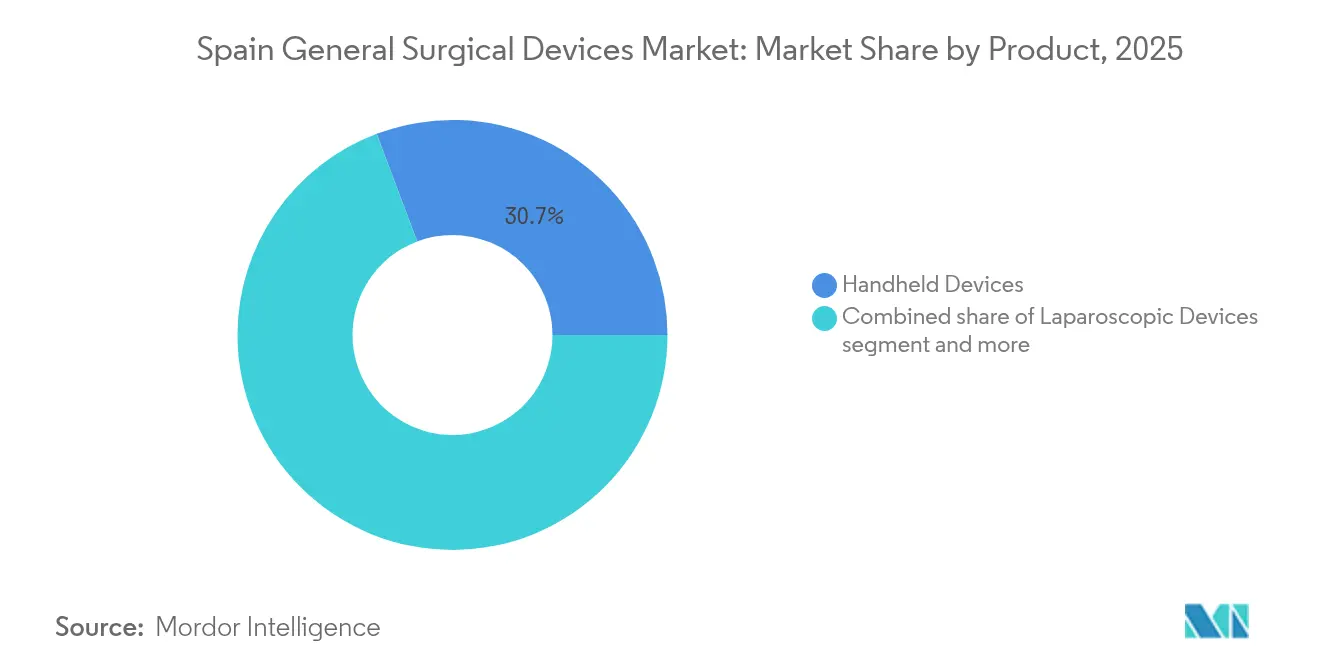

- By product, handheld devices led with 30.74% revenue share in 2025, while electrosurgical devices are the fastest-growing segment at a 7.82% CAGR through 2031.

- By procedure approach, minimally invasive surgery held 69.52% of Spain general surgical devices market share in 2025 and is projected to expand at a 7.28% CAGR to 2031.

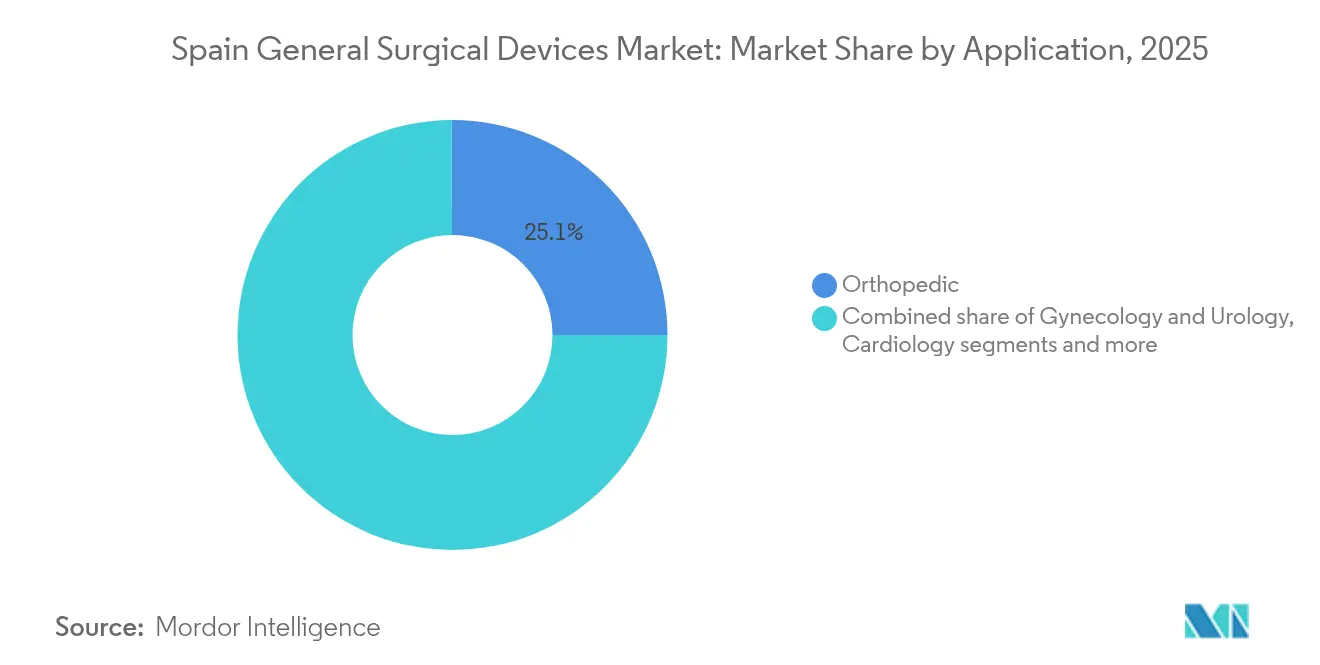

- By application, orthopedic segment accounted for 25.08% share of the Spain general surgical devices market size in 2025; neurology is advancing at an 7.89% CAGR to 2031.

- By end user, hospitals commanded 74.41% share in 2025, whereas ambulatory surgery centers record the highest projected CAGR at 7.62% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive surgeries | +1.8% | National, with concentration in Madrid, Catalonia, Basque Country | Medium term (2-4 years) |

| Growing burden of chronic diseases requiring surgical intervention | +1.2% | National, with higher impact in aging regions like Asturias, Galicia | Long term (≥ 4 years) |

| Aging population accelerating procedure volumes | +1.0% | National, with acute impact in rural autonomous communities | Long term (≥ 4 years) |

| Growth of inbound surgical tourism to Spanish private hospitals | +0.7% | Madrid, Catalonia, Balearic Islands, Valencia | Medium term (2-4 years) |

| Shift to single-use instruments to mitigate hospital-acquired-infection risk | +0.9% | National, with early adoption in university hospitals | Short term (≤ 2 years) |

| Expansion of ambulatory surgery centres across autonomous communities | +0.6% | National, with accelerated growth in Madrid, Catalonia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Surgeries

Spain's surgical landscape is undergoing a paradigm shift as minimally invasive procedures gain traction across specialties, though adoption rates reveal significant regional disparities. The uneven adoption creates market opportunities for device manufacturers who can provide comprehensive training programs alongside their surgical instruments. Post-pandemic surgical recovery guidelines show that 85% of Spanish procedures can transition to outpatient settings. These trends elevate demand for specialized trocars, energy devices, and robotic staplers within the Spain general surgical devices market.

Growing Burden of Chronic Diseases Requiring Surgical Intervention

Spain's demographic transition is creating sustained demand for surgical interventions as chronic disease prevalence rises across age cohorts. This trend drives demand for specialized surgical devices that enable complex procedures in ambulatory settings. Ambulatory oncology programs in Valencia substitute 72.8% of traditional breast surgeries, promoting high-turnover device use. Electrophysiology innovations such as the Varipulse catheter respond to Spain’s expanding cardiovascular workload.

Aging Population Accelerating Procedure Volumes

Spain's rapidly aging population is fundamentally reshaping surgical device demand patterns, with demographic pressures most acute in rural autonomous communities experiencing population decline. WHO notes mounting pressure to sustain access as rural provinces age faster than the national mean. A hydrocephalus case series using the ExcelsiusGPS platform cut error risk by 66% relative to freehand techniques. Orthopedic robotics see uptake despite an incremental EUR 2,084 cost premium over laparoscopic hernia repair.[1]Source: S. Morales-Conde, “Economic analysis of the robotic approach to inguinal hernia versus laparoscopic: is it sustainable for the healthcare system?” springer.com Hospitals justify expenditure through shorter recoveries and reduced readmissions.

Growth of Inbound Surgical Tourism to Spanish Private Hospitals

Spain's emergence as a surgical tourism destination is creating new demand dynamics for high-end surgical devices, particularly in private hospitals serving international patients. Private facilities in Catalonia house significant percentage of Spain’s high-tech equipment, including MRI and lithotripsy systems. The hospitals housing the Da Vinci robotic systems indicate the volume requirements that justify premium device investments. Public–private collaboration and digital follow-up services offer device firms partnership avenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictive reimbursement for selected MIS procedures | -0.8% | National, with acute impact in public hospital systems | Medium term (2-4 years) |

| Stringent regulations | -0.5% | National, with heightened compliance costs in Madrid, Catalonia | Short term (≤ 2 years) |

| Recalls & supply-chain disruptions for electrosurgical generators | -0.7% | Global, with concentrated impact on Spanish hospitals using affected devices | Short term (≤ 2 years) |

| Shortage of advanced laparoscopy-trained surgeons | -0.6% | National, with concentration in smaller autonomous communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Restrictive Reimbursement for Selected MIS Procedures

Spain's reimbursement framework creates significant barriers to minimally invasive surgery adoption, with DRG-based payment systems failing to adequately compensate hospitals for the higher upfront costs of advanced surgical devices. Real-world evidence programs such as RedETS progress slowly due to hospital recruitment hurdles, prolonging uncertainty around coverage expansion.

Shortage of Advanced Laparoscopy-Trained Surgeons

Spain faces a critical shortage of surgeons trained in advanced laparoscopic techniques, creating a bottleneck that constrains surgical device market growth despite strong demand for minimally invasive procedures. Spanish residency curricula fall short of European Hernia Society benchmarks, with only 5.7% of inguinal hernia repairs executed laparoscopically. Simulation-based training initiatives are gaining traction, yet equipment and faculty costs restrict scale-up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Handheld Devices Lead Despite Electrosurgical Innovation

Handheld instruments captured 30.74% of Spain general surgical devices market share in 2025 owing to universal utility across open and minimally invasive cases. Disposable scissors, forceps, and retractors meet infection-control targets while remaining cost-efficient for regional hospitals. Electrosurgical platforms are expanding at a 7.82% CAGR supported by single-use pencil adoption to curb a 4.51% national surgical site infection rate. Spain general surgical devices market size for electrosurgical equipment is projected to grow steadily as recalls subside and updated instructions mitigate stroke risk.

Spain’s laparoscopic towers, wound-closure kits, and novel single-use duodenoscopes create specialist niches. EXALT Model D has entered reference centers for liver transplant follow-up, proving value in high-risk cohorts. Manufacturers able to bundle disposables with training and after-sales support gain traction in procurement tenders.

By Procedure Approach: Minimally Invasive Surgery Dominance Accelerates

Minimally invasive surgery commanded 69.52% of the Spain general surgical devices market in 2025 and is rising at a 7.28% CAGR. Ambulatory care models endorsed during the pandemic normalized outpatient pathways for up to 85% of operations. Spain general surgical devices market size for minimally invasive systems benefits from robotic console times that now average 37 minutes for unilateral inguinal hernia repair.

Open surgery preserves a 30.48% share by supporting trauma, complex oncology, and multisite procedures. Surgeons in smaller hospitals without robotic units rely on improved handheld sets and energy devices. Inter-regional training programs are being piloted to increase laparoscopic uptake, aiming to raise Spain general surgical devices market share for minimally invasive approaches in underserved provinces.

By Application: Orthopedic Leadership Meets Neurological Innovation

Orthopedic procedures generated 25.08% of 2025 revenue as an aging population drives hip and knee implants. Robotics and infection-resistant coatings position the segment for incremental gains despite reimbursement scrutiny. Spain general surgical devices market size for neurology is set to register the fastest 7.89% CAGR through 2031, fueled by robotic platforms that reduce intraoperative error in hydrocephalus shunting by 66%.

Gynecology and urology maintain steady adoption of single-port robots that shorten stays and lower analgesic use, while cardiology applications profit from growth in electrophysiology labs. Spain general surgical devices market share for orthopedic devices remains high as hospitals balance cost and improved revision outcomes.

By End User: Hospital Dominance Challenged by ASC Expansion

Hospitals accounted for 74.41% of 2025 revenue, benefitting from EUR 1.725 billion of European recovery funds directed to infrastructure. Diagnostic integration projects in Madrid streamline procurement by centralizing imaging and surgical capital budgets.

Ambulatory surgery centers grow at a 7.62% CAGR as procedures shifting to day care deliver average savings of 48.70% compared with inpatient pathways. The Spain general surgical devices market size attributable to ASCs is therefore expanding faster than overall growth. Specialty clinics and outpatient units comprise the remainder, adopting portable towers and compact energy sources that match limited footprint.

Geography Analysis

Madrid, Catalonia, and Andalusia jointly represent significant percentage of Spanish public healthcare outlays, giving them oversized influence on national tenders. Madrid’s hospital-centric spending pattern, combined with university centers hosting multiple Da Vinci robots, underpins robust uptake of premium minimally invasive systems. Spain general surgical devices market size attributable to Madrid alone is expected to climb steadily through 2031.

Catalonia serves as an innovation anchor. Private providers concentrate 58% of Spain’s high-tech equipment, supporting premium device turnover and surgical tourism flows. Barcelona’s life-sciences ecosystem attracts multinationals such as Galderma, which is expanding a Global Capability Center that could facilitate regional training partnerships.

The Basque Country spends EUR 1,710 per capita on health, surpassing the EUR 1,370 national average, and channels resources into infection-control modernization. Galicia and Asturias, both aging sharply, prioritize robotic orthopedic and neurology systems to manage higher procedure volumes. Spain general surgical devices market share gains in smaller communities rely on public grants that offset capital barriers. Rural provinces face surgeon shortages and longer procurement cycles. Innovation uptake therefore lags, prompting mobile training labs and shared-service models. These programs aim to raise minimally invasive penetration and cut readmission costs that average EUR 1,334 per episode in public hospitals.

Regulatory Landscape

General surgical devices marketed in Spain operate under the EU framework set by Regulation (EU) 2017/745 (MDR) and require CE marking. The Agencia Espanola de Medicamentos y Productos Sanitarios (AEMPS) serves as the national competent authority, overseeing commercialization requirements, vigilance, and related controls. Real Decreto 192/2023 also sets out Spanish procedures for items such as registration of economic operators and products, post-market surveillance, clinical investigations, and advertising, which increases the documentation and reporting burden for manufacturers, importers, and distributors active in Spain.

A compliance workflow shift is underway as AEMPS aligns national processes with the EU EUDAMED transition. AEMPS communicated that the first four EUDAMED modules become mandatory from May 28, 2026, and the regulator also activated RECOPS as a national application for registration of medical devices and IVD commercialization (June 2026). This raises the importance of accurate operator data, UDI and traceability readiness, and timely updates across national and EU systems.

Competitive Landscape

The Spain general surgical devices market is moderately fragmented. Multinationals such as Johnson & Johnson MedTech, Medtronic, Stryker, and B. Braun compete with regional distributors that tailor service contracts to autonomous communities. Johnson & Johnson MedTech restored Varipulse catheter sales after safety updates, underscoring rapid regulatory response capability.

Stryker projects higher 2025 profit on European device demand, signalling continued momentum. Smith+Nephew’s orthopedics portfolio grew 3.2% in Q1 2025 as hip and knee lines benefited from backlog recovery. Intuitive Surgical remains dominant in multi-port robotics.

Training solutions emerge as a differentiator. Vendors partner with teaching hospitals to alleviate laparoscopy skill gaps, combining simulator leases with disposable instrument bundles. Single-use innovations also spur rivalry; companies offering sterile barrier kits and disposable duodenoscopes position themselves as infection-control leaders. Supply-chain reliability is an ongoing theme, with recalls prompting providers to diversify sourcing of electrosurgical generators and sterile drapes.

Spain General Surgical Devices Industry Leaders

Boston Scientific Corporation

Medtronic PLC

B. Braun SE

Johnson & Johnson (Ethicon)

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and market-access reforms create clear whitespace for suppliers that can generate evidence and support hospitals and autonomous communities through standardized assessment and financing processes. Real Decreto 415/2026 (published in May 2026) establishes Spain's first national framework for health technology evaluation (ETS) covering medical devices and procedures, reinforcing the role of coordinated evidence submission and RedETS-linked pathways as hospitals compare minimally invasive systems, energy devices, and wound-closure technologies across regions. In parallel, Real Decreto 90/2026 introduces a selective financing regime for medical devices in the National Health System effective July 1, 2026, increasing the focus on pricing, portfolio segmentation, and tender strategy for general surgical device vendors.

Local capability build-out and procurement scrutiny are shaping near-term opportunity areas as well. In January 2026, Rob Surgical inaugurated a production facility in El Prat de Llobregat (Barcelona) for its Bitrack surgical robot, with stated capacity of 15-20 units, supporting a domestic base for robotic platforms and related instrument ecosystems, training, and service models in Spain. At the same time, the May 2026 investigation in Murcia reporting 492 surgeries (2018-2025) involving expired vascular prostheses and materials points to a compliance and traceability gap, favoring suppliers that offer stronger supply-chain controls, inventory management support, and single-use or track-and-trace enabled surgical consumables aligned with hospital governance requirements.

Recent Industry Developments

- May 2026: Medtronic received CE Mark for the Stealth AXiS surgical system, integrating surgical planning, navigation, and robotics for spine and cranial procedures. The approval supports broader EU commercialization, expanding access to integrated guidance platforms that can influence capital equipment decisions in high-acuity surgical departments and pull-through demand for compatible instruments and disposables.

- May 2026: Boston Scientific announced a USD 1.5 billion strategic investment in MiRus LLC for an approximately 34% equity stake, with an option tied to MiRus TAVR activities. The deal strengthens Boston Scientific's cardiovascular technology pipeline and can shape competitive positioning for procedure-enabling device portfolios used in hospital-based surgical and interventional settings.

- October 2024: INFORMA (DBK) reported Spain's medical-surgical materials market reached EUR 1.91 billion in 2023, reflecting 3.2% growth versus the prior year. The update indicates steady purchasing volumes in core consumables and equipment categories, reinforcing the role of public tenders and distributor reach in capturing demand across autonomous communities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers general surgical devices sold and used in Spain for routine and complex surgeries, including core instruments, access and closure products, and common surgical consumables used in operating rooms across care settings.

Scope exclusions: We exclude veterinary surgical devices, dental procedure tools, and home-use or cosmetic-only kits where they are not used in general surgery care pathways.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Other Products

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedics

- Neurology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear Spain-only demand picture for general surgery activity and purchasing. We used public sources such as Spain's Ministry of Health publications, Eurostat health and population tables, OECD health statistics, and WHO health indicators to understand procedure pressure, aging trends, and hospital capacity signals.

To connect demand to devices, we also reviewed medical device rules and notices from the European Commission and the Spanish medicines and medical devices authority, along with hospital procurement updates, association websites, and peer-reviewed clinical journals that describe shifts in surgical approach and usage patterns. Company annual reports and investor materials were used to spot portfolio mix and pricing commentary, and a paid subscription for company financials and news helped validate timing of launches, recalls, and tender momentum. These desk research sources are not exhaustive, and we also relied on other public references to collect, validate, and clarify inputs used in the model.

Primary Interviews and Surveys

Primary work was used to pressure-test device scope boundaries, Spain pricing ranges, and the share of volume moving between open and minimally invasive surgeries. We spoke with a mix of manufacturers, distributors, hospital procurement stakeholders, and clinicians, and we checked inputs across the main Spanish care settings (public hospitals, private hospitals, and ambulatory surgery centers) to avoid over-weighting a single channel.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | |

| Mid tier: 47% | Functional/Unit leaders: 37% | |

| Smaller Players: 22% | Managers: 44% |

Market-Sizing & Forecasting

Sizing is built using a top-down structure where Spain procedure volumes and care capacity signals are converted into device demand pools, followed by category-level spend allocation to arrive at a total market value. We then corroborate the totals with selective bottom-up checks, such as sampled price points for sutures and staplers, typical case-level usage factors, and distributor channel checks, which helps adjust the final number if one input looks stretched.

Key model inputs include the annual surgical throughput trend, the split between open and minimally invasive approaches, average units used per case for closure and access items, replacement and replenishment cycles for reusable instruments, and observed price movement by major device groups (including currency timing for imported items). For forecasting, we used scenario analysis anchored on expected procedure growth, hospital budgeting signals, and adoption pace of minimally invasive techniques, with assumptions reviewed and refined through expert feedback to keep near-term and mid-term paths realistic.

Where a clean supplier roll-up was not possible, gaps were handled by using share-based allocations from channel conversations and then checking the implied per-procedure spend against hospital purchasing patterns.

Data Validation & Update Cycle

Outputs are checked in several steps so the final market value aligns with real-world signals. We compare implied spending per surgery with what procurement teams and distributors describe, and we also look for breaks in trend that can be explained by policy changes, tender timing, recalls, or sudden shifts in procedure mix.

Before sign-off, analysts run variance checks across years and across device groups, and any outliers trigger a re-check of unit assumptions and price logic. Reports are refreshed annually, with interim updates when a material event changes demand or pricing, and before delivery a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Spain General Surgical Devices Market Size Compared Against Other Published Estimates

Published market values for Spain general surgical devices can look far apart because the boundaries are not the same, and the year and currency timing behind the price assumptions are often not stated clearly. Differences also show up when one estimate leans heavily on broad medical device spend splits instead of surgery-linked usage indicators.

In this study, pricing is refreshed through recent tender and distributor checks and then normalized to the base-year USD conversion timing. These steps, followed by re-contact when a price shift looks inconsistent, are what keep Mordor Intelligence aligned to how Spanish hospitals actually buy high-volume consumables versus reusable instruments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 431.51 M (2025) | |

| Industry Databook A | USD 488.60 M (2024) | Uses a surgical equipment lens that can include adjacent operating room equipment lines, and the base year differs, which can inflate comparisons when procedure mix and pricing moved between 2024 and 2025. |

| Global Publisher B | USD 1.40 B (2026) | Appears to apply a broader device bundle and a forward-year value, where higher assumed adoption and pricing progression can push the 2026 number above a Spain general surgery-only scope. |

The spread mainly comes from what is counted as a general surgery device, plus whether a source is showing an earlier base year or a forward-year value. By tying spend to surgery activity, updating price points with real purchasing signals, and keeping currency timing consistent, the estimate stays traceable to simple inputs that can be repeated and rechecked.

Key Questions Answered in the Report

What is the current size of the Spain general surgical devices market?

The market is valued at USD 458.48 million in 2026 and is on course to reach USD 620.99 million by 2031.

Which procedure approach dominates the Spain general surgical devices market?

Minimally invasive surgery leads with a 69.52% share in 2025 and is growing at a 7.28% CAGR.

Which product category is expanding fastest?

Electrosurgical devices record the highest growth, advancing at a 7.82% CAGR through 2031 as hospitals shift to single-use instruments.

Why are ambulatory surgery centers important for device suppliers?

ASCs show a 7.62% CAGR because outpatient pathways cut average costs by 48.70%, encouraging investment in compact and disposable device lines.

Which Spanish regions present the largest procurement opportunities?

Madrid, Catalonia, and Andalusia together control 45% of public healthcare expenditure, making them priority targets for device vendors.

What is the main challenge to wider adoption of robotic surgery in Spain?

Restrictive reimbursement and a shortage of advanced laparoscopy-trained surgeons slow uptake despite clear clinical benefits.

Page last updated on: